The Impact of Intangible Capital on Firm Profitability in the Technology and Healthcare Sectors

Abstract

1. Introduction

2. Literature Review

3. Methods and Sample

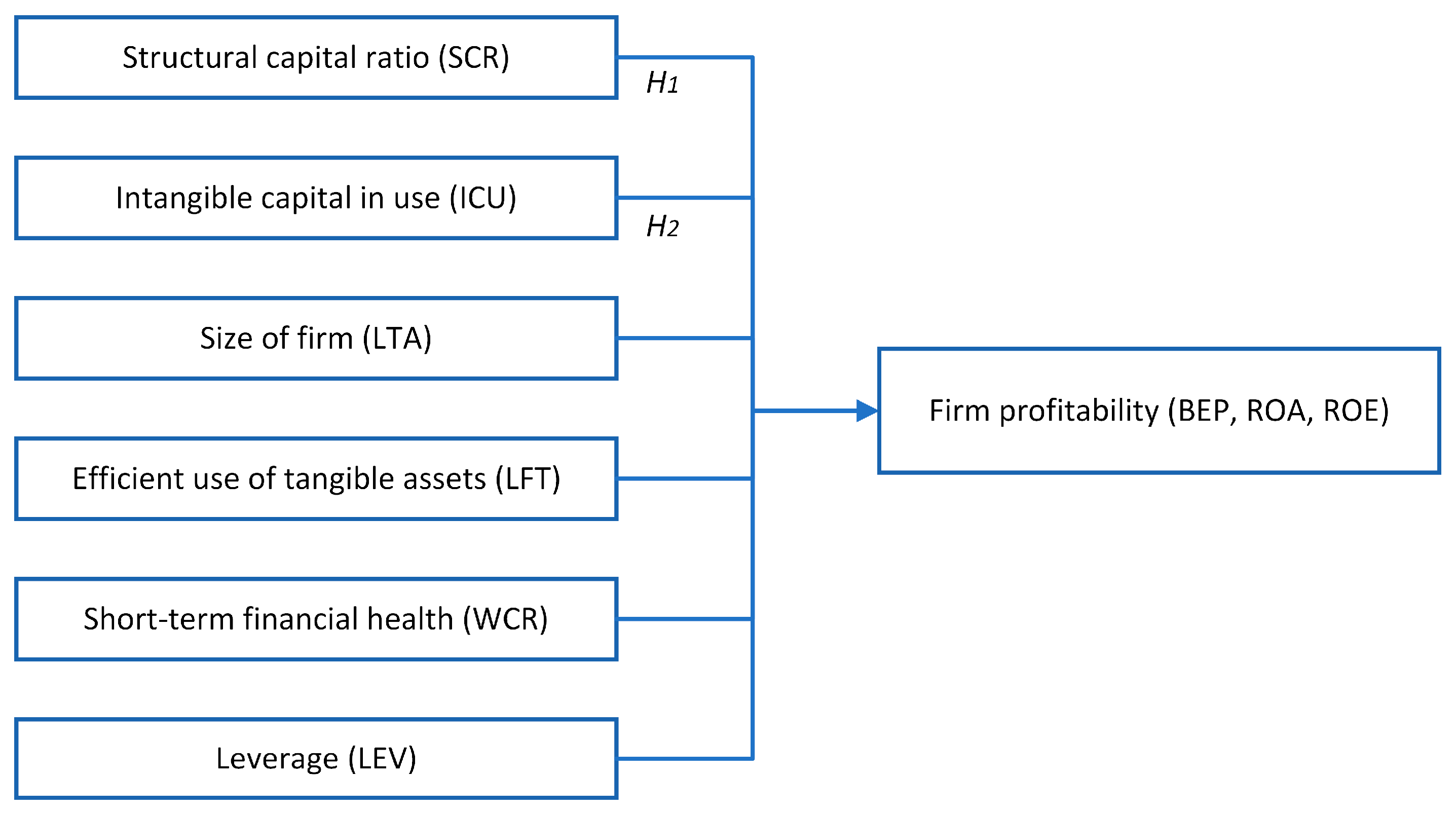

3.1. Variable Descriptions and Model Specifications

- Basic earnings power (BEP) illustrates the capacity of the firm to generate profits before tax and debt service, in relation to total assets. BEP is comparable across various tax conditions and levels of financial leverage, so that it is a financial ratio that is still relevant in an international comparison. BEP can be positive or negative depending on the sign of numerator (earnings before interest and tax). This indicator has been used before in a similar model by Tiwari (2022).

- Return on assets (ROA) shows how profitable a company is in relation to its total assets. ROA is a financial performance ratio which is frequently used in accounting research as a dependent variable, while being sector-specific. This indicator is calculated starting from net income but excluding extraordinary (one-time) elements that could influence financial performance (such as mergers or divestments). ROA can be positive or negative, depending on the sign of the numerator (net income). This profitability indicator has been used in several articles testing similar models (Chowdhury et al. 2019; Rahman and Liu 2023; Sardo et al. 2018; Scafarto et al. 2023).

- Return on equity (ROE) is a financial performance indicator in relation to net assets (i.e., total assets minus total liabilities). Shareholders’ equity is a residual amount that can be positive or negative, depending on the size of the total liabilities compared to total assets. If net income is a loss and total equity is negative, ROE becomes positive. Database cleaning solves this situation by removing entries with negative shareholders’ equity. This profitability indicator has been used in several articles testing similar models (Chowdhury et al. 2019; Rahman and Liu 2023; Scafarto et al. 2023).

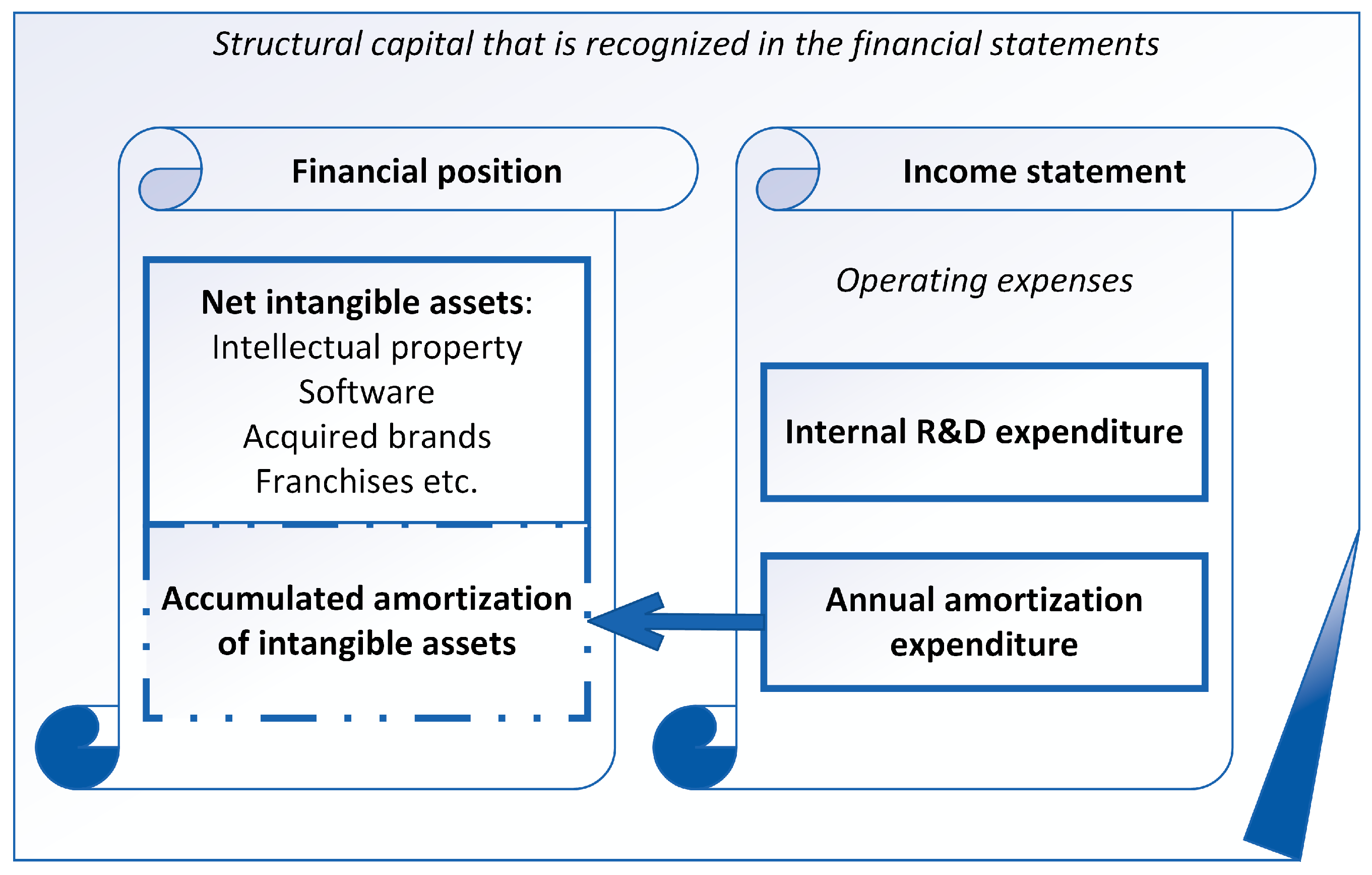

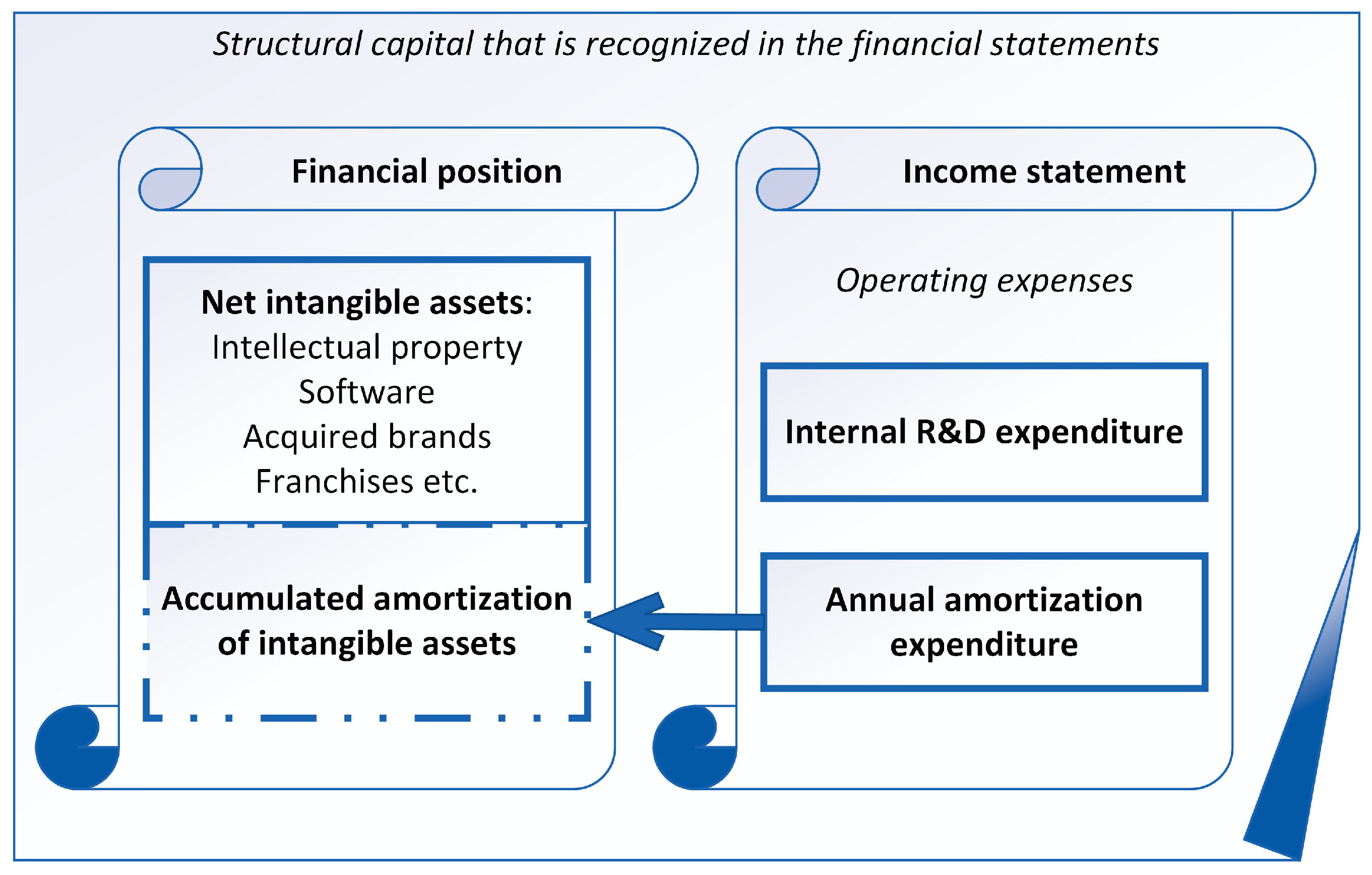

- The structural capital ratio (SCR) is calculated as the proportion of intangible assets (excluding goodwill) to total non-current assets (net of depreciation and amortization). This ratio shows the degree of reliance on intangible assets during operations. This ratio is a snapshot at year end, after the utilization of these assets. From another perspective, it shows the proportion of intangible assets that are available for use during the next financial year. Therefore, SCR at the end of year t is expected to have an effect in the t + 1 period.

- Intangible capital in use (ICU) is the ratio of intangible asset-related expenses to total operating expenses. It shows how much intangible capital (if quantified) was used during the year, in relation to the use of the entire set of company resources. The ICU is expected to have an immediate effect on profitability, but also a delayed effect because intangible capital is an investment. Intangible capital in use captures a different economic reality than SCR because it does not strictly refer to capitalized resources, but also to expenditures that may not appear on the balance sheet. The ICU depends on the correct classification of R&D expenditures according to the IFRS or US GAAP.

- Company size (LTA), calculated as the natural logarithm of total assets, is a control variable frequently used in similar models (Chowdhury et al. 2019; Rahman and Liu 2023; Sardo et al. 2018; Scafarto et al. 2023; Tiwari 2022). It is expected that larger companies are different in terms of their profitability compared to smaller companies. This variable isolates this effect.

- Fixed assets turnover (LFT) indicates the efficiency in the use of property, plant and equipment (PPE). This indicator shows how tangible non-current assets are used by the company, distinct from intangible capital. Compared to the intangible capital ratios used in this paper, LFT is an efficiency indicator, meaning that the numerator is sales, the outcome of economic activity.

- The working capital ratio (WCR) is an indicator of the short-term liquidity and financial health of the business. It measures the capacity of the company to pay its short-term obligations using current assets other than cash. The denominator (total assets) is introduced to provide a relative scale for the numerator (which can also be negative). WCR has been used before in a similar model by Rahman and Liu (2023).

- Leverage (LEV) is an indicator used to isolate the effect of company indebtedness. It is a structural ratio for which total debt has been chosen as the numerator and total equity as the denominator. Variables with the same significance have been used in articles testing similar models (Rahman and Liu 2023; Sardo et al. 2018; Scafarto et al. 2023; Tiwari 2022). It is expected that higher levels of leverage are associated with a less strong financial position and a lower capacity to generate revenue and cash flows.

3.2. Data Collection and Cleaning

- Countries of incorporation: all 27 European Union (EU) countries, plus the United Kingdom, Norway and Switzerland. In total, the population included 30 countries. All EU-based companies in the sample apply IFRS (Regulation (EC) 1606 2002; Zeghal et al. 2012). Companies listed on the London Stock Exchange apply IFRS (IFRS Foundation 2021). The authorities in Norway require the application of IFRS for listed companies on the Oslo Stock Exchange. The SIX Exchange in Switzerland allows reporting according to IFRS or US GAAP. The differences between IFRS and US GAAP on the matter of intangibles do not affect the reported values (EY 2021). Therefore, the measurement of intangibles and the recognition of amortization and R&D expenditures are consistent throughout the sample.

- Industries: technology and healthcare, as these are the most intangible-oriented economic sectors.

- Checked and removed negative values on total assets.

- Removed negative values on intangible assets and total non-current assets.

- Removed zeros and negative values on fixed assets turnover. The natural logarithm of fixed assets turnover was computed to normalize the distribution.

- Removed negative values on total debt and total equity. While total equity can be negative (if the net loss is higher than common equity), the calculated leverage would not make sense with a negative denominator.

- Removed negative values on research and development expenses and the amortization of intangibles.

- Removed zeros and negative values on total operating expenses (i.e., the denominator of ICU).

3.3. Panel Estimation

4. Results

4.1. Descriptive Statistics and Correlations

4.2. Main Model Estimation for the Full Sample

4.3. Robustness Tests: Main Model Estimation for First Differences

4.4. Robustness Tests: Main Model Estimation for Each Industry

4.5. Robustness Tests: Estimation with One-Year-Lagged Dependent Variables

4.6. Robustness Tests: One-Year-Lagged Dependent and Main Predictor Variables

4.7. Robustness Tests: One-Year-Lagged Dependent and Two-Year-Lagged Main Predictor Variables

5. Discussion and Conclusions

Supplementary Materials

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Indicator | Name in Refinitiv | Description from Refinitiv |

|---|---|---|

| Expenses with amortization of intangibles | Amortization of Intangibles, Operating | Represents the financial year’s amortization expense by allocating the cost of assets that lack physical existence over those periods expected to benefit from the use of these assets. |

| Earnings before interest and tax (EBIT) | EBIT | Computed as total revenues for the fiscal year minus total operating expenses plus operating interest expense, unusual expense/income and non-recurring items, for the same period. This definition excludes non-operating income and expenses. |

| Fixed asset turnover | Fixed Asset Turnover | The amount of revenue generated for each unit of fixed assets. It is calculated as primary revenue for the fiscal period divided by the sum of total net property, plant and equipment and total net utility plant for the same period. |

| Intangible assets (net) | Intangibles, Net | Represents intangibles, gross reduced by accumulated intangible amortization. Excludes goodwill net of amortization. |

| Net income before extraordinary items | Net Income Before Extraordinary Items | Represents net income before being adjusted by extraordinary items, such as accounting change, discontinued operations, extraordinary items and taxes on extraordinary items. |

| Net sales | Net Sales | Represents sales receipts for products and services, less cash discounts, trade discounts, excise tax and sales returns and allowances. Revenues are recognized according to applicable accounting principles. |

| Net working capital | Working Capital | This item is defined as the difference between current assets and current liabilities for the fiscal period. Available for industrial and utility companies. Can take negative values. |

| Primary revenue | Revenue | Is used for industrial and utility companies. It consists of revenue from the sale of merchandise, manufactured goods and services and the distribution of regulated energy resources, depending on a specific company’s industry. |

| R&D expenditures | Research and Development | Represents expenses for the research and development of new products and services by a company to obtain a competitive advantage. |

| ROE | ROE Total Equity % | This value is calculated as the net income before extraordinary items for the fiscal period divided by the same period’s average total equity and is expressed as a percentage. Average total equity is the average of total equity at the beginning and the end of the year. Available for industrial and utility companies. |

| Total assets | Total Assets, Reported | Represents the total assets of a company. |

| Total debt | Total Debt | Represents total debt outstanding, which includes notes payable/short-term debt, current portion of long-term debt/capital leases and total long-term debt. |

| Total equity | Total Equity | Consists of the equity value of preferred shareholders, general and limited partners and common shareholders, but does not include minority shareholders’ interest. |

| Total non-current assets (net) | Total Fixed Assets, Net | This item represents the sum of total net property, plant and equipment, net intangibles, long term investments, other total long-term assets, other total assets and total net utility plant for the fiscal period. Not available for banks and insurance (financial) companies. |

| Total operating expenses | Total Operating Expense | Represents the sum of the cost of revenue; selling/general/administrative expenses; research and development; depreciation and amortization; net-operating interest expense (income); unusual expenses (income); and other operating expenses. |

References

- Ahmad, Fawad. 2023. Modified VAIC model: Measuring missing components information and treatment of exogenous factors. Managerial Finance 49: 1453–73. [Google Scholar] [CrossRef]

- Arellano, Manuel. 1987. Computing Robust Standard Errors for Within-groups Estimators. Oxford Bulletin of Economics and Statistics 49: 431–34. [Google Scholar] [CrossRef]

- Ashraf, Sumaira, Misbah Sadiq, Paulo Ferreira, and António Martins Almeida. 2023. Intellectual Capital and a Firm’s Sustainable Performance and Growth before and during the COVID-19 Crisis: A Comparative Analysis of Small and Large European Hospitality Firms. Sustainability 15: 9743. [Google Scholar] [CrossRef]

- Ballester, Marta, Manuel Garcia-Ayuso, and Joshua Livnat. 2003. The economic value of the R&D intangible asset. European Accounting Review 12: 605–33. [Google Scholar] [CrossRef]

- Baltagi, Badi H. 2005. Econometric Analysis of Panel Data, 3rd ed. Hoboken: John Wiley & Sons. [Google Scholar]

- Barbiroli, Giancarlo. 2011. Economic consequences of the transition process toward green and sustainable economies: Costs and advantages. International Journal of Sustainable Development & World Ecology 18: 17–27. [Google Scholar] [CrossRef]

- Bătae, Oana Marina, Voicu Dan Dragomir, and Liliana Feleagă. 2021. The relationship between environmental, social, and financial performance in the banking sector: A European study. Journal of Cleaner Production 290: 125791. [Google Scholar] [CrossRef]

- Bouri, Elie, Muhammad Abubakr Naeem, Safwan Mohd Nor, Imen Mbarki, and Tareq Saeed. 2022. Government responses to COVID-19 and industry stock returns. Economic Research-Ekonomska Istraživanja 35: 1967–90. [Google Scholar] [CrossRef]

- Butt, Moeen Naseer, Ahmed S. Baig, and Fazal Jawad Seyyed. 2023. Tobin’s Q approximation as a metric of firm performance: An empirical evaluation. Journal of Strategic Marketing 31: 532–48. [Google Scholar] [CrossRef]

- Chen, Fu-Chiang, Z.-John Liu, and Qian Long Kweh. 2014. Intellectual capital and productivity of Malaysian general insurers. Economic Modelling 36: 413–20. [Google Scholar] [CrossRef]

- Chowdhury, Leena Afroz Mostofa, Tarek Rana, and Mohammad Istiaq Azim. 2019. Intellectual capital efficiency and organisational performance: In the context of the pharmaceutical industry in Bangladesh. Journal of Intellectual Capital 20: 784–806. [Google Scholar] [CrossRef]

- Chu, Hanfang, Hanxin Wang, and Zhaoyun Wang. 2023. Impact of Innovation Quality on the Growth Performance of Entrepreneurial Enterprises: The Role of Knowledge Capital. Sustainability 15: 8207. [Google Scholar] [CrossRef]

- Cillo, Valentina, Gian Luca Gregori, Lucia Michela Daniele, Francesco Caputo, and Nathalie Bitbol-Saba. 2022. Rethinking companies’ culture through knowledge management lens during Industry 5.0 transition. Journal of Knowledge Management 26: 2485–98. [Google Scholar] [CrossRef]

- Clausen, Saskia, and Stefan Hirth. 2016. Measuring the value of intangibles. Journal of Corporate Finance 40: 110–27. [Google Scholar] [CrossRef]

- Croissant, Yves, and Givanni Millo, eds. 2018. Panel Data Econometrics with R, 1st ed. Hoboken: Wiley. [Google Scholar] [CrossRef]

- Croissant, Yves, Givanni Millo, and Kevin Tappe. 2023. Package ‘Plm’. Version 2.6-3. Available online: https://cran.r-project.org/web/packages/plm/plm.pdf (accessed on 27 November 2023).

- Dai, Lu, Jiajun Zhang, and Shougui Luo. 2022. Effective R&D capital and total factor productivity: Evidence using spatial panel data models. Technological Forecasting and Social Change 183: 121886. [Google Scholar] [CrossRef]

- Dancaková, Darya, Jakub Sopko, Jozef Glova, and Alena Andrejovská. 2022. The Impact of Intangible Assets on the Market Value of Companies: Cross-Sector Evidence. Mathematics 10: 3819. [Google Scholar] [CrossRef]

- Dragomir, Voicu Dan, and Valentin Florentin Dumitru. 2023. Recognition and Measurement of Crypto-Assets from the Perspective of Retail Holders. FinTech 2: 543–59. [Google Scholar] [CrossRef]

- Duho, King Carl Tornam. 2022. Intangibles, Intellectual Capital, and the Performance of Listed Non-Financial Services Firms in West Africa: A Cross-Country Analysis. Merits 2: 101–25. [Google Scholar] [CrossRef]

- EY. 2021. US GAAP versus IFRS. The Basics. Ernst & Young LLP. Available online: https://assets.ey.com/content/dam/ey-sites/ey-com/en_us/topics/assurance/accountinglink/ey-ifrs11560-211us-01-14-2021.pdf (accessed on 27 November 2023).

- Faraji, Omid, Kaveh Asiaei, Zabihollah Rezaee, Nick Bontis, and Ehsan Dolatzarei. 2022. Mapping the conceptual structure of intellectual capital research: A co-word analysis. Journal of Innovation & Knowledge 7: 100202. [Google Scholar] [CrossRef]

- Feleagă, Liliana, Niculae Feleagă, Voicu Dan Dragomir, and Luciana Râbu. 2013. European evidence on intellectual capital: Linking methodologies with firm disclosures. Acta Oeconomica 63: 139–56. [Google Scholar] [CrossRef]

- Fernández, Esteban, José M. Montes, and Camilo J. Vázquez. 2000. Typology and strategic analysis of intangible resources. Technovation 20: 81–92. [Google Scholar] [CrossRef]

- Fontana, Stefano, Daniela Coluccia, and Silvia Solimene. 2019. VAIC as a Tool for Measuring Intangibles Value in Voluntary Multi-Stakeholder Disclosure. Journal of the Knowledge Economy 10: 1679–99. [Google Scholar] [CrossRef]

- Fritsch, Markus, Andrew Adrian Yu Pua, and Joachim Schnurbus. 2019. Pdynmc—An R-Package for Estimating Linear Dynamic Panel Data Models Based on Linear and Nonlinear Moment Conditions (Passauer Diskussionspapiere-Betriebswirtschaftliche Reihe, No. B-39-19). Available online: https://www.econstor.eu/bitstream/10419/204584/1/1678189383.pdf (accessed on 27 November 2023).

- Gupta, Juhi, Payal Rathore, and Smita Kashiramka. 2023. Impact of Intellectual Capital on the Financial Performance of Innovation-Driven Pharmaceutical Firms: Empirical Evidence from India. Journal of the Knowledge Economy 14: 1052–76. [Google Scholar] [CrossRef]

- Habibniya, Houshang, Suzan Dsouza, Mustafa Raza Rabbani, Nishad Nawaz, and Rezart Demiraj. 2022. Impact of Capital Structure on Profitability: Panel Data Evidence of the Telecom Industry in the United States. Risks 10: 157. [Google Scholar] [CrossRef]

- Hsiao, Cheng. 2007. Panel data analysis—Advantages and challenges. TEST 16: 1–22. [Google Scholar] [CrossRef]

- IASB. 2014. IAS 38. Intangible Assets. IFRS Foundation. Available online: https://www.ifrs.org/content/dam/ifrs/publications/pdf-standards/english/2021/issued/part-a/ias-38-intangible-assets.pdf (accessed on 27 November 2023).

- Iazzolino, Gianpaolo, and Domenico Laise. 2013. Value added intellectual coefficient (VAIC): A methodological and critical review. Journal of Intellectual Capital 14: 547–63. [Google Scholar] [CrossRef]

- IFRS Foundation. 2021. Who uses IFRS Accounting Standards? United Kingdom. IFRS. September 3. Available online: https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/view-jurisdiction/united-kingdom/ (accessed on 27 November 2023).

- Kasoga, Pendo Shukrani. 2020. Does investing in intellectual capital improve financial performance? Panel evidence from firms listed in Tanzania DSE. Cogent Economics & Finance 8: 1802815. [Google Scholar] [CrossRef]

- Katona, Klára. 2018. Impact of Knowledge Capital on the Production of Hungarian Firms. International Advances in Economic Research 24: 135–46. [Google Scholar] [CrossRef]

- Kristandl, Gerhard, and Nick Bontis. 2007. Constructing a definition for intangibles using the resource based view of the firm. Management Decision 45: 1510–24. [Google Scholar] [CrossRef]

- Krstić, Bojan, Ljiljana Bonić, Tamara Rađenović, Milica Jovanović Vujatović, and Jasmina Ognjanović. 2023. Improving Profitability Measurement: Impact of Intellectual Capital Efficiency on Return on Total Employed Resources in Smart and Knowledge-Intensive Companies. Sustainability 15: 12076. [Google Scholar] [CrossRef]

- Lev, Baruch, and Suresh Radhakrishnan. 2005. The Valuation of Organization Capital. In Measuring Capital in the New Economy. Edited by Carol Corrado, John Haltiwanger and Dan Sichel. Chicago: University of Chicago Press, pp. 73–110. Available online: http://www.nber.org/chapters/c10619 (accessed on 27 November 2023).

- Marzo, Giuseppe. 2022. A theoretical analysis of the value added intellectual coefficient (VAIC). Journal of Management and Governance 26: 551–77. [Google Scholar] [CrossRef]

- Marzo, Giuseppe, and Stefano Bonnini. 2023. Uncovering the non-linear association between VAIC and the market value and financial performance of firms. Measuring Business Excellence 27: 71–88. [Google Scholar] [CrossRef]

- Meles, Antonio, Claudio Porzio, Gabriele Sampagnaro, and Vincenzo Verdoliva. 2016. The impact of the intellectual capital efficiency on commercial banks performance: Evidence from the US. Journal of Multinational Financial Management 36: 64–74. [Google Scholar] [CrossRef]

- Molloy, Janice C., Clint Chadwick, Robert E. Ployhart, and Simon J. Golden. 2011. Making Intangibles “Tangible” in Tests of Resource-Based Theory: A Multidisciplinary Construct Validation Approach. Journal of Management 37: 1496–518. [Google Scholar] [CrossRef]

- Moon, Yun Ji, and Hyo Gun Kym. 2006. A Model for the Value of Intellectual Capital. Canadian Journal of Administrative Sciences/Revue Canadienne Des Sciences de l’Administration 23: 253–69. [Google Scholar] [CrossRef]

- Mooneeapen, Oren, Subhash Abhayawansa, and Naushad Mamode Khan. 2022. The influence of the country governance environment on corporate environmental, social and governance (ESG) performance. Sustainability Accounting, Management and Policy Journal 13: 953–85. [Google Scholar] [CrossRef]

- Nawaz, Tasawar, and Oliver Ohlrogge. 2023. Clarifying the impact of corporate governance and intellectual capital on financial performance: A longitudinal study of Deutsche Bank (1957–2019). International Journal of Finance & Economics 28: 3808–23. [Google Scholar] [CrossRef]

- Nguyen, Nguyet Thi. 2023. The Impact of Intellectual Capital on Service Firm Financial Performance in Emerging Countries: The Case of Vietnam. Sustainability 15: 7332. [Google Scholar] [CrossRef]

- Norkio, Antti. 2023. Intangible capital and financial leverage in SMEs. Managerial Finance. ahead-of-print. [Google Scholar] [CrossRef]

- Novas, Jorge Casas, Maria Do Céu Gaspar Alves, and António Sousa. 2017. The role of management accounting systems in the development of intellectual capital. Journal of Intellectual Capital 18: 286–315. [Google Scholar] [CrossRef]

- Porter, Michael. 2001. The value chain and competitive advantage. In Understanding Business: Processes. Edited by David Barnes. London: Routledge, Taylor and Francis Group, pp. 50–66. [Google Scholar]

- Pulic, Ante. 2000. VAICTM an accounting tool for IC management. International Journal of Technology Management 20: 702. [Google Scholar] [CrossRef]

- Pulic, Ante. 2004. Intellectual capital—Does it create or destroy value? Measuring Business Excellence 8: 62–68. [Google Scholar] [CrossRef]

- Radonić, Milenko, Miloš Milosavljević, and Snežana Knežević. 2021. Intangible Assets as Financial Performance Drivers of IT Industry: Evidence from an Emerging Market. E+M Ekonomie a Management 24: 119–35. [Google Scholar] [CrossRef]

- Rahman, Md. Jahidur, and Hongyi Liu. 2023. Intellectual capital and firm performance: The moderating effect of auditor characteristics. Asian Review of Accounting 31: 522–58. [Google Scholar] [CrossRef]

- Regulation (EC) 1606. 2002. Regulation (EC) 1606/2002 of the European Parliament and of the Council of 19 July 2002 on the Application of International Accounting Standards 2002. Available online: http://data.europa.eu/eli/reg/2002/1606/oj (accessed on 27 November 2023).

- Sardo, Filipe, Zélia Serrasqueiro, and Helena Alves. 2018. On the relationship between intellectual capital and financial performance: A panel data analysis on SME hotels. International Journal of Hospitality Management 75: 67–74. [Google Scholar] [CrossRef]

- Scafarto, Vincenzo, Tamanna Dalwai, Federica Ricci, and Gaetano Della Corte. 2023. Digitalization and Firm Financial Performance in Healthcare: The Mediating Role of Intellectual Capital Efficiency. Sustainability 15: 4031. [Google Scholar] [CrossRef]

- Shakil, Mohammad Hassan, Nihal Mahmood, Mashiyat Tasnia, and Ziaul Haque Munim. 2019. Do environmental, social and governance performance affect the financial performance of banks? A cross-country study of emerging market banks. Management of Environmental Quality: An International Journal 30: 1331–44. [Google Scholar] [CrossRef]

- Sichigea, Mirela, Marian Ilie Siminica, Daniel Circiumaru, Silviu Carstina, and Nela-Loredana Caraba-Meita. 2020. A Comparative Approach of the Environmental Performance between Periods with Positive and Negative Accounting Returns of EEA Companies. Sustainability 12: 7382. [Google Scholar] [CrossRef]

- Ståhle, Pirjo, Sten Ståhle, and Samuli Aho. 2011. Value added intellectual coefficient (VAIC): A critical analysis. Journal of Intellectual Capital 12: 531–51. [Google Scholar] [CrossRef]

- Tiwari, Ranjit. 2022. Nexus between intellectual capital and profitability with interaction effects: Panel data evidence from the Indian healthcare industry. Journal of Intellectual Capital 23: 588–616. [Google Scholar] [CrossRef]

- Vergauwen, Philip, Laury Bollen, and Els Oirbans. 2007. Intellectual capital disclosure and intangible value drivers: An empirical study. Management Decision 45: 1163–80. [Google Scholar] [CrossRef]

- Zéghal, Daniel, and Anis Maaloul. 2011. The accounting treatment of intangibles—A critical review of the literature. Accounting Forum 35: 262–74. [Google Scholar] [CrossRef]

- Zeghal, Daniel, Sonda M. Chtourou, and Yosra M. Fourati. 2012. The Effect of Mandatory Adoption of IFRS on Earnings Quality: Evidence from the European Union. Journal of International Accounting Research 11: 1–25. [Google Scholar] [CrossRef]

| Study | Industry | Countries | Sample (Firms) | Dependent | Predictor | Relationship 1 |

|---|---|---|---|---|---|---|

| Ahmad (2023) | All | US | 6019 | ROA, ROE, MB | Innovation capital efficiency | All: + (sig.) |

| Ashraf et al. (2023) | Hospitality | 18 EU countries | 42,516 | ROA, AG | Structural capital = working capital turnover | ROA: − (sig.) AG: + (sig.) |

| Chowdhury et al. (2019) | Pharma | Bangladesh | 23 | AT, ROA, ROE, MB | Structural capital efficiency | All: n/s |

| Chu et al. (2023) | Technology | China | 44 | ROA | Invention patents | + (sig.) |

| Dancaková et al. (2022) | All | Germany, France, Switzerland | 250 | TQ | Intangible assets intensity | n/s |

| Duho (2022) | Not specified | West African countries | 59 | ROA | Structural capital efficiency | + (sig.) |

| Gupta et al. (2023) | Pharma | India | 82 | ROA, ROE, ROS | Structural capital efficiency | ROA, ROE− (sig.) ROS: n/s |

| Kasoga (2020) | Manufacturing | Tanzania | 22 | ROA, AT, SG, TQ | Structural capital efficiency | All: + (sig.) |

| Katona (2018) | 7 industries | Hungary | 36,801 | Firm production | Technological capital | 1996–2005: − (sig.) 2005–2014: + (sig.) |

| Krstić et al. (2023) | Not specified | International (global brands) | 36 | ROA, RUE | Efficiency in the use of intangible assets | All: + (sig.) |

| Marzo and Bonnini (2023) | All | Italy | 126 | ROA, ROE, MB | Structural capital efficiency | ROA 2018: n/s ROE 2018: + (sig.) MB 2018: n/s |

| Meles et al. (2016) | Banks | US | 5749 | ROA, ROE | Structural capital efficiency | All: n/s |

| Nawaz and Ohlrogge (2023) | Banks | Germany | 1 (60 years) | ROA, ROE | Structural capital efficiency | All: + (sig.) |

| Nguyen (2023) | Services | Vietnam | Not specified | ROE | Structural capital efficiency | Small firms: n/s Large firms: + (sig.) |

| Radonić et al. (2021) | Technology | Serbia | 101 | ROA, ROE | Structural capital, innovation capital | + (sig.) |

| Rahman and Liu (2023) | Transportation | China | 76 | ROA, ROE, AT | Structural capital efficiency | All: n/s |

| Sardo et al. (2018) | Hotels | Portugal | 934 | ROA | Structural capital = working capital turnover | + (sig.) |

| Scafarto et al. (2023) | Healthcare | EU | 193 | ROA | Structural capital efficiency | + (sig.) |

| Tiwari (2022) | Healthcare | India | 84 | ROA | Structural capital efficiency | + (sig.) |

| Abbreviation | Description | Calculation |

|---|---|---|

| Dependent variables | ||

| BEP 1 | Basic earnings power | Earnings before interest and tax (EBIT)/Total assets |

| ROA 1 | Return on assets | Net income before extraordinary items/Total assets |

| ROE 2 | Return on equity | Net income before extraordinary items/Total equity |

| Main predictors | ||

| SCR 1 | Structural capital ratio (proportion of intangible assets) | Intangible assets (net)/ Total non-current assets (net) |

| ICU 1 | Intangible capital in use | (Expenses with amortization of intangibles + R&D expenditures)/Total operating expenses |

| Control variables | ||

| LTA 2 | Company size | Natural logarithm (Total assets) |

| LFT 2 | Fixed asset turnover (efficient use of PPE) | Natural logarithm (Net sales/Property, plant, and equipment, PPE) |

| WCR 1 | Net working capital ratio (short-term financial health) | Net working capital/Total assets |

| LEV 1 | Leverage | Total debt/Total equity |

| Country | No. of Companies | Country | No. of Companies |

|---|---|---|---|

| Austria | 3 | Malta | 3 |

| Belgium | 14 | Netherlands | 12 |

| Bulgaria | 3 | Norway | 13 |

| Croatia | 3 | Poland | 48 |

| Denmark | 17 | Portugal | 4 |

| Finland | 22 | Romania | 3 |

| France | 94 | Slovak Republic | 1 |

| Germany | 117 | Slovenia | 3 |

| Greece | 13 | Spain | 19 |

| Hungary | 5 | Sweden | 79 |

| Italy | 17 | Switzerland | 31 |

| Latvia | 1 | United Kingdom | 99 |

| Lithuania | 1 |

| Variable 1 | Min | Median | Mean | Max | SD | Zeros | Skewness | Kurtosis |

|---|---|---|---|---|---|---|---|---|

| BEP | −0.4982 | 0.0595 | 0.0357 | 0.3315 | 0.1457 | - | −1.5490 | 3.8332 |

| ROA | −0.5275 | 0.0361 | 0.0092 | 0.2595 | 0.1412 | - | −1.8459 | 4.4530 |

| ROE | −1.0565 | 0.0856 | 0.2744 | 0.5946 | 0.2878 | - | −1.6549 | 4.1161 |

| SCR | 0.0027 | 0.3945 | 0.4187 | 0.9618 | 0.2961 | - | 0.2340 | −1.2118 |

| ICU | 0 | 0.0166 | 0.0699 | 0.5643 | 0.1158 | 34% | 2.5269 | 6.7794 |

| LTA | 15.0259 | 18.5929 | 18.8279 | 24.6027 | 2.2453 | - | 0.5675 | −0.1597 |

| LFT | −0.5171 | 2.2536 | 2.2867 | 5.2452 | 1.3525 | - | 0.0504 | −0.5291 |

| WCR | −0.1846 | 0.1892 | 0.2126 | 0.7621 | 0.2204 | - | 0.4785 | 0.2862 |

| LEV | 0 | 0.2674 | 0.4859 | 3.0187 | 0.6313 | 10.6% | 2.2008 | 5.1739 |

| Vars. | BEP | ROA | ROE | SCR | ICU | LTA | LFT | WCR | LEV |

|---|---|---|---|---|---|---|---|---|---|

| BEP | 1 | 0.9365 ** | 0.8625 ** | −0.1714 ** | −0.2706 ** | 0.3016 ** | 0.1406 ** | −0.0627 ** | −0.0381 ** |

| ROA | 1 | 0.9211 ** | −0.1803 ** | −0.2532 ** | 0.2766 ** | 0.1336 ** | −0.0271 * | −0.0825 ** | |

| ROE | 1 | −0.1639 ** | −0.2259 ** | 0.2870 ** | 0.1351 ** | −0.0073 | −0.1223 ** | ||

| SCR | 1 | 0.1768 ** | −0.1993 ** | 0.3736 ** | −0.1203 ** | −0.0906 ** | |||

| ICU | 1 | 0.0976 ** | −0.1425 ** | 0.1938 ** | −0.0933 ** | ||||

| LTA | 1 | −0.3296 ** | −0.2743 ** | 0.2548 ** | |||||

| LFT | 1 | 0.1201 ** | −0.2021 ** | ||||||

| WCR | 1 | −0.4397 ** | |||||||

| LEV | 1 |

| Models | |||

|---|---|---|---|

| Predictors/Statistics | BEP Coeff. (t-Value) | ROA Coeff. (t-Value) | ROE Coeff. (t-Value) |

| SCR | −0.0941 (−6.907) ** | −0.0902 (−6.654) ** | −0.1607 (−5.773) ** |

| ICU | −0.1264 (−2.359) * | −0.0629 (−1.269) | −0.1791 (−2.116) * |

| LTA | 0.0366 (8.276) ** | 0.0385 (9.173) ** | 0.0804 (8.915) ** |

| LFT | 0.0409 (10.455) ** | 0.0381 (10.662) ** | 0.0712 (9.653) ** |

| WCR | 0.1021 (6.256) ** | 0.1146 (7.294) ** | 0.2496 (7.505) ** |

| LEV | −0.0133 (−3.128) ** | −0.0203 (−4.234) ** | −0.0961 (−7.139) ** |

| Firms (periods) | 625 (10) | 625 (10) | 625 (10) |

| Obs. (balanced) | 6250 | 6250 | 6250 |

| Countries | 25 | 25 | 25 |

| Breusch–Pagan time effects test: chi-sq (df) | 0.0009 (1) | 1.2957 (1) | 0.7056 (1) |

| Time effects | Non-significant | Non-significant | Non-significant |

| Hausman: chi-sq (df) | 88.732 (6) ** | 124.26 (6) ** | 113.66 (6) ** |

| Wooldridge’s test for serial correlation | 277.48 (1, 5623) ** | 138.48 (1, 5623) ** | 170.74 (1, 5623) ** |

| Estimation | FE (firms) | FE (firms) | FE (firms) |

| R-squared | 0.1637 | 0.1492 | 0.1693 |

| F (df) | 43.2411 (6, 624) ** | 52.3138 (6, 624) ** | 51.1267 (6, 624) |

| Models | |||

|---|---|---|---|

| Predictors/Statistics | ΔBEP Coeff. (t-Value) | ΔROA Coeff. (t-Value) | ΔROE Coeff. (t-Value) |

| ΔSCR | −0.0450 (−3.821) ** | −0.0355 (−2.510) * | 0.0681 (−2.164) * |

| ΔICU | −0.0888 (−1.249) | 0.0618 (0.908) | 0.1228 (1.054) |

| Firms (periods) | 625 (9) | 625 (9) | 625 (9) |

| Obs. (balanced) | 5625 | 5625 | 5625 |

| Countries | 25 | 25 | 25 |

| Estimation | FE (firms) | FE (firms) | FE (firms) |

| R-Squared | 0.0055 | 0.0022 | 0.0017 |

| F (df) | 8.4706 (2, 624) ** | 3.4902 (2, 624) * | 2.8525 (2, 624) |

| Models (Technology Sample) | |||

|---|---|---|---|

| Predictors/Statistics | BEP Coeff. (t-Value) | ROA Coeff. (t-Value) | ROE Coeff. (t-Value) |

| SCR | −0.0772 (−4.973) ** | −0.0785 (−5.110) ** | −0.1606 (−5.125) ** |

| ICU | −0.1601 (−2.114) * | −0.0412 (−0.589) | −0.0914 (−0.723) |

| LTA | 0.0266 (4.987) ** | 0.0301 (6.001) ** | 0.0695 (6.204) ** |

| LFT | 0.0336 (7.765) ** | 0.0302 (7.870) ** | 0.0619 (7.118) ** |

| WCR | 0.0911 (4.222) ** | 0.1118 (5.417) ** | 0.2368 (5.647) ** |

| LEV | −0.0176 (3.235) ** | −0.0243 (−3.883) ** | −0.0927 (−5.253) ** |

| Firms (periods) | 429 (10) | 429 (10) | 429 (10) |

| Obs. (balanced) | 4290 | 4290 | 4290 |

| Countries | 23 | 23 | 23 |

| Breusch–Pagan time effects test: chi-sq (df) | 1.2832 (1) | 0.0002 (1) | 0.0315 (1) |

| Time effects | Non-significant | Non-significant | Non-significant |

| Hausman: chi-sq (df) | 26.472 (6) ** | 42.14 (6) ** | 46.237 (6) ** |

| Wooldridge’s test for serial correlation | 190.54 (1, 3859) ** | 88.135 (1, 3859) ** | 102.67 (1, 3859) ** |

| Estimation | FE (firms) | FE (firms) | FE (firms) |

| R-squared | 0.1229 | 0.1126 | 0.1310 |

| F (df) | 20.5925 (6, 428) ** | 25.9047 (6, 428) ** | 27.6549 (6, 428) ** |

| Models (Healthcare Sample) | |||

|---|---|---|---|

| Predictors/Statistics | BEP Coeff. (t-Value) | ROA Coeff. (t-Value) | ROE Coeff. (t-Value) |

| SCR | −0.1284 (−4.687) ** | −0.1144 (−4.141) ** | −0.1594 (−2.758) ** |

| ICU | −0.1066 (−1.690) | −0.0893 (−1.495) | −0.2690 (−2.607) ** |

| LTA | 0.0497 (7.053) ** | 0.0505 (7.156) ** | 0.0952 (6.283) ** |

| LFT | 0.0555 (7.855) ** | 0.0554 (8.079) ** | 0.0922 (7.142) ** |

| WCR | 0.0983 (3.964) ** | 0.0984 (3.929) ** | 0.2442 (4.427) ** |

| LEV | −0.0063 (−0.979) | −0.0138 (−1.944) | −0.1019 (−5.006) ** |

| Firms (periods) | 196 (10) | 196 (10) | 196 (10) |

| Obs. (balanced) | 1960 | 1960 | 1960 |

| Countries | 20 | 20 | 20 |

| Breusch–Pagan time effects test: chi-sq (df) | 0.2009 (1) | 0.6118 (1) | 0.1224 (1) |

| Time effects | Non-significant | Non-significant | Non-significant |

| Hausman: chi-sq (df) | 65.545 (6) ** | 75.22 (6) ** | 67.699 (6) ** |

| Wooldridge’s test for serial correlation | 84.819 (1, 1762) ** | 49.803 (1, 1762) ** | 67.541 (1, 1762) ** |

| Estimation | FE (firms) | FE (firms) | FE (firms) |

| R-squared | 0.2512 | 0.2284 | 0.2497 |

| F (df) | 26.7485 (6, 195) ** | 31.4943 (6, 195) ** | 25.5486 (6, 195) ** |

| Models | |||

|---|---|---|---|

| Predictors/Statistics | BEP Coeff. (t-Value) | ROA Coeff. (t-Value) | ROE Coeff. (t-Value) |

| BEPt−1 | 0.2694 (9.162) ** | ||

| ROAt−1 | 0.1502 (5.333) ** | ||

| ROEt−1 | 0.1720 (6.301) ** | ||

| SCR | −0.0931 (−7.768) ** | −0.0930 (−7.091) ** | −0.1626 (−5.742) ** |

| ICU | −0.0833 (−1.746) | −0.0087 (−0.196) | −0.0614 (−0.792) |

| LTA | 0.0223 (4.636) ** | 0.0297 (5.804) ** | 0.0583 (5.386) ** |

| LFT | 0.0391 (9.812) ** | 0.0393 (9.611) ** | 0.0710 (8.040) ** |

| WCR | 0.0727 (4.588) ** | 0.0957 (5.871) ** | 0.2175 (6.531) ** |

| LEV | −0.0090 (−2.194) * | −0.0171 (−3.390) ** | −0.0874 (−6.219) ** |

| Firms (periods) | 625 (9) | 625 (9) | 625 (9) |

| Obs. (balanced) | 5625 | 5625 | 5625 |

| Countries | 25 | 25 | 25 |

| Breusch–Pagan time effects test: chi-sq (df) | 18.751 (1) ** | 29.348 (1) ** | 16.952 (1) ** |

| Time effects | Significant 2020 (+), 2021 (+) | Significant 2021 (+) | Significant 2021 (+) |

| Hausman: chi-sq (df) | 2658.5 (7) ** | 3062.3 (7) ** | 2512.1 (7) ** |

| Wooldridge’s test for serial correlation | 34.499 (1, 4998) ** | 31.343 (1, 4998) ** | 35.894 (1, 4998) ** |

| Estimation | FE (firms and years) | FE (firms and years) | FE (firms and years) |

| R-squared | 0.2363 | 0.1716 | 0.2007 |

| F (df) | 60.784 (7, 624) ** | 48.792 (7, 624) ** | 55.643 (7, 624) ** |

| Vars. | SCR | SCRt−1 | SCRt−2 | ICU | ICUt−1 | ICUt−2 |

|---|---|---|---|---|---|---|

| SCR | 1 | 0.9216 ** | 0.8479 ** | 0.1768 ** | 0.1659 ** | 0.1563 ** |

| SCRt−1 | 1 | 0.9202 ** | 0.1818 ** | 0.1728 ** | 0.1629 ** | |

| SCRt−2 | 1 | 0.1812 ** | 0.1815 ** | 0.1729 ** | ||

| ICU | 1 | 0.9405 ** | 0.9017 ** | |||

| ICUt−1 | 1 | 0.9408 ** | ||||

| ICUt−2 | 1 |

| Models | |||

|---|---|---|---|

| Predictors/Statistics | BEP Coeff. (t-Value) | ROA Coeff. (t-Value) | ROE Coeff. (t-Value) |

| BEPt−1 | 0.2634 (8.807) ** | ||

| ROAt−1 | 0.1433 (4.983) ** | ||

| ROEt−1 | 0.1668 (6.045) ** | ||

| SCRt−1 | −0.0724 (−6.361) ** | −0.0782 (−5.932) ** | −0.1349 (−4.773) ** |

| ICUt−1 | −0.0459 (−1.165) | −0.0909 (−2.279) * | −0.2102 (−2.543) * |

| LTA | 0.0205 (4.232) ** | 0.0284 (5.474) ** | 0.0561 (5.118) ** |

| LFT | 0.0371 (9.111) ** | 0.0374 (9.113) ** | 0.0678 (7.822) ** |

| WCR | 0.0826 (5.256) ** | 0.1060 (6.666) ** | 0.2362 (7.230) ** |

| LEV | −0.0085 (−2.039) * | −0.0168 (−3.321) ** | −0.0869 (−6.163) ** |

| Firms (periods) | 625 (9) | 625 (9) | 625 (9) |

| Obs. (balanced) | 5625 | 5625 | 5625 |

| Countries | 25 | 25 | 25 |

| Breusch–Pagan time effects test: chi-sq (df) | 17.62 (1) ** | 28.341 (1) ** | 16.854 (1) ** |

| Time effects | Significant 2020 (+), 2021 (+) | Significant 2021 (+) | Significant 2021 (+) |

| Hausman: chi-sq (df) | 2619.3 (7) ** | 3032.4 (7) ** | 2496.7 (7) ** |

| Wooldridge’s test for serial correlation | 36.541 (1, 4998) ** | 34.171 (1, 4998) ** | 37.579 (1, 4998) ** |

| Estimation | FE (firms and years) | FE (firms and years) | FE (firms and years) |

| R-squared | 0.2271 | 0.1697 | 0.20001 |

| F (df) | 59.9877 (7, 624) ** | 46.8963 (7, 624) ** | 53.6279 (7, 624) ** |

| Models | |||

|---|---|---|---|

| Predictors/Statistics | BEP Coeff. (t-Value) | ROA Coeff. (t-Value) | ROE Coeff. (t-Value) |

| BEPt−1 | 0.2471 (7.660) ** | ||

| ROAt−1 | 0.1272 (4.098) ** | ||

| ROEt−1 | 0.1514 (5.139) ** | ||

| SCRt−2 | −0.0347 (−3.135) ** | −0.0366 (−2.752) ** | −0.0460 (−1.356) |

| ICUt−2 | −0.0383 (−0.857) | −0.0842 (−1.773) | −0.2248 (−2.535) * |

| LTA | 0.0193 (3.709) ** | 0.0282 (5.015) ** | 0.0532 (4.474) ** |

| LFT | 0.0341 (7.707) ** | 0.0341 (8.014) ** | 0.0595 (6.554) ** |

| WCR | 0.0932 (5.039) ** | 0.1167 (6.443) ** | 0.2482 (6.821) ** |

| LEV | −0.0092 (−2.019) * | 0.0169 (−3.034) ** | −0.1009 (−6.665) ** |

| Firms (periods) | 625 (8) | 625 (8) | 625 (8) |

| Obs. (balanced) | 5000 | 5000 | 5000 |

| Countries | 25 | 25 | 25 |

| Breusch–Pagan time effects test: chi-sq (df) | 26.57 (1) ** | 39.801 (1) ** | 22.618 (1) ** |

| Time effects | Significant 2020 (+), 2021 (+) | Significant 2020 (+), 2021 (+) | Significant 2019 (−) 2021 (+) |

| Hausman: chi-sq (df) | 2351.1 (7) ** | 2794.1 (7) ** | 2372.2 (7) ** |

| Wooldridge’s test for serial correlation | 45.115 (1, 4373) ** | 35.232 (1, 4373) ** | 33.718 (1, 4373) ** |

| Estimation | FE (firms and years) | FE (firms and years) | FE (firms and years) |

| R-squared | 0.1979 | 0.1482 | 0.1915 |

| F (df) | 53.328 (7, 624) ** | 43.634 (7, 624) ** | 49.035 (7, 624) ** |

| Models | |||

|---|---|---|---|

| Predictors/Statistics | BEP Coeff. (z-Value) | ROA Coeff. (z-Value) | ROE Coeff. (z-Value) |

| BEPt−1 | 0.4493 (9.535) ** | ||

| ROAt−1 | 0.3403 (6.664) ** | ||

| ROEt−1 | 0.2997 (6.741) ** | ||

| SCR | −0.1018 (−5.718) ** | −0.0797 (−3.902) ** | −0.1501 (−3.703) ** |

| SCRt−1 | −0.0220 (−1.379) | −0.0266 (−1.483) | −0.0734 (−2.168) * |

| SCRt−2 | 0.0049 (0.338) | 0.0081 (0.513) | 0.0494 (1.539) |

| ICU | 0.0106 (0.110) | 0.2417 (2.348) * | 0.4184 (2.555) * |

| ICUt−1 | −0.0353 (−0.629) | −0.1528 (−2.276) * | −0.1718 (−1.329) |

| ICUt−2 | −0.0195 (−0.415) | −0.0244 (−0.435) | −0.0751 (−0.696) |

| LTA | 0.0452 (4.433) ** | 0.0715 (6.949) ** | 0.1430 (8.091) ** |

| LFT | 0.0591 (9.105) ** | 0.0571 (8.886) ** | 0.0969 (8.441) ** |

| WCR | 0.0767 (4.048) ** | 0.1025 (4.927) ** | 0.2131 (4.944) ** |

| LEV | −0.0192 (−3.107) ** | −0.0264 (−3.608) ** | −0.1198 (−6.151) ** |

| Firms (periods) | 625 (10) | 625 (10) | 625 (10) |

| Obs. (balanced) | 6250 | 6250 | 6250 |

| Countries | 25 | 25 | 25 |

| Time effects | Significant | Significant | Significant |

| No of instruments | 37 | 37 | 37 |

| J-Test: ch-sq (df) overidentifying restrictions are valid | 16.29 (19) | 24.73 (19) | 14.99 (19) |

| Estimation | GMM (time effects) | GMM (time effects) | GMM (time effects) |

| F-Statistic (slope coeff.) | 329.86 (11) ** | 308.97 (11) ** | 353.04 (11) ** |

| F-Statistic (time dummies) | 52.88 (7) ** | 52.26 (7) ** | 42.65 (7) ** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dragomir, V.D. The Impact of Intangible Capital on Firm Profitability in the Technology and Healthcare Sectors. Int. J. Financial Stud. 2024, 12, 5. https://doi.org/10.3390/ijfs12010005

Dragomir VD. The Impact of Intangible Capital on Firm Profitability in the Technology and Healthcare Sectors. International Journal of Financial Studies. 2024; 12(1):5. https://doi.org/10.3390/ijfs12010005

Chicago/Turabian StyleDragomir, Voicu D. 2024. "The Impact of Intangible Capital on Firm Profitability in the Technology and Healthcare Sectors" International Journal of Financial Studies 12, no. 1: 5. https://doi.org/10.3390/ijfs12010005

APA StyleDragomir, V. D. (2024). The Impact of Intangible Capital on Firm Profitability in the Technology and Healthcare Sectors. International Journal of Financial Studies, 12(1), 5. https://doi.org/10.3390/ijfs12010005