Are We Ready for the Challenge of Banks 4.0? Designing a Roadmap for Banking Systems in Industry 4.0

,

,  ,

,  and

and

Abstract

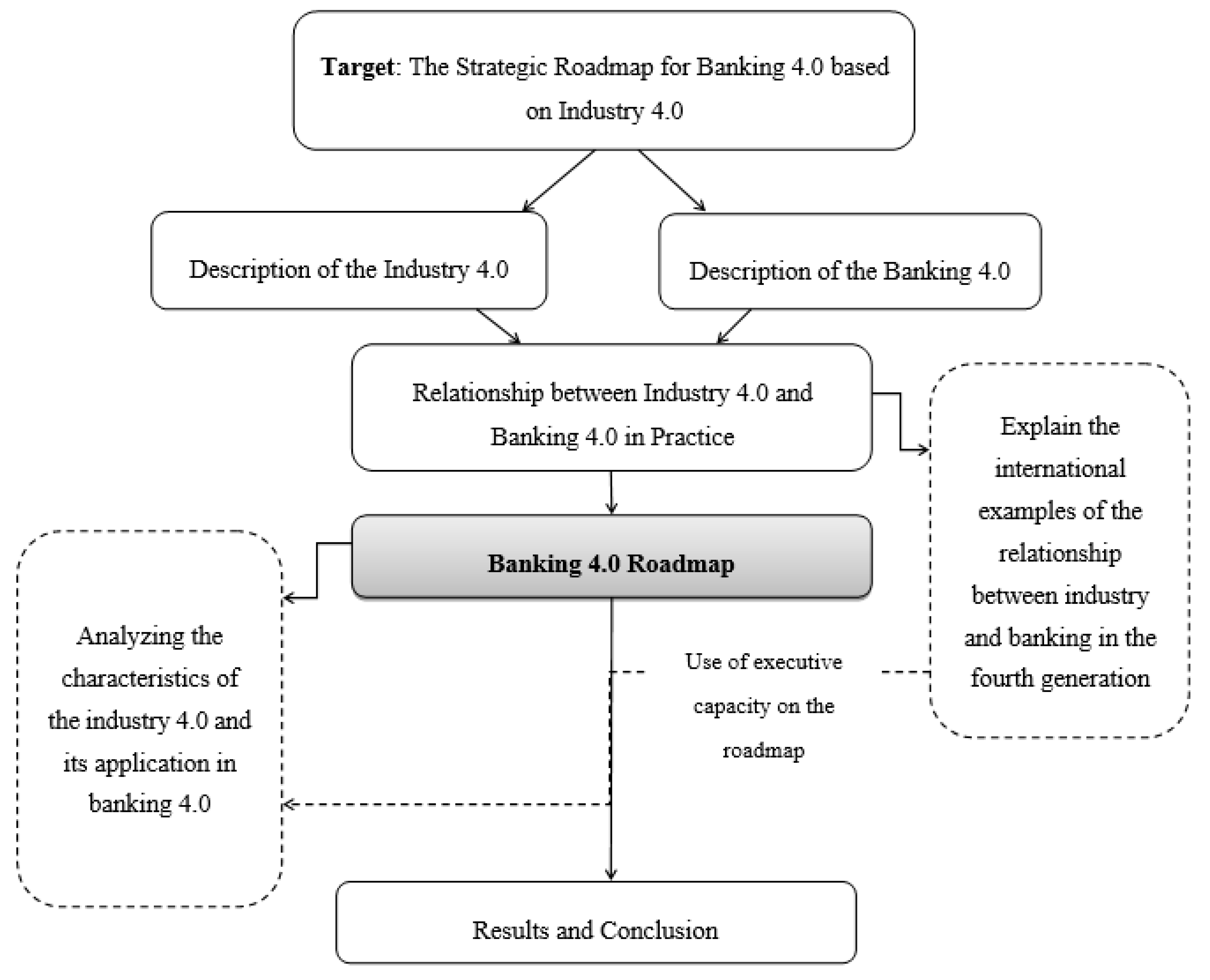

1. Introduction

- Is it necessary for the banking sector to join Banking 4.0?

- In practice, is there an interaction between Industry 4.0 and Banking 4.0 within the organizations?

- Is it possible to develop a codified roadmap for entering Industry 4.0?

2. Literature Review

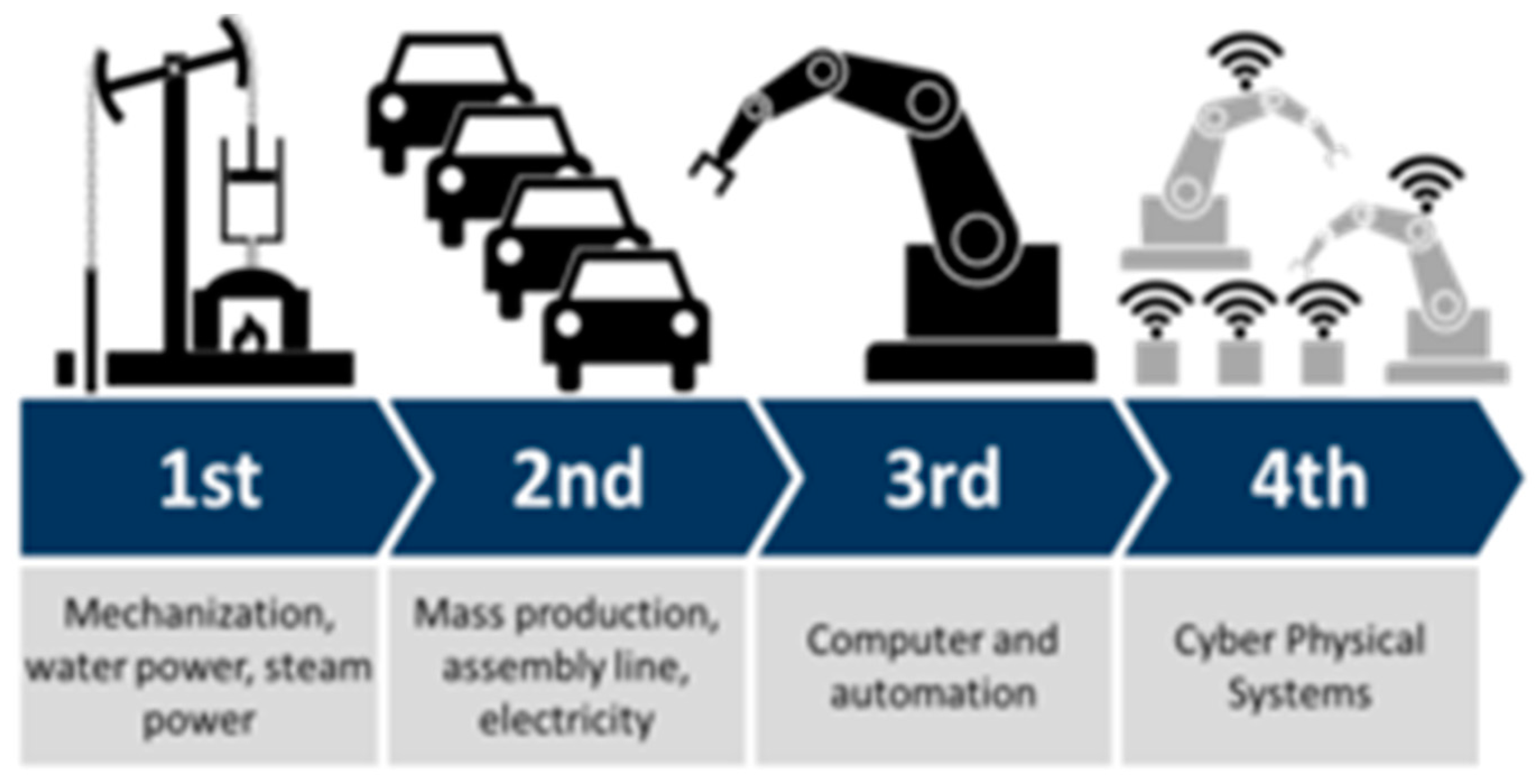

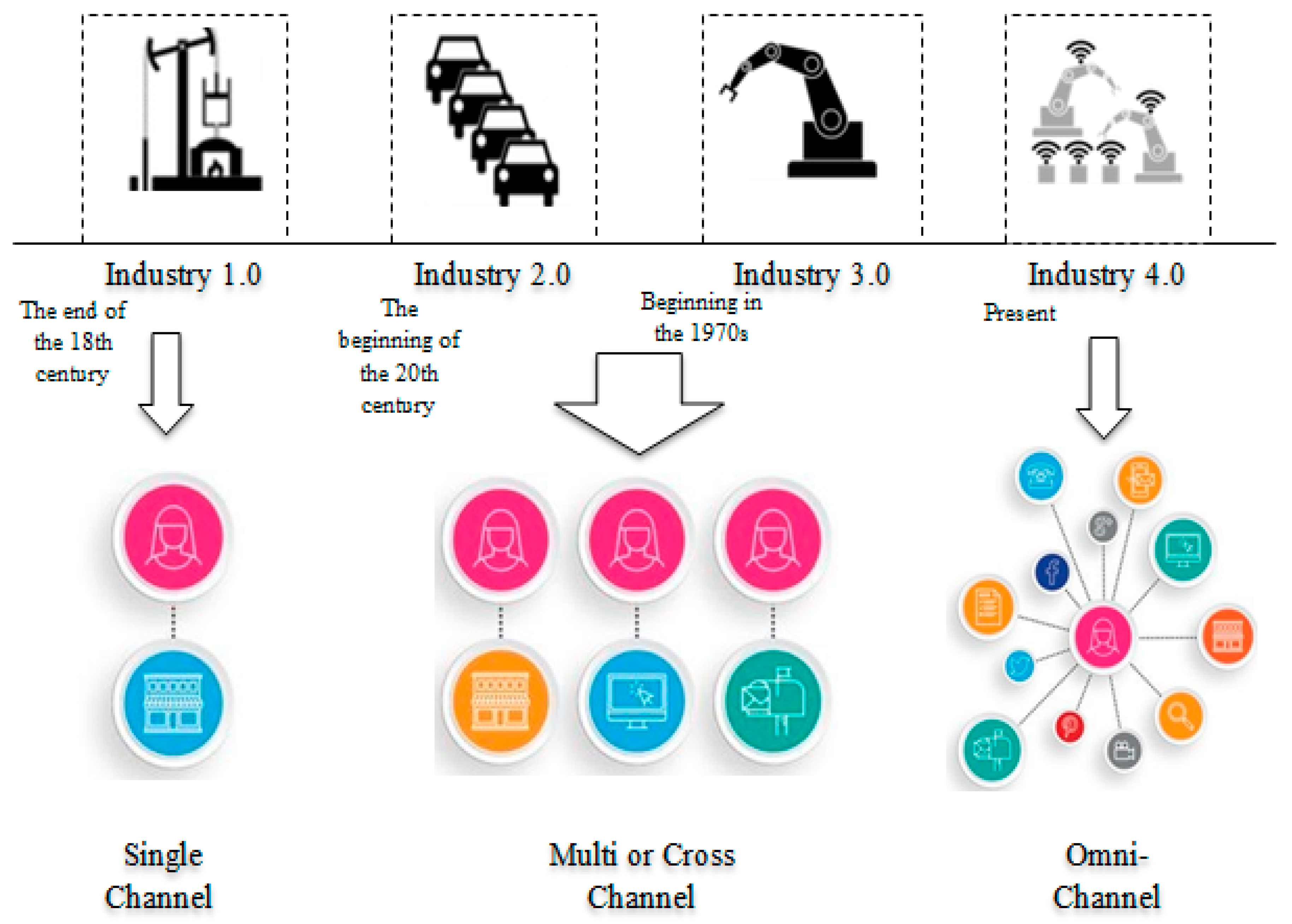

2.1. Industry 4.0

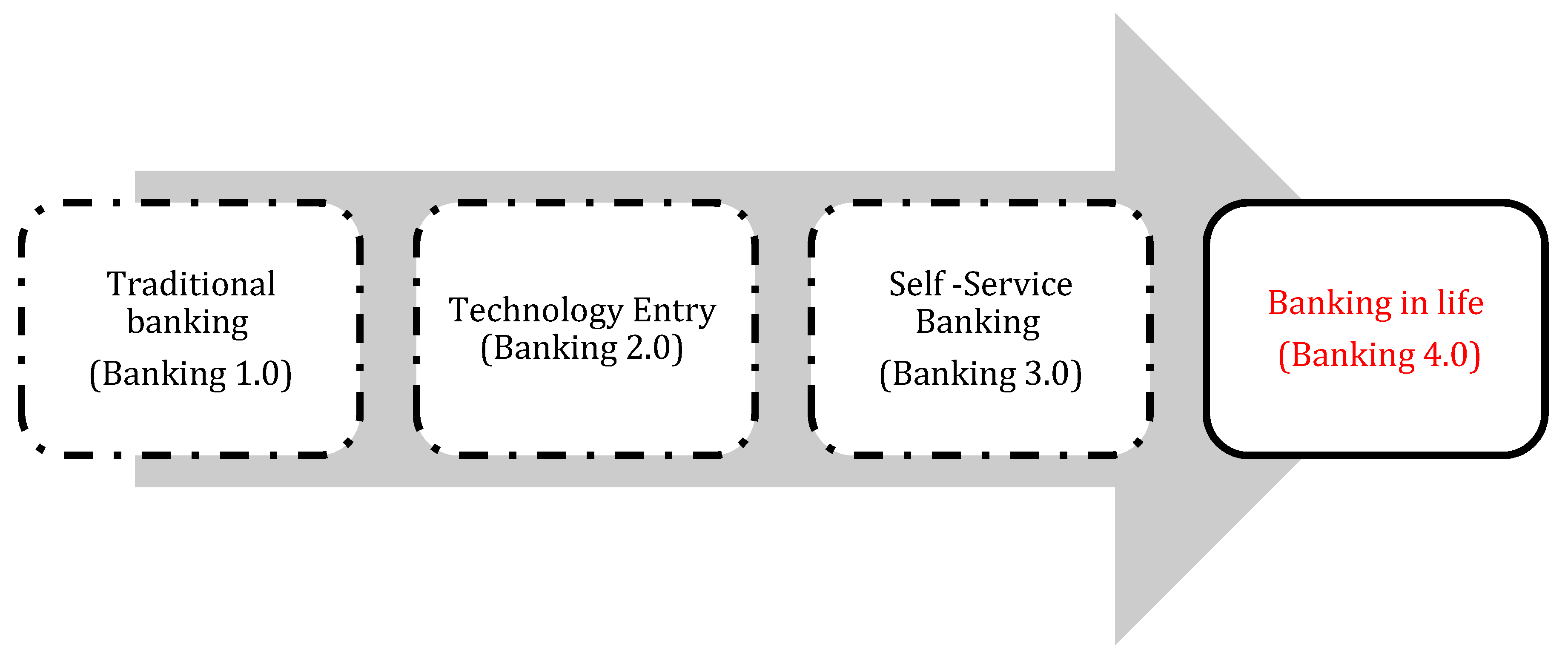

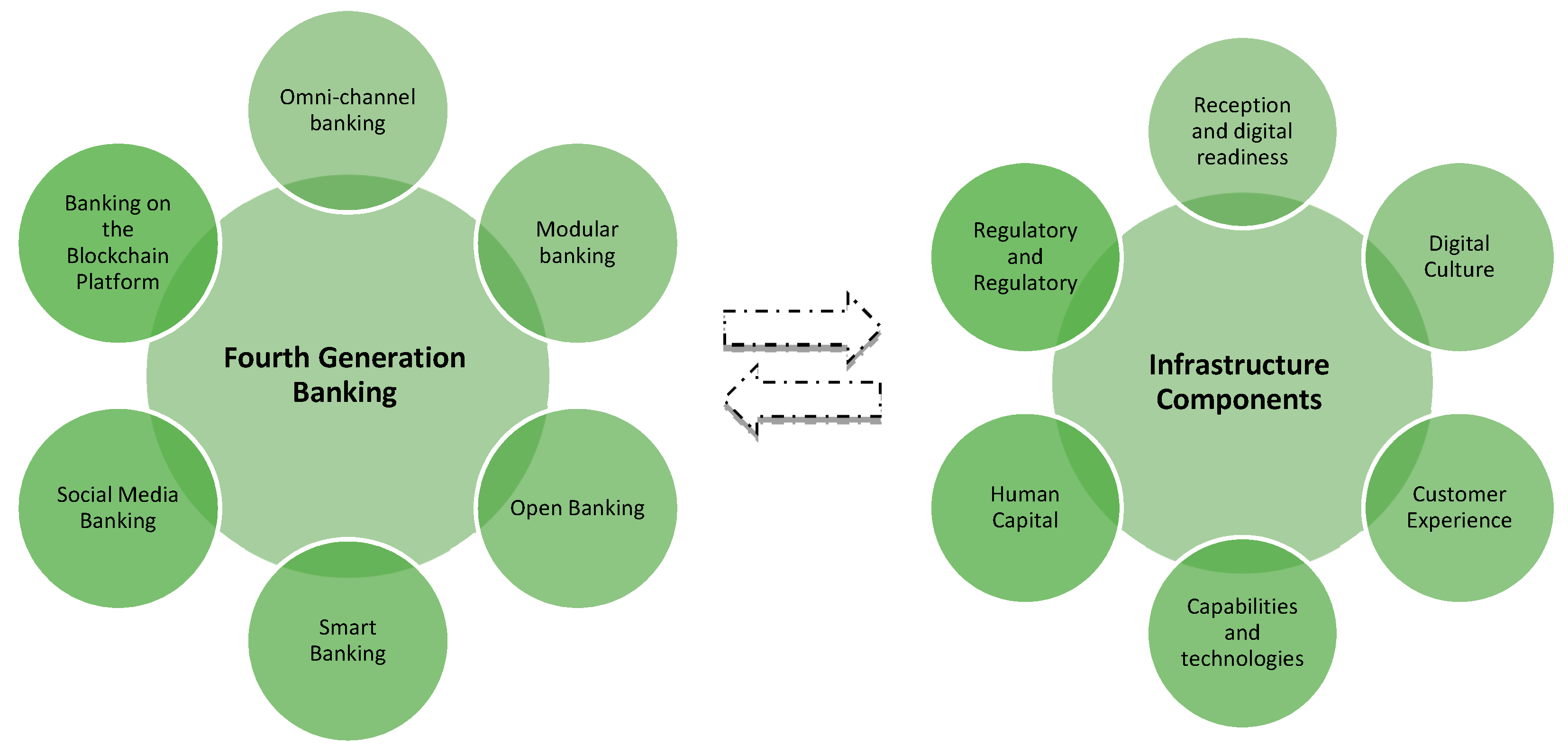

2.2. Banking 4.0

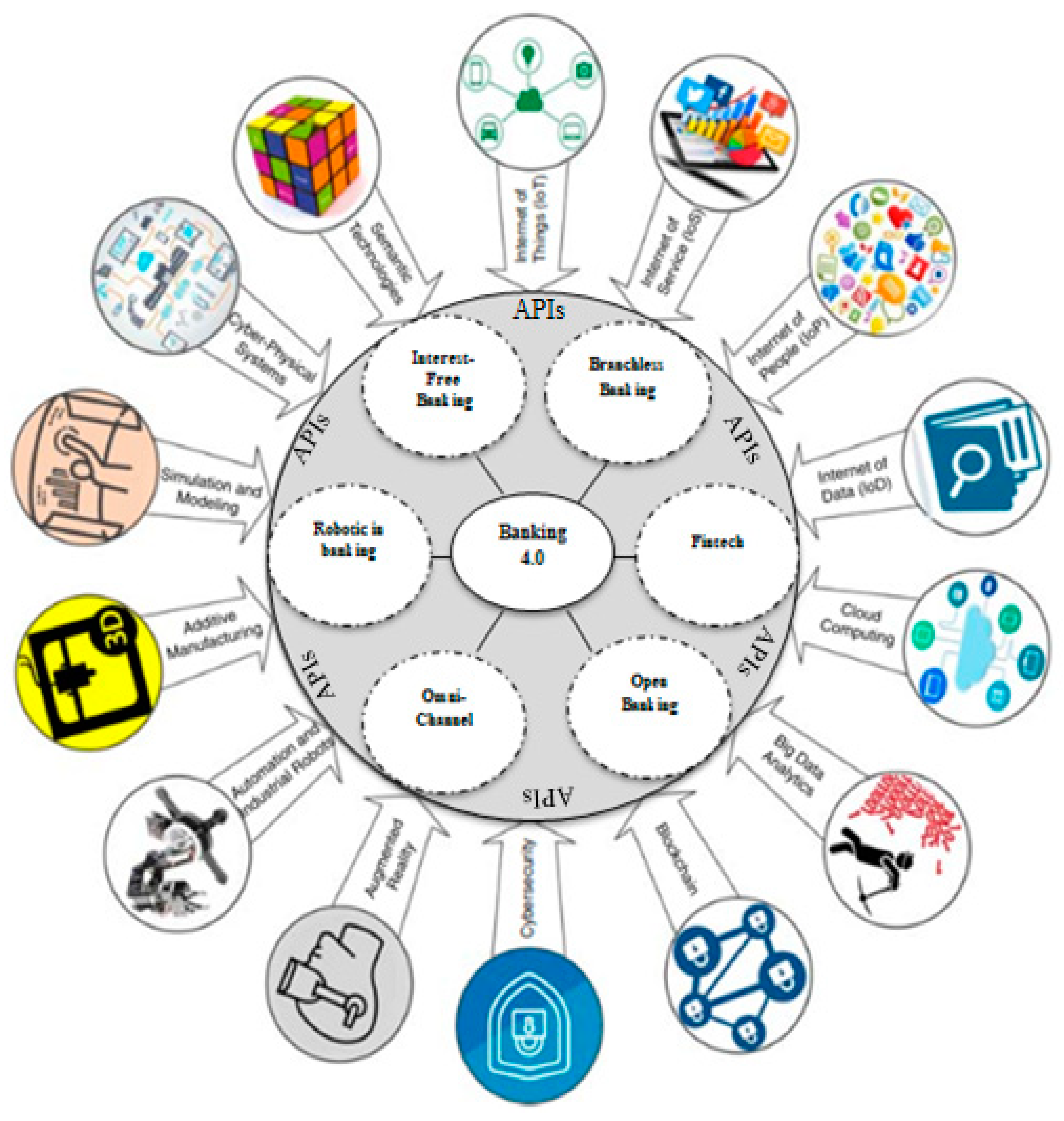

2.3. The Relationship between Industry 4.0 and Banking 4.0 in Practice

2.3.1. Replacing Banks with Organizations and Institutions

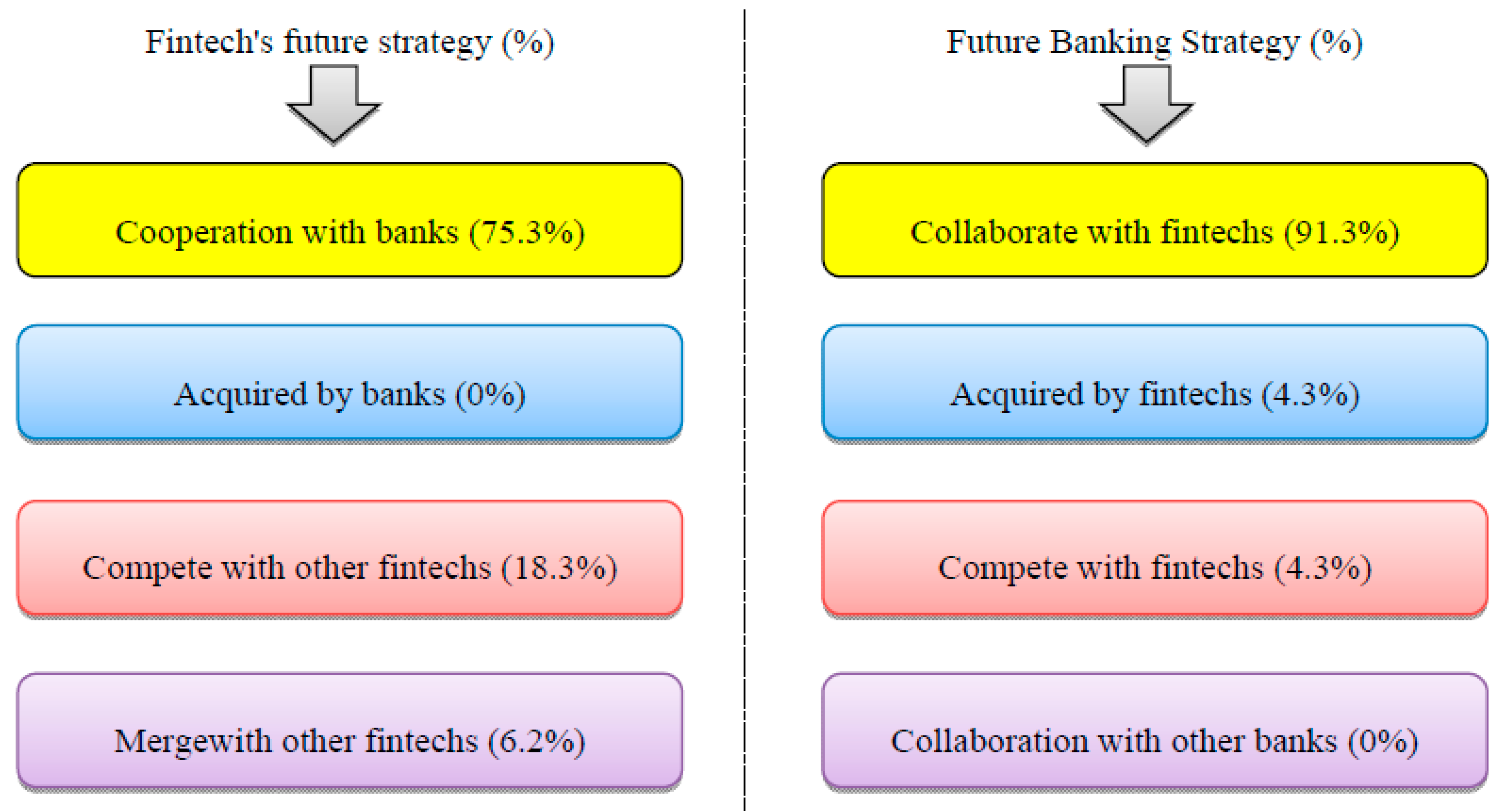

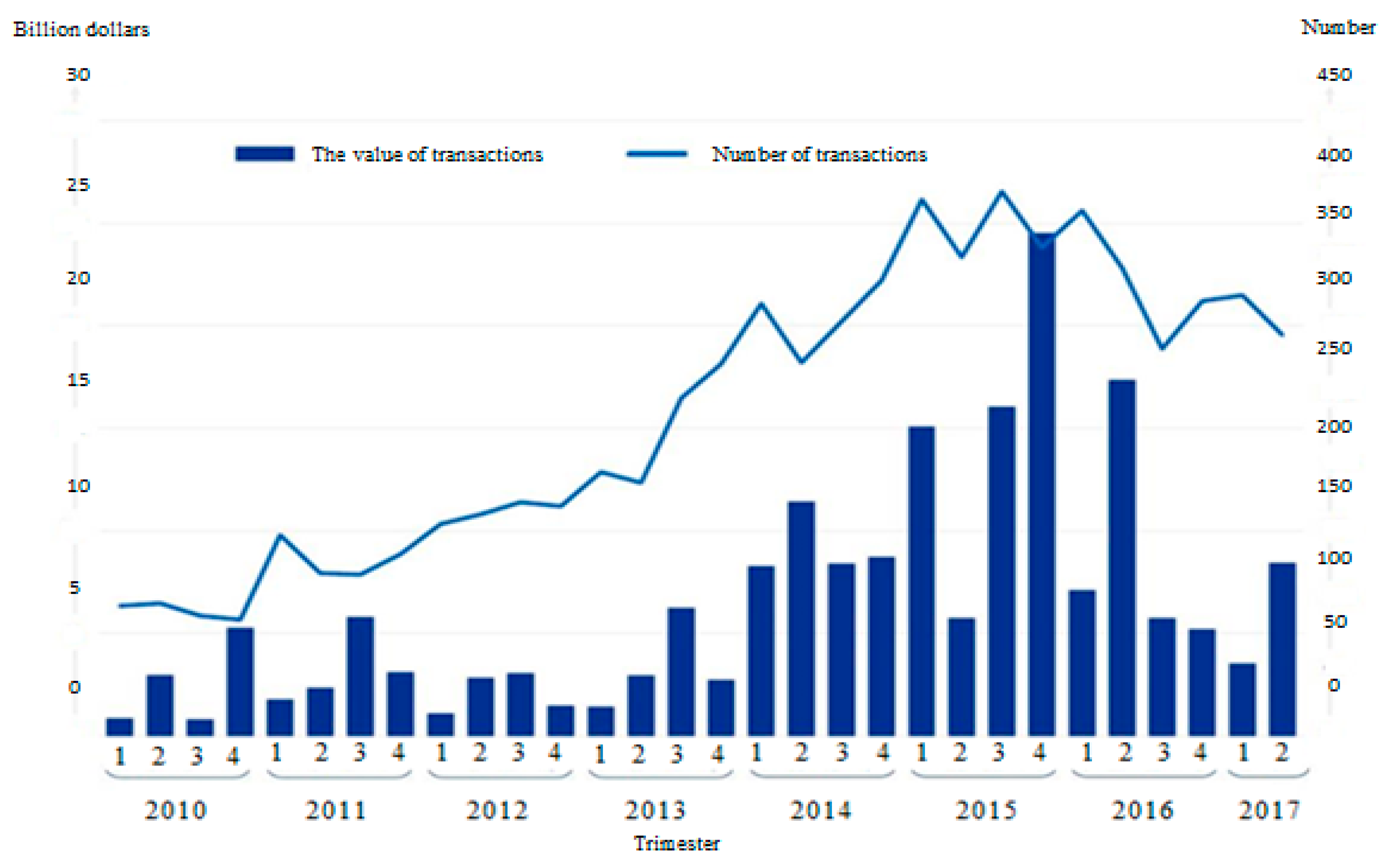

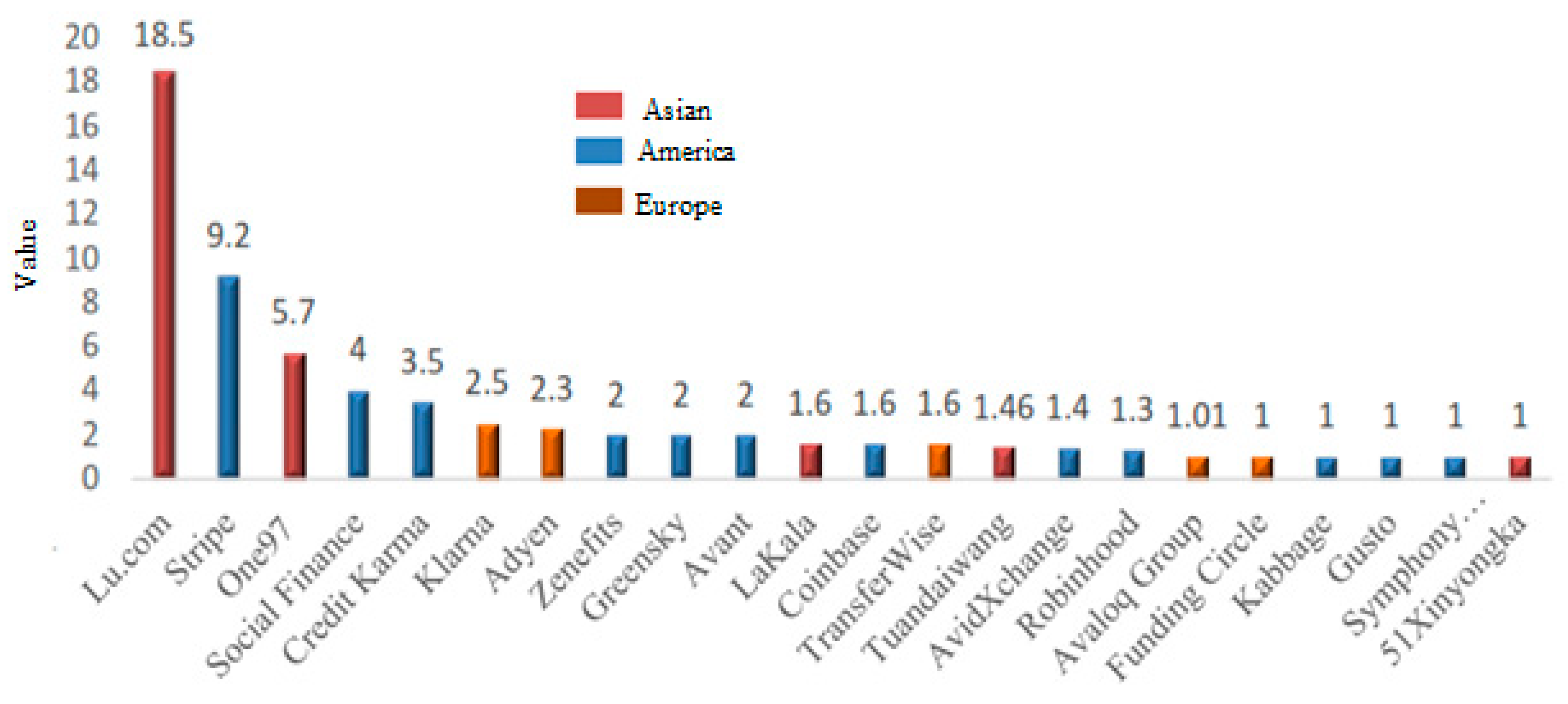

2.3.2. Advantages and Disadvantages of FinTech Development in Banking

2.3.3. JAK Bank: Interest-Free Banking

2.3.4. Atom Bank and Gobank: Branchless Banking (BB)

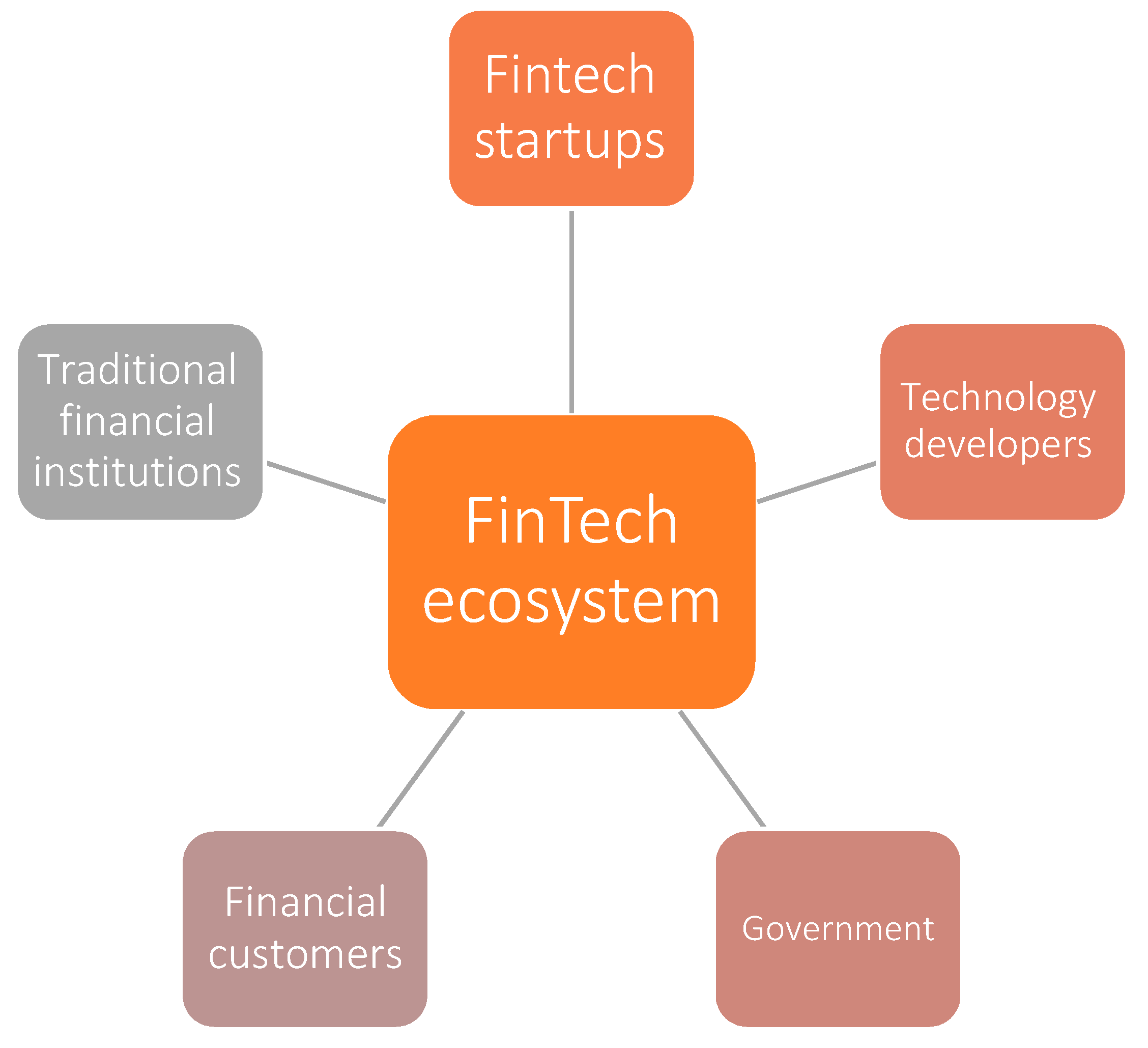

2.3.5. Financial Technology (FinTech)

- FinTech startups (e.g., payment, wealth management, lending, crowdfunding, capital market, and insurance FinTech companies);

- Technology developers (e.g., big data analytics, cloud computing, cryptocurrency, and social media developers);

- Government (e.g., financial regulators and legislature);

- Financial customers (e.g., individuals and organizations);

- Traditional financial institutions (e.g., traditional banks, insurance companies, stock brokerage firms, and venture capitalists).

2.3.6. Open Banking (OB): APIs and Fidor Bank

2.3.7. Omni-Channel (O-C): Disney Company and Starbucks

- Port uniformity

- Integration of ports versus independent ports

- Customer-centric versus bank-centric

- Interaction versus transaction

- Guessing customer needs versus making requests

- Disney Company: Disney is one of the companies that has good communication with customers by using the O-C concept. It is based on fiction and creative stories, and it is no wonder that in the real world, it also uses creative ways to omni-channel. Disney paid close attention to details and made it possible to access all parts of the website via mobile. After logging in, the user can plan each minute of the trip through the app. Visitors can follow the park through the app, the location of all sights, and the length of time they need to queue. Users also get their rooms through the app and charge all the purchases they make to room service. All Disney communication channels are interconnected and provide a good user experience.

- Starbucks: Starbucks is another brand that has made good use of the omni-channel concept. Starbucks has branches in most cities around the world and provides a good customer experience.Each time a user pays his account via bank or mobile card, the purchase points he has are added to his account. The Starbucks app also introduces the nearest branch to the user and prepares the coffee by the time the user arrives. Users can also view the new coffee list in the menu and be informed of the song played in each branch (Starbuck works with many companies. Playing all kinds of music and having a lot of branches around the world has made customers understand different pleasures. So, customers can choose their Starbucks according to the music played). Surely every user after experiencing such features will become a permanent customer of the brand.

2.3.8. Robotics in Banking

- Secure efficient interaction between different systems, thus eliminating the need for employees to manually source data

- Upgrade middle and back-office processes (faster execution, fewer errors)

- Speed up the processing of big data

- Free up employees to focus more on clients and provide a better customer experience

- Reduce time-to-market and total cost of ownership (TCO)

- Simplify regulatory compliance with greater transparency

- Pave the way for a new wave of transformation toward 100% digital banking.

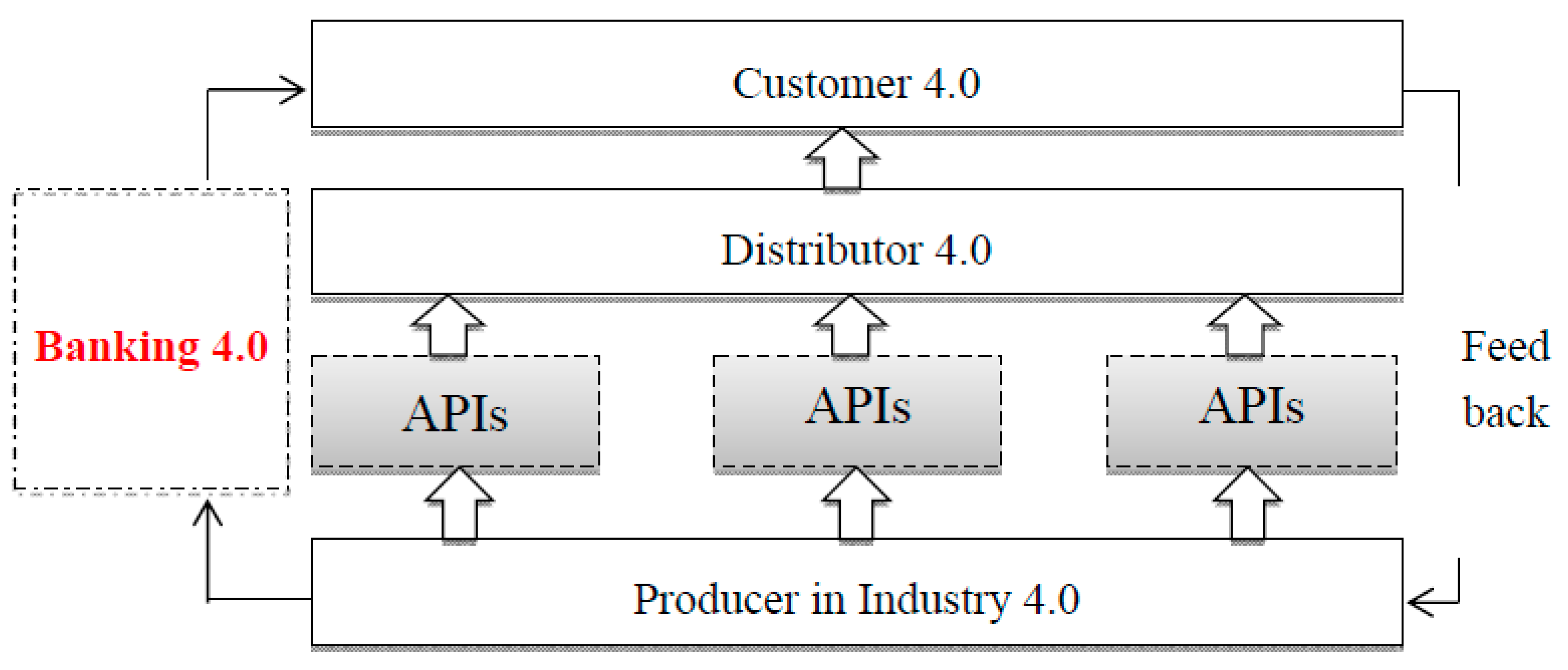

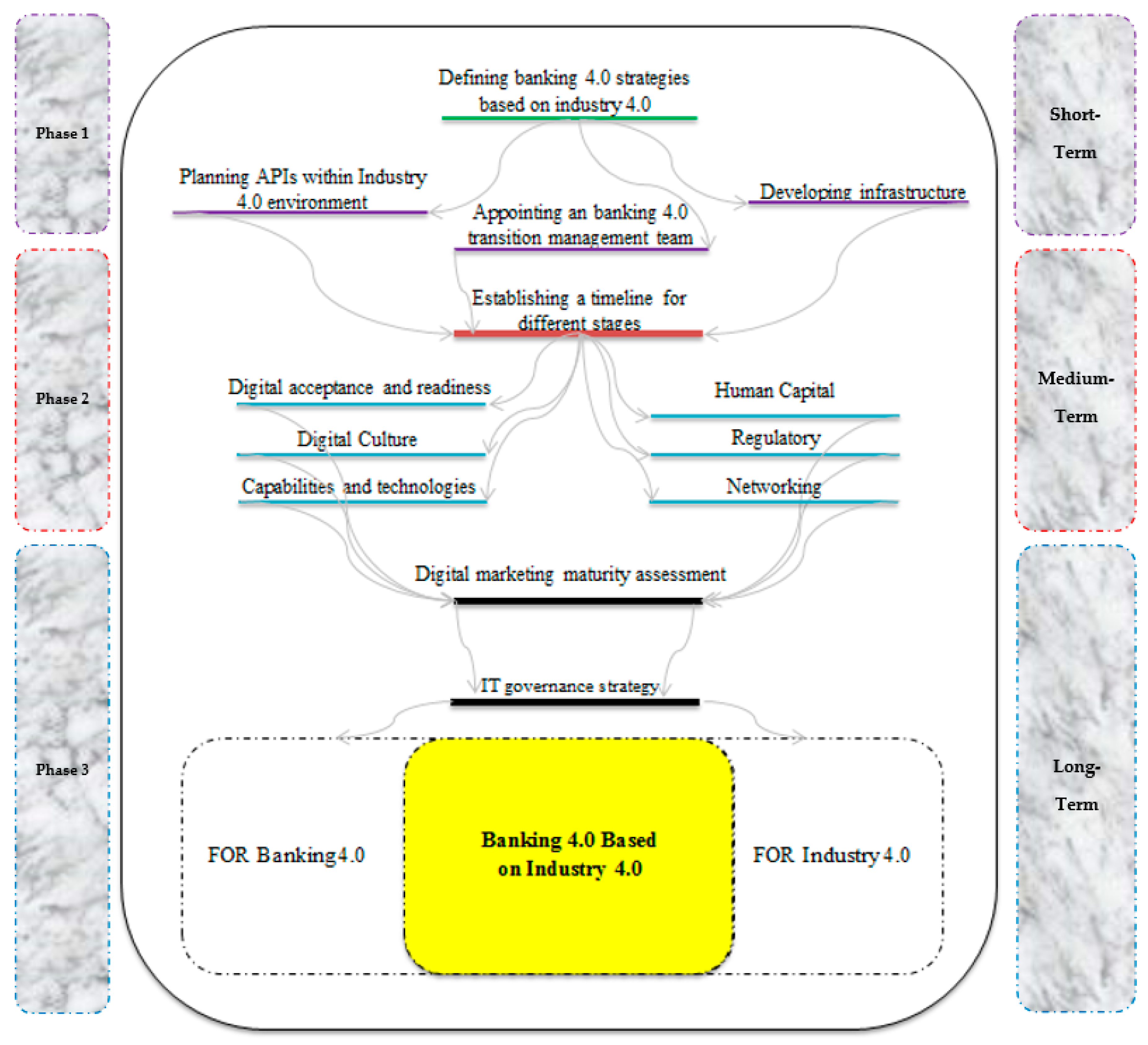

3. Banking 4.0 Roadmap in Industry 4.0

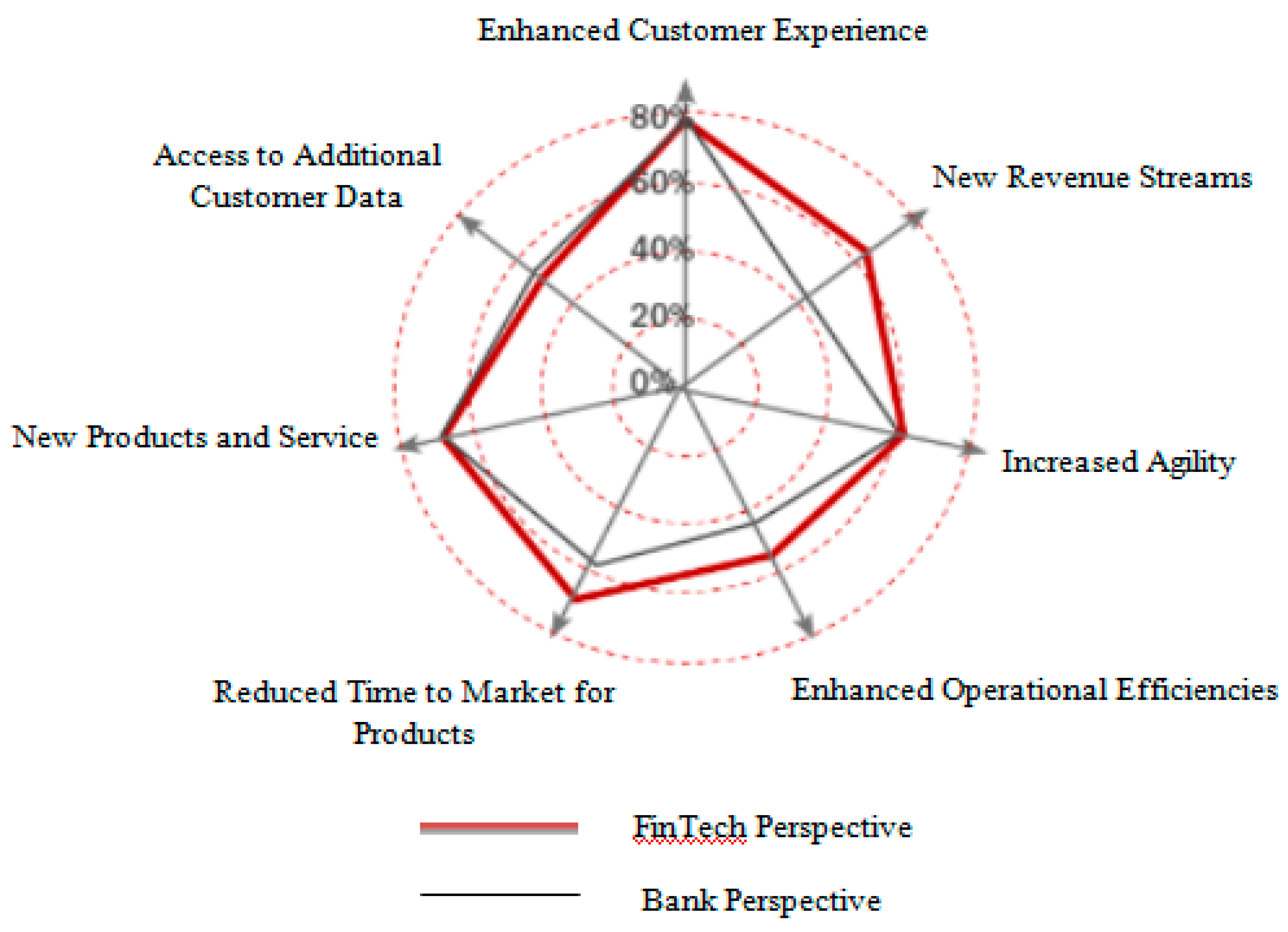

4. Results

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Ahmad, Khurshid. 2000. Islamic finance and banking: The challenge and prospects. Review of Islamic Economics 9: 57–82. [Google Scholar]

- Al-Fuqaha, Ala, Mohsen Guizani, Mehdi Mohammadi, Mohammed Aledhari, and Moussa Ayyash. 2015. Internet of things: A survey on enabling technologies, protocols, and applications. IEEE Communications Surveys & Tutorials 17: 2347–76. [Google Scholar]

- Anderl, Reiner. 2014. Industrie 4.0-advanced engineering of smart products and smart production. Paper presented at the 19th International Seminar on High Technology, Technological Innovations in the Product Development, Piracicaba, Brazil, October 9; pp. 1–14. [Google Scholar]

- Agrawal, Anirudh, Sebastian Schaefer, and Thomas Funke. 2017. Incorporating Industry 4.0 in Corporate Strategy. Hershey: IGIGlobal. [Google Scholar]

- Apiacademy Homepage. 2018. Available online: https://www.apiacademy.co/lessons/2015/04/api-strategy-lesson101-what-is-an-api (accessed on 10 September 2018).

- Arner, Douglas W., Janos Barberis, and Ross P. Buckley. 2015. The Evolution of FinTech: A New PostCrisis Paradigm. Geo. J. Int’l L 47: 1271–71. [Google Scholar]

- Athanasoglou, Panayiotis P., Matthaios D. Delis, and Christos K. Staikouras. 2006. Determinants of Bank Profitability in the South Eastern European Region. Working paper no. 40. Athens: Bank of Greece. [Google Scholar]

- Atombank. 2016a. Fabulous Atom Questions. Available online: https://www.atombank.co.uk/ (accessed on 7 October 2016).

- Atombank. 2016b. The Future of Banking. Available online: https://www.atombank.co.uk/ (accessed on 7 October 2016).

- Atzori, Luigi, Antonio Iera, and Giacomo Morabito. 2010. The internet of things: A survey. Computer Networks 54: 2787–805. [Google Scholar] [CrossRef]

- Babiceanu, Radu F., and Remzi Seker. 2016. Big Data and virtualization for manufacturing cyber-physical systems: A survey of the current status and future outlook. Computers in Industry 81: 128–37. [Google Scholar] [CrossRef]

- Bandara, Oshadhi, Kasuni Vidanagamachchi, and Ruwan Wickramarachchi. 2019. A Model for Assessing Maturity of Industry 4.0 in the Banking Sector. Paper presented at the International Conference on Industrial Engineering and Operations Management, Bangkok, Thailand, March 5–7. [Google Scholar]

- Banker. 2019. Annual Report. Available online: https://www.thebanker.com/ (accessed on 18 July 2019).

- Becker, Tilman, Catherina Burghart, Kawa Nazemi, Patrick Ndjiki-Nya, Thomas Riegel, Ralf Schäfer, Thomas Sporer, Volker Tresp, and Jens Wissmann. 2014. Core technologies for the internet of services. In Towards the Internet of Services: The THESEUS Research Program. Edited by Wolfgang Wahlster, Hans-Joachim Grallert, Stefan Wess, Hermann Friedrichand and Thomas Widenka. Heidelberg: Springer, pp. 59–88. [Google Scholar]

- Benbasat, Izak, and Henri Barki. 2007. Quo vadisTAM. Journal of Association for Information Systems 8: 3–13. [Google Scholar] [CrossRef]

- Berger, Roland. 2017. Industry 4.0, New Industrial Revolution HowEurope will Succeed. Munich: Roland Berger Strategic Consultants. Available online: http://www.iberglobal.com/files/Roland_Berger_Industry.pdf (accessed on 10 March 2020).

- Bhattacharya, Sudipto, and Anjan V. Thakor. 1993. Contemporary banking theory. Journal of Financial Intermediation 3: 2–50. [Google Scholar] [CrossRef]

- Bohács, Gábor, Ivett Frikker, and Gabor Kovács. 2013. Intermodal logistics processes supported by electronic freight and warehouse exchanges. Transport and Telecommunication 14: 206–13. [Google Scholar] [CrossRef]

- Capgemini. 2012. Trends in Retail Banking Channels: Improving Client Service and Operating Costs. Available online: www.capgemini.com/banking (accessed on 25 June 2019).

- Capgemini. 2017a. Capgemini Financial Service Analysis, World_FinTech_Report_2017. Available online: https://www.capgemini.com/wp-content/uploads/2017/09/world_fintech_report_2017.pdf (accessed on 18 July 2019).

- Capgemini. 2017b. Capgemini Financial Service Analysis, Retail Banking Executive Interview Survey, Capgemini Global Financial Services. Available online: https://www.capgemini.com/at-de/wp-content/uploads/sites/25/2018/08/WorldRetailBankingReport2017.pdf (accessed on 30 July 2019).

- CGAP. 2008. Banking through Network of Retail Agents. Washington, DC: CGAP/World Bank. [Google Scholar]

- CGAP. 2010. CGAP Annual Report 2010. Available online: https://www.cgap.org/about/key-documents/cgap-annual-report-2010 (accessed on 1 December 2016).

- CGAP. 2011. Bank Agents: Risk Management, Mitigation, and Supervision. Available online: https://www.cgap.org/ (accessed on 1 December 2016).

- Cividino, Sirio, Gianluca Egidi, Ilaria Zambon, and Andrea Colantoni. 2019. Evaluating the Degree of Uncertainty of Research Activities in Industry 4.0. Future Internet 11: 196. [Google Scholar] [CrossRef]

- CNI, National Confederation of Industry. 2016. Industry 4.0: A new challenge for Brazilian industry. CNI Indicators 17. [Google Scholar]

- Conti, Marco, Andrea Passarella, and Sajal K. Das. 2017. The Internet of People (IoP): A new wave in pervasive mobile computing. Pervasive and Mobile Computing 41: 1–27. [Google Scholar] [CrossRef]

- David, Loide, and Teresia Kaulihowa. 2018. The Impact of E- Banking on Commercial Banks’ Performance in Namibia. International Journal of Economics and Financial Research 4: 313–21. [Google Scholar]

- Delloite. 2012. Are We Headed towards Branchless Banking? Available online: www.deloitte.com/ar (accessed on 7 December 2019).

- Devezas, Tessaleno, and Askar Sarygulov. 2017. Industry 4.0: Entrepreneurship and Structural Change in the New Digital Landscape. Heidelberg: Springer. [Google Scholar]

- Dzombo, Gift Kimonge, James M. Kilika, and James Maingi. 2017. The Effect of Branchless Banking Strategy on the Financial Performanof Commercial Banks in Kenya. International Journal of Financial Research 8: 167–83. [Google Scholar] [CrossRef]

- Doshi, Ashish, Ross T. Smith, Bruce H. Thomas, and Con Bouras. 2017. Use of projector based augmented reality to improve manual spot-welding precision and accuracy for automotive manufacturing. The International Journal of Advanced Manufacturing Technology 89: 1279–93. [Google Scholar] [CrossRef]

- Elia, Valerio, Maria Grazia Gnoni, and Alessandra Lanzilotto. 2016. Evaluating the application of augmented reality devices in manufacturing from a process point of view: An AHP based model. Expert Systems with Applications 63: 187–97. [Google Scholar] [CrossRef]

- Ernst and Young. 2016. FinTech on the Cutting Edge. Available online: http://www.ey.com/uk/en/industries/financial-services/banking--capital-markets/ey-uk-fintech-on-the-cutting-edge (accessed on 18 January 2020).

- Erol, Selim, Andreas Jäger, Philipp Hold, Karl Ott, and Wilfried Sihn. 2016. Tangible Industry 4.0: A scenario-based approach to learning for the future of production. Procedia CIRP 54: 13–18. [Google Scholar] [CrossRef]

- Esmaeilian, Behzad, Sara Behdad, and Ben Wang. 2016. The evolution and future of manufacturing: A review. Journal of Manufacturing Systems 39: 79–100. [Google Scholar] [CrossRef]

- Fan, Wei, Zhengyong Chen, Zhang Xiong, and Hui Chen. 2012. The internet of data: A new idea to extend the IOT in the digital world. Frontiers of Computer Science 6: 660–67. [Google Scholar] [CrossRef]

- Faure, Alexander Pierre. 2013. Banking: An Introduction, 1st ed. Western Cape: Quoin Institute (Pty) Limited. [Google Scholar]

- Ghobakhloo, Morteza. 2018. The future of manufacturing industry: A strategic roadmap toward Industry 4.0. Journal of Manufacturing Technology Management 29: 910–36. [Google Scholar] [CrossRef]

- Gilchrist, Alasdair. 2016. Industry 4.0: The Industrial Internet of Things. Heidelberg: Springer. [Google Scholar]

- Gjeldum, Nikola, Marko Mladineo, and Ivica Veža. 2016. Transfer of model of innovative smart factory to Croatian economy using Lean Learning Factory. Procedia CIRP 54: 158–63. [Google Scholar] [CrossRef][Green Version]

- GoBank. 2016. Green Dot’s GoBank Opens its US-Only Branchless Mobile Bank to the Public, Available Today. Available online: http://thenextweb.com (accessed on 20 October 2016).

- Gökalp, Ebru, Umut Şener, and P. Erhan Eren. 2017. Development of an Assessment Model for Industry 4.0: Industry 4.0-MM, Software Process Improvement and Capability Determination. New York: Springer International Publishing. [Google Scholar]

- Harjanti, Istidana, Faisal Nasution, Nerifa Gusmawati, Muhammad Jihad, Muhammad Rifki Shihab, Benny Ranti, and Indra Budi. 2019. IT Impact on Business Model Changes in Banking Era 4.0: Case Study Jenius. Paper presented at 2nd International Conference of Computer and Informatics Engineering (IC2IE), Banyuwangi, Indonesia, September 10–11; pp. 53–57. [Google Scholar]

- Hawaldar, Iqbal Thonse, Mithun S. Ullal, Felicia Ramona Birau, and Cristi Marcel Spulbar. 2019. Trapping Fake Discounts as Drivers of Real Revenues and Their Impact on Consumer’s Behavior in India: A Case Study. Sustainability 11: 4637. [Google Scholar] [CrossRef]

- He, Wu, and Lida Xu. 2015. A state-of-the-art survey of cloud manufacturing. International Journal of Computer Integrated Manufacturing 28: 239–50. [Google Scholar] [CrossRef]

- Heffernan, Shelagh. 2005. Modern Banking. Chichester: John Wiley & Sons, Ltd. [Google Scholar]

- Herčko, J., E. Slamková, and J. Hnát. 2015. Industry 4.0—New era of manufacturing. Proceedings of InvEnt 2015: Industrial Engineering–From Integration to Innovation 1: 80–83. [Google Scholar]

- Hu, Han, Yonggang Wen, Tat-Seng Chua, and Xuelong Li. 2014. Toward scalable systems for big data analytics: A technology tutorial. IEEE Access 2: 652–87. [Google Scholar]

- Huang, Taoying. 2017. Development of Small-scale Intelligent Manufacturing System (SIMS)—A case study at Stella Polaris. Master’s thesis, AS UIT Faculty of Engineering Science and Technology the Artic University of Norway, Narvik, Norway. [Google Scholar]

- Hyder, Akmal S. 2013. Interest-free banking in Sweden: How much is it Islamic? Paper presented at the Second International Conference on Emerging Research Paradigms in Business and Social Sciences, Dubai, UAE, November 26–28. [Google Scholar]

- IBM Business Partner Directory. 2018. Available online: https://www.ibm.com/partnerworld/public (accessed on 10 March 2017).

- Ielasi, Federica, and Giulia Vichi. 2013. A particular model of interest-free bank: The case of JAK bank in Italy. Available online: www.jakitalia.it (accessed on 10 March 2017).

- Janev, Valentina, and Sanja Vraneš. 2011. Applicability assessment of semantic web technologies. Information Processing & Management 47: 507–17. [Google Scholar]

- Jasińska, Katarzyna, and Bartosz Jasiński. 2019. Conditions of a Corporate Communication in the Industry 4.0: Case Study. IBIMA Publishing 1: 1–15. [Google Scholar]

- Kagermann, Henning, Johannes Helbig, Ariane Hellinger, and Wolfgang Wahlster. 2013. Recommendations for implementing the strategic initiative INDUSTRIE 4.0: Securing the future of German manufacturing industry. Final Report of the Industrie 4.0 Working Group. Munich: Forschungsunion. [Google Scholar]

- Kandırmaz, Ebru Özdoğru, and Ufuk Tiryaki. 2018. A Real Time Price Sharing Architecture for Open Banking. Paper presented at 7th Turkish National Software Architecture Conference, Istanbul, Turkey, November 29. [Google Scholar]

- Khan, Ateeq, and Klaus Turowski. 2016. A Perspective on Industry 4.0: From Challenges to Opportunities in Production Systems. Paper presented at the International Conference on Internet of Things and Big Data (IoTBD2016), Rome, Italy, April 23–25; pp. 441–48. [Google Scholar]

- Khan, Wasim Ahmed, Abdul Raouf, and Kai Cheng. 2011. Augmented reality for manufacturing. In Virtual Manufacturing. Edited by W. A. Khan, A. Raouf and K. Cheng. Heidelberg: Springer, pp. 1–56. [Google Scholar]

- Kocian, Jiri, Michal Tutsch, Stepan Ozana, and Jiri Koziorek. 2012. Application of modeling and simulation techniques for technology units in industrial control. In Frontiers in Computer Education. Edited by Sambath Sabo and Egui Zhu. Heidelberg: Springer, pp. 491–99. [Google Scholar]

- Koesworo, Yulius, Ninuk Muljani, and Lena Ellitan. 2019. Fintech in the industrial revolution era 4.0. International Journal of Research Culture Society 3: 53–56. [Google Scholar]

- Kolberg, Dennis, Joshua Knobloch, and Detlef Zuehlke. 2017. Towards a lean automation interface for workstations. International Journal of Production Research 55: 2845–56. [Google Scholar] [CrossRef]

- KPMG. 2017. The Pulse of Fintech Q2 2017 Global Analysis of Investment in Fintech. Available online: www.kpmg.com/fintechpulse (accessed on 19 June 2019).

- KPMG. 2018. Global Analysis of Investment in Unicorn Companies. Available online: https://home.kpmg/xx/en/home/campaigns/2018/12/global-review.html (accessed on 19 June 2019).

- Landscheidt, Steffen, and Mirka Kans. 2016. Automation practices in wood product industries: Lessons learned, current practices and future perspectives. Paper presented at 7th Swedish Production Symposium SPS, Lund, Sweden, October 25–27. [Google Scholar]

- LaValle, Steve, Eric Lesser, Rebecca Shockley, Michael S. Hopkins, and Nina Kruschwitz. 2011. Big data, analytics and the path from insights to value. MIT Sloan Management Review 52: 21–32. [Google Scholar]

- Lee, In, and Yong Jae Shin. 2018. Fintech: Ecosystem, Business Models, Investment Decisions, and Challenges. Business Horizons 61: 35–46. [Google Scholar] [CrossRef]

- Lee, Jay, Behrad Bagheri, and Hung-An Kao. 2015. A cyber-physical systems architecture for Industry 4.0-based manufacturing systems. Manufacturing Letters 3: 18–23. [Google Scholar] [CrossRef]

- Leonard, Kenneth. 2019. Banking Rules for Non-Profit Organizations, Small Business, Business Models & Organizational Structure. Available online: https://smallbusiness.chron.com/banking-rules-non-profit-organizations-829.html (accessed on 28 December 2019).

- Lu, Yang. 2017. Industry 4.0: A survey on technologies, applications and open research issues. Journal of Industrial Information Integration 6: 1–10. [Google Scholar] [CrossRef]

- Lee, Min Hwa, Jin Hyo Joseph Yun, Andreas Pyka, Dong Kyu Won, Fumio Kodama, Giovanni Schiuma, Hang Sik Park, Jeonghwan Jeon, Kyung Bae Park, Kwang Ho Jung, and et al. 2018. How to Respond to the Fourth Industrial Revolution, or the Second Information Technology Revolution? Journal of Open Innovation: Technology, Market, Complexity 4: 21. [Google Scholar] [CrossRef]

- Martinez, Felipe, Petr Jirsak, and Miroslav Lorenc. 2016. Industry 4.0. The end lean management. Paper presented at 10th International Days of Statistics and Economics, Prague, Czech Republic, September 8–10. [Google Scholar]

- McKinney, Tonya. 2014. Omni-Channel Banking Customer Experience: Forget What You thought You Knew about Channels. Available online: https://docplayer.net/18988425-Omni-channel-banking-customer-experience-forget-what-you-thought-you-knew-about-channels.html (accessed on 3 December 2019).

- Mehnen, Jörn, Hongmei He, Stefano Tedeschi, and Nikolaos Tapoglou. 2017. Practical security aspects of the internet of things. In Cybersecurity for Industry 4.0. Edited by Lane Thames and Dirk Schaefer. Heidelberg: Springer, pp. 225–42. [Google Scholar]

- Mekinjić, Boško. 2019. The impact of industry 4.0 on the transformation of the banking sector. Journal of Contemporary Economics 1. [Google Scholar] [CrossRef]

- Mlađenović, Srđan. 2018. Banking Industry 4.0: Robotic Automation as an Answer to the Challenges of Tomorrow. Available online: https://www.comtradeintegration.com/en/banking-in-industry-4-0-robotic-automation-as-an-answer-to-the-challenges-of-tomorrow (accessed on 15 April 2020).

- Mohamed, Mamad. 2018. Challenges and Benefits of Industry 4.0: An overview. International Journal of Supply and Operations Management 5: 256–65. [Google Scholar]

- Muscio, Alessandro, and Andrea Ciffolilli. 2019. What drives the capacity to integrate Industry 4.0 technologies? Evidence from European R&D projects. Economics of Innovation and New Technology 29: 1–15. [Google Scholar]

- Nethravathi, Periyapatna, Sathyanarayana Rao, Gokarna Vidya Bai, Cristi Spulbar, Mendon Suhan, Ramona Birau, Toni Calugaru, Iqbal Thonse Hawaldar, and Abdullah Ejaz. 2020. Business intelligence appraisal based on customer behaviour profile by using hobby based opinion mining in India: A case study. Economic Research -EkonomskaIstraživanja 33: 1889–908. [Google Scholar] [CrossRef]

- Oliveira, Tiago, Manoj Thomas, and Mariana Espadanal. 2014. Assessing the determinants of cloud computing adoption: An analysis of the manufacturing and services sectors. Information & Management 51: 497–510. [Google Scholar]

- Ooi, Keng-Boon, Voon-Hsien Lee, Garry Wei-Han Tan, Teck-Soon Hew, and Jun-Jie Hew. 2018. Cloud computing in manufacturing: The next industrial revolution in Malaysia? Expert Systems with Applications 93: 376–94. [Google Scholar] [CrossRef]

- Open Banking Homepage. 2018. Available online: https://www.openbanking.org.uk/customers (accessed on 10 September 2018).

- Pagliosa, Marcos, Guilherme Tortorella, and Joao Carlos Espindola Ferreira. 2019. Industry 4.0 and Lean Manufacturing A systematic literature review and future research directions. Journal of Manufacturing Technology Management, Emerald Publishing Limited 1741–038X. [Google Scholar] [CrossRef]

- PwC. 2017. Global FinTech Report. Available online: https://www.pwc.com/fintechreport (accessed on 24 April 2020).

- Romao, Mário, Joao Costa, and Carlos J. Costa. 2019. Robotic Process Automation: A Case Study in the Banking Industry. Paper presented at 14th Iberian Conference on Information Systems and Technologies (CISTI), Coimbra, Portugal, June 19–22; pp. 1–6. [Google Scholar]

- Rosman, Tobias. 2015. Investigating Omni-Channel Banking Opportunities in Sweden: From a User Perspective. Stockholm: KHT Royal Institute of Technology, School of Computer Science and Communication. [Google Scholar]

- Rossini, Matteo, Federica Costa, Guilherme L. Tortorella, and Alberto Portioli-Staudacher. 2019. The interrelation between Industry 4.0 and lean production: An empirical study on European manufacturers. The International Journal of Advanced Manufacturing Technology 102: 3963–76. [Google Scholar] [CrossRef]

- Rüamann, Michael, Markus Lorenz, Philipp Gerbert, Manuela Waldner, Jan Justus, Pascal Engel, and Michael Harnisch. 2015. Industry 4.0: The future of productivity and growth in manufacturing industries. Boston Consulting Group 9: 54–89. [Google Scholar]

- Saghiri, Soroosh, Richard Wilding, Carlos Mena, and Michael Bourlakis. 2017. Toward a three-dimensional framework for omni-channel. Journal of Business Research 77: 53–67. [Google Scholar] [CrossRef]

- Sanders, Adam, Chola Elangeswaran, and Jens P. Wulfsberg. 2016. Industry 4.0 implies lean manufacturing: Research activities in industry 4.0 function as enablers for lean manufacturing. Journal of Industrial Engineering and Management 9: 811–33. [Google Scholar] [CrossRef]

- Santorella, Gary. 2017. Lean Culture for the Construction Industry: Building Responsible and Committed Project Teams. New York: Productivity Press. [Google Scholar]

- Saravanan, K., and K. Muthu Lakshmi. 2016. A Study on Banking Services of New Generation Banking in the Indian Banking Sector. Purakala with ISSN 0971-2143 is an UGC CARE Journal 31: 552–61. [Google Scholar]

- Schuh, Günther, Reiner Anderl, Jürgen Gausemeier, Michael ten Hompel, and Wolfgang Wahlster, eds. 2017. Industrie 4.0 Maturity Index: Managing the Digital Transformation of Companies. Acatech Study. Munich: Utz, Herbert. [Google Scholar]

- SCOOP. 2017. Industry 4.0: The Fouth Industrial Revolution Guide to Industrie 4.0. Available online: www.i-scoop.eu/industry-4-0/ (accessed on 6 June 2017).

- Dasho, Anni, Elvin Meka, Genci Sharko, and Indrit Baholli. 2017. Digital Banking the Wave of the Future. Paper presented at ISTI 2016: The New Paradigm for a Smarter Economy, Tirana, Albania, June 17–18. [Google Scholar]

- Sikorski, Janusz J., Joy Haughton, and Markus Kraft. 2017. Blockchain technology in the chemical industry: Machine-to-machine electricity market. Applied Energy 195: 234–46. [Google Scholar] [CrossRef]

- Simpson, John. 2002. The impact of the Internet in banking, Observations and evidence from developed and emerging markets. Telematics and Informatics Journal 19: 315–30. [Google Scholar] [CrossRef]

- Ślusarczyk, Beata. 2018. Industry 4.0—Are we ready? Polish Journal of Management Studies 17: 232–48. [Google Scholar] [CrossRef]

- Sohrab Uddin, S. M., and S. Mahmood Sohel. 2018. Performance of Fourth Generation Private Banks in Bangladesh: An Evaluation. In 9th PIMG International Conference, Prestige Institute of Management. Gwalior: Jiwaji University. [Google Scholar]

- Spulbar, Cristi, and Ramona Birau. 2019a. Emerging Research on Monetary Policy, Banking, and Financial Markets. Pennsylvania: IGI Global. 322p. [Google Scholar]

- Spulbar, Cristi, and Ramona Birau. 2019b. Financial Technology and Disruptive Innovation in ASEAN (book). In The Effects of Cybercrime on the Banking Sector in ASEAN. Pennsylvania: IGIGlobal, chp. 7. [Google Scholar]

- Srivastava, Utkarsh, and Santosh Gopalkrishnan. 2015. Impact of Big Data Analytics on Banking Sector: Learning for Indian Banks, 2nd International Symposium on Big Data and Cloud Computing (ISBCC’15). Procedia Computer Science 50: 643–52. [Google Scholar] [CrossRef]

- Stock, Tim, and Günther Seliger. 2016. Opportunities of Sustainable Manufacturing in Industry 4.0, 13th Global Conference on Sustainable Manufacturing—Decoupling Growth from Resource Use. Procedia CIRP 40: 536–41. [Google Scholar] [CrossRef]

- Tamás, Péter, and Béla Illés. 2016. Process improvement trends for manufacturing systems in Industry 4.0. Academic Journal of Manufacturing Engineering 14: 119–25. [Google Scholar]

- Thames, Lane, and Dirk Schaefer. 2017. Industry 4.0: An overview of key benefits, technologies, and challenges. In Cybersecurity for Industry 4.0. Edited by Lane Thames and Dirk Schaefer. Heidelberg: Springer, pp. 1–33. [Google Scholar]

- Temenos. 2018. Annual Reportand Accounts. Available online: https://www.temenos.com/wp-content/uploads/2019/07/2018-annual-report-2019-mar-26.pdf (accessed on 30 October 2019).

- Thuluva, Aparna Saisree, Darko Anicic, and Sebastian Rudolph. 2017. Semantic web of things for Industry 4.0. Paper presented at the Doctoral Consortium, Challenge, Industry Track, Tutorials and Posters, London, UK; pp. 11–15. [Google Scholar]

- Turk Ariss, R. 2008. Financial liberalization and bank efficiency: Evidence from post-war Lebanon. Applied Financial Economics 18: 931–46. [Google Scholar] [CrossRef]

- Underwood, Sarah. 2016. Blockchain beyond Bitcoin. Communications of the ACM 59: 15–17. [Google Scholar] [CrossRef]

- Vaidya, Saurabh, Prashant Ambad, and Santosh Bhosle. 2018. Industry 4.0—A Glimpse. Procedia Manufacturing 20: 233–38. [Google Scholar] [CrossRef]

- Wang, Gang, Angappa Gunasekaran, Eric W.T. Ngai, and Thanos Papadopoulos. 2016a. Big data analytics in logistics and supply chain management: Certain investigations for research and applications. International Journal of Production Economics 176: 98–110. [Google Scholar] [CrossRef]

- Wang, Shiyong, Jiafu Wan, Daqiang Zhang, Di Li, and Chunhua Zhang. 2016b. Towards smart factory for Industry 4.0: A self-organized multi-agent system with big data based feedback and coordination. Computer Networks 101: 158–68. [Google Scholar] [CrossRef]

- Williams, Bob, and Mark Anielski. 2004. An Assessment of Sweden’s No-Interest Bank. Available online: www.anielski.com (accessed on 15 March 2017).

- Xu, Yuchun, and Mu Chen. 2016. Improving just-in-time manufacturing operations by using internet of things based solutions. Procedia CIRP 56: 326–31. [Google Scholar] [CrossRef]

- Yew, A. W. W., S. K. Ong, and Andrew Y. C. Nee. 2016. Towards a Griddable distributed manufacturing system with augmented reality interfaces. Robotics and Computer-Integrated Manufacturing 39: 43–55. [Google Scholar] [CrossRef]

- Zambon, Ilaria, Massimo Cecchini, Gianluca Egidi, Maria Grazia Saporito, and Andrea Colantoni. 2019. Revolution 4.0: Industry vs. agriculture ina future development for SMEs. Processes 7: 36. [Google Scholar] [CrossRef]

- Zuehlke, Detlef. 2010. SmartFactory—Towards a factory-of-things. Annual Reviews in Control 34: 129–38. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Difference | JAK Bank | Other Banks |

|---|---|---|

| Customers | Partner-centric, joint venture, one-vote-one-share model | Based on customer-centric model and activity sharing |

| Bank system | A fully savings-based system, loans are based on savings. On the other hand, loans are fully backed by member savings | Partial storage system; when a loan is granted, new money enters the bank through retained earnings. The loan is not backed by other investors. Only a small amount of the required loan is protected by the private bank. Of course, under the supervision of the central bank. Money saving in private banks in the United States is between 1% and 3%. |

| Loans | Loans are offered on the basis of deposit and member capacity, and the sole purpose is to repay the loan | Loans are repaid on the basis of the customer’s credit value, and loan repayments include the principal and interest of the money. |

| Interest on loans | Interest is not credited, but the price of executive services is reviewed annually | All loans and credits accrue interest. |

| Interest on deposits | For deposits, interest is not paid, but concessions are granted equal benefits | The deposits accrue interest, but it is not so high. |

| Investor Profits | JAK Bank does not operate similar toother banks. Does not even benefit from the loans | Other banks obtain a return on their investment based on value and profitability results, which is used to pay employees and so on. |

| The Main Criteria | Islamic Banking | JAK |

|---|---|---|

| Ownership | The shareholders own the bank | Members own the bank |

| Taking Part | Shareholders participate by sharing capital | Members, especially the borrowers, contribute capital |

| Main Products | Profit and loss sharing, joint venture, leasing | Savings and lending |

| Attributes | Spirituality, ethics, rationality and philanthropy | Economic freedom, justice, democracy, shared responsibility, and no interest |

| The Cost of Loans | No interest | No interest |

| Marketing | Using experienced media similar to traditional banks | Selective and informative, regular efforts to train members and customers of the bank |

| Vision | Borrowers have to make long-term savings | Borrowers do not have to make long-term savings |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mehdiabadi, A.; Tabatabeinasab, M.; Spulbar, C.; Karbassi Yazdi, A.; Birau, R. Are We Ready for the Challenge of Banks 4.0? Designing a Roadmap for Banking Systems in Industry 4.0. Int. J. Financial Stud. 2020, 8, 32. https://doi.org/10.3390/ijfs8020032

Mehdiabadi A, Tabatabeinasab M, Spulbar C, Karbassi Yazdi A, Birau R. Are We Ready for the Challenge of Banks 4.0? Designing a Roadmap for Banking Systems in Industry 4.0. International Journal of Financial Studies. 2020; 8(2):32. https://doi.org/10.3390/ijfs8020032

Chicago/Turabian StyleMehdiabadi, Amir, Mariyeh Tabatabeinasab, Cristi Spulbar, Amir Karbassi Yazdi, and Ramona Birau. 2020. "Are We Ready for the Challenge of Banks 4.0? Designing a Roadmap for Banking Systems in Industry 4.0" International Journal of Financial Studies 8, no. 2: 32. https://doi.org/10.3390/ijfs8020032

APA StyleMehdiabadi, A., Tabatabeinasab, M., Spulbar, C., Karbassi Yazdi, A., & Birau, R. (2020). Are We Ready for the Challenge of Banks 4.0? Designing a Roadmap for Banking Systems in Industry 4.0. International Journal of Financial Studies, 8(2), 32. https://doi.org/10.3390/ijfs8020032