Overreaction in a Frontier Market: Evidence from the Ho Chi Minh Stock Exchange

Abstract

1. Introduction

2. Literature Review

3. Data and Methodology

3.1. Data

3.2. Research Methodology

4. Empirical Results

4.1. Descriptive Statistics of the Portfolios for the Tracking Periods

4.2. Results of Overreaction Tests

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Antoniou, Antonios, Emilios C. Galariotis, and Spyros I. Spyrou. 2005. Contrarian profits and the overreaction hypothesis: The case of the Athens stock exchange. European Financial Management 11: 71–98. [Google Scholar] [CrossRef]

- Baytas, Ahmet, and Nusret Cakici. 1999. Do market overreaction: International evidence. Journal of Banking and Finance 23: 1121–44. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Hisham Farag, and Duc Khuong Nguyen. 2015. Short-term overreaction to specific events: Evidence from an emerging market. Research in International Business and Finance 35: 153–65. [Google Scholar] [CrossRef]

- Bowman, Robert G., and David Iverson. 1998. Short-run overreaction in the New Zealand stock market. Pacific-Basin Finance Journal 6: 475–91. [Google Scholar] [CrossRef]

- Brown, Keith C., and W. Van Harlow. 1988. Market overreaction: Magnitude and intensity. Journal of Portfolio Management 14: 6–13. [Google Scholar] [CrossRef]

- Chang, Rosita P., Dennis W. McLeavey, and S. Ghon Rhee. 1995. Short-term abnormal returns of the contrarian strategy in the Japanese stock market. Journal of Business Finance & Accounting 22: 1035–48. [Google Scholar] [CrossRef]

- Chopra, Navin, Josef Lakonishok, and Jay R. Ritter. 1992. Measuring abnormal performance: Do stocks overreact? Journal of Financial Economics 31: 235–68. [Google Scholar] [CrossRef]

- Clare, Andrew, and Stephen Thomas. 1995. The overreaction hypothesis and the UK stock market. Journal of Business Finance & Accounting 22: 961–73. [Google Scholar] [CrossRef]

- Da Costa, Newton C. A. 1994. Overreaction in the Brazilian stock market. Journal of Banking and Finance 18: 633–42. [Google Scholar] [CrossRef]

- Daniel, Kent, David Hirshleifer, and Avanidhar Subrahmanyam. 1998. Investor psychology and security market under-and overreactions. The Journal of Finance 53: 1839–85. [Google Scholar] [CrossRef]

- Davidson, Wallace N., III, and Dipa Dutia. 1989. A note on the behavior of security returns: A test of stock market overreaction and efficiency. The Journal of Financial Research 12: 245–52. [Google Scholar] [CrossRef]

- De Bondt, Werner F. M., and Richard Thaler. 1985. Does the stock market overreact? Journal of Finance 40: 793–805. [Google Scholar] [CrossRef]

- De Bondt, Werner F. M., and Richard Thaler. 1987. Further evidence on investor overreaction and stock market seasonality. Journal of Finance 42: 557–81. [Google Scholar] [CrossRef]

- Ho, Kung-Cheng, Lu Yang, and Sijia Luo. 2022. Information disclosure ratings and continuing overreaction: Evidence from the Chinese capital market. Journal of Business Research 140: 638–56. [Google Scholar] [CrossRef]

- Howe, John S. 1986. Evidence on Stock Market Overreaction. Financial Analysis Journal 42: 74–77. [Google Scholar] [CrossRef]

- Jegadeesh, Narasimhan, and Sheridan Titman. 1993. Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance 48: 65–91. [Google Scholar] [CrossRef]

- Jegadeesh, Narasimhan, and Sheridan Titman. 1995. Overreaction, delayed reaction, and contrarian profits. Review of Financial Studies 8: 973–93. [Google Scholar] [CrossRef]

- Lerskullawat, Polwat, and Teerapan Ungphakorn. 2019. Does overreaction still exist in Thailand? Kasetsart Journal of Social Sciences 40: 689–94. [Google Scholar] [CrossRef]

- Lo, Andrew W., and A. Craig MacKinlay. 1990. When are contrarian profits due to stock market overreaction? Review of Financial Studies 3: 175–205. [Google Scholar] [CrossRef]

- Lobe, Sebastian, and Johannes Rieks. 2011. Short-term market overreaction on the Frankfurt stock exchange. The Quarterly Review of Economics and Finance 51: 113–23. [Google Scholar] [CrossRef]

- Ma, Yulong, Alex P. Tang, and Tanweer Hasan. 2005. The stock price overreaction effect: Evidence on Nasdaq stocks. Quarterly Journal of Business & Economics 44: 113–27. [Google Scholar]

- Musnadi, Said, Faisal, and M. Sabhri Abd. Majid. 2018. Overreaction and underreaction anomalies in the Indonesian stock market: A sectoral analysis. International Journal of Ethics and Systems 34: 442–57. [Google Scholar] [CrossRef]

- Nguyen, Anh Thi Kim, and Loc Dong Truong. 2020. The impact of index future introduction on spot market returns and trading volume: Evidence from Ho Chi Minh Stock Exchange. Journal of Asian Finance, Economics and Business 7: 51–59. [Google Scholar] [CrossRef]

- Nguyen, Thi Kim Anh, Dong Loc Truong, and H. Swint Friday. 2022. Expiration-day effects of index futures in a frontier market: The case of Ho Chi Minh Stock Exchange. International Journal of Financial Studies 10: 3. [Google Scholar] [CrossRef]

- Otchere, Isaac, and Jonathan Chan. 2003. Short-term overreaction in the Hong Kong stock market: Can a contrarian trading strategy beat the market? Journal of Behavioral Finance 4: 157–71. [Google Scholar] [CrossRef]

- Piccoli, Pedro, Mo Chaudhury, Alceu Souza, and Wesley Vieira da Silva. 2017. Stock overreaction to extreme market events. The North American Journal of Economics and Finance 41: 97–111. [Google Scholar] [CrossRef]

- Tripathi, Vanita, and Shalini Aggarwal. 2009. The overreaction effect in the Indian stock market. Asian Journal of Business and Accounting 2: 93–114. [Google Scholar]

- Truong, Loc Dong, Anh Thi Kim Nguyen, and Dut Van Vo. 2021. Index future trading and spot market volatility in frontier markets: Evidence from Ho Chi Minh Stock Exchange. Asia-Pacific Financial Markets 28: 353–66. [Google Scholar] [CrossRef]

- Truong, Loc Dong, Thai Xuan Le, and H. Swint Friday. 2022. The influence of information transparency and disclosure on the value of listed companies: Evidence from Vietnam. Journal of Risk and Financial Management 15: 345. [Google Scholar] [CrossRef]

- Wang, J., B. M. Burton, and D. M. Power. 2004. Analysis of the overreaction effect in the Chinese stock market. Applied Economics Letters 11: 437–42. [Google Scholar] [CrossRef]

- Wu, Yangru. 2011. Momentum trading, mean reversal and overreaction in Chinese stock market. Review of Quantitative Finance and Accounting 37: 301–23. [Google Scholar] [CrossRef]

- Zarowin, Paul. 1990. Size, seasonality, and stock market overreaction. Journal of Financial and Quantitative Analysis 25: 113–25. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

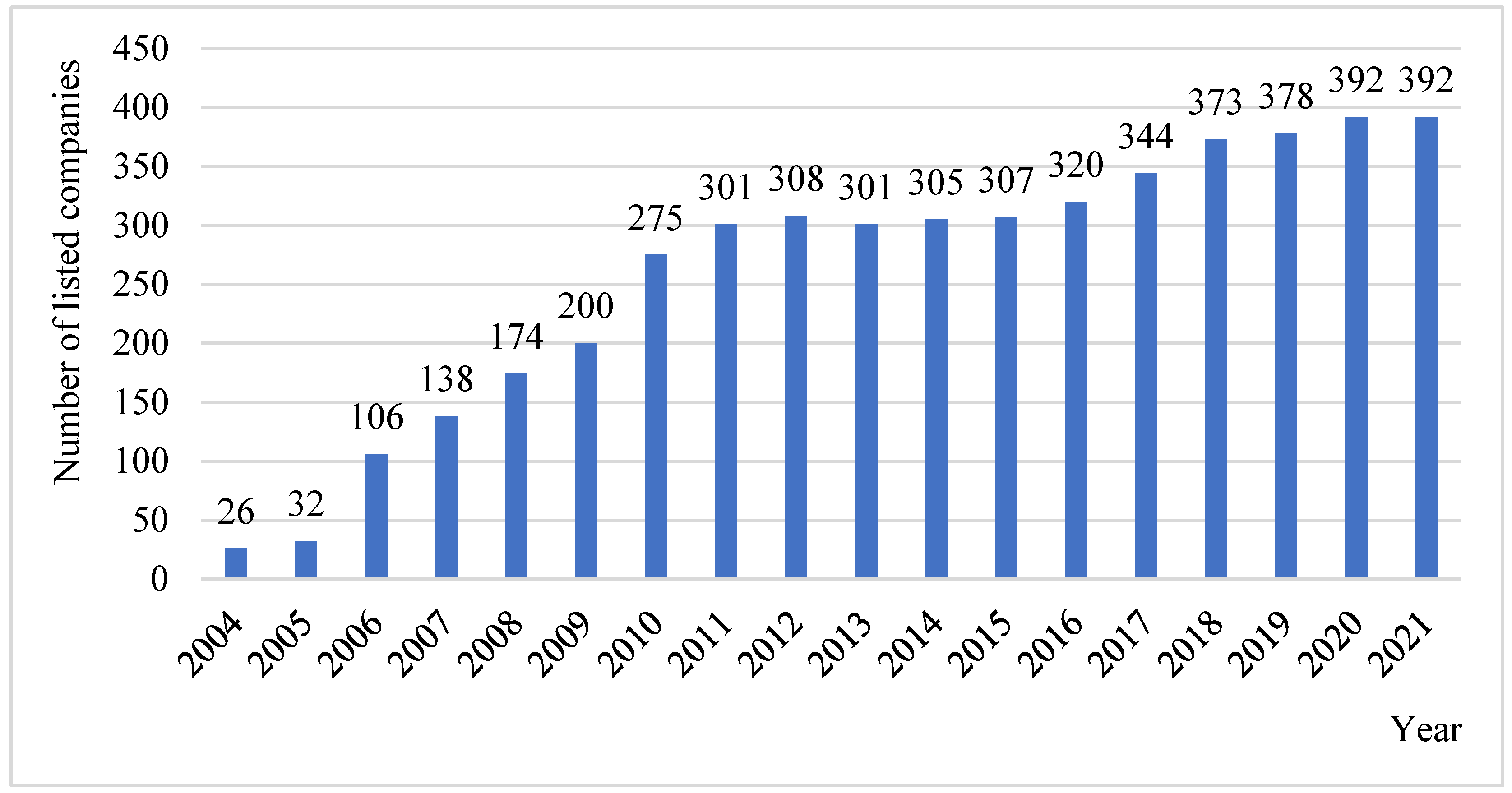

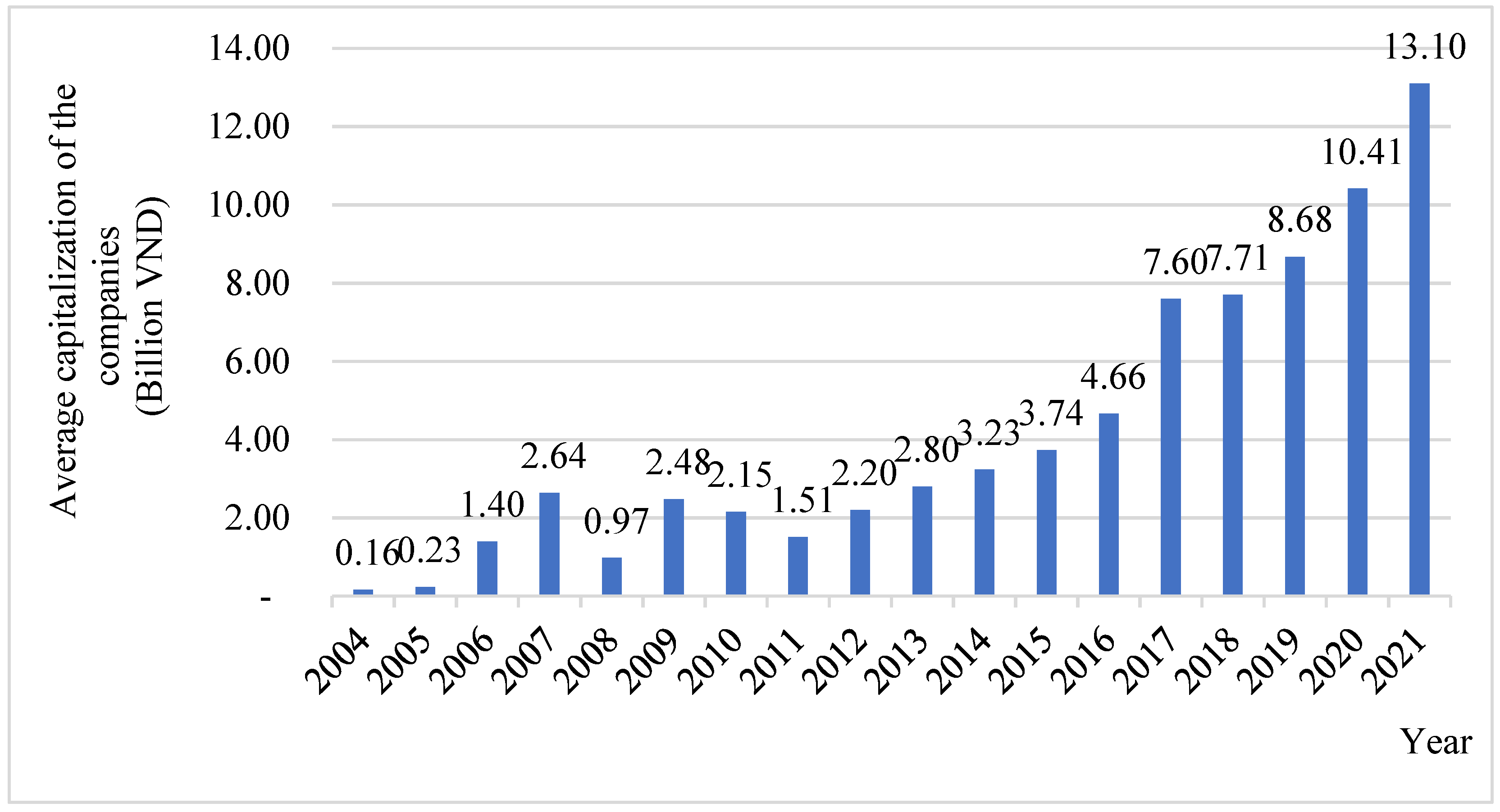

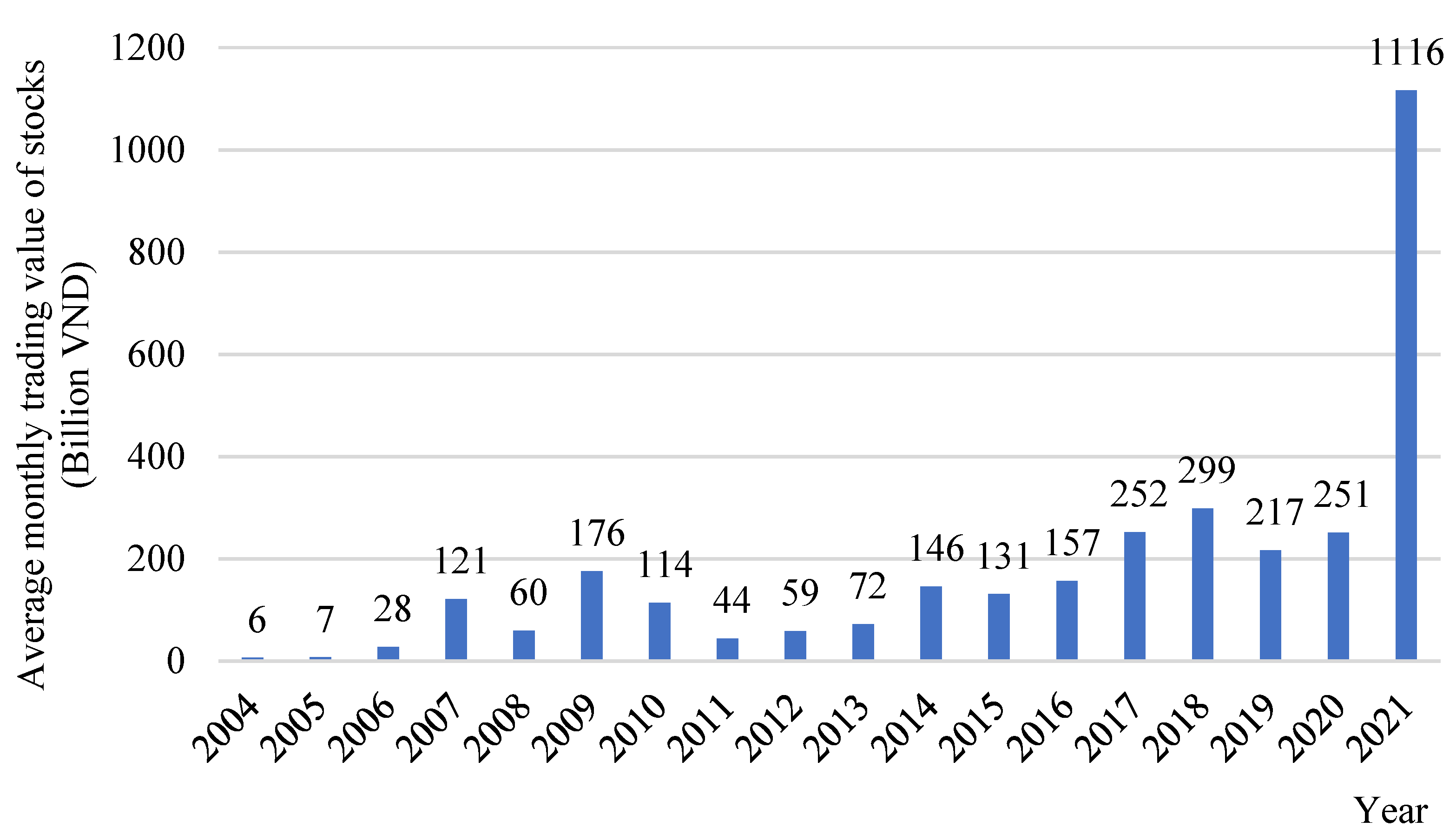

| Year | Number of Listed Companies | Average Capitalization of the Companies (VND Billion) | Average Monthly Trading Value of Stocks (VND Billion) |

|---|---|---|---|

| 2004 | 26 | 163.0 | 6.3 |

| 2005 | 32 | 230.9 | 7.2 |

| 2006 | 106 | 1395.9 | 27.9 |

| 2007 | 138 | 2640.8 | 121.2 |

| 2008 | 174 | 973.3 | 59.7 |

| 2009 | 200 | 2475.5 | 176.0 |

| 2010 | 275 | 2150.3 | 114.1 |

| 2011 | 301 | 1507.6 | 44.1 |

| 2012 | 308 | 2202.6 | 58.7 |

| 2013 | 301 | 2797.7 | 72.3 |

| 2014 | 305 | 3230.4 | 145.6 |

| 2015 | 307 | 3735.9 | 130.8 |

| 2016 | 320 | 4661.8 | 156.8 |

| 2017 | 344 | 7599.3 | 252.2 |

| 2018 | 373 | 7709.2 | 298.8 |

| 2019 | 378 | 8676.2 | 216.5 |

| 2020 | 392 | 10,410.1 | 251.4 |

| 2021 | 392 | 13,101.7 | 1116.3 |

| Tracking Periods | Observations | Minimum | Mean | Maximum | Range | Standard Deviation |

|---|---|---|---|---|---|---|

| F (T0) | 30 | 0.0108 | 0.1017 | 0.2231 | 0.2123 | 0.0550 |

| T + 1 | 30 | −0.0657 | −0.0040 | 0.0717 | 0.1374 | 0.0331 |

| T + 2 | 30 | −0.0796 | −0.0071 | 0.0811 | 0.1607 | 0.0334 |

| T + 3 | 30 | −0.1201 | −0.0111 | 0.0301 | 0.1502 | 0.0309 |

| T + 4 | 30 | −0.0559 | −0.0097 | 0.0697 | 0.1256 | 0.0276 |

| T + 5 | 30 | −0.0551 | −0.0112 | 0.0355 | 0.0906 | 0.0257 |

| T + 6 | 30 | −0.0878 | −0.0085 | 0.0454 | 0.1332 | 0.0314 |

| Tracking Periods | Observations | Minimum | Mean | Maximum | Range | Standard Deviation |

|---|---|---|---|---|---|---|

| F (T0) | 30 | −0.1931 | −0.1178 | −0.0218 | 0.1713 | 0.0467 |

| T + 1 | 30 | −0.0590 | −0.0134 | 0.0659 | 0.1249 | 0.0240 |

| T + 2 | 30 | −0.0383 | 0.0109 | 0.0839 | 0.1222 | 0.0341 |

| T + 3 | 30 | −0.0721 | 0.0106 | 0.0753 | 0.1474 | 0.0379 |

| T + 4 | 30 | −0.0979 | −0.0073 | 0.0780 | 0.1759 | 0.0339 |

| T + 5 | 30 | −0.0961 | −0.0087 | 0.0283 | 0.1244 | 0.0241 |

| T + 6 | 30 | −0.0980 | −0.0044 | 0.0735 | 0.1715 | 0.0356 |

| Month | Observations | Winner | Loser | Loser-Winner (ARL − ARW) | |

|---|---|---|---|---|---|

| ARW | ARL | ARD | t-Statistics | ||

| F | 30 | 0.1017 | −0.1178 | −0.2195 | −16.66 *** |

| T + 1 | 30 | −0.0040 | −0.0134 | −0.0094 | −1.25 |

| T + 2 | 30 | −0.0071 | 0.0109 | 0.0180 | 2.06 ** |

| T + 3 | 30 | −0.0111 | 0.0106 | 0.0217 | 2.43 ** |

| T + 4 | 30 | −0.0097 | −0.0073 | 0.0024 | 0.30 |

| T + 5 | 30 | −0.0112 | −0.0087 | 0.0025 | 0.39 |

| T + 6 | 30 | −0.0085 | −0.0044 | 0.0041 | 0.47 |

| Month | Observations | Winner | Loser | Loser-Winner (ARL − ARW) | |

|---|---|---|---|---|---|

| ARW | ARL | ARD | t-Statistics | ||

| F | 30 | 0.1017 | −0.1178 | −0.2195 | −16.66 *** |

| T + 1 | 30 | −0.0040 | −0.0134 | −0.0094 | −1.25 |

| T + 2 | 30 | −0.0056 | −0.0012 | 0.0044 | 0.96 |

| T + 3 | 30 | −0.0074 | 0.0027 | 0.0101 | 2.41 ** |

| T + 4 | 30 | −0.0080 | 0.0002 | 0.0082 | 2.32 ** |

| T + 5 | 30 | −0.0086 | −0.0016 | 0.0070 | 2.09 ** |

| T + 6 | 30 | −0.0086 | −0.0021 | 0.0065 | 2.00 * |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Truong, L.D.; Cao, G.N.; Friday, H.S.; Doan, N.T. Overreaction in a Frontier Market: Evidence from the Ho Chi Minh Stock Exchange. Int. J. Financial Stud. 2023, 11, 58. https://doi.org/10.3390/ijfs11020058

Truong LD, Cao GN, Friday HS, Doan NT. Overreaction in a Frontier Market: Evidence from the Ho Chi Minh Stock Exchange. International Journal of Financial Studies. 2023; 11(2):58. https://doi.org/10.3390/ijfs11020058

Chicago/Turabian StyleTruong, Loc Dong, Giang Ngan Cao, H. Swint Friday, and Nhien Tuyet Doan. 2023. "Overreaction in a Frontier Market: Evidence from the Ho Chi Minh Stock Exchange" International Journal of Financial Studies 11, no. 2: 58. https://doi.org/10.3390/ijfs11020058

APA StyleTruong, L. D., Cao, G. N., Friday, H. S., & Doan, N. T. (2023). Overreaction in a Frontier Market: Evidence from the Ho Chi Minh Stock Exchange. International Journal of Financial Studies, 11(2), 58. https://doi.org/10.3390/ijfs11020058