Cross Hedging Stock Sector Risk with Index Futures by Considering the Global Equity Systematic Risk

Abstract

:1. Introduction

2. Regime Switching Volatility Spillover GARCH (RSVSG) Model

3. Measurements of Hedging Performance, Minimum Variance Hedge Ratio (MVHR), and Volatility Spillover Ratio

4. Data Description and Empirical Results

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Adams, Zeno, and Mathias Gerner. 2012. Cross hedging jet-fuel price exposure. Energy Economics 34: 1301–9. [Google Scholar] [CrossRef]

- Alizadeh, Amir H., Nikos K. Nomikos, and Panos K. Pouliasis. 2008. A Markov regime switching approach for hedging energy commodities. Journal of Banking and Finance 32: 1970–83. [Google Scholar] [CrossRef]

- Arouri, Mohamed El Hedi, Jamel Jouini, and Duc Khuong Nguyen. 2011. Volatility Spillovers between Oil Prices and Stock Sector Returns: Implications for Portfolio Management. Journal of International Money and Finance 30: 1387–405. [Google Scholar] [CrossRef]

- Baillie, Richard T., and Robert J. Myers. 1991. Bivariate GARCH estimation of the optimal commodity futures hedge. Journal of Applied Econometrics 6: 109–24. [Google Scholar] [CrossRef]

- Brooks, Chris, Olan T. Henry, and Gita Persand. 2002. The Effect of Asymmetries on Optimal Hedge Ratios. Journal of Business 75: 333–52. [Google Scholar] [CrossRef]

- Byström, Hans NE. 2003. The Hedging Performance of Electricity Futures on the Nordic Power Exchange. Applied Economics 35: 1–11. [Google Scholar] [CrossRef]

- Chang, Chia-Lin, Michael McAleer, and Roengchai Tansuchat. 2011. Crude oil hedging strategies using dynamic multivariate GARCH. Energy Economics 33: 912–23. [Google Scholar] [CrossRef]

- Choudhry, Taufiq. 2009. Short-run deviations and time-varying hedge ratios: evidence from agricultural futures markets. International Review of Financial Analysis 18: 58–65. [Google Scholar] [CrossRef]

- Cifarelli, Giulio, and Giovanna Paladino. 2015. A Dynamic Model of Hedging and Speculation in the Commodity Futures Markets. Journal of Financial Markets 25: 1–15. [Google Scholar] [CrossRef]

- Dark, Jonathan. 2015. Futures hedging with Markov switching vector error correction FIEGARCH and FIAPARCH. Journal of Banking and Finance 61: 269–85. [Google Scholar] [CrossRef]

- Engle, Robert F., and Kenneth F. Kroner. 1995. Multivariate simultaneous generalized ARCH. Econometric Theory 11: 122–50. [Google Scholar] [CrossRef]

- Fernandez, Viviana. 2008. Multi-period hedge ratios for a multi-asset portfolio when accounting for returns co-movement. The Journal of Futures Markets 28: 182–207. [Google Scholar] [CrossRef]

- Gagnon, Louis, and Greg Lypny. 1998. Hedging short-term interest risk under time-varying distribution. The Journal of Futures Markets 15: 767–83. [Google Scholar] [CrossRef]

- Gray, Stephen F. 1996. Modeling the conditional distribution of interest rates as a regime-switching process. Journal of Financial Economics 42: 27–62. [Google Scholar] [CrossRef]

- Kroner, Kenneth F., and Jahangir Sultan. 1993. Time-varying distribution and dynamic hedging with foreign currency futures. Journal of Financial and Quantitative Analysis 28: 535–51. [Google Scholar] [CrossRef]

- Lafuente, Juan A., and Alfonso Novales. 2003. Optimal hedging under departures from the cost-of-carry valuation: Evidence from the Spanish stock index futures market. Journal of Banking and Finance 27: 1053–78. [Google Scholar] [CrossRef]

- Lai, Yu-Sheng, and Donald Lien. 2017. A Bivariate High-Frequency-Based Volatility Model for Optimal Futures Hedging. The Journal of Futures Markets 37: 913–29. [Google Scholar] [CrossRef]

- Lai, Yu-Sheng, Her-Jiun Sheu, and Hsiang-Tai Lee. 2017. A Multivariate Markov Regime-Switching High-Frequency-Based Volatility Model for Optimal Futures Hedging. The Journal of Futures Markets 37: 1124–40. [Google Scholar] [CrossRef]

- Lee, Hsiang-Tai. 2009a. Optimal futures hedging under jump switching dynamics. Journal of Empirical Finance 16: 446–56. [Google Scholar] [CrossRef]

- Lee, Hsiang-Tai. 2009b. A copula-based regime-switching GARCH model for optimal futures hedging. The Journal of Futures Markets 29: 946–72. [Google Scholar] [CrossRef]

- Lee, Hsiang-Tai. 2010. Regime switching correlation hedging. Journal of Banking and Finance 34: 2728–41. [Google Scholar] [CrossRef]

- Lee, Hsiang-Tai, and Wei-Lun Tsang. 2011. Cross hedging single stock with American Depositary Receipt and stock index futures. Finance Research Letters 8: 146–57. [Google Scholar] [CrossRef]

- Lee, Hsiang-Tai, and Jonathan K. Yoder. 2007a. A bivariate Markov regime switching GARCH approach to estimate the time varying minimum variance hedge ratio. Applied Economics 39: 1253–65. [Google Scholar] [CrossRef]

- Lee, Hsiang-Tai, and Jonathan Yoder. 2007b. Optimal hedging with a regime-switching time-varying correlation GARCH Model. The Journal of Futures Markets 27: 495–16. [Google Scholar] [CrossRef]

- Pan, Zhiyuan, Yudong Wang, and Li Yang. 2014. Hedging Crude Oil Using Refined Product: A Regime Switching Asymmetric DCC Approach. Energy Economics 46: 472–84. [Google Scholar] [CrossRef]

- Park, Jin Suk, and Yukun Shi. 2017. Hedging and speculative pressures and the transition of the spot-futures relationship in energy and metal markets. International Review of Financial Analysis 54: 176–91. [Google Scholar] [CrossRef]

- Park, Tae H., and Lorne N. Switzer. 1995. Bivariate GARCH Estimation of the Optimal Hedge Ratios for Stock Index Futures: A Note. The Journal of Futures Markets 15: 61–67. [Google Scholar] [CrossRef]

- Ratner, Mitchell, and Chih-Chieh Jason Chiu. 2013. Hedging stock sector risk with credit default swaps. International Review of Financial Analysis 30: 18–25. [Google Scholar] [CrossRef]

- Sarno, Lucio, and Giorgio Valente. 2000. The cost of carry model and regime shifts in stock index futures markets: An empirical investigation. The Journal of Futures Markets 20: 603–24. [Google Scholar] [CrossRef]

- Sarno, Lucio, and Giorgio Valente. 2005a. Empirical exchange rate models and currency risk: Some evidence from density forecasts. Journal of International Money and Finance 24: 363–85. [Google Scholar] [CrossRef]

- Sarno, Lucio, and Giorgio Valente. 2005b. Modelling and forecasting stock returns: Exploiting the futures market, regime shifts, and international spillovers. Journal of Applied Econometrics 20: 345–76. [Google Scholar] [CrossRef]

- Sheu, Her-Jiun, and Hsiang-Tai Lee. 2014. Optimal futures hedging under multi-chain Markov regime switching. The Journal of Futures Markets 34: 173–202. [Google Scholar] [CrossRef]

- Sukcharoen, Kunlapath, and David J. Leatham. 2017. Hedging downside risk of oil refineries: A vine copula approach. Energy Economics 66: 493–507. [Google Scholar] [CrossRef]

- Wu, Feng, Zhengfei Guan, and Robert J. Myers. 2011. Volatility spillover effects and cross hedging in corn and crude oil futures. The Journal of Futures Markets 31: 1052–75. [Google Scholar] [CrossRef]

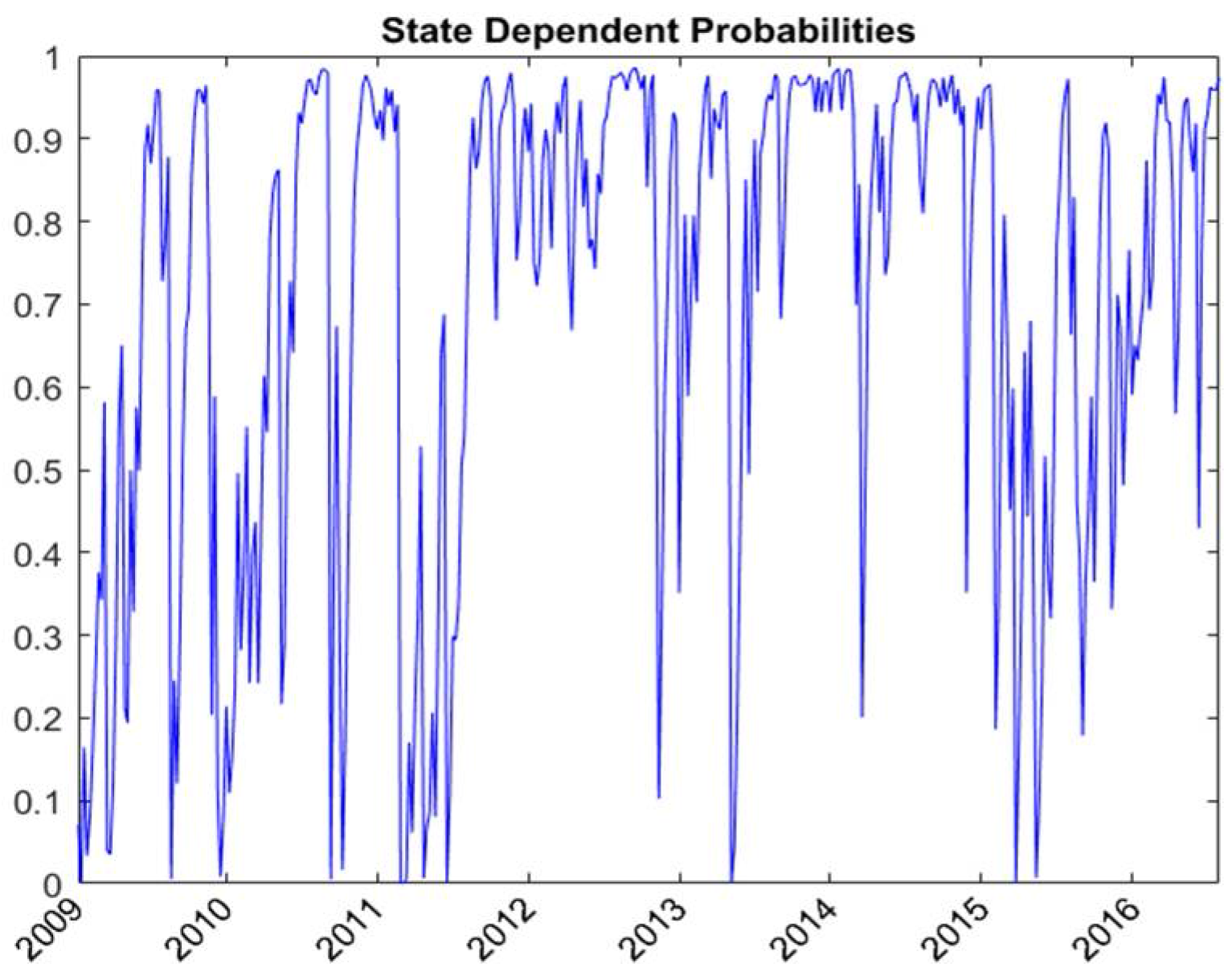

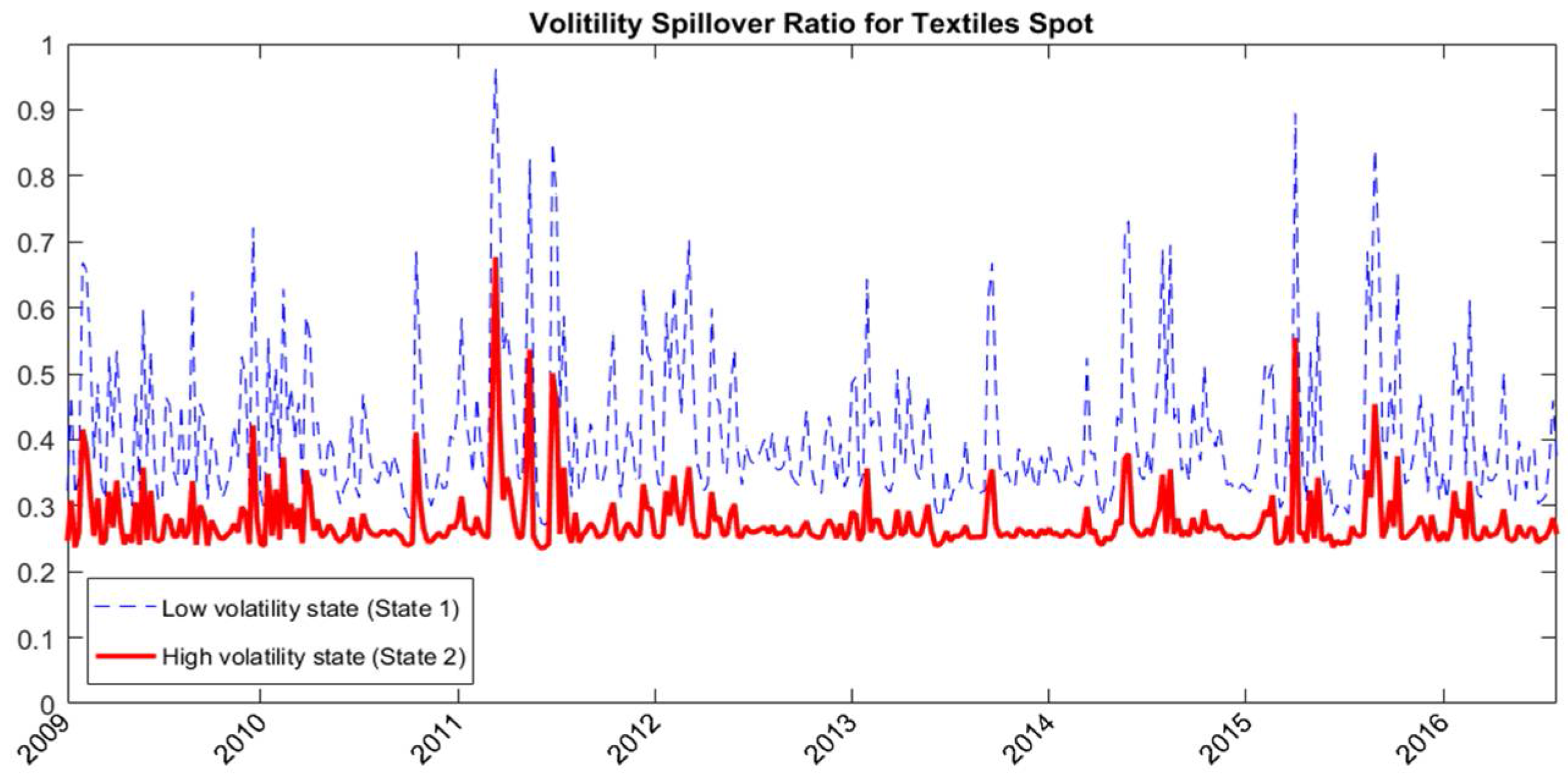

| 1 | Because the state probability is time varying, and are also time varying after taking the weighted average using state probabilities. |

| 2 | Because all hedged portfolio returns are pretty small, the value of the expected utility is dominated by the second moment of the hedged portfolio return. Although it is not reported here, we find that hedging results are robust to the choice of the coefficient of absolute risk aversion for a wide range of (). A hedging strategy with lower volatility has higher expected utility regardless the choice of the coefficient of absolute risk aversion. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Textiles | Communication and Internet | Transportation | Retailing | |

|---|---|---|---|---|

| Mean | 0.086 | 0.028 | −0.111 | 0.147 |

| Maximum | 9.232 | 6.265 | 7.658 | 9.363 |

| Minimum | −11.979 | −8.869 | −11.430 | −11.416 |

| SD | 2.953 | 2.171 | 2.938 | 2.727 |

| Skewness | −0.478 | −0.414 | −0.437 | −0.317 |

| Kurtosis | 4.548 | 4.679 | 4.293 | 4.333 |

| Jarque–Bera | 54.808 *** | 57.960 *** | 40.306 *** | 36.042 *** |

| Automobile | Plastics and Chemicals | TAIFEX Futures | Taiwan 50 Futures | |

| Mean | 0.246 | 0.114 | 0.085 | 0.106 |

| Maximum | 12.810 | 8.512 | 6.392 | 6.540 |

| Minimum | −14.360 | −11.618 | −10.015 | −10.328 |

| SD | 3.867 | 2.786 | 2.560 | 2.588 |

| Skewness | −0.279 | −0.478 | −0.546 | −0.330 |

| Kurtosis | 3.940 | 4.605 | 3.897 | 3.493 |

| Jarque–Bera | 19.770 *** | 57.683 *** | 33.023 *** | 11.215 *** |

| Taiwan NFNE Futures | MSCI World Index Futures | |||

| Mean | 0.090 | 0.192 | ||

| Maximum | 7.668 | 7.941 | ||

| Minimum | −9.659 | −10.044 | ||

| SD | 2.579 | 2.173 | ||

| Skewness | −0.490 | −0.577 | ||

| Kurtosis | 4.113 | 5.134 | ||

| Jarque–Bera | 36.371 *** | 97.375 *** |

| Textiles | Retailing | Transportation | Textiles | Retailing | Transportation | ||

|---|---|---|---|---|---|---|---|

| Transition Probability | Spillover Equation | ||||||

| 2.829 | 1.525 | 0.653 | 1.137 | 0.000 | 0.000 | ||

| (0.399) *** | (0.576) *** | (0.430) * | (0.463) *** | (0.041) | (0.083) | ||

| 1.954 | −0.352 | 1.332 | 0.240 | 0.270 | 0.166 | ||

| (0.566) *** | (0.453) | (0.468) *** | (0.098) *** | (0.126) ** | (0.082) *** | ||

| Covariance Equation | 0.242 | 0.544 | 0.379 | ||||

| 3 | −1.270 | 0.152 | 1.165 | (0.154) * | (0.085) *** | (0.094) *** | |

| (0.396) *** | (0.531) | (0.267) *** | 0.768 | 0.600 | 0.495 | ||

| 3.604 | 1.480 | 2.277 | (0.086) *** | (0.080) *** | (0.107) *** | ||

| (0.414) *** | (0.765) ** | (0.859) *** | 0.763 | 0.719 | 0.391 | ||

| −0.418 | 0.377 | 1.203 | (0.071) *** | (0.074) *** | (0.112) *** | ||

| (0.293) * | (0.282) * | (0.210) *** | 7.291 | 3.046 | 1.314 | ||

| 2.313 | 0.657 | 2.317 | (2.446) *** | (5.129) | (0.649) *** | ||

| (0.302) *** | (0.585) | (0.199) *** | 0.220 | 0.000 | 0.118 | ||

| 0.014 | 0.001 | −0.002 | (0.153) * | (0.039) | (0.086) * | ||

| (0.059) | (0.040) | (0.076) | 0.049 | 1.000 | 0.874 | ||

| 1.158 | 0.002 | 0.245 | (0.284) | (1.212) | (0.185) *** | ||

| (0.510) *** | (0.022) | (0.974) | 0.544 | 0.775 | 0.701 | ||

| 0.000 | 0.021 | 0.038 | (0.131) *** | (0.168) *** | (0.090) *** | ||

| (0.035) ** | (0.056) | (0.065) | 0.739 | 0.844 | 0.841 | ||

| −0.029 | −0.050 | 0.000 | (0.092) *** | (0.138) *** | (0.073) *** | ||

| (0.163) | (0.147) | (0.04) | |||||

| 0.000 | 0.080 | −0.076 | |||||

| (0.049) | (0.071) | (0.087) | |||||

| −0.145 | 0.066 | 0.000 | |||||

| (0.128) | (0.153) | (0.018) | |||||

| 0.591 | 0.781 | 0.236 | |||||

| (0.194) * | (0.075) *** | (0.210) | |||||

| 0.428 | 1.365 | −0.835 | |||||

| (0.269) *** | (0.155) *** | (0.332) *** | |||||

| 0.863 | 0.845 | −0.169 | |||||

| (0.050) * | (0.057) *** | (0.315) | |||||

| −0.156 | 1.286 | 0.091 | |||||

| (0.303) *** | (0.135) *** | (0.571) | |||||

| 2 | −1797.51 | −1781.97 | −1827.45 | ||||

| Communication and Internet | Automobile | Plastics and Chemicals | Communication and Internet | Automobile | Plastics and Chemicals | ||

| Transition Probability | Spillover Equation | ||||||

| 1.624 | 2.208 | 1.463 | 0.000 | 0.000 | 0.000 | ||

| (1.122) * | (0.829) *** | (0.485) *** | (0.050) | (0.080) | (0.076) | ||

| 0.001 | −0.013 | 0.026 | 0.234 | 0.196 | 0.279 | ||

| (0.036) | (0.098) | (0.202) | (0.114) ** | (0.224) | (0.198) * | ||

| Covariance Equation | 0.579 | 0.593 | 0.512 | ||||

| 3 | (0.564) | 0.163 | 0.711 | (0.188) *** | (0.147) *** | (0.102) *** | |

| (0.691) | (0.768) | (0.340) ** | 0.436 | 0.863 | 0.760 | ||

| 2.729 | 2.936 | 2.172 | (0.058) *** | (0.110) *** | (0.078) *** | ||

| (0.520) *** | (1.434) ** | (0.699) *** | 0.781 | 0.688 | 0.725 | ||

| 0.424 | 0.093 | 0.743 | (0.094) *** | (0.067) *** | (0.074) *** | ||

| (0.282) * | (0.514) | (0.475) * | 2.976 | 5.378 | 2.880 | ||

| 1.868 | 0.785 | 1.173 | (9.570) | (18.033) | (8.560) | ||

| (1.070) *** | (0.211) *** | (0.376) *** | 0.000 | 0.128 | 0.000 | ||

| −0.001 | 0.000 | 0.000 | (0.035) | (0.316) | (0.040) | ||

| (0.031) | (0.030) | (0.115) | 1.000 | 0.872 | 1.000 | ||

| 0.516 | 0.000 | 0.228 | (2.055) | (4.023) | (2.150) | ||

| (3.655) | (0.044) | (1.430) | 0.485 | 1.048 | 0.949 | ||

| −0.075 | 0.014 | 0.120 | (0.137) *** | (0.264) *** | (0.147) *** | ||

| (0.121) | (0.033) | (0.081) * | 0.727 | 0.897 | 0.794 | ||

| 0.485 | −0.010 | 0.185 | (0.204) *** | (0.116) *** | (0.122) *** | ||

| (0.273) ** | (0.104) | (0.121) * | |||||

| −0.130 | 0.063 | 0.072 | |||||

| (0.120) | (0.083) | (0.091) | |||||

| 0.153 | −0.129 | 0.098 | |||||

| (0.265) | (0.106) | (0.102) | |||||

| 0.662 | 0.853 | 0.699 | |||||

| (0.126) *** | (0.077) *** | (0.057) *** | |||||

| −0.395 | 1.278 | 0.990 | |||||

| (1.109) | (0.251) *** | (0.329) *** | |||||

| 0.805 | 0.956 | 0.760 | |||||

| (0.124) *** | (0.031) *** | (0.063) *** | |||||

| 0.948 | 1.089 | 1.162 | |||||

| (0.743) | (0.105) *** | (0.088) *** | |||||

| 2 | −1762.47 | −1933.01 | −1615.74 | ||||

| Variance of Hedged Portfolio Return | Percentage Variance Reduction 1 | Improvement of NFNE Futures over Other Futures 2 | Hedged Portfolio Returns | Expected Weekly Utility 3 | Utility Gain of NFNE Futures over Other Futures 4 | |

|---|---|---|---|---|---|---|

| Textiles | ||||||

| Unhedged | 6.745 | 0.086 | ||||

| TAIEX | 2.983 | 55.78% | 0.25% | −0.457 | −12.389 | 0.075 |

| Taiwan 50 | 3.198 | 52.59% | 3.44% | −0.485 | −13.277 | 0.963 |

| NFNE subindex | 2.966 | 56.03% | −0.450 | −12.314 | ||

| Retailing | ||||||

| Unhedged | 4.481 | 0.147 | ||||

| TAIEX | 2.457 | 45.17% | −2.46% | −0.104 | −9.932 | −0.451 |

| Taiwan 50 | 2.394 | 46.56% | −3.85% | −0.137 | −9.714 | −0.669 |

| NFNE subindex | 2.567 | 42.71% | −0.114 | −10.383 | ||

| Transportation | ||||||

| Unhedged | 5.132 | −0.111 | ||||

| TAIEX | 2.028 | 60.49% | 3.93% | −0.477 | −8.588 | 0.815 |

| Taiwan 50 | 2.127 | 58.56% | 5.86% | −0.517 | −9.025 | 1.252 |

| NFNE subindex | 1.826 | 64.42% | −0.468 | −7.773 | ||

| Communication and Internet | ||||||

| Unhedged | 3.166 | 0.028 | ||||

| TAIEX | 1.485 | 53.10% | −3.81% | 0.006 | −5.933 | −0.474 |

| Taiwan 50 | 1.238 | 60.91% | −11.62% | −0.035 | −4.985 | −1.422 |

| NFNE subindex | 1.606 | 49.29% | 0.016 | −6.407 | ||

| Automobile | ||||||

| Unhedged | 6.921 | 0.246 | ||||

| TAIEX | 2.026 | 70.73% | 2.34% | −0.394 | −8.497 | 0.672 |

| Taiwan 50 | 1.950 | 71.82% | 1.25% | −0.439 | −8.241 | 0.416 |

| NFNE subindex | 1.864 | 73.07% | −0.370 | −7.825 | ||

| Plastics and Chemicals | ||||||

| Unhedged | 4.404 | 0.114 | ||||

| TAIEX | 1.096 | 75.12% | 11.85% | 0.124 | −4.258 | 2.095 |

| Taiwan 50 | 1.054 | 76.06% | 10.91% | 0.068 | −4.150 | 1.987 |

| NFNE subindex | 0.574 | 86.97% | 0.133 | −2.163 | ||

| Variance of Hedged Portfolio Return | Percentage Variance Reduction 1 | Improvement of RSVSG over VSG and BEKK 2 | Hedged Portfolio Returns | Expected Weekly Utility 3 | Utility Gain of RSVSG over VSG and BEKK 4 | |

|---|---|---|---|---|---|---|

| Textiles | ||||||

| Unhedged | 6.745 | 0.086 | ||||

| BEKK | 2.966 | 56.03% | 0.53% | −0.450 | −12.314 | 0.135 |

| VSG | 2.946 | 56.32% | 0.23% | −0.448 | −12.233 | 0.053 |

| RSVSG | 2.930 | 56.56% | −0.458 | −12.180 | ||

| Retailing | ||||||

| Unhedged | 4.481 | 0.147 | ||||

| BEKK | 2.567 | 42.71% | 4.36% | −0.114 | −10.383 | 0.791 |

| VSG | 2.405 | 46.32% | 0.74% | −0.102 | −9.722 | 0.131 |

| RSVSG | 2.372 | 47.06% | −0.104 | −9.591 | ||

| Transportation | ||||||

| Unhedged | 5.132 | −0.111 | ||||

| BEKK | 1.826 | 64.42% | −0.43% | −0.468 | −7.773 | −0.094 |

| VSG | 1.800 | 64.93% | −0.95% | −0.466 | −7.664 | −0.203 |

| RSVSG | 1.849 | 63.98% | −0.473 | −7.867 | ||

| Communication and Internet | ||||||

| Unhedged | 3.166 | 0.028 | ||||

| BEKK | 1.606 | 49.29% | 2.05% | 0.016 | −6.407 | 0.244 |

| VSG | 1.554 | 50.93% | 0.40% | −0.005 | −6.220 | 0.057 |

| RSVSG | 1.541 | 51.33% | 0.001 | −6.162 | ||

| Automobile | ||||||

| Unhedged | 6.921 | 0.246 | ||||

| BEKK | 1.864 | 73.07% | 0.10% | −0.370 | −7.825 | 0.023 |

| VSG | 1.977 | 71.43% | 1.74% | −0.386 | −8.294 | 0.492 |

| RSVSG | 1.857 | 73.17% | −0.375 | −7.802 | ||

| Plastics and Chemicals | ||||||

| Unhedged | 4.404 | 0.114 | ||||

| BEKK | 0.574 | 86.97% | −1.64% | 0.133 | −2.163 | −0.300 |

| VSG | 0.710 | 83.88% | 1.44% | 0.106 | −2.733 | 0.270 |

| RSVSG | 0.646 | 85.32% | 0.123 | −2.463 | ||

| Semivariance of Hedged Portfolio Return | Percentage Semivariance Reduction 1 | Improvement of RSVSG over VSG and BEKK 2 | Hedged Portfolio Returns | Expected Weekly Semi-Utility 3 | Semi-Utility Gain of RSVSG over VSG and BEKK 4 | |

|---|---|---|---|---|---|---|

| Textiles | ||||||

| Short hedgers‘ positions (negative semivariance) | ||||||

| Unhedged | 3.896 | 0.086 | ||||

| BEKK | 2.085 | 46.49% | 0.80% | −0.450 | −8.789 | 0.117 |

| VSG | 2.068 | 46.91% | 0.38% | −0.448 | −8.722 | 0.050 |

| RSVSG | 2.054 | 47.29% | −0.458 | −8.672 | ||

| Long hedgers‘ positions (positive semivariance) | ||||||

| Unhedged | 2.779 | 0.086 | ||||

| BEKK | 1.027 | 63.06% | 1.30% | −0.450 | −4.556 | 0.136 |

| VSG | 1.010 | 63.67% | 0.69% | −0.448 | −4.487 | 0.067 |

| RSVSG | 0.991 | 64.36% | −0.458 | −4.420 | ||

| Retailing | ||||||

| Short hedgers‘ positions (negative semivariance) | ||||||

| Unhedged | 2.135 | 0.147 | ||||

| BEKK | 1.323 | 38.05% | 7.26% | −0.114 | −5.404 | 0.630 |

| VSG | 1.181 | 44.69% | 0.62% | −0.102 | −4.826 | 0.052 |

| RSVSG | 1.168 | 45.31% | −0.104 | −4.774 | ||

| Long hedgers‘ positions (positive semivariance) | ||||||

| Unhedged | 2.265 | 0.147 | ||||

| BEKK | 1.208 | 46.66% | 1.71% | −0.114 | −4.947 | 0.165 |

| VSG | 1.174 | 48.18% | 0.20% | −0.102 | −4.798 | 0.016 |

| RSVSG | 1.169 | 48.38% | −0.104 | −4.781 | ||

| Transportation | ||||||

| Short hedgers‘ positions (negative semivariance) | ||||||

| Unhedged | 3.048 | −0.111 | ||||

| BEKK | 1.318 | 56.78% | 0.16% | −0.468 | −5.738 | 0.015 |

| VSG | 1.291 | 57.65% | −0.71% | −0.466 | −5.629 | −0.094 |

| RSVSG | 1.313 | 56.94% | −0.473 | −5.723 | ||

| Long hedgers‘ positions (positive semivariance) | ||||||

| Unhedged | 2.066 | −0.111 | ||||

| BEKK | 0.692 | 66.49% | 0.84% | −0.468 | −3.237 | 0.064 |

| VSG | 0.689 | 66.65% | 0.69% | −0.466 | −3.222 | 0.049 |

| RSVSG | 0.675 | 67.33% | −0.473 | −3.173 | ||

| Communication and Internet | ||||||

| Short hedgers‘ positions (negative semivariance) | ||||||

| Unhedged | 1.516 | 0.028 | ||||

| BEKK | 0.796 | 47.46% | 0.04% | 0.016 | −3.170 | −0.012 |

| VSG | 0.818 | 46.01% | 1.49% | −0.005 | −3.279 | 0.097 |

| RSVSG | 0.796 | 47.50% | 0.001 | −3.182 | ||

| Long hedgers‘ positions (positive semivariance) | ||||||

| Unhedged | 1.602 | 0.028 | ||||

| BEKK | 0.778 | 51.40% | 3.55% | 0.016 | −3.098 | 0.213 |

| VSG | 0.713 | 55.50% | −0.55% | −0.005 | −2.857 | −0.029 |

| RSVSG | 0.722 | 54.95% | 0.001 | −2.885 | ||

| Automobile | ||||||

| Short hedgers‘ positions (negative semivariance) | ||||||

| Unhedged | 4.012 | 0.246 | ||||

| BEKK | 1.323 | 67.01% | 2.33% | −0.370 | −5.664 | 0.370 |

| VSG | 1.412 | 64.81% | 4.54% | −0.386 | −6.033 | 0.739 |

| RSVSG | 1.230 | 69.34% | −0.375 | −5.294 | ||

| Long hedgers‘ positions (positive semivariance) | ||||||

| Unhedged | 2.794 | 0.246 | ||||

| BEKK | 0.642 | 77.04% | 0.68% | −0.370 | −2.936 | 0.072 |

| VSG | 0.694 | 75.16% | 2.57% | −0.386 | −3.162 | 0.298 |

| RSVSG | 0.622 | 77.72% | −0.375 | −2.865 | ||

| Plastics and Chemicals | ||||||

| Short hedgers‘ positions (negative semivariance) | ||||||

| Unhedged | 2.044 | 0.114 | ||||

| BEKK | 0.219 | 89.27% | 0.91% | 0.133 | −0.744 | 0.064 |

| VSG | 0.241 | 88.19% | 1.99% | 0.106 | −0.860 | 0.179 |

| RSVSG | 0.201 | 90.18% | 0.123 | −0.680 | ||

| Long hedgers‘ positions (positive semivariance) | ||||||

| Unhedged | 2.385 | 0.114 | ||||

| BEKK | 0.361 | 84.85% | −0.93% | 0.133 | −1.312 | −0.099 |

| VSG | 0.401 | 83.17% | 0.75% | 0.106 | −1.500 | 0.088 |

| RSVSG | 0.383 | 83.92% | 0.123 | −1.411 | ||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hsu, W.-C.; Lee, H.-T. Cross Hedging Stock Sector Risk with Index Futures by Considering the Global Equity Systematic Risk. Int. J. Financial Stud. 2018, 6, 44. https://doi.org/10.3390/ijfs6020044

Hsu W-C, Lee H-T. Cross Hedging Stock Sector Risk with Index Futures by Considering the Global Equity Systematic Risk. International Journal of Financial Studies. 2018; 6(2):44. https://doi.org/10.3390/ijfs6020044

Chicago/Turabian StyleHsu, Wen-Chung, and Hsiang-Tai Lee. 2018. "Cross Hedging Stock Sector Risk with Index Futures by Considering the Global Equity Systematic Risk" International Journal of Financial Studies 6, no. 2: 44. https://doi.org/10.3390/ijfs6020044

APA StyleHsu, W.-C., & Lee, H.-T. (2018). Cross Hedging Stock Sector Risk with Index Futures by Considering the Global Equity Systematic Risk. International Journal of Financial Studies, 6(2), 44. https://doi.org/10.3390/ijfs6020044