Reaction of US and Chinese Stock Markets to COVID-19 News

Abstract

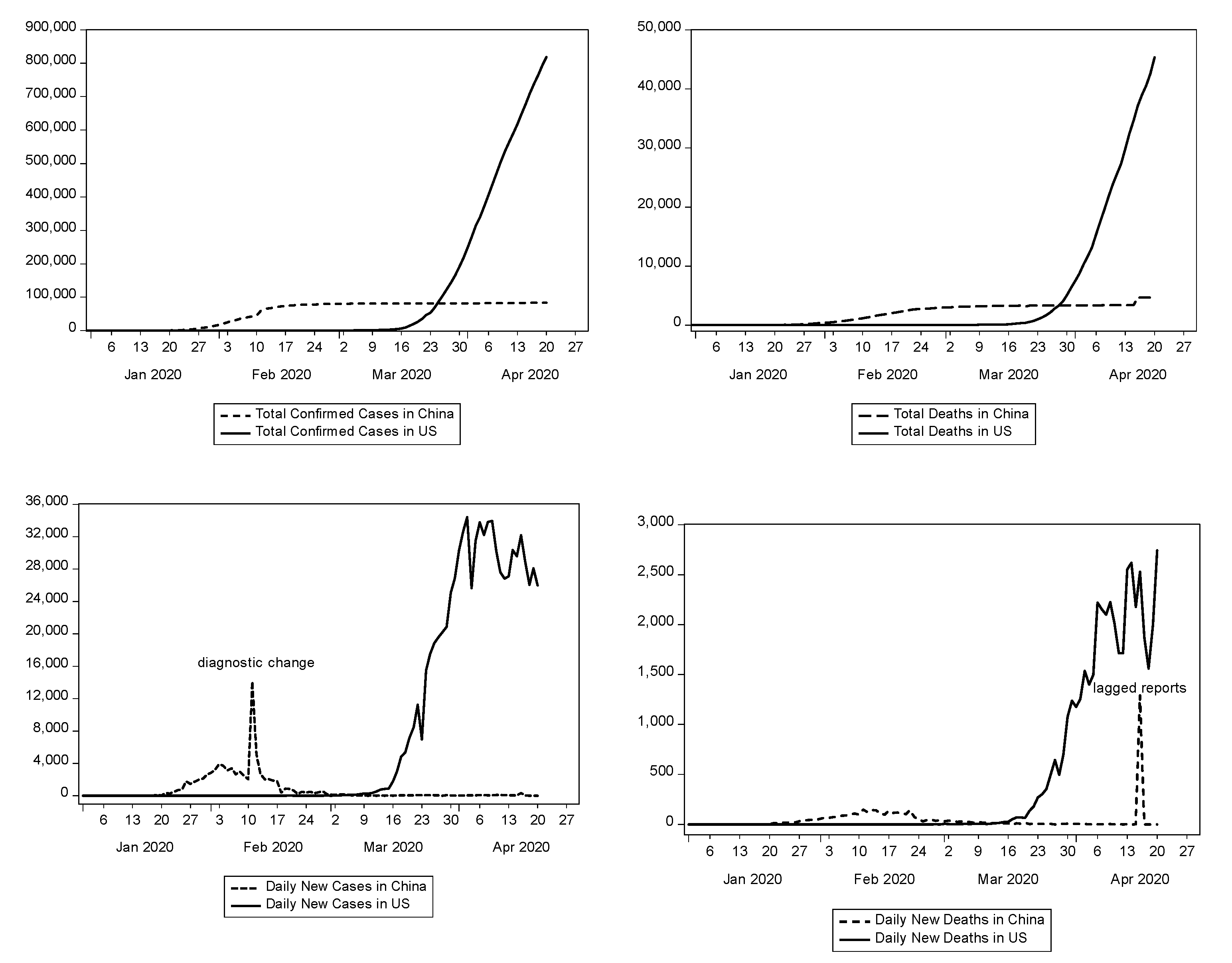

1. Introduction

2. Data

3. Returns on Indices

- = daily observed return of index at the closing of day ,

- = closing price of index on trading day , and

- = closing price of index on the previous trading day.

4. Event Study Specification

5. Cumulative Abnormal Returns on Indices

6. Concluding Remarks

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | As of 26 February 2023, the US has the world’s highest number of total cases (105,251,154) and total deaths (1,145,293), whereas China ranked 41st in terms of total cases (503,352) and 89th in terms of total deaths (5272) (Worldometer 2023). |

| 2 | This lockdown seems to have successfully brought down the daily new cases and deaths to a low level within 3 months. Nevertheless, soon after the lockdown was lifted on 8 April 2020, many new cases were imported from outside (The Star 2020). |

| 3 | At least 80% of Americans were subject to lockdowns in the US by their respective state governors from 12 March 2020, although the federal government was against the practice (The Hindu Bisnessline 2020). See Hodge (2020) for a map of states that imposed full or partial shelter-in-place and stay-at-home orders (with implementation dates) as of 24 March 2020. See also Gershman (2020) for updates until 15 April 2020. |

| 4 | Secon et al. (2020) report a list of countries that were on lockdown due to COVID-19. |

| 5 | In actual fact, the US gross domestic product contracted by 4.6% and 29.9% respectively in the first and second halves of 2020 (Trading Economics 2023). |

| 6 | Besides, they are known to be not quite on par in their fight against the pandemic, let alone other aspects of misunderstandings. |

| 7 | All returns are measured in percentages in this study. |

| 8 | The virus was then reported as unidentified pneumonia with an unknown cause. Chinese officials identified the virus as a new coronavirus on 9 January 2020, which is trading day 6 in this study (World Health Organization 2020). |

| 9 | There were 830 confirmed COVID-19 cases with 25 deaths in China on 23 January 2020 (Worldometer 2020). However, while COVID-19 had already proven threatening and deadly in China, it was just in the initial stages of development, with the first known COVID-19 case confirmed in the US on 20 January 2020 (Holshue et al. 2020). |

| 10 | The events occurred one after another back-to-back; for instance, the second event occurred on Day 16 after the first event. As a result, this study only considers up to Day 10 to reduce the probability of the overlapping effect (Schweitzer 1989). Liew (2020) points out that studying events up to Day 10 is considered long enough, as otherwise it might run into another incoming event. |

| 11 | The CAARt is essentially the same, while negligible differences are observed for returns on each individual index. |

References

- Ahmed, Farhan, Aamir Aijaz Syed, Muhammad Abdul Kamal, Maria de las Nieves López-García, Jose Pedro Ramos-Requena, and Swati Gupta. 2021. Assessing the impact of COVID-19 pandemic on the stock and commodity markets performance and sustainability: A comparative analysis of South Asian countries. Sustainability 13: 5669. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, and Ahmet Sensoy. 2021. Financial contagion during COVID–19 crisis. Finance Research Letters 38: 101604. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, and Zaghum Umar. 2022. COVID-19 media coverage and ESG leader indices. Finance Research Letters 45: 102170. [Google Scholar] [CrossRef]

- Ashraf, Badar Nadeem, and John W. Goodell. 2022. COVID-19 social distancing measures and economic growth: Distinguishing short-and long-term effects. Finance Research Letters 47: 102639. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, Kyle J. Kost, Marco C. Sammon, and Tasaneeya Viratyosin. 2020. The Unprecedented stock market impact of COVID-19. The Review of Asset Pricing Studies 10: 742–58. [Google Scholar] [CrossRef]

- Boubaker, Sabri, John W. Goodell, Satish Kumar, and Riya Sureka. 2023. COVID-19 and finance scholarship: A systematic and bibliometric analysis. International Review of Financial Analysis 85: 102458. [Google Scholar] [CrossRef]

- Brown, Stephen J., and Jerold B. Warner. 1985. Using daily stock returns: The case of event studies. Journal of Financial Economics 14: 3–31. [Google Scholar] [CrossRef]

- Chia, Ricky Chee-Jiun, Venus Khim-Sen Liew, and Racquel Rowland. 2020. Daily new COVID-19 cases, movement control order and the Malaysian stock market returns. International Journal of Business and Society 21: 553–68. [Google Scholar] [CrossRef]

- European Centre for Disease Prevention and Control. 2020. Cluster of Pneumonia Cases Caused by a Novel Coronavirus, Wuhan, China. January 17. Available online: https://www.ecdc.europa.eu/sites/default/files/documents/Risk%20assessment%20-%20pneumonia%20Wuhan%20China%2017%20Jan%202020.pdf (accessed on 1 May 2020).

- Gershman, Jacob. 2020. A guide to state coronavirus lockdowns: Governors in most states have ordered businesses to shut and people to stay home. The Wall Street Journal. April 15. Available online: https://www.wsj.com/articles/a-state-by-state-guide-to-coronavirus-lockdowns-11584749351 (accessed on 1 May 2020).

- Goodell, John W. 2020. COVID-19 and finance: Agendas for future research. Finance Research Letters 35: 101512. [Google Scholar] [CrossRef]

- Hodge, James G., Jr. 2020. COVID-19 emergency legal preparedness primer. The Network. March 24. Available online: https://www.networkforphl.org/wp-content/uploads/2020/03/Western-Region-Primer-COVID-3-24-2020.pdf (accessed on 1 May 2020).

- Holshue, Michelle L., Chas DeBolt, Scott Lindquist, Kathy H. Lofy, John Wiesman, Hollianne Bruce, Christopher Spitters, Keith Ericson, Sara Wilkerson, Ahmet Tural, and et al. 2020. First case of 2019 novel coronavirus in the United States. New England Journal of Medicine 382: 929–36. [Google Scholar] [CrossRef]

- Liew, Venus Khim-Sen. 2020. Abnormal returns on tourism shares in the Chinese Stock Exchanges amid the COVID-19 pandemic. International Journal of Economics and Management 14: 247–62. [Google Scholar] [CrossRef]

- Liu, Zhifeng, Toan Luu Duc Huynh, and Peng-Fei Dai. 2021. The impact of COVID-19 on the stock market crash risk in China. Research in international Business and Finance 57: 101419. [Google Scholar] [CrossRef]

- Mazur, Mieszko, Man Dang, and Miguel Vega. 2021. COVID-19 and the March 2020 stock market crash. Evidence from S&P1500. Finance Research Letters 38: 101690. [Google Scholar]

- Nazir, Mian Sajid, Hassan Younus, Ahmad Kaleem, and Zeshan Anwar. 2014. Impact of political events on stock market returns: Empirical evidence from Pakistan. Journal of Economic and Administrative Sciences 30: 60–78. [Google Scholar] [CrossRef]

- Rahman, Md Lutfur, Abu Amin, and Mohammed Abdullah Al Mamun. 2021. The COVID-19 outbreak and stock market reactions: Evidence from Australia. Finance Research Letters 38: 101832. [Google Scholar] [CrossRef]

- Reuters. 2020. Take Five: Quarter-life crisis. Business News. March 28. Available online: https://uk.reuters.com/article/uk-global-markets-themes-graphic/take-five-quarter-life-crisis-idUKKBN21E2S9 (accessed on 1 May 2020).

- Schweitzer, Robert. 1989. How do stock returns react to special event? Business Review July/August: 17–29. [Google Scholar]

- Secon, Holly, Lauren Frias, and Morgan McFall-Johnsen. 2020. A running list of countries that are on lockdown because of the Coronavirus pandemic. Business Insider. March 20. Available online: https://www.businessinsider.my/countries-on-lockdown-coronavirus-italy-2020-3?r=US&IR=T (accessed on 1 May 2020).

- Smales, Lee A. 2022. Investor attention in cryptocurrency markets. International Review of Financial Analysis 79: 101972. [Google Scholar] [CrossRef]

- Talwar, Manish, Shalini Talwar, Puneet Kaur, Naliniprava Tripathy, and Amandeep Dhir. 2021. Has financial attitude impacted the trading activity of retail investors during the COVID-19 pandemic? Journal of Retailing and Consumer Services 58: 102341. [Google Scholar] [CrossRef]

- Tao, Zhengru. 2012. Event study in measuring the effect of Tohoku earthquake. International Journal of Digital Content Technology and Its Applications 6: 384–92. [Google Scholar]

- The Hindu Bisnessline. 2020. US: Four More States Issue Lockdown Orders, 925 Die due To coronavirus. April 2. Available online: https://www.thehindubusinessline.com/news/world/us-four-more-states-issue-lockdown-orders-925-die-due-to-coronavirus/article31233332.ece# (accessed on 1 May 2020).

- The Star. 2020. China Reports 30 New COVID-19 Cases, 23 Imported. April 22. Available online: https://www.thestar.com.my/news/regional/2020/04/22/china-reports-30-new-covid-19-cases-23-imported (accessed on 1 May 2020).

- Trading Economics. 2023. United States GDP Growth Rate. Available online: https://tradingeconomics.com/united-states/gdp-growth (accessed on 28 February 2023).

- Wen, Fenghua, Xi Tong, and Xiaohang Ren. 2022. Gold or Bitcoin, which is the safe haven during the COVID-19 pandemic? International Review of Financial Analysis 81: 102121. [Google Scholar] [CrossRef]

- World Health Organization. 2020. Coronavirus Disease (COVID-19) Outbreak Situation. Available online: https://www.who.int/emergencies/diseases/novel-coronavirus-2019 (accessed on 1 May 2020).

- Worldometer. 2020. Total Coronavirus Deaths in China. Available online: https://www.worldometers.info/coronavirus/country/china/ (accessed on 1 May 2020).

- Worldometer. 2023. Reported Cases and Deaths by Country or Territory. Available online: https://www.worldometers.info/coronavirus/ (accessed on 28 February 2023).

- Wuhan Center for Novel Coronavirus Disease Control and Prevention. 2020. Wuhan Center for Novel Coronavirus Disease Control and Prevention Notice (No. 1). January 23. Available online: http://www.hubei.gov.cn/zhuanti/2020/gzxxgzbd/zxtb/202001/t20200123_2014402.shtml (accessed on 1 May 2020). (In Chinese)

- Wuhan Municipal Health Commission. 2019. Wuhan Municipal Health Commission Report on the Pneumonia Epidemic Situation. December 31. Available online: http://wjw.wuhan.gov.cn/front/web/showDetail/2019123108989 (accessed on 1 May 2020). (In Chinese)

- Zhang, Dayong, Min Hu, and Qiang Ji. 2020. Financial markets under the global pandemic of COVID-19. Finance Research Letters 36: 101528. [Google Scholar] [CrossRef]

{kind=link}

| Day | ND | NY | SZ | SH | ND | NY | SZ | SH | ND | NY | SZ | SH |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Day 0 = 31 December 2019 | Day 0 = 23 January 2020 | Day 0 = 11 March 2020 | ||||||||||

| 0 | 0.30 | 0.27 | 0.55 | 0.33 | 0.20 | −0.06 | −3.45 | −2.75 | −4.70 | −5.22 | −1.48 | −0.94 |

| 1 | 1.33 | 0.64 | 1.93 | 1.15 | −0.93 | −0.88 | −8.41 | −7.72 | −9.43 | −9.99 | −2.20 | −1.52 |

| 2 | −0.79 | −0.61 | 0.27 | −0.05 | −1.89 | −1.49 | 1.80 | 1.34 | 9.35 | 7.86 | −1.08 | −1.23 |

| 3 | 0.56 | 0.18 | 0.44 | −0.01 | 1.43 | 0.78 | 2.48 | 1.25 | −12.32 | −11.84 | −4.83 | −3.40 |

| 4 | −0.03 | −0.31 | 1.31 | 0.69 | 0.06 | −0.24 | 2.90 | 1.72 | 6.23 | 5.18 | −0.43 | −0.34 |

| 5 | 0.67 | 0.26 | −1.24 | −1.22 | 0.26 | 0.13 | 0.52 | 0.33 | −4.70 | −6.74 | −1.55 | −1.83 |

| 6 | 0.81 | 0.45 | 1.76 | 0.91 | −1.59 | −1.79 | 1.21 | 0.51 | 2.30 | 0.82 | 0.28 | −0.98 |

| 7 | −0.27 | −0.28 | −0.15 | −0.08 | 1.34 | 0.47 | 0.04 | 0.39 | −3.79 | −3.47 | 1.28 | 1.61 |

| 8 | 1.04 | 0.61 | 1.36 | 0.75 | 2.10 | 1.35 | 1.55 | 0.87 | −0.27 | −3.90 | −4.26 | −3.11 |

| 9 | −0.24 | −0.04 | −0.23 | −0.28 | 0.43 | 1.17 | −0.77 | −0.71 | 8.12 | 10.04 | 2.10 | 2.34 |

| 10 | 0.08 | 0.11 | −0.22 | −0.54 | 0.67 | 0.07 | 0.44 | 0.38 | −0.45 | 3.14 | 2.92 | 2.17 |

| Cum | 3.46 | 1.28 | 5.77 | 1.66 | 2.07 | −0.48 | −1.68 | −4.42 | −9.68 | −14.12 | −9.24 | −7.23 |

| Max | 1.33 | 0.64 | 1.93 | 1.15 | 2.10 | 1.35 | 2.90 | 1.72 | 9.35 | 10.04 | 2.92 | 2.34 |

| Mean | 0.31 | 0.12 | 0.52 | 0.15 | 0.19 | −0.04 | −0.15 | −0.40 | −0.88 | −1.28 | −0.84 | −0.66 |

| Min | −0.79 | −0.61 | −1.24 | −1.22 | −1.89 | −1.79 | −8.41 | −7.72 | −12.32 | −11.84 | −4.83 | −3.40 |

| S.D. | 0.63 | 0.40 | 0.98 | 0.70 | 1.25 | 1.01 | 3.24 | 2.71 | 6.99 | 7.22 | 2.43 | 1.96 |

| 0.76 | 0.76 | 0.76 | 0.08 | 0.76 | 0.83 | 0.76 | 0.76 | 0.03 | 0.08 | 0.03 | 0.01 | |

| 0.03 | 0.03 | 0.03 | 0.83 | 0.01 | 0.08 | 0.01 | 0.01 | 0.76 | 0.83 | 0.76 | 0.76 | |

| Index | ND | NY | SZ | SH |

|---|---|---|---|---|

| Day 0 = 31 December 2019 | ||||

| ND | 0.86 ** | 0.38 | 0.35 | |

| NY | [0.00] | 0.38 | 0.35 | |

| SZ | [0.10] | [0.10] | 0.96 ** | |

| SH | [0.14] | [0.14] | [0.00] | |

| Day 0 = 23 January 2020 | ||||

| ND | 0.82 ** | 0.06 | 0.13 | |

| NY | [0.00] | 0.02 | 0.02 | |

| SZ | [0.82] | [0.94] | 0.86 ** | |

| SH | [0.59] | [0.94] | [0.00] | |

| Day 0 = 11 March 2020 | ||||

| ND | 0.84 ** | 0.40 | 0.37 | |

| NY | [0.00] | 0.56 * | 0.53 * | |

| SZ | [0.09] | [0.02] | 0.82 ** | |

| SH | [0.12] | [0.02] | [0.00] | |

| United States | China | |||||||||||

| Day 0 = 31 December 2019 | Day 0 = 31 December 2019 | |||||||||||

| Window | ND | NY | CAAR | SZ | SH | CAAR | ||||||

| [0, 1] | 0.59 (0.66) | 0.19 (0.40) | 0.39 (0.61) | 2.39 (1.20) | 1.45 (1.29) | 1.51 (1.01) | ||||||

| [0, 2] | 0.94 (0.73) | 0.56 (0.83) | 0.75 (0.82) | 2.62 (0.93) | 1.38 (0.87) | 1.59 (0.76) | ||||||

| [0, 3] | 1.09 (0.69) | 0.59 (0.72) | 0.84 (0.75) | 3.02 (0.87) | 1.36 (0.70) | 1.78 (0.69) | ||||||

| [0, 4] | 1.09 (0.60) | 0.51 (0.53) | 0.80 (0.62) | 4.29 (1.07) | 2.03 (0.91) | 2.75 (0.92) | ||||||

| [0, 5] | 1.79 (0.88) | 0.79 (0.74) | 1.29 (0.90) | 3.00 (0.67) | 0.79 (0.32) | 1.49 (0.45) | ||||||

| [0, 6] | 1.53 (0.69) | 0.77 (0.66) | 1.15 (0.73) | 4.71 (0.96) | 1.69 (0.61) | 2.79 (0.77) | ||||||

| [0, 7] | 0.78 (0.32) | 0.24 (0.19) | 0.51 (0.30) | 4.52 (0.85) | 1.59 (0.53) | 2.64 (0.67) | ||||||

| [0, 8] | 0.99 (0.39) | 0.46 (0.34) | 0.73 (0.40) | 5.84 (1.03) | 2.32 (0.73) | 3.67 (0.87) | ||||||

| [0, 9] | 2.25 (0.83) | 1.05 (0.74) | 1.65 (0.85) | 5.56 (0.93) | 2.03 (0.60) | 3.38 (0.76) | ||||||

| [0, 10] | 1.38 (0.48) | 0.40 (0.26) | 0.89 (0.44) | 5.30 (0.84) | 1.47 (0.41) | 2.97 (0.63) | ||||||

| United States | China | |||||||||||

| Day 0 = 23 January 2020 | Day 0 = 23 January 2020 | |||||||||||

| Window | ND | NY | CAAR | SZ | SH | CAAR | ||||||

| [0, 1] | 0.94 (1.07) | 0.55 (1.21) | −0.22 (−0.35) | −3.88 (−4.90) | ** | −7.71 (−8.00) | ** | −8.08 (−4.46) | ** | |||

| [0, 2] | −0.34 (−0.39) | −0.09 (−0.20) | −0.19 (−0.22) | −6.66 (−2.73) | ** | −6.36 (−4.67) | ** | −6.51 (−2.94) | ** | |||

| [0, 3] | −0.02 (−0.02) | 0.06 (0.13) | 0.58 (0.54) | −4.21 (−1.41) | −5.10 (−3.06) | ** | −4.66 (−1.82) | * | ||||

| [0, 4] | 0.97 (1.10) | 0.58 (1.27) | 0.82 (0.66) | −1.34 (−0.39) | −3.37 (−1.75) | * | −2.36 (−0.82) | |||||

| [0, 5] | 0.24 (0.28) | 0.24 (0.53) | 0.39 (0.28) | −0.85 (−0.22) | −3.03 (−1.40) | −1.94 (−0.62) | ||||||

| [0, 6] | −0.29 (−0.33) | −0.57 (−1.25) | 0.38 (0.25) | 0.34 (0.08) | −2.51 (−1.06) | −1.09 (−0.32) | ||||||

| [0, 7] | 0.04 (0.05) | −0.05 (−0.11) | 0.38 (0.23) | 0.35 (0.08) | −2.11 (−0.83) | −0.88 (−0.24) | ||||||

| [0, 8] | 0.10 (0.12) | −0.11 (−0.25) | −0.60 (−0.34) | 1.88 (0.39) | −1.23 (−0.45) | 0.33 (0.09) | ||||||

| [0, 9] | −1.03 (−1.17) | −0.93 (−2.04) | * | −2.36 (−1.27) | 1.09 (0.21) | −1.93 (−0.67) | −0.42 (−0.10) | |||||

| [0, 10] | −1.98 (−2.26) | * | −1.55 (−3.40) | ** | −1.33 (−0.68) | 1.50 (0.28) | −1.54 (−0.50) | −0.02 (0.00) | ||||

| United States | China | |||||||||||

| Day 0 = 11 March 2020 | Day 0 = 11 March 2020 | |||||||||||

| Window | ND | NY | CAAR | SZ | SH | CAAR | ||||||

| [0, 1] | −4.75 (−5.50) | ** | −5.20 (−11.18) | ** | −9.73 (−6.65) | ** | −3.88 (−1.85) | * | −2.49 (−2.01) | * | −1.91 (−1.19) | |

| [0, 2] | −9.49 (−10.98) | ** | −9.97 (−21.44) | ** | −1.14 (−0.55) | −5.05 (−1.70) | * | −3.74 (−2.14) | * | −3.13 (−1.38) | ||

| [0, 3] | 9.29 (10.76) | ** | 7.89 (16.97) | ** | −13.23 (−5.22) | ** | −9.99 (−2.74) | ** | −7.16 (−3.34) | ** | −7.30 (−2.62) | ** |

| [0, 4] | −12.37 (−14.33) | ** | −11.81 (−25.41) | ** | −7.54 (−2.58) | * | −10.51 (−2.50) | ** | −7.52 (−3.04) | ** | −7.75 (−2.41) | * |

| [0, 5] | 6.18 (7.15) | ** | 5.21 (11.20) | ** | −13.28 (−4.06) | ** | −12.17 (−2.59) | ** | −9.36 (−3.38) | ** | −9.50 (−2.64) | ** |

| [0, 6] | −4.76 (−5.51) | ** | −6.72 (−14.46) | ** | −11.73 (−3.27) | ** | −11.99 (−2.33) | ** | −10.36 (−3.41) | ** | −9.90 (−2.51) | * |

| [0, 7] | 2.25 (2.60) | ** | 0.84 (1.81) | * | −15.38 (−3.97) | ** | −10.81 (−1.94) | * | −8.76 (−2.68) | ** | −8.52 (−2.00) | * |

| [0, 8] | −3.84 (−4.45) | ** | −3.44 (−7.41) | ** | −17.48 (−4.22) | ** | −15.17 (−2.55) | ** | −11.89 (−3.40) | ** | −12.26 (−2.70) | ** |

| [0, 9] | −0.33 (−0.38 | −3.87 (−8.33) | ** | −8.41 (−1.92) | * | −13.16 (−2.09) | * | −9.57 (−2.58) | ** | −10.10 (−2.09) | * | |

| [0, 10] | 8.07 (9.34) | ** | 10.06 (21.64) | ** | −7.09 (−1.53) | −10.34 (−1.56) | −7.41 (−1.89) | * | −7.61 (−1.50) | |||

| United States | China | |||||||||||

| Day 0 = 31 December 2019 | Day 0 = 31 December 2019 | |||||||||||

| Window | ND | NY | CAAR | SZ | SH | CAAR | ||||||

| [0, 1] | 0.61 (0.67) | 0.17 (0.36) | 0.39 (0.61) | 2.42 (1.21) | 1.42 (1.27) | 1.51 (1.01) | ||||||

| [0, 2] | 0.97 (0.76) | 0.53 (0.78) | 0.75 (0.82) | 2.66 (0.94) | 1.35 (0.85) | 1.59 (0.76) | ||||||

| [0, 3] | 1.14 (0.73) | 0.54 (0.65) | 0.84 (0.75) | 3.07 (0.89) | 1.30 (0.67) | 1.78 (0.69) | ||||||

| [0, 4] | 1.16 (0.64) | 0.44 (0.46) | 0.80 (0.62) | 4.35 (1.09) | 1.97 (0.88) | 2.75 (0.92) | ||||||

| [0, 5] | 1.87 (0.92) | 0.70 (0.66) | 1.29 (0.90) | 3.08 (0.69) | 0.72 (0.29) | 1.49 (0.45) | ||||||

| [0, 6] | 1.63 (0.74) | 0.67 (0.57) | 1.15 (0.73) | 4.80 (0.98) | 1.60 (0.58) | 2.79 (0.77) | ||||||

| [0, 7] | 0.90 (0.37) | 0.12 (0.09) | 0.51 (0.30) | 4.62 (0.87) | 1.49 (0.50) | 2.64 (0.67) | ||||||

| [0, 8] | 1.13 (0.44) | 0.32 (0.24) | 0.73 (0.40) | 5.95 (1.05) | 2.21 (0.70) | 3.67 (0.87) | ||||||

| [0, 9] | 2.40 (0.88) | 0.90 (0.63) | 1.65 (0.85) | 5.69 (0.95) | 1.90 (0.56) | 3.38 (0.76) | ||||||

| [0, 10] | 1.55 (0.54) | 0.23 (0.15) | 0.89 (0.44) | 5.44 (0.86) | 1.33 (0.37) | 2.97 (0.63) | ||||||

| United States | China | |||||||||||

| Day 0 = 23 January 2020 | Day 0 = 23 January 2020 | |||||||||||

| Window | ND | NY | CAAR | SZ | SH | CAAR | ||||||

| [0, 1] | 0.96 (1.10) | 0.53 (1.17) | −0.22 (−0.35) | −3.79 (−4.89) | ** | −7.73 (−8.02) | ** | −8.08 (−4.46) | ** | |||

| [0, 2] | −0.32 (−0.36) | −0.11 (−0.25) | −0.19 (−0.22) | −6.62 (−2.72) | ** | −6.40 (−4.70) | ** | −6.51 (−2.94) | ** | |||

| [0, 3] | 0.00 (0.01) | 0.04 (0.09) | 0.58 (0.54) | −4.15 (−1.39) | −5.16 (−3.09) | ** | −4.66 (−1.82) | * | ||||

| [0, 4] | 0.99 (1.13) | 0.56 (1.22) | 0.82 (0.66) | −1.26 (−0.37) | −3.45 (−1.79) | * | −2.36 (−0.82) | |||||

| [0, 5] | 0.27 (0.30) | 0.22 (0.48) | 0.39 (0.28) | −0.75 (−0.20) | −3.13 (−1.45) | −1.94 (−0.62) | ||||||

| [0, 6] | −0.27 (−0.31) | −0.59 (−1.30) | 0.38 (0.25) | 0.46 (0.11) | −2.63 (−1.11) | −1.09 (−0.32) | ||||||

| [0, 7] | 0.06 (0.07) | −0.07 (−0.16) | 0.38 (0.23) | 0.49 (0.11) | −2.25 (−0.88) | −0.88 (−0.24) | ||||||

| [0, 8] | 0.12 (0.14) | −0.13 (−0.29) | −0.60 (−0.34) | 2.04 (0.42) | −1.38 (−0.51) | 0.33 (0.09) | ||||||

| [0, 9] | −1.01 (−1.15) | −0.95 (−2.09) | * | −2.36 (−1.27) | 1.26 (0.24) | −2.10 (−0.73) | −0.42 (−0.10) | |||||

| [0, 10] | −1.96 (−2.24) | * | −1.57 (−3.45) | ** | −1.33 (−0.68) | 1.70 (0.31) | −1.73 (−0.57) | −0.02 (0.00) | ||||

| United States | China | |||||||||||

| Day 0 = 11 March 2020 | Day 0 = 11 March 2020 | |||||||||||

| Window | ND | NY | CAAR | SZ | SH | CAAR | ||||||

| [0, 1] | −4.72 (−5.46) | ** | −5.24 (−11.27) | ** | −9.73 (−6.65) | ** | −3.79 (−1.81) | * | −2.58 (−2.08) | * | −1.91 (−1.19) | |

| [0, 2] | −9.45 (−10.94) | ** | −10.00 (−21.52) | ** | −1.14 (−0.55) | −4.93 (−1.66) | * | −3.87 (−2.21) | * | −3.13 (−1.38) | ||

| [0, 3] | 9.33 (10.80) | ** | 7.85 (16.88) | ** | −13.23 (−5.22) | ** | −9.82 (−2.70) | ** | −7.33 (−3.42) | ** | −7.30 (−2.62) | ** |

| [0, 4] | −12.34 (−14.28) | ** | −11.85 (−25.49) | ** | −7.54 (−2.58) | * | −10.30 (−2.45) | ** | −7.73 (−3.12) | ** | −7.75 (−2.41) | * |

| [0, 5] | 6.22 (7.20) | ** | 5.17 (11.12) | ** | −13.28 (−4.06) | ** | −11.91 (−2.54) | ** | −9.62 (−3.47) | ** | −9.50 (−2.64) | ** |

| [0, 6] | −4.72 (−5.46) | ** | −6.76 (−14.54) | ** | −11.73 (−3.27) | ** | −11.69 (−2.27) | * | −10.65 (−3.51) | ** | −9.90 (−2.51) | * |

| [0, 7] | 2.28 (2.64) | ** | 0.80 (1.73) | * | −15.38 (−3.97) | ** | −10.47 (−1.88) | * | −9.10 (−2.78) | ** | −8.52 (−2.00) | * |

| [0, 8] | −3.81 (−4.41) | ** | −3.48 (−7.49) | ** | −17.48 (−4.22) | ** | −14.79 (−2.49) | ** | −12.27 (−3.50) | ** | −12.26 (−2.70) | ** |

| [0, 9] | −0.29 (−0.33) | −3.91 (−8.41) | ** | −8.41 (−1.92) | * | −12.74 (−2.02) | * | −9.99 (−2.69) | ** | −10.10 (−2.09) | * | |

| [0, 10] | 8.11 (9.38) | ** | 10.02 (21.56) | ** | −7.09 (−1.53) | −9.88 (−1.49) | −7.87 (−2.01) | * | −7.61 (−1.50) | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, H.-A.; Liew, V.K.-S.; Ghazali, M.F.; Riaz, S. Reaction of US and Chinese Stock Markets to COVID-19 News. Int. J. Financial Stud. 2023, 11, 59. https://doi.org/10.3390/ijfs11020059

Lee H-A, Liew VK-S, Ghazali MF, Riaz S. Reaction of US and Chinese Stock Markets to COVID-19 News. International Journal of Financial Studies. 2023; 11(2):59. https://doi.org/10.3390/ijfs11020059

Chicago/Turabian StyleLee, Hock-Ann, Venus Khim-Sen Liew, Mohd Fahmi Ghazali, and Samina Riaz. 2023. "Reaction of US and Chinese Stock Markets to COVID-19 News" International Journal of Financial Studies 11, no. 2: 59. https://doi.org/10.3390/ijfs11020059

APA StyleLee, H.-A., Liew, V. K.-S., Ghazali, M. F., & Riaz, S. (2023). Reaction of US and Chinese Stock Markets to COVID-19 News. International Journal of Financial Studies, 11(2), 59. https://doi.org/10.3390/ijfs11020059