The Mediating Effect of the Internal Control System on the Relationship between the Accounting Information System and Employee Performance in Jordan Islamic Banks

, ,

, ,

Abstract

1. Introduction

2. Literature Review

2.1. Accounting Information System (AIS)

2.2. Information Quality (IQ)

2.3. System Quality (SQ1)

2.4. Service Quality (SQ2)

2.5. Internal Control Systems (ICS)

2.6. Employee Performance (EP)

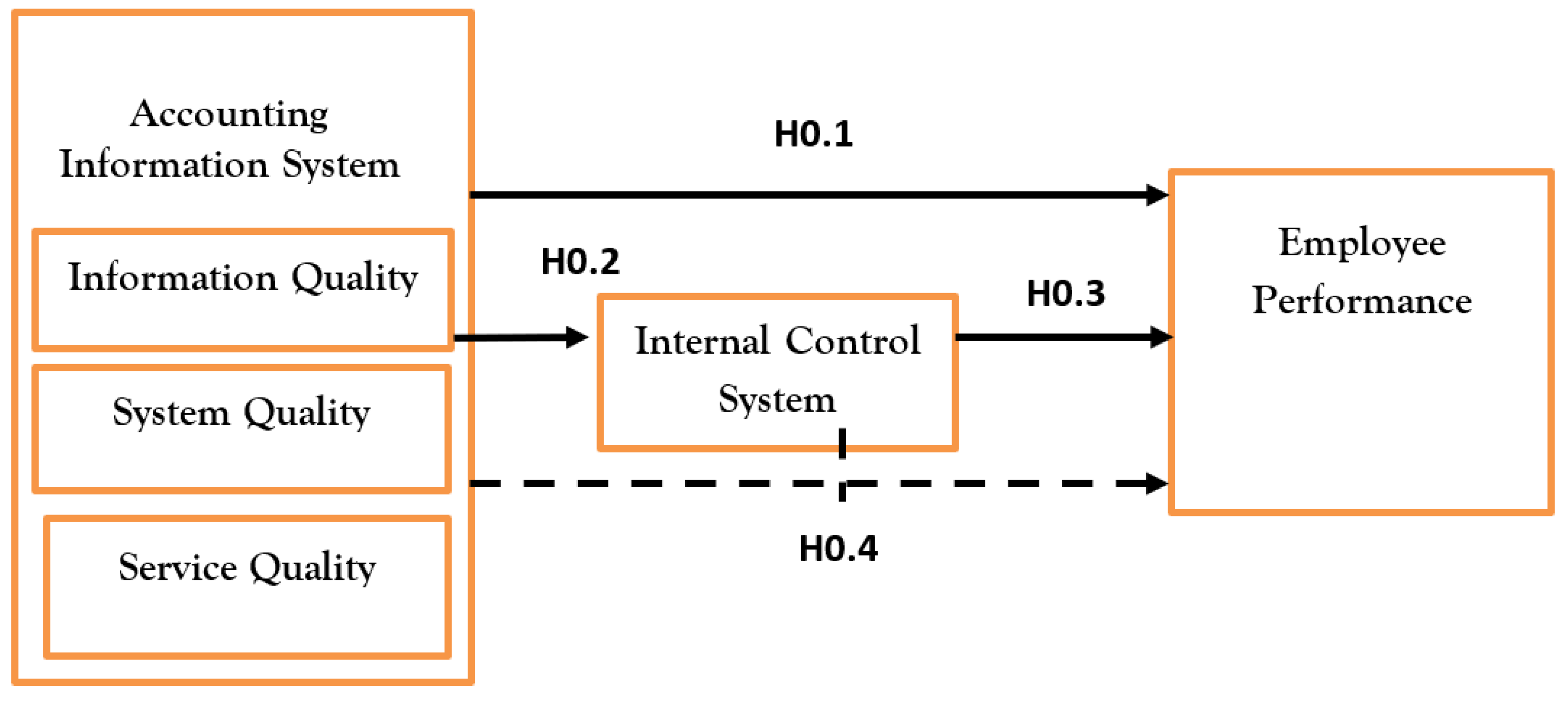

3. Methodology

3.1. Study Population

3.2. Sampling Technique and Data Collection Procedures and Measures

4. Data Analysis and Result

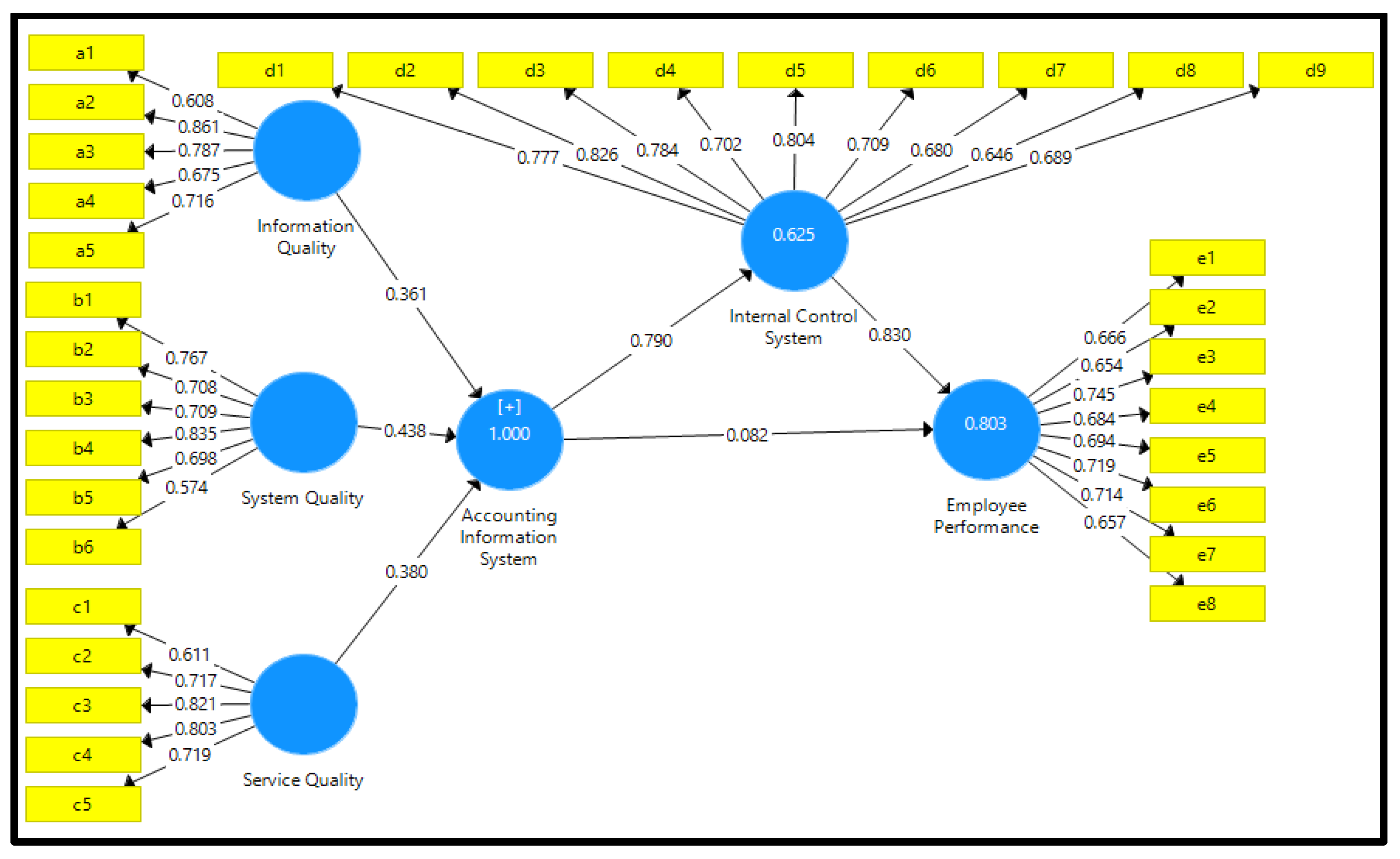

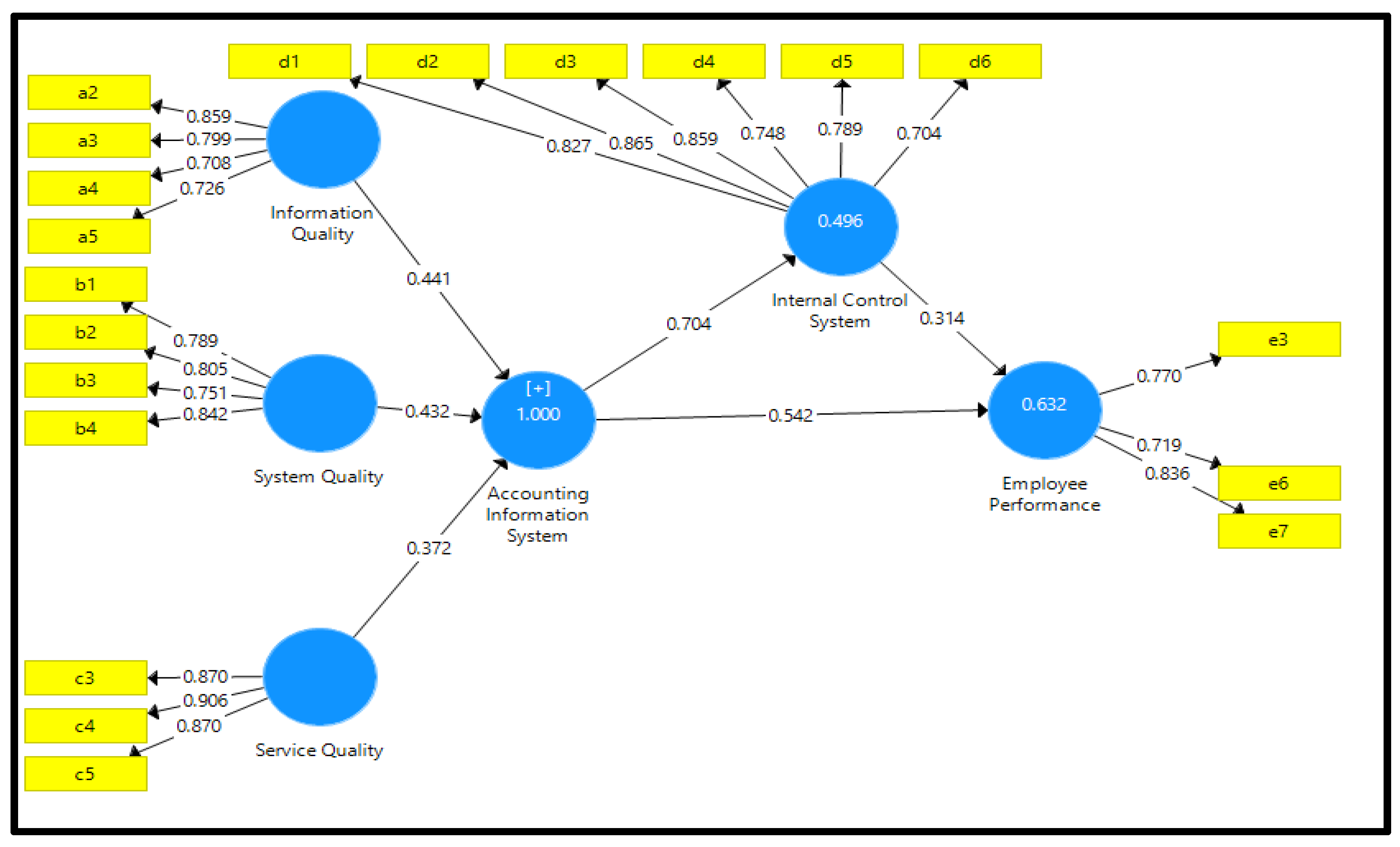

4.1. Data Analysis

4.2. The Measurement Criteria

R-Squared Test

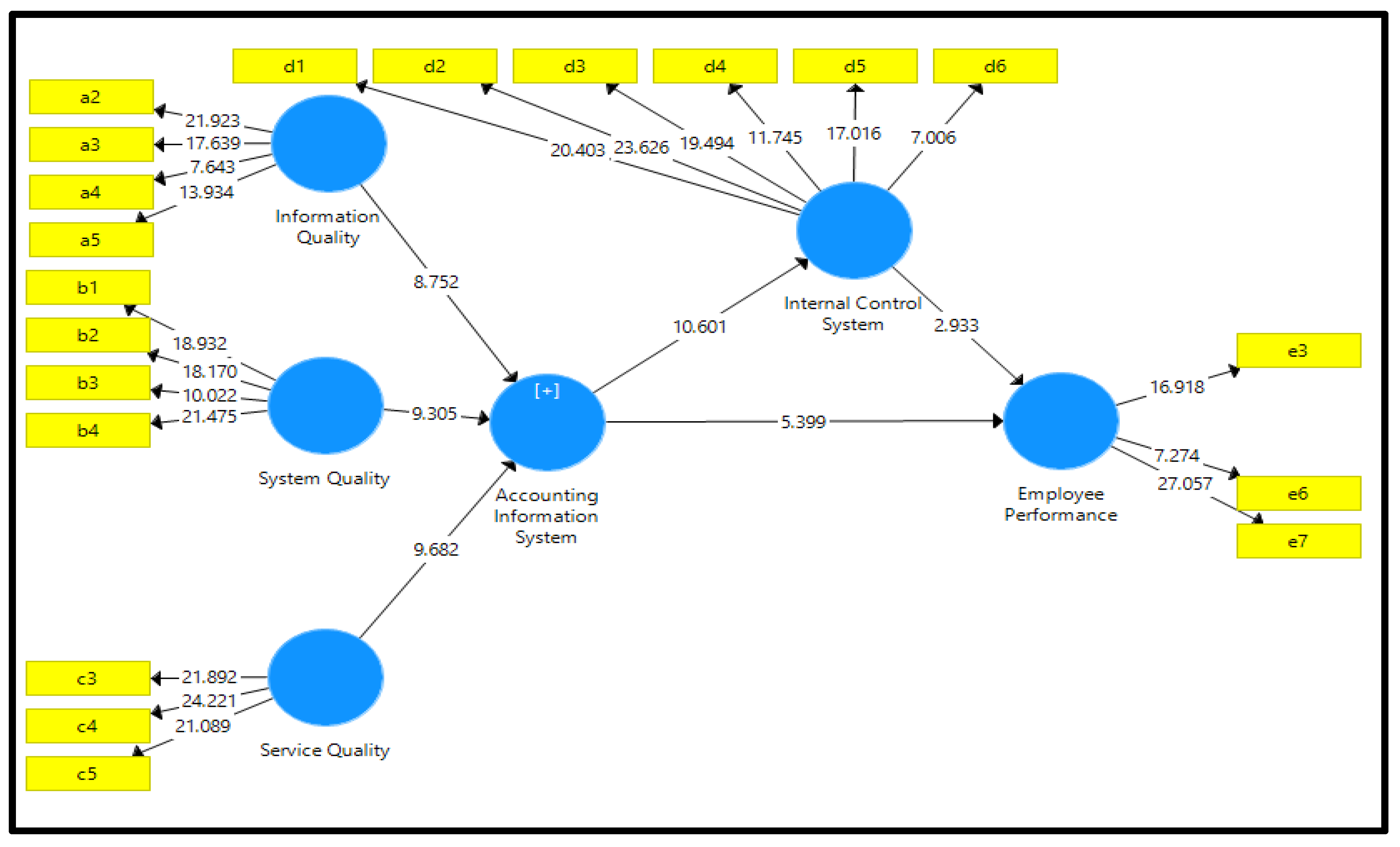

4.3. Hypotheses Test

5. Discussion

6. Implications and Limitations and Future Research and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abd Aziz, Mohamad Azizal, Hilmi Ab Rahman, Md Mahmudul Alam, and Jamaliah Said. 2015. Enhancement of the accountability of public sectors through integrity system, internal control system and leadership practices: A review study. Procedia Economics and Finance 28: 163–69. [Google Scholar] [CrossRef]

- Akdere, Mesut, Mehmet Top, and Sabahattin Tekingündüz. 2020. Examining patient perceptions of service quality in Turkish hospitals: The SERVPERF model. Total Quality Management & Business Excellence 31: 342–52. [Google Scholar] [CrossRef]

- Al Hanini, Eman. 2015. Evaluating the Reliability of the Internal Control on the Computerized Accounting Information Systems: An Empirical Study on Banks Operating in Jordan. Environment 4: 6. [Google Scholar]

- Alawaqleh, Qasim Ahmad. 2021. The Effect of Internal Control on Employee Performance of Small and Medium-Sized Enterprises in Jordan: The Role of Accounting Information System. The Journal of Asian Finance, Economics and Business 8: 855–63. [Google Scholar] [CrossRef]

- Albashabsheh, Aisar Ayed Nahar, Modafar Nayel Alhroob, Belal Eid Irbihat, and Sarfaraz Javed. 2018. Impact of accounting information system in reducing costs in Jordanian banks. International Journal of Research-Granthaalayah 6: 210–15. [Google Scholar] [CrossRef]

- Al-Dmour, Ahamed, Khaled Mofawiz Al-Fawaz, Rand Al-dmour, and Nurah Musa Allozi. 2017. Accounting information system and its role on business performance: A theoretical study. Journal of Management and Strategy 8: 79–87. [Google Scholar] [CrossRef]

- Ali, B. J., Wan Ahmad Wan Omar, and Rosni Bakar. 2016. Accounting Information System (AIS) and organizational performance: Moderating effect of organizational culture. International Journal of Economics, Commerce and Management 4: 138–58. [Google Scholar]

- Almatarneh, Zeyad, Jarah Baker Akram Falah, and Mufleh Amin AL Jarrah. 2022. The role of management accounting in the development of supply chain performance in logistics manufacturing companies. Uncertain Supply Chain Management 10: 13–18. [Google Scholar] [CrossRef]

- Alnajjar, Mohd I. M. 2017. Impact of accounting information system on organizational performance: A study of SMEs in the UAE. Global Review of Accounting And Finance 8: 20–38. [Google Scholar] [CrossRef]

- Al-Zaqeba, Murad Ali Ahmad, Jarah Baker Akram Falah, Ineizeh Nehad Ibrahim, Almatarneh Zeyad, and AL Jarrah Mufleh Amin. 2022. The effect of management accounting and blockchain technology characteristics on supply chains efficiency. Uncertain Supply Chain Management 10: 973–82. [Google Scholar] [CrossRef]

- Alzoubi, Ali. 2011. The effectiveness of the accounting information system under the enterprise resources planning (ERP). Research Journal of Finance and Accounting 2: 10–19. [Google Scholar]

- Al-Zoubi, Abdullah M. 2017. The Extent of Electronic Accounting Information Systems’ Ability to Provide Quantitative Indicators of Financial Performance in both Public and Private Universities in Jordan. International Journal of Academic Research in Accounting, Finance and Management Sciences 7: 97–107. [Google Scholar] [CrossRef] [PubMed]

- Anderson, James C., and David W. Gerbing. 1988. Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin 103: 411–23. [Google Scholar] [CrossRef]

- Anitha, Jagannathan. 2014. Determinants of employee engagement and their impact on employee performance. International Journal of Productivity and Performance Management 63: 308–23. [Google Scholar]

- Bani Ahmad, Ahmad. 2022. Empirical Analysis on Accounting Information System Usage in Banking Sector in Jordan. Available at SSRN 4241257. Available online: https://www.abacademies.org/articles/Empirical-Analysis-on-Accounting-Information%20System-Usage-in-Banking-Sector-in-Jordan-1528-2635-23-5-454.pdf (accessed on 20 February 2023).

- Binh, Vu Thi Thanh, Nhat-Minh Tran, and Manh-Chien Vu. 2022. The effect of organizational culture on the quality of accounting information systems: Evidence from Vietnam. SAGE Open 12: 21582440221121599. [Google Scholar] [CrossRef]

- Bramasto, Ari, and Ridwan Hana Adiwiguna. 2020. The Effect of The Implementation of Accounting Information Systems and Internal Control on Employee Performance. JASa. Jurnal Akuntansi, Audit dan Sistem Informasi Akuntansi 4: 328–37. [Google Scholar] [CrossRef]

- Bukenya, Moses. 2014. Quality of accounting information and financial performance of Uganda’s public sector. American Journal of Research Communication 2: 183–203. [Google Scholar]

- Burgos, Chrisha P., Irish S. Namoc, Jasmeren P. Padilla, and Joe Mari N. Flores. 2022. The Influence of Accounting Information System on the Organizational Performance Among SMEs in Tagum City. International Journal of Multidisciplinary: Applied Business and Education Research 3: 781–90. [Google Scholar] [CrossRef]

- Dandago, Kabiru I., and Abdullahi Sani Rufai. 2014. Information technology and accounting information system in the Nigerian banking industry. Asian Economic and Financial Review 4: 655–70. [Google Scholar]

- Diamantidis, Anastasios D., and Prodromos Chatzoglou. 2019. Factors affecting employee performance: An empirical approach. International Journal of Productivity and Performance Management 68: 171–93. [Google Scholar] [CrossRef]

- Fakhimuddin, Muhammad. 2018. Reconsidering Accounting Information Systems: Effective Formulations for Company’s Internal Control. Arthatama 2: 26–34. [Google Scholar]

- Fitriati, Azmi, and Sri Mulyani. 2015. The influence of leadership style on accounting information system success and its impact on accounting information quality. Research Journal of Finance and Accounting 6: 167–73. [Google Scholar]

- Gaur, Ajai S., and Sanjaya S. Gaur. 2006. Statistical Methods for Practice and Research: A Guide to Data Analysis Using SPSS, 1st ed. Thousand Oaks: Sage. [Google Scholar]

- Gorla, Narasimhaiah, Toni M. Somers, and Betty Wong. 2010. Organizational impact of system quality, information quality, and service quality. The Journal of Strategic Information Systems 19: 207–28. [Google Scholar] [CrossRef]

- Gunawan, Sri, and Nengzih Nengzih. 2023. The Influence of Accounting Information System Quality, Accounting Information Quality and Accounting Information System Security on End User Satisfaction of S4/Hana System Application Product (SAP) with Perceived Usefulness as a Moderating Variable at PT Hakaaston. Saudi Journal of Economics and Finance 7: 22–32. [Google Scholar]

- Hair, Joseph F., Jr., Marko Sarstedt, Christian M. Ringle, and Siegfried P. Gudergan. 2017. Advanced Issues in Partial Least Squares Structural Equation Modelling. Los Angeles: Sage. [Google Scholar]

- Hameed, Abdul, and Aamer Waheed. 2011. Employee development and its affect on employee performance a conceptual framework. International Journal of Business and Social Science 2: 224–29. [Google Scholar]

- Hla, Daw, and Susan Peter Teru. 2015. Efficiency of accounting information system and performance measures. International Journal of Multidisciplinary and Current Research 3: 976–84. [Google Scholar]

- Jarah, Baker Akram Falah, and Mufleh Amin AL Jarrah. 2022. The role of accounting information systems (AIS) in increasing performance efficiency (IPE) in Jordanian companies. Academy of Strategic Management Journal 21: 111. [Google Scholar]

- Jarah, Baker Akram Falah, and Takiah Binti Mohd Iskandar. 2019a. The Mediating Effect of Acceptance of Using AIS on the Relationship between the Accounting Information Systems and Financial Performance in Jordanian Companies. International Journal of Research and Innovation in Social Science (IJRISS) 3: 256–63. [Google Scholar]

- Jarah, Baker Akram Falah, and Takiah Binti Mohd Iskandar. 2019b. The role of characteristics of accounting information systems in the improve the financial performance of Jordanian companies. International Journal Of All Research Writings 1: 32–45. [Google Scholar]

- Jarah, Baker Akram Falah, and Zeyad Almatarneh. 2021. The effect of the elements of accounting information system (AIS) on organizational culture (OC)-A field study. Academy of Strategic Management Journal 20: 1–10. [Google Scholar]

- Jarah, Baker Akram Falah, Mufleh Amin AL Jarrah, Murad Ali Ahmad Al-Zaqeba, and Mefleh Faisal Mefleh Al-Jarrah. 2022a. The Role of Internal Audit to Reduce the Effects of Creative Accounting on the Reliability of Financial Statements in the Jordanian Islamic Banks. International Journal of Financial Studies 10: 60. [Google Scholar] [CrossRef]

- Jarah, Baker Akram Falah, Mufleh Amin AL Jarrah, and Murad Ali Ahmad Al-Zaqeba. 2022b. The role of internal audit in improving supply chain management in shipping companies. Uncertain Supply Chain Management 10: 1023–28. [Google Scholar] [CrossRef]

- Jarah, Baker Akram Falah, Mufleh Amin AL Jarrah, Salam Nawaf Almomani, Emran AlJarrah, and Maen Al-Rashdan. 2023. The effect of reliable data transfer and efficient computer network features in Jordanian banks accounting information systems performance based on hardware and software, database and number of hosts. International Journal of Data and Network Science 7: 357–62. [Google Scholar] [CrossRef]

- Khan, Hajera Fatima. 2016. Accounting Information System: The Need of Modernization. International Journal of Management and Commerce Innovations 4: 4–10. [Google Scholar]

- Ladan Shagari, Shamsudeen, Akilah Abdullah, and Rafeah Mat Saat. 2017. Accounting information systems effectiveness: Evidence from the Nigerian banking sector. Interdisciplinary Journal of Information, Knowledge, and Management 12: 309–35. [Google Scholar] [CrossRef]

- Maharani, Pande Putu Gayatri, and I. G. A. E. Damayanthi. 2020. The effect of accounting information systems and internal control of employee performance with organizational culture as a mediation variable. American Journal of Humanities and Social Sciences Research (AJHSSR) 4: 233–41. [Google Scholar]

- Matovu, Bakisa Harriet. 2011. Perceived Quality of Accounting Information and Performance of Small and Medium Enterprises (SMEs). Doctoral dissertation, Makerere University, Kampala, Uganda. [Google Scholar]

- Napitupulu, Ilham Hidayah. 2020. Internal Control, Manager’s Competency, Management Accounting Information Systems and Good Corporate Governance: Evidence from Rural Banks in Indonesia. Global Business Review. [Google Scholar] [CrossRef]

- Neogy, Taposh Kumar. 2014. Evaluation of efficiency of accounting information systems: A study on mobile telecommunication companies in Bangladesh. Global Disclosure of Economics and Business 3. [Google Scholar] [CrossRef]

- Nugroho, Muchamad Aqil. 2019. Analysis of internal control of inventory accounting information system at pt. ANDRE LAURENT. Dinasti International Journal of Education Management And Social Science 1: 73–86. [Google Scholar] [CrossRef]

- Olufunmilayo, Adedeji Abosede, and Olubodun Opeyemi Hannah. 2018. Effect of Internal Control System on Employee Performance of Small-Scale Manufacturing Enterprises in Ondo State, Nigeria. Human Resource Research 2: 48–60. [Google Scholar] [CrossRef]

- Onaolapo, A. A., and T. A. Odetayo. 2012. Effect of accounting information system on organisational effectiveness: A case study of selected construction companies in Ibadan, Nigeria. American Journal of Business and Management 1: 183–89. [Google Scholar] [CrossRef]

- Qatawneh, Adel M. 2012. The effect of electronic commerce on the accounting information system of Jordanian banks. International Business Research 5: 158. [Google Scholar] [CrossRef]

- Ranganath, Malitha, and Nadarajah Rajeshwaran. 2022. Quality of accounting information systems and organizational effectiveness in an emerging country. SMART Journal of Business Management Studies 18: 22–29. [Google Scholar] [CrossRef]

- Romney, Marshall, and Barry Steinbart. 2006. Accounting Information Systems, 10th ed. Hoboken: Prentice Hall International Inc. [Google Scholar]

- Sabri, Syamimi Nabilah, Nor Hanani Ahamad Rapani, and Oday Jasim Almaliki. 2022. The Accounting Information System (AIS) Effectiveness and SMEs Performance: A Conceptual Paper. Management Research Journal 11: 64–73. [Google Scholar]

- Saeidi, Hadi, and Bhavani Prasad. 2014. Impact of accounting information systems (AIS) on organizational performance: A case study of TATA consultancy services (TCS)-India. Journal of Management and Accounting Studies 2: 54–60. [Google Scholar] [CrossRef]

- Sagala, Friska Zagita. 2020. The Effect of Accounting Information Systems and Internal Control of Employee Performance. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi Akuntansi) 4: 69–81. [Google Scholar] [CrossRef]

- Salehi, Mahdi, Mahmoud Mousavi Shiri, and Fatemeh Ehsanpour. 2013. Effectiveness of internal control in the banking sector: Evidence from bank Mellat, Iran. IUP Journal of Bank Management 12: 23–34. [Google Scholar]

- Sekaran, Uma, and Roger Bougie. 2016. Research Methods for Business: A Skill-Building Approach, 5th ed. New York: John Wiley & Sons Inc. [Google Scholar]

- Setyaningsih, S. D., S. Mulyani, B. Akbar, and Ida Farida. 2021. Implementation and Performance of Accounting Information Systems, Internal Control and Organizational Culture in the Quality of Financial Information. Utopía y Praxis Latinoamericana: Revista Internacional de Filosofía Iberoamericana y Teoría Social 26: 222–36. [Google Scholar]

- Shahzadi, Irum, Ayesha Javed, Syed Shahzaib Pirzada, Shagufta Nasreen, and Farida Khanam. 2014. Impact of employee motivation on employee performance. European Journal of Business and Management 6: 159–66. [Google Scholar]

- Sodiq, Dinar Irfani, Hadi Samanto, and Sri Laksmi Pardanawati. 2022. The influence of quality of service, commitment and quality of accounting information systems on community satisfaction (Survey in Kalikotes District, Klaten Regency). International Journal of Economics, Business and Accounting Research (IJEBAR) 6: 1869–70. [Google Scholar]

- Soudani, Siamak Nejadhosseini. 2012. The usefulness of an accounting information system for effective organizational performance. International Journal of Economics and Finance 4: 136–45. [Google Scholar] [CrossRef]

- Susanto, Azhar. 2016. The effect of internal control on accounting information system. International Business Management 10: 5523–29. [Google Scholar] [CrossRef]

- Syah, L. Y., S. N. Nafsiah, and K. Saddhono. 2019. Linear regression statistic from accounting information system application for Employee integrity. In Journal of Physics: Conference Series. Bristol: IOP Publishing, vol. 1339, p. 012131. [Google Scholar]

- Teru, Susan Peter, Innocent Idoku, and Jane Tinyang Ndeyati. 2017. A review of the impact of accounting information system for effective internal control on firm performance. Indian Journal of Finance and Banking 1: 52–59. [Google Scholar] [CrossRef]

- Widyani, Rachma, and Ajeng Wijayanti. 2022. Effect of Perceived Reputation and Service Quality on Accounting Information Systems that Moderate Purchase Decisions. Journal Research of Social, Science, Economics, and Management 1: 1870–77. [Google Scholar] [CrossRef]

- Wongsim, Manirath, and Pawornprat Hongsakon. 2015. The Adoption of Process Management for Accounting Information Systems in Thailand. World Academy of Science, Engineering and Technology, International Journal of Computer, Electrical, Automation, Control and Information Engineering 9: 1327–35. [Google Scholar]

- Zuo, Zhigang, and Zhibin Lin. 2022. Government R&D subsidies and firm innovation performance: The moderating role of accounting information quality. Journal of Innovation & Knowledge 7: 100176. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Description | Variable | Result | Percentage |

|---|---|---|---|

| Gender | Male | 82 | 89.1% |

| Female | 10 | 10.9% | |

| Qualification | Bachelor’s | 56 | 60% |

| Master’s | 30 | 32.6% | |

| Doctorate | 6 | 6.5% | |

| Experience | Less than 5 years | 10 | 10.9% |

| From 6 years to less than 10 years | 27 | 29.3% | |

| From 11 years to less than 15 years | 37 | 40.2% | |

| From 16 years & more | 18 | 19.6% |

| Construct | Item | Loading (>0.7) | Result |

|---|---|---|---|

| Information quality (IQ) | a1 | 0.608 | Not accept |

| a2 | 0.861 | Accept | |

| a3 | 0.787 | Accept | |

| a4 | 0.675 | Accept | |

| a5 | 0.716 | Accept | |

| System quality (SQ1) | b1 | 0.767 | Accept |

| b2 | 0.708 | Accept | |

| b3 | 0.709 | Accept | |

| b4 | 0.835 | Accept | |

| b5 | 0.698 | Not accept | |

| b6 | 0.575 | Not accept | |

| Service quality (SQ2) | c1 | 0.611 | Not accept |

| c2 | 0.711 | Accept | |

| c3 | 0.821 | Accept | |

| c4 | 0.803 | Accept | |

| c5 | 0.719 | Accept | |

| Internal control system (ICS) | d1 | 0.777 | Accept |

| d2 | 0.826 | Accept | |

| d3 | 0.784 | Accept | |

| d4 | 0.702 | Accept | |

| d5 | 0.804 | Accept | |

| d6 | 0.709 | Accept | |

| d7 | 0.680 | Not accept | |

| d8 | 0.646 | Not accept | |

| d9 | 0.686 | Not accept | |

| Employee performance (EP) | e1 | 0.666 | Not accept |

| e2 | 0.654 | Not accept | |

| e3 | 0.745 | Accept | |

| e4 | 0.684 | Not accept | |

| e5 | 0.694 | Not accept | |

| e6 | 0.719 | Accept | |

| e7 | 0.714 | Accept | |

| e8 | 0.657 | Not accept |

| Construct | Item | Loading (>0.7) | Result | Cronbach’s Alpha (>0.7) | CR (>0.7) | AVE (>0.5) |

|---|---|---|---|---|---|---|

| IQ | a2 | 0.859 | Accept | 0.77 | 0.85 | 0.60 |

| a3 | 0.799 | Accept | ||||

| a4 | 0.708 | Accept | ||||

| a5 | 0.726 | Accept | ||||

| SQ1 | b1 | 0.789 | Accept | 0.81 | 0.87 | 0.63 |

| b2 | 0.805 | Accept | ||||

| b3 | 0.751 | Accept | ||||

| b4 | 0.842 | Accept | ||||

| SQ2 | c3 | 0.870 | Accept | 0.85 | 0.91 | 0.77 |

| c4 | 0.906 | Accept | ||||

| c5 | 0.870 | Accept | ||||

| ICS | d1 | 0.827 | Accept | 0.70 | 0.91 | 0.64 |

| d2 | 0.865 | Accept | ||||

| d3 | 0.859 | Accept | ||||

| d4 | 0.748 | Accept | ||||

| d5 | 0.789 | Accept | ||||

| d6 | 0.704 | Accept | ||||

| EP | e3 | 0.770 | Accept | 0.67 | 0.82 | 0.60 |

| e6 | 0.719 | Accept | ||||

| e7 | 0.836 | Accept |

| Factors | IQ | SQ | SQ | ICS | EP |

|---|---|---|---|---|---|

| IQ | 0.775 | ||||

| SQ1 | 0.541 | 0.798 | |||

| SQ2 | 0.504 | 0.334 | 0.882 | ||

| ICS | 0.548 | 0.650 | 0.504 | 0.801 | |

| EP | 0.690 | 0.533 | 0.739 | 0.695 | 0.777 |

| Factor | R (Square) |

|---|---|

| AIS on EP without ICS as a mediating variable | 0.490 |

| AIS on EP with ICS as a mediating variable | 0.632 |

| Relation (Direct Effect) Hypothetical Path | T-Value | p-Value | Beta Path Coefficient | Result |

|---|---|---|---|---|

| AIS → EP | 2.399 | 0.000 | 0.542 | Supported |

| IQ → EP | 8.051 | 0.000 | 0.704 | Supported |

| SQ1 → EP | 10.214 | 0.000 | 0.337 | Supported |

| SQ2 → EP | 8.439 | 0.000 | 0.284 | Supported |

| AIS → ICS | 10.601 | 0.000 | 0.704 | Supported |

| IQ → ICS | 10.361 | 0.000 | 0.311 | Supported |

| SQ1 → ICS | 7.630 | 0.000 | 0.304 | Supported |

| SQ2 → ICS | 8.018 | 0.000 | 0.262 | Supported |

| ICS → EP | 2.933 | 0.000 | 0.314 | Supported |

| Hypotheses | Hypothetical Path | Direct Effect T Value | Direct Effect Beta | Indirect Effect Beta | Total Effect T Value | Total Effect Beta | Result |

|---|---|---|---|---|---|---|---|

| H0.4 | AIS → ICS | 10.601 | 0.704 | 10.601 | 0.704 | Supported | |

| ICS → EP | 2.933 | 0.314 | 2.933 | 0.314 | Supported | ||

| AIS → EP by ICS | 0.221 | Supported Partially mediate | |||||

| AIS → EP | 2.399 | 0.542 | 18.075 | 0.763 | Supported | ||

| H0.4.1 | IQ → ICS | 10.631 | 0.311 | 10.631 | 0.311 | Supported | |

| ICS → EP | 2.933 | 0.314 | 2.933 | 0.314 | Supported | ||

| IQ → EP by ICS | 0.097 | Supported Partially mediated | |||||

| IQ → EP | 8.051 | 0.704 | 8.051 | 0.801 | Supported | ||

| H0.4.2 | SQ1 → ICS | 7.630 | 0.304 | 7.630 | 0.304 | Supported | |

| ICS → EP | 2.933 | 0.314 | 2.933 | 0.314 | Supported | ||

| SQ1 → EP by ICS | 0.095 | Supported Partially mediated | |||||

| SQ1 → EP | 10.214 | 0.377 | 10.214 | 0.472 | Supported | ||

| H0.4.3 | SQ2 → ICS | 8.018 | 0.262 | 8.018 | 0.262 | Supported | |

| ICS → EP | 2.933 | 0.314 | 2.933 | 0.314 | Supported | ||

| SQ2 → EP by ICS | 0.082 | Supported Partially mediated | |||||

| SQ2 → EP | 8.439 | 0.284 | 8.439 | 0.633 | Supported |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jarah, B.A.F.; Zaqeeba, N.; Al-Jarrah, M.F.M.; Al Badarin, A.M.; Almatarneh, Z. The Mediating Effect of the Internal Control System on the Relationship between the Accounting Information System and Employee Performance in Jordan Islamic Banks. Economies 2023, 11, 77. https://doi.org/10.3390/economies11030077

Jarah BAF, Zaqeeba N, Al-Jarrah MFM, Al Badarin AM, Almatarneh Z. The Mediating Effect of the Internal Control System on the Relationship between the Accounting Information System and Employee Performance in Jordan Islamic Banks. Economies. 2023; 11(3):77. https://doi.org/10.3390/economies11030077

Chicago/Turabian StyleJarah, Baker Akram Falah, Nidal Zaqeeba, Mefleh Faisal Mefleh Al-Jarrah, Abdalla Mohammad Al Badarin, and Zeyad Almatarneh. 2023. "The Mediating Effect of the Internal Control System on the Relationship between the Accounting Information System and Employee Performance in Jordan Islamic Banks" Economies 11, no. 3: 77. https://doi.org/10.3390/economies11030077

APA StyleJarah, B. A. F., Zaqeeba, N., Al-Jarrah, M. F. M., Al Badarin, A. M., & Almatarneh, Z. (2023). The Mediating Effect of the Internal Control System on the Relationship between the Accounting Information System and Employee Performance in Jordan Islamic Banks. Economies, 11(3), 77. https://doi.org/10.3390/economies11030077