Economic Reforms, Labour Markets and Formal Sector Employment: Evidence from India

Abstract

:1. Introduction

2. Background and Context

2.1. Literature Review

2.1.1. Impacts of Economic Reform on Firm Level Employment

2.1.2. Does Labour Market Flexibility Matter?

2.2. Context to the Indian Reforms of 1991–1997

3. Data

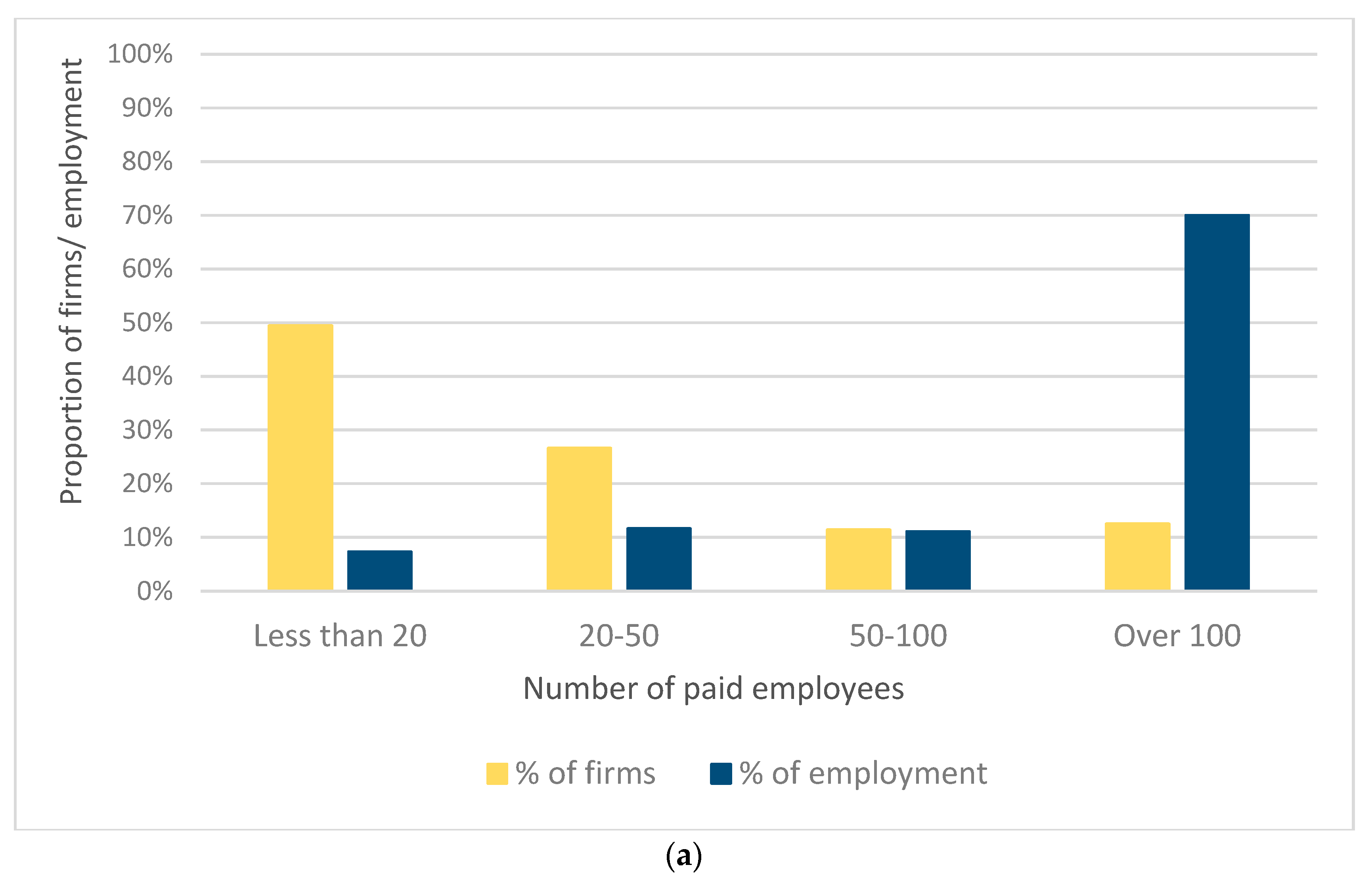

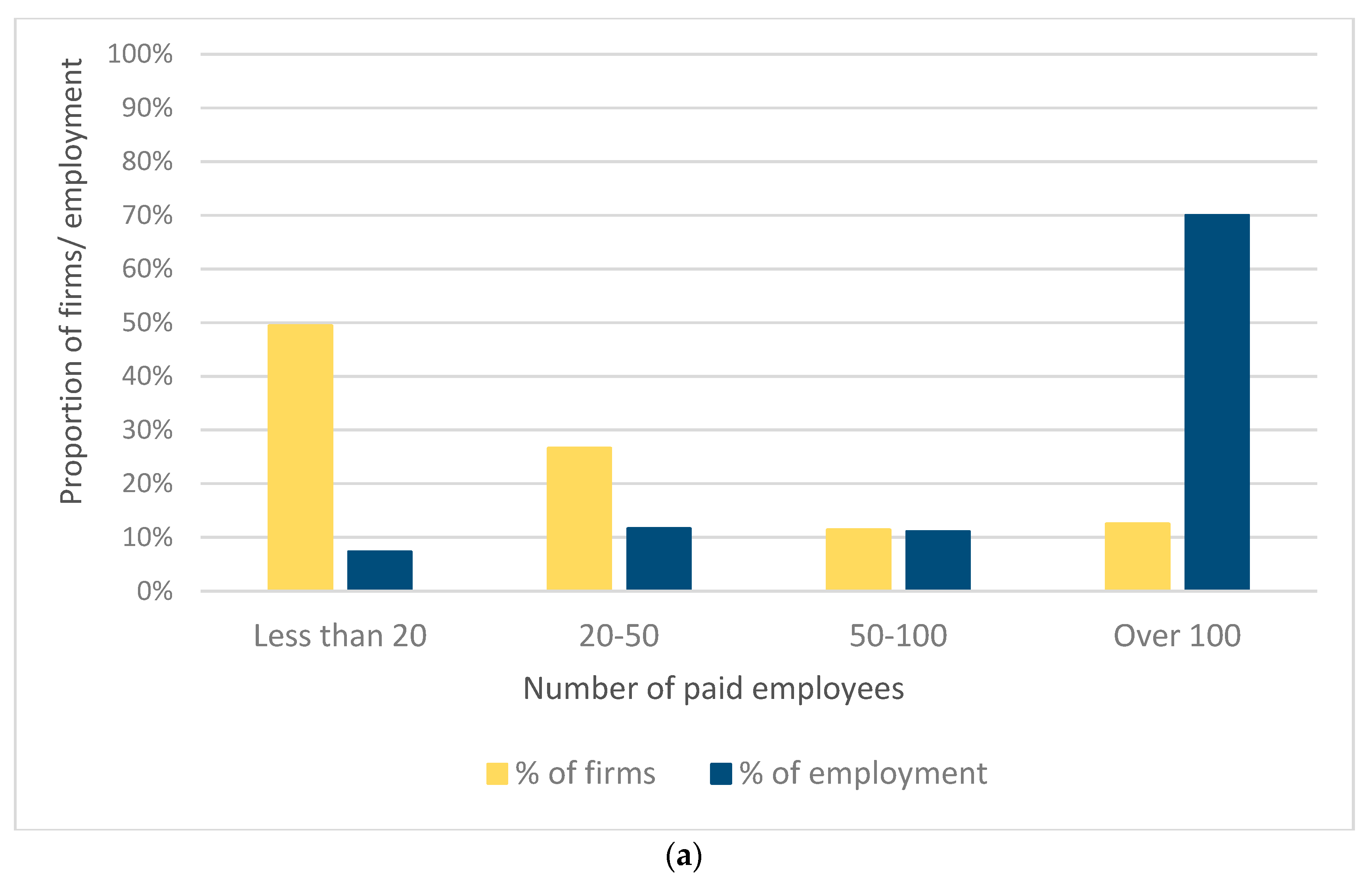

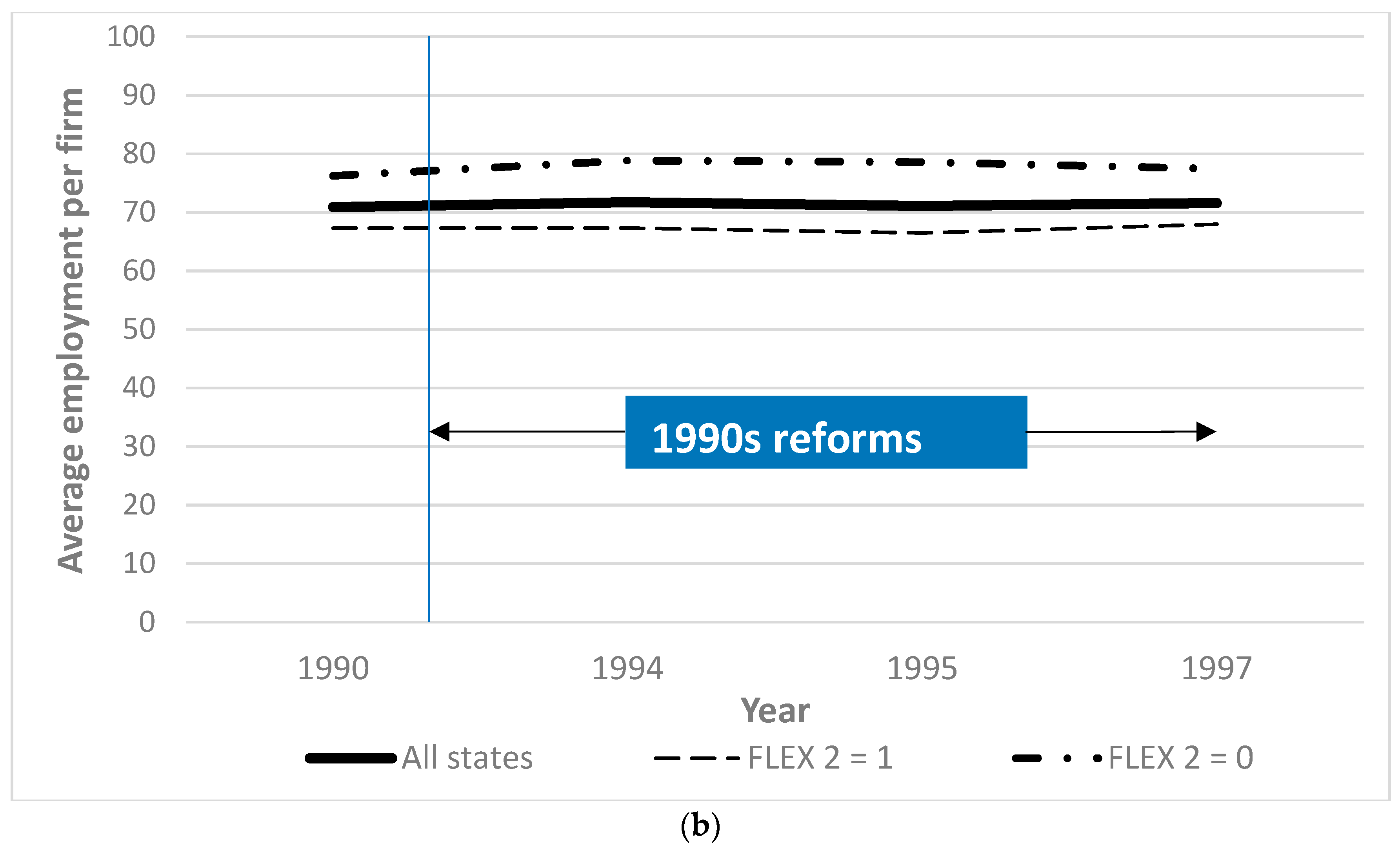

3.1. Labour Market Data

3.2. Data on the 1990s Reforms

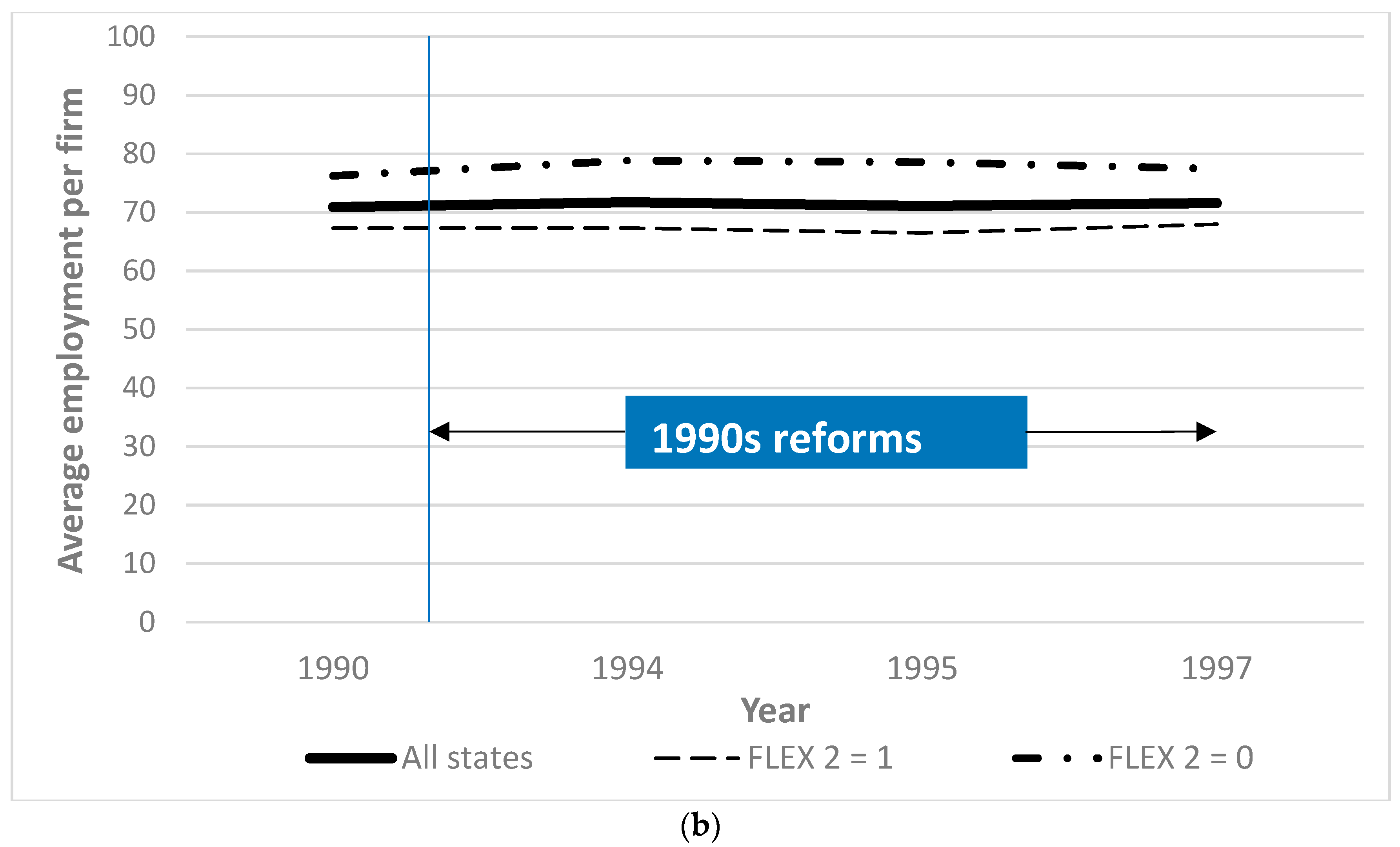

3.3. Measure of Labour Market Flexibility

4. Method

5. Results

5.1. Baseline Regressions: Firm Level

5.2. Industry Level Results

5.3. Implications for the Indian Labour Market

5.4. Increases in Product Market Competition

5.5. Composition of Employment

6. Further Analysis and Robustness Checks

7. Discussion and Conclusions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Period (Dependent Variable) | t + 1 | t + 2 | t + 3 |

|---|---|---|---|

| Dependent variable: Final goods tariffs | |||

| ln (Formal employment—paid) | 0.005810 | 0.017725 | 0.025388 |

| (0.061842) | (0.023411) | (0.019702) | |

| ln (Formal employment—total) | 0.004561 | 0.019872 | 0.023948 |

| (0.061523) | (0.022773) | (0.019359) | |

| Absolute formal employment (paid) | −0.000000 | 0.000000 | 0.000001 |

| (0.000000) | (0.000000) | (0.000000) | |

| Share of formal employment (paid) | −4.120364 * | −0.750120 | 0.803087 |

| (1.600927) | (0.924981) | (0.895980) | |

| Dependent variable: Input tariffs | |||

| ln (Formal employment—paid) | −0.036929 | 0.000577 | −0.000784 |

| (0.031397) | (0.008518) | (0.006740) | |

| ln (Formal employment—total) | −0.032653 | 0.002355 | −0.000268 |

| (0.029948) | (0.008517) | (0.006744) | |

| Absolute formal employment (paid) | −0.000000 | −0.000000 | −0.000000 |

| (0.000000) | (0.000000) | (0.000000) | |

| Share of formal employment (paid) | −6.129283 ** | −0.745511 | 0.048776 |

| (2.239942) | (0.534617) | (0.513832) | |

| Period (Dependent Variable) | t + 1 | t + 2 | t + 3 |

|---|---|---|---|

| Dependent variable: Change in final goods tariffs | |||

| Change in ln (formal employment) | 0.097508 | 0.057736 | 0.022285 |

| (0.076559) | (0.044515) | (0.035028) | |

| ln (formal employment) | 0.219995 * | 0.097065 | 0.074310 |

| (0.107854) | (0.057578) | (0.057011) | |

| Change in absolute formal employment | 0.000001 | 0.000001 | 0.000001 * |

| (0.000001) | (0.000001) | (0.000000) | |

| Absolute formal employment | 0.000002 ** | 0.000001 * | 0.000002 * |

| (0.000001) | (0.000001) | (0.000001) | |

| Dependent variable: Change in input tariffs | |||

| Change in ln (formal employment) | 0.019153 | 0.014280 | −0.001239 |

| (0.024563) | (0.015291) | (0.010634) | |

| ln (formal employment) | 0.069189 * | 0.003984 | 0.007497 |

| (0.031352) | (0.016301) | (0.013051) | |

| Change in absolute formal employment | 0.000001 * | 0.000000 | 0.000000 |

| (0.000001) | (0.000000) | (0.000000) | |

| Absolute formal employment | 0.000002 | −0.000000 | −0.000000 |

| (0.000001) | (0.000000) | (0.000000) | |

| Baseline | Change in ‘FLEX 2’ Value for Delhi and Jammu & Kashmir (0 to 1) | Excluding Firms with Fewer Than Ten Paid Employees | Including Firms Reporting Zero or No Value for Raw Material Use/Physical Products | Using Input Tariffs Based on Final Goods Tariffs for Manufacturing Industries Only | |

|---|---|---|---|---|---|

| Final goods tariffs | −0.020 | −0.018 | 0.059 | −0.007 | −0.130 * |

| (0.075) | (0.081) | (0.054) | (0.075) | (0.076) | |

| Final goods tariffs * FLEX 2 | 0.132 | 0.122 | 0.039 | 0.118 | 0.199 * |

| (0.115) | (0.119) | (0.084) | (0.114) | (0.115) | |

| Input tariffs | −0.680 *** | −0.703 *** | −0.656 *** | −0.720 *** | −0.059 |

| (0.211) | (0.218) | (0.191) | (0.215) | (0.187) | |

| Input tariffs * FLEX 2 | 0.021 | 0.056 | 0.189 | 0.028 | −0.162 |

| (0.216) | (0.222) | (0.193) | (0.216) | (0.149) | |

| Delicensing | 0.084 | 0.089 | 0.072 | 0.081 | 0.073 |

| (0.061) | (0.066) | (0.048) | (0.061) | (0.063) | |

| Delicensing * FLEX 2 | −0.098 | −0.099 | −0.048 | −0.086 | −0.119 |

| (0.083) | (0.085) | (0.067) | (0.085) | (0.087) | |

| FDI reform | −0.115 ** | −0.103 ** | −0.080 ** | −0.107 ** | −0.090 * |

| (0.045) | (0.048) | (0.035) | (0.046) | (0.047) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.178 *** | 0.140 *** | 0.206 *** | 0.192 *** |

| (0.067) | (0.069) | (0.051) | (0.067) | (0.068) | |

| Flexible labour markets: Effects of changes in final goods tariffs | |||||

| Row 1 + Row 2 | 0.111 | 0.104 | 0.098 | 0.111 | 0.069 |

| Standard Error | 0.063 | 0.061 | 0.046 | 0.062 | 0.062 |

| p-value (combined effect = 0) | 0.078 | 0.088 | 0.035 | 0.075 | 0.268 |

| Flexible labour markets: Effects of changes in input tariffs | |||||

| Row 3 + Row 4 | −0.659 | −0.646 | −0.468 | −0.692 | −0.221 |

| Standard Error | 0.199 | 0.195 | 0.181 | 0.202 | 0.176 |

| p-value (combined effect = 0) | 0.001 | 0.001 | 0.010 | 0.001 | 0.209 |

| Flexible labour markets: Effects of delicensing | |||||

| Row 5 + Row 6 | −0.013 | −0.010 | 0.025 | −0.005 | −0.046 |

| Standard Error | 0.036 | 0.034 | 0.029 | 0.038 | 0.039 |

| p-value (combined effect = 0) | 0.707 | 0.781 | 0.400 | 0.896 | 0.238 |

| Flexible labour markets: Effects of FDI reform | |||||

| Row 7 + Row 8 | 0.093 | 0.075 | 0.060 | 0.099 | 0.102 |

| Standard Error | 0.039 | 0.038 | 0.027 | 0.039 | 0.039 |

| p-value (combined effect = 0) | 0.017 | 0.047 | 0.027 | 0.011 | 0.010 |

| State FE | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 160,883 | 131,147 | 163,921 | 160,883 |

| R-squared | 0.205 | 0.205 | 0.201 | 0.203 | 0.205 |

| Baseline (All Firms) | Consumer Goods Industries | Basic/Capital/Intermediate Goods Industries | Single Product Firms | Multi-Product Firms | Firms That Are Fully Privately Owned | Firms That Are Not Fully Privately Owned | |

|---|---|---|---|---|---|---|---|

| Final goods tariffs | −0.020 | 0.031 | −0.010 | 0.042 | 0.035 | −0.070 | 0.078 |

| (0.075) | (0.083) | (0.080) | (0.057) | (0.089) | (0.077) | (0.126) | |

| Final goods tariffs * FLEX 2 | 0.132 | 0.073 | 0.198 | −0.033 | 0.140 | 0.178 | 0.037 |

| (0.115) | (0.119) | (0.136) | (0.076) | (0.142) | (0.121) | (0.143) | |

| Input tariffs | −0.680 *** | −0.667 ** | −0.623 ** | −0.407 | −1.317 *** | −0.537 *** | −0.554 |

| (0.211) | (0.295) | (0.265) | (0.248) | (0.265) | (0.206) | (0.472) | |

| Input tariffs * FLEX 2 | 0.021 | −0.022 | −0.460 * | −0.141 | 0.417 | −0.070 | −0.080 |

| (0.216) | (0.298) | (0.244) | (0.233) | (0.272) | (0.211) | (0.348) | |

| Delicensing | 0.084 | 0.183 * | −0.095 * | 0.148 | 0.011 | 0.100 | −0.063 |

| (0.061) | (0.096) | (0.051) | (0.095) | (0.051) | (0.066) | (0.076) | |

| Delicensing * FLEX 2 | −0.098 | −0.189 | 0.068 | −0.253 * | −0.004 | −0.099 | 0.011 |

| (0.083) | (0.128) | (0.067) | (0.140) | (0.059) | (0.089) | (0.081) | |

| FDI reform | −0.115 ** | −0.136 ** | 0.015 | −0.049 | −0.092 * | −0.108 ** | 0.185 ** |

| (0.045) | (0.067) | (0.046) | (0.050) | (0.048) | (0.046) | (0.093) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.338 *** | −0.043 | 0.006 | 0.281 *** | 0.218 *** | −0.278 ** |

| (0.067) | (0.097) | (0.046) | (0.056) | (0.075) | (0.068) | (0.127) | |

| Flexible labour markets: Effects of changes in final goods tariffs | |||||||

| Row 1 + Row 2 | 0.111 | 0.104 | 0.188 | 0.010 | 0.174 | 0.108 | 0.115 |

| Standard Error | 0.063 | 0.070 | 0.098 | 0.060 | 0.083 | 0.067 | 0.106 |

| p-value (combined effect = 0) | 0.078 | 0.139 | 0.056 | 0.874 | 0.035 | 0.106 | 0.279 |

| Flexible labour markets: Effects of changes in input tariffs | |||||||

| Row 3 + Row 4 | −0.659 | −0.689 | −1.083 | −0.548 | −0.900 | −0.606 | −0.634 |

| Standard Error | 0.199 | 0.279 | 0.305 | 0.249 | 0.236 | 0.201 | 0.496 |

| p-value (combined effect = 0) | 0.001 | 0.014 | 0.000 | 0.028 | 0.000 | 0.003 | 0.202 |

| Flexible labour markets: Effects of delicensing | |||||||

| Row 5 + Row 6 | −0.013 | −0.006 | −0.027 | −0.105 | 0.007 | 0.001 | −0.052 |

| Standard Error | 0.036 | 0.050 | 0.041 | 0.061 | 0.040 | 0.038 | 0.081 |

| p-value (combined effect = 0) | 0.707 | 0.901 | 0.503 | 0.087 | 0.854 | 0.981 | 0.523 |

| Flexible labour markets: Effects of FDI reform | |||||||

| Row 7 + Row 8 | 0.093 | 0.202 | −0.028 | −0.042 | 0.189 | 0.110 | −0.093 |

| Standard Error | 0.039 | 0.058 | 0.041 | 0.042 | 0.048 | 0.040 | 0.095 |

| p-value (combined effect = 0) | 0.017 | 0.000 | 0.497 | 0.310 | 0.000 | 0.006 | 0.328 |

| State FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 96,947 | 63,936 | 59,164 | 83,640 | 150,347 | 10,536 |

| R-squared | 0.205 | 0.236 | 0.146 | 0.198 | 0.243 | 0.189 | 0.400 |

| Excluding: | |||||||

|---|---|---|---|---|---|---|---|

| Baseline (All Firms) | Jammu & Kashmir | Punjab | Haryana | Delhi | Rajasthan | Uttar Pradesh | |

| Final goods tariffs | −0.020 | −0.020 | 0.043 | 0.007 | −0.028 | −0.034 | −0.042 |

| (0.075) | (0.076) | (0.066) | (0.079) | (0.079) | (0.075) | (0.090) | |

| Final goods tariffs * FLEX 2 | 0.132 | 0.131 | 0.029 | 0.083 | 0.135 | 0.147 | 0.153 |

| (0.115) | (0.116) | (0.093) | (0.117) | (0.119) | (0.117) | (0.130) | |

| Input tariffs | −0.680 *** | −0.676 *** | −0.685 *** | −0.717 *** | −0.714 *** | −0.605 *** | −0.620 *** |

| (0.211) | (0.212) | (0.211) | (0.217) | (0.218) | (0.212) | (0.239) | |

| Input tariffs * FLEX 2 | 0.021 | 0.017 | 0.045 | 0.102 | 0.047 | −0.042 | −0.062 |

| (0.216) | (0.218) | (0.206) | (0.218) | (0.223) | (0.221) | (0.238) | |

| Delicensing | 0.084 | 0.084 | 0.070 | 0.084 | 0.094 | 0.082 | 0.114 * |

| (0.061) | (0.062) | (0.064) | (0.065) | (0.065) | (0.061) | (0.068) | |

| Delicensing * FLEX 2 | −0.098 | −0.097 | −0.084 | −0.092 | −0.102 | −0.104 | −0.116 |

| (0.083) | (0.083) | (0.086) | (0.086) | (0.086) | (0.085) | (0.084) | |

| FDI reform | −0.115 ** | −0.115 ** | −0.095 * | −0.129 *** | −0.109 ** | −0.109 ** | −0.121 ** |

| (0.045) | (0.046) | (0.049) | (0.048) | (0.048) | (0.045) | (0.057) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.206 *** | 0.153 ** | 0.221 *** | 0.202 *** | 0.198 *** | 0.216 *** |

| (0.067) | (0.067) | (0.062) | (0.070) | (0.069) | (0.068) | (0.079) | |

| Flexible labour markets: Effects of changes in final goods tariffs | |||||||

| Row 1 + Row 2 | 0.111 | 0.111 | 0.072 | 0.091 | 0.107 | 0.113 | 0.110 |

| Standard Error | 0.063 | 0.063 | 0.055 | 0.062 | 0.063 | 0.066 | 0.065 |

| p-value (combined effect = 0) | 0.078 | 0.081 | 0.188 | 0.145 | 0.090 | 0.085 | 0.087 |

| Flexible labour markets: Effects of changes in input tariffs | |||||||

| Row 3 + Row 4 | −0.659 | −0.658 | −0.641 | −0.615 | −0.666 | −0.646 | −0.682 |

| Standard Error | 0.199 | 0.200 | 0.201 | 0.201 | 0.201 | 0.207 | 0.207 |

| p-value (combined effect = 0) | 0.001 | 0.001 | 0.001 | 0.002 | 0.001 | 0.002 | 0.001 |

| Flexible labour markets: Effects of delicensing | |||||||

| Row 5 + Row 6 | −0.013 | −0.014 | −0.013 | −0.008 | −0.008 | −0.022 | −0.002 |

| Standard Error | 0.036 | 0.036 | 0.036 | 0.036 | 0.035 | 0.038 | 0.033 |

| p-value (combined effect = 0) | 0.707 | 0.702 | 0.711 | 0.831 | 0.818 | 0.557 | 0.961 |

| Flexible labour markets: Effects of FDI reform | |||||||

| Row 7 + Row 8 | 0.093 | 0.091 | 0.058 | 0.092 | 0.092 | 0.089 | 0.094 |

| Standard Error | 0.039 | 0.039 | 0.034 | 0.039 | 0.039 | 0.040 | 0.039 |

| p-value (combined effect = 0) | 0.017 | 0.019 | 0.083 | 0.018 | 0.018 | 0.027 | 0.016 |

| State FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 160,075 | 151,784 | 154,624 | 155,381 | 154,261 | 144,998 |

| R-squared | 0.205 | 0.206 | 0.212 | 0.208 | 0.208 | 0.207 | 0.198 |

| Excluding: | |||||||

|---|---|---|---|---|---|---|---|

| Baseline (All Firms) | Bihar | Assam | West Bengal | Orissa | Madhya Pradesh | Gujarat | |

| Final goods tariffs | −0.020 | −0.016 | −0.033 | −0.064 | −0.027 | −0.036 | −0.038 |

| (0.075) | (0.080) | (0.076) | (0.087) | (0.079) | (0.081) | (0.072) | |

| Final goods tariffs * FLEX 2 | 0.132 | 0.147 | 0.154 | 0.182 | 0.137 | 0.149 | 0.117 |

| (0.115) | (0.119) | (0.115) | (0.127) | (0.118) | (0.121) | (0.119) | |

| Input tariffs | −0.680 *** | −0.754 *** | −0.685 *** | −0.690 *** | −0.653 *** | −0.643 *** | −0.591 *** |

| (0.211) | (0.216) | (0.213) | (0.225) | (0.216) | (0.223) | (0.214) | |

| Input tariffs * FLEX 2 | 0.021 | 0.018 | −0.016 | −0.005 | 0.016 | 0.038 | 0.125 |

| (0.216) | (0.221) | (0.215) | (0.228) | (0.219) | (0.223) | (0.224) | |

| Delicensing | 0.084 | 0.091 | 0.098 | 0.090 | 0.077 | 0.095 | 0.084 |

| (0.061) | (0.063) | (0.064) | (0.067) | (0.063) | (0.065) | (0.061) | |

| Delicensing * FLEX 2 | −0.098 | −0.091 | −0.117 | −0.098 | −0.088 | −0.110 | −0.107 |

| (0.083) | (0.083) | (0.084) | (0.087) | (0.084) | (0.087) | (0.088) | |

| FDI reform | −0.115 ** | −0.133 *** | −0.125 *** | −0.124 ** | −0.126 *** | −0.133 *** | −0.128 *** |

| (0.045) | (0.047) | (0.046) | (0.051) | (0.046) | (0.049) | (0.043) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.239 *** | 0.216 *** | 0.215 *** | 0.219 *** | 0.237 *** | 0.252 *** |

| (0.067) | (0.068) | (0.067) | (0.073) | (0.068) | (0.071) | (0.070) | |

| Flexible labour markets: Effects of changes in final goods tariffs | |||||||

| Row 1 + Row 2 | 0.111 | 0.130 | 0.121 | 0.118 | 0.110 | 0.113 | 0.079 |

| Standard Error | 0.063 | 0.064 | 0.063 | 0.064 | 0.063 | 0.065 | 0.071 |

| p-value (combined effect = 0) | 0.078 | 0.040 | 0.057 | 0.066 | 0.081 | 0.081 | 0.263 |

| Flexible labour markets: Effects of changes in input tariffs | |||||||

| Row 3 + Row 4 | −0.659 | −0.736 | −0.701 | −0.695 | −0.637 | −0.606 | −0.467 |

| Standard Error | 0.199 | 0.201 | 0.201 | 0.204 | 0.201 | 0.205 | 0.204 |

| p-value (combined effect = 0) | 0.001 | 0.000 | 0.000 | 0.001 | 0.002 | 0.003 | 0.023 |

| Flexible labour markets: Effects of delicensing | |||||||

| Row 5 + Row 6 | −0.013 | −0.000 | −0.018 | −0.008 | −0.011 | −0.015 | −0.023 |

| Standard Error | 0.036 | 0.035 | 0.036 | 0.036 | 0.036 | 0.036 | 0.041 |

| p-value (combined effect = 0) | 0.707 | 0.997 | 0.605 | 0.827 | 0.752 | 0.674 | 0.575 |

| Flexible labour markets: Effects of FDI reform | |||||||

| Row 7 + Row 8 | 0.093 | 0.106 | 0.091 | 0.091 | 0.094 | 0.104 | 0.125 |

| Standard Error | 0.039 | 0.038 | 0.039 | 0.039 | 0.039 | 0.039 | 0.044 |

| p-value (combined effect = 0) | 0.017 | 0.006 | 0.019 | 0.020 | 0.017 | 0.008 | 0.004 |

| State FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 156,478 | 157,852 | 153,119 | 157,954 | 154,757 | 144,400 |

| R-squared | 0.205 | 0.206 | 0.198 | 0.207 | 0.203 | 0.207 | 0.207 |

| Excluding: | ||||||

|---|---|---|---|---|---|---|

| Baseline (All Firms) | Maharashtra | Andhra Pradesh | Karnataka | Kerala | Tamil Nadu | |

| Final goods tariffs | −0.020 | −0.013 | −0.011 | −0.016 | −0.033 | −0.004 |

| (0.075) | (0.072) | (0.071) | (0.075) | (0.078) | (0.066) | |

| Final goods tariffs * FLEX 2 | 0.132 | 0.133 | 0.161 | 0.133 | 0.143 | 0.128 |

| (0.115) | (0.124) | (0.118) | (0.119) | (0.117) | (0.104) | |

| Input tariffs | −0.680 *** | −0.713 *** | −0.751 *** | −0.716 *** | −0.609 *** | −0.569 *** |

| (0.211) | (0.216) | (0.213) | (0.214) | (0.212) | (0.195) | |

| Input tariffs * FLEX 2 | 0.021 | 0.126 | 0.023 | 0.037 | −0.004 | −0.250 |

| (0.216) | (0.237) | (0.220) | (0.225) | (0.215) | (0.215) | |

| Delicensing | 0.084 | 0.077 | 0.013 | 0.098 | 0.096 | 0.084 |

| (0.061) | (0.066) | (0.050) | (0.063) | (0.062) | (0.062) | |

| Delicensing * FLEX 2 | −0.098 | −0.101 | −0.026 | −0.107 | −0.123 | −0.115 |

| (0.083) | (0.098) | (0.071) | (0.087) | (0.080) | (0.091) | |

| FDI reform | −0.115 ** | −0.089 ** | −0.113 *** | −0.110 ** | −0.084 ** | −0.096 ** |

| (0.045) | (0.043) | (0.042) | (0.044) | (0.042) | (0.044) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.218 *** | 0.185 *** | 0.204 *** | 0.161 ** | 0.162 ** |

| (0.067) | (0.072) | (0.067) | (0.068) | (0.064) | (0.067) | |

| Flexible labour markets: Effects of changes in final goods tariffs | ||||||

| Row 1 + Row 2 | 0.111 | 0.120 | 0.149 | 0.117 | 0.110 | 0.124 |

| Standard Error | 0.063 | 0.077 | 0.068 | 0.068 | 0.063 | 0.067 |

| p-value (combined effect = 0) | 0.078 | 0.119 | 0.028 | 0.085 | 0.081 | 0.065 |

| Flexible labour markets: Effects of changes in input tariffs | ||||||

| Row 3 + Row 4 | −0.659 | −0.587 | −0.728 | −0.679 | −0.613 | −0.819 |

| Standard Error | 0.199 | 0.221 | 0.208 | 0.209 | 0.192 | 0.227 |

| p-value (combined effect = 0) | 0.001 | 0.008 | 0.000 | 0.001 | 0.001 | 0.000 |

| Flexible labour markets: Effects of delicensing | ||||||

| Row 5 + Row 6 | −0.013 | −0.025 | −0.012 | −0.010 | −0.028 | −0.031 |

| Standard Error | 0.036 | 0.045 | 0.036 | 0.038 | 0.034 | 0.045 |

| p-value (combined effect = 0) | 0.707 | 0.583 | 0.730 | 0.803 | 0.423 | 0.494 |

| Flexible labour markets: Effects of FDI reform | ||||||

| Row 7 + Row 8 | 0.093 | 0.129 | 0.072 | 0.095 | 0.077 | 0.066 |

| Standard Error | 0.039 | 0.047 | 0.041 | 0.040 | 0.039 | 0.045 |

| p-value (combined effect = 0) | 0.017 | 0.006 | 0.082 | 0.020 | 0.048 | 0.142 |

| State FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 138,989 | 146,228 | 151,390 | 153,984 | 137,854 |

| R-squared | 0.205 | 0.213 | 0.210 | 0.206 | 0.204 | 0.209 |

| Baseline (All Firms) | Firms in Industries with CR8 above Median in 1990 (Less Competitive) | Firms in Industries with CR8 below Median in 1990 (More Competitive) | Firms in Industries with HHI Above Median in 1990 (Less Competitive) | Firms in Industries with HHI below Median in 1990 (More Competitive) | |

|---|---|---|---|---|---|

| Final goods tariffs | −0.020 | 0.193 ** | −0.115 | 0.231 ** | −0.054 |

| (0.075) | (0.076) | (0.099) | (0.109) | (0.083) | |

| Final goods tariffs * FLEX 2 | 0.132 | −0.114 | 0.257 * | −0.135 | 0.156 |

| (0.115) | (0.077) | (0.155) | (0.127) | (0.127) | |

| Input tariffs | −0.680 *** | −0.892 ** | −0.530 ** | −0.942 ** | −0.621 *** |

| (0.211) | (0.441) | (0.247) | (0.438) | (0.231) | |

| Input tariffs * FLEX 2 | 0.021 | 0.842 *** | −0.160 | 0.868 ** | −0.018 |

| (0.216) | (0.277) | (0.273) | (0.341) | (0.236) | |

| Delicensing | 0.084 | −0.068 | 0.093 | −0.061 | 0.094 |

| (0.061) | (0.065) | (0.069) | (0.064) | (0.071) | |

| Delicensing * FLEX 2 | −0.098 | 0.236 *** | −0.128 | 0.215 *** | −0.132 |

| (0.083) | (0.073) | (0.095) | (0.073) | (0.097) | |

| FDI reform | −0.115 ** | −0.089 | −0.120 ** | −0.093 | −0.125 ** |

| (0.045) | (0.069) | (0.049) | (0.067) | (0.050) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.174 * | 0.219 *** | 0.186 ** | 0.224 *** |

| (0.067) | (0.095) | (0.071) | (0.093) | (0.073) | |

| Flexible labour markets: Effects of changes in final goods tariffs | |||||

| Row 1 + Row 2 | 0.111 * | 0.079 | 0.142 | 0.096 | 0.102 |

| Standard Error | 0.063 | 0.086 | 0.082 | 0.113 | 0.070 |

| p-value (combined effect = 0) | 0.078 | 0.361 | 0.084 | 0.398 | 0.145 |

| Flexible labour markets: Effects of changes in input tariffs | |||||

| Row 3 + Row 4 | −0.659 *** | −0.050 | −0.690 | −0.075 | −0.639 |

| Standard Error | 0.199 | 0.431 | 0.233 | 0.411 | 0.225 |

| p-value (combined effect = 0) | 0.001 | 0.908 | 0.003 | 0.856 | 0.005 |

| Flexible labour markets: Effects of delicensing | |||||

| Row 5 + Row 6 | −0.013 | 0.168 | −0.036 | 0.154 | −0.037 |

| Standard Error | 0.036 | 0.057 | 0.041 | 0.056 | 0.042 |

| p-value (combined effect = 0) | 0.707 | 0.003 | 0.384 | 0.006 | 0.371 |

| Flexible labour markets: Effects of FDI reform | |||||

| Row 7 + Row 8 | 0.093 ** | 0.085 | 0.098 | 0.093 | 0.100 |

| Standard Error | 0.039 | 0.075 | 0.043 | 0.073 | 0.043 |

| p-value (combined effect = 0) | 0.017 | 0.260 | 0.021 | 0.200 | 0.020 |

| State FE | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 23,709 | 137,174 | 24,376 | 136,507 |

| R-squared | 0.205 | 0.217 | 0.205 | 0.204 | 0.207 |

| A: All States | Dependent Variable: ln (Number of Formal Firms in Three-Digit Industry) | ||||

|---|---|---|---|---|---|

| All Industries | Industries with CR8 above Median in 1990 (Less Competitive) | Industries with CR8 below Median in 1990 (More Competitive) | Industries with HHI above Median in 1990 (Less Competitive) | Industries with HHI below Median in 1990 (More Competitive) | |

| Final goods tariffs | −0.057 | 0.026 | −0.060 | 0.091 | −0.064 |

| (0.045) | (0.066) | (0.057) | (0.076) | (0.055) | |

| Input tariffs | 0.151 | −0.881 * | 0.201 | −0.884 * | 0.204 |

| (0.249) | (0.481) | (0.294) | (0.466) | (0.296) | |

| Delicensing | 0.079 ** | −0.011 | 0.096 ** | −0.041 | 0.096 ** |

| (0.036) | (0.069) | (0.044) | (0.076) | (0.045) | |

| FDI reform | 0.019 | 0.016 | 0.018 | 0.026 | 0.018 |

| (0.034) | (0.057) | (0.038) | (0.057) | (0.038) | |

| Observations | 556 | 256 | 300 | 260 | 296 |

| R-squared | 0.379 | 0.159 | 0.458 | 0.174 | 0.457 |

| B: States with flexible labour markets (FLEX 2 = 1) | |||||

| Final goods tariffs | −0.068 | −0.088 | −0.045 | −0.027 | −0.053 |

| (0.059) | (0.073) | (0.072) | (0.081) | (0.070) | |

| Input tariffs | 0.003 | −0.845 | −0.059 | −0.862 * | −0.058 |

| (0.300) | (0.537) | (0.368) | (0.509) | (0.367) | |

| Delicensing | 0.086 ** | −0.010 | 0.110 ** | −0.036 | 0.113 ** |

| (0.042) | (0.079) | (0.052) | (0.084) | (0.052) | |

| FDI reform | −0.005 | −0.027 | −0.011 | −0.021 | −0.011 |

| (0.036) | (0.079) | (0.041) | (0.077) | (0.042) | |

| Observations | 520 | 228 | 292 | 232 | 288 |

| R-squared | 0.386 | 0.156 | 0.466 | 0.147 | 0.471 |

| C: States with inflexible labour markets (FLEX 2 = 0) | |||||

| Final goods tariffs | −0.041 | 0.131 | −0.064 | 0.158 | −0.062 |

| (0.052) | (0.085) | (0.064) | (0.129) | (0.061) | |

| Input tariffs | 0.271 | −0.682 | 0.362 | −0.684 | 0.362 |

| (0.291) | (0.535) | (0.325) | (0.576) | (0.325) | |

| Delicensing | 0.045 | −0.005 | 0.055 | −0.011 | 0.050 |

| (0.037) | (0.084) | (0.042) | (0.099) | (0.042) | |

| FDI reform | 0.052 | 0.133 * | 0.045 | 0.133 * | 0.045 |

| (0.038) | (0.072) | (0.041) | (0.077) | (0.041) | |

| Observations | 484 | 188 | 296 | 192 | 292 |

| R-squared | 0.169 | 0.101 | 0.221 | 0.111 | 0.215 |

References

- Aghion, Philippe, Robin Burgess, Stephen J. Redding, and Fabrizio Zilibotti. 2008. The Unequal Effects of Liberalization: Evidence from Dismantling the License Raj in India. American Economic Review 98: 1397–412. [Google Scholar] [CrossRef]

- Ahsan, Reshad. 2013. Input Tariffs, Speed of Contract Enforcement, and the Productivity of Firms in India. Journal of International Economics 90: 181–92. [Google Scholar] [CrossRef]

- Ahsan, Ahmed, and Carmen Pagés. 2009. Are All Labor Regulations Equal? Evidence from Indian Manufacturing. Journal of Comparative Economics 37: 62–75. [Google Scholar] [CrossRef]

- Alessandrini, Michele, Bassam Fattouh, Benno Ferrarini, and Pasquale Scaramozzino. 2011. Tariff Liberalization and Trade Specialization: Lessons from India. Journal of Comparative Economics 39: 499–513. [Google Scholar] [CrossRef]

- Amirapu, Amrit, and Michael Gechter. 2017. Labor Regulations and the Cost of Corruption: Evidence from the Indian Firm Size Distribution. IED Working Paper No. 266. The Review of Economics and Statistics. accepted. [Google Scholar]

- Amiti, Mary, and Jozef Konings. 2007. Trade Liberalization, Intermediate Inputs, and Productivity: Evidence from Indonesia. American Economic Review 97: 1611–38. [Google Scholar] [CrossRef]

- Anant, T. C. A., Rana Hasan, Prabhu Mohapatra, Rayaprolu Nagaraj, and S. K. Sasikumar. 2006. Labor Markets in India: Issues and Perspectives. In Labor Markets in Asia: Issues and Perspectives. London: Palgrave Macmillan, pp. 205–300. [Google Scholar]

- Besley, Tim, and Robin Burgess. 2004. Can Labor Regulation Hinder Economic Performance? Evidence from India. The Quarterly Journal of Economics 119: 91–134. [Google Scholar] [CrossRef]

- Bhattacharjea, Aditya. 2006. Labour Market Regulation and Industrial Performance in India: A Critical Review of the Empirical Evidence. Indian Journal of Labour Economics 49: 211–32. [Google Scholar]

- Bosch, Mariano, Edwin Goni, and William Maloney. 2007. The Determinants of Rising Informality in Brazil: Evidence from Gross Worker Flows. Policy Research Working Papers. The World Bank. Available online: http://elibrary.worldbank.org/doi/book/10.1596/1813-9450-4375 (accessed on 4 April 2019).

- Botero, Juan C., Simeon Djankov, Rafael La Porta, Florencio Lopez-de-Silanes, and Andrei Shleifer. 2004. The Regulation of Labor. The Quarterly Journal of Economics 119: 1339–82. [Google Scholar] [CrossRef]

- Bown, Chad P., and Patricia Tovar. 2011. Trade Liberalization, Antidumping, and Safeguards: Evidence from India’s Tariff Reform. Journal of Development Economics 96: 115–25. [Google Scholar] [CrossRef]

- De Loecker, Jan, Pinelopi K. Goldberg, Amit K. Khandelwal, and Nina Pavcnik. 2016. Prices, Markups, and Trade Reform. Econometrica 84: 445–510. [Google Scholar] [CrossRef]

- Dougherty, Sean. 2009. Labour Regulation and Employment Dynamics at the State Level in India. Review of Market Integration 1: 295–337. [Google Scholar] [CrossRef]

- Dyson, Tim, Robert Cassen, and Leela Visaria. 2004. Twenty-First Century India: Population, Economy, Human Development, and the Environment. Oxford: Oxford University Press. [Google Scholar]

- Goldberg, Pinelopi K., and Nina Pavcnik. 2003. The response of the informal sector to trade liberalization. Journal of Development Economics 72: 463–96. [Google Scholar] [CrossRef]

- Goldberg, Pinelopi, Amit K. Khandelwal, Nina Pavcnik, and Petia Topalova. 2010. Imported Intermediate Inputs and Domestic Product Growth: Evidence from India. The Quarterly Journal of Economics 125: 1727–67. [Google Scholar] [CrossRef]

- Groizard, Jose L., Priya Ranjan, and Antonio Rodriguez-Lopez. 2015. Trade Costs and Job Flows: Evidence from Establishment-Level Data. Economic Inquiry 53: 173–204. [Google Scholar] [CrossRef]

- Gupta, Poonam, Rana Hasan, and Utsav Kumar. 2009. Big Reforms but Small Payoffs: Explaining the Weak Record of Growth and Employment in Indian Manufacturing. India Policy Forum 5: 59–123. [Google Scholar] [CrossRef]

- Haltiwanger, John, Ron S. Jarmin, and Javier Miranda. 2013. Who Creates Jobs? Small versus Large versus Young. Review of Economics and Statistics 95: 347–61. [Google Scholar] [CrossRef]

- Harrison, Ann E., Leslie A. Martin, and Shanthi Nataraj. 2013. Learning versus Stealing: How Important Are Market-Share Reallocations to India’s Productivity Growth? The World Bank Economic Review 27: 202–28. [Google Scholar] [CrossRef]

- Hasan, Rana, Devashish Mitra, Priya Ranjan, and Reshad N. Ahsan. 2012. Trade Liberalization and Unemployment: Theory and Evidence from India. Journal of Development Economics 97: 269–80. [Google Scholar] [CrossRef]

- Javorcik, Beata. 2015. Does FDI Bring Good Jobs to Host Countries? World Bank Research Observer 30: 74–94. [Google Scholar] [CrossRef]

- Kambhampati, Uma, and Ashok Parikh. 2005. Has liberalization affected profit margins in Indian Industry? Bulletin of Economic Research 57: 273–304. [Google Scholar] [CrossRef]

- Kambhampati, Uma, Pravin Krishna, and Devashish Mitra. 1997. The effect of trade policy reforms on labour markets: Evidence from India. Journal of International Trade & Economic Development 6: 287–97. [Google Scholar] [CrossRef]

- Kis-Katos, Krisztina, and Robert Sparrow. 2015. Poverty, Labour Markets and Trade Liberalization in Indonesia. Journal of Development Economics 117: 94–106. [Google Scholar] [CrossRef]

- Martin, Lesley A., Shanthi Nataraj, and Ann E. Harrison. 2017. In with the Big, Out with the Small: Removing Small-Scale Reservations in India. American Economic Review 107: 354–86. [Google Scholar] [CrossRef]

- Melitz, Marc J. 2003. The Impact of Trade on Intra-Industry Reallocations and Aggregate Industry Productivity. Econometrica 71: 1695–725. [Google Scholar] [CrossRef]

- Menezes-Filho, Naércio Aquino, and Marc-Andreas Muendler. 2011. Labor Reallocation in Response to Trade Reform. NBER Working Paper 17372. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Munshi, Kaivan, and Mark Rosenzweig. 2009. Why Is Mobility in India so Low? Social Insurance, Inequality, and Growth. Working Paper 14850. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Nataraj, Shanthi. 2011. The Impact of Trade Liberalization on Productivity: Evidence from India’s Formal and Informal Manufacturing Sectors. Journal of International Economics 85: 292–301. [Google Scholar] [CrossRef]

- Nouroz, Hasheem. 2001. Protection in Indian Manufacturing: An Empirical Study. Delhi: Macmillan India. [Google Scholar]

- Nunn, Nathan, and Daniel Trefler. 2014. Domestic Institutions as a Source of Comparative Advantage. Handbook of International Economics 4: 263–315. [Google Scholar] [CrossRef]

- Organization for Economic Co-operation and Development (OECD). 2007. OECD Economic Surveys: India. 2007–2014. Paris: Organization for Economic Co-operation and Development. [Google Scholar]

- Organization for Economic Co-operation and Development (OECD). 2012. Trade and Employment in a Fast-Changing World. In Policy Priorities for International Trade and Jobs. A product of the International Collaboration Initiative for Trade and Employment (ICITE). Paris: OECD. [Google Scholar]

- Paunov, Caroline. 2011. Imports, Innovation and Employment after Crisis. OECD Science, Technology and Industry Working Paper 2011/05. Paris: OECD. [Google Scholar]

- Saha, Bibhas, Kunal Sen, and Dibyendu Maiti. 2013. Trade Openness, Labour Institutions and Flexibilisation: Theory and Evidence from India. Labour Economics 24: 180–95. [Google Scholar] [CrossRef]

- Sen, Kunal. 2008. Trade Policy and Wage Inequality: Evidence from Indian Manufacturing. Indian Growth and Development Review 1: 147–71. [Google Scholar] [CrossRef]

- Sharma, Gunjan. 2008. Competing or Collaborating Siblings? Industrial and Trade Policies in India. Working Paper 06-10. Columbia: University of Missouri-Columbia. [Google Scholar]

- Sharma, Shruti. 2013. Imported Intermediate Inputs and Workforce Composition: Evidence from India’s Tariff Liberalization. Economics Program Working Papers 13-03. Hong Kong, China: The Conference Board, Economics Program. [Google Scholar]

- Sivadasan, Jagadeesh. 2009. Barriers to Competition and Productivity: Evidence from India. The B.E. Journal of Economic Analysis & Policy 9. [Google Scholar] [CrossRef]

- Topalova, Petia. 2010. Factor Immobility and Regional Impacts of Trade Liberalization: Evidence on Poverty from India. American Economic Journal: Applied Economics 2: 1–41. [Google Scholar] [CrossRef]

- Topalova, Petia, and Amit K. Khandelwal. 2011. Trade Liberalization and Firm Productivity: The Case of India. Review of Economics and Statistics 93: 995–1009. [Google Scholar] [CrossRef]

- World Bank. 2005. Improving the Investment Climate in India. Washington: The World Bank. [Google Scholar]

| 1 | Up to the 1980s, all manufacturing firms with over 50 employees (over 100 employees if electricity was not used) and with assets above a specified threshold were required to obtain a license from the government. This policy was extremely restrictive and discouraged industry entry and competition (Sharma 2008). In this context, the term ‘delicensing’ implies that firms in a given industry or industries were no longer required to obtain such a license. |

| 2 | Prior to 1991, most industries were characterised by a 40 per cent FDI ceiling. In 1991 and in the following years, this ceiling was raised to 51 per cent for a number of industries, with ‘automatic’ FDI approval, and other regulations concerning FDI were liberalised (Sivadasan 2009). |

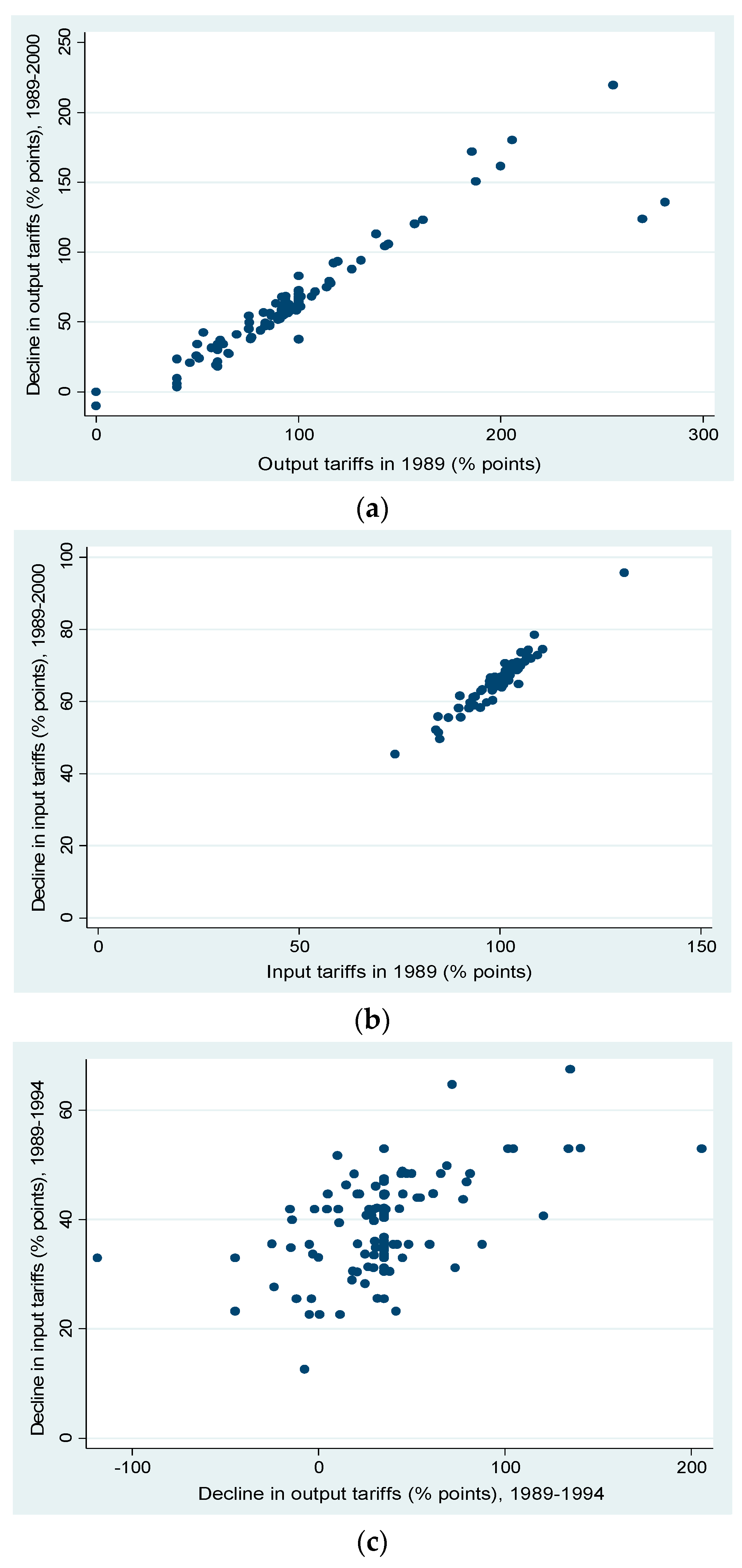

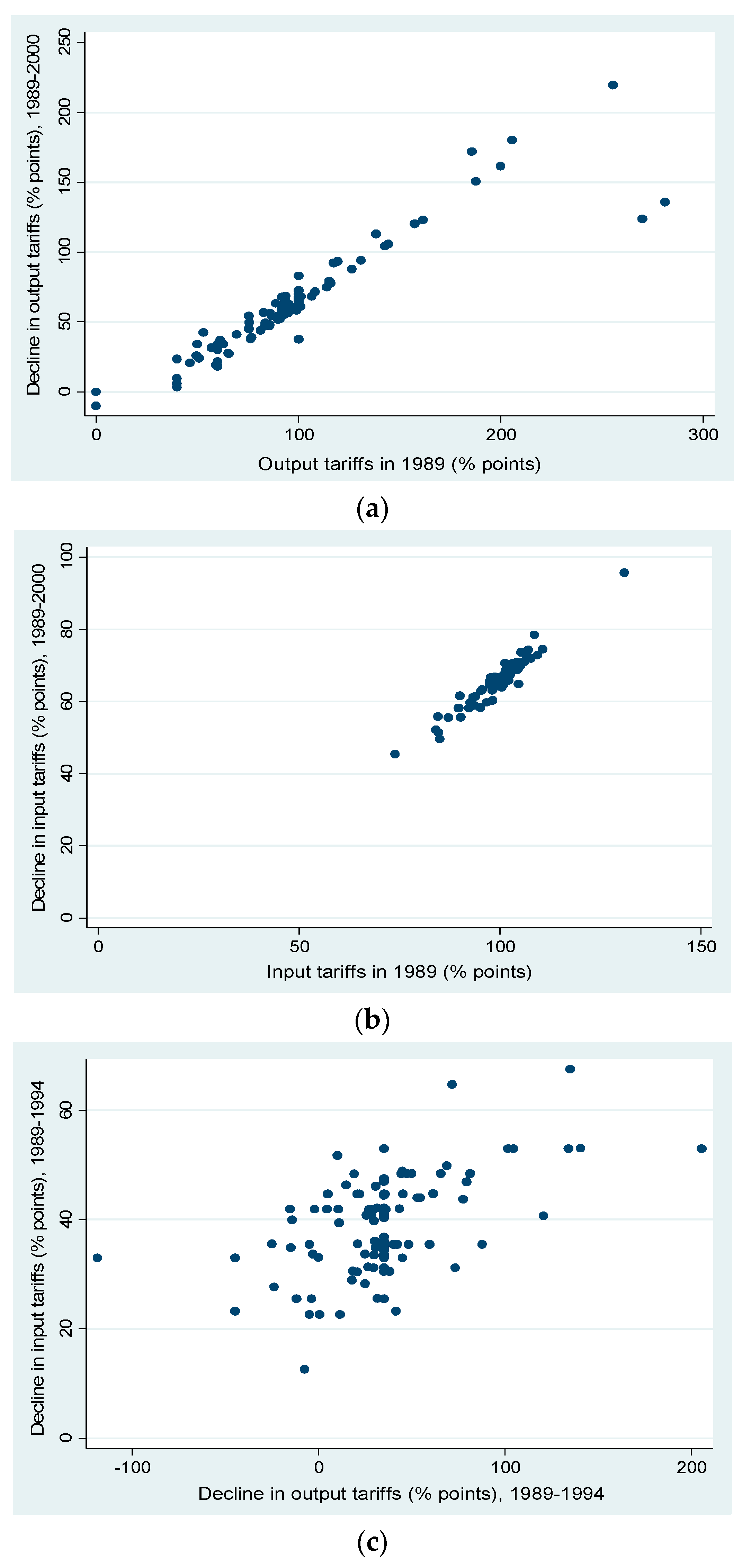

| 3 | This was purposefully undertaken in the case of final goods tariffs, with input tariffs undergoing related, albeit not equivalent, declines. |

| 4 | The correlation coefficient for the changes in output and input tariffs over the 1989–1994 period is 0.5776, while that for the corresponding changes over the 1989–2000 period is 0.5927. |

| 5 | The two outliers visible to the right of this graph are the wine manufacturing and spirit distillation, rectification and blending industries, the tariffs for which amounted to over 250 per cent in 1989, but were subjected to smaller reductions relative to other industries with very high tariff rates in 1989. A robustness check which omits these outliers from the baseline regressions (outlined in Section 4) is discussed in Section 6. |

| 6 | Besley and Burgess (2004) consider sixteen states in their analysis, but the state of Jammu and Kashmir made no amendment to the IDA in the 1958–1990 period. |

| 7 | The Besley–Burgess measure, with a minor correction incorporated for the state of Madhya Pradesh, is labelled ‘FLEX 1’ by Hasan et al. (2012). |

| 8 | In their online appendix, Hasan et al. (2012) provide additional detail in this regard. Gujarat and Maharashtra are typically considered to be prime business locations by Indian businessmen, whereas Kerala is not. The World Bank’s 2005 research presents firm level survey findings in which managers rank Maharashtra and Gujarat highly, labelling them to be ‘Best Investment Climate’ states more consistently than other states. Kerala, conversely, attains a ‘Poor Investment Climate’ ranking. Small and medium-sized firms report having been subjected to twice as many factory inspections in ‘Poor Investment Climate’ states as in ‘Best Investment Climate’ states, suggesting that enforcement of ostensibly ‘pro-worker’ amendments to the IDA is likely to be less stringent in the latter type of state. Further, firms perceive that ‘over-manning’ (the gap between optimal and actual employment levels given current output levels) is on average less visible in Maharashtra and Gujarat than elsewhere. In ‘Poor Investment Climate’ states (such as Kerala), restrictive labour regulations were considered to be a primary driver of ‘over-manning’, whereas in ‘Best Investment Climate’ states, ‘over-manning’ (lower than in other states in the first place) was perceived more favourably, in the sense that it was considered to occur when firms expected higher future growth. |

| 9 | |

| 10 |

| Year | FINAL GOODS TARIFFS (%) | INPUT TARIFFS (%) | % DEL | % FDI | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Median | Max | Min | SD | Mean | Median | Max | Min | SD | |||

| 1985 | 88.97 | 91.93 | 203.91 | 0.00 | 32.83 | 57.89 | 58.09 | 86.82 | 23.42 | 11.73 | 35 | 0 |

| 1986 | 95.37 | 100.00 | 242.22 | 0.00 | 37.95 | 60.29 | 59.77 | 88.30 | 23.97 | 11.23 | 36 | 0 |

| 1987 | 94.75 | 100.00 | 242.22 | 0.00 | 37.60 | 58.63 | 58.16 | 79.50 | 23.67 | 10.25 | 36 | 0 |

| 1988 | 94.86 | 100.00 | 248.89 | 0.00 | 37.53 | 59.33 | 58.92 | 83.09 | 23.89 | 10.55 | 36 | 0 |

| 1989 | 95.54 | 100.00 | 281.25 | 0.00 | 40.34 | 59.44 | 59.05 | 83.11 | 23.89 | 10.58 | 37 | 0 |

| 1990 | 95.68 | 100.00 | 281.25 | 0.00 | 40.56 | 59.45 | 58.99 | 83.22 | 23.90 | 10.57 | 37 | 0 |

| 1991 | 95.68 | 100.00 | 281.25 | 0.00 | 40.56 | 59.44 | 58.99 | 83.22 | 23.90 | 10.57 | 84 | 38 |

| 1992 | 63.48 | 64.65 | 281.25 | 0.00 | 27.71 | 39.73 | 40.25 | 53.27 | 20.54 | 5.42 | 84 | 38 |

| 1993 | 63.92 | 64.15 | 340.63 | 22.50 | 31.03 | 38.53 | 39.70 | 54.35 | 20.42 | 5.31 | 86 | 38 |

| 1994 | 64.46 | 65.00 | 400.00 | 11.28 | 36.06 | 37.34 | 37.97 | 55.42 | 8.92 | 6.06 | 86 | 38 |

| 1995 | 53.57 | 53.50 | 320.75 | 12.08 | 30.86 | 30.11 | 30.83 | 48.97 | 8.64 | 5.32 | 86 | 38 |

| 1996 | 42.41 | 44.25 | 254.27 | 0.00 | 24.85 | 22.76 | 23.39 | 42.51 | 8.15 | 5.15 | 86 | 38 |

| 1997 | 34.15 | 34.48 | 176.67 | 0.00 | 18.59 | 18.37 | 19.31 | 32.95 | 6.37 | 4.09 | 89 | 45 |

| State | Measure of Labour Market Flexibility * | ||

|---|---|---|---|

| FLEX 1 | FLEX 2 | FLEX 3 | |

| Andhra Pradesh | 1 | 1 | 1 |

| Assam | 0 | 0 | 0 |

| Bihar | 0 | 0 | 0 |

| Gujarat | 0 | 1 | 0 |

| Haryana | 0 | 0 | 0 |

| Karnataka | 1 | 1 | 1 |

| Kerala | 1 | 0 | 0 |

| Madhya Pradesh | 0 | 0 | 0 |

| Maharashtra | 0 | 1 | 0 |

| Orissa | 0 | 0 | 0 |

| Punjab | 0 | 0 | 0 |

| Rajasthan | 1 | 1 | 1 |

| Tamil Nadu | 1 | 1 | 1 |

| Uttar Pradesh | 0 | 0 | 1 |

| West Bengal | 0 | 0 | 0 |

| Year | Observations | Mean | Median | Standard Deviation | Minimum | Maximum | Weighted Total ** |

|---|---|---|---|---|---|---|---|

| All states | |||||||

| 1990 | 41,463 | 116.50 | 24.00 | 407.02 | 1 | 7479 | 4,830,441 |

| 1994 | 47,576 | 116.81 | 25.67 | 387.67 | 1 | 7619 | 5,557,393 |

| 1995 | 48,435 | 114.71 | 25.00 | 369.14 | 1 | 6715 | 5,556,124 |

| 1997 | 48,724 | 116.52 | 26.00 | 357.97 | 1 | 6192 | 5,677,288 |

| Overall | 186,198 | 115.12 | 25.00 | 379.83 | 1 | 7619 | 21,621,246 |

| States with flexible labour markets (FLEX 2 = 1) | |||||||

| 1990 | 23,109 | 114.45 | 23.00 | 386.95 | 1 | 7282 | 2,644,720 |

| 1994 | 27,325 | 113.21 | 25.00 | 367.54 | 1 | 6869 | 3,093,462 |

| 1995 | 27,830 | 110.80 | 25.00 | 347.13 | 1 | 6125 | 3,083,672 |

| 1997 | 28,312 | 113.49 | 26.00 | 341.98 | 1 | 6192 | 3,213,061 |

| Overall | 106,576 | 112.92 | 25.00 | 360.04 | 1 | 7282 | 12,034,915 |

| States with inflexible labour markets (FLEX 2 = 0) | |||||||

| 1990 | 18,354 | 119.09 | 25.00 | 430.96 | 1 | 7479 | 2,185,721 |

| 1994 | 20,251 | 121.67 | 27.00 | 413.25 | 1 | 7619 | 2,463,931 |

| 1995 | 20,605 | 119.99 | 26.00 | 396.88 | 1 | 6715 | 2,472,451 |

| 1997 | 20,412 | 120.72 | 27.00 | 379.01 | 1 | 5975 | 2,464,228 |

| Overall | 79,622 | 120.40 | 26.00 | 404.76 | 1 | 7619 | 9,586,331 |

| Dependent Variable: Paid Employment | Dependent Variable: Total Employment | |||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Final goods tariffs | 0.063 * | 0.055 | 0.061 * | 0.061 * | 0.052 | 0.059 * |

| (0.035) | (0.036) | (0.036) | (0.033) | (0.034) | (0.034) | |

| Input tariffs | −0.753 *** | −0.706 *** | −0.737 *** | −0.675 *** | −0.619 *** | −0.653 *** |

| (0.168) | (0.170) | (0.174) | (0.162) | (0.163) | (0.167) | |

| Delicensing | 0.019 | 0.020 | 0.021 | 0.023 | ||

| (0.023) | (0.024) | (0.022) | (0.023) | |||

| FDI reform | 0.005 | 0.009 | 0.007 | 0.012 | ||

| (0.024) | (0.025) | (0.023) | (0.024) | |||

| State FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 160,883 | 160,883 | 160,984 | 160,984 | 160,984 |

| R-squared | 0.204 | 0.204 | 0.204 | 0.203 | 0.203 | 0.203 |

| Dependent Variable: Paid Employment | Dependent Variable: Total Employment | |||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Row 1 + Row 2 | 0.124 * | 0.124 | 0.111 * | 0.115 * | 0.116 | 0.103 * |

| Final goods tariffs | −0.030 | −0.037 | −0.020 | −0.023 | −0.031 | −0.014 |

| (0.078) | (0.078) | (0.075) | (0.073) | (0.074) | (0.070) | |

| Final goods tariffs * FLEX 2 | 0.154 | 0.161 | 0.132 | 0.138 | 0.147 | 0.117 |

| (0.122) | (0.122) | (0.115) | (0.114) | (0.115) | (0.108) | |

| Input tariffs | −0.609 *** | −0.729 *** | −0.680 *** | −0.531 ** | −0.646 *** | −0.597 *** |

| (0.214) | (0.202) | (0.211) | (0.207) | (0.195) | (0.205) | |

| Input tariffs * FLEX 2 | −0.182 | 0.044 | 0.021 | −0.170 | 0.041 | 0.018 |

| (0.228) | (0.211) | (0.216) | (0.218) | (0.204) | (0.209) | |

| Delicensing | 0.046 | 0.021 | 0.084 | 0.054 | 0.024 | 0.089 |

| (0.059) | (0.024) | (0.061) | (0.057) | (0.023) | (0.059) | |

| Delicensing * FLEX 2 | −0.040 | −0.098 | −0.047 | −0.101 | ||

| (0.081) | (0.083) | (0.080) | (0.081) | |||

| FDI reform | 0.010 | −0.105 ** | −0.115 ** | 0.013 | −0.092 ** | −0.103 ** |

| (0.026) | (0.045) | (0.045) | (0.025) | (0.043) | (0.043) | |

| FDI reform * FLEX 2 | 0.191 *** | 0.208 *** | 0.174 *** | 0.192 *** | ||

| (0.066) | (0.067) | (0.063) | (0.063) | |||

| Flexible labour markets: Effects of changes in final goods tariffs | ||||||

| Standard Error | 0.066 | 0.066 | 0.063 | 0.062 | 0.062 | 0.059 |

| p-value (combined effect = 0) | 0.061 | 0.059 | 0.078 | 0.065 | 0.060 | 0.082 |

| Flexible labour markets: Effects of changes in input tariffs | ||||||

| Row 3 + Row 4 | −0.791 *** | −0.684 *** | −0.659 *** | −0.701 *** | −0.605 *** | −0.579 *** |

| Standard Error | 0.209 | 0.202 | 0.199 | 0.199 | 0.192 | 0.190 |

| p-value (combined effect = 0) | 0.000 | 0.001 | 0.001 | 0.000 | 0.002 | 0.002 |

| Flexible labour markets: Effects of delicensing | ||||||

| Row 5 + Row 6 | 0.007 | −0.013 | 0.007 | −0.012 | ||

| Standard Error | 0.037 | 0.036 | 0.036 | 0.036 | ||

| p-value (combined effect = 0) | 0.854 | 0.707 | 0.854 | 0.737 | ||

| Flexible labour markets: Effects of FDI reform | ||||||

| Row 7 + Row 8 | 0.086 ** | 0.093 ** | 0.082 ** | 0.089 ** | ||

| Standard Error | 0.038 | 0.039 | 0.036 | 0.037 | ||

| p-value (combined effect = 0) | 0.022 | 0.017 | 0.022 | 0.016 | ||

| State FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 160,883 | 160,883 | 160,984 | 160,984 | 160,984 |

| R-squared | 0.204 | 0.205 | 0.205 | 0.203 | 0.204 | 0.205 |

| A: All States | Dependent Variable (in Natural Logarithms): | ||

|---|---|---|---|

| Paid Employment | Total Employment | Number of Firms | |

| (1) | (2) | (3) | |

| Final goods tariffs | 0.042 | 0.039 | −0.057 |

| (0.061) | (0.059) | (0.045) | |

| Input tariffs | −0.544 | −0.518 | 0.151 |

| (0.363) | (0.357) | (0.249) | |

| Delicensing | 0.052 | 0.056 | 0.079 ** |

| (0.046) | (0.046) | (0.036) | |

| FDI reform | 0.026 | 0.017 | 0.019 |

| (0.045) | (0.045) | (0.034) | |

| Observations | 556 | 556 | 556 |

| R-squared | 0.240 | 0.215 | 0.379 |

| B: States with flexible labour markets (FLEX 2 = 1) | |||

| Final goods tariffs | −0.026 | −0.043 | −0.068 |

| (0.118) | (0.115) | (0.059) | |

| Input tariffs | −0.610 | −0.551 | 0.003 |

| (0.441) | (0.431) | (0.300) | |

| Delicensing | 0.068 | 0.069 | 0.086 ** |

| (0.073) | (0.072) | (0.042) | |

| FDI reform | 0.012 | 0.004 | −0.005 |

| (0.058) | (0.056) | (0.036) | |

| Observations | 520 | 520 | 520 |

| R-squared | 0.234 | 0.213 | 0.386 |

| C: States with inflexible labour markets (FLEX 2 = 0) | |||

| Final goods tariffs | 0.100 * | 0.113 * | −0.041 |

| (0.057) | (0.060) | (0.052) | |

| Input tariffs | −0.363 | −0.364 | 0.271 |

| (0.412) | (0.406) | (0.291) | |

| Delicensing | 0.022 | 0.029 | 0.045 |

| (0.057) | (0.057) | (0.037) | |

| FDI reform | 0.035 | 0.024 | 0.052 |

| (0.056) | (0.057) | (0.038) | |

| Observations | 484 | 484 | 484 |

| R-squared | 0.116 | 0.098 | 0.169 |

| Baseline (All Firms) | Firms Producing at Least One SSI Reserved Item (Less Competitive) | Firms Producing (Only) Items that Were Never SSI Reserved (More Competitive) | |

|---|---|---|---|

| Final goods tariffs | −0.020 | −0.373 ** | 0.089 |

| (0.075) | (0.179) | (0.055) | |

| Final goods tariffs * FLEX 2 | 0.132 | 0.677 ** | −0.037 |

| (0.115) | (0.321) | (0.077) | |

| Input tariffs | −0.680 *** | −0.131 | −0.698 *** |

| (0.211) | (0.401) | (0.221) | |

| Input tariffs * FLEX 2 | 0.021 | −0.759 | 0.198 |

| (0.216) | (0.486) | (0.236) | |

| Delicensing | 0.084 | 0.127 * | 0.067 |

| (0.061) | (0.070) | (0.062) | |

| Delicensing * FLEX 2 | −0.098 | −0.087 | −0.129 |

| (0.083) | (0.088) | (0.091) | |

| FDI reform | −0.115 ** | −0.022 | −0.098 ** |

| (0.045) | (0.068) | (0.039) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.094 | 0.164 *** |

| (0.067) | (0.081) | (0.054) | |

| Flexible labour markets: Effects of changes in final goods tariffs | |||

| Row 1 + Row 2 | 0.111 * | 0.305 | 0.052 |

| Standard Error | 0.063 | 0.183 | 0.057 |

| p-value (combined effect = 0) | 0.078 | 0.096 | 0.362 |

| Flexible labour markets: Effects of changes in input tariffs | |||

| Row 3 + Row 4 | −0.659 *** | −0.891 | −0.500 |

| Standard Error | 0.199 | 0.406 | 0.215 |

| p-value (combined effect = 0) | 0.001 | 0.029 | 0.020 |

| Flexible labour markets: Effects of delicensing | |||

| Row 5 + Row 6 | −0.013 | 0.040 | −0.063 |

| Standard Error | 0.036 | 0.062 | 0.043 |

| p-value (combined effect = 0) | 0.707 | 0.516 | 0.143 |

| Flexible labour markets: Effects of FDI reform | |||

| Row 7 + Row 8 | 0.093 ** | 0.072 | 0.066 |

| Standard Error | 0.039 | 0.057 | 0.036 |

| p-value (combined effect = 0) | 0.017 | 0.205 | 0.071 |

| State FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Observations | 160,883 | 41,529 | 94,764 |

| R-squared | 0.205 | 0.171 | 0.235 |

| Baseline (All Firms) | Firms in Industries with CR4 above Median in 1990 (Less Competitive) | Firms in Industries with CR4 below Median in 1990 (More Competitive) | |

|---|---|---|---|

| Final goods tariffs | −0.020 | 0.226 ** | −0.053 |

| (0.075) | (0.110) | (0.083) | |

| Final goods tariffs * FLEX 2 | 0.132 | −0.136 | 0.157 |

| (0.115) | (0.127) | (0.127) | |

| Input tariffs | −0.680 *** | −0.915 ** | −0.626 *** |

| (0.211) | (0.450) | (0.230) | |

| Input tariffs * FLEX 2 | 0.021 | 0.877 ** | −0.021 |

| (0.216) | (0.346) | (0.236) | |

| Delicensing | 0.084 | −0.057 | 0.093 |

| (0.061) | (0.065) | (0.071) | |

| Delicensing * FLEX 2 | −0.098 | 0.212 *** | −0.129 |

| (0.083) | (0.074) | (0.097) | |

| FDI reform | −0.115 ** | −0.106 | −0.123 ** |

| (0.045) | (0.069) | (0.049) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.208 ** | 0.222 *** |

| (0.067) | (0.097) | (0.072) | |

| Flexible labour markets: Effects of changes in final goods tariffs | |||

| Row 1 + Row 2 | 0.111 * | 0.089 | 0.104 |

| Standard Error | 0.063 | 0.113 | 0.070 |

| p-value (combined effect = 0) | 0.078 | 0.431 | 0.139 |

| Flexible labour markets: Effects of changes in input tariffs | |||

| Row 3 + Row 4 | −0.659 *** | −0.039 | −0.647 *** |

| Standard Error | 0.199 | 0.423 | 0.223 |

| p-value (combined effect = 0) | 0.001 | 0.927 | 0.004 |

| Flexible labour markets: Effects of delicensing | |||

| Row 5 + Row 6 | −0.013 | 0.155 *** | −0.036 |

| Standard Error | 0.036 | 0.058 | 0.041 |

| p-value (combined effect = 0) | 0.707 | 0.007 | 0.385 |

| Flexible labour markets: Effects of FDI reform | |||

| Row 7 + Row 8 | 0.093 ** | 0.103 | 0.099 ** |

| Standard Error | 0.039 | 0.078 | 0.042 |

| p-value (combined effect = 0) | 0.017 | 0.190 | 0.020 |

| State FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Observations | 160,883 | 23,244 | 137,639 |

| R-squared | 0.205 | 0.210 | 0.206 |

| A: All States | Dependent Variable: ln (Number of Formal Firms in Three Digit Industry) | ||

|---|---|---|---|

| All Industries | Industries with CR4 Above Median in 1990 (Less Competitive) | Industries with CR4 Below Median in 1990 (More Competitive) | |

| Final goods tariffs | −0.057 | 0.097 | −0.064 |

| (0.045) | (0.078) | (0.054) | |

| Input tariffs | 0.151 | −0.922 * | 0.208 |

| (0.249) | (0.489) | (0.291) | |

| Delicensing | 0.079 ** | −0.046 | 0.096 ** |

| (0.036) | (0.078) | (0.044) | |

| FDI reform | 0.019 | 0.015 | 0.019 |

| (0.034) | (0.061) | (0.038) | |

| Observations | 556 | 252 | 304 |

| R-squared | 0.379 | 0.167 | 0.458 |

| B: States with flexible labour markets (FLEX 2 = 1) | |||

| Final goods tariffs | −0.068 | −0.023 | −0.054 |

| (0.059) | (0.081) | (0.069) | |

| Input tariffs | 0.003 | −0.890 * | −0.050 |

| (0.300) | (0.528) | (0.360) | |

| Delicensing | 0.086 ** | −0.042 | 0.112 ** |

| (0.042) | (0.087) | (0.051) | |

| FDI reform | −0.005 | −0.032 | −0.011 |

| (0.036) | (0.085) | (0.041) | |

| Observations | 520 | 224 | 296 |

| R-squared | 0.386 | 0.139 | 0.472 |

| C: States with inflexible labour markets (FLEX 2 = 0) | |||

| Final goods tariffs | −0.041 | 0.166 | −0.062 |

| (0.052) | (0.132) | (0.060) | |

| Input tariffs | 0.271 | −0.727 | 0.367 |

| (0.291) | (0.612) | (0.322) | |

| Delicensing | 0.045 | −0.018 | 0.051 |

| (0.037) | (0.102) | (0.042) | |

| FDI reform | 0.052 | 0.122 | 0.046 |

| (0.038) | (0.081) | (0.041) | |

| Observations | 484 | 184 | 300 |

| R-squared | 0.169 | 0.110 | 0.217 |

| Baseline (All Paid Employees) | Directly Employed Adult Male Workers | Directly Employed Adult Female Workers | Contract Workers | Supervisory/Managerial Level Employees | Other Employees | |

|---|---|---|---|---|---|---|

| Final goods tariffs | −0.020 | 0.059 | −0.114 | −0.138 | 0.098 ** | 0.031 |

| (0.075) | (0.059) | (0.143) | (0.107) | (0.047) | (0.057) | |

| Final goods tariffs * FLEX 2 | 0.132 | −0.016 | 0.225 | 0.245 * | −0.018 | −0.001 |

| (0.115) | (0.088) | (0.167) | (0.129) | (0.063) | (0.084) | |

| Input tariffs | −0.680 *** | −0.676 *** | −0.222 | 0.025 | −0.275 | −0.323 |

| (0.211) | (0.212) | (0.369) | (0.412) | (0.196) | (0.206) | |

| Input tariffs * FLEX 2 | 0.021 | 0.223 | −0.552 * | −0.204 | −0.034 | 0.405 ** |

| (0.216) | (0.198) | (0.331) | (0.378) | (0.190) | (0.192) | |

| Delicensing | 0.084 | 0.032 | 0.225 * | 0.204 | 0.019 | −0.018 |

| (0.061) | (0.039) | (0.125) | (0.144) | (0.049) | (0.034) | |

| Delicensing * FLEX 2 | −0.098 | −0.055 | −0.208 | −0.202 | −0.067 | −0.020 |

| (0.083) | (0.053) | (0.143) | (0.178) | (0.059) | (0.044) | |

| FDI reform | −0.115 ** | −0.117 *** | −0.191 * | 0.035 | −0.094 *** | −0.106 *** |

| (0.045) | (0.041) | (0.109) | (0.081) | (0.035) | (0.032) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.180 *** | 0.211 | 0.196 ** | 0.105 *** | 0.193 *** |

| (0.067) | (0.055) | (0.132) | (0.088) | (0.039) | (0.046) | |

| Flexible labour markets: Effects of changes in final goods tariffs | ||||||

| Row 1 + Row 2 | 0.111 * | 0.043 | 0.111 | 0.107 | 0.080 * | 0.030 |

| Standard Error | 0.063 | 0.055 | 0.072 | 0.106 | 0.045 | 0.054 |

| p-value (combined effect = 0) | 0.078 | 0.428 | 0.126 | 0.313 | 0.078 | 0.578 |

| Flexible labour markets: Effects of changes in input tariffs | ||||||

| Row 3 + Row 4 | −0.659 *** | −0.452 ** | −0.774 *** | −0.179 | −0.310 * | 0.082 |

| Standard Error | 0.199 | 0.205 | 0.265 | 0.430 | 0.182 | 0.176 |

| p-value (combined effect = 0) | 0.001 | 0.027 | 0.004 | 0.677 | 0.089 | 0.641 |

| Flexible labour markets: Effects of delicensing | ||||||

| Row 5 + Row 6 | −0.013 | −0.023 | 0.017 | 0.001 | −0.048 * | −0.037 |

| Standard Error | 0.036 | 0.029 | 0.049 | 0.083 | 0.028 | 0.026 |

| p-value (combined effect = 0) | 0.707 | 0.430 | 0.729 | 0.987 | 0.087 | 0.148 |

| Flexible labour markets: Effects of FDI reform | ||||||

| Row 7 + Row 8 | 0.093 ** | 0.062 ** | 0.021 | 0.231 *** | 0.011 | 0.087 *** |

| Standard Error | 0.039 | 0.032 | 0.049 | 0.078 | 0.026 | 0.029 |

| p-value (combined effect = 0) | 0.017 | 0.049 | 0.674 | 0.003 | 0.667 | 0.003 |

| State FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 153,284 | 51,979 | 30,221 | 122,368 | 131,267 |

| R-squared | 0.205 | 0.219 | 0.312 | 0.187 | 0.149 | 0.181 |

| A: All States | ln (Number of Firms Employing Contract Workers) | ln (Number of Firms Using Imported Inputs) |

|---|---|---|

| Final goods tariffs | −0.082 | −0.148 |

| (0.117) | (0.194) | |

| Input tariffs | −0.739 | 1.986 |

| (0.518) | (1.251) | |

| Delicensing | 0.087 | −0.215 |

| (0.082) | (0.262) | |

| FDI reform | 0.135 * | −0.320 |

| (0.077) | (0.260) | |

| Observations | 544 | 479 |

| R-squared | 0.251 | 0.507 |

| B: States with flexible labour markets (FLEX 2 = 1) | ||

| Final goods tariffs | −0.168 | −0.316 |

| (0.143) | (0.237) | |

| Input tariffs | −0.539 | 2.231 |

| (0.629) | (1.477) | |

| Delicensing | 0.103 | −0.160 |

| (0.097) | (0.243) | |

| FDI reform | 0.219 ** | −0.176 |

| (0.097) | (0.261) | |

| Observations | 504 | 440 |

| R-squared | 0.224 | 0.433 |

| C: States with flexible labour markets (FLEX 2 = 0) | ||

| Final goods tariffs | −0.096 | −0.208 |

| (0.117) | (0.247) | |

| Input tariffs | −0.318 | 1.181 |

| (0.707) | (1.264) | |

| Delicensing | 0.001 | −0.298 |

| (0.097) | (0.202) | |

| FDI reform | 0.065 | −0.095 |

| (0.085) | (0.191) | |

| Observations | 467 | 378 |

| R-squared | 0.144 | 0.384 |

| Export Oriented Industries (Nouroz 2001) | Non-Export Oriented Industries (Nouroz 2001) | Export-Output Ratio above Median (1990 IOTT) | Export-Output Ratio below Median (1990 IOTT) | Import-Output Ratio above Median (1990 IOTT) | Import-Output Ratio below Median (1990 IOTT) | |

|---|---|---|---|---|---|---|

| Final goods tariffs | −0.723 | −0.017 | −0.318 * | 0.127 ** | −0.071 | −0.002 |

| (0.573) | (0.075) | (0.167) | (0.051) | (0.072) | (0.087) | |

| Final goods tariffs * FLEX 2 | 0.349 | 0.126 | 0.539 ** | −0.074 | 0.200 ** | 0.076 |

| (0.587) | (0.115) | (0.247) | (0.075) | (0.094) | (0.137) | |

| Input tariffs | −1.742 ** | −0.620 *** | −0.121 | −0.898 *** | 0.167 | −0.773 *** |

| (0.837) | (0.217) | (0.390) | (0.257) | (0.294) | (0.254) | |

| Input tariffs * FLEX 2 | −0.293 | 0.044 | −0.388 | −0.057 | −0.266 | 0.018 |

| (0.428) | (0.228) | (0.432) | (0.244) | (0.213) | (0.289) | |

| Delicensing | −0.208 * | 0.123 * | −0.024 | 0.076 | 0.029 | 0.141 * |

| (0.123) | (0.067) | (0.051) | (0.080) | (0.050) | (0.079) | |

| Delicensing * FLEX 2 | 0.178 | −0.145 | 0.033 | −0.058 | 0.003 | −0.164 |

| (0.154) | (0.092) | (0.060) | (0.121) | (0.068) | (0.108) | |

| FDI reform | −0.061 | −0.119 ** | −0.153 *** | −0.020 | −0.041 | −0.151 ** |

| (0.110) | (0.048) | (0.058) | (0.055) | (0.044) | (0.065) | |

| FDI reform * FLEX 2 | −0.029 | 0.255 *** | 0.253 *** | 0.014 | 0.058 | 0.249 ** |

| (0.129) | (0.071) | (0.077) | (0.072) | (0.048) | (0.097) | |

| Flexible labour markets: Effects of changes in final goods tariffs | ||||||

| Row 1 + Row 2 | −0.374 | 0.109 * | 0.221 * | 0.053 | 0.129 * | 0.075 |

| Standard Error | 0.439 | 0.064 | 0.114 | 0.061 | 0.074 | 0.080 |

| p-value (combined effect = 0) | 0.394 | 0.089 | 0.052 | 0.383 | 0.081 | 0.353 |

| Flexible labour markets: Effects of changes in input tariffs | ||||||

| Row 3 + Row 4 | −2.035 *** | −0.576 *** | −0.509 * | −0.955 *** | −0.099 | −0.755 *** |

| Standard Error | 0.776 | 0.207 | 0.299 | 0.288 | 0.284 | 0.250 |

| p-value (combined effect = 0) | 0.009 | 0.005 | 0.089 | 0.001 | 0.727 | 0.003 |

| Flexible labour markets: Effects of delicensing | ||||||

| Row 5 + Row 6 | −0.030 | −0.022 | 0.008 | 0.018 | 0.032 | −0.022 |

| Standard Error | 0.075 | 0.040 | 0.042 | 0.056 | 0.044 | 0.046 |

| p-value (combined effect = 0) | 0.692 | 0.579 | 0.839 | 0.750 | 0.466 | 0.624 |

| Flexible labour markets: Effects of FDI reform | ||||||

| Row 7 + Row 8 | −0.090 | 0.136 *** | 0.100 ** | −0.006 | 0.017 | 0.099 * |

| Standard Error | 0.082 | 0.040 | 0.049 | 0.044 | 0.038 | 0.053 |

| p-value (combined effect = 0) | 0.276 | 0.001 | 0.040 | 0.892 | 0.646 | 0.065 |

| State FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 23,887 | 136,996 | 96,814 | 64,069 | 57,795 | 103,088 |

| R-squared | 0.179 | 0.214 | 0.179 | 0.252 | 0.108 | 0.257 |

| Baseline (All Firms) | Dropping Outlier Industries | Adding State-Year Interactions | |

|---|---|---|---|

| Final goods tariffs | −0.020 | −0.085 | −0.016 |

| (0.075) | (0.090) | (0.075) | |

| Final goods tariffs * FLEX 2 | 0.132 | 0.241 * | 0.133 |

| (0.115) | (0.141) | (0.114) | |

| Input tariffs | −0.680 *** | −0.583 ** | −0.984 *** |

| (0.211) | (0.228) | (0.281) | |

| Input tariffs * FLEX 2 | 0.021 | −0.141 | 0.445 |

| (0.216) | (0.254) | (0.377) | |

| Delicensing | 0.084 | 0.085 | 0.099 |

| (0.061) | (0.061) | (0.063) | |

| Delicensing * FLEX 2 | −0.098 | −0.100 | −0.118 |

| (0.083) | (0.083) | (0.091) | |

| FDI reform | −0.115 ** | −0.113 ** | −0.117 *** |

| (0.045) | (0.045) | (0.045) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.204 *** | 0.200 *** |

| (0.067) | (0.066) | (0.070) | |

| Flexible labour markets: Effects of changes in final goods tariffs | |||

| Row 1 + Row 2 | 0.111 * | 0.156 ** | 0.117 * |

| Standard Error | 0.063 | 0.075 | 0.063 |

| p-value (combined effect = 0) | 0.078 | 0.037 | 0.062 |

| Flexible labour markets: Effects of changes in input tariffs | |||

| Row 3 + Row 4 | −0.659 *** | −0.725 *** | −0.539 ** |

| Standard Error | 0.199 | 0.210 | 0.228 |

| p-value (combined effect = 0) | 0.001 | 0.001 | 0.018 |

| Flexible labour markets: Effects of delicensing | |||

| Row 5 + Row 6 | −0.013 | −0.015 | −0.019 |

| Standard Error | 0.036 | 0.036 | 0.040 |

| p-value (combined effect = 0) | 0.707 | 0.676 | 0.641 |

| Flexible labour markets: Effects of FDI reform | |||

| Row 7 + Row 8 | 0.093 ** | 0.091 ** | 0.083 ** |

| Standard Error | 0.039 | 0.039 | 0.038 |

| p-value (combined effect = 0) | 0.017 | 0.019 | 0.031 |

| State FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| State-Year FE | No | No | Yes |

| Observations | 160,883 | 160,255 | 160,883 |

| R-squared | 0.205 | 0.204 | 0.207 |

| Baseline (All Firms) | Delicensed by 1986 | Not Delicensed by 1986 | Controlling for Firm Age | FLEX 1 Instead of FLEX 2 | FLEX 3 Instead of FLEX 2 | |

|---|---|---|---|---|---|---|

| Final goods tariffs | −0.020 | −0.135 | 0.110 * | −0.045 | 0.068 | 0.071 |

| (0.075) | (0.096) | (0.066) | (0.075) | (0.054) | (0.061) | |

| Final goods tariffs * FLEX | 0.132 | 0.392 ** | −0.156 * | 0.165 | −0.011 | 0.009 |

| (0.115) | (0.153) | (0.083) | (0.116) | (0.122) | (0.120) | |

| Input tariffs | −0.680 *** | −0.722 ** | −0.823 *** | −0.600 *** | −0.846 *** | −0.961 *** |

| (0.211) | (0.289) | (0.254) | (0.203) | (0.201) | (0.230) | |

| Input tariffs * FLEX | 0.021 | −0.014 | 0.281 | −0.049 | 0.740 *** | 0.580 ** |

| (0.216) | (0.252) | (0.264) | (0.210) | (0.265) | (0.262) | |

| Delicensing | 0.084 | 0.092 | 0.061 | 0.034 | ||

| (0.061) | (0.062) | (0.042) | (0.050) | |||

| Delicensing * FLEX | −0.098 | −0.094 | −0.103 | −0.038 | ||

| (0.083) | (0.084) | (0.083) | (0.088) | |||

| FDI reform | −0.115 ** | −0.158 *** | 0.021 | −0.113 ** | −0.071 ** | −0.094 *** |

| (0.045) | (0.050) | (0.067) | (0.045) | (0.028) | (0.035) | |

| FDI reform * FLEX | 0.208 *** | 0.304 *** | −0.060 | 0.208 *** | 0.200 *** | 0.230 *** |

| (0.067) | (0.081) | (0.096) | (0.069) | (0.071) | (0.070) | |

| Firm age | 0.008 *** | |||||

| (0.001) | ||||||

| Flexible labour markets: Effects of changes in final goods tariffs | ||||||

| Row 1 + Row 2 | 0.111 * | 0.257 *** | −0.046 | 0.120 * | 0.057 | 0.081 |

| Standard Error | 0.063 | 0.092 | 0.063 | 0.064 | 0.089 | 0.080 |

| p-value (combined effect = 0) | 0.078 | 0.005 | 0.469 | 0.060 | 0.517 | 0.313 |

| Flexible labour markets: Effects of changes in input tariffs | ||||||

| Row 3 + Row 4 | −0.659 *** | −0.736 ** | −0.542 ** | −0.649 *** | −0.106 | −0.381 * |

| Standard Error | 0.199 | 0.305 | 0.266 | 0.192 | 0.203 | 0.203 |

| p-value (combined effect = 0) | 0.001 | 0.016 | 0.042 | 0.001 | 0.602 | 0.061 |

| Flexible labour markets: Effects of delicensing | ||||||

| Row 5 + Row 6 | −0.013 | −0.003 | −0.042 | −0.004 | ||

| Standard Error | 0.036 | 0.035 | 0.053 | 0.050 | ||

| p-value (combined effect = 0) | 0.707 | 0.944 | 0.430 | 0.937 | ||

| Flexible labour markets: Effects of FDI reform | ||||||

| Row 7 + Row 8 | 0.093 ** | 0.147 *** | −0.040 | 0.095 ** | 0.129 ** | 0.136 *** |

| Standard Error | 0.039 | 0.053 | 0.058 | 0.040 | 0.060 | 0.051 |

| p-value (combined effect = 0) | 0.017 | 0.006 | 0.495 | 0.017 | 0.031 | 0.008 |

| State FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 77,692 | 83,191 | 159,872 | 160,883 | 160,883 |

| R-squared | 0.205 | 0.099 | 0.277 | 0.211 | 0.206 | 0.206 |

| Baseline (All Firms, Time Lag: 2 Years) | Time Lag: 1 Year | Time Lag: 3 Years | Excluding 1994 | Excluding 1995 | Excluding 1997 | |

|---|---|---|---|---|---|---|

| Final goods tariffs | −0.020 | −0.039 | −0.084 | −0.041 | −0.015 | 0.003 |

| (0.075) | (0.078) | (0.065) | (0.079) | (0.069) | (0.070) | |

| Final goods tariffs * FLEX 2 | 0.132 | 0.165 | 0.126 | 0.178 | 0.122 | 0.120 |

| (0.115) | (0.123) | (0.098) | (0.119) | (0.103) | (0.101) | |

| Input tariffs | −0.680 *** | −0.574 *** | −0.306 ** | −0.766 *** | −0.703 *** | −0.866 *** |

| (0.211) | (0.197) | (0.154) | (0.226) | (0.212) | (0.225) | |

| Input tariffs * FLEX 2 | 0.021 | −0.090 | −0.062 | −0.062 | 0.014 | 0.261 |

| (0.216) | (0.199) | (0.196) | (0.216) | (0.199) | (0.229) | |

| Delicensing | 0.084 | 0.085 | 0.088 | 0.066 | 0.078 | 0.060 |

| (0.061) | (0.061) | (0.060) | (0.058) | (0.058) | (0.059) | |

| Delicensing * FLEX 2 | −0.098 | −0.100 | −0.115 | −0.074 | −0.076 | −0.057 |

| (0.083) | (0.083) | (0.080) | (0.076) | (0.076) | (0.078) | |

| FDI reform | −0.115 ** | −0.112 ** | −0.092 ** | −0.109 ** | −0.118 *** | −0.123 *** |

| (0.045) | (0.045) | (0.044) | (0.047) | (0.045) | (0.044) | |

| FDI reform * FLEX 2 | 0.208 *** | 0.203 *** | 0.199 *** | 0.199 *** | 0.209 *** | 0.214 *** |

| (0.067) | (0.065) | (0.064) | (0.067) | (0.067) | (0.066) | |

| Flexible labour markets: Effects of changes in final goods tariffs | ||||||

| Row 1 + Row 2 | 0.111 * | 0.127 ** | 0.042 | 0.137 ** | 0.107 * | 0.122 ** |

| Standard Error | 0.063 | 0.061 | 0.047 | 0.065 | 0.061 | 0.062 |

| p-value (combined effect = 0) | 0.078 | 0.037 | 0.367 | 0.035 | 0.080 | 0.049 |

| Flexible labour markets: Effects of changes in input tariffs | ||||||

| Row 3 + Row 4 | −0.659 *** | −0.665 *** | −0.368 ** | −0.829 *** | −0.689 *** | −0.604 *** |

| Standard Error | 0.199 | 0.172 | 0.153 | 0.217 | 0.204 | 0.202 |

| p-value (combined effect = 0) | 0.001 | 0.000 | 0.017 | 0.000 | 0.001 | 0.003 |

| Flexible labour markets: Effects of delicensing | ||||||

| Row 5 + Row 6 | −0.013 | −0.015 | −0.027 | −0.007 | 0.002 | 0.004 |

| Standard Error | 0.036 | 0.038 | 0.034 | 0.037 | 0.034 | 0.035 |

| p-value (combined effect = 0) | 0.707 | 0.691 | 0.431 | 0.841 | 0.947 | 0.919 |

| Flexible labour markets: Effects of FDI reform | ||||||

| Row 7 + Row 8 | 0.093 ** | 0.091 ** | 0.108 *** | 0.090 ** | 0.091 ** | 0.091 ** |

| Standard Error | 0.039 | 0.038 | 0.037 | 0.040 | 0.038 | 0.039 |

| p-value (combined effect = 0) | 0.017 | 0.017 | 0.004 | 0.027 | 0.018 | 0.020 |

| State FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 160,883 | 160,883 | 160,883 | 119,735 | 119,075 | 118,602 |

| R-squared | 0.205 | 0.205 | 0.205 | 0.205 | 0.204 | 0.209 |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shembavnekar, N. Economic Reforms, Labour Markets and Formal Sector Employment: Evidence from India. Economies 2019, 7, 31. https://doi.org/10.3390/economies7020031

Shembavnekar N. Economic Reforms, Labour Markets and Formal Sector Employment: Evidence from India. Economies. 2019; 7(2):31. https://doi.org/10.3390/economies7020031

Chicago/Turabian StyleShembavnekar, Nihar. 2019. "Economic Reforms, Labour Markets and Formal Sector Employment: Evidence from India" Economies 7, no. 2: 31. https://doi.org/10.3390/economies7020031

APA StyleShembavnekar, N. (2019). Economic Reforms, Labour Markets and Formal Sector Employment: Evidence from India. Economies, 7(2), 31. https://doi.org/10.3390/economies7020031