The Impact of the COVID-19 Pandemic on the Volatility of Cryptocurrencies

,

,  ,

,  and

and

Abstract

1. Introduction

2. Literature Review

3. Data and Methods

3.1. Data

3.2. Methodology

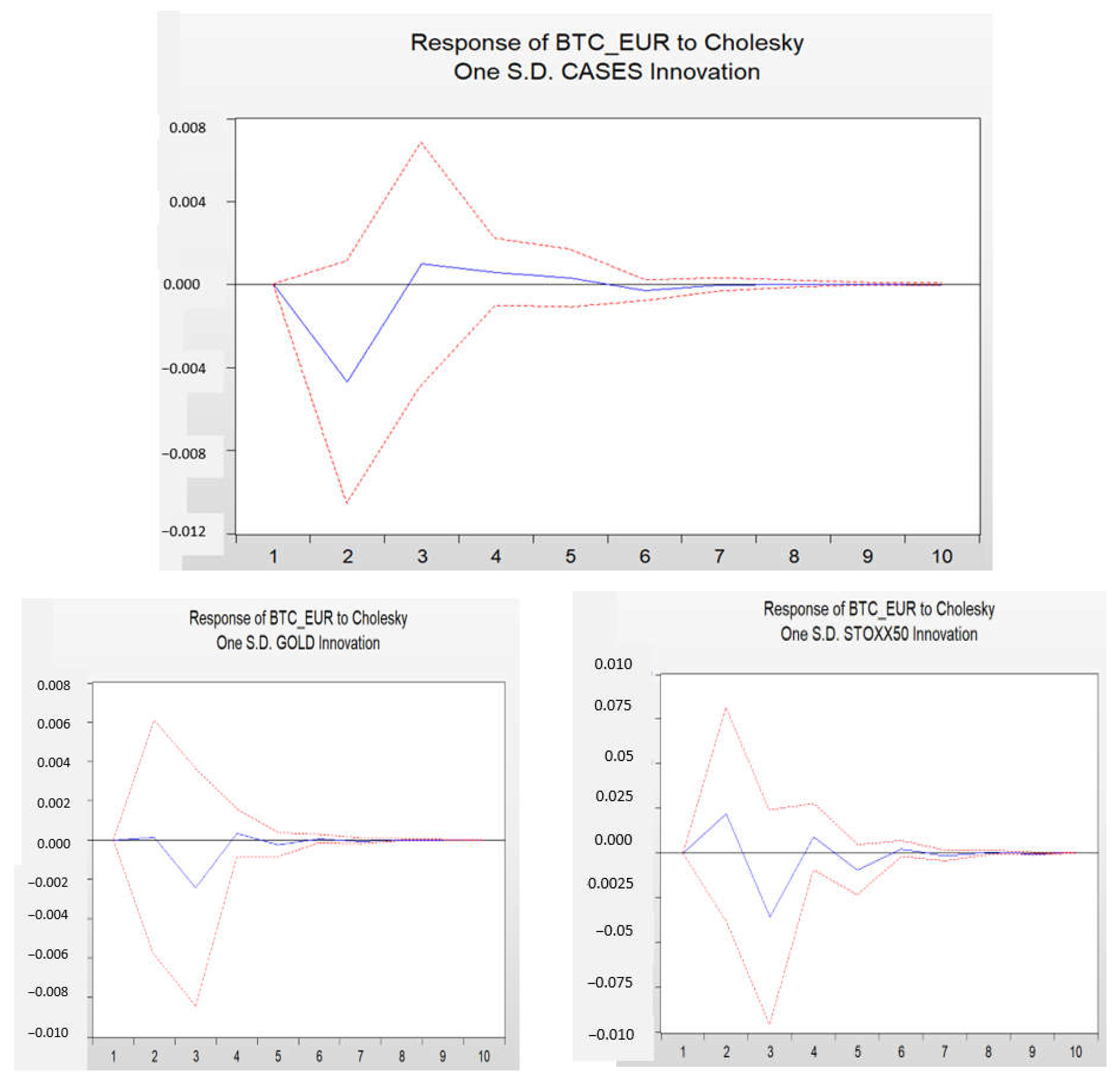

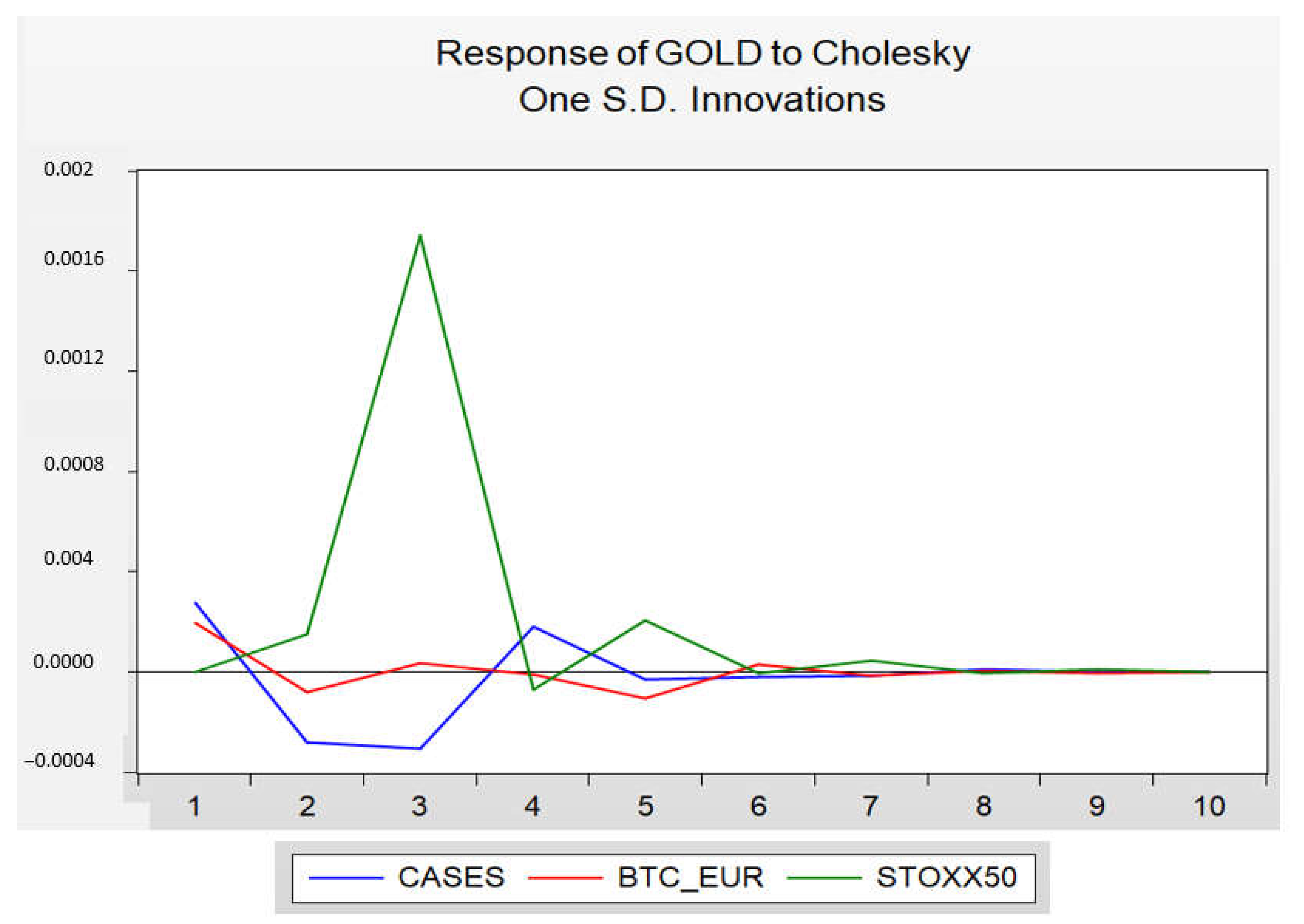

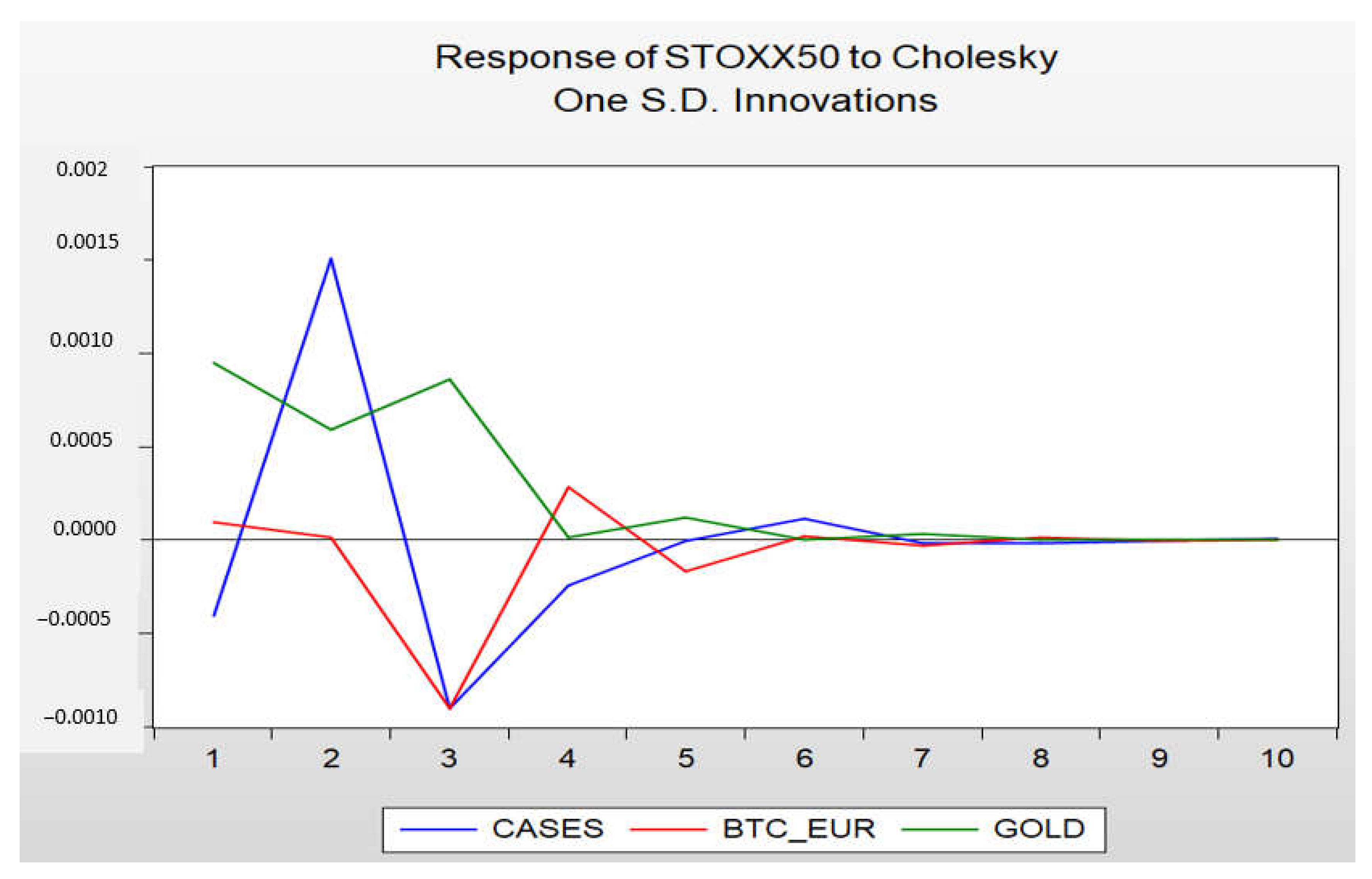

4. Results

5. Discussion and Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Adekoya, Oluwasegun B., and Johnson A. Oliyide. 2022. Commodity and Financial Markets’ Fear before and during COVID-19 Pandemic: Persistence and Causality Analyses. Resources Policy 76: 102598. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, and Ahmet Sensoy. 2021. Financial Contagion during COVID–19 Crisis. Finance Research Letters 38: 101604. [Google Scholar] [CrossRef] [PubMed]

- Ampountolas, Apostolos. 2023. The Effect of COVID-19 on Cryptocurrencies and the Stock Market Volatility: A Two-Stage DCC-EGARCH Model Analysis. Journal of Risk and Financial Management 16: 25. [Google Scholar] [CrossRef]

- Apergis, Nicholas. 2022. COVID-19 and Cryptocurrency Volatility: Evidence from Asymmetric Modelling. Finance Research Letters 2022: 102659. [Google Scholar] [CrossRef]

- Assaf, Ata, Khaled Mokni, Imran Yousaf, and Avishek Bhandari. 2023. Long Memory in the High Frequency Cryptocurrency Markets Using Fractal Connectivity Analysis: The Impact of COVID-19. Research in International Business and Finance 64: 101821. [Google Scholar] [CrossRef]

- Atri, Hanen, Saoussen Kouki, and Mohamed imen Gallali. 2021. The Impact of COVID-19 News, Panic and Media Coverage on the Oil and Gold Prices: An ARDL Approach. Resources Policy 72: 102061. [Google Scholar] [CrossRef]

- Azimli, Asil. 2022. Degree and Structure of Return Dependence among Commodities, Energy Stocks and International Equity Markets during the Post-COVID-19 Period. Resources Policy 77: 102679. [Google Scholar] [CrossRef] [PubMed]

- Baig, Ahmed S., Hassan Anjum Butt, Omair Haroon, and Syed Aun R. Rizvi. 2021. Deaths, Panic, Lockdowns and US Equity Markets: The Case of COVID-19 Pandemic. Finance Research Letters 38: 101701. [Google Scholar] [CrossRef] [PubMed]

- Baker, Scott, Nicholas Bloom, Steven Davis, and Stephen Terry. 2020. COVID-Induced Economic Uncertainty. Cambridge, MA: National Bureau of Economic Research, vol. 17. [Google Scholar]

- Balcilar, Mehmet, Zeynel Abidin Ozdemir, and Muhammad Shahbaz. 2019. On the Time-Varying Links between Oil and Gold: New Insights from the Rolling and Recursive Rolling Approaches. International Journal of Finance and Economics 24: 1047–65. [Google Scholar] [CrossRef]

- Banerjee, Ameet Kumar, Md Akhtaruzzaman, Andreia Dionisio, Dora Almeida, and Ahmet Sensoy. 2022. Nonlinear Nexus between Cryptocurrency Returns and COVID–19 COVID-19 News Sentiment. Journal of Behavioral and Experimental Finance 36: 100747. [Google Scholar] [CrossRef] [PubMed]

- Baur, Dirk G., Lai T. Hoang, and Md Zakir Hossain. 2022. Is Bitcoin a Hedge? How Extreme Volatility Can Destroy the Hedge Property. Finance Research Letters 47: 102655. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Thomas K. McDermott. 2010. Is Gold a Safe Haven? International Evidence. Journal of Banking and Finance 34: 1886–98. [Google Scholar] [CrossRef]

- Bekiros, Stelios, Axel Hedström, Evgeniia Jayasekera, Tapas Mishra, and Gazi Salah Uddin. 2021. Correlated at the Tail: Implications of Asymmetric Tail-Dependence Across Bitcoin Markets. Computational Economics 58: 1289–99. [Google Scholar] [CrossRef]

- Benlagha, Noureddine, and Salaheddine El Omari. 2022. Connectedness of Stock Markets with Gold and Oil: New Evidence from COVID-19 Pandemic. Finance Research Letters 46: 102373. [Google Scholar] [CrossRef] [PubMed]

- Bourghelle, David, Fredj Jawadi, and Philippe Rozin. 2022. Do Collective Emotions Drive Bitcoin Volatility? A Triple Regime-Switching Vector Approach. Journal of Economic Behavior and Organization 196: 294–306. [Google Scholar] [CrossRef]

- Chen, Conghui, Lanlan Liu, and Ningru Zhao. 2020. Fear Sentiment, Uncertainty, and Bitcoin Price Dynamics: The Case of COVID-19. Emerging Markets Finance and Trade 56: 2298–2309. [Google Scholar] [CrossRef]

- Conlon, Thomas, and Richard McGee. 2020. Safe Haven or Risky Hazard? Bitcoin during the Covid-19 Bear Market. Finance Research Letters 35: 101607. [Google Scholar] [CrossRef]

- Corbet, Shaen, Charles Larkin, and Brian Lucey. 2020. The Contagion Effects of the COVID-19 Pandemic: Evidence from Gold and Cryptocurrencies. Finance Research Letters 35: 101554. [Google Scholar] [CrossRef]

- Danish, Bo Wang, and Zhaohua Wang. 2018. Imported Technology and CO2 Emission in China: Collecting Evidence through Bound Testing and VECM Approach. Renewable and Sustainable Energy Reviews 82: 4204–14. [Google Scholar] [CrossRef]

- Di, Michael, and Ke Xu. 2022. COVID-19 Vaccine and Post-Pandemic Recovery: Evidence from Bitcoin Cross-Asset Implied Volatility Spillover. Finance Research Letters 50: 103289. [Google Scholar] [CrossRef] [PubMed]

- Dutta, Anupam, Debojyoti Das, R. K. Jana, and Xuan Vinh Vo. 2020. COVID-19 and Oil Market Crash: Revisiting the Safe Haven Property of Gold and Bitcoin. Resources Policy 69: 101816. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2016. Bitcoin, Gold and the Dollar—A GARCH Volatility Analysis. Finance Research Letters 16: 85–92. [Google Scholar] [CrossRef]

- Etokakpan, Mfonobong Udom, Sakiru Adebola Solarin, Vedat Yorucu, Festus Victor Bekun, and Samuel Asumadu Sarkodie. 2020. Modeling Natural Gas Consumption, Capital Formation, Globalization, CO2 Emissions and Economic Growth Nexus in Malaysia: Fresh Evidence from Combined Cointegration and Causality Analysis. Energy Strategy Reviews 31: 100526. [Google Scholar] [CrossRef]

- Foroutan, Parisa, and Salim Lahmiri. 2022. The Effect of COVID-19 Pandemic on Return-Volume and Return-Volatility Relationships in Cryptocurrency Markets. Chaos, Solitons and Fractals 162: 112443. [Google Scholar] [CrossRef]

- Gautam, Roshan, Yoochan Kim, Erkan Topal, and Michael Hitch. 2022. Correlation between COVID-19 Cases and Gold Price Fluctuation. International Journal of Mining, Reclamation and Environment 36: 574–86. [Google Scholar] [CrossRef]

- Goodell, John W., and Stephane Goutte. 2021. Co-Movement of COVID-19 and Bitcoin: Evidence from Wavelet Coherence Analysis. Finance Research Letters 38: 101625. [Google Scholar] [CrossRef] [PubMed]

- Ha, Le Thanh, and Nguyen Thi Hong Nham. 2022. An Application of a TVP-VAR Extended Joint Connected Approach to Explore Connectedness between WTI Crude Oil, Gold, Stock and Cryptocurrencies during the COVID-19 Health Crisis. Technological Forecasting and Social Change 183: 121909. [Google Scholar] [CrossRef] [PubMed]

- Harbourt, David E., Andrew D. Haddow, Ashley E. Piper, Holly Bloomfield, Brian J. Kearney, David Fetterer, Kathleen Gibson, and Timothy Minogue. 2020. Modeling the Stability of Severe Acute Respiratory Syndrome Coronavirus 2 (SARS-CoV-2) on Skin, Currency, and Clothing. PLoS Neglected Tropical Diseases 14: e0008831. [Google Scholar] [CrossRef]

- Hung, Ngo Thai, and Xuan Vinh Vo. 2021. Directional Spillover Effects and Time-Frequency Nexus between Oil, Gold and Stock Markets: Evidence from Pre and during COVID-19 Outbreak. International Review of Financial Analysis 76: 10–11. [Google Scholar] [CrossRef] [PubMed]

- Jeribi, Ahmed, Sangram Keshari Jena, and Amine Lahiani. 2021. Are Cryptocurrencies a Backstop for the Stock Market in a Covid-19-Led Financial Crisis? Evidence from the Nardl Approach. International Journal of Financial Studies 9: 33. [Google Scholar] [CrossRef]

- Ji, Qiang, Dayong Zhang, and Yuqian Zhao. 2020. Searching for Safe-Haven Assets during the COVID-19 Pandemic. International Review of Financial Analysis 71: 101526. [Google Scholar] [CrossRef]

- Karamti, Chiraz, and Olfa Belhassine. 2022. COVID-19 Pandemic Waves and Global Financial Markets: Evidence from Wavelet Coherence Analysis. Finance Research Letters 45: 102136. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Larisa Yarovaya, and Damian Zięba. 2022. High-Frequency Connectedness between Bitcoin and Other Top-Traded Crypto Assets during the COVID-19 Crisis. Journal of International Financial Markets, Institutions and Money 79: 101578. [Google Scholar] [CrossRef]

- Koch, Sophia, and Thomas Dimpfl. 2023. Attention and Retail Investor Herding in Cryptocurrency Markets. Finance Research Letters 51: 103474. [Google Scholar] [CrossRef]

- Kwapié, M., José F. F. Mendes, Marcin W. Atorek, Jarosław Kwapié, and Stanisław Dro Zdz. 2023. Cryptocurrencies Are Becoming Part of the World Global Financial Market. Entropy 25: 377. [Google Scholar] [CrossRef]

- Le, Lan T. N., Larisa Yarovaya, and Muhammad Ali Nasir. 2021. Did COVID-19 Change Spillover Patterns between Fintech and Other Asset Classes? Research in International Business and Finance 58: 101441. [Google Scholar] [CrossRef]

- Li, Rongrong, and Min Su. 2017. The Role of Natural Gas and Renewable Energy in Curbing Carbon Emission: Case Study of the United States. Sustainability 9: 600. [Google Scholar] [CrossRef]

- Li, Yuze, Shangrong Jiang, Xuerong Li, and Shouyang Wang. 2021. The Role of News Sentiment in Oil Futures Returns and Volatility Forecasting: Data-Decomposition Based Deep Learning Approach. Energy Economics 95: 105140. [Google Scholar] [CrossRef]

- Loizia, Pantelitsa, Irene Voukkali, Antonis A. Zorpas, Jose Navarro Pedreño, Georgia Chatziparaskeva, Vassilis J. Inglezakis, Ioannis Vardopoulos, and Maria Doula. 2021. Measuring the Level of Environmental Performance in Insular Areas, through Key Performed Indicators, in the Framework of Waste Strategy Development. Science of The Total Environment 753: 141974. [Google Scholar] [CrossRef]

- Maneejuk, Paravee, Nuttaphong Kaewtathip, Peemmawat Jaipong, and Woraphon Yamaka. 2022. The Transition of the Global Financial Markets’ Connectedness during the COVID-19 Pandemic. North American Journal of Economics and Finance 63: 101816. [Google Scholar] [CrossRef]

- Pal, Rimesh, and Sanjay K. Bhadada. 2020. Cash, Currency and COVID-19. Postgraduate Medical Journal 96: 427–28. [Google Scholar] [CrossRef] [PubMed]

- Paramati, Sudharshan Reddy, Hussein Abedi Shamsabadi, and Harshavardhan Reddy Kummitha. 2022. How Did Gold Prices Respond to the COVID-19 Pandemic? Applied Economics Letters 2022: 1–7. [Google Scholar] [CrossRef]

- Salisu, Afees A., and Ahamuefula E. Ogbonna. 2021. The Return Volatility of Cryptocurrencies during the COVID-19 Pandemic: Assessing the News Effect. Global Finance Journal 2021: 100641. [Google Scholar] [CrossRef]

- Salisu, Afees A., and Xuan Vinh Vo. 2020. Predicting Stock Returns in the Presence of COVID-19 Pandemic: The Role of Health News. International Review of Financial Analysis 71: 101546. [Google Scholar] [CrossRef]

- Shehzad, Khurram, Faik Bilgili, Umer Zaman, Emrah Kocak, and Sevda Kuskaya. 2021. Is Gold Favourable than Bitcoin during the COVID-19 Outbreak? Comparative Analysis through Wavelet Approach. Resources Policy 73: 102163. [Google Scholar] [CrossRef]

- Sifat, Imtiaz. 2021. On Cryptocurrencies as an Independent Asset Class: Long-Horizon and COVID-19 Pandemic Era Decoupling from Global Sentiments. Finance Research Letters 43: 102013. [Google Scholar] [CrossRef]

- Sims, Christopher A. 1980. Macroeconomics and Reality. Econometrica 48: 1. [Google Scholar] [CrossRef]

- Smales, L. A. 2021. Investor Attention and Global Market Returns during the COVID-19 Crisis. International Review of Financial Analysis 73: 101616. [Google Scholar] [CrossRef]

- Su, Jung Bin, and Yu Sheng Kao. 2022. How Does the Crisis of the COVID-19 Pandemic Affect the Interactions between the Stock, Oil, Gold, Currency, and Cryptocurrency Markets? Frontiers in Public Health 10: 933264. [Google Scholar] [CrossRef] [PubMed]

- Syuhada, Khreshna, Arief Hakim, Djoko Suprijanto, Intan Muchtadi-Alamsyah, and Lukman Arbi. 2022. Is Tether a Safe Haven of Safe Haven amid COVID-19? An Assessment against Bitcoin and Oil Using Improved Measures of Risk. Resources Policy 79: 103111. [Google Scholar] [CrossRef] [PubMed]

- Tuna, Gülfen, and Vedat Ender Tuna. 2022. Are Effects of COVID-19 Pandemic on Financial Markets Permanent or Temporary? Evidence from Gold, Oil and Stock Markets. Resources Policy 76: 102637. [Google Scholar] [CrossRef]

- Ullah, Subhan, Rexford Attah-Boakye, Kweku Adams, and Ghasem Zaefarian. 2022. Assessing the Influence of Celebrity and Government Endorsements on Bitcoin’s Price Volatility. Journal of Business Research 145: 228–39. [Google Scholar] [CrossRef]

- Umar, Muhammad, Chi Wei Su, Syed Kumail Abbas Rizvi, and Xue Feng Shao. 2021. Bitcoin: A Safe Haven Asset and a Winner amid Political and Economic Uncertainties in the US? Technological Forecasting and Social Change 167: 120680. [Google Scholar] [CrossRef]

- Vardopoulos, Ioannis, Ioannis Konstantopoulos, Antonis A. Zorpas, Lionel Limousy, Simona Bennici, Vassilis J. Inglezakis, and Irene Voukkali. 2021. Sustainable Metropolitan Areas Perspectives through Assessment of the Existing Waste Management Strategies. Environmental Science and Pollution Research 28: 24305–20. [Google Scholar] [CrossRef] [PubMed]

- Wang, Jingjing, and Xiaoyang Wang. 2021. COVID-19 and Financial Market Efficiency: Evidence from an Entropy-Based Analysis. Finance Research Letters 42: 101888. [Google Scholar] [CrossRef]

- Yan, Yu, Yiming Lei, and Yiming Wang. 2022. Bitcoin as a Safe-Haven Asset and a Medium of Exchange. Axioms 11: 415. [Google Scholar] [CrossRef]

- Yarovaya, Larisa, Roman Matkovskyy, and Akanksha Jalan. 2022. The COVID-19 Black Swan Crisis: Reaction and Recovery of Various Financial Markets. Research in International Business and Finance 59: 101521. [Google Scholar] [CrossRef]

- Zhang, Chi, Kaile Zhou, Shanlin Yang, and Zhen Shao. 2017. Exploring the Transformation and Upgrading of China’s Economy Using Electricity Consumption Data: A VAR–VEC Based Model. Physica A: Statistical Mechanics and Its Applications 473: 144–55. [Google Scholar] [CrossRef]

- Zhang, Dayong, Min Hu, and Qiang Ji. 2020. Financial Markets under the Global Pandemic of COVID-19. Finance Research Letters 36: 101528. [Google Scholar] [CrossRef]

- Zhang, Stephen, and Ganesh Mani. 2021. Popular Cryptoassets (Bitcoin, Ethereum, and Dogecoin), Gold, and Their Relationships: Volatility and Correlation Modeling. Data Science and Management 4: 30–39. [Google Scholar] [CrossRef]

- Zhang, Yue Jun. 2011. The Impact of Financial Development on Carbon Emissions: An Empirical Analysis in China. Energy Policy 39: 2197–2203. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | BTC/EUR | CASES | GOLD | STOXX50 |

|---|---|---|---|---|

| Mean | 0.000968 | 0.006988 | 1.000382 | 0.000221 |

| Median | 0.002761 | 0.011616 | 1.000811 | 0.000763 |

| Maximum | 0.418035 | 0.610045 | 1.059738 | 0.088343 |

| Minimum | −0.580335 | −0.703200 | 0.951312 | −0.132405 |

| Std. Dev | 0.068304 | 0.209430 | 0.011385 | 0.016085 |

| Skewness | −1.131362 | 0.082114 | −0.169894 | −1.289818 |

| Kurtosis | 20.28825 | 3.369737 | 7.569779 | 15.91682 |

| Variables | Intercept | Trend and Intercept |

|---|---|---|

| t-Statistic | t-Statistic | |

| BTC/EUR | −27.61717 * | −27.74215 * |

| CASES | −5.445705 * | −5.647285 * |

| GOLD | −24.05165 * | −24.04325 * |

| STOXX50 | −26.66801 * | −26.74654 * |

| Period | BTC/EUR | CASES | GOLD | STOXX50 |

|---|---|---|---|---|

| 1 | 100.0000 | 0.000000 | 0.000000 | 0.000000 |

| 2 | 99.43263 | 0.465345 | 0.000284 | 0.101741 |

| 3 | 99.01847 | 0.484428 | 0.125595 | 0.371506 |

| 4 | 98.99203 | 0.491697 | 0.127803 | 0.388474 |

| 5 | 98.97021 | 0.493587 | 0.128967 | 0.407234 |

| 6 | 98.96718 | 0.495325 | 0.129035 | 0.408459 |

| 7 | 98.96658 | 0.495329 | 0.129116 | 0.408979 |

| 8 | 98.96651 | 0.495345 | 0.129117 | 0.409027 |

| 9 | 98.96646 | 0.495364 | 0.129119 | 0.409054 |

| 10 | 98.96646 | 0.495366 | 0.129119 | 0.409056 |

| Null Hypothesis: | F-Statistic | Prob. |

|---|---|---|

| CASES does not Granger Cause BTC/EUR | 1.24033 | 0.2902 |

| BTC/EUR does not Granger Cause CASES | 1.28356 | 0.2779 |

| GOLD does not Granger Cause BTC/EUR | 0.34747 | 0.7066 |

| BTC/EUR does not Granger Cause GOLD | 0.00021 | 0.9998 |

| STOXX50 does not Granger Cause BTC/EUR | 0.90151 | 0.4066 |

| BTC/EUR does not Granger Cause STOXX50 | 0.82065 | 0.4407 |

| GOLD does not Granger Cause CASES | 0.29560 | 0.7442 |

| CASES does not Granger Cause GOLD | 0.40572 | 0.6667 |

| STOXX50 does not Granger Cause CASES | 0.21923 | 0.8032 |

| CASES does not Granger Cause STOXX50 | 3.32819 | 0.0366 ** |

| STOXX50 does not Granger Cause GOLD | 6.27341 | 0.0020 *** |

| GOLD does not Granger Cause STOXX50 | 1.13881 | 0.3210 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Karagiannopoulou, S.; Ragazou, K.; Passas, I.; Garefalakis, A.; Sariannidis, N. The Impact of the COVID-19 Pandemic on the Volatility of Cryptocurrencies. Int. J. Financial Stud. 2023, 11, 50. https://doi.org/10.3390/ijfs11010050

Karagiannopoulou S, Ragazou K, Passas I, Garefalakis A, Sariannidis N. The Impact of the COVID-19 Pandemic on the Volatility of Cryptocurrencies. International Journal of Financial Studies. 2023; 11(1):50. https://doi.org/10.3390/ijfs11010050

Chicago/Turabian StyleKaragiannopoulou, Sofia, Konstantina Ragazou, Ioannis Passas, Alexandros Garefalakis, and Nikolaos Sariannidis. 2023. "The Impact of the COVID-19 Pandemic on the Volatility of Cryptocurrencies" International Journal of Financial Studies 11, no. 1: 50. https://doi.org/10.3390/ijfs11010050

APA StyleKaragiannopoulou, S., Ragazou, K., Passas, I., Garefalakis, A., & Sariannidis, N. (2023). The Impact of the COVID-19 Pandemic on the Volatility of Cryptocurrencies. International Journal of Financial Studies, 11(1), 50. https://doi.org/10.3390/ijfs11010050