1. Introduction

The term “FinTech” pertains to a type of technology that has emerged alongside novel financial practices, such as using credit cards and other financial services. This technology has been in existence for a considerable period and continues to advance, hence its appellation as “FinTech.” Presently, some of the most prevalent examples of this technology include mobile wallets, payment applications, automated investment advisors, and financing platforms for non-traditional funding alternatives (

Huei et al. 2018;

Koroleva 2022).

The growth of mobile payment systems is staggering, indicating that it is a rapidly expanding industry of significant importance to consumers. Non-financial institutions are now offering these services, which are gaining popularity due to their ease of use and absence of complex add-ons. Users are only required to enter their login information, PIN number, or biometric authentication, making the process effortless (

Lim et al. 2019). An essential initial stride towards fully unlocking the boundless potential of this sector entails the timely embracement of FinTech payment services. Ultimately, the continued use of these services by consumers will determine their long-term success. Despite the extensive digitization of the banking system, mobile payment services have not been widely adopted due to various regulatory and marketability challenges (

Lee and Ahn 2016;

Park and Lee 2013). However, the popularity of online shopping and the widespread availability of mobile devices has contributed to the rapid growth of the digital mobile payment industry in recent years (

Thakur and Srivastava 2014;

Dahlberg et al. 2015;

Perez et al. 2018;

Yang et al. 2012). The mobile payment industry is experiencing a remarkable surge, with tremendous potential for growth (

Trapanese and Lanotte 2023). According to a study conducted by (

Allied Market Research 2020), the global mobile payment market initially projected to reach a value of USD 1.48 trillion in 2019, is expected to soar to an astonishing USD 12.06 trillion by 2027, exhibiting a remarkable compounded annual growth rate of 30.1% from 2020 to 2027. This tremendous expansion can be attributed to two key factors: the widespread adoption of smartphones on a global scale and the flourishing mobile commerce market, particularly in developing economies. This exponential growth, marked by an impressive average annual rate of 38%, embodies immense potential and promises a prosperous future for this burgeoning sector. This growth is driven by the increasing usage of mobile payments by consumers. In 2016, Capgemini estimated that non-cash transactions worldwide had increased 8.9% in 2014 to 387.3 billion (

Capgemini 2016). The demand for dependable, quick payment solutions will increase in 2023 as the mobile payment market is anticipated to continue expanding in the coming years. The usage of digital wallets offered by BigTechs has significantly increased from 6.5% in 2019 to 44.5% in 2020, as reported by the

Financial Stability Board (

2022). This indicates a rise in the popularity and ease of online transactions.

FinTech, a type of technology that enhances access to financial services, has the potential to revolutionize how people manage their finances. By making financial services more transparent, cheaper, and more accessible, FinTech is particularly beneficial to individuals with limited time for financial management (

Lee and Shin 2018;

Zavolokina et al. 2016). The landscape of financial technology has undergone a sweeping transformation due to the integration of pivotal technologies, including but not limited to internet technology, big data, artificial intelligence, distributed technology, and security technology leveraging biometric authentication (

Allioui and Mourdi 2023). This confluence of powerful tools has ushered in a new era of sophistication, enabling businesses to operate with unprecedented efficiency and security while empowering individuals to make informed financial choices with ease and confidence. These technologies have brought about significant changes in the conventional financial sector development model (

Ediagbonya and Tioluwani 2023). Consumers can now easily access financial services through Internet technologies (

Ruan et al. 2019). Big data enables better risk evaluation and fraud detection (

Chen et al. 2017). Artificial intelligence allows for accurate forecasts and automated financial operations (

Belanche et al. 2019). Security technology has improved the security of financial transactions (

Gai et al. 2018;

Fosso Wamba et al. 2020), and distributed technology provides a decentralized and secure means of exchanging value (

Belanche et al. 2019;

Gomber et al. 2018;

Chen et al. 2019;

Fosso Wamba et al. 2020;

Miau and Yang 2018). Overall, these developments have improved the efficiency, accessibility, and security of financial services. Banks are also idopting FinTech to tap into its commercial value. In the second quarter of 2019, FinTech saw a significant investment of USD 8.3 billion, representing a 24% increase from the first quarter (

CB Insights 2019). FinTech’s widespread adoption creates a more diversified financial landscape, providing access to innovative financial services to people (

Demertzis et al. 2018;

Imerman and Fabozzi 2020). The adoption of FinTech services by customers may be hindered by their concerns over security and privacy. Although there are many affordable financial service platforms and user-friendly features available, consumers are hesitant to trust FinTech companies with their personal and financial information due to the risk of unauthorized access or misuse (

Lim 2016). McKinsey and Company has reported that these concerns pose a significant obstacle to the further growth of FinTech services (

Lee and Ahn 2016). As such, it is essential for FinTech companies to address these concerns by implementing robust security and privacy measures to ensure the protection of their customer’s sensitive information.

The expansion of the mobile payment market has led to various security concerns that need to be addressed (

Park and Jang 2014;

Liang et al. 2014). It is crucial to identify the security needs and difficulties associated with mobile FinTech payment methods in order to develop a practical and secure service. Several research studies have been conducted on mobile payments and security to ensure that such services can be safely offered (

Smalley and Craig 2013;

Li and Clark 2013). Have proposed security techniques and outlined security characteristics for different types of mobile payments. Linck et al. have suggested a security standard that caters to the customer’s security concerns by analyzing and investigating mobile payment security issues from the consumer’s perspective (

Kadhiwal and Zulfiquar 2007;

Linck et al. 2006).

Within the realm of FinTech, there is a prominent focus on the advancement and implementation of mobile payment technologies, along with the associated concerns regarding security and privacy. The extensive use of mobile payment technology has led to a significant increase in digital financial transactions, bringing both advantages and disadvantages to consumers and the financial industry. This research intends to explore the potential of mobile payment services to revolutionize financial management while also identifying the challenges that need to be addressed to ensure their long-term success. Furthermore, this study will examine the regulatory and marketability obstacles that must be overcome for the advancement of these services. Moreover, this study aims to explore the intricate matters of security and privacy that could potentially impede the widespread acceptance of mobile payment services and present compelling remedies to overcome these challenges. By addressing these critical issues, our study seeks to offer a thorough comprehension of the present state of mobile payment technology in the FinTech sector, as well as its potential for future progress and ingenuity. Furthermore, we aim to present actionable solutions to overcome any obstacles that may arise.

The motivation behind conducting the study on FinTech stems from the increasing importance of technology-driven financial services and the evolving landscape of digital transactions. With the rapid integration of FinTech solutions into everyday financial activities, understanding the factors that influence customer adoption becomes critical. By delving into the dynamics of Perceived Security (PS), Perceived Risk (PR), Perceived Trust (PT), and Customer Intention to Adopt (CIA) within the FinTech domain, the study seeks to provide valuable insights for both researchers and industry practitioners. Through a thorough examination of this complex interplay, our research endeavors to provide invaluable support in formulating pragmatic strategies to bolster consumer trust and promote a wider adoption of FinTech offerings. Ultimately, our study aspires to inspire the advancement of FinTech solutions that exude an air of accessibility, security, and user-friendliness while seamlessly adapting to the ever-evolving needs of customers in our contemporary digital realm. This study addresses a notable research gap by comprehensively analyzing the combined impact of Perceived Security, Perceived Risk, Perceived Trust, and Customer Intention to Adopt within the FinTech adoption process. Previous studies have often focused on specific aspects of FinTech adoption, neglecting the intricate interactions between these crucial elements (

Shiau et al. 2020). By elucidating how Perceived Security, Perceived Risk, and Perceived Trust collaborate to influence customers’ intentions to adopt FinTech products and services, this study effectively bridges this knowledge gap. This research contributes to a more nuanced understanding of the factors influencing FinTech adoption by identifying the interconnected dynamics among these variables, offering valuable insights for both academia and industry professionals in the ever-evolving FinTech landscape.

2. Theoretical Background and Hypothesis Development

2.1. Perceived Security

The level of assurance individuals have in the security of their personal data during mobile payment transactions is referred to as Perceived Security, as defined by

Fan et al. (

2018). It pertains to safeguarding against cyber threats, such as hacking and unauthorized access to financial and personal data (

Dwivedi et al. 2022). To enhance Perceived Security, mobile payment service providers continuously monitor user data in real-time, regularly audit their applications, and evaluate the privacy and connection of wireless and wired networks, as emphasized by

Zhang and Kim (

2020) and

Lim et al. (

2019), without compromising user privacy. Service providers are not only required to provide digital security but also need to create a user-friendly mobile payment environment, facilitate interaction with customer service, and deliver superior customer service (

Arcand et al. 2017). The functionality of a mobile payment system can be improved by providing a high level of Perceived Security, particularly in terms of users’ belief in the ability of the payment provider to protect their personal data (

Chen et al. 2017). Providers of mobile payment services ensure users’ confidence in the reliability of the payment service by regularly monitoring their platforms and private data (

Lim et al. 2019). Enhancing consumer trust by mitigating security risks and promoting digital safety and security can increase the adoption of financial services through mobile technology, Suggest that customers’ intention to use mobile payments or e-banking is positively affected by their perception of Perceived Security. Usefulness is based on the security in determining a consumer’s intention to adopt a product. According to the findings of this study, it refers to how strongly a consumer thinks a product will have an effect on how well they perform. According to Huei et al. 2018, Perceived Security is a crucial factor in determining consumers’ intention to adopt a product. Previous studies have shown a positive correlation between perceived usefulness and consumers’ intention to adopt a product, including FinTech services (

Al-Fahim 2016;

Chuang et al. 2016;

Lee 2016;

Lim and Cham 2015). Self-efficacy, or one’s belief in one's ability to use a product if it is secured, has been identified as a key predictor of Perceived Security in the context of mobile banking (

Alalwan et al. 2016). Additionally, research by

Chen et al. (

2011) found that self-efficacy with smartphones positively influences the perceived utility of those devices. As mobile devices have become increasingly popular for accessing FinTech services, it is likely that consumers’ intention towards these services will improve as they perceive them to be more valuable and accessible. A study by

Chuang et al. (

2016) found that customers’ intentions to adopt FinTech products were strongly correlated with Perceived Security. This emphasizes the need to create FinTech services that are simple to use and provide customers with clear advantages. By doing so, FinTech companies can increase the Perceived Security of their products and improve overall consumer intention towards the industry. Based on the aforementioned arguments, this study proposes the following hypothesis:

Hypothesis 1 (H1). Perceived Security has a positive effect on the customer’s intention to adopt FinTech products.

2.2. Perceived Risk

When considering the adoption of FinTech, consumers need to evaluate the Perceived Risks associated with it.

Ryu (

2018a) discusses Perceived Risks related to goods or services discovered through research on the use and adoption of innovations. Since 1960, Perceived Risk has been studied to determine its relationship with human behavior (

Damghanian et al. 2016). Risk is an action that results in a choice with both positive and negative consequences (

Yang et al. 2015). Users’ attitudes toward risk can be expressed in various ways, such as awareness of the potential harms associated with usage (

Damghanian et al. 2016). Risk is crucial in both safety and finance (

Yang et al. 2015;

Hansen et al. 2018;

Hu et al. 2019). FinTech has significantly increased the accessibility, virtualization, and remote transactions of contemporary banking services, as well as real-time investment and the financial industry’s reliance on information technology and the Internet (

Jagtiani and John 2018;

Brummer and Yadav 2018;

Anagnostopoulos 2018;

Senyo and Osabutey 2020). However, technical flaws in Internet businesses can result in information technology risks such as data theft, privacy invasion, and Internet site threats, which can lead to significant financial losses for both consumers and businesses (

Odinet 2017;

Hinson et al. 2019;

Arner et al. 2016;

Abdul-Rahim et al. 2022).

The rapid rise of the FinTech industry has significantly impacted traditional financial companies, resulting in changes in non-traditional financial businesses’ terms, credit, income, and risk conversions (

Dapp et al. 2014;

Gomber et al. 2018;

Buchak et al. 2018). The risk aspects of the financial sector as a whole have also been significantly altered (

Zetsche et al. 2017). Perceived Risk is an important factor to consider when examining the factors influencing FinTech adoption due to the risk characteristics of financial products.

Thakur and Srivastava (

2014) found that people’s perceptions of risk significantly impact the adoption of mobile payments, a finding further supported by

Slade et al. (

2015).

De Luna et al. (

2019) investigated the elements involved in using various utilizations of mobile payment platforms and their significant impact on customers’ perception of security in shaping their inclination towards their usage. The biggest barriers to adopting FinTech platforms are the risks associated with finance and the unpredictability of e-commerce. Based on the aforementioned arguments, this study proposes the following hypothesis:

Hypothesis 2 (H2). Perceived Risk has a positive effect on the customer’s intention to adopt FinTech products.

2.3. Perceived Trust

Perceived Trust is a complex and multifaceted phenomenon that significantly impacts corporate relationships (

Stewart and Jürjens 2018;

Jena 2023). When it comes to adopting FinTech innovations, cultural factors, continuous wireless connectivity, smartphone accessibility, payment security, and organizational credibility all influence trust, according to

Whitman and Mattord (

2009). In addition to people, technology is also trusted, which can alter people’s behavior and decision-making about its use (

Cao et al. 2018;

Smith 2010;

Kuriyan et al. 2010;

Kuriyan and Ray 2009). Trust is a crucial factor in technology-related studies (

De Visser et al. 2016), particularly when people depend on technology (

Ali et al. 2021). The fundamental concern of users is to have a solid foundation of trust in all engagements, including the use of FinTech (

Wu et al. 2016). Effective communication to build relationships is critical for businesses to enhance user confidence (

Malaquias and Hwang 2016). A different study shows that consumers’ trust in FinTech products and services significantly impacts their adoption intentions (

Moon and Kim 2016;

Wu et al. 2016;

Malaquias and Hwang 2016;

Agag and El-Masry 2017;

Damghanian et al. 2016). The notion of user-friendliness as a determinant of trustworthiness assumes a pivotal position in influencing the embrace of FinTech innovations, specifically within the realm of mobile banking. This refers to how easily or conveniently users perceive a particular technology to be compared to others, even when operating under time constraints.

Lee and Shin’s (

2011) study found that technological readiness and expertise are directly linked to the ease of use of mobile banking. Applications that are user-friendly and easy to navigate are often more appealing to users and are more likely to retain their usage in the long term (

Widyastuti and Anggraeni 2017). In contrast, consumers may grow frustrated and stop using a program if it is extremely complicated and challenging to use. Furthermore, simplicity in design and functionality is generally considered more advantageous to the user experience (

Anjelina 2018;

Heryani et al. 2020). Therefore, a well-designed and easily understandable technology would impact consumer intention and promote its adoption. This emphasizes the importance of user-centric design in the progress of FinTech technology. As the FinTech industry continues to grow and evolve, it is important for technology developers to prioritize ease of use as a critical factor in increasing adoption and driving customer satisfaction (

Kim et al. 2015). Based on the aforementioned arguments, this study proposes the following hypothesis:

Hypothesis 3 (H3). Perceived Trust has a positive effect on the customer’s intention to adopt FinTech products.

2.4. Customer Intention to Adopt

Satisfaction leads to Customer Intention to Adopt, which is an emotional response that occurs when individuals compare their intentions and outcomes, according to

Paul et al. (

2016). Customer satisfaction, resulting from a positive customer experience, can significantly influence future purchasing decisions, as per

Dai et al. (

2015). Customer loyalty is a key outcome of customer satisfaction (

Marinkovic and Kalinic 2017;

Anshari et al. 2021). The extent of customer satisfaction plays a vital role in determining whether existing customers will make repeat purchases or use the services again in the future (

Daragahi 2017). A company’s ability to compete and thrive in its industry is primarily influenced by customer satisfaction with its goods or services (

Alwi et al. 2019). Numerous studies have demonstrated that satisfied customers tend to purchase more frequently and are less sensitive to price fluctuations, which can reduce future transaction costs (

Jannat and Ahmed 2015). When the execution of a product or service does not meet customer expectations, dissatisfaction arises (

Armstrong et al. 2014). Customer satisfaction leads to the development of strong brands and successful relationships (

Eshghi et al. 2007). Businesses with satisfied customers have an edge over their competitors, including higher earnings, lower entry barriers, and reduced costs (

Zhang and Luximon 2021). Based on the aforementioned arguments, this study proposes the following hypothesis:

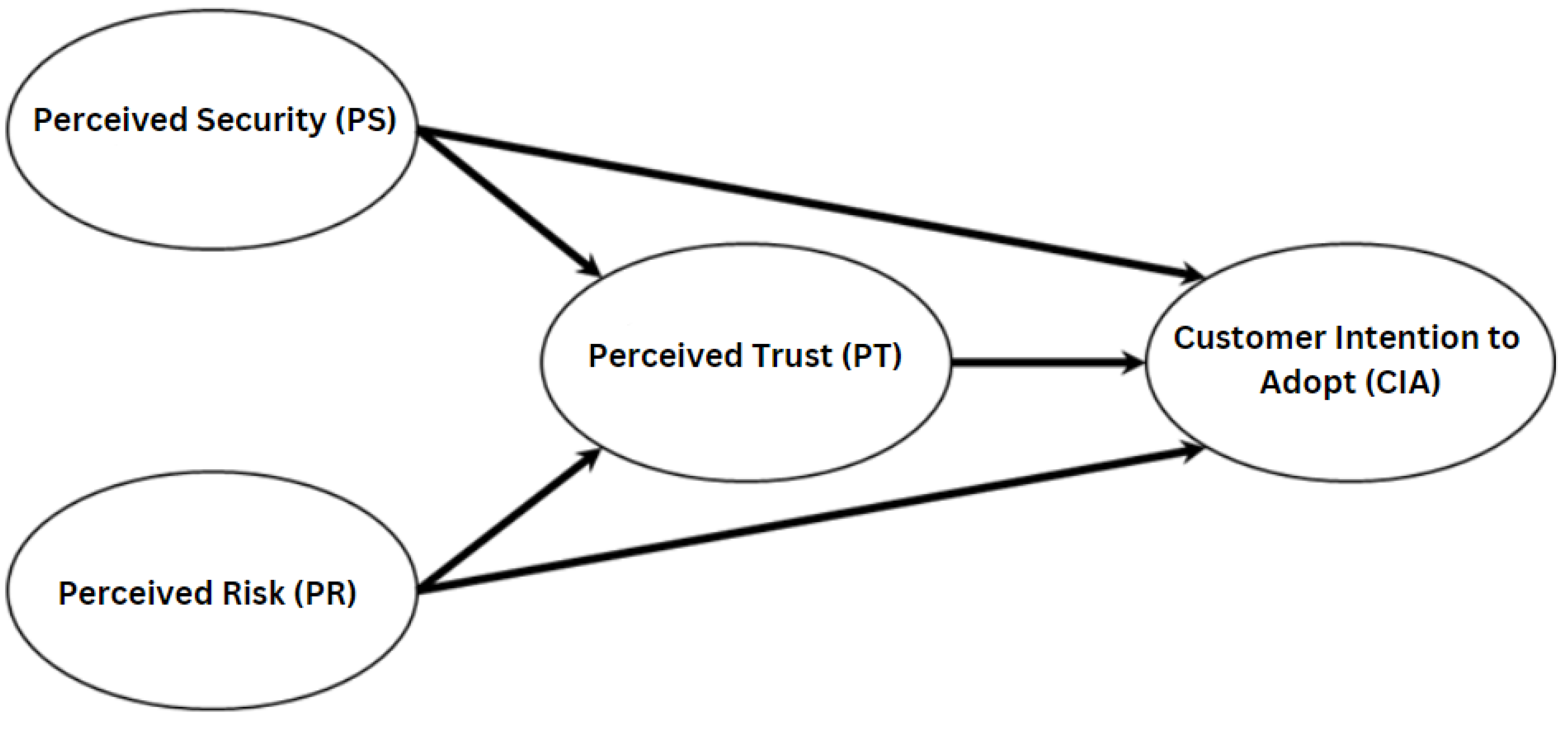

Hypothesis 4 (H4). Perceived Trust mediates the relationship between Perceived Security and the Customer’s Intention to Adopt FinTech products.

Hypothesis 5 (H5). Perceived trust mediates the relationship between Perceived Risk and the Customer’s Intention to Adopt FinTech products.

With this said, the relationship can be better exhibited through

Figure 1 as given below:

Based on previous theoretical foundations, scholars have analyzed the adoption and utilization of FinTech services by applying various theoretical frameworks, such as the unified theory of acceptance and use of technology (UTAUT) (

Dzogbenuku et al. 2022), the trust transfer theory and the technology acceptance model (TAM) (

Bommer et al. 2023;

Ryu 2018b). Nonetheless, previous research did not comprehensively investigate all facets of consumer intention. To learn more about what customers want to achieve by embracing and using FinTech services, more research is required. Despite the increasing popularity of such services in countries like Malaysia (

Alam et al. 2021), Saudi Arabia (

Abubotain and Chamakiotis 2021), and Indonesia (

Yang et al. 2021), there is limited research on these concerns in various cultural contexts. Additionally, little research has been conducted on the adoption and usage of FinTech services in developing economies (

Rehman et al. 2021). As a result, additional research is required to pinpoint the elements that affect consumers’ adoption of and use of FinTech services, particularly in emerging nations. To meet the rising demand, several research studies have examined how FinTech services are adopted and used. According to this research (conducted by

Nangin et al. 2020;

Hu et al. 2019;

Ali et al. 2021), a number of variables, including perceived utility, usability, and risk, affect customers’ propensity to utilize FinTech services. Some studies have also looked at how elements like trust, social influence, and perceived behavioral control affect consumers’ intentions to adopt FinTech services (

Yang et al. 2021). The research’s overall goal is to better understand the variables that affect consumers’ intention to adopt and use FinTech services in various cultural contexts, particularly in developing nations.The prior studies/extracts are given in the

Table 1 below:

3. Research Methodology

Our study sought to ascertain the extent to which customer perceptions and intentions regarding FinTech offerings are shaped by considerations of risk perception, security, and trustworthiness. The primary objective of this research was to explore the impact of various factors within the post-COVID-19 landscape on customers’ intention to use FinTech products and services. A quantitative approach was employed, utilizing a standardized questionnaire to gather data from FinTech users within the targeted demographic. By employing a cross-sectional survey methodology, we were able to capture a snapshot of participants’ viewpoints and experiences, offering valuable insights at a specific point in time.

The research centered around individuals in a specific area who engage with FinTech, specifically those who regularly utilize e-wallets, mobile banking, or other FinTech services. To ensure a diverse representation of users within this demographic, convenience sampling was employed to select participants. A well-designed questionnaire was employed to gather information on crucial elements such as Perceived Trust, security, and risks associated with FinTech offerings. In order to ensure utmost clarity and comprehension, the survey was formulated in English and subsequently translated into the native language of the target audience. Its purpose was to gather comprehensive data pertaining to participants’ demographics, viewpoints, and behavioral inclinations regarding the embrace of FinTech solutions. Through intimate and personalized discussions over a six-month duration, we carefully selected participants using a convenience sampling method (

Stratton 2021). To confirm that the survey questionnaire was appropriate and accurate, a preliminary test consisting of fifty respondents was conducted. When creating the concluded edition of the questionnaire, all suggestions for phrasing and informational modifications were taken into account. By exclusively focusing on individuals within this specific demographic, we aimed to maintain a harmonious alignment with the regional cultural context. Consequently, our study encompassed a final sample size of 405 meticulously curated responses, carefully chosen from a pool of 496 potential participants.

The study was conducted in a carefully selected geographic region renowned for its burgeoning FinTech industry and increased digital engagement in the wake of the COVID-19 pandemic (

Table 2). City-wide data have a fair representation of the total data collection. The decision to focus on this location was guided by the remarkable rate of digital assimilation and the widespread utilization of FinTech services within the local community. The data that were obtained underwent thorough analysis utilizing appropriate statistical methodologies, including regression analysis and structural equation modeling (SEM) (

Kline 2015). This thorough examination aimed to explore the intricate connections between Perceived Trust, security, risks, and the inclination of consumers to utilize FinTech products and services. In this particular FinTech context, the analysis provided invaluable insights into the factors that influence customer intention and adoption patterns.

The study adhered to a set of rigorous ethical guidelines, upholding the highest standards of participant confidentiality, voluntary engagement, and well-informed consent. At every stage of the research process, appropriate measures were implemented to safeguard the privacy of participants and the security of their data. The study has acknowledged several constraints that may have restricted the generalizability of the findings, such as the utilization of convenience sampling, the limited geographical scope, and the specific context involved. However, it is crucial to emphasize that these limitations were fairly considered while assessing the data and drawing conclusive remarks. Reliability tests show the constructs outcomes: (Perceived Security): -CronbachAlpha-0.887, (Perceived Risk): -CronbachAlpha-0.881, (Perceived Trust): -CronbachAlpha-0.870, and (Customer Intention to Adopt): CronbachAlpha-0.853. All Cronbach alphas of the value constructs are greater than 0.80. The demographic structure of the surveyed respondents is presented in

Table 3:

4. Findings and Analysis

4.1. EFA, CFA, and Model Fit

Exploratory factor analysis (EFA) was applied to 17 items to generate factors. The approximate Chi-square statistic is 3188.655 with 105 degrees of freedom, which is significant at the 0.05 level. The value of the Kaiser–Meyer–Olkin statistic is 0.908 and is also large and greater than 0.5. The relationships between the retrieved constructs and their attributes are shown in

Table 4, together with the weighted values that these attributes attained. The construct “Perceived Security” is created by combining the initial three features, which represent the opinions of consumers and are shown in the table. In a similar way, the construct “Perceived Risk” is created by adding the three attributes listed below, which represent how dangerous consumers are contributing to the environment. In addition, “Perceived Trust” is a collection of eight more features that offer ideas for how to begin developing trust. “Customer Intention to Adopt” applies to the last three criteria demonstrating customers’ desires to use FinTech products.

EFA was followed by confirmatory factor analysis (CFA). The AVE of each idea was greater than 0.5, according to

Fornell and Larcker (

1981), showing high convergent validity. The square root of the AVE surpassed the performance of every link, proving the constructs’ individuality (

Table 5).

The model fit indices are given below in

Table 6.

Even if the difference in values may be disregarded since it is minor and lowered even more, all the structures and objects are considered essential and are thus kept in the model and not removed. The discriminant validity of these variables and covariates was also assessed using the

Henseler et al. (

2014) test using HTMT at a threshold of 0.85.

The model’s discriminant validity was found to be supported by the finding that all of the constructs were over the cut-off. Sobel tests (

Baron and Kenny 1986;

Sobel 1982) were carried out to evaluate the effects of PT as a mediator on the connection based on the assumptions. The results are provided in

Table 7.

The statistical significance of the indirect links was also examined separately and in the structural diagram using AMOS, and parallels to the Sobel test for mediation were identified.

According to the measurement model in the software AMOS 25,

Table 5 lists the model fit indices, all of which were found to be satisfactory. The evaluation of the precision with which these models represented the data was conducted using a combination of absolute fit measures, such as the two statistics and the goodness-of-fit index (GFI), and incremental fit indicators, such as the comparative fit index (CFI) and the root mean square error of approximation (RMSEA). This comprehensive assessment ensured a thorough and reliable analysis. According to

Medsker et al. (

1994), values >0.95 are regarded as having a good match for GFI and CFI, while values >0.90 are regarded as having an acceptable fit. For the RMSEA,

Browne and Cudeck (

1992) determined that values under 0.05 were great fits, values between 0.05 and 0.08 were acceptable fits, values between 0.08 and 0.10 were marginal fits, and values over 0.10 were bad fits. The Chi-square in the model has a

p-value below 0.05 and is significant (

Wheaton et al. 1977).

Bentler (

1995) asserts that GFI and CFI should be more than 0.90 and closer to 1. The model fit indices (RMSEA, SRMR, and CFI) meet the threshold requirements (

Barrett 2007). According to

Byrne (

2010) and

Diamantopoulos et al. (

2000), well-fitting models frequently produce values below 0.05 for the SRMR, which has values between 0 and 1. The findings for different models are suitable because they are near 0.05. The RMSEA is satisfactory at 0.08 based on the most current standard (

Hu and Bentler 1999;

Steiger 2007), and the model fits the data rather well.

4.2. Mediation

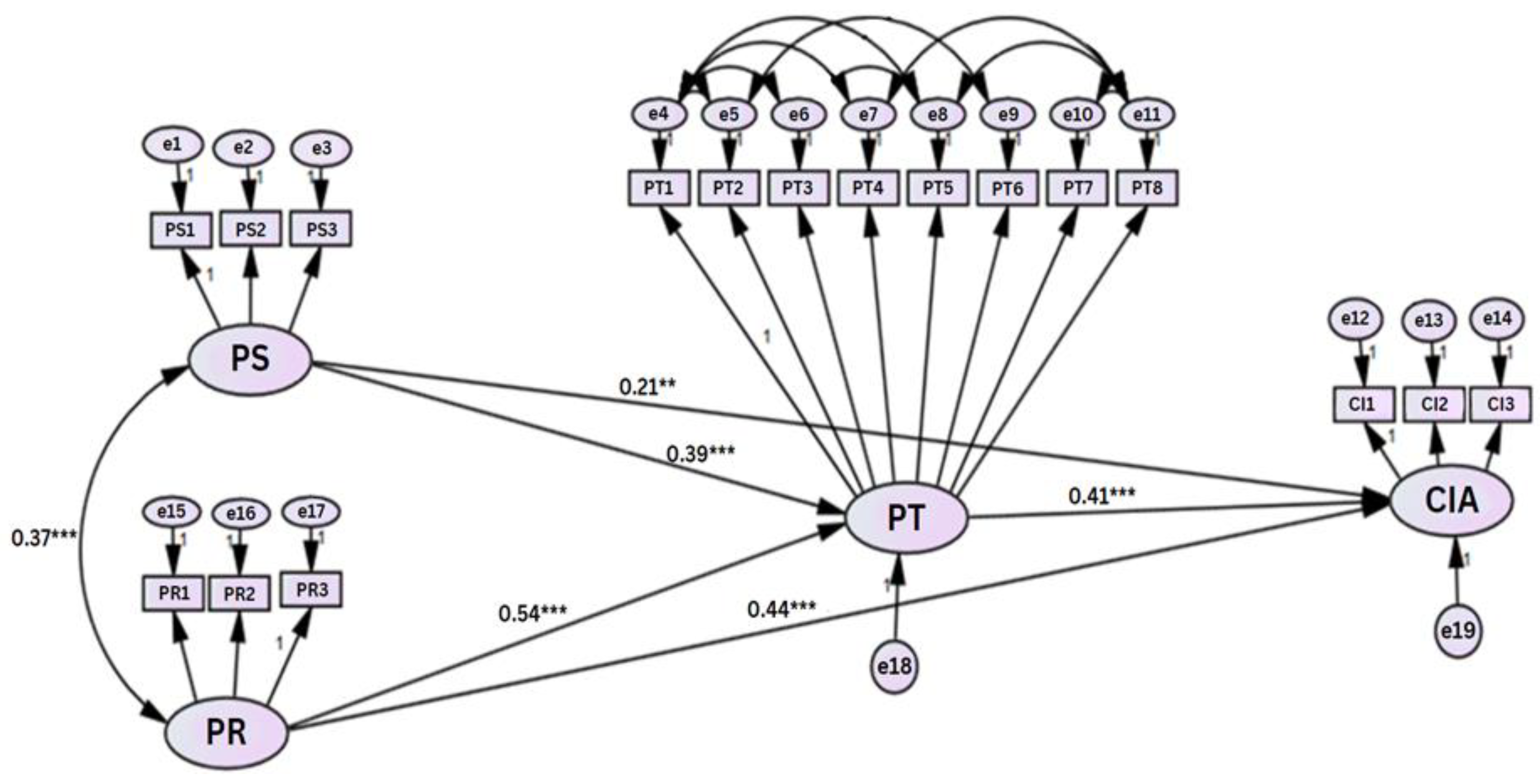

In

Table 8 and

Figure 2, the structural correlations are displayed. According to the results of the Sobel tests, there are favorable mediation effects between PT and CIA as well as PS and CIA via PT. The Sobel test for mediation’s statistical significance (

Table 8) was found to be comparable to that of AMOS. The link between PR and CIA is discovered to be positively mediated by PR → PT → CIA [H4: β = 0.159 (

p < 0.01)]. The link between PS and CIA is discovered to be positively mediated by PS → PT → CIA [H5: β = 0.221 (

p < 0.01)].

5. Discussion

The outcomes of this research offer an understanding of the determinants that shape customers’ intention towards the adoption of FinTech products and services. The study was well constructed upon a robust theoretical foundation, with the hypotheses formulated around the relevant variables of Perceived Trust, Perceived Security, and Perceived Risks. These variables have been recognized in previous studies as paramount factors that significantly impact customers’ acceptance of innovative financial technological offerings (

Meyliana and Fernando 2019;

Nangin et al. 2020).

The findings of this research affirm the belief that customers’ inclination to embrace FinTech products and services is significantly influenced by their level of trust in them (

Al Nawayseh 2020). This aligns harmoniously with previous studies that have underscored the pivotal role of trust in shaping consumer adoption intentions toward technology. Essentially, this study divulges that individuals are more inclined to embrace FinTech offerings when they possess unwavering faith in the companies offering these services, the technological innovations employed, and the stringent security measures in place. Consequently, it becomes imperative for the FinTech industry to prioritize effective communication, robust security controls, and a sterling organizational reputation in order to heighten adoption intentions and foster enduring trust with consumers.

The results of the study lend support to the hypothesis that customers’ intention to adopt FinTech products and services is augmented by their perception of security. This is in line with prior research that emphasizes the significance of security in mobile payment transactions (

Hwang et al. 2021). The findings imply that customers are more inclined to avail of FinTech products and services when they have confidence that their personal and financial data are protected during transactions. To improve customers’ perception of security and boost their adoption intentions, FinTech firms should give top priority to implementing stringent security measures, real-time monitoring systems, and user-friendly privacy policies.

The study proposes the hypothesis that the customer’s intention to adopt and use FinTech products is adversely affected by the level of Perceived Risk. This suggests that customers may not be as inclined to embrace FinTech offerings if they perceive greater risks associated with them (

Tang et al. 2020). Financial technology companies must take into account consumers’ concerns about Perceived Risk and address them through strong safety measures, effective communication, and transparency. To encourage customers to adopt FinTech products, companies should educate them about the security measures in place and provide clear information on how their data and information are protected. Furthermore, FinTech firms must continuously evaluate any risks associated with their products and take the necessary steps to mitigate them in order to gain the trust and confidence of potential customers.

The study’s findings supported the last hypothesis, which postulated that customer satisfaction is a key factor in the uptake of FinTech goods and services. Consumer satisfaction must be improved by a variety of means, including quick and easy transactions, quick access to financial data, and individualized services (

Rani 2021). This improvement is essential to the success of FinTech goods and services. A happy client is more inclined to make further purchases, show brand loyalty, and share favorable word-of-mouth promotions. Additionally, happy consumers play a crucial role in building powerful brands and fruitful connections, both of which eventually boost client acquisition and retention. Customer satisfaction and ongoing use of their solutions are two ways that FinTech companies might achieve financial success.

The study’s results highlight the importance of consumers’ perceptions of usefulness, ease of use, trustworthiness, security, risks, and satisfaction in their decision to adopt FinTech products and services. These findings are valuable for both FinTech companies and governments in designing and promoting FinTech offerings that are perceived as beneficial, user-friendly, trustworthy, and secure to encourage adoption. Future research could investigate other factors that may impact consumer adoption of FinTech offerings or examine the relationships between these factors and adoption intentions in different contexts.

6. Theoretical Implications

The theoretical implications of the current study provide valuable insights into the ever-evolving nature of customers’ security perceptions and their profound impact on their willingness to embrace FinTech products and services. Previous research has consistently emphasized the pivotal role of Perceived Security in shaping users’ emotional and cognitive responses toward adopting novel technologies (

Lim et al. 2019;

Wendy Zhu and Morosan 2014).

Building upon this foundation, the current research expands our understanding of users’ behavioral intentions and their perception of security within the specific realm of mobile FinTech services. This study contributes to a more comprehensive grasp of the intricate relationship between these security characteristics and consumers’ perspectives by delineating the nuanced interplay between them. It is crucial to recognize that security in the FinTech landscape encompasses various dimensions. Moreover, this study underscores the significance of Perceived Security in fostering sustained engagement with FinTech services. It elucidates the vital role that consumers’ trust in the reliability and stability of mobile FinTech services plays in shaping their inclination to adopt. By illuminating the direct impact of users’ Perceived Security on their propensity to continue utilizing the system, this research significantly advances previous studies and establishes a clear correlation between users’ long-term involvement and their perception of security.

The present research adds a significant enhancement to our understanding of the intricate dynamics of trust and its impact on customers’ intentions to adopt and embrace FinTech products and services. Extensive previous research has consistently demonstrated the pivotal role that trust plays in shaping individuals’ attitudes and behaviors toward technology adoption (

Ali et al. 2021). Notably, past studies have underscored the indispensable nature of trust in fostering strong customer relationships and driving the adoption of technological innovations. Trust is regarded as a fundamental element, instilling a sense of reliability and assurance in service providers (

Cao et al. 2018;

Smith 2010;

Dahiyat et al. 2011).

Building upon this foundation, the present study delves into the intricate attributes of trust within the specific realm of FinTech implementation. By contributing to a more comprehensive understanding of the factors that shape users’ perspectives and decisions toward adoption, this study elucidates the intricate interplay between users’ trust in technology and the reliability of FinTech platforms. Moreover, this study enriches the existing body of knowledge by underscoring the pivotal role trust plays in mitigating the risks associated with FinTech transactions and bolstering user confidence in the security and dependability of the technology. The study accentuates the significance of cultivating robust relationships between FinTech companies and customers, underscoring the indispensable role trust plays in fostering user adoption intentions (

Wang et al. 2015). The study’s findings underscore the importance of trust at various stages of the transaction process, from the initiation of payment to the merchant’s receipt, and also shed light on the intricate process of cultivating trust within the FinTech ecosystem.

Furthermore, this study presents a significant advancement in our understanding of the impact of Perceived Risks on individuals’ intention to adopt FinTech goods and services. For quite some time, Perceived Risk has been recognized as a prominent obstacle hindering financial engagement, impeding consumers from acting upon their intentions and making purchases (

Xie et al. 2021). Expanding on this groundwork, the present study offers a comprehensive comprehension of the intricate interplay between uncertainty and individuals’ apprehensions regarding unfavorable consequences associated with the utilization of FinTech goods and services.

In addition, this research contributes to the existing body of literature by shedding light on the significant role that Perceived Risk plays in deterring the acceptance of new technologies (

Amirtha et al. 2020), particularly in the realm of e-commerce and financial transactions (

Chong 2013). As

De Luna et al. (

2019) assert, the study underscores the crucial influence of risk perception on users’ decision-making and willingness to adopt these technologies. Furthermore, it underscores the growing apprehension among consumers regarding the potential threats to security and privacy associated with conducting financial transactions through mobile devices. By examining the intricate connection between individuals’ risk perceptions and their intentions to utilize FinTech platforms, this study deepens our comprehension of the factors that impact user decisions and impede the widespread utilization of FinTech products and services. Moreover, this study underscores the utmost significance of adept handling and alleviating Perceived Risks to foster trust among consumers and promote the adoption of FinTech platforms. It sheds light on the paramountcy of implementing robust risk management tactics and stringent security measures to assuage users’ apprehensions and bolster their faith in the reliability and safety of FinTech offerings. By acknowledging the pivotal role that risk perception plays as a precursor that detrimentally impacts adoption intentions, this study underscores the vital need for effective risk mitigation strategies.

7. Practical Implications

Emphasize ease of use: In the realm of FinTech product and service development, placing utmost importance on user-friendliness and simplicity is paramount. Achieving this objective entails streamlining functionality, refining the user interface, and providing unambiguous instructions that effortlessly guide customers in utilizing these services. By offering sufficient guidance, comprehensive instructions, and dependable customer support, we can greatly enhance customers’ perception of ease of use and their inclination to embrace and make the most of our offerings. By ensuring a seamless and hassle-free user experience, FinTech companies can profoundly elevate customer satisfaction and cultivate enduring loyalty.

Build and maintain trust: The trust that consumers have in FinTech products and services is a crucial factor that influences their decisions. Therefore, it is vital for FinTech organizations to prioritize trust-building through transparent communication and robust security measures. This requires strict adherence to security protocols and the protection of users’ confidential data while also being open about data utilization. Establishing a reputation for reliability, integrity, and excellence in services will enhance consumer trust and cultivate a positive brand image, resulting in enhanced customer loyalty and sustained business success. By prioritizing trust-building, FinTech companies can develop strong relationships with customers.

Mitigating the Perceived Risks associated with FinTech can have a profound impact on fostering customer trust, as substantiated by the correlation between Perceived Risk and trust (refer to

Figure 1). To accomplish this, organizations ought to direct their efforts towards proficiently handling and mitigating potential risks linked to fraudulent activities, system dependability, and safeguarding data privacy. Employing robust tactics such as transparent and comprehensive risk disclosures, proactive risk management approaches, and exemplary customer assistance holds the potential to assuage consumer apprehensions and bolster trust levels.

The correlation between Customer Intention to Adopt FinTech and their Perceived Trust highlights the importance of building trust. To achieve this, companies should prioritize establishing strong relationships with customers through clear communication, personalized interactions, and reliable customer service. Building trust can be accomplished by providing positive customer experiences, which will ultimately increase the usage of FinTech products and services.

Enhance Perceived Security: Consumers’ readiness to embrace FinTech products is heavily influenced by their perception of security. Therefore, it is paramount for FinTech companies to prioritize the implementation of robust security measures, such as encryption, two-factor authentication, and regular security audits, to safeguard customers’ personal and financial information. FinTech companies must focus on creating and promoting products and services that are viewed as advantageous by their intended audience. This can encourage more people to adopt their FinTech products. Furthermore, it is essential for businesses to maintain transparency by clearly communicating their security protocols, providing concise and easily understandable privacy policies, and educating customers on best practices to ensure their safety while using FinTech products and services. By demonstrating unwavering commitment to security and fostering customer awareness, FinTech companies can establish trust, enhance consumer confidence, and promote the widespread adoption of their offerings.

Stay updated with regulatory requirements: The ever-evolving regulatory landscape surrounding FinTech enterprises demands continuous adaptation and strict adherence to compliance standards and regulations. Ensuring compliance with appropriate rules and regulations can significantly bolster consumer trust in FinTech products and services. As a result, forging partnerships with regulatory bodies can enable businesses to uphold a positive reputation and fulfill legal requirements. By proactively engaging with regulatory authorities and demonstrating a commitment to compliance, FinTech companies can cultivate trust, build credibility, and foster a favorable business environment.

Continuous improvement based on consumer feedback: In order to optimize the quality of their products and services, FinTech companies must actively solicit and incorporate customer feedback as an integral part of their business strategy. Consistent input from users can provide valuable insights that help identify areas for improvement and enable businesses to tailor their offerings to better align with customer preferences and needs. It is imperative for companies to establish effective systems for collecting, evaluating, and implementing customer feedback to ensure the acceptance and success of their FinTech products and services in the market. By proactively engaging with customers and leveraging their feedback, FinTech companies can continuously refine their offerings, cultivate customer loyalty, and maintain a competitive edge.

8. Limitation and Scope of the Future Study

The way the study was performed was very careful and detailed, but there are a few things that might make it less reliable. The people who were chosen to be in the study might not be a good representation of everyone because they were picked based on convenience. Also, the study only looked at people from India who use e-wallets and mobile banking, so we cannot be sure if the findings apply to other people, too. Even though experts helped with translating, there might still be some things that were lost in the translation, which could affect how accurate the survey was. Lastly, because people had to report their own information, they might have answered in a way that was not completely truthful, which could make the results less trustworthy.

9. Conclusions

This research underscores the utmost importance of factors such as Perceived Trust, Perceived Security, and Perceived Risk in shaping consumer behavior in the realm of financial goods and services. These elements have been meticulously examined and thoroughly explored in relation to the factors that influence customers’ intention to adopt FinTech products and services. The empirical findings from this study validate the pivotal role of trust as a significant factor for consumer adoption intentions, underscoring the imperative for FinTech businesses to prioritize the establishment and maintenance of trust through transparent communication and robust security measures. Similarly, the study affirms the criticality of Perceived Security in fostering favorable adoption intentions, highlighting the necessity for FinTech companies to fortify their security measures and implement real-time monitoring systems to bolster customer trust in their offerings. The findings also underscore the impact of Perceived Risks on customers’ intention to adopt FinTech products and services, emphasizing the crucial need for proactive risk mitigation and transparent communication methods to assuage customer apprehensions and foster trust.

Despite the notable contributions this study has made to our comprehension of the factors influencing consumers’ adoption of FinTech products and services, it is imperative to acknowledge the limitations arising from sample selection bias, geographical constraints, potential linguistic translation inaccuracies, and self-report biases. Moving forward, it is crucial for future research endeavors to address and transcend these constraints while also delving into additional variables that may impact consumers’ adoption of FinTech offerings under diverse circumstances.

This study serves as a crucial initial stride towards formulating effective techniques and exemplary approaches for FinTech companies, enabling them to prioritize customer-centric strategies, enhance security protocols, mitigate Perceived Risks, and foster enduring consumer trust. By resolutely tackling these pivotal factors, FinTech companies can establish themselves for sustainable growth, heightened client acquisition, and unwavering triumph in a dynamic and fiercely competitive market landscape.

{kind=link}

{kind=link}