The Lead–Lag Relationship between Oil Futures and Spot Prices—A Literature Review

Abstract

1. Introduction

2. Crude Oil Background

3. Spot and Futures Prices

4. Lead–Lag Relationship

4.1. Long Term Relationship

4.2. Short Term Relationship

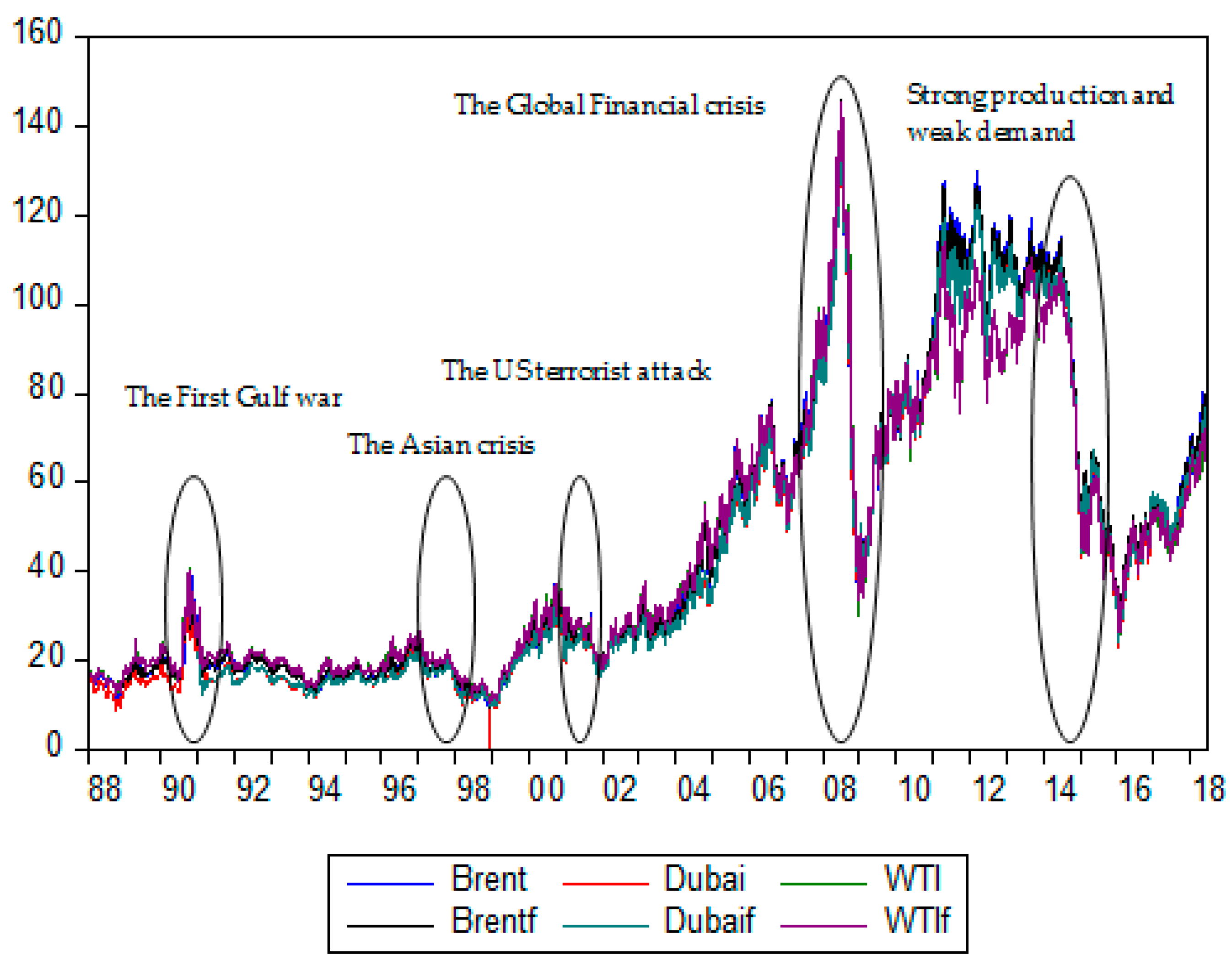

5. Major Shocks in the Oil Markets and Structural Breaks

5.1. The First Gulf War

5.2. The Asian Financial Crisis

5.3. The US Terrorist Attack

5.4. The Global Financial Crisis

6. Oil Volatility and Forecasting

7. Market Efficiency

8. What Have We Learned about the Lead–Lag Relationship?

9. Conclusions

Funding

Conflicts of Interest

References

- Agnolucci, Paolo. 2009. Volatility in crude oil futures: A comparison of the predictive ability of GARCH and implied volatility models. Energy Economics 31: 316–21. [Google Scholar] [CrossRef]

- Ahmadi, Maryam, Niaz Bashiri Behmiri, and Matteo Manera. 2016. How is volatility in commodity markets linked to oil price shocks? Energy Economics 59: 11–23. [Google Scholar] [CrossRef]

- Aloui, Chaker, and Samir Mabrouk. 2010. Value-at-risk estimations of energy commodities via long-memory, asymmetry and fat-tailed GARCH models. Energy Policy 38: 2326–39. [Google Scholar] [CrossRef]

- Alquist, Ron, and Lutz Kilian. 2010. What do we learn from the price of crude oil futures? Journal of Applied Econometrics 25: 539–73. [Google Scholar] [CrossRef]

- Alzahrani, Mohammed, Mansur Masih, and Omar Al-Titi. 2014. Linear and non-linear Granger causality between oil spot and futures prices: A wavelet based test. Journal of International Money and Finance 48: 175201. [Google Scholar] [CrossRef]

- Andriosopoulos, Kostas, Emilios Galariotis, and Spyros Spyrou. 2017. Contagion, Volatility Persistence and Volatility Spill-Overs: The Case of Energy Markets during the European Financial Crisis. Energy Economics 66: 217–27. [Google Scholar] [CrossRef]

- Arouri, Mohamed El Hedi, Shawkat Hammoudeh, Amine Lahiani, and Duc Khuong Nguyen. 2012. Long memory and structural breaks in modeling the return and volatility dynamics of precious metals. The Quarterly Review of Economics and Finance 52: 207–18. [Google Scholar] [CrossRef]

- Bagchi, Bhaskar. 2017. Volatility spillovers between crude oil price and stock markets: Evidence from BRIC countries. International Journal of Emerging Markets 12: 352–65. [Google Scholar] [CrossRef]

- Bekiros, Stelios D., and Cees G. H. Diks. 2008. The relationship between crude oil spot and futures prices: Cointegration, linear and nonlinear causality. Energy Economics 30: 2673–85. [Google Scholar] [CrossRef]

- Berghöfer, Britta, and Brian Lucey. 2014. Fuel hedging, operational hedging and risk exposure—Evidence from the global airline industry. International Review of Financial Analysis 34: 124–39. [Google Scholar] [CrossRef]

- Bouri, Elie. 2015. Oil volatility shocks and the stock markets of oil-importing MENA economies: A tale from the financial crisis. Energy Economics 51: 590–98. [Google Scholar] [CrossRef]

- Broadstock, David C., Ying Fan, Qiang Ji, and Dayong Zhang. 2016. Shocks and stocks: A bottom-up assessment of the relationship between oil prices, gasoline prices and the returns of Chinese firms. The Energy Journal 37: 55–86. [Google Scholar] [CrossRef]

- Büyükşahin, Bahattin, and Michel Robe. 2011. Speculators, Commodities and Cross-Market Linkages. Mimeo. Available online: http://www.ou.edu/content/dam/price/Finance/Oklahoma_conference/2011/Michel%20Robe%20paper.pdf (accessed on 3 April 2018).

- Candelon, Bertrand, Marc Joëts, and Sessi Tokpavi. 2013. Testing for Granger causality in distribution tails: An application to oil markets integration. Economic Modelling 31: 276–85. [Google Scholar] [CrossRef]

- CBOT. 2006. CBOT Handbook of Futures and Options. New York: McGraw-Hill. [Google Scholar]

- Chang, Chun-Ping, and Chien-Chiang Lee. 2015. Do oil spot and futures prices move together? Energy Economics 50: 379–90. [Google Scholar] [CrossRef]

- Chang, Chia-Lin, Michael McAleer, and Roengchai Tansuchat. 2011. Crude oil hedging strategies using dynamic multivariate GARCH. Energy Economics 33: 912–23. [Google Scholar] [CrossRef]

- Charfeddine, Lanouar. 2014. True or spurious long memory in volatility: Further evidence on the energy futures markets. Energy Policy 71: 76–93. [Google Scholar] [CrossRef]

- Charfeddine, Lanouar. 2016. Breaks or long range dependence in the energy futures volatility: Out-of-sample forecasting and VaR analysis. Economic Modelling 53: 354–74. [Google Scholar] [CrossRef]

- Charles, Amélie, and Olivier Darné. 2009. Variance-ratio tests of random walk: An overview. Journal of Economic Surveys 23: 503–27. [Google Scholar] [CrossRef]

- Charles, Amélie, and Olivier Darné. 2014. Volatility persistence in crude oil markets. Energy Policy 65: 729–42. [Google Scholar] [CrossRef]

- Chen, Pei-Fen, Chien-Chiang Lee, and Jhih-Hong Zeng. 2014. The relationship between spot and futures oil prices: Do structural breaks matter? Energy Economics 43: 206–17. [Google Scholar] [CrossRef]

- Chkili, Walid, Shawkat Hammoudeh, and Duc Khuong Nguyen. 2014. Volatility forecasting and risk management for commodity markets in the presence of asymmetry and long memory. Energy Economics 41: 1–18. [Google Scholar] [CrossRef]

- CME. 2018. CME Group. The Chicago Board of Trade. Available online: htpps://cmegroup.com// (accessed on 18 August 2018).

- Crowder, William J., and Anas Hamed. 1993. A cointegration test for oil futures market efficiency. Journal of Futures Markets 13: 933–41. [Google Scholar] [CrossRef]

- Davidson, Paul. 2008. Crude Oil Prices: “Market Fundamentals” or Speculation? Challenge 51: 110–18. [Google Scholar] [CrossRef]

- Ding, Haoyuan, Hyung-Gun Kim, and Sung Y. Park. 2014. Do net positions in the futures market cause spot prices in crude oil? Economic Modelling 41: 177–90. [Google Scholar] [CrossRef]

- Epstein, Gerald A., ed. 2005. Financialization and the World Economy. Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Fama, Eugene F. 1965. The behavior of stock-market prices. The Journal of Business 38: 34–105. [Google Scholar] [CrossRef]

- Fattouh, Bassam, Lutz Kilian, and Lavan Mahadeva. 2013. The role of speculation in oil markets: What have we learned so far? The Energy Journal 34: 7–33. [Google Scholar] [CrossRef]

- Ferderer, J. Peter. 1996. Oil price volatility and the macroeconomy. Journal of Macroeconomics 18: 1–26. [Google Scholar] [CrossRef]

- Fernandez, Viviana. 2004. Detection of Breakpoints in Volatility. Estudios de Administracion 11: 1–38. [Google Scholar]

- Fong, Wai Mun, and Kim Hock See. 2002. A Markov switching model of the conditional volatility of crude oil futures prices. Energy Economics 24: 71–95. [Google Scholar] [CrossRef]

- Forni, Lorenzo, Andrea Gerali, Alessandro Notarpietro, and Massimiliano Pisani. 2015. Euro Area, Oil and Global Shocks: An Empirical Model-Based Analysis. Journal of Macroeconomics 46: 295–314. [Google Scholar] [CrossRef]

- Ftiti, Zied, Ibrahim Fatnassi, and Aviral Kumar Tiwari. 2016. Neoclassical finance, behavioral finance and noise traders: Assessment of gold–oil markets. Finance Research Letters 17: 33–40. [Google Scholar] [CrossRef]

- Garbade, Kenneth D., and William L. Silber. 1983. Price Movements and Price Discovery in Futures and Cash Markets. The Review of Economics and Statistics 65: 289–97. [Google Scholar] [CrossRef]

- Gu, Rongbao, and Bing Zhang. 2016. Is efficiency of crude oil market affected by multifractality? Evidence from the WTI crude oil market. Energy Economics 53: 151–58. [Google Scholar] [CrossRef]

- Gu, Rongbao, Hongtao Chen, and Yudong Wang. 2010. Multifractal analysis on international crude oil markets based on the multifractal detrended fluctuation analysis. Physica A: Statistical Mechanics and its Applications 389: 2805–15. [Google Scholar] [CrossRef]

- Gujarati, Damodar N. 2009. Basic Econometrics. Delhi: Tata McGraw-Hill Education. [Google Scholar]

- Gülen, S. Gürcan. 1998. Efficiency in the crude oil futures market. Journal of Energy Finance & Development 3: 13–21. [Google Scholar]

- Hamilton, James D. 2003. What is an oil shock? Journal of Econometrics 113: 363–98. [Google Scholar] [CrossRef]

- Hamilton, James D. 2009. Causes and consequences of the oil shock of 2007-08. Brookings Papers on Economic Activity 40: 215–61. [Google Scholar] [CrossRef]

- Hamilton, James D. 2013. Historical Oil Shocks. In The Routledge Handbook of Major Events in Economic History. Edited by Randall E. Parker and Robert M. Whaples. New York: Routledge Taylor and Francis Group, pp. 239–65. [Google Scholar]

- Hamilton, James D. 2014. The Changing Face of World Oil Markets. No. w20355. New York: National Bureau of Economic Research. [Google Scholar]

- Haugom, Erik, and Rina Ray. 2017. Heterogeneous traders, liquidity, and volatility in crude oil futures market. Journal of Commodity Markets 5: 36–49. [Google Scholar] [CrossRef]

- Huang, Bwo-Nung, Chinwei Yang, and Mingjeng Hwang M. J. 2009. The dynamics of a nonlinear relationship between crude oil spot and futures prices: A multivariate threshold regression approach. Energy Economics 31: 91–98. [Google Scholar] [CrossRef]

- Irwin, Scott H., and Dwight R. Sanders. 2012. Testing the Masters Hypothesis in commodity futures markets. Energy Economics 34: 256–69. [Google Scholar] [CrossRef]

- Jiang, Zhi-Qiang, Wen-Jie Xie, and Wei-Xing Zhou. 2014. Testing the weak-form efficiency of the WTI crude oil futures market. Physica A: Statistical Mechanics and Its Applications 405: 235–44. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 1979. Prospect theory: An analysis of decision under risk. Econometrica 47: 263–91. [Google Scholar] [CrossRef]

- Kaufmann, Robert K. 2011. The role of market fundamentals and speculation in recent price changes for crude oil. Energy Policy 39: 105–15. [Google Scholar] [CrossRef]

- Kaufmann, Robert K., and Ben Ullman. 2009. Oil prices, speculation, and fundamentals: Interpreting causal relations among spot and futures prices. Energy Economics 31: 550–58. [Google Scholar] [CrossRef]

- Khediri, Karim Ben, and Lanouar Charfeddine. 2015. Evolving efficiency of spot and futures energy markets: A rolling sample approach. Journal of Behavioral and Experimental Finance 6: 67–79. [Google Scholar] [CrossRef]

- Kilian, Lutz. 2006. Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. American Economic Review 99: 1053–69. [Google Scholar] [CrossRef]

- Kilian, Lutz, and Cheolbeom Park. 2009. The impact of oil price shocks on the US stock market. International Economic Review 50: 1267–87. [Google Scholar] [CrossRef]

- Kim, Abby. 2015. Does futures speculation destabilise commodity markets? The Journal of Futures Markets 35: 696–714. [Google Scholar] [CrossRef]

- Klein, Tony, and Thomas Walther. 2016. Oil price volatility forecast with mixture memory GARCH. Energy Economics 58: 46–58. [Google Scholar] [CrossRef]

- Lambert, Emily. 2010. The Futures: The Rise of the Speculator and the Origins of the World’s Biggest Markets. New York: Basic Books. [Google Scholar]

- Lean, Hooi Hooi, Michael McAleer, and Wing-Keung Wong. 2010. Market efficiency of oil spot and futures: A mean-variance and stochastic dominance approach. Energy Economics 32: 979–86. [Google Scholar] [CrossRef]

- Lee, Chien-Chiang, and Jhih-Hong Zeng. 2011. Revisiting the relationship between spot and futures oil prices: Evidence from quantile cointegrating regression. Energy Economics 33: 924–35. [Google Scholar] [CrossRef]

- Lee, Junsoo, John A. List, and Mark C. Strazicich. 2006. Non-renewable resource prices: Deterministic or stochastic trends? Journal of Environmental Economics and Management 51: 354–70. [Google Scholar] [CrossRef]

- Lee, Yen-Hsien, Hsu-Ning Hu, and Jer-Shiou Chiou. 2010. Jump dynamics with structural breaks for crude oil prices. Energy Economics 32: 343–50. [Google Scholar] [CrossRef]

- Lim, Kian-Ping, Robert D. Brooks, and Jae H. Kim. 2008. Financial crisis and stock market efficiency: Empirical evidence from Asian countries. International Review of Financial Analysis 17: 571–91. [Google Scholar] [CrossRef]

- Liu, Ming-Lei, Qiang Ji, and Ying Fan. 2013. How does oil market uncertainty interact with other markets? An empirical analysis of implied volatility index. Energy 55: 860–68. [Google Scholar] [CrossRef]

- Ma, Feng, Jing Liu, Dengshi Huang, and Wang Chen. 2017. Forecasting the oil futures price volatility: A new approach. Economic Modelling 64: 560–66. [Google Scholar] [CrossRef]

- Malkiel, Burton G., and Eugene F. Fama. 1970. Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance 25: 383–417. [Google Scholar] [CrossRef]

- Mamatzakis, Emmanuel, and Panos Remoundos. 2011. Testing for adjustment costs and regime shifts in Brent crude futures market. Economic Modelling 28: 1000–8. [Google Scholar] [CrossRef]

- Mehrara, Mohsen, and Monire Hamldar. 2014. The Relationship between Spot and Futures Prices in Brent Crude Oil Market. International Letters of Social and Humanistic Sciences 28: 15–19. [Google Scholar] [CrossRef]

- Mensi, Walid, Shawkat Hammoudeh, and Seong-Min Yoon. 2014. How do OPEC news and structural breaks impact returns and volatility in crude oil markets? Further evidence from a long memory process. Energy Economics 42: 343–54. [Google Scholar] [CrossRef]

- Morales, Lucía, and Bernadette Andreosso-O’Callaghan. 2014. Volatility analysis on precious metals returns and oil returns: An ICSS approach. Journal of Economics and Finance 38: 492–517. [Google Scholar] [CrossRef]

- Morales, Lucia, and Bernadette Andreosso-O’Callaghan. 2017. Volatility in Agricultural Commodity and Oil Markets during Times of Crises. Economics, Management and Financial Markets 12: 59–82. [Google Scholar]

- Morales, Lucía, and Esmeralda Gassie-Falzone. 2014. Structural breaks and financial volatility: Lessons from the BRIC countries. Economics, Management and Financial Markets 9: 67–91. [Google Scholar]

- Mork, Knut Anton, Øystein Olsen, and Hans Terje Mysen. 1994. Macroeconomic responses to oil price increases and decreases in seven OECD countries. The Energy Journal 15: 19–35. [Google Scholar]

- Narayan, Paresh Kumar, and Seema Narayan. 2007. Modelling oil price volatility. Energy Policy 35: 6549–53. [Google Scholar] [CrossRef]

- Nguyen, Duc Khuong, and Thomas Walther. 2018. Modeling and Forecasting Commodity Market Volatility with Long-Term Economic and Financial Variables. Munich: University Library of Munich. [Google Scholar]

- Nomikos, Nikos K., and Panos K. Pouliasis. 2011. Forecasting petroleum futures markets volatility: The role of regimes and market conditions. Energy Economics 33: 321–37. [Google Scholar] [CrossRef]

- Oberndorfer, Ulrich. 2009. Energy prices, volatility, and the stock market: Evidence from the Eurozone. Energy Policy 37: 5787–95. [Google Scholar] [CrossRef]

- Oil Price. 2018. Energy, Oil Prices. Available online: https: //oilprice.com/Energy/Oil-Prices.html (accessed on 15 May 2018).

- Ozdemir, Zeynel Abidin, Korhan Gokmenoglu, and Cagdas Ekinci. 2013. Persistence in crude oil spot and futures prices. Energy 59: 29–37. [Google Scholar] [CrossRef]

- Öztek, Mehmet Fatih, and Nadir Öcal. 2017. Financial crises and the nature of correlation between commodity and stock markets. International Review of Economics & Finance 48: 56–68. [Google Scholar]

- Palley, Thomas I. 2013. Financialization: What it is and Why it Matters. In Financialization. London: Palgrave Macmillan, pp. 17–40. [Google Scholar]

- Park, Jungwook, and Ronald A. Ratti. 2008. Oil price shocks and stock markets in the US and 13 European countries. Energy Economics 30: 2587–608. [Google Scholar] [CrossRef]

- Perron, Pierre. 1989. The great crash, the oil price shock, and the unit root hypothesis. Econometrica: Journal of the Econometric Society 57: 1361–401. [Google Scholar] [CrossRef]

- Phan, Dinh Hoang Bach, Susan Sunila Sharma, and Paresh Kumar Narayan. 2015. Oil price and stock returns of consumers and producers of crude oil. Journal of International Financial Markets, Institutions and Money 34: 245–62. [Google Scholar] [CrossRef]

- Pindyck, Robert S. 2001. The dynamics of commodity spot and futures markets: A primer. The Energy Journal 22: 1–29. [Google Scholar] [CrossRef]

- Polanco-Martínez, Josué M., and Luis M. Abadie. 2016. Analyzing Crude Oil Spot Price Dynamics versus Long Term Future Prices: A Wavelet Analysis Approach. Energies 9: 1089. [Google Scholar] [CrossRef]

- Priog, R. 2005. World Oil Demand and Its Effect on Oil Prices. Washington, DC: Library of Congress Washington DC Congressional Research Service. [Google Scholar]

- Reboredo, Juan C. 2011. How do crude oil prices co-move? A copula approach. Energy Economics 33: 948–55. [Google Scholar] [CrossRef]

- Robe, Michel A., and Jonathan Wallen. 2016. Fundamentals, Derivatives Market Information and Oil Price Volatility. The Journal of Futures Markets 36: 317–44. [Google Scholar] [CrossRef]

- Sadorsky, Perry. 1999. Oil price shocks and stock market activity. Energy Economics 21: 449–69. [Google Scholar] [CrossRef]

- Sadorsky, Perry. 2000. The empirical relationship between energy futures prices and exchange rates. Energy Economics 22: 253–66. [Google Scholar] [CrossRef]

- Sadorsky, Perry. 2006. Modelling and forecasting petroleum futures volatility. Energy Economics 28: 467–88. [Google Scholar] [CrossRef]

- Sadorsky, Perry. 2012. Correlations and volatility spillovers between oil prices and the stock prices of clean energy and technology companies. Energy Economics 34: 248–55. [Google Scholar] [CrossRef]

- Salisu, Afees A., and Ismail O. Fasanya. 2013. Modelling oil price volatility with structural breaks. Energy Policy 52: 554–62. [Google Scholar] [CrossRef]

- Sanders, Dwight R., and Scott H. Irwin. 2017. Bubbles, froth and facts: Another look at the Masters Hypothesis in commodity futures markets. Journal of Agricultural Economics 68: 345–65. [Google Scholar] [CrossRef]

- Sanusi, Muhammad Surajo, and Farooq Ahmad. 2016. Modelling oil and gas stock returns using multi factor asset pricing model including oil price exposure. Finance Research Letters 18: 89–99. [Google Scholar] [CrossRef]

- Schwarz, Thomas V., and Andrew C. Szakmary. 1994. Price discovery in petroleum markets: Arbitrage, cointegration, and the time interval of analysis. Journal of Futures Markets 14: 147–67. [Google Scholar] [CrossRef]

- Serletis, Apostolos, and Ioannis Andreadis. 2004. Random fractal structures in North American energy markets. Energy Economics 26: 389–99. [Google Scholar] [CrossRef]

- Silvapulle, Param, and Imad A. Moosa. 1999. The relationship between spot and futures prices: Evidence from the crude oil market. Journal of Futures Markets 19: 175–93. [Google Scholar] [CrossRef]

- Singleton, Kenneth J. 2013. Investors flow and the 2008 boom/bust in the oil prices. Management Science 60: 300–18. [Google Scholar] [CrossRef]

- Tabak, Benjamin M., and Daniel O. Cajueiro. 2007. Are the crude oil markets becoming weakly efficient over time? A test for time-varying long-range dependence in prices and volatility. Energy Econ. 29: 28–36. [Google Scholar] [CrossRef]

- Tang, Ke, and Wei Xiong. 2012. Index investment and financialization of commodities Princeton University. Financial Analysts Journal 68: 54–74. [Google Scholar] [CrossRef]

- Tonn, Victor Lux, Hsi Li, and Joseph McCarthy. 2010. Wavelet domain correlation between the futures prices of natural gas and oil. The Quarterly Review of Economics and Finance 50: 408–14. [Google Scholar] [CrossRef]

- Wang, Yu Shan. 2013. Oil prices effect on the personal consumption expenditures. Energy Economics 36: 198–204. [Google Scholar] [CrossRef]

- Wang, Yudong, and Chongfeng Wu. 2012. Forecasting energy market volatility using GARCH models: Can multivariate models beat univariate models? Energy Economics 34: 2167–81. [Google Scholar] [CrossRef]

- Wang, Yudong, and Chongfeng Wu. 2013. Are crude oil spot and futures prices cointegrated? Not always! Economic Modelling 33: 641–50. [Google Scholar] [CrossRef]

- Wang, Yudong, Chongfeng Wu, and Li Yang. 2016. Forecasting crude oil market volatility: A Markov switching multifractal volatility approach. International Journal of Forecasting 32: 1–9. [Google Scholar] [CrossRef]

- Zhang, Bing, and Xiao-Ming Li. 2016. Recent hikes in oil-equity market correlations: Transitory or permanent? Energy Economics 53: 305–15. [Google Scholar] [CrossRef]

- Zhang, Yue-Jun, and Zi-Yi Wang. 2013. Investigating the price discovery and risk transfer functions in the crude oil and gasoline futures markets: Some empirical evidence. Applied Energy 104: 220–28. [Google Scholar] [CrossRef]

- Zhang, Jin-Liang, Yue-Jun Zhang, and Lu Zhang. 2015. A novel hybrid method for crude oil price forecasting. Energy Economics 49: 649–59. [Google Scholar] [CrossRef]

{kind=link}

| Theme | Article | Issue Covered |

|---|---|---|

| Relationship and dynamics | Bekiros and Diks (2008) | Long and short term relationship between spot and futures oil prices of West Texas Intermediate (WTI) |

| Huang et al. (2009) | Dynamics of nonlinear relationship using a multivariate threshold regression approach | |

| Tonn et al. (2010) | Wavelet domain correlation between oil and gas futures | |

| Wang and Wu (2013) | Long term relationship between WTI spot and futures prices | |

| Mehrara and Hamldar (2014) | Long and short term relationship between Brent spot and futures prices | |

| Ding et al. (2014) | Short term relationship of WTI | |

| Alzahrani et al. (2014) | Linear and nonlinear Granger causality between oil spot and futures prices | |

| Chang and Lee (2015) | Oil causal relationship using wavelet coherency approach | |

| Polanco-Martínez and Abadie (2016) | Oil spot price dynamics and long term futures prices using wavelet approach | |

| Structural breaks | Lee et al. (2010) | Evidence of structural breaks in crude oil markets |

| Salisu and Fasanya (2013) | Structural breaks in oil time series | |

| Charles and Darné (2014) | Numerous structural breaks affecting oil series | |

| Mensi et al. (2014) | Importance of structural breaks in oil markets | |

| Charfeddine (2016) | Breaks or long range dependence in oil futures | |

| Volatility analysis | Fong and See (2002) | Markov switching model of conditional volatility |

| Sadorsky (2006) | Oil price fluctuations | |

| Arouri et al. (2012) | Long memory and structural breaks in oil volatility | |

| Wang and Wu (2012) | GARCH modelling in energy markets volatility | |

| Salisu and Fasanya (2013) | Volatility analysis with structural breaks | |

| Charles and Darné (2014) | Volatility persistence in crude oil markets | |

| Wang et al. (2016) | Forecasting oil market volatility | |

| Efficiency | Serletis and Andreadis (2004) | WTI price efficiency |

| Lim et al. (2008) | Impact of OPEC on oil efficiency | |

| Charles and Darné (2009) | Crude oil markets efficiency | |

| Khediri and Charfeddine (2015) | WTI market efficiency | |

| Gu and Zhang (2016) | WTI efficiency |

| Researchers | Period | Data | Methodology | Empirical Findings |

|---|---|---|---|---|

| COINTEGRATION AND CAUSALITY | ||||

| Bekiros and Diks (2008) | October 1991 to October 1999 and November 1999 to October 2007 | WTI spot and futures prices, daily data | Granger causality, VECM, GARCH-BEKK | Neither market leads or lags the other consistently, and the pattern changes over time |

| Wang and Wu (2013) | January 1986 to February 2011 | WTI spot and futures prices, weekly data | TVECM | Different relationship in the long run and short run, futures prices dominate in the short run |

| Mehrara and Hamldar (2014) | August 1990 to November 2014 | Brent spot and futures prices, daily data | Johansen cointegration, Granger causality, VECM | Bidirectional long and short run relationship |

| Ding et al. (2014) | 1996 to 2003 and 2004 to 2012 | WTI spot prices and net long financial positions, weekly data | Granger non-causality test in quantiles | Some causal relationship between crude oil and financial positions |

| STRUCTURAL BREAKS AND MOVING WINDOWS | ||||

| Lee et al. (2010) | January 1990 to December 2007 | WTI spot and futures prices, daily data | Bai–Perron test | Evidence of four structural breaks |

| Salisu and Fasanya (2013) | January 2000 to March 2012 | WTI and Brent spot prices, daily data | NP procedure | Two structural breaks, one in 1990 and second in 2008 |

| Charles and Darné (2014) | January 1985 to June 2011 | Brent, WTI and OPEC | Outliers clustering | Numerous structural breaks |

| Mensi et al. (2014) | May 1987 to December 2012 | Brent and WTI, daily data | Bai–Perron test | Evidence of five break points in WTI market and six break points in Brent market |

| Khediri and Charfeddine (2015) | January 1986 to January 2014 | Crude oil, gasoline and heating oil spot and futures prices, daily data | Moving Window | Two year moving windows shows mean reversion towards markets efficiency |

| VOLATILITY | ||||

| Sadorsky (1999) | January 1947 to April 1996 | Oil price index, monthly data | GARCH (1,1) | Evidence of asymmetric effects of oil price volatility shocks |

| Wang and Wu (2012) | July 1992 to August 2011 | WTI spot prices, weekly data | Uni and Multi-GARCH | Uni-variate models show greater accuracy |

| Salisu and Fasanya (2013) | January 2000 to March 2012 | WTI and Brent spot prices, daily data | GARCH models | Evidence of persistence and leverage effects |

| Charles and Darné (2014) | January 1985 to June 2011 | Brent, WTI and OPEC | GARCH models | Various GARCH-type models showed different parameter estimates |

| Wang et al. (2016) | January 1993 to September 2013 | WTI and Brent spot prices, daily data | GARCH models and Markov switching model | MSM model captures volatility forecast better than GARCH models |

| EFFICIENCY | ||||

| Serletis and Andreadis (2004) | January 1990 to February 2001 | WTI and Henry Hub natural gas, daily data | Hurst test | Evidence of multifractal turbulent structure |

| Charles and Darné (2009) | 1982 to 2008 | Brent and WTI spot prices, daily data | VR tests and wild-bootstrapping | Brent is efficient, WTI is not efficient between 1994 to 2008 period |

| Khediri and Charfeddine (2015) | 1986 to 2014 | WTI, Gasoline and Heating oil spot and futures prices, daily data | VR tests, Run test, R/S statistic and DFA | Crude oil and gasoline prices show highest degree of efficiency |

| Gu and Zhang (2016) | 1986 to 2012 | WTI spot prices, daily data | Multifractality, Granger non-causality | Evidence of nonlinear relationship between crude oil market inefficiency and multifractality |

| Existing Research | Direction of Leading Price |

|---|---|

| Schwarz and Szakmary (1994) | Spot |

| Gülen (1998) | Spot |

| Pindyck (2001) | Spot |

| Alquist and Kilian (2010) | Spot |

| Wang and Wu (2013) | Spot |

| Zhang and Wang (2013) | Spot |

| Kim (2015) | Spot |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zavadska, M.; Morales, L.; Coughlan, J. The Lead–Lag Relationship between Oil Futures and Spot Prices—A Literature Review. Int. J. Financial Stud. 2018, 6, 89. https://doi.org/10.3390/ijfs6040089

Zavadska M, Morales L, Coughlan J. The Lead–Lag Relationship between Oil Futures and Spot Prices—A Literature Review. International Journal of Financial Studies. 2018; 6(4):89. https://doi.org/10.3390/ijfs6040089

Chicago/Turabian StyleZavadska, Miroslava, Lucía Morales, and Joseph Coughlan. 2018. "The Lead–Lag Relationship between Oil Futures and Spot Prices—A Literature Review" International Journal of Financial Studies 6, no. 4: 89. https://doi.org/10.3390/ijfs6040089

APA StyleZavadska, M., Morales, L., & Coughlan, J. (2018). The Lead–Lag Relationship between Oil Futures and Spot Prices—A Literature Review. International Journal of Financial Studies, 6(4), 89. https://doi.org/10.3390/ijfs6040089