Foreign Direct Investment (FDI), Investment in Construction and Poverty in Economic Crises (Denmark, Italy, Germany, Romania, China, India and Russia)

Abstract

:1. Introduction

2. Methodology and Data

3. Results

3.1. First Stage. The Assessment of the Dynamics of Variables for 2005–2020 and the Factor Countries (Denmark, Italy, Germany, Romania, China, India, Russian Federation)

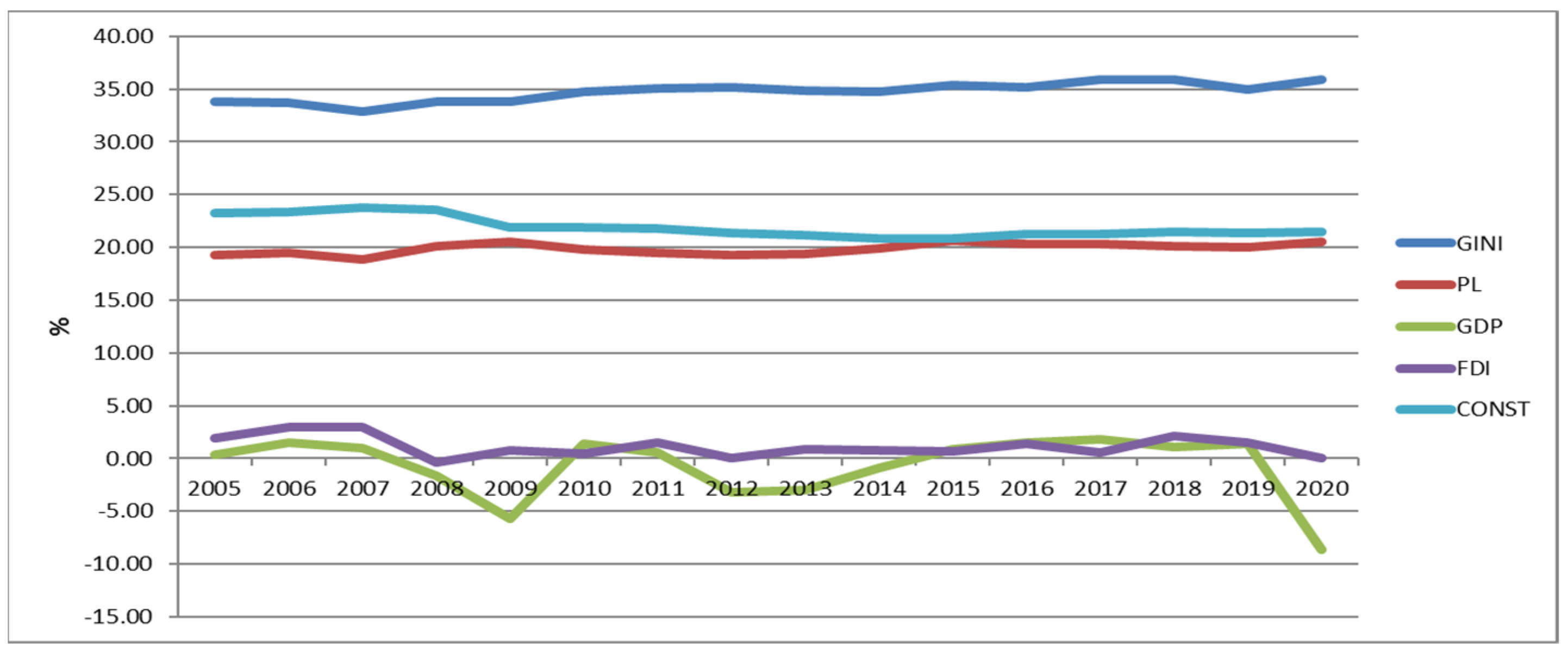

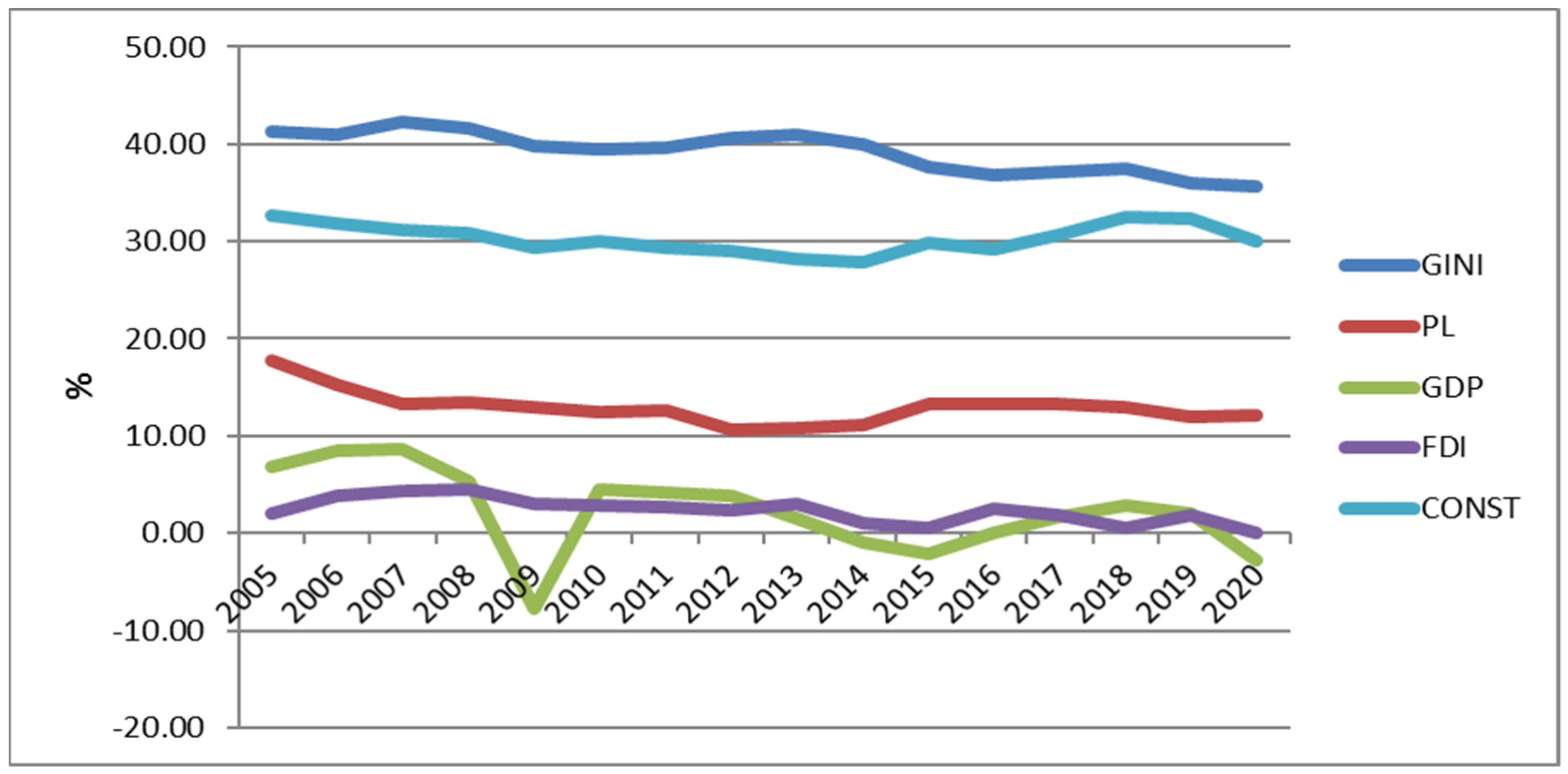

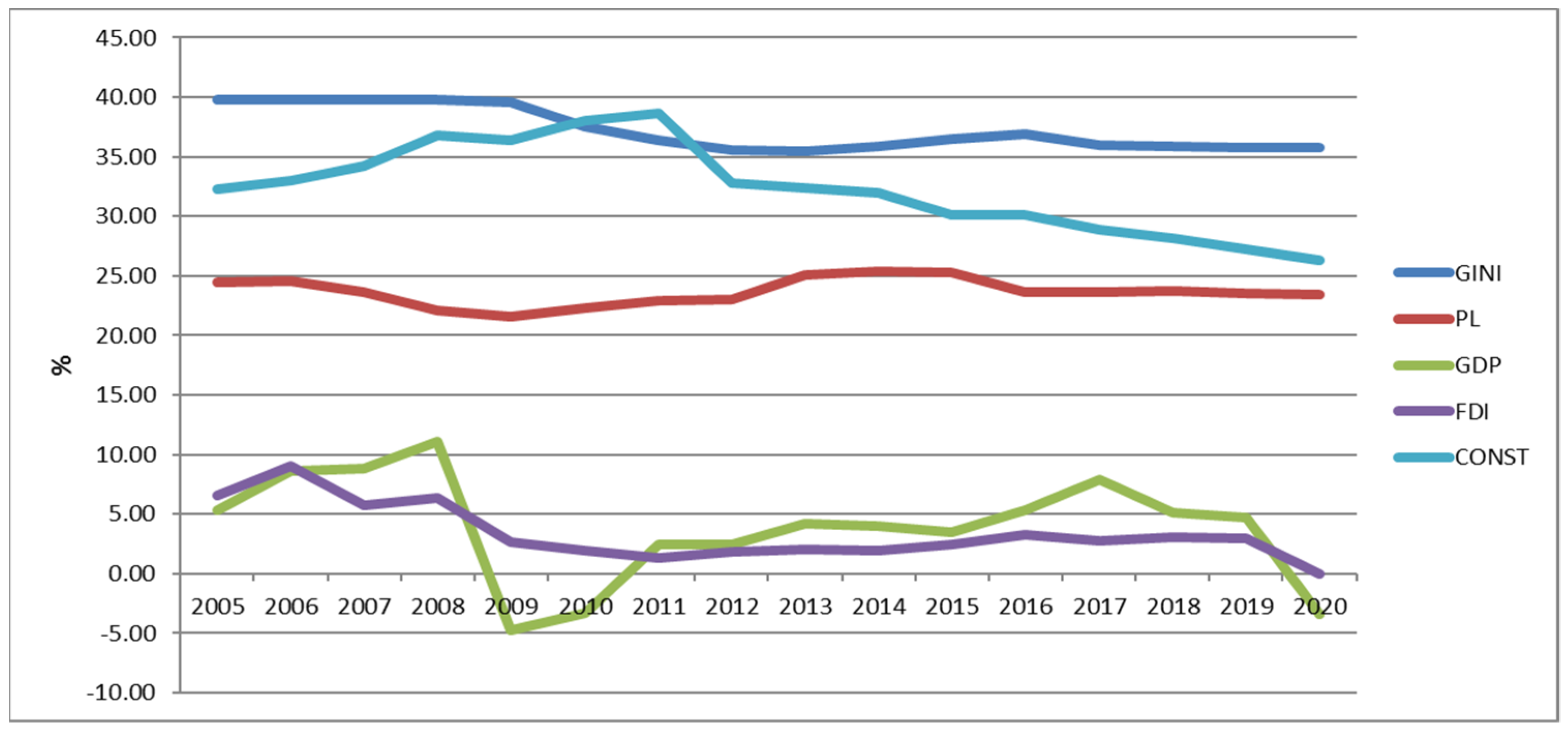

3.1.1. Denmark

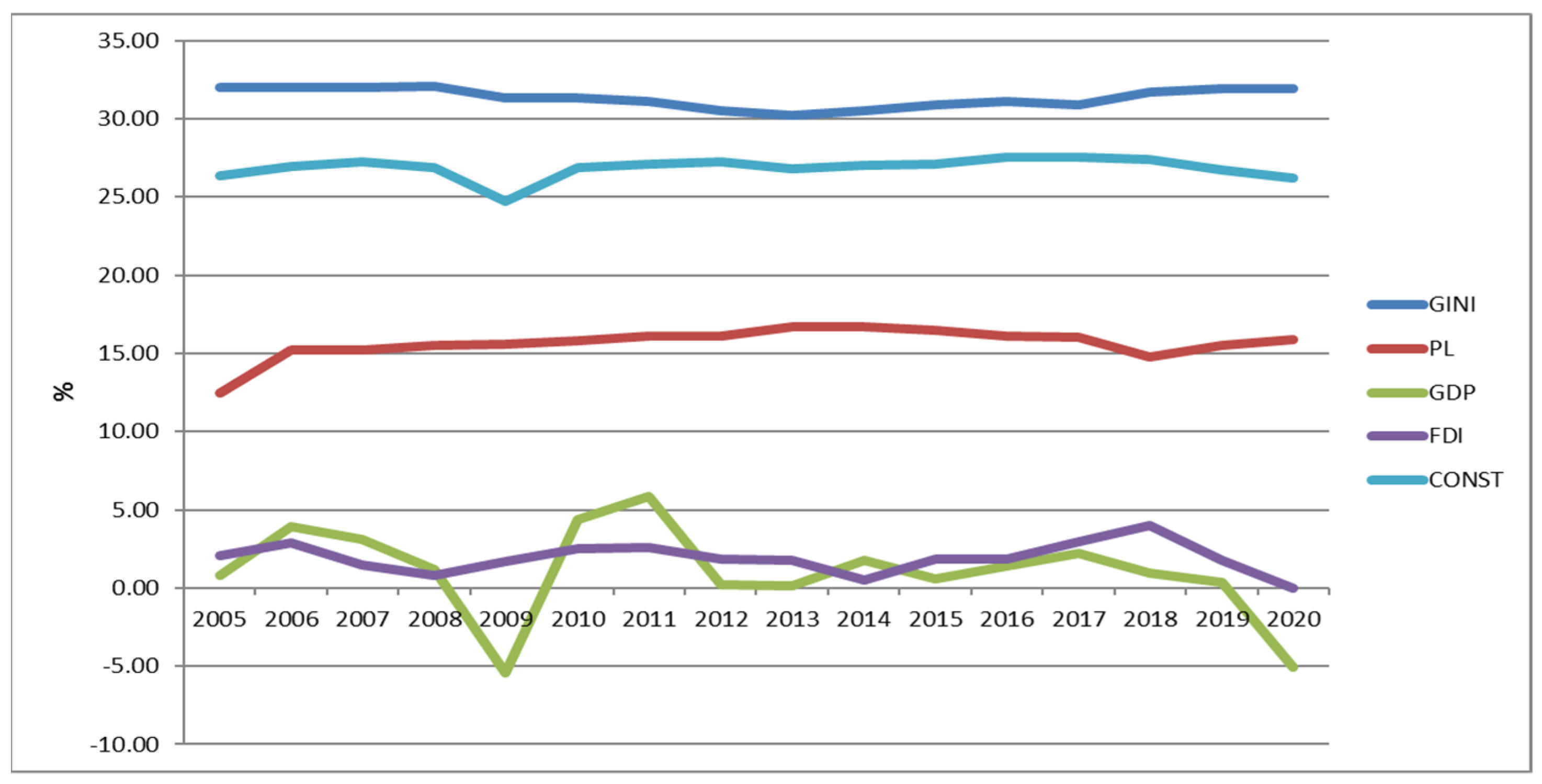

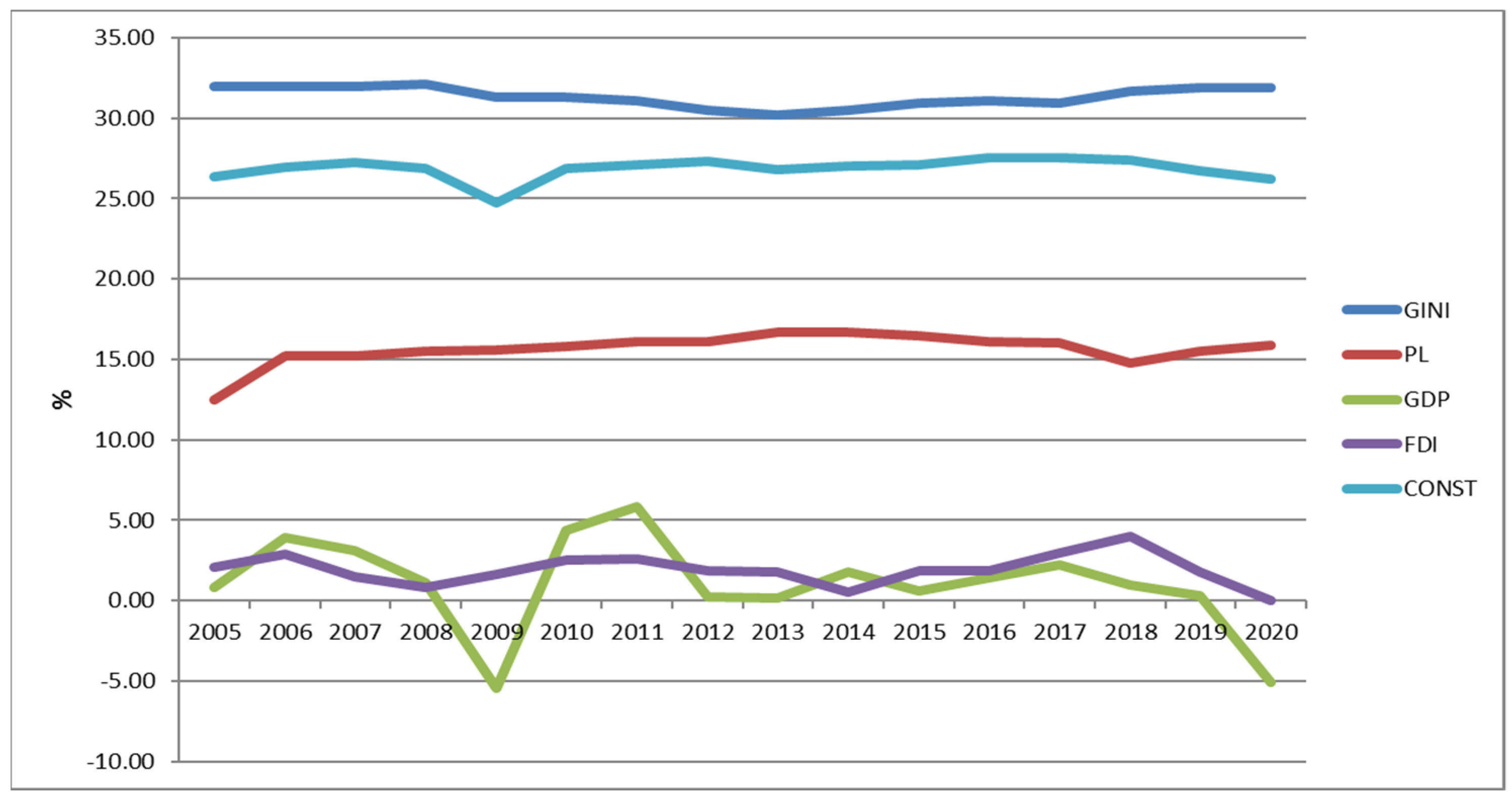

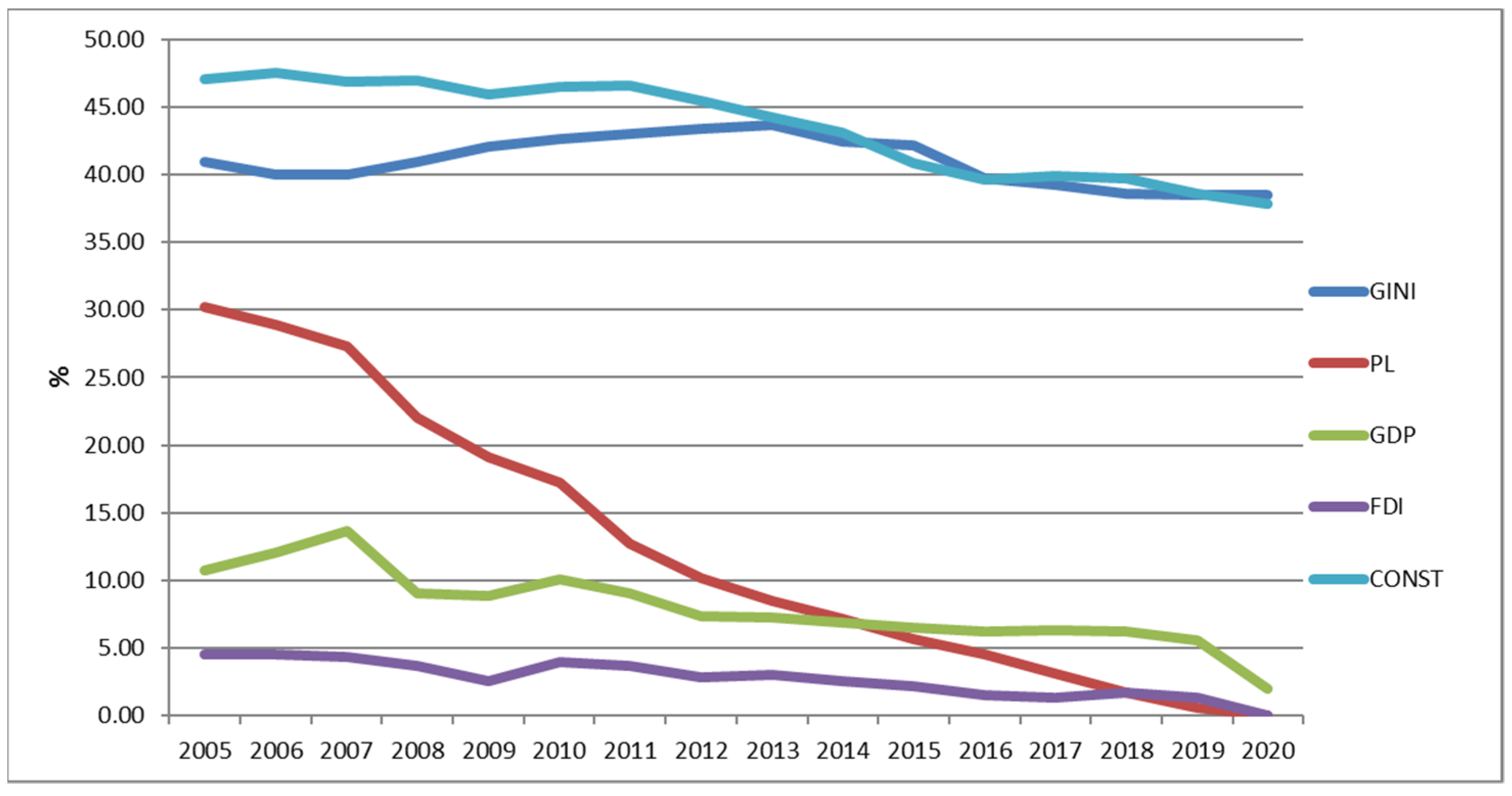

3.1.2. Italy

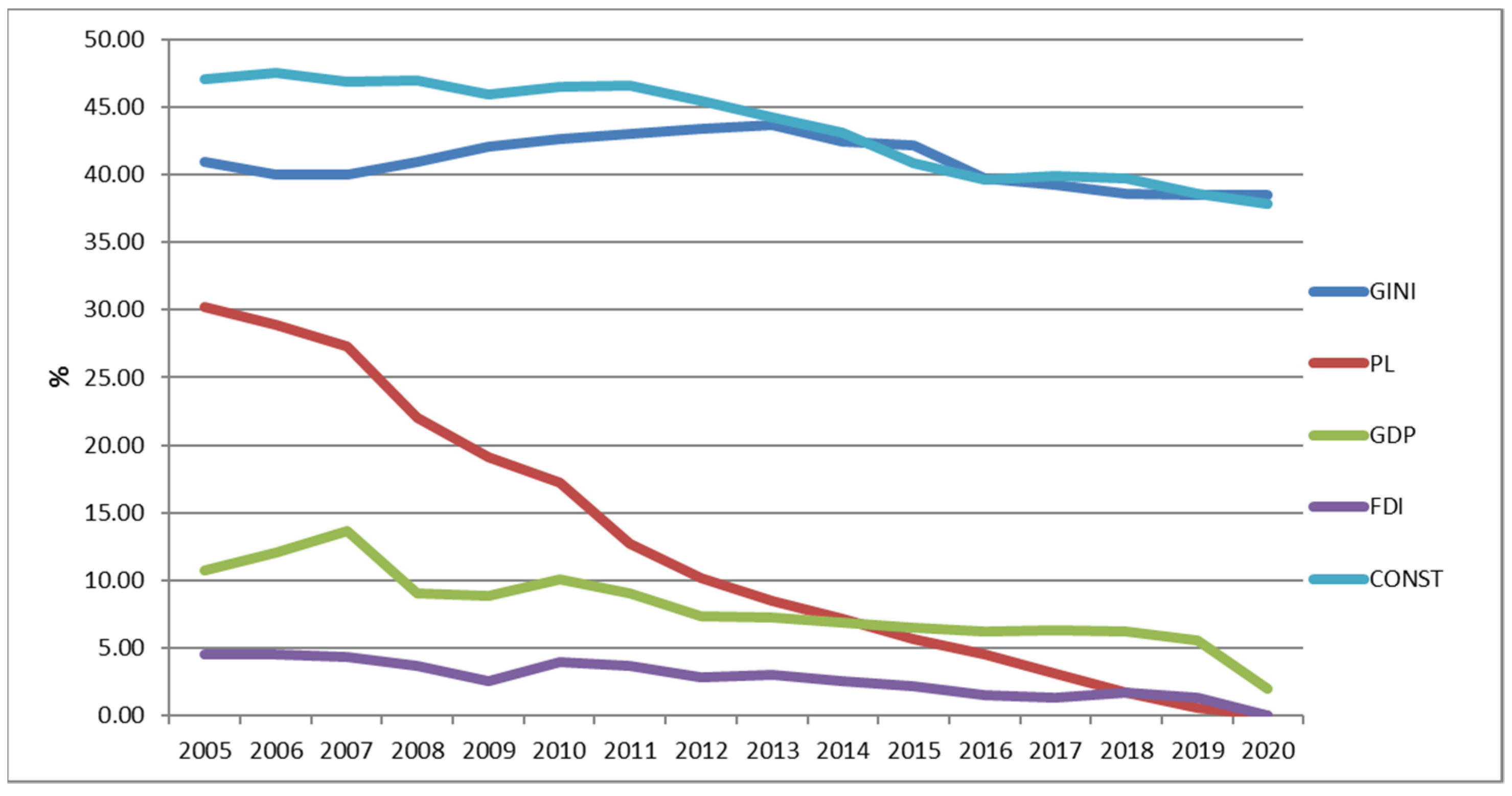

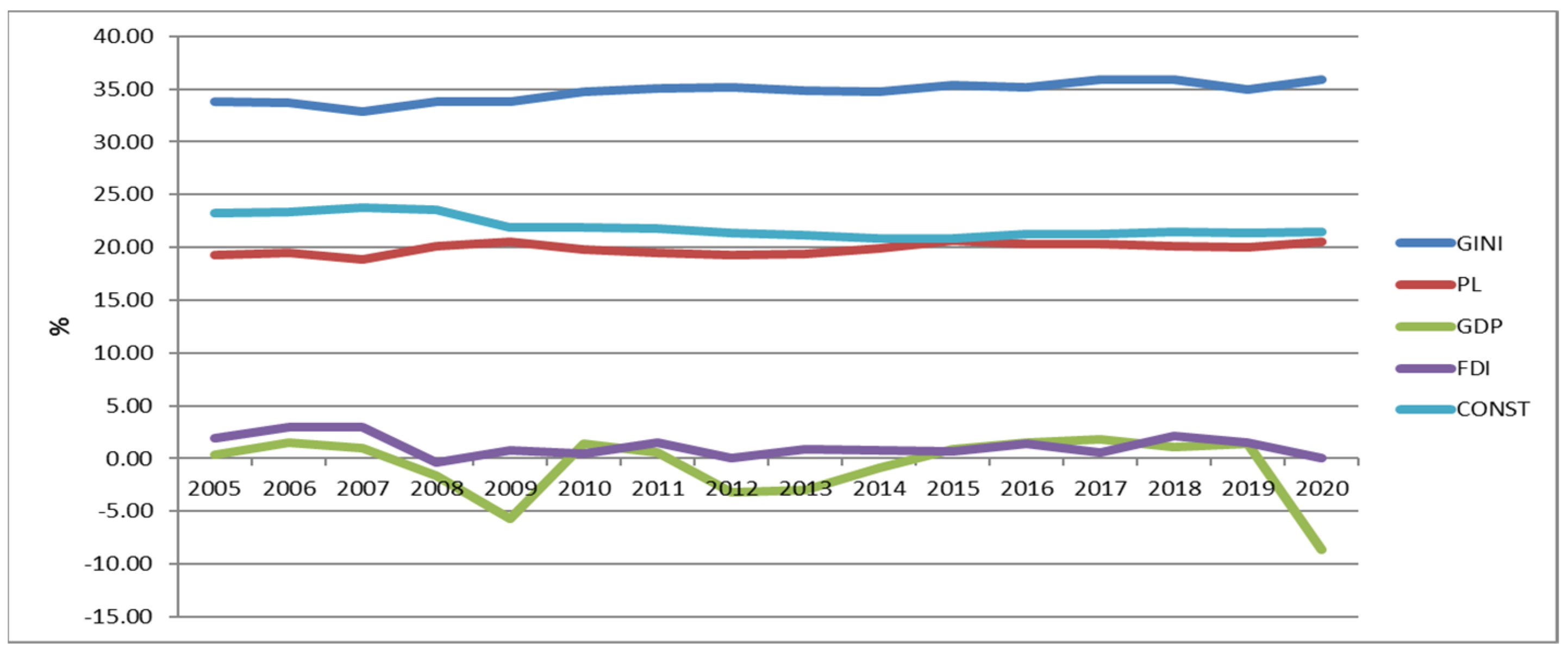

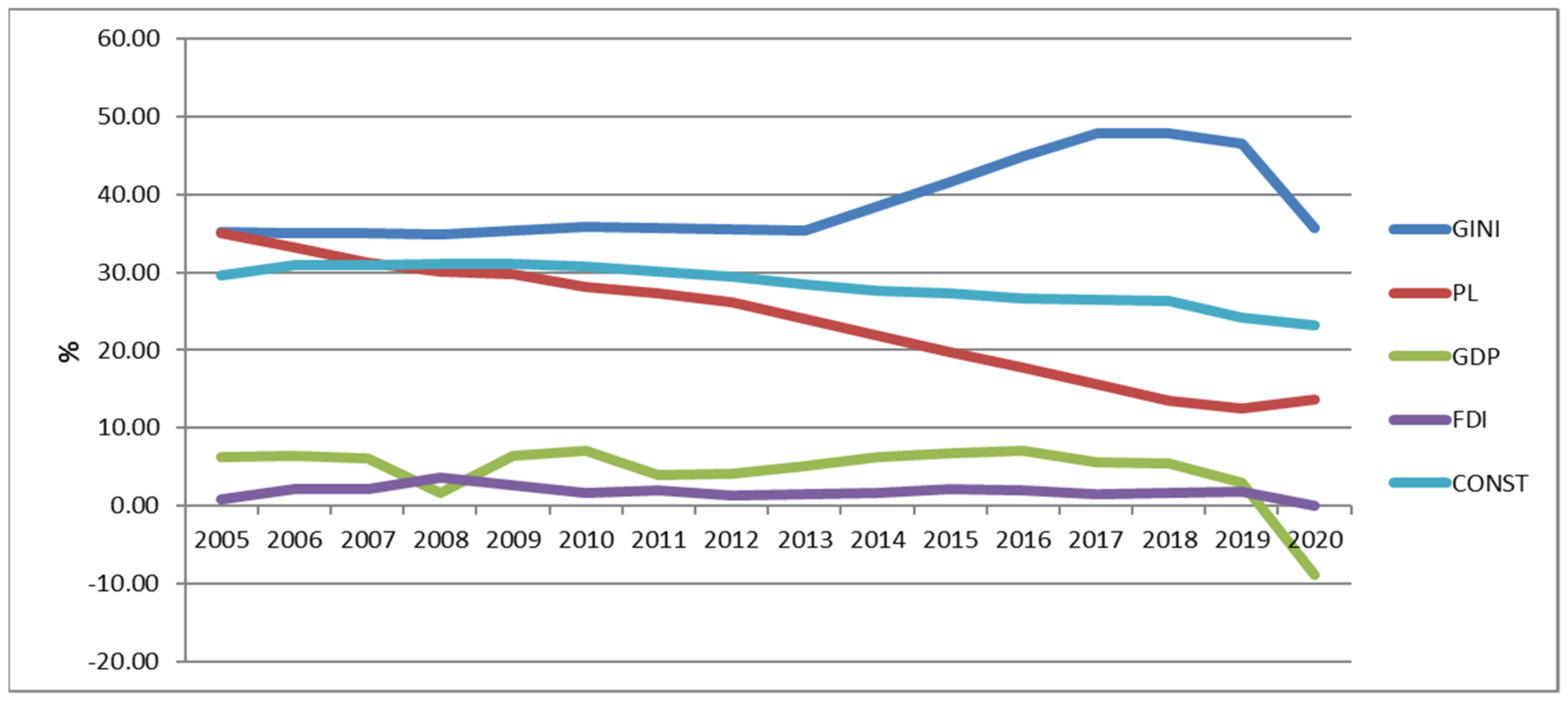

3.1.3. Germany

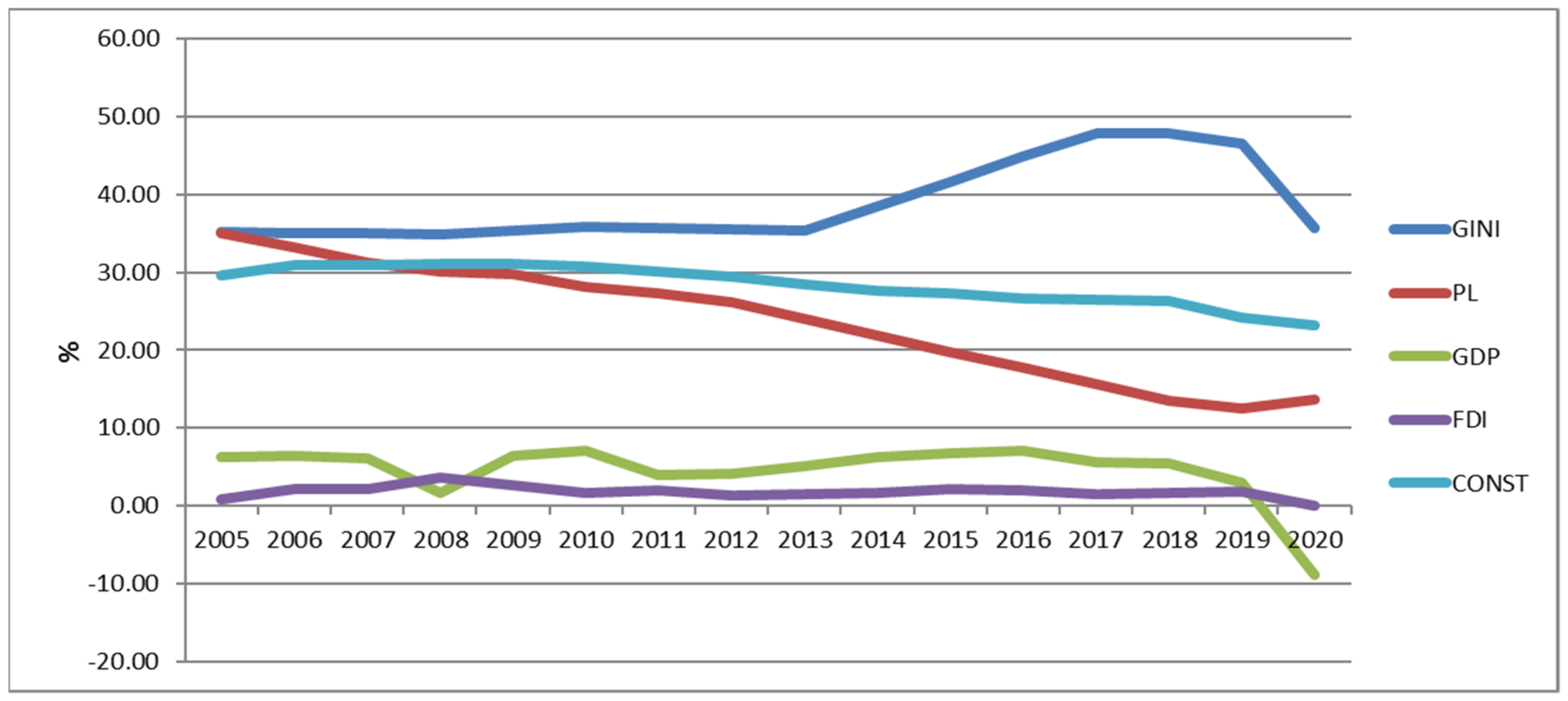

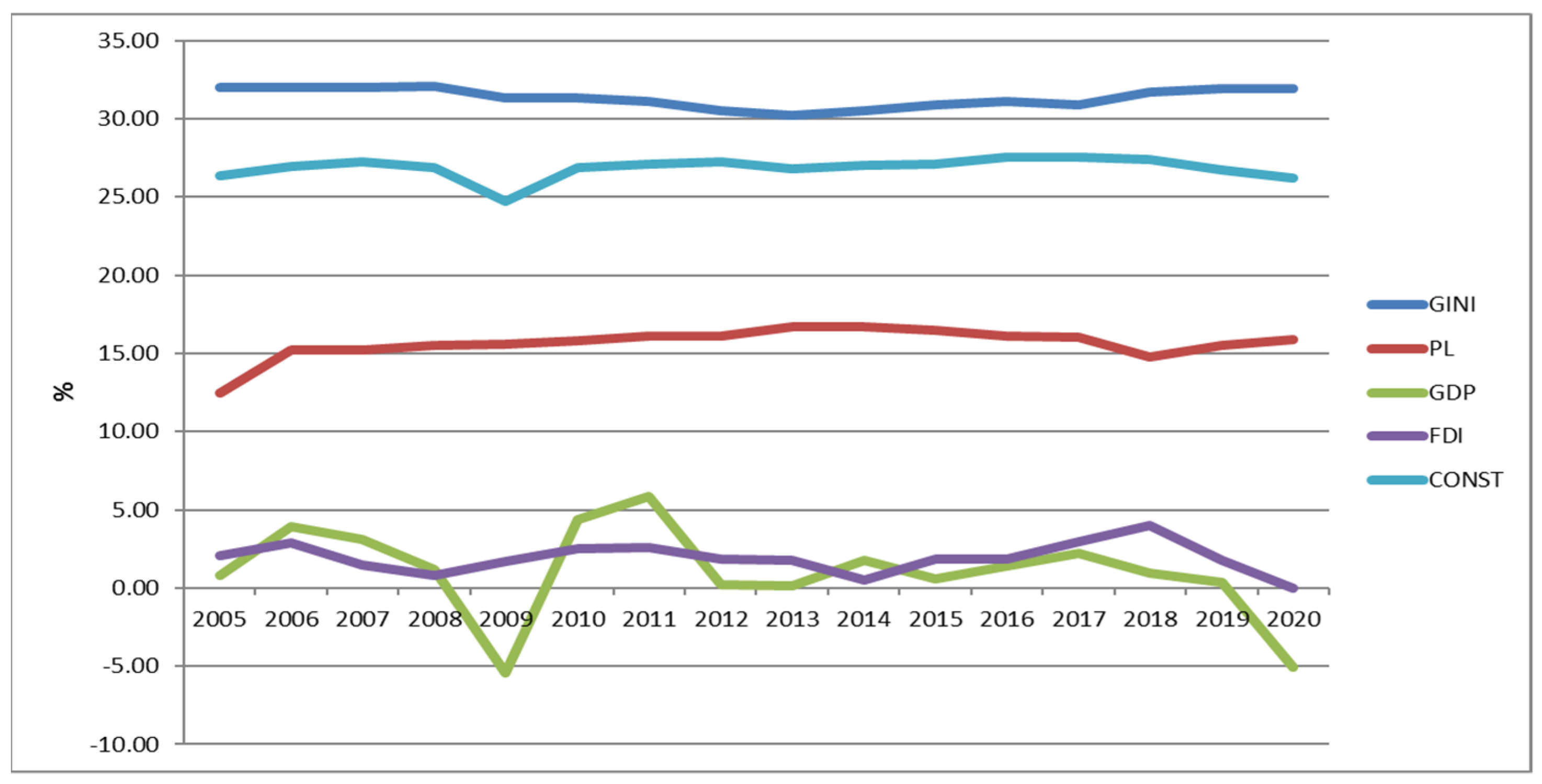

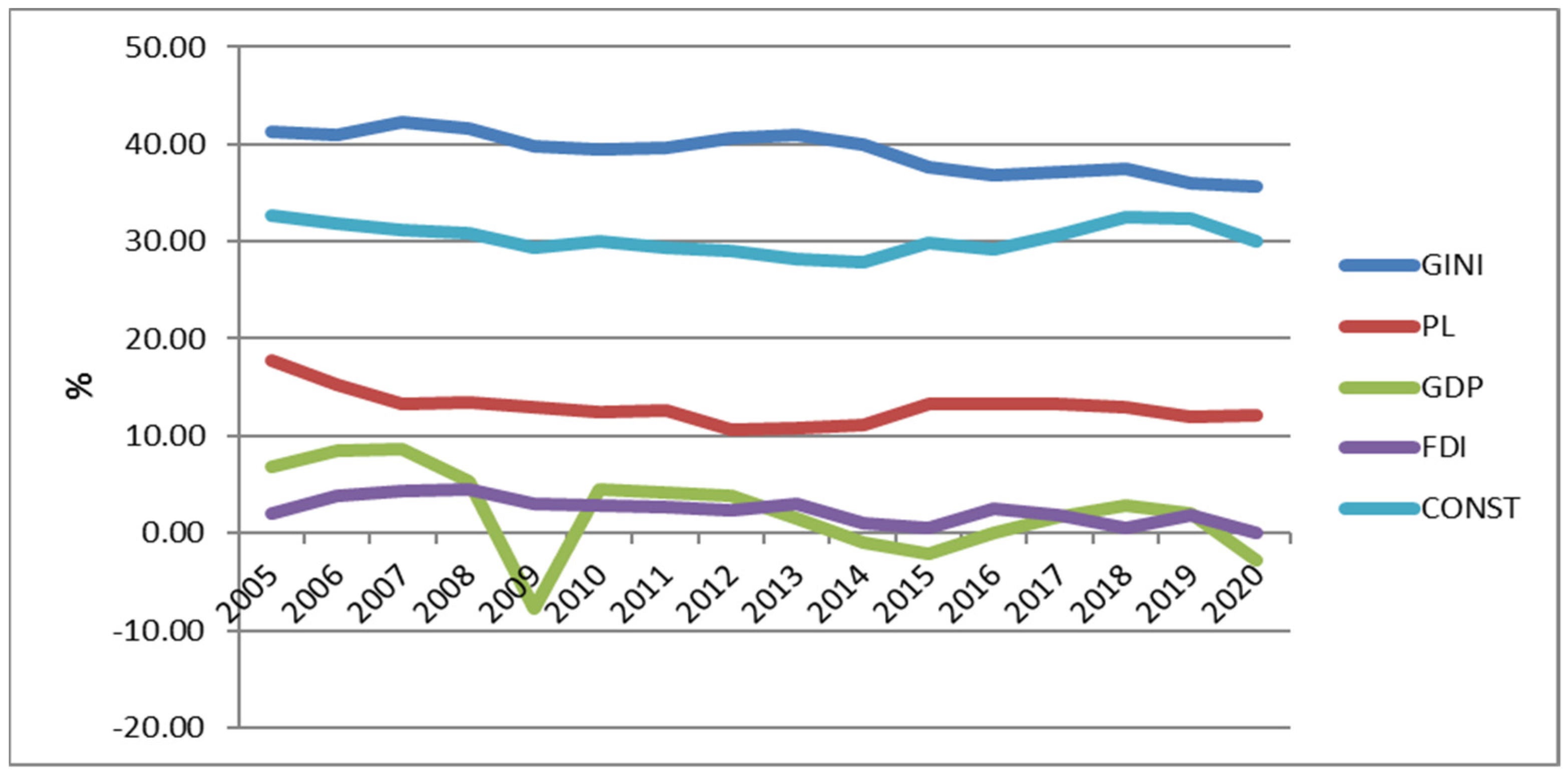

3.1.4. Romania

3.1.5. China

3.1.6. India

3.1.7. Russian Federation

3.2. Second Stage. The Testing Variables GINI, PL (Dependent); GDP, FDI, CONST, Time (Independent)

3.3. Third Stage. The Testing Variables PL (Dependent); GDP, FDI, Time (Independent)

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Adato, Michelle, Michael R. Carter, and Julian May. 2006. Exploring poverty traps and social exclusion in South Africa using qualitative and quantitative data. The Journal of Development Studies 42: 226–47. [Google Scholar] [CrossRef] [Green Version]

- Ahmad, Munir, Zhen-Yu Zhao, Muhammad Irfan, and Marie Claire Mukeshimana. 2019. Empirics on influencing mechanisms among energy, finance, trade, environment, and economic growth: A heterogeneous dynamic panel data analysis of China. Environmental Science and Pollution Research 26: 14148–14170. [Google Scholar] [CrossRef] [PubMed]

- Akaike, Hirotugu. 1981. This Week’s Citation Classic. Current Contents Engineering, Technology, and Applied Sciences 12: 42. Available online: http://www.garfield.library.upenn.edu/classics1981/A1981MS54100001.pdf (accessed on 28 September 2021).

- Anand, Abhishek. 2019. FDI and Its Role in Developing Economy. 4. Available online: https://rrjournals.com/wp-content/uploads/2020/09/2102-2104_RRIJM190404444.pdf (accessed on 28 September 2021).

- Andersen, Torben M. 2015. A flexicurity labor market during recession. IZA World of Labor 173. [Google Scholar] [CrossRef] [Green Version]

- Anetor, Friday Osemenshan. 2019. Economic growth effect of private capital inflows: A structural VAR approach for Nigeria. Journal of Economics and Development 21: 18–29. [Google Scholar] [CrossRef] [Green Version]

- Antoniades, Andreas, Indra Widiarto, and Alexander S. Antonarakis. 2020. Financial Crises and the Attainment of the SDGs: An Adjusted Multidimensional Poverty Approach. Sustainability Science 15: 1683–98. [Google Scholar] [CrossRef] [Green Version]

- Arnal, Elena, and Alexander Hijzen. 2008. The Impact of Foreign Direct Investment on Wages and Working Conditions. Available online: https://scholar.google.com/scholar?hl=en&as_sdt=0%2C5&q=Arnal%2C+E.%2C+and+A.+Hijzen.+%E2%80%98The+Impact+of+Foreign+Direct+Investment+on+Wages+and+Working+Conditions%E2%80%99%2C+2008.&btnG= (accessed on 28 September 2021).

- Asian Development Bank. 2021. Asian Development Bank and India: Fact Sheet (India). Available online: https://www.adb.org/sites/default/files/publication/27768/ind-2020.pdf (accessed on 28 September 2021).

- Azam, Muhammad, and Yi Feng. 2021. Does Foreign Aid Stimulate Economic Growth in Developing Countries? Further Evidence in Both Aggregate and Disaggregated Samples. Quality & Quantity, 1–24. [Google Scholar] [CrossRef]

- Ball, Michael, and Andrew Wood. 1996. Does building investment affect economic growth? Journal of Property Research 13: 99–114. [Google Scholar] [CrossRef]

- Bebczuk, Ricardo. 2003. Asymmetric Information in Financial Markets Cambridge Books. Cambridge Books. Cambridge: Cambridge University, Available online: https://ideas.repec.org/b/cup/cbooks/9780521797320.html (accessed on 28 September 2021).

- Bermejo Carbonell, Jorge, and Richard A. Werner. 2018. Does Foreign Direct Investment Generate Economic Growth? A New Empirical Approach Applied to Spain. Economic Geography 94: 425–56. [Google Scholar] [CrossRef]

- Bhuimali, Anil, Partha Pratim Sengupta, Sidhartha Sankar Laha, and Madhabendra Sinha. 2019. FDI, Trade, and Economic Growth: A Dynamic Panel Study on Global Economy. In The Gains and Pains of Financial Integration and Trade Liberalization. Edited by Rajib Bhattacharyya. Bingley: Emerald Publishing Limited, pp. 77–87. [Google Scholar] [CrossRef]

- Camarero, Mariam, Laura Montolio, and Cecilio Tamarit. 2019. What Drives German Foreign Direct Investment? New Evidence Using Bayesian Statistical Techniques. Economic Modelling 83: 326–45. [Google Scholar] [CrossRef]

- Cantwell, John, and Christian Bellak. 1998. How Important Is Foreign Direct Investment? Oxford Bulletin of Economics and Statistics 60: 99–106. [Google Scholar] [CrossRef]

- Chung, Ming Lau, and Garry D. Bruton. 2008. FDI in China: What We Know and What We Need to Study Next. Academy of Management Perspectives 22: 30–44. [Google Scholar] [CrossRef]

- Coppola, Lusia, and Davide Di Laurea. 2016. Dynamics of Persistent Poverty in Italy at the Beginning of the Crisis. Genus 72: 1–17. Available online: https://genus.springeropen.com/articles/10.1186/s41118-016-0007-x (accessed on 28 September 2021). [CrossRef] [Green Version]

- Coulibaly, Sara Elder, Phu Huynh, Arun Kumar, Dong Eung Lee, Bashar Marafie, Yuki Otsuji, and Netsanet Tesfay. 2021. COVID-19 and Multinational Enterprises: Impacts on FDI, Trade and Decent Work in Asia and the Pacific. ILO Brief. Available online: https://www.researchgate.net/profile/Pelin-Sekerler-Richiardi/publication/350994880_COVID-19_and_multinational_enterprises_Impacts_on_FDI_trade_and_decent_work_in_Asia_and_the_Pacific/links/607e97ad2fb9097c0cf7632e/COVID-19-and-multinational-enterprises-Impacts-on-FDI-trade-and-decent-work-in-Asia-and-the-Pacific.pdf (accessed on 28 September 2021).

- Dhrifi, Abdelhafidh, Raouf Jaziri, and Saleh Alnahdi. 2020. Does Foreign Direct Investment and Environmental Degradation Matter for Poverty? Evidence from Developing Countries. Structural Change and Economic Dynamics 52: 13–21. [Google Scholar] [CrossRef]

- Dickey, David A., and Wayne A. Fuller. 1981. Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica 49: 1057–72. [Google Scholar] [CrossRef]

- Drabek, Zdenek. 2021. Governance of FDI and the East Asian Economic Community. Asia and the Global Economy 1: 100001. [Google Scholar] [CrossRef]

- Durbin, James, and Geoffrey Watson. 1950. Testing for Serial Correlation in Least Squares Regression: I. Biometrika 37: 409–28. [Google Scholar] [CrossRef]

- Engle, Robert F., and Clive W. J. Granger. 1987. Co-Integration and Error Correction: Representation, Estimation, and Testing. Econometrica 55: 251–76. [Google Scholar] [CrossRef]

- Eurostat. 2020. Europe 2020 Indicators—Poverty and Social Exclusion. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Archive:Europe_2020_indicators_-_poverty_and_social_exclusion&oldid=394836 (accessed on 28 September 2021).

- Fang, Jing, Alan Collins, and Shujie Yao. 2021. On the Global COVID-19 Pandemic and China’s FDI. Journal of Asian Economics 74: 101300. [Google Scholar] [CrossRef]

- Friedman, Milton, and Anna J. Schwartz. 1991. A Monetary History of the United States 1867–1960 (1963). The American Economic Review 81: 1. Available online: www.jstor.org/stable/2006787 (accessed on 28 September 2021).

- Hillebrandt, Patricia M. 2000. Economic Theory and the Construction Industry. London: Palgrave Macmillan UK, p. 224. [Google Scholar] [CrossRef]

- Hollander, Samuel. 1997. The Economics of Thomas Robert Malthus. Toronto: University of Toronto Press, vol. 4. [Google Scholar] [CrossRef]

- Jensen, Per H. 2017. Danish Flexicurity: Preconditions and Future Prospects. Industrial Relations Journal 48: 218–30. [Google Scholar] [CrossRef]

- Jensen, Thais Lærkholm, and Niels Johannesen. 2017. The Consumption Effects of the 2007–2008 Financial Crisis: Evidence from Households in Denmark. American Economic Review 107: 3386–414. [Google Scholar] [CrossRef] [Green Version]

- Kargi, Bilal. 2013. Integration between the Economic Growth and the Construction Industry: A Time Series Analysis on Turkey (2000–2012). Political Economy—Development: Public Service Delivery EJournal 2013: 20–34. [Google Scholar] [CrossRef] [Green Version]

- Kastratović, Radovan. 2020. The Impact of Foreign Direct Investment on Host Country Exports: A Meta-Analysis. The World Economy 43: 3142–83. [Google Scholar] [CrossRef]

- Knoerich, Jan. 2017. How Does Outward Foreign Direct Investment Contribute to Economic Development in Less Advanced Home Countries? Oxford Development Studies 45: 443–59. [Google Scholar] [CrossRef]

- Krygina, A. M., I. P. Avilova, M. I. Oberemok, and A. G. Grebenik. 1088. Modeling of Organizational and Functional Components of Investment and Construction Controlling in the Reproduction of Eco-Residential Real Estate. Bristol: IOP Publishing. [Google Scholar] [CrossRef]

- Ly, Bora. 2021. The Implication of FDI in the Construction Industry in Cambodia under BRI. Edited by Albert Tan. Cogent Business & Management 8: 1875542. [Google Scholar] [CrossRef]

- Ma, Le, Chunlu Liu, and Richard Reed. 2017. The Impacts of Residential Construction and Property Prices on Residential Construction Outputs: An Inter-Market Equilibrium Approach. International Journal of Strategic Property Management 21: 296–306. [Google Scholar] [CrossRef]

- Mahembe, Edmore, and Nicholas Odhiambo. 2019. Foreign Aid, Poverty and Economic Growth in Developing Countries: A Dynamic Panel Data Causality Analysis. Cogent Economics & Finance 7: 1626321. [Google Scholar] [CrossRef]

- Mainassara, Yacouba Boubacar, and Célestin C. Kokonendji. 2016. Modified Schwarz and Hannan–Quinn Information Criteria for Weak VARMA Models. Statistical Inference for Stochastic Processes 19: 199–217. [Google Scholar] [CrossRef]

- Mamun, Muhammed, and Irfan Ullah. 2020. COVID-19 Suicides in Pakistan, Dying off Not COVID-19 Fear but Poverty?–The Forthcoming Economic Challenges for a Developing Country. Brain, Behavior, and Immunity 87: 163. [Google Scholar] [CrossRef]

- Mehar, Muhammad Ayub Khan. 2021. Bridge financing during covid-19 pandemics: Nexus of FDI, external borrowing and fiscal policy. Transnational Corporations Review 13: 109–24. [Google Scholar] [CrossRef]

- Michael Osterwald-Lenum Statistics. 2017. Household Balance Sheet Structure in Denmark and Sensitivity to Rising Rates. Available online: https://www.elibrary.imf.org/view/journals/002/2017/159/article-A001-en.xml (accessed on 28 September 2021).

- Mishkin, Frederic S. 1992. Anatomy of a Financial Crisis. Journal of Evolutionary Economics 2: 115–30. [Google Scholar] [CrossRef] [Green Version]

- Mudambi, Ram, and Pietro Navarra. 2003. Political Culture and Foreign Direct Investment: The Case of Italy. Economics of Governance 4: 37–56. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Pinelli, Dino, Roberta Torre, Lucianajulia Pace, Laura Cassio, and Alfonso Arpaia. 2017. The Recent Reform of the Labour Market in Italy: A Review. European Economy Discussion Papers. Available online: https://ec.europa.eu/info/sites/default/files/economy-finance/dp072_en.pdf (accessed on 28 September 2021).

- Ranaldo, Angelo, and Fabricius Somogyi. 2021. Asymmetric Information Risk in FX Markets. Journal of Financial Economics 140: 391–411. [Google Scholar] [CrossRef]

- Reuters Staff. 2021. China Was Largest Recipient of FDI in 2020: Report, REUTERS Edition ed. January 25. Available online: https://www.reuters.com/article/us-china-economy-fdi-idUSKBN29T0TC (accessed on 28 September 2021).

- Ripamonti, Alexandre. 2020. Financial Institutions, Asymmetric Information and Capital Structure Adjustments. The Quarterly Review of Economics and Finance 77: 75–83. [Google Scholar] [CrossRef]

- Ruddock, Les, and Jorge Lopes. 2006. The Construction Sector and Economic Development: The “Bon Curve”. Construction Management and Economics 24: 717–23. [Google Scholar] [CrossRef]

- Saraceno, Chiara, and David Benassi. 2020. Poverty in Italy: Features and Drivers in a European Perspective. Bristol: Policy Press, ISBN 978-1447352211. [Google Scholar]

- Sârbu, Maria-Ramona. 2015. The Impact of Foreign Direct Investment on Economic Growth: The Case of Romania. Acta Universitatis Danubius: Oeconomica 11: 4. Available online: http://journals.univ-danubius.ro/index.php/oeconomica/article/view/2820/2839 (accessed on 28 September 2021).

- Sharma, Rajesh, and Pradeep Kautish. 2020. Examining the Nonlinear Impact of Selected Macroeconomic Determinants on FDI Inflows in India. Journal of Asia Business Studies. [Google Scholar] [CrossRef]

- Shin, Yongcheol, Byungchul Yu, and Matthew Greenwood-Nimmo. 2014. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in honor of Peter Schmidt. New York: Springer, pp. 281–314. [Google Scholar] [CrossRef]

- Shukur, Ghazi, and Panagiotis Mantalos. 2000. A Simple Investigation of the Granger-Causality Test in Integrated-Cointegrated VAR Systems. Journal of Applied Statistics 27: 1021–31. [Google Scholar] [CrossRef]

- Simplice, Asongu, and Nicholas M. Odhiambo. 2020. Foreign Direct Investment, Information Technology and Economic Growth Dynamics in Sub-Saharan Africa. Telecommunications Policy 44: 101838. [Google Scholar] [CrossRef]

- Smith, Adam. 2016. The Wealth of Nations. Aegitas. Available online: https://books.google.ru/books/about/The_Wealth_of_Nations.html?id=lMgDDQAAQBAJ&redir_esc=y (accessed on 28 September 2021).

- Solow, Robert. 2001. From Neoclassical Growth Theory to New Classical Macroeconomics. In Advances in Macroeconomic Theory. Berlin/Heidelberg: Springer, pp. 19–29. [Google Scholar] [CrossRef]

- Toda, Hiro Y., and Taku Yamamoto. 1995. Statistical Inference in Vector Autoregressions with Possibly Integrated Processes. Journal of Econometrics 66: 225–50. [Google Scholar] [CrossRef]

- Tourette, John E. La. 1964. Technological Change and Equilibrium Growth in the Harrod-domar Model. Kyklos 17: 207–26. [Google Scholar] [CrossRef]

- Watanabe, Sumio. 2013. A Widely Applicable Bayesian Information Criterion. Journal of Machine Learning Research 14: 867–97. Available online: https://www.jmlr.org/papers/volume14/watanabe13a/watanabe13a.pdf (accessed on 28 September 2021).

- Zhang, Xiaobo, and Kevin H. Zhang. 2003. How Does Globalisation Affect Regional Inequality within A Developing Country? Evidence from China. The Journal of Development Studies 39: 47–67. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Variable Description | Source |

|---|---|---|

| GINI | The GINI coefficient measures the inequality among values of a frequency distribution (for example, levels of income). | Databank of the World Bank, The People’s Bank of China, The Central Bank of India, The Eurostat Database, The Bank of Russia |

| PL | Poverty headcount ratio at national poverty lines (% of population). National poverty headcount ratio is the percentage of the population living below the national poverty line(s) *. National estimates are based on population-weighted subgroup estimates from household surveys. | Databank of the World Bank, The People’s Bank of China, The Central Bank of India, The Eurostat Database, The Bank of Russia |

| GDP | Gross domestic product (%). | Databank of the World Bank, The People’s Bank of China, The Central Bank of India, The Eurostat Database, The Bank of Russia |

| FDI | Foreign direct investment is an investment in the form of a controlling ownership in a business in one country by an entity based in another country (% of GDP). | Databank of the World Bank, The People’s Bank of China, The Central Bank of India, The Eurostat Database, The Bank of Russia |

| CONST | Investment in construction (% of GDP). | Databank of the World Bank, The People’s Bank of China, The Central Bank of India, The Eurostat Database, The Bank of Russia |

| Coefficient | Std. Error | t-Statistic | p-Value | |||

|---|---|---|---|---|---|---|

| GINI | 0.026618 | 0.256879 | 0.1036 | 0.9197 | ||

| GDP | 0.0809871 | 0.0566291 | 1.43 | 0.1865 | ||

| FDI | −0.000762464 | 0.0427622 | −0.01783 | 0.9862 | ||

| CONST | −0.454022 | 0.132775 | −3.419 | 0.0076 | *** | |

| Denmark | time | 0.172093 | 0.0628942 | 2.736 | 0.023 | ** |

| PL | 0.592239 | 0.161965 | 3.657 | 0.0044 | *** | |

| GDP | −0.0754308 | 0.0580401 | −1.300 | 0.2229 | ||

| FDI | 0.0470311 | 0.0503178 | 0.9347 | 0.372 | ||

| CONST | 0.233361 | 0.0906402 | 2.575 | 0.0277 | ** | |

| time | 0.021956 | 0.0306726 | 0.7158 | 0.4905 | ||

| GINI | 0.893916 | 0.109627 | 8.154 | <0.0001 | *** | |

| GDP | 0.0384199 | 0.049328 | 0.7789 | 0.4541 | ||

| FDI | −0.478590 | 0.157772 | −3.033 | 0.0126 | ** | |

| CONST | 0.187259 | 0.156835 | 1.194 | 0.26 | ||

| Italy | time | 0.0310803 | 0.0528444 | 0.5881 | 0.5695 | |

| PL | 1.13539 | 0.303569 | 3.74 | 0.0038 | *** | |

| GDP | −0.0590081 | 0.19111 | −0.3088 | 0.7638 | ||

| FDI | −0.423821 | 0.498366 | −0.8504 | 0.415 | ||

| CONST | −0.0467304 | 0.274328 | −0.1703 | 0.8681 | ||

| time | −0.177423 | 0.0894793 | −1.983 | 0.0755 | * | |

| GINI | 0.944452 | 0.127836 | 7.388 | <0.0001 | *** | |

| GDP | 0.0494171 | 0.0589708 | 0.838 | 0.4216 | ||

| FDI | −0.0121249 | 0.112351 | −0.1079 | 0.9162 | ||

| CONST | 0.0492485 | 0.156907 | 0.3139 | 0.7601 | ||

| Germany | time | 0.0422493 | 0.0321646 | 1.314 | 0.2183 | |

| PL | 0.342472 | 0.160316 | 2.136 | 0.0584 | * | |

| GDP | −0.0386750 | 0.0586016 | −0.6600 | 0.5242 | ||

| FDI | −0.208123 | 0.162546 | −1.280 | 0.2293 | ||

| CONST | 0.417231 | 0.093077 | 4.483 | 0.0012 | *** | |

| time | −0.0316649 | 0.0369549 | −0.8569 | 0.4116 | ||

| GINI | 1.01525 | 0.170158 | 5.966 | 0.0001 | *** | |

| GDP | 0.0170253 | 0.0740764 | 0.2298 | 0.8229 | ||

| FDI | 0.114891 | 0.285843 | 0.4019 | 0.6962 | ||

| CONST | −0.0506263 | 0.145319 | −0.3484 | 0.7348 | ||

| Romania | time | 0.0409068 | 0.125751 | 0.3253 | 0.7517 | |

| PL | 0.964071 | 0.200072 | 4.819 | 0.0007 | *** | |

| GDP | 0.0086928 | 0.0860435 | 0.101 | 0.9215 | ||

| FDI | −0.176010 | 0.259211 | −0.6790 | 0.5125 | ||

| CONST | 0.0406611 | 0.0959284 | 0.4239 | 0.6806 | ||

| time | −0.00247523 | 0.145654 | −0.01699 | 0.9868 | ||

| GINI | 0.648236 | 0.129482 | 5.006 | 0.0005 | *** | |

| GDP | −0.386015 | 0.188637 | −2.046 | 0.0679 | * | |

| FDI | 0.28575 | 0.533604 | 0.5355 | 0.604 | ||

| CONST | 0.377307 | 0.116818 | 3.23 | 0.009 | *** | |

| China | time | 0.027213 | 0.119843 | 0.2271 | 0.8249 | |

| PL | 0.869258 | 0.152618 | 5.696 | 0.0002 | *** | |

| GDP | 0.640596 | 0.337184 | 1.9 | 0.0866 | * | |

| FDI | −0.859157 | 0.933718 | −0.9201 | 0.3792 | ||

| CONST | −0.0598627 | 0.126663 | −0.4726 | 0.6466 | ||

| time | −0.0482681 | 0.321312 | −0.1502 | 0.8836 | ||

| GINI | 0.770693 | 0.100268 | 7.686 | <0.0001 | *** | |

| GDP | 0.726296 | 0.0813799 | 8.925 | <0.0001 | *** | |

| FDI | 1.50709 | 0.501455 | 3.005 | 0.0132 | ** | |

| CONST | −0.0345463 | 0.0965495 | −0.3578 | 0.7279 | ||

| India | time | 0.445038 | 0.16533 | 2.692 | 0.0226 | ** |

| PL | 0.793757 | 0.200599 | 3.957 | 0.0027 | *** | |

| GDP | −0.364087 | 0.0503832 | −7.226 | <0.0001 | *** | |

| FDI | −0.500581 | 0.366927 | −1.364 | 0.2024 | ||

| CONST | 0.298762 | 0.25015 | 1.194 | 0.2599 | ||

| time | −0.237685 | 0.205122 | −1.159 | 0.2735 | ||

| GINI | 1.02894 | 0.11062 | 9.302 | <0.0001 | *** | |

| GDP | 0.180971 | 0.077181 | 2.345 | 0.041 | ** | |

| FDI | 0.0362492 | 0.334864 | 0.1083 | 0.9159 | ||

| CONST | −0.0839122 | 0.164685 | −0.5095 | 0.6214 | ||

| Russian | time | 0.0634127 | 0.108797 | 0.5829 | 0.5729 | |

| Federation | PL | 0.448745 | 0.214044 | 2.097 | 0.0624 | * |

| GDP | −0.0797962 | 0.0612406 | −1.303 | 0.2218 | ||

| FDI | −0.133466 | 0.305894 | −0.4363 | 0.6719 | ||

| CONST | 0.263845 | 0.115098 | 2.292 | 0.0448 | ** | |

| time | −0.0773405 | 0.101365 | −0.7630 | 0.4631 |

| Coefficient | Std. Error | t-Statistic | R2 | p-Value | |||

|---|---|---|---|---|---|---|---|

| Denmark | PL | 1.01205 | 0.0438296 | 23.09 | 0.998114 | <0.0001 | *** |

| GDP | 0.0576537 | 0.0867968 | 0.6642 | 0.5232 | |||

| FDI | 0.0239685 | 0.0699591 | 0.3426 | 0.7398 | * | ||

| time | −0.0207794 | 0.0497498 | −0.4177 | 0.686 | |||

| Italy | PL | 1.01703 | 0.02016 | 50.45 | 0.999548 | <0.0001 | *** |

| GDP | −0.0400252 | 0.0497395 | −0.8047 | 0.438 | |||

| FDI | −0.186006 | 0.159022 | −1.170 | 0.2668 | |||

| time | −0.0103191 | 0.0314909 | −0.3277 | 0.7493 | |||

| Germany | PL | 1.00014 | 0.0363862 | 27.49 | 0.99923 | <0.0001 | *** |

| GDP | 0.0347939 | 0.0608743 | 0.5716 | 0.5816 | |||

| FDI | 0.098741 | 0.223448 | 0.4419 | 0.669 | |||

| time | −0.0199719 | 0.0396249 | −0.5040 | 0.6264 | |||

| Romania | PL | 1.00336 | 0.379329 | 2.645 | 0.99919 | 0.0457 | ** |

| GDP | −0.0537240 | 0.108067 | −0.4971 | 0.6402 | |||

| FDI | −0.195987 | 0.363587 | −0.5390 | 0.613 | |||

| time | −0.138467 | 0.177902 | −0.7783 | 0.4716 | |||

| China | PL | 0.679165 | 0.0440323 | 15.42 | 0.998822 | <0.0001 | *** |

| GDP | 0.468362 | 0.124559 | 3.76 | 0.0045 | *** | ||

| FDI | −0.229234 | 0.289017 | −0.7932 | 0.4481 | |||

| time | −0.202878 | 0.0405263 | −5.006 | 0.0007 | *** | ||

| India | PL | 0.935378 | 0.0537443 | 17.4 | 0.99841 | <0.0001 | *** |

| GDP | 0.066882 | 0.220774 | 0.3029 | 0.7688 | |||

| FDI | 0.297874 | 0.53714 | 0.5546 | 0.5927 | |||

| time | −0.0827006 | 0.0948836 | −0.8716 | 0.4061 | |||

| Russian | PL | 0.994995 | 0.0788866 | 12.61 | 0.99859 | <0.0001 | *** |

| Federation | GDP | −0.0628013 | 0.105468 | −0.5955 | 0.5662 | ||

| FDI | 0.0340828 | 0.24887 | 0.1369 | 0.8941 | |||

| time | 0.02244 | 0.132899 | 0.1689 | 0.8696 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sukhadolets, T.; Stupnikova, E.; Fomenko, N.; Kapustina, N.; Kuznetsov, Y. Foreign Direct Investment (FDI), Investment in Construction and Poverty in Economic Crises (Denmark, Italy, Germany, Romania, China, India and Russia). Economies 2021, 9, 152. https://doi.org/10.3390/economies9040152

Sukhadolets T, Stupnikova E, Fomenko N, Kapustina N, Kuznetsov Y. Foreign Direct Investment (FDI), Investment in Construction and Poverty in Economic Crises (Denmark, Italy, Germany, Romania, China, India and Russia). Economies. 2021; 9(4):152. https://doi.org/10.3390/economies9040152

Chicago/Turabian StyleSukhadolets, Tatyana, Elena Stupnikova, Natalia Fomenko, Nadezhda Kapustina, and Yuri Kuznetsov. 2021. "Foreign Direct Investment (FDI), Investment in Construction and Poverty in Economic Crises (Denmark, Italy, Germany, Romania, China, India and Russia)" Economies 9, no. 4: 152. https://doi.org/10.3390/economies9040152

APA StyleSukhadolets, T., Stupnikova, E., Fomenko, N., Kapustina, N., & Kuznetsov, Y. (2021). Foreign Direct Investment (FDI), Investment in Construction and Poverty in Economic Crises (Denmark, Italy, Germany, Romania, China, India and Russia). Economies, 9(4), 152. https://doi.org/10.3390/economies9040152