Evidence of Intraday Multifractality in European Stock Markets during the Recent Coronavirus (COVID-19) Outbreak

Abstract

1. Introduction

2. Materials and Methods

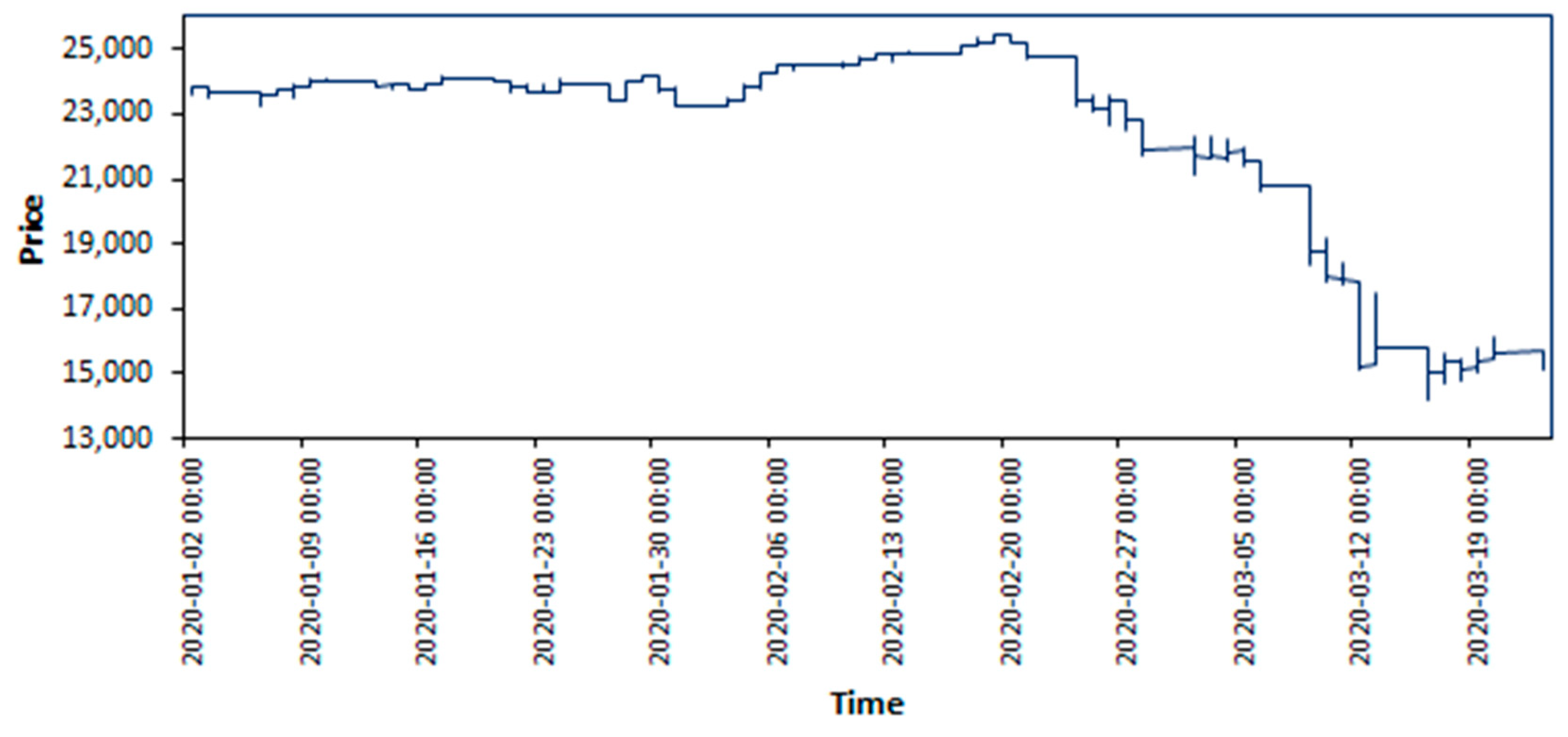

2.1. Data Description

2.2. Methodology

2.2.1. Stage 1

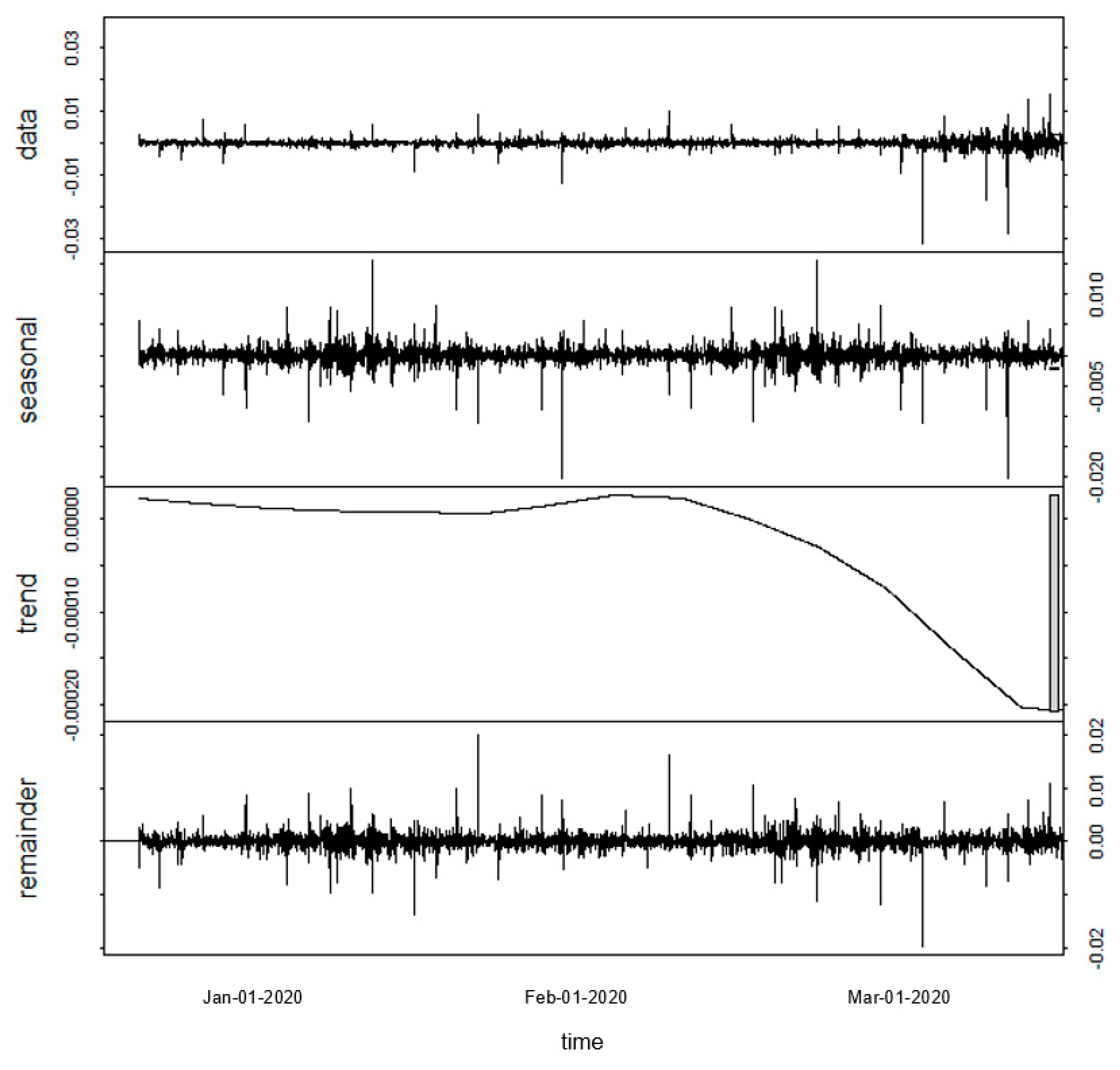

2.2.2. Stage 2: Seasonal and Trend Decomposition using Loess (STL)

2.2.3. Stage 3: Multifractal Detrended Fluctuation Analysis (MFDFA)

3. Results

4. Discussion

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- Adrangi, Bahram, Arjun Chatrath, Kanwalroop Kathy Dhanda, and Kambiz Raffiee. 2001. Chaos in oil prices? Evidence from futures markets. Energy Economics 23: 405–25. [Google Scholar] [CrossRef]

- Alvarez-Ramirez, Jose, Jesus Alvarez, and Eduardo Rodriguez. 2008. Short-term predictability of crude oil markets: A detrended fluctuation analysis approach. Energy Economics 30: 2645–56. [Google Scholar] [CrossRef]

- Bachelier, Louis. 1900. Theory of Speculation in the Random Character of Stock Market Prices. Cambridge: MIT. [Google Scholar]

- Barabási, Albert-László, and Tamás Vicsek. 1991. Multifractality of self-affine fractals. Physical Review A 44: 2730. [Google Scholar] [CrossRef]

- Bowe, Michael, and Daniela Domuta. 2004. Investor herding during financial crisis: A clinical study of the Jakarta Stock Exchange. Pacific-Basin Finance Journal 12: 387–418. [Google Scholar] [CrossRef]

- Cajueiro, Daniel, and Benjamin Tabak. 2004. Evidence of long range dependence in Asian equity markets: The role of liquidity and market restrictions. Physica A: Statistical Mechanics and Its Applications 342: 656–64. [Google Scholar] [CrossRef]

- Cajueiro, Daniel, Periklis Gogas, and Benjamin Tabak. 2009. Does financial market liberalization increase the degree of market efficiency? The case of the Athens stock exchange. International Review of Financial Analysis 18: 50–57. [Google Scholar] [CrossRef]

- Caraiani, Petre. 2012. Evidence of multifractality from emerging European stock markets. PLoS ONE 7: 40693. [Google Scholar] [CrossRef]

- Chang, Eric, Joseph Cheng, and Ajay Khorana. 2000. An examination of herd behavior in equity markets: An international perspective. Journal of Banking & Finance 24: 1651–79. [Google Scholar]

- Christodoulou-Volos, Christos, and Fotios Siokis. 2006. Long range dependence in stock market returns. Applied Financial Economics 16: 1331–38. [Google Scholar] [CrossRef]

- Ciner, Cetin, and Ahmet Karagozoglu. 2008. Information asymmetry, speculation and foreign trading activity: Emerging market evidence. International Review of Financial Analysis 17: 664–80. [Google Scholar] [CrossRef]

- Cleveland, Robert, William Cleveland, Jean McRae, and Irma Terpenning. 1990. STL: A seasonal-trend decomposition. Journal of Official Statistics 6: 3–73. [Google Scholar]

- Domino, Krzysztof. 2011. The use of the Hurst exponent to predict changes in trends on the Warsaw Stock Exchange. Physica A: Statistical Mechanics and Its Applications 390: 98–109. [Google Scholar] [CrossRef]

- Dragotă, Victor, and Elena Ţilică. 2014. Market efficiency of the Post Communist East European stock markets. Central European Journal of Operations Research 22: 307–37. [Google Scholar] [CrossRef]

- Epstein, Larry, and Tan Wang. 2004. Intertemporal asset pricing under Knightian uncertainty. In Uncertainty in Economic Theory. London: Routledge, pp. 445–87. [Google Scholar]

- Ferreira, Paulo. 2018. Long-range dependencies of Eastern European stock markets: A dynamic detrended analysis. Physica A: Statistical Mechanics and Its Applications 505: 454–70. [Google Scholar] [CrossRef]

- Gopikrishnan, Parameswaran, Vasiliki Plerou, Xavier Gabaix, Luís Amaral, and Harry Stanley. 2001. Price fluctuations and market activity. Physica A: Statistical Mechanics and Its Applications 299: 137–43. [Google Scholar] [CrossRef]

- He, Ling-Yun, Ying Fan, and Yi-Ming Wei. 2007. The empirical analysis for fractal features and long-run memory mechanism in petroleum pricing systems. International Journal of Global Energy Issues 27: 492–502. [Google Scholar] [CrossRef]

- Horta, Paulo, Sérgio Lagoa, and Luis Martins. 2014. The impact of the 2008 and 2010 financial crises on the Hurst exponents of international stock markets: Implications for efficiency and contagion. International Review of Financial Analysis 35: 140–53. [Google Scholar] [CrossRef]

- Jagric, Timotej, Boris Podobnik, and Marko Kolanovic. 2005. Does the Efficient Market Hypothesis Hold? Evidence from Six Transition Economies. Eastern European Economics 43: 79–103. [Google Scholar] [CrossRef]

- Kantelhardt, Jan, Stephan Zschiegner, Eva Koscielny-Bunde, Shlomo Havlin, Armin Bunde, and Harry Stanley. 2002. Multifractal detrended fluctuation analysis of nonstationary time series. Physica A: Statistical Mechanics and its Applications 316: 87–114. [Google Scholar] [CrossRef]

- Kim, Seunghwan, and Cheoljun Eom. 2008. Long-term memory and volatility clustering in high-frequency price changes. Physica A: Statistical Mechanics and Its Applications 387: 1247–54. [Google Scholar]

- Kumar, Sunil, and Nivedita Deo. 2009. Multifractal properties of the Indian financial market. Physica A: Statistical Mechanics and Its Applications 388: 1593–602. [Google Scholar] [CrossRef]

- Laib, Mohamed, Jean Golay, Luciano Telesca, and Mikhail Kanevski. 2018a. Multifractal analysis of the time series of daily means of wind speed in complex regions. Chaos, Solitons & Fractals 109: 118–27. [Google Scholar]

- Laib, Mohamed, Luciano Telesca, and Mikhail Kanevski. 2018b. Long-range fluctuations and multifractality in connectivity density time series of a wind speed monitoring network. Chaos: An Interdisciplinary Journal of Nonlinear Science 28: 033108. [Google Scholar] [CrossRef]

- Levy, Ori, and Itai Galili. 2006. Terror and trade of individual investors. The Journal of Socio-Economics 35: 980–91. [Google Scholar] [CrossRef]

- Mandelbrot, Benoit. 1967. The variation of some other speculative prices. The Journal of Business 40: 393–413. [Google Scholar] [CrossRef]

- Mandelbrot, Benoit. 1971. When can price be arbitraged efficiently? A limit to the validity of the random walk and martingale models. The Review of Economics and Statistics 53: 225–36. [Google Scholar] [CrossRef]

- Mandelbrot, Benoit. 1997. The variation of the prices of cotton, wheat, and railroad stocks, and of some financial rates. In Fractals and Scaling in Finance. Berlin: Springer, pp. 419–43. [Google Scholar]

- Mandelbrot, Benoit, Adlai J Fisher, and Laurent E Calvet. 1997. A Multifractal Model of Asset Returns. Cowles Foundation Discussion Papers 1164. New Haven: Yale University, Cowles Foundation for Research in Economics. [Google Scholar]

- McGavin, Katherine. 2010. Short selling in a financial crisis: The regulation of short sales in the United Kingdom and the United States. Northwestern Journal of International Law & Business 30: 201–39. [Google Scholar]

- Miloş, Laura Raisa, Cornel Haţiegan, Marius Cristian Miloş, Flavia Mirela Barna, and Claudiu Boțoc. 2020. Multifractal Detrended Fluctuation Analysis (MF-DFA) of Stock Market Indexes. Empirical Evidence from Seven Central and Eastern European Markets. Sustainability 12: 535. [Google Scholar] [CrossRef]

- Mohti, Wahbeeah, Andreia Dionísio, Paulo Ferreira, and Isabel Vieira. 2019. Frontier markets’ efficiency: Mutual information and detrended fluctuation analyses. Journal of Economic Interaction and Coordination 14: 551–72. [Google Scholar] [CrossRef]

- Mukerji, Sujoy, and Jean-Marc Tallon. 2001. Ambiguity aversion and incompleteness of financial markets. The Review of Economic Studies 68: 883–904. [Google Scholar] [CrossRef]

- Norouzzadeh, Payam, and Bahareh Rahmani. 2006. A multifractal detrended fluctuation description of Iranian rial–US dollar exchange rate. Physica A: Statistical Mechanics and Its Applications 367: 328–36. [Google Scholar] [CrossRef]

- Oh, Gabjin, Seunghwan Kim, and Cheoljun Eom. 2010. Multifractal Analysis of Korean Stock Market. Journal of the Korean Physical Society 56: 982–85. [Google Scholar] [CrossRef]

- Peng, Chung-Kang, Sergey Buldyrev, Shlomo Havlin, Michael Simons, Harry Eugene Stanley, and Ary Goldberger. 1994. Mosaic organization of DNA nucleotides. Physical Review 49: 1685. [Google Scholar] [CrossRef]

- Peters, Edgar. 1991. Chaos and Order in the Capital Markets, A New View of Cycles, Prices and Market Volatility. New York: John Wiley Sons, Inc. [Google Scholar]

- Peters, Edgar. 1994. Fractal Market Analysis: Applying Chaos Theory to Investment and Economics. New York: John Wiley & Sons, vol. 24. [Google Scholar]

- Pleşoianu, Anita, Alexandru Todea, and Răzvan Căpuşan. 2012. The informational efficiency of the Romanian stock market: Evidence from fractal analysis. Procedia Economics and Finance 3: 111–18. [Google Scholar] [CrossRef]

- Podobnik, Boris, and Harry Stanley. 2008. Detrended cross-correlation analysis: A new method for analyzing two nonstationary time series. Physical Review Letters 100: 084102. [Google Scholar] [CrossRef]

- Rizvi, Syed, and Shaista Arshad. 2016. How does crisis affect efficiency? An empirical study of East Asian markets. Borsa Istanbul Review 16: 1–8. [Google Scholar] [CrossRef]

- Rizvi, Syed, Ginanjar Dewandaru, Obiyathulla Bacha, and Mansur Masih. 2014. An analysis of stock market efficiency: Developed vs. Islamic stock markets using MF-DFA. Physica A: Statistical Mechanics and Its Applications 407: 86–99. [Google Scholar] [CrossRef]

- Ruan, Yong-Ping, and Wei-Xing Zhou. 2011. Long-term correlations and multifractal nature in the intertrade durations of a liquid Chinese stock and its warrant. Physica A: Statistical Mechanics and Its Applications 390: 1646–54. [Google Scholar] [CrossRef]

- Shahzad, Syed Jawad Hussain, Jose Areola Hernandez, Waqas Hanif, and Ghulam Mujtaba Kayani. 2018. Intraday return inefficiency and long memory in the volatilities of forex markets and the role of trading volume. Physica A: Statistical Mechanics and Its Applications 506: 433–50. [Google Scholar] [CrossRef]

- Shiskin, Julius. 1965. The X-11 Variant of the Census Method II Seasonal Adjustment Program; Washington: US Government Printing Office.

- Sukpitak, Jessada, and Varagorn Hengpunya. 2016. Efficiency of Thai stock markets: Detrended fluctuation analysis. Physica A: Statistical Mechanics and Its Applications 458: 204–9. [Google Scholar] [CrossRef]

- Telesca, Luciano, Vincenzo Lapenna, and Maria Macchiato. 2005. Multifractal fluctuations in seismic interspike series. Physica A: Statistical Mechanics and Its Applications 354: 629–40. [Google Scholar] [CrossRef]

- Wang, Yudong, Yu Wei, and Chongfeng Wu. 2010. Cross-correlations between Chinese A-share and B-share markets. Physica A: Statistical Mechanics and Its Applications 389: 5468–78. [Google Scholar] [CrossRef]

- Yuan, Ying, Xin-tian Zhuang, and Xiu Jin. 2009. Measuring multifractality of stock price fluctuation using multifractal detrended fluctuation analysis. Physica A: Statistical Mechanics and Its Applications 388: 2189–97. [Google Scholar] [CrossRef]

- Zhou, Rhea, and Rose Lai. 2009. Herding and information based trading. Journal of Empirical Finance 16: 388–93. [Google Scholar] [CrossRef]

- Zunino, Luciano, Benjamin Miranda Tabak, Alejandra Figliola, Dario Pérez, Mario Garavaglia, and Osvaldo Rosso. 2008. A multifractal approach for stock market inefficiency. Physica A: Statistical Mechanics and Its Applications 387: 6558–66. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| S.No. | Country | Index Symbol | Observations (5 min Interval) |

|---|---|---|---|

| 1 | Italy | FTSMIB | 5916 |

| 2 | France | FCHI | 5916 |

| 3 | Germany | GDAXI | 5916 |

| 4 | Spain | IBEX | 5916 |

| 5 | Belgium | BFX | 5916 |

| 6 | Austria | ATX | 5916 |

| 7 | Netherlands | AAX | 5916 |

| 8 | UK | FTSE | 5916 |

| Order q | Italy | France | Germany | Spain | Austria | Belgium | Netherlands | UK |

|---|---|---|---|---|---|---|---|---|

| −10 | 0.80 | 0.83 | 0.80 | 0.79 | 0.93 | 0.88 | 0.87 | 0.82 |

| −8 | 0.79 | 0.81 | 0.78 | 0.77 | 0.91 | 0.86 | 0.85 | 0.80 |

| −6 | 0.76 | 0.77 | 0.75 | 0.74 | 0.88 | 0.82 | 0.81 | 0.77 |

| −4 | 0.72 | 0.72 | 0.70 | 0.70 | 0.83 | 0.76 | 0.75 | 0.72 |

| −2 | 0.66 | 0.65 | 0.63 | 0.63 | 0.76 | 0.68 | 0.67 | 0.64 |

| 0 | 0.57 | 0.55 | 0.54 | 0.54 | 0.66 | 0.59 | 0.56 | 0.54 |

| 2 | 0.45 | 0.43 | 0.43 | 0.43 | 0.52 | 0.49 | 0.45 | 0.43 |

| 4 | 0.34 | 0.34 | 0.33 | 0.34 | 0.39 | 0.41 | 0.37 | 0.32 |

| 6 | 0.28 | 0.28 | 0.27 | 0.28 | 0.32 | 0.36 | 0.32 | 0.26 |

| 8 | 0.24 | 0.25 | 0.24 | 0.25 | 0.28 | 0.32 | 0.28 | 0.22 |

| 10 | 0.22 | 0.23 | 0.21 | 0.23 | 0.25 | 0.30 | 0.26 | 0.20 |

| ∆h | 0.59 | 0.60 | 0.59 | 0.56 | 0.68 | 0.58 | 0.61 | 0.63 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aslam, F.; Mohti, W.; Ferreira, P. Evidence of Intraday Multifractality in European Stock Markets during the Recent Coronavirus (COVID-19) Outbreak. Int. J. Financial Stud. 2020, 8, 31. https://doi.org/10.3390/ijfs8020031

Aslam F, Mohti W, Ferreira P. Evidence of Intraday Multifractality in European Stock Markets during the Recent Coronavirus (COVID-19) Outbreak. International Journal of Financial Studies. 2020; 8(2):31. https://doi.org/10.3390/ijfs8020031

Chicago/Turabian StyleAslam, Faheem, Wahbeeah Mohti, and Paulo Ferreira. 2020. "Evidence of Intraday Multifractality in European Stock Markets during the Recent Coronavirus (COVID-19) Outbreak" International Journal of Financial Studies 8, no. 2: 31. https://doi.org/10.3390/ijfs8020031

APA StyleAslam, F., Mohti, W., & Ferreira, P. (2020). Evidence of Intraday Multifractality in European Stock Markets during the Recent Coronavirus (COVID-19) Outbreak. International Journal of Financial Studies, 8(2), 31. https://doi.org/10.3390/ijfs8020031