Gender, Perception of Audits, Access to Finance, and Self-Assessed Corporate Tax Compliance

, and

, and

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

3. Methodology

3.1. Data and Sample

3.2. Measurement

3.3. Model Specification

3.4. Data Analysis

4. Results

4.1. Descriptive Statistics

4.2. Verification of Hypothesis

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Alm, James, Liu Yongzheng, and Zhang Kewei. 2019. Financial constraints and firm tax evasion. International Tax and Public Finance 26: 71–102. [Google Scholar] [CrossRef] [Green Version]

- Alrashidi, Rasheed, Diogenis Baboukardos, and Thankom Arun. 2021. Audit fees, non-audit fees and access to finance: Evidence from India. Journal of International Accounting, Auditing and Taxation 43: 1–15. [Google Scholar] [CrossRef]

- Amponsah, Stephen, and Kofi Osei Adu. 2017. Socio-demographics of tax stamp compliance in Upper Denkyira East Municipal and Upper Denkyira West District in Ghana. International Journal of Law and Management 59: 1315–30. [Google Scholar] [CrossRef]

- Arnaboldi, Francesca, Barbara Casu, Elena Kalotychou, and Anna Sarkisyan. 2020. The performance effects of board heterogeneity: What works for EU banks? European Journal of Finance 26: 897–924. [Google Scholar] [CrossRef]

- Bacha, Sami, Aymen Ajina, and Ben Sourour Saad. 2021. CSR performance and the cost of debt: Does audit quality matter? Corporate Governance (Bingley) 21: 137–58. [Google Scholar] [CrossRef]

- Beck, Thorsten, Asli Demirguc-Kunt, and Vojislav Maksimovic. 2004. Bank Competition and Access to Finance: International Evidence. Journal of Money, Credit, and Banking 36: 627–48. [Google Scholar] [CrossRef]

- Beck, Thorsten, Chen Lin, and Yue Ma. 2014. Why do firms evade taxes? The role of information sharing and financial sector outreach. Journal of Finance 69: 763–817. [Google Scholar] [CrossRef] [Green Version]

- Clarke, George R. G. 2021. How do women managers avoid paying bribes? Economies 9: 19. [Google Scholar] [CrossRef]

- D’attoma, John W., Clara Volintiru, and Antoine Malézieux. 2020. Gender, Social Value Orientation, and Tax Compliance. CESifo Economic Studies 66: 265–84. [Google Scholar] [CrossRef]

- Damayanti, Theresia Woro, and Supramono Supramono. 2019. Women in control and tax compliance. Gender in Management 34: 444–64. [Google Scholar] [CrossRef]

- Dobija, Dorota. 2020. Institutionalizing corporate governance reforms in Poland: External auditors’ perspective. Journal of Management and Business Administration. Central Europe 27: 28–54. [Google Scholar] [CrossRef]

- Downing, Jeff, and John Christian Langli. 2018. Audit exemptions and compliance with tax and accounting regulations. Accounting and Business Research 49: 28–67. [Google Scholar] [CrossRef]

- Dyreng, Scott, Michelle Hanlon, and Edward Maydew. 2008. Long-run corporate tax avoidance. The Accounting Review 83: 61–82. [Google Scholar] [CrossRef]

- Elbannan, Mohammad, and Omar Farooq. 2020. Do more financing obstacles trigger tax avoidance behavior? Evidence from Indian SMEs. Journal of Economics and Finance 44: 161–78. [Google Scholar] [CrossRef]

- Ferrando, Annalisa, and Allesandro Ruggieri. 2018. Financial constraints and productivity: Evidence from euro area companies. International Journal of Finance and Economics 23: 257–82. [Google Scholar] [CrossRef]

- Fisk, Susan R. 2018. Who’s on Top? Gender Differences in Risk-Taking Produce Unequal Outcomes for High-Ability Women and Men. Social Psychology Quarterly 81: 185–206. [Google Scholar] [CrossRef]

- Francis, Jere R., Inder K. Khurana, Xuimin Martin, and Raynolde Pereira. 2011. The relative importance of firm incentives versus country factors in the demand for assurance services by private entities. Contemporary Accounting Research 28: 487–516. [Google Scholar] [CrossRef]

- Galasso, Adele, Francesco Gerotto, Giancarlo Infantino, Francesco Nucci, and Ottavio Ricchi. 2018. Does Access to Finance Improve Productivity? The Case of Italian Manufacturing. In Getting Globalization Right. Cham: Springer-Nature. [Google Scholar] [CrossRef]

- Giang, Mai Huong, Bui Hui Trung, Yuichiro Yoshida, Tran Dang Xuan, and Mai Thanh Que. 2019. The causal effect of access to finance on productivity of small and medium enterprises in Vietnam. Sustainability 11: 5451. [Google Scholar] [CrossRef] [Green Version]

- Gökalp, Ebru, Umut Şener, and P. Erhan Eren. 2017. Development of an Assessment Model for Industry 4.0: Industry 4.0-MM. Informatics Institute. Ankara: Middle East Technical University. [Google Scholar] [CrossRef]

- Gomez-Mejia, Luis, J. Samuel Baixauli-Soler, Maria Belda-Ruiz, and Gregorio Sanchez-Marin. 2019. CEO stock options and gender from the behavioral agency model perspective: Implications for risk and performance. Management Research 17: 68–88. [Google Scholar] [CrossRef]

- Guo, Jang Ting, and Fu Sheng Hung. 2020. Tax evasion and financial development under asymmetric information in credit markets. Journal of Development Economics 145: 102463. [Google Scholar] [CrossRef] [Green Version]

- Hambrick, Donald, and P Phyllis Mason. 1984. Upper Echelons: The Organization as a Reflection of Its Top Managers. Academy of Management Review 9: 193–206. [Google Scholar] [CrossRef]

- Hope, Ole Kristian, Shushu Jiang, and Dushyantkumar Vyas. 2021. Government procurement and financial statement certification: Evidence from private firms in emerging economies. Journal of International Business Studies 52: 718–45. [Google Scholar] [CrossRef]

- Hoseini, Mohammadreza, and Mahdi Safari Gerayli. 2018. The presence of women on the board and tax avoidance: Evidence from Tehran Stock Exchange. International Journal of Finance & Managerial Accounting 3: 53–62. [Google Scholar]

- Ibrahim, Hassan Bashir, Caren Ouma, and Jeremiah Koshal. 2019. Effect of gender diversity on the financial performance of insurance firms in Kenya. International Journal of Research in Business and Social Science 8: 274–85. [Google Scholar] [CrossRef]

- Jabari, Huthayfa Nabeel, and Rusnah Muhamad. 2020. Gender diversity and financial performance of Islamic banks. Journal of Financial Reporting and Accounting 19: 412433. [Google Scholar] [CrossRef]

- Kangave, Jalla, Ronald Waiswa, and Nathan Sebaggala. 2021. Are Women More Tax Compliant than Men? How Would We Know? African Tax Administration Paper 23: 1–23. [Google Scholar] [CrossRef]

- Kasper, Matthias, and James Alm. 2020. Audits, Audit Effectiveness, and Post-audit Tax Compliance. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Kassem, Rasha, and Umut Turksen. 2021. Role of Public Auditors in Fraud Detection: A Critical Review. In Contemporary Issues in Public Sector Accounting and Auditing (Contemporary Studies in Economic and Financial Analysis). Edited by S. Grima and E. Boztepe. Bingley: Emerald Publishing Limited, vol. 105, pp. 33–56. [Google Scholar] [CrossRef]

- Kong, Xiaowei, Deng Kui Si, Haiyang Li, and Dongmin Kong. 2021. Does access to credit reduce SMEs’ tax avoidance? Evidence from a regression discontinuity design. Financial Innovation 7: 1–23. [Google Scholar] [CrossRef]

- Lim, Mark, and Jessica Foster. 2020. Credit Constraints and the Productivity of Small and Medium-sized Enterprises: Evidence from Canada. Asian Journal of Economics and Empirical Research 7: 178–85. [Google Scholar] [CrossRef]

- Luo, Jinbo, Xiaoran Ni, and Gary Gan Tian. 2020. Short selling and corporate tax avoidance: Insights from a financial constraint view. Pacific Basin Finance Journal 61: 1–21. [Google Scholar] [CrossRef]

- MacKinnon, David. 2008. Introduction to Statistical Mediation Analysis. Routledge: New York. [Google Scholar]

- Mackinnon, David, and James Dwyer. 1993. Estimating Mediated Effects in Prevention Studies. Evaluation Review 17: 144–58. [Google Scholar] [CrossRef]

- MacKinnon, David, Ghulam Warsi, and James Dwyer. 1995. A Simulation Study of Mediated Effect Measures. Multivariate Behavioral Research 30: 41–62. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Maydew, Edward, and Douglas Shackelford. 2007. The changing role of auditors in corporate tax planning. In Taxing Corporate Income in the 21st Century. Cambridge: Cambridge University Press. [Google Scholar] [CrossRef] [Green Version]

- Mills, Lilian, Sarah Nutter, and Casey Schwab. 2013. The effect of political sensitivity and bargaining power on taxes: Evidence from federal contractors. The Accounting Review 88: 977–1005. [Google Scholar] [CrossRef]

- Moalla, Hanen, and Rahma Baili. 2019. Credit ratings and audit opinion: Evidence from Tunisia. Journal of Accounting in Emerging Economies 9: 103–25. [Google Scholar] [CrossRef]

- Modigliani, Franco, and Merton Miller. 1958. The Cost of Capital, Corporate Finance and the Theory of Investment. The American Economic Review 48: 261–97. [Google Scholar]

- Morsy, Hanan. 2020. Access to finance—Mind the gender gap. Quarterly Review of Economics and Finance 78: 12–21. [Google Scholar] [CrossRef] [Green Version]

- OECD. 2014. Measures of Tax Compliance Outcomes: A Practical Guide. Paris: OECD Publishing. [Google Scholar] [CrossRef]

- Olayinka, Joshua Akinlolu, and Sirinuch Loykulnanta. 2019. How domestic firms benefit from the presence of multinational enterprises: Evidence from Indonesia and Philippines. Economies 7: 94. [Google Scholar] [CrossRef] [Green Version]

- Orazalin, Nurlan, and Rassul Akhmetzhanov. 2019. Earnings management, audit quality, and cost of debt: Evidence from a Central Asian economy. Managerial Auditing Journal 34: 696–721. [Google Scholar] [CrossRef]

- Suherman, Suherman, Berto Usman, Titis Fatarina Mahfirah, and Renhard Vesta. 2021. Do female executives and CEO tenure matter for corporate cash holdings? Insight from a Southeast Asian country. Corporate Governance 2: 939–60. [Google Scholar] [CrossRef]

- Svanström, Tobias. 2014. Audits of private companies. In The Routledge Companion to Auditing. Edited by David Hay, Robert Knechel and Marleen Willekens. New York: Routledge, pp. 148–58. [Google Scholar]

- Tomkiewicz, Jacek, and Postula Marta. 2020. State Autonomy in Shaping Tax Policies: Facts and Myths Based on the Situation in OECD Countries. Central European Management Journal 28: 83–97. [Google Scholar] [CrossRef]

- Trpeska, Marina, Atanasko Atanasovski, and Bozinovska Zorica Lazarevska. 2017. The relevance of financial information and contents of the new audit report for lending decisions of commercial banks. Journal of Accounting and Management Information Systems 16: 455–71. [Google Scholar] [CrossRef]

- Vanstraelen, Aan, and Caren Schelleman. 2017. Auditing private companies: What do we know? Accounting and Business Research 47: 565–84. [Google Scholar] [CrossRef] [Green Version]

- Wang, Ying, Michael Campbell, and Debra Johnson. 2014. Determinants of effective tax rate of China publicly listed companies. International Management Review 10: 10–20. [Google Scholar]

- World Bank. 2009. Enterprise Survey and Indicator Surveys: Sampling Methodology. Available online: www.enterprisesurveys.org (accessed on 1 March 2022).

{kind=link}

| Variable | Measurement |

|---|---|

| Tax compliance | Measured with three answer categories: 1 = no compliance if, in the observation year, the firm was inspected by the tax officials for more than thirty days; 2 = partial compliance if the firm was inspected by the tax officials in less than thirty days; and 3 = full compliance if the tax officer never checks the company. |

| Financial statement audit | A dummy variable is equal to one if the firm has its financial statements audited by an external auditor and zero otherwise. |

| Access to finance | “To what degree is access to finance an obstacle to the current operations of this establishment?” and quantified on a scale from 0 (very severe obstacle) to 5 (no obstacle). |

| Top manager’s gender | A dummy variable is equal to one if the top manager is female and zero otherwise. |

| Firm size | Classified into four categories: 1 = the firm is a micro-firm with the number of employees less than 5; 2 = the firm is a small firm with 6–19 employees; 3 = the firm is a medium firm with 20–99 employees; and 4 = the firm is a large firm with more than 100 employees. |

| Firm age | Firm age in 2018. |

| Family ownership | A dummy variable is equal to one if the firm is a family firm and zero otherwise. |

| Variables | Total | Female Managers | Male Managers | |||

|---|---|---|---|---|---|---|

| N | % | N (14.988) | % | N (30.516) | % | |

| Audit | ||||||

| With financial statement audits | 28.209 | 61.99 | 9.472 | 63.2 | 18.737 | 61.401 |

| Without financial statement audits | 17.295 | 38.01 | 5.516 | 36.8 | 11.779 | 38.599 |

| Access to Finance | ||||||

| No obstacle | 14.268 | 31.36 | 4.901 | 32.7 | 9.367 | 30.695 |

| Minor disagreement | 10.192 | 22.40 | 3.477 | 23.2 | 6.715 | 22.005 |

| Moderate obstacle | 10.420 | 22.90 | 3.402 | 22.7 | 7.018 | 22.998 |

| Major obstacle | 7.223 | 15.87 | 2.278 | 15.2 | 4.945 | 16.205 |

| Very severe obstacle | 3.400 | 7.47 | 929 | 6.2 | 2.471 | 8.097 |

| Tax Compliance | ||||||

| Full compliance | 17.043 | 37.45 | 5.966 | 39.8 | 11.077 | 36.299 |

| Partial compliance | 25.470 | 55.97 | 8.168 | 54.5 | 17.302 | 56.698 |

| No compliance | 2.990 | 6.57 | 854 | 5.7 | 2.136 | 7.000 |

| Variables | Model 1 | Model 2 | Model 3 | |||

|---|---|---|---|---|---|---|

| Coef. | p-Value | Coef. | p-Value | Coef. | p-Value | |

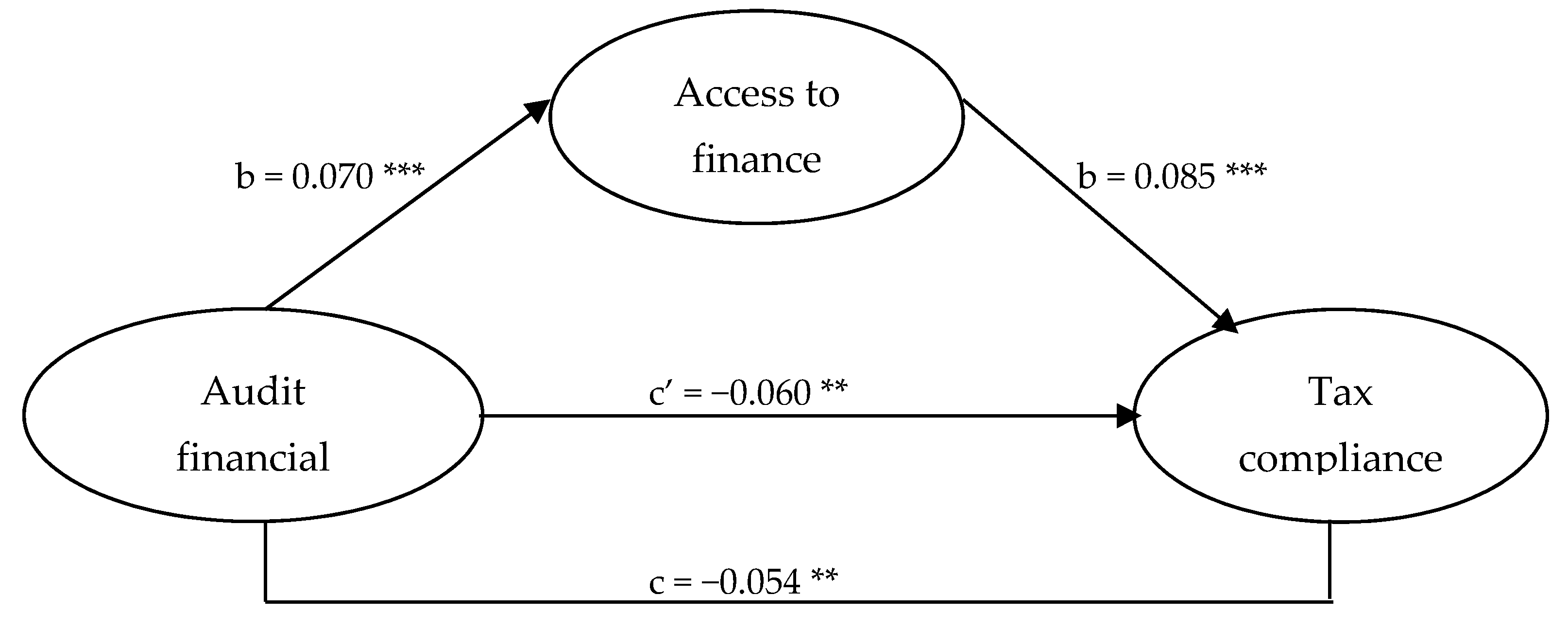

| Audit | −0.060 | 0.023 ** | 0.070 | 0.000 *** | −0.066 | 0.012 |

| Access to finance | 0.085 | 0.000 *** | ||||

| Firm size | −0.085 | 0.000 *** | 0.131 | 0.000 *** | −0.096 | 0.000 *** |

| Firm age | −0.004 | 0.000 *** | −0.002 | 0.000 *** | −0.004 | 0.000 *** |

| Family ownership | 0.021 | 0.454 | 0.052 | 0.000 *** | 0.017 | 0.551 |

| Adjusted R2 | 0.002 | 0.008 | 0.004 | |||

| Panel A. Mediation Test Berdasar t Value | |||

| Z | p-Value | ||

| Sobel | 4.5960 ** | 0.0000043 | |

| Goodman 1 (Aroian) | 4.5749 ** | 0.0000047 | |

| Goodman 2 | 4.6175 ** | 0.0000038 | |

| Panel B. Mediation Test Based on Coefficient and Standard Error | |||

| Z | Std. Error | p-Value | |

| Sobel | 4.5487 ** | 0.00130806 | 0.0000054 |

| Goodman 1 (Aroian) | 4.5264 ** | 0.00131451 | 0.0000060 |

| Goodman 2 | 4.5713 ** | 0.00130159 | 0.0000485 |

| Variables | Female Managers | Male Managers | ||

|---|---|---|---|---|

| Coefficient | p-Value | Coefficient | p-Value | |

| Panel A. Effect of financial statement audit on tax compliance | ||||

| Audit | 0.008 | 0.064 * | −0.091 | 0.005 ** |

| Firm size | −0.119 | 0.000 *** | −0.070 | 0.001 ** |

| Firm age | −0.004 | 0.001 ** | −0.004 | 0.000 *** |

| Family ownership | 0.000 | 0.996 | 0.066 | 0.078 * |

| Adjusted R2 | 0.003 | 0.002 | ||

| Observation | 14.988 | 30.516 | ||

| Panel B. Effect of access to finance on tax compliance | ||||

| Audit | 0.016 | 0.097 * | −0.094 | 0.004 ** |

| Access to finance | 0.103 | 0.000 *** | 0.075 | 0.000 *** |

| Firm size | −0.128 | 0.000 *** | −0.081 | 0.000 *** |

| Firm age | −0.004 | 0.002 ** | −0.004 | 0.000 *** |

| Family ownership | −0.008 | 0.867 | 0.063 | 0.000 *** |

| Adjusted R2 | 0.,005 | 0.003 | ||

| Observation | 14.988 | 30.516 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sunardi, S.; Damayanti, T.W.; Supramono, S.; Hermanto, Y.B. Gender, Perception of Audits, Access to Finance, and Self-Assessed Corporate Tax Compliance. Economies 2022, 10, 65. https://doi.org/10.3390/economies10030065

Sunardi S, Damayanti TW, Supramono S, Hermanto YB. Gender, Perception of Audits, Access to Finance, and Self-Assessed Corporate Tax Compliance. Economies. 2022; 10(3):65. https://doi.org/10.3390/economies10030065

Chicago/Turabian StyleSunardi, Sunardi, Theresia Woro Damayanti, Supramono Supramono, and Yustinus Budi Hermanto. 2022. "Gender, Perception of Audits, Access to Finance, and Self-Assessed Corporate Tax Compliance" Economies 10, no. 3: 65. https://doi.org/10.3390/economies10030065

APA StyleSunardi, S., Damayanti, T. W., Supramono, S., & Hermanto, Y. B. (2022). Gender, Perception of Audits, Access to Finance, and Self-Assessed Corporate Tax Compliance. Economies, 10(3), 65. https://doi.org/10.3390/economies10030065