Abstract

Despite the spread and progress in the literature related to the disclosure of corporate social responsibility (CSR) performance around the world as one of the most essential tools for achieving sustainable development in society, its value relevance is still uncertain. Using a survey approach involving investors dealing in stocks of 60 enterprises listed on the Egyptian Stock Exchange (EGX) and included in the environmental, social, and governance index (S&P/EGX ESG index) and the equal-weight index (EGX100 EWI index), we empirically examine the importance of CSR financial performance disclosure by examining the extent to which it can influence investors’ choices. In addition, we assess whether company reputation acquired through online social media (OSM) influences the extent to which CSR performance disclosure influences such judgments. To examine these matters, we conduct two tests: the first examines the influence of disclosure of company environmental activities on investors’ decisions and the other examines the influence of disclosure of company social activities on investor decisions. Turning to our key results, we find that investment decision makers in both experiments tend to invest only in companies that have higher CSR performance scores. In the context of OSM, we provide and discuss empirical evidence that investment decision makers are more responsive to investing in companies included in the S&P/EGX ESG index, which have a positive e-reputation for CSR performance, than companies included in the EGX100 EWI index, which do not have such a reputation, which confirms that e-reputation, as one of the most important outputs of OSM, has a marginal impact on investment decisions and moderates the relation between disclosure of high CSR scores and investors’ decisions. Therefore, this paper presents a modern starting point for CSR experts and academics, particularly in the emerging markets. In general, our paper expands the CSR-related investment literature. In line with the affect-as-information theory, our paper also expands the OSM literature by indicating that the effects of OSM depend on the information context, where failure to provide information to investors or other stakeholders in a timely manner may render the information useless.

1. Introduction

Recent technological and media advancements are driving noteworthy alterations in the way financial markets and institutions take in and react to information (Miller and Skinner 2015). In the field of accounting and finance, these innovations in technology have noticeably changed the disclosure media that enterprises embrace (Amin et al. 2021; Shafeeq Nimr Al-Maliki et al. 2023). This allows news articles, earnings conference calls, and others, which provide sufficient opportunities to apply the technology, to be accessed online (Loughran and McDonald 2016). Therefore, IT-enabled channels such as online social media (OSM) allow clients and prospective investors to be reached more quickly, cheaply, and interactively. This relation gives corporate social responsibility (CSR) activities higher visibility and trustworthiness (Benitez et al. 2020).

The Internet has become more and more prevalent both as a venue to carry out trading and as a basic source of information; more critically, the search volume conveyed by Google is likely to be demonstrative of the Internet search behavior of the general population (Da et al. 2011; Drake et al. 2017). The superior information dissemination facilitated by contemporary information technologies such as OSM is creating an upsurge in information. In particular, deals by shareholders in shares turn out to be more instructive regarding potential stock earnings, especially for shareholders with Internet access who are proficient in information generation (Gao and Huang 2020). Athari and Hung (2022) conclude that after the COVID-19 crisis, the interdependences between financial assets have increased, and there is a lack of hedging opportunities. So, the impact of new information about listed firms on the value of portfolios is also higher in this new context. Because of this, studies on the use of OSM by companies are of key importance. OSM not only provides organizations with a new technique for disseminating information but also provides exterior operators with the ability to generate and disseminate their own content. This shrinks firms’ ability to firmly manage their information surroundings, which means they need to cultivate new disclosure strategies (Miller and Skinner 2015). One of the strategies that needs to be disclosed is the CSR strategy. In this regard, it is noticeable that studies of CSR and corporate reputation are scarce in developing countries, especially in Egypt (Khamis and Ismail 2022; Osman et al. 2021).

The concept of CSR will remain an important element of business language and practice, as it is an important foundation for many other theories and is consistently aligned with what the public expects from the business community (Carroll 1999). CSR can be defined as a self-controlling business model that comprises activities that help organizations act responsibly toward their stakeholders and the community as well as themselves, where CSR practices take into consideration the effects that corporations have on economic, environmental, and social matters in their business surroundings (Kim and Stepchenkova 2021). Nevertheless, the modern methods of disclosure of CSR strategies are presently OSM platforms, which are now considered imperative due to rising social awareness among societies (Amin et al. 2021).

We empirically study whether OSM has a moderating effect on the relation between CSR and investment decisions in companies listed on the EGX. Two experiments were conducted using a 2 × 2 full factorial method research design. We used survey questionnaire data from 386 investors in 60 enterprises listed on the Egyptian Stock Exchange (EGX). All participants were asked some questions relating to CSR performance and use of OSM for the disclosure of either environmental or social activities and the extent to which the company employs OSM, the extent to which following OSM leads to an understanding of the CSR trends, the extent to which OSM encourages the adoption of community support policies, and the extent to which OSM leads to defining the firm’s vision, principles, concerns, and goals. Following that, questions pertaining to investment decisions were asked. We argue that firms with high CSR performance scores may attract investors; thus, CSR may have a true effect on investment decisions. Companies disclose information about CSR performance through OSM to demonstrate high dedication to society, to improve the company’s relations with stakeholders, and to achieve leadership among companies (Nandy et al. 2020). Therefore, disseminating information about CSR performance via OSM as a modern tool for rapid disclosure that cannot be ignored when studying the CSR performance disclosure in financial statements can be helpful for investors in making optimal investment decisions.

The current study includes the following contributions to the existing literature: first, whereas prior research compares top-listed companies in terms of CSR performance in developing and developed countries (El-Bassiouny and El-Bassiouny 2019; Hetze and Winistörfer 2016), our research compares the impact of high and low CSR performances of listed Egyptian companies on investment decisions and provides a clear vision for studying the way to disclose CSR financial performance of companies included in the environmental, social, and governance index (S&P/EGX ESG index) and the equal-weight index (EGX100 EWI index). Second, multiple studies on the association between CSR performance and investment decisions have administered experiments to MBA students who enrolled in or completed financial statement analysis courses as a reasonable proxy for the experimental tasks (Cohen et al. 2017; Elliott et al. 2014), whereas our paper administers experiments to investors in companies listed on the EGX rather than MBA students, as they have greater professionalism and experience, leading to more accurate and more relevant results for real-world investment practice. Third, as far as we know, our paper is the first to explore the direct impact of OSM on investors’ decisions in the Egyptian context. Finally, multiple accounting studies have examined the relationship between CSR and investment decisions (e.g., Christensen et al. 2021; Sekerci et al. 2022), whereas our paper, to the best of our knowledge, is the first to highlight the role of the modern disclosure tool OSM as a moderating variable in this relationship. We investigate the moderating effect through univariate and multivariate tests in different sectors and two different indexes of Egyptian listed companies and provide an important basis for organizing the disclosure of CSR activities through OSM.

The current research is appropriate for the Egyptian context for the following reasons: first, OSM is remarkably important for the economy in Africa and the Middle East, as it plays a vital and pivotal role in political, social, and economic changes such as those that occurred in the Arab Spring revolutions in 2010. These changes have greatly affected the Egyptian economic situation. Therefore, further analysis of the economic implications of OSM in the Egyptian context is needed. Second, Egypt is one of the most important pioneering economies not only in North Africa but also in the Middle East region, as it has the largest economy, population, and stock exchange amongst the countries of that region (Mohmed et al. 2020). In terms of trading value and turnover rates employed by Nasr and Ntim (2018), the EGX is considered the most active market and the most attractive to international investors in the region. Therefore, the results of this research are expected to positively affect the economy of the rest of the countries in this region. Finally, the Egyptian companies do not adopt CSR initiatives sufficiently, as the EGX announces the weights of only the top 30 companies in terms of CSR practices but does not announce the weights for the CSR practices of the rest of the companies included in other EGX indexes, despite the global trend towards sustainability.

The research contribution can be summarized as responding to the following research question:

Is the relationship between investors’ decisions on the EGX and the different levels of CSR performance amplified by OSM? To address this question, the remainder of this paper is structured as follows: Section 2 reviews the previous literature; Section 3 discusses the theoretical framework and development of hypotheses; Section 4 discusses the research method; Section 5 reports our results; Section 6 discusses and concludes the study.

2. Literature Review

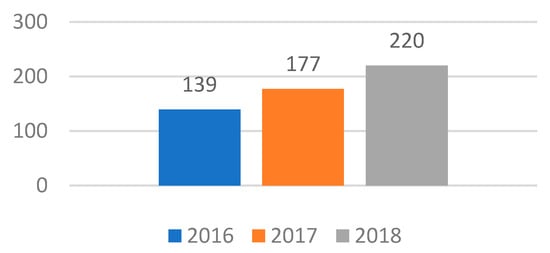

The Securities and Exchange Commission (SEC) has given public corporations permission to use OSM platforms to communicate essential information to investment decision makers. This has given corporations the chance to move disclosure from the print era to the digital age (U.S. Securities and Exchange Commission 2013). In 2018, the EGX started urging companies to use the Online Disclosure System (ODS). This system allows investors to extract the companies’ information in an efficient and swift way. By the end of 2018, the number of companies using this system increased to 220 listed companies from 249 listed companies since the beginning of 2018, an increase of 24.29% (The Egyptian Exchange, Annual Report 2018). Figure 1 shows the number of listed companies using ODS in the Egyptian market.

Figure 1.

Number of listed companies using ODS in the Egyptian market. Source: (The Egyptian Exchange, Annual Report 2018, p. 22).

Digital CSR communication on OSM is an instrument of disclosure, but its potential for value co-creation has been empirically inspected infrequently (Amin et al. 2021; Okazaki et al. 2020). CSR performance disclosures, according to the literature, highlight the different judgements about investment decisions; for instance, Khamis and Ismail (2022) confirm that CSR is an important tool that could become useful in the global business community by changing the way organizations deal with their shareholders so that companies have to be moral and liable to the general stakeholders. Intrinsically, investing in social capital may be understood as an insurance policy that pays off when shareholders face a severe crisis of trust. Bird et al. (2007) illustrate that CSR strategies have an impact on corporate value, and this impact differs depending on the classification of CSR without compromising the profit of company owners much. Ibrahim et al. (2021) suggest that directors should consider the circumstances that can activate the influence of CSR practices on companies’ profit efficiency and that they should be patient because the results of fulfilling CSR in Egypt—as investments—are not shown directly.

In his review of the literature, Malik (2015) discusses the way in which disclosure of CSR activities is utilized as an effective means of enhancing company value by aligning social objectives with firm objectives; in addition, a company with a high CSR performance has a better chance of increasing shareholder value and taking into account the interests of other parties. Given the affect-as-information theory, Elliott et al. (2014) expect that CSR performance will have an impact on the estimates of investors, who clearly consider CSR activities as a valuable part of the investment evaluation. This relation has likewise been demonstrated in the accounting literature by Anwar and Malik (2020), who find empirical evidence that the disclosure of strong CSR performance has a positive influence on investment decisions by reducing information asymmetry, which ultimately leads to increased investment behavior, while symbolic disclosure has the opposite impact according to Ferrell et al. (2016), who find that CSR is clearly related to the legal protection of shareholder privileges and negatively related to controlling shareholders’ expropriation of the rights of minority shareholders, and also according to Dhaliwal et al. (2012), who conclude that the nonfinancial disclosure of CSR performance presents valuable information to stockholders. Even though CSR is widely believed to be related to corporate value, previous studies of how CSR performance disclosure influences financial behavior remain scarce.

The current study fundamentally builds on the findings of Hao et al. (2018), who find that there is a dearth of research papers on the role of information systems in the spread of CSR and that there is a missing link between OSM and CSR. Hao et al. (2018) indicate that more interest by upcoming researchers is required due to the need for a deeper examination of the moderating impact of cross-cultural management, which reinforces the association between OSM and the awareness of CSR. Our paper is a modern starting point for empirical studies to construct a new model built on the methods, tests, and measurements prearranged here to recognize the effect of the use of OSM as a tool of CSR disclosure. The current study likewise relies on the findings of Elliott et al. (2014), who conclude that shareholders have a special interest in CSR financial performance when it is reported alongside other financial information during the consideration of investment choices. Elliott et al. (2014) confirm that when shareholders are provided with information about CSR activities without frankly being asked to evaluate it, they make investment decisions based on their emotional responses toward CSR. We expand on their paper by examining two aspects of CSR—the environmental and social dimensions—as well as assessing the business reputation, an OSM dimension which might affect the credibility of the CSR communication (Du et al. 2010). In our testing, we model both strong and weak performances of CSR. Furthermore, we study the manner in which the various dimensions of CSR activities might influence investment choices. Simnett and Huggins (2015) indicate that it is helpful to explore several CSR dimensions since CSR activities are more than just a company’s environmental dimension. Hence, given the scarcity of research about the implications of social performance in the context of CSR disclosures, the current paper studies the impact of disclosures of both environmental and social activities. Hartzmark and Sussman (2019) show that participants who consider environmental or social issues when making their choices invest more money in five-globe funds and less in one-globe funds than their performance and riskiness expectations can account for, whilst those who do not consider such issues do not show this behavior. Cheng et al. (2015) confirm that shareholders are more inclined to invest in a firm if its environmental and social performance is better and more consistent with its strategic direction. In the current paper, we also build on the work of Khanal et al. (2021) by including respondents’ opinions about the effect of OSM and CSR information presented in the models of our study.

Benitez et al. (2020) found that OSM ability behaves as an amplifier, strengthening the effect of CSR activities on firm reputation when the firm is skillful in using OSM to achieve business goals (OSM capability). The firm can use OSM to raise the social visibility and trustworthiness of its CSR activities in the market and ameliorate firm reputation. They also find that overall, although OSM ability amplifies the relationship between CSR activities and the reputation of the firm’s proprietor, advertising expenditure does not. OSM ability is thus a more effective tool than advertising to enable the firm to benefit from its investment in CSR activities. Although the findings of the current study on the link between OSM and CSR imply that investors should use CSR information, the issue is still sophisticated due to the difficulty regarding the credibility of this information (KPMG 2011; Simnett et al. 2009). There is almost no regulatory control over the creation of this information (Moroney et al. 2012). Elliott et al. (2014) demonstrate that the affect-as-information theory is helpful for understanding how investment decision makers might evaluate the benefit of CSR performance disclosure. Corporate reputation comprises different dimensions, such as product goodness, innovation, investment value, supervision of labor, and CSR. One side of corporate reputation, a firm’s present or previous CSR record, will be perceived as a special diagnostic in stakeholders’ evaluation of its CSR communication (Du et al. 2010).

However, Durnev and Kim (2005) argue that if corporations do not become more socially responsible when they have better growth chances, need more extrinsic financing, or have a higher ownership concentration, it is probably because they reckon that social responsibility is not important to investors. Indeed, CSR does not solely focus on corporate strategic actions to reinforce financial performance (engagement) or compliance with the rules and regulations. Rather, both engagement and compliance are systematically related to variations in legal regimes between countries. The level of CSR in a country expresses the intersection of the supply of socially responsible activity by firms and society’s demand for CSR practices (Liang and Renneboog 2017). In addition, OSM is increasingly becoming a vital channel for information diffusion (Feng and Johansson 2019). In particular, CSR information diffusion and additional diffusion of firm-initiated news via OSM are associated with lower abnormal bid-ask extents and larger abnormal depths, consistent with a decrement in information asymmetry (Boyd et al. 2016). This is consistent with companies being in greater need of this extra dissemination channel. Furthermore, dissemination is positively associated with liquidity (Blankespoor et al. 2014). In this regard, trust is an imperative factor when debating culture in different cultures and disciplines (Hao et al. 2018).

Despite the insufficient interest in implementing CSR in the Middle East, as well as the varying nature of environmental institutions’ and stakeholders’ need for it, CSR can create great economic and social benefits in this region (Al-Abdin et al. 2018). In Egypt, as one of the countries of the Middle East, the rise of CSR activities is foremost a result of the culture of charity and the neo-liberal tendencies that accompany most of the multinational firms, and this rise reached its peak during Mubarak’s era due to the enormous flows of foreign investment into the country (Abdelhalim and Eldin 2019). In this context, creating systems to assess CSR performance could help attract local and international investors (Fakoussa et al. 2020). Hence, a CSR disclosure strategy is a vital tool for enhancing collaboration between stakeholders, as it will empower investment decision makers to play an important role in encouraging companies to improve transparency, developing reporting standards, and supporting sustainable development (Aboud and Diab 2018). Additionally, attention to CSR practices supports companies’ financial positions in the long term, improves companies’ reputations, helps build excellent relationships with both current and prospective investors, and maximizes firm value (Mohmed et al. 2020). This is because companies with high CSR performance disclosure may give the impression to shareholders that they are less risky than companies with low CSR performance (El-Bassiouny and El-Bassiouny 2019).

So, firms participating in CSR practices and included in the Egyptian corporate responsibility index (S&P/EGX ESG) are more likely to be viewed more positively by investment decision makers (Aboud and Diab 2018). The S&P/EGX ESG index was designed and created as the foremost index among the existing indexes in Egypt to deal positively with shareholders’ fears about CSR matters (Aboud and Diab 2018). The companies with the 30 highest CSR scores announced by the S&P/ESG index care about investors and all the other stakeholders by providing transparent information to help them make wise decisions (Mohmed et al. 2020). In contrast, low-ranked companies with regard to CSR are not highly valued by shareholders in the Egyptian market (Eldomiaty et al. 2016).

Furthermore, in order to foster the discussion of CSR information with stakeholders, companies should create a community through OSM (Abdelmoety et al. 2022). OSM is one of the outstanding disclosure tools used by some organizations to provide two-way communication between the company and stakeholders to discuss CSR performance (Hetze and Winistörfer 2016). This is because CSR performance disclosure via OSM as an active channel of communication about firms’ activities has become a notable indicator for investment decision makers that the firm has a favorable financial position and can spend funds on CSR activities without negatively affecting performance (Mądra-Sawicka and Paliszkiewicz 2020). Table 1 contains an overview of some of the previous studies dealing with the research variables in the Egyptian context.

Table 1.

The research variables in the Egyptian context.

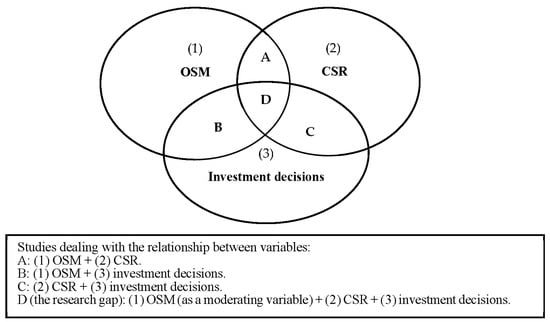

Taking into account the above argumentation, it appears that many papers have studied the relationship between CSR and investment decisions, and some papers have studied the relationship between OSM and investment decisions. The research gap we try to address in this study is focused on the scarcity of research linking the three variables to highlight the moderating effect of OSM as a disclosure tool for CSR. This provides valuable and clear insights for investors on the EGX and may thus impact on the Egyptian economy in general.

From the perspective of Table 1 and Figure 2, we examine the extent to which OSM influences the relationship between CSR performance and investment decisions. We empirically study this using a moderating model to evaluate whether the impact of OSM is conditional on whether CSR performance has a positive or negative effect on investment decisions and whether OSM has a positive or negative effect on the previous relation. Finally, prior research (Dyck et al. 2019) indicates that the significance of CSR is considerably affected by cultural considerations during investment decision making. Therefore, we also test the investment decisions of respondents from companies listed in the EGX100 EWI index on the EGX, including both those listed in the S&P/EGX index and those not listed in this index, as those companies vary in their levels of CSR performance (Mohmed et al. 2020). Using a survey approach, we also examine whether the online disclosure of environmental and social performance influences respondents’ investment decisions. We perform two tests for the two CSR dimensions, environmental and social, and compare the greater influence of CSR performance (companies included in the S&P/EGX ESG index) with the lower influence of CSR performance (companies not included in the S&P/EGX ESG index) for each dimension. By examining the impacts of OSM on the investment choice, we assess whether a modern disclosure tool, OSM, amplifies the relationship between CSR performance disclosure and investment decisions. One of the distinctive features of our research is that the outcome variable “investment decision” includes several factors of the independent variable “CSR”; the moderating variable (OSM) also includes a factor. Findings involving investors dealing in stocks that are traded through brokerage firms suggest that respondents are more inclined to invest in companies with higher CSR performance in the context of environmental and social dimensions. The results also evidence that OSM has a moderating effect on the association between high CSR performance and investment decisions but does not have a moderating effect on the association between low CSR performance and investment decisions, so the moderating effect of the current study depends on whether the CSR performance is high or low.

Figure 2.

The research gap identified by the literature review in the Egyptian context.

3. Theoretical Framework and Development of Hypotheses

The EGX launched the S&P/EGX ESG index (2010), which is the first and only ESG index in the Middle East and North Africa Region aimed at tracking the performance of companies listed on the EGX that show leadership in environmental, social, and corporate governance (ESG) matters. The EGX simplifies the listing process for companies working in the area of eco-industries, that is, renewable energy, waste recycling, transportation, and so on. EGX provides a diverse platform to finance eco-industries through IPOs, bonds, sukuk, and infrastructure funds (EGX 2018). The fundamental reason for the remarkable growth in investment in socially responsible products is that CSR initiatives may pose a risk to the company (Lindgreen et al. 2009). This is because a corporation that shows a weak social performance might experience a decline in sales, which will negatively affect the firm value, whereas a corporation with a strong image of its social performance might improve client loyalty and enhance firm value (Adams 2004). So, the board of directors has the authority to fire CEOs and hire others based on compliance in achieving the required levels of CSR performance (Mousavi et al. 2022).

3.1. Operational Factors

3.1.1. CSR and Investment Decisions

In recent years, international associations have concentrated their attention on the issue of sustainable development (Mawad et al. 2022; Pizzi et al. 2021). Prior research (e.g., Deng et al. 2013; Dimson et al. 2015; Nour et al. 2020; Bartov et al. 2021) proves a positive relationship between CSR as a sustainable development aspect, firm performance, stockholders’ fortune, and investment decisions. In addition, Ioannou and Serafeim (2015) find a positive relationship between favorable CSR performance and favorable analyst recommendations. Although CSR focuses on stakeholders as well as stockholders, it is often considered as a form of cash diversion and an agency problem. However, there is no empirical evidence that CSR is related to ex ante agency concerns, such as an abundance of cash or a weak connection between managerial pay and corporate performance (Ferrell et al. 2016). Eccles et al. (2014) illustrate that companies that were the first to implement CSR practices noticeably outclass their peers in terms of accounting and stock market performance. Moreover, incentive remuneration in those organizations reinforces the strong performance of CSR. Sekerci et al. (2022) confirm that the CSR signals sent by firms (and distributed by agencies) serve to reduce investors’ information asymmetries regarding firms’ quality. Bird et al. (2007) illuminate the previous findings by using a stockholder interest model in which the stock exchange rewards enterprises that satisfy basic criteria while punishing enterprises that exceed the minimum requirements. Some considerations, such as the data source, limit the helpfulness of previous studies, as most research depends on archived data. Even though archival research has provided many worthwhile insights and extended the scope of knowledge, it still lacks the ability to sufficiently control the information provided to shareholders and does not allow the direct assessment of shareholders’ decisions based on various forms of disclosures. The Kinder, Lydenberg, and Domini (KLD) index of CSR performance, which was used in several prior research efforts, has another type of drawback, namely that the extent to which the companies have market profiles may influence the accuracy of information to which the public has access before the ratings are announced. It is also possible that the current information about CSR initiatives as well as information unrelated to the CSR may have influenced the data utilized on the share price. This leads to difficulty in ascribing observable behavior to either one of the inputs or both with certainty. The results of prior research on capital markets (e.g., Salehi et al. 2023), mainly conducted using American and European data, cannot be extrapolated to the case of Arab countries. The final point is that previous literature sheds light on corporate evaluation instead of investors’ judgements in financial markets (Cohen et al. 2017).

CSR mechanisms are typically viewed as an aspect of moral hazard to the investors. The antithetical view, called here the “stakeholder value maximization” view, following the conception of doing well by doing good as presented in the managerial literature, argues that strategic CSR spending can maximize corporate value (Manchiraju and Rajgopal 2017). The relationship between CSR and investment decisions has been confirmed and agreed upon by many previous studies. Elliott et al. (2014) conclude that investors’ decisions are influenced by CSR performance disclosure, but when investors are first requested to assess the CSR performance explicitly, the posterior investing choices remain the same. In spite of the vast scope of themes that constitute CSR activities, previous studies commonly tend to place the spotlight on the environmental aspect of CSR (Cohen and Simnett 2015). This study investigates the environmental and social aspects of CSR activities. This is paramount since it addresses two of the three standard disclosure categories (economic, environmental, and social) that are regulated by the GRI Guidelines 4 (2013). Egyptian society would also benefit from the publication of the Egyptian companies with the top 100 CSR scores in terms of environmental and social performance rather than only the top 30, as is the existing practice, which would direct scarce funding to the higher CSR-performing businesses (Mohmed et al. 2020).

One reason why environmental aspects have been studied more than social aspects is that environmental effects are potentially simpler to scale (Cohen and Simnett 2015). Moreover, explicit standards have been issued to regulate environmental practices such as the heat emissions regulation standard (IAASB 2013), while no similar explicit standards have been issued regarding social issues.

Having into account the above argumentations, the first hypothesis of this study is stated as follows:

H1:

Investors are inclined to invest in companies that rank higher in CSR practices compared to companies that rank lower in CSR practices.

Extending the spotlight in the literature from focusing only on the environmental dimension of CSR, we formulate the two following sub-hypotheses:

H1a:

Investors are inclined to invest in companies with higher CSR performance on environmental practices than in those with lower CSR performance on environmental practices.

H1b:

Investors are inclined to invest in companies with higher CSR performance on social practices than in those with lower CSR performance on social practices.

3.1.2. Differential Impacts of OSM

OSM has become the most important network for interaction and development of relationships, notably with young users, and this network should also be used by banks to enhance financial literacy (Kuchciak and Wiktorowicz 2021). Previously, little consideration has been given to the significance of OSM in the CSR literature (Whelan et al. 2013). Recently, many research efforts have been designed to assess the relationship between CSR strategies and OSM as a modern channel (Yang and Stohl 2020). Prior research essentially proposes that the social capital of a firm is the substance of CSR and that OSM helps firms to have public information, set up good relationships, and meet public needs and can bring many benefits for firms’ future development.1 Since enterprises increasingly disclose CSR information using OSM, the ability to disseminate corporate messages rapidly has turned out to be a fundamental requirement for successful CSR disclosure (Hartmann et al. 2021). Zhang and Yang (2021) confirm that crises communicated by shareholders on OSM provide opportunities for organizations to enhance their CSR engagement. Even though OSM is an important aspect of disseminating CSR information, it is noticeable that OSM is only a starting point that can be effectively used to a large degree not only within the firm but also outside it (Whelan et al. 2013).

However, the findings of Gómez-Carrasco et al. (2021) indicate that the use of Twitter to transmit CSR information through OSM shows considerable differences among the information interests of enterprises and stakeholders. Studies have expounded that OSM advances efficient information participation and allows better communication and the fulfilment of the prescribed criteria. For example, Hoi et al. (2019) and Saxton et al. (2019) show the effectiveness of OSM for collaborative-deliberative CSR communication in a moral environment where messages are clear and noticeable to others, influence wider audiences, tap into current social movement debates, and support two-way interaction. Hao et al. (2018) assert that OSM helps firms find out public information, form good relations, and meet public requirements. Dialogic OSM use in CSR can achieve considerable advantages for firms’ future development. Hartmann et al. (2021) recommend that business communications directors should get an appropriate level of early OSM support as a CSR disclosure tool so that stakeholders receive messages in timely way to enable them to understand public pressure, which drives the business communications directors to share messages along with their OSM counterparts. Castelló et al. (2016) report that CSR argumentations on OSM can develop into a space for symbolic interaction and interactive, two-way, online dialogic communication about CSR topics that eventually assist in ameliorating the authenticity of CSR endeavors at a societal level. This orientation has accelerated with the growth of OSM such as Twitter and Facebook, which are primarily public message networks that firms are leveraging to participate with involved audiences. In particular, the strength of customer word-of-mouth has been extremely augmented, given the popularity and great reach of OSM such as blogs, chat rooms, and websites (e.g., Facebook). Firms can be proactive in using OSM to engage customers to be their CSR promoters. OSM can serve as an important framing mechanism in CSR communication on firm websites. CSR information on firms’ websites is readily attainable, often comprising the use of multimedia technologies and sometimes OSM platforms. Rich media (e.g., graphs, video) can communicate convoluted and often value-laden CSR messages, and OSM has the potential to involve stakeholders in a two-way dialogue (Du and Vieira 2012).

Then, we can formulate the following hypothesis:

H2:

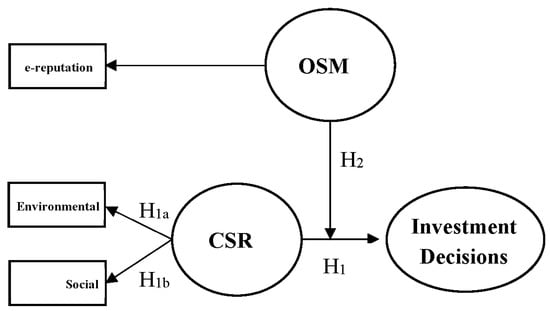

A firm’s reputation acquired through OSM has a moderating effect on the relation between a high CSR performance score and investment decisions.

Consequently, this paper empirically examines the moderating role of OSM in the relation between CSR and investment decisions. Figure 3 contains a graphical representation of the hypotheses of the model.

Figure 3.

Conceptual Model.

4. Research Method

4.1. Data and Sample

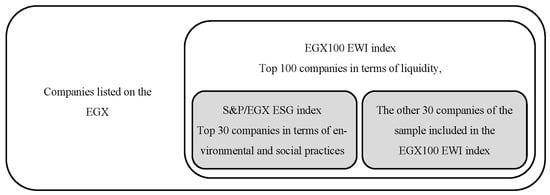

As explained above, the current study seeks to test the moderating effect of OSM on the relation between CSR performance and investment decisions on the EGX. The study is based on the survey technique to collect data from participants using online questionnaires. The online survey technique is commonly used in recent times, as it is a cost-effective tool, can be employed in less time, is more enjoyable for respondents, and avoids data entry. In addition, it does not lead to as many mistakes or blank items as paper surveys (Nayak and Narayan 2019). The online survey link was mainly shared on Facebook. The questions about CSR performance (either environmental or social) were adapted from questions posed by Liao et al. (2017). For OSM, the questions were adapted from those posed by Khanal et al. (2021). The survey questions were categorized into two main sections: demographic data and data related to the research axes. The data related to the research axes were structured into four axes: CSR towards the environment/society, the adoption of online social media, investment decisions, and the degree of viewing of financial statements. The participants were asked to select their level of agreement on a seven-point Likert scale anchored by 1 (“strongly disagree”), 2 (“disagree”), 3 (“somewhat disagree”), 4 (“neither agree nor disagree”), 5 (“somewhat agree”), 6 (“agree”), and 7 (“strongly agree”). The questions employed in each experiment are presented in Appendix A. All respondents had to be investors dealing in stocks or bonds of companies listed in the EGX100 EWI index. The sample used in the current study includes all 30 companies included in the S&P/ESG index (listed in Table 2). In addition, we selected another 30 companies included in the EGX100 EWI index (listed in Table 3) based on two criteria: (1) firms should be listed in the EGX100 EWI index and not included in the S&P/EGX ESG index; (2) firms should include disclosure of CSR practices in their annual financial reports and/or on their websites to ensure familiarity with the minimum level of knowledge of the various social responsibilities. The respondent must be an investor in one of the sample companies. If he or she is not an investor in one of the sample companies, he or she will not find his or her company as an option among the companies. Therefore, he or she will not be able to fill out the questionnaire. The study employs the CSR score presented at the end of the fiscal year of 2019–2020. Only the top 30 S&P/ESG index scores are published by the EGX. The 30 highest-scoring S&P/ESG companies have a strong commitment to CSR performance disclosure.2 The other 30 companies listed in the EGX100 EWI index have comparatively less commitment to CSR performance disclosure. This presents a chance to perform a comparison and to examine whether a strong commitment to CSR performance disclosure has a positive effect on investment decisions or not.3 A total of 386 replies were received from the shareholders in 60 companies listed on the EGX in the EGX100 EWI index and divided evenly into two groups: one comprising the 30 companies included in the S&P/EGX ESG index (199 responses were received from this group of companies, 105 of them related to the environmental experiment, and the remaining 94 to the social experiment) as shown in Table 2. The other 30 companies not included in the S&P/EGX ESG index but are included in the EGX100 EWI index (187 responses were received from this group of companies, 100 of them related to the environmental experiment, and the remaining 87 to the social experiment), as shown in Table 3. According to the EGX regulations, companies may be included in more than one index.4 The manipulation mentioned in Table 1 and Table 2 has been explained in Section 4.4 (manipulation inspections).

Table 2.

Sample companies included in the S&P/EGX ESG index.

Table 3.

Sample companies not included in the S&P/EGX ESG index.

According to S&P Dow Jones Indices in 2019, the S&P/EGX index measures the performance of firms that score higher on ESG parameters relative to their market analogues. Shareholders of firms included in both indexes are from various cultural backgrounds, belong to different firms in different sectors, and are reasonable proxies for both tasks that test the effect of higher reported CSR scores (firms included in the S&P/EGX ESG index) against the effect of lower reported CSR scores (firms not included in the index). In the first experiment, both sets of respondents were asked the same questions about the firm’s environmental practices (see Appendix A). In the second experiment, both sets of respondents were asked the same questions about the company’s social practices (see Appendix A). Each respondent participated in only one experiment.

4.2. Independent Variables

We examined the study hypotheses regarding the aspects of CSR and firm reputation on OSM by running two experiments using a 2 × 2 full factorial method research design. The two experiments utilized CSR performance disclosure and included two different kinds of policies demonstrated by Christensen et al. (2021) to be convenient for the stock exchange: environmental activities and social activities. All respondents (whether shareholders of companies listed in the S&P/EGX ESG index or of companies not listed in this index) were asked some questions relating to CSR performance and OSM. These questions include sub-questions about accomplishment in either environmental activities (the first experiment) or social activities (the second experiment) and a commitment to uniqueness in that area. The question about OSM incorporates sub-questions pertaining to the extent of the company’s use of OSM, the extent to which following OSM leads to an understanding of the CSR trends, the extent to which OSM encourages the adoption of community support policies, and the extent to which OSM leads to defining the firm’s vision, principles, concerns, and goals. Following that, questions on investment decisions were asked. Except for questions about demographic data, all other questions asked participants to evaluate the research variables on a seven-point Likert scale. Lastly, we extracted demographic information from the respondents.

4.3. Dependent Variable

Long-term earnings as a key factor in which investment decisions are based were measured by the respondent’s answer to the following investment question: “According to your knowledge about the environmental and social performance of CSR, to what degree do you intend to purchase the company stock in the coming year?”. Therefore, the outcome variable for every respondent has a value between 1 and 7, with a higher score indicating more intent to invest. The explanations of both dependent and independent variables (listed in Table 4).

Table 4.

The considered variables.

4.4. Manipulation Inspections

The Likert-scale-based instrument is the tool that involved manipulation inspections in our study asking respondents to evaluate firms’ CSR performance. A seven-point Likert-type scale running from 1 (not high) to 7 (extremely high) was used. Respondents who are investors in the companies listed on the S&P/EGX ESG index but rated the condition as “not high” were excluded from the test and vice versa: respondents who are investors in the companies not included in the S&P/EGX ESG index but rated the condition as “extremely high” were also excluded from the test. Forty-nine of the initial 386 respondents did not pass the manipulation inspections.5 Figure 4 reviews the structure of the remaining 337 respondents with investments in companies included in both indexes who evaluated the CSR performance in a manner appropriate to the experimental circumstances. The net sample includes 179 respondents in the environmental experiment and 158 respondents in the social experiment. The respondent characteristics (listed in Table 5) have acceptable representation between both pools. With regard to gender, 70.3% of the respondents are male, and 29.97% are female. Respondents aged from 35 to 44 and from 45 to 54 years old are the most common in the survey, representing 29.08% and 28.19% of participants, respectively. Although 75.67% of the respondents hold a bachelor’s degree or equivalent, the research participants have various educational levels. With regard to experience, 33.53% of the respondents have five to nine years of experience. Most of the respondents (41.25%) have invested less than 50,000 US dollars, and 67.06% of the respondents reported dealing with stocks.

Figure 4.

Final sample after excluding manipulation.

Table 5.

Respondent characteristics.

For the high CSR score condition (included in the S&P/EGX ESG index), the mean and standard deviation (SD) of CSR performance perceived by respondents are 5.2714 and 0.56950, respectively, in the first experiment, and 5.0965 and 0.76258, respectively, in the second experiment. For the low CSR score condition (not included in the S&P/EGX ESG index), the mean and SD of CSR performance perceived by respondents are 3.1185 and 0.71539, respectively, in the first experiment, and 2.9151 and 0.76443 in the second experiment. The mean (SD) influential role of OSM perceived by respondents with investments in companies listed in the S&P/EGX ESG index is 4.3878 (1.02490) in the first experiment and 4.4294 (1.05193) in the second experiment. The mean (SD) influential role of OSM perceived by respondents with investments in companies not listed in the S&P/EGX ESG index is 3.9506 (1.19858) in the first experiment and 3.9281 (1.15356) in the second experiment.

4.5. Models

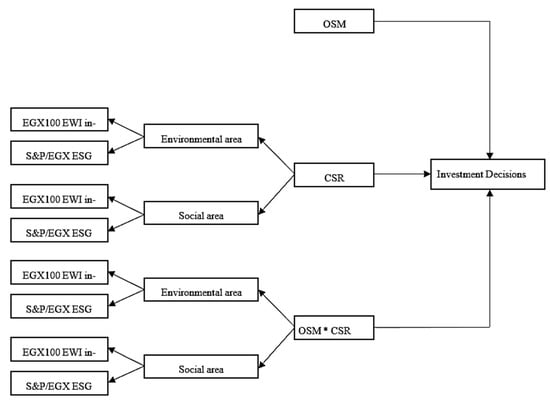

The dependent variable, as detailed above, is the respondent’s rating of investment intent on a seven-point Likert-type scale. Thus, the limited nature of this variable indicates the inappropriateness of conducting analysis of variance (ANOVA) or least squares on this type of data (Cohen et al. 2017). In this case, Grilli and Rampichini (2014) suggest using an ordered logit model to yield robust estimates because questions pertaining to satisfaction with an evaluation of something and expectations are frequently ordinal in nature. This estimation technique clearly shapes the implicit threshold parameters, which lead a participant to move from a ranking of “1” to a ranking of “2” and so on (Cohen et al. 2017). We examine our first hypothesis through both high and low CSR performance conditions and the second hypothesis through CSR–OSM interaction. We explore the potential impact of the extent to which respondents view the environmental and social financial information included in the financial statements with the variable VIEW. We also explore the potential impact of the inclusion of companies in the S&P/EGX ESG index with the variable ESGINDEX. Figure 5 shows the statistical model.

INVEST = β0 + β1CSR + β2OSM + β3CSR ∗ OSM + β4VIEW + β5ESGINDEX (the equation model)

Figure 5.

Statistical Model.

The low CSR performance condition assumes a value of 0, while the high CSR performance condition assumes a value of 1. VIEW is the respondent’s ranking of the degree to which he or she is familiar with financial statements related to environmental and social performance issued by companies, using a seven-point Likert-type scale based on 1 (“strongly disagree”) to 7 (“strongly agree”). ESGINDEX assumes a value of 0 for the non-S&P/EGX ESG index and a value of 1 otherwise.

5. Findings

Table 6 shows the descriptive statistics and univariate analyses for the dependent variable investment decisions as well as the elementary variables of interest: OSM and CSR. In line with the first hypothesis, the results in Panel A suggest that disclosure of a high CSR score (in the S&P/EGX ESG index) is significantly associated with investment decisions (at p < 0.01) for the two experiments (1, 2). Hence, participants are inclined to invest in companies with a higher level of CSR activities, and this result supports both forms (H1a, H1b) of the first hypothesis (H1) and is consistent with the findings of Aboud and Diab (2018), Anwar and Malik (2020), and Kouaib and Amara (2022). Panel B of Table 6 illustrates that there is a major influence of OSM, as the mean difference (MD) in the outcome variable based on OSM is statistically significant at the level of p < 0.01 for both environmental and social experiments for the S&P/EGX ESG index only, and this result is consistent with the results obtained by Ismail et al. (2018) and Rantala (2019). Panel C displays the matrix for both areas (environmental and social) for both companies in the index and those not included the index and evidences that the moderating variable OSM is significantly related to the relation between CSR high performance score and investment decisions (at p < 0.05). Hence, OSM moderates the relation between investment decisions and high CSR performance scores for both experiments only (in the S&P/EGX ESG index), and this result supports the second hypothesis H2. Based on the foregoing, it appears that the univariate test supports both hypotheses of our study.

Table 6.

Descriptive statistics and univariate analyses.

5.1. Multivariate Test

Table 7 includes the ordinal logistic regression outcomes for the study model. The set of companies with a low CSR performance score (the companies not in the S&P/EGX ESG index) is the reference set of CSR and OSM*CSR cases. The p-value tests and parameter estimates for the environmental area indicated in Panel A show that both a high CSR performance score and OSM are meaningful determinants of the outcome variable “INVEST” at a strong positive significance level of p < 0.01. Respondents in the high CSR performance group (companies in the S&P/EGX ESG index) are more willing to invest, as indicated by the positive coefficients of the two variables; this result supports the first form of the first hypothesis H1a and is consistent with the results obtained by Cohen et al. (2017) and Kouaib and Amara (2022). The significance of the production term “OSM*CSR” demonstrates that the influence of the high CSR performance score is related to the influence of OSM, and this result supports the second hypothesis H2. Therefore, affect-as-information theory may be used to interpret this positive effect of OSM on investment choices. The respondent’s ranking “VIEW” of the degree to which he or she is familiar with financial statements has a strong positive significance level of p < 0.01, and the participants in companies included in the S&P/EGX ESG index seem to be more reactive to these financial statements than the participants in companies not included in the S&P/EGX ESG index (p < 0.05), as indicated by the negative coefficients of the second index “ESGINDEX”. The overall model of the environmental area is significant at p < 0.01.

Table 7.

Ordinal logistic regression of the model of the impact of OSM and CSR on investment decision.

Panel B of Table 7 displays the outcomes of the model estimates for the second experiment. As in the environmental area, a high CSR score is a significant determining factor of the dependent variable investment decision at p < 0.05, supporting the second form of the first hypothesis H1b. However, OSM is not a significant determining factor of it. The production term and the perceived view are significant determining factors at p < 0.05, supporting the second hypothesis H2. As with the environmental area, the participants in the social area in the S&P/EGX ESG index seem to be more reactive to the financial statements than the participants in companies not included in the S&P/EGX ESG index at p < 0.01, and this result also supports the second sub-hypothesis H1b and is consistent with the findings of Kouaib and Amara (2022). The model for the social area is also statistically significant (p > 0.01). Based on the foregoing, the outcomes shown in Panel A of Table 7 support the first form of the first hypothesis (H1a) and prove that there is a major effect of the moderating variable OSM on the relation between the predictor and the outcome variable in the environmental area, which also provides support for the second hypothesis (H2). The outcomes shown in Panel B of Table 7 support the second form of the first hypothesis (H1b) and prove that the moderating variable has an effect in the social area.6 The findings of both univariate and multivariate tests (listed in Table 8).

Table 8.

Evidence summary.

The major findings of the multivariate test may be interpreted as suggesting that CSR performance disclosure is directly proportional to company reputation with stakeholders, which may lead to the acquisition of intangible resources (Merkl-Davies and Brennan 2007). OSM has been broadly used for intercommunication and networking objectives among firms. The literature suggests that OSM platforms have also been used by corporations to build their reputations and relationships with various stakeholders (i.e., customers, employees, and investors), and this confirms the outcome obtained by Grover et al. (2019) that CSR disclosures reported via OSM positively affect the relationship between a firm’s CEO and investors.

5.2. The Role of OSM

Interpreting all types of logistic regression is rather sophisticated because the models are linear in the logit context, such as models with a linear index specification or quadratic and interaction terms, and these measures do not provide a logically attractive explanation (Dumitrescu et al. 2022; Kennedy 2008). The use of probabilities is the easiest method of interpreting them, but this makes the surface of the model entirely nonlinear in the X and Y dimensions. Therefore, Cohen et al. (2017) base their hypothesis testing on the statistical significance of the coefficients instead of interpreting the economic significance. This leads to the production of specific difficulties related to understanding the interaction terms of dummy variables. The main issue arises when a model contains continuous variables, like our model, as the accretion of probability of Y might increment quicker through the dependence of one of the two dummy variables on the setup of the other. That is, the values of the continuous variables may possibly have a robust influence on the accretion of eventualities at different settings of the elements of interaction terms. The second hypothesis, as well as the outcomes of univariate analyses displayed in Table 5, imply that this asymmetric influence regarding OSM may potentially exist.

6. Summary and Conclusions

We expand prior studies about the significance of CSR performance disclosure on investment decisions (Cohen et al. 2017; Elliott et al. 2014). We conduct environmental and social experiments for two different CSR performance ratings (companies included and not included in the S&P/EGX ESG index) and the reputation acquired through OSM. Firstly, we present empirical evidence that CSR performance has a significant impact on investors’ decisions. This applies to both the environmental and social aspects of CSR activities. This result implies that investment decision makers are becoming increasingly interested in CSR activities, especially as this information is becoming more ubiquitous and gets more news coverage (Cohen and Simnett 2015).

We also present empirical evidence that OSM has an impact on investors’ decisions. Nonetheless, we conclude that OSM seems to be significant only in the case of high CSR performance (companies included in the S&P/EGX ESG), and this is evident in the linear regression analytics (moderator 1, 2). This indicates that in the absence of any e-reputation indicators, investment decision makers might be skeptical about the reliability of disclosure of positive CSR performance. This reinforces the interpretation of the affect-as-information theory, where investment decision makers inadvertently utilize their emotional responses toward the CSR performance level to make posterior decisions (Elliott et al. 2014; Schwarz and Clore 2003). This result indicates that the importance of OSM is determined by the investment judgement and information perspective, a topic that has not received sufficient attention in the current research. The growing trend towards the use of OSM by regulatory entities, in addition to the huge funds earmarked for OSM by companies, indicates that this is a very important topic that must be carefully explored in academic studies. The interesting question that arises is whether there is an added value for enterprises in assigning CSR specialists to their boards of directors to observe CSR activities, such as assigning financial specialists to observe the preparation of financial reporting (Cohen et al. 2008). We also realize that the e-disclosure of CSR performance via OSM could be implemented in several ways. The current paper employed an e-reputation-based strategy, which might have given rise to demand impacts in guiding the respondents’ decisions. This indicates that upcoming studies will have the chance to analyze the impacts of OSM on CSR performance-related decisions from a variety of viewpoints, as shown by the establishment of a theoretical framework and measurements of the role of OSM in implementing CSR outlined by Hao et al. (2018).

Overall, our research expands on the current CSR-related investment study (Christensen et al. 2021; Sekerci et al. 2022) by looking at how both environmental and social performance of CSR affects investment judgements. We theoretically and empirically study the specific frame of measuring the effect of adding OSM as a moderating variable for the underlying relationship between CSR performance and investment decisions to explore the extent to which OSM or the e-reputation on OSM moderates this relationship (Benitez et al. 2020; Grover et al. 2019; Pizzi et al. 2021; Khanal et al. 2021). We hope that our hypothesizing and examination will urge and help academics to address the array of extant research gaps in this scope.

The findings of our study have several positive and valuable implications. Firstly, regarding the practical implications, Aboud and Diab (2018) provide empirical explanations to EGX regulators, investors, and policy makers about the utility of the S&P/ESG index. These explanations enable investors to appraise companies more appropriately based on S&P/ESG weights. Mohmed et al. (2020) provide helpful findings—according to their expectations—for shareholders in making their decisions, because these findings shed light on the projected transparency of gains disclosed by businesses categorized by EGX indexes related to CSR performance. Our results highlight the positive impact of OSM as one of the most important and fastest modern disclosure tools of CSR performance that can help investment decision makers in the EGX to make optimal and timely decisions. This impact is expected to attract more investors to invest in companies that adopt such practices and encourage corporate policy makers to seek leadership in CSR practices to improve the reputation of their companies among various stakeholders. Secondly, regarding the economic implications, the findings by Aboud and Diab (2018) confirm the economic advantages of disclosures related to the environmental and social dimensions of CSR performance, as they indicate that businesses listed in the S&P/ESG index have a greater firm value than all other firms listed on the EGX. Our findings are expected to attract the attention of regulators of the EGX towards publishing all the weights of the listed companies in terms of CSR performance, not only the top 30 companies as is currently the case, in addition to requiring the adoption of CSR initiatives and the disclosure of these initiatives through the official online disclosure channels as one of the basic requirements for listing companies on the EGX. The results of the research are also expected to motivate professional organizations to raise the minimum standards of CSR performance and to develop guiding criteria to facilitate the task of companies in implementing CSR initiatives. Thirdly, regarding the policy implications, our findings are expected to motivate the Egyptian authorities to tighten control of the implementation of laws on environmental and social practices, in addition to directing companies to periodically disclose CSR information through OSM. Finally, regarding the academic implications, Mohmed et al. (2020) provide a guiding model for more study in this area as well as for testing other emerging markets in the Middle East region. Our findings provide an ideal starting point for academics to investigate how modern disclosure tools such as OSM can be used to improve transparency, reduce information asymmetry, and address more economic issues in emerging markets in general.

Research Limitations and Future Directions

The current study, like previous empirical research, has certain constraints, which can open up the way to deeper research in the future. First, the outcomes of this exploratory study are limited to the perceptions of investors dealing in the securities of companies listed in two Egyptian indexes, the S&P/EGX ESG index and the EGX100 EWI index on the EGX, and this restricts the generalization of the results of the study to some extent. Therefore, conducting another study on companies listed in other Egyptian indexes or on one of the Middle Eastern countries exchanges that have been exposed to the Arab Spring revolutions in recent times may lead to gaining insight into the various aspects related to the importance of adopting OSM as a common and vital tool of CSR performance disclosure to improve investment decisions. Hence, this would provide greater generalization of the results and more solutions for the region. The study also did not consider the role of demographic attributes in the moderating effect of OSM on the relationship between CSR activities and investment decisions. We recommend performing a study dealing with socio-economic demographic features of participants, which may provide interesting information about the use of OSM as a tool of CSR communication among individuals from diverse cultures and economic, social, and political backgrounds. Additionally, it is important to test the efficiency, effectiveness, and ease of use of different OSM platforms to successfully disclose CSR financial performance to shareholders. A standard condition could be included in future research to build an indicative model to compare differential levels of the extent to which OSM is used to disclose CSR performance or to disclose a company’s overall financial performance. A future research effort could also inspect whether investment decision makers in nations with experience of adopting CSR initiatives, such as countries in the EU (Simnett et al. 2009), might employ CSR financial information in a more complex way in comparison to Egypt. Future research could also study the direct impact of social media on firm value on the Egyptian market due to the scarcity of these studies in the Egyptian context.

Author Contributions

Conceptualization, A.A.M., K.H., J.D.A. and P.L.; methodology, A.A.M., K.H., J.D.A. and P.L.; software, A.A.M., K.H., J.D.A. and P.L.; validation, A.A.M., K.H., J.D.A. and P.L.; formal analysis, A.A.M., K.H., J.D.A. and P.L.; investigation, A.A.M., K.H., J.D.A. and P.L.; resources, A.A.M., K.H., J.D.A. and P.L.; data curation, A.A.M., K.H., J.D.A. and P.L.; writing—original draft preparation, A.A.M., K.H., J.D.A. and P.L.; writing—review and editing, A.A.M., K.H., J.D.A. and P.L.; visualization, A.A.M., K.H., J.D.A. and P.L.; supervision, K.H., J.D.A. and P.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Data are available from the authors upon request.

Acknowledgments

We would like to express our sincere gratitude to Ashraf Ahmed Mohamed Ghali, Vice Dean for Postgraduate Studies and Research, Faculty of Commerce, Suez Canal University, Egypt, for his invaluable support and encouragement throughout the paper.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Appendix A.1. Manipulations for CSR Performance and the Influential Role of OSM

Appendix A.1.1. First Experiment: CSR (Environmental Performance)

Considering the important role of the company in the disclosure of issues related to environmental performance, participants were asked to give their opinions on: (1) The extent to which environmental rules and regulations are followed by the company; (2) The extent to which the company is devoted to technological innovation in green building design and applies the technology in the construction process; (3) The extent to which the company ensures that building materials meet safety standards; (4) The extent to which the company conducts environmental impact assessments during the project life cycle; (5) The extent to which the company discloses accurate information about the company’s vision of sustainable development.

Appendix A.1.2. Second Experiment: CSR (Social Performance)

Considering the important role of the company in disclosure of issues related to social performance, participants were asked to give their opinions on: (1) The extent to which the company maintains effective communication and handles complaints from the community in a timely way; (2) The extent to which the company assists in public disease control and prevention; (3) The extent to which the company increases charitable donations to help and support disadvantaged groups in society; (4) The extent to which the company gives the right to freedom of association; (5) The company provides fair impartial job opportunities.

Appendix A.1.3. OSM (in Both Experiments)

Considering the important role of OSM as a tool of CSR disclosure, participants were asked to give their opinions on: (1) The extent to which the company employs OSM; (2) The extent to which following OSM leads to an understanding of the CSR trends; (3) The extent to which OSM encourages the adoption of community support policies; (4) The extent to which OSM leads to defining the firm’s vision, principles, concerns, and goals.

Notes

| 1 | For instance, Hao et al. (2018) provide a theoretical framework and measures supporting the role of OSM in realizing CSR. |

| 2 | According to the EGX (www.egx.com.eg/ar/Indices.aspx, accessed on 22 September 2020), the S&P/EGX ESG index measures the performance of 30 companies listed on the EGX that are among the highest ESG scoring and also meet the requirements detailed in the eligibility criteria. Index constituents are ESG score weighted. The S&P/EGX ESG index is a sub-index of the EGX EWI index, which includes the top 100 companies which are active players in the EGX in terms of liquidity, activity, and total value traded during the 12-month period ending in May of every year. |

| 3 | The method of comparing companies included and not included in the Egyptian index to assess CSR practices is used in some previous studies such as Mohmed et al. (2020). |

| 4 | The EGX regulations can be seen at www.egx.com.eg/ar/homepage.aspx, accessed on 11 May 2020. |

| 5 | This description is used by Cohen et al. (2017) and Elliott et al. (2014). |

| 6 | The judgement on whether there is a moderating effect is made based on a statistically significant relationship between the interaction term and the outcome variable (Aguinis et al. 2017; Memon et al. 2019). |

References

- Abdelhalim, Khalid, and Amani Eldin. 2019. Can CSR help achieve sustainable development? Applying a new assessment model to CSR cases from Egypt. International Journal of Sociology and Social Policy 39: 773–95. [Google Scholar] [CrossRef]

- Abdelmoety, Hassan, Sameh Aboul-Dahab, and Gomaa Agag. 2022. A cross cultural investigation of retailers commitment to CSR and customer citizenship behaviour: The role of ethical standard and value relevance. Journal of Retailing and Consumer Services 64: 102796. [Google Scholar] [CrossRef]

- Aboud, Ahmed, and Ahmed Diab. 2018. The impact of social, environmental and corporate governance disclosures on firm value: Evidence from Egypt. Journal of Accounting in Emerging Economies 8: 442–58. [Google Scholar] [CrossRef]

- Adams, Carol. 2004. The ethical, social and environmental reporting-performance portrayal gap. Accounting, Auditing & Accountability Journal 17: 731–57. [Google Scholar] [CrossRef]

- Aguinis, Herman, Jeffrey Edwards, and Kyle Bradley. 2017. Improving Our Understanding of Moderation and Mediation in Strategic Management Research. Organizational Research Methods 20: 665–85. [Google Scholar] [CrossRef]

- Al-Abdin, Ahmed, Taposh Roy, and John Nicholson. 2018. Researching Corporate Social Responsibility in the Middle East: The Current State and Future Directions. Corporate Social Responsibility and Environmental Management 25: 47–65. [Google Scholar] [CrossRef]

- Amin, Marian, Ehab Mohamed, and Ahmed Elragal. 2021. CSR disclosure on Twitter: Evidence from the UK. International Journal of Accounting Information Systems 40: 100500. [Google Scholar] [CrossRef]

- Anwar, Rehana, and Jaleel Malik. 2020. When Does Corporate Social Responsibility Disclosure Affect Investment Efficiency? A New Answer to an Old Question. SAGE Open 10: 1–14. [Google Scholar] [CrossRef]

- Athari, Seyed, and Ngo Hung. 2022. Time–frequency return co-movement among asset classes around the COVID-19 outbreak: Portfolio implications. Journal of Economics and Finance 46: 736–56. [Google Scholar] [CrossRef]

- Bartov, Eli, Antonio Marra, and Francesco Momenté. 2021. Corporate Social Responsibility and the Market Reaction to Negative Events: Evidence from Inadvertent and Fraudulent Restatement Announcements. The Accounting Review 96: 81–106. [Google Scholar] [CrossRef]

- Benitez, Jose, Laura Ruiz, Ana Castillo, and Javier Llorens. 2020. How corporate social responsibility activities influence employer reputation: The role of social media capability. Decision Support Systems 129: 113223. [Google Scholar] [CrossRef]

- Bird, Ron, Anthony Hall, Francesco Momentè, and Francesco Reggiani. 2007. What corporate social responsibility activities are valued by the market? Journal of Business Ethics 76: 189–206. [Google Scholar] [CrossRef]

- Blankespoor, Elizabeth, Gregory S. Miller, and Hal D. White. 2014. The Role of Dissemination in Market Liquidity: Evidence from Firms’ Use of Twitter™. The Accounting Review 89: 79–112. [Google Scholar] [CrossRef]

- Boyd, Eric, Benjamin McGarry, and Theresa Clarke. 2016. Exploring the empowering and paradoxical relationship between social media and CSR activism. Journal of Business Research 69: 2739–46. [Google Scholar] [CrossRef]

- Carroll, Archie. 1999. Evolution of a Definitional Construct. Business & Society 38: 268–95. [Google Scholar]

- Castelló, Itziar, Michael Etter, and Finn Nielsen. 2016. Strategies of Legitimacy Through Social Media: The Networked Strategy. Journal of Management Studies 53: 402–32. [Google Scholar] [CrossRef]

- Cheng, Mandy, Wendy Green, and John Ko. 2015. The Impact of Strategic Relevance and Assurance of Sustainability Indicators on Investors’ Decisions. AUDITING: A Journal of Practice & Theory 34: 131–62. [Google Scholar] [CrossRef]

- Christensen, Dane, George Serafeim, and Anywhere Sikochi. 2021. Why is Corporate Virtue in the Eye of The Beholder? The Case of ESG Ratings. The Accounting Review 97: 147–75. [Google Scholar] [CrossRef]

- Cohen, Jeffrey, and Roger Simnett. 2015. CSR and Assurance Services: A Research Agenda. AUDITING: A Journal of Practice & Theory 34: 59–74. [Google Scholar] [CrossRef]

- Cohen, Jeffrey, Lori Holder-Webb, and Samer Khalil. 2017. A Further Examination of the Impact of Corporate Social Responsibility and Governance on Investment Decisions. Journal of Business Ethics 146: 203–18. [Google Scholar] [CrossRef]

- Cohen, Lauren, Andrea Frazzini, and Christopher Malloy. 2008. The small world of investing: Board connections and mutual fund returns. Journal of Political Economy 116: 951–79. [Google Scholar] [CrossRef]

- Da, Zhi, Joseph Engelber, and Pengjie Gao. 2011. In Search of Attention. Journal of Finance 66: 1461–99. [Google Scholar] [CrossRef]

- Darrag, Menatallah, and David Crowther. 2017. Reflections on CSR: The case of Egypt. Society and Business Review 12: 94–116. [Google Scholar] [CrossRef]

- Deng, Xin, Jun-koo Kang, and Buen Low. 2013. Corporate social responsibility and stakeholder value maximization: Evidence from mergers. Journal of Financial Economics 110: 87–109. [Google Scholar] [CrossRef]

- Dhaliwal, Dan, Suresh Radhakrishnan, Albert Tsang, and Yong Yang. 2012. Nonfinancial Disclosure and Analyst Forecast Accuracy: International Evidence on Corporate Social Responsibility Disclosure. The Accounting Review 87: 723–59. [Google Scholar] [CrossRef]

- Dimson, Elroy, Oğuzhan Karakaş, and Xi Li. 2015. Active Ownership. Review of Financial Studies 28: 3225–68. [Google Scholar] [CrossRef]

- Drake, Michael, Jacob Thornock, and Brady Twedt. 2017. The internet as an information intermediary. Review of Accounting Studies 22: 543–76. [Google Scholar] [CrossRef]

- Du, Shuili, and Edward Vieira. 2012. Striving for Legitimacy Through Corporate Social Responsibility: Insights from Oil Companies. Journal of Business Ethics 110: 413–27. [Google Scholar] [CrossRef]

- Du, Shuili, C. B. Bhattacharya, and Sankar Sen. 2010. Maximizing business returns to corporate social responsibility (CSR): The role of CSR communication. International Journal of Management Reviews 12: 8–19. [Google Scholar] [CrossRef]

- Dumitrescu, Elena, Sullivan Hué, Christophe Hurlin, and Sessi Tokpavi. 2022. Machine learning for credit scoring: Improving logistic regression with non-linear decision-tree effects. European Journal of Operational Research 297: 1178–92. [Google Scholar] [CrossRef]

- Durnev, Art, and Han Kim. 2005. To steal or not to steal: Firm attributes, legal environment, and valuation. Journal of Finance 60: 1461–93. [Google Scholar] [CrossRef]

- Dyck, Alexander, Karl Lins, Lukas Roth, and Hannes Wagner. 2019. Do institutional investors drive corporate social responsibility? International evidence. Journal of Financial Economics 131: 693–714. [Google Scholar] [CrossRef]

- Eccles, Robert, Ioannis Ioannou, and George Serafeim. 2014. The Impact of a Corporate Culture of Sustainability on Corporate Behavior and Performance. Management Science 60: 2835–57. [Google Scholar] [CrossRef]

- EGX. 2018. EGX & SUSTAINABILITY. Cairo: The Egyptian Exchange. Available online: https://www.egx.com.eg/en/egx-and-sustainability.aspx (accessed on 12 November 2020).

- El-Bassiouny, Dina, and Noha El-Bassiouny. 2019. Diversity, corporate governance and CSR reporting: A comparative analysis between top-listed firms in Egypt, Germany and the USA. Management of Environmental Quality: An International Journal 30: 116–36. [Google Scholar] [CrossRef]

- Eldomiaty, Tarek, Ahmad Soliman, Ahmed Fikri, and Marwa Anis. 2016. The financial aspects of the corporate responsibility index in Egypt: A quantitative approach to institutional economics. International Journal of Social Economics 43: 284–307. [Google Scholar] [CrossRef]

- Elliott, Brooke, Kevin Jackson, Mark Peecher, and Brian White. 2014. The Unintended Effect of Corporate Social Responsibility Performance on Investors’ Estimates of Fundamental Value. The Accounting Review 89: 275–302. [Google Scholar] [CrossRef]

- Fakoussa, Rebecca, Simon O’Leary, and Suzan Salem. 2020. An exploratory study on social entrepreneurship in Egypt. Journal of Islamic Accounting and Business Research 11: 694–707. [Google Scholar] [CrossRef]

- Feng, Xunan, and Anders Johansson. 2019. Top executives on social media and information in the capital market: Evidence from China. Journal of Corporate Finance 58: 824–57. [Google Scholar] [CrossRef]

- Ferrell, Allen, Hao Liang, and Luc Renneboog. 2016. Socially responsible firms. Journal of Financial Economics 122: 585–606. [Google Scholar] [CrossRef]

- Gao, Meng, and Jiekun Huang. 2020. Informing the Market: The Effect of Modern Information Technologies on Information Production. The Review of Financial Studies 33: 1367–411. [Google Scholar] [CrossRef]

- Gómez-Carrasco, Pablo, Encarna Guillamón-Saorín, and Beatriz Osma. 2021. Stakeholders versus Firm Communication in Social Media: The Case of Twitter and Corporate Social Responsibility Information. European Accounting Review 30: 31–62. [Google Scholar] [CrossRef]

- Grilli, Leonardo, and Carla Rampichini. 2014. Ordered Logit Model. Encyclopedia of Quality of Life and Well-Being Research, 4510–13. [Google Scholar] [CrossRef]

- Grover, Purva, Arpan Kar, and Vigneswara Ilavarasan. 2019. Impact of corporate social responsibility on reputation—Insights from tweets on sustainable development goals by CEOs. International Journal of Information Management 48: 39–52. [Google Scholar] [CrossRef]

- Hao, Yunhong, Qamar Farooq, and Yuan Sun. 2018. Development of theoretical framework and measures for the role of social media in realizing corporate social responsibility through native and non-native communication modes: Moderating effects of cross-cultural management. Corporate Social Responsibility and Environmental Management 25: 704–11. [Google Scholar] [CrossRef]