How Do Climate Concerns and Value Orientation Among Bankers Influence Agricultural Financing and Development?

Abstract

1. Introduction

1.1. Agriculture and Banking System in Bangladesh

1.2. Theoretical Perspective and Hypothesis Development

2. Methods

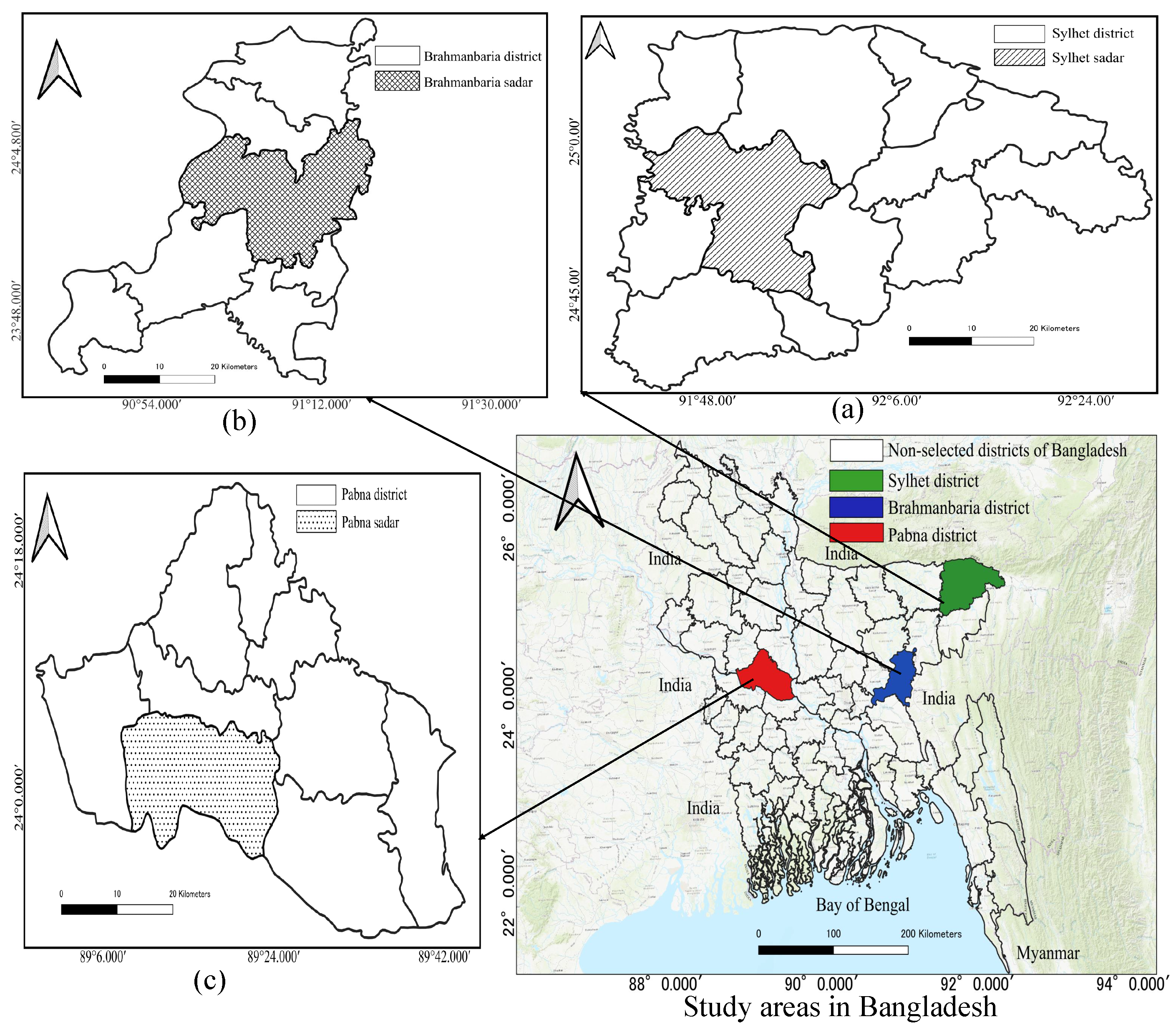

2.1. Study Area, Sample and Sampling Strategy

2.2. Key Variables

2.3. Statistical Analysis

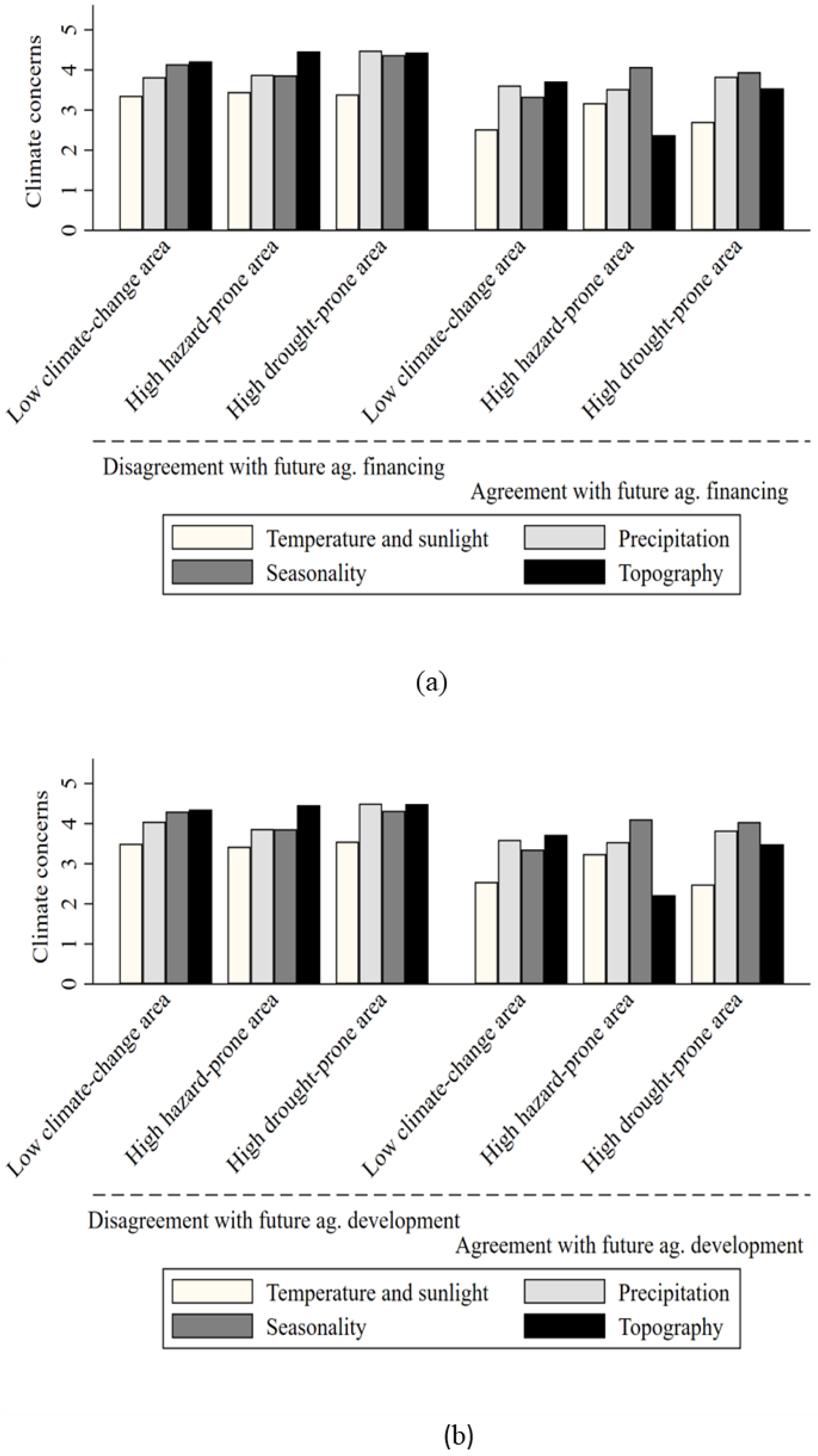

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Future Agricultural Financing (FAF) | ||||||

|---|---|---|---|---|---|---|

| Coefficient | Marginal Probability of Responses by a Five-Point Likert-Scale | |||||

| Model 1 | 1 | 2 | 3 | 4 | 5 | |

| Cognitive factors | ||||||

| Climate concerns | ||||||

| Temperature and sunlight | *** | 0.02 *** | 0.03 *** | ** | *** | ** |

| Precipitation | 0.01 | 0.01 | ||||

| Seasonality | 0.01 | 0.02 | ||||

| Topography | *** | 0.04 *** | 0.06 *** | *** | *** | *** |

| Prosocial attitude for future generations | 0.13 *** | *** | *** | 0.01 *** | 0.04 *** | 0.01 *** |

| Climate-change areas (r a = Low climate-change area)) | ||||||

| High hazard-prone area | *** | 0.38 *** | 0.18 *** | *** | *** | *** |

| High drought-prone area | *** | 0.23 *** | 0.25 *** | *** | *** | *** |

| Sociodemographic & bank characteristics | ||||||

| Age | 0.005 | 0.0003 | 0.001 | 0.0002 | ||

| Gender () | 0.29 | * | 0.02 | 0.08 * | 0.01 * | |

| Educational background () | 0.002 | 0.003 | ||||

| Bank type () | 0.06 | 0.004 | 0.02 | 0.003 | ||

| Bank fixed-asset collateral () | *** | 0.10 *** | 0.24 *** | 0.002 | *** | *** |

| Agricultural loan b | 0.02 | 0.001 | 0.005 | 0.001 | ||

| Future Agricultural Development (FAD) | ||||||

|---|---|---|---|---|---|---|

| Coefficient | Marginal Probability of Responses by a Five-Point Likert-Scale | |||||

| Model 1 | 1 | 2 | 3 | 4 | 5 | |

| Cognitive factors | ||||||

| Climate concerns | ||||||

| Temperature and sunlight | *** | 0.01 *** | 0.04 *** | *** | *** | *** |

| Precipitation | ** | 0.01 ** | 0.03 ** | * | ** | ** |

| Seasonality | 0.005 | 0.02 | ||||

| Topography | *** | 0.03 *** | 0.11 *** | *** | *** | *** |

| Prosocial attitude for future generations | 0.07 *** | *** | *** | 0.004 *** | 0.02 *** | 0.01 *** |

| Climate-change areas (r a = Low climate-change area) | ||||||

| High hazard-prone area | *** | 0.30 *** | 0.32 *** | *** | *** | *** |

| High drought-prone area | *** | 0.12 *** | 0.33 *** | *** | *** | *** |

| Sociodemographic & bank characteristics | ||||||

| Age | * | 0.001 | 0.004 * | * | * | |

| Gender () | 0.21 | 0.02 | 0.05 | 0.01 | ||

| Educational background () | 0.03 | 0.002 | 0.01 | 0.002 | ||

| Bank type () | 0.08 | 0.01 | 0.02 | 0.01 | ||

| Bank fixed-asset collateral () | *** | 0.04 *** | 0.21 *** | *** | *** | |

| Agricultural loan b | * | 0.002 * | 0.01 * | * | * | * |

References

- Durán-Sandoval, D.; Uleri, F.; Durán-Romero, G.; López, A. Food, climate change, and the challenge of innovation. Encyclopedia 2023, 3, 839–852. [Google Scholar] [CrossRef]

- Nicholls, N.; Alexander, L. Has the climate become more variable or extreme? Progress 1992–2006. Prog. Phys. Geogr. 2007, 31, 77–87. [Google Scholar] [CrossRef]

- Gumel, D. Assessing climate change vulnerability: A conceptual and theoretical review. J. Sustain. Environ. Manag. 2022, 1, 22–31. [Google Scholar]

- FAO. The Impact of Disasters on Agriculture and Food Security 2023— Avoiding and Reducing Losses Through Investment in Resilience; Technical Report; Food and Agriculture Organization: Rome, Italy, 2023. [Google Scholar]

- Alam, G.; Alam, K.; Mushtaq, S. Climate change perceptions and local adaptation strategies of hazard-prone rural households in Bangladesh. Clim. Risk Manag. 2017, 17, 52–63. [Google Scholar] [CrossRef]

- Asma, K.; Kotani, K. Salinity and water-related disease risk in coastal Bangladesh. EcoHealth 2021, 18, 61–75. [Google Scholar] [CrossRef] [PubMed]

- Chen, J.; Siddik, A.; Zheng, G.; Masukujjaman, M.; Bekhzod, S. The effect of green banking practices on banks’ environmental performance and green financing: An empirical study. Energies 2022, 15, 1292. [Google Scholar] [CrossRef]

- Buranatrakul, T.; Swierczek, F. Climate change strategic actions in the international banking industry. Glob. Bus. Rev. 2018, 19, 32–47. [Google Scholar] [CrossRef]

- Zheng, G.; Siddik, A.; Masukujjaman, M.; Fatema, N.; Alam, S. Green finance development in Bangladesh: The role of private commercial banks (PCBs). Sustainability 2021, 13, 795. [Google Scholar] [CrossRef]

- Hasan, M.; Al Amin, M.; Moon, Z.; Afrin, F. Role of environmental sustainability, psychological and managerial supports for determining bankers’ green banking usage behavior: An integrated framework. Psychol. Res. Behav. Manag. 2022, 15, 3751–3773. [Google Scholar] [CrossRef]

- Palmucci, D.; Ferraris, A. Climate change inaction: Cognitive bias influencing managers’ decision making on environmental sustainability choices. The role of empathy and morality with the need of an integrated and comprehensive perspective. Front. Psychol. 2023, 14, 1130059. [Google Scholar] [CrossRef]

- Syropoulos, S.; Markowitz, E. Responsibility towards future generations is a strong predictor of proenvironmental engagement. J. Environ. Psychol. 2024, 93, 102218. [Google Scholar] [CrossRef]

- Islam, N. Foreign Aid to Agriculture: Review of Facts and Analysis; Technical Report; IFPRI Discussion Paper No. 01053; International Food Policy Research Institute: Washington, DC, USA, 2011. [Google Scholar]

- Huang, J.; Wang, Y. Financing sustainable agriculture under climate change. J. Integr. Agric. 2014, 13, 698–712. [Google Scholar] [CrossRef]

- IPCC. Climate Change 2013: The Physical Science Basis; Technical Report, Working Group I Contribution to the Fifth Assessement Report; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2013. [Google Scholar]

- World Bank. World Development Report 2008: Agriculture for Development; Technical Report; World Bank: Washington, DC, USA, 2007. [Google Scholar]

- Hossain, M. Green Finance in Bangladesh: Policies, Institutions, and Challenges; Technical Report; Working Paper No. 892; Asian Development Bank Institute: Tokyo, Japan, 2018. [Google Scholar]

- Chowdhury, M. Agrarian Transition and Livelihoods of The Rural Poor: Agricultural Credit Market; Technical Report; Unnayan Onneshan; The Innovators: Dhaka, Bangladesh, 2009. [Google Scholar]

- Rahman, M. Policies and performances of agricultural/rural credit in Bangladesh: What is the influence on agricultural production? Afr. J. Agric. Res. 2011, 6, 6440–6452. [Google Scholar]

- Abraham, T.; Fonta, W. Climate change and financing adaptation by farmers in northern Nigeria. Financ. Innov. 2018, 4, 1–17. [Google Scholar] [CrossRef]

- Aiello, F. Experiences with Traditional Compensatory Finance Schemes and Lessons from FLEX; Technical Report; Working Paper No. 12; Department of Economics and Statistics, University of Calabria: Calabria, Italy, 2009. [Google Scholar]

- Nawaz, M.; Seshadri, U.; Kumar, P.; Aqdas, R.; Patwary, A.; Riaz, M. Nexus between green finance and climate change mitigation in N-11 and BRICS countries: Empirical estimation through difference in differences (DID) approach. Environ. Sci. Pollut. Res. 2021, 28, 6504–6519. [Google Scholar] [CrossRef]

- Zheng, G.; Siddik, A.B.; Masukujjaman, M.; Fatema, N. Factors affecting the sustainability performance of financial institutions in Bangladesh: The role of green finance. Sustainability 2021, 13, 10165. [Google Scholar] [CrossRef]

- Alauddin, M.; Biswas, J. Agricultural credit in Bangladesh: Trends, patterns, problems and growth impacts. Jahangirnagar Econ. Rev. 2014, 25, 125–138. [Google Scholar]

- Alauddin, M.; Sarker, M. Climate change and farm-level adaptation decisions and strategies in drought-prone and groundwater-depleted areas of Bangladesh: An empirical investigation. Ecol. Econ. 2014, 106, 204–213. [Google Scholar] [CrossRef]

- Ghosh, R.; Sen, K.; Riva, F. Behavioral determinants of nonperforming loans in Bangladesh. Asian J. Account. Res. 2020, 5, 327–340. [Google Scholar] [CrossRef]

- Kuenzi, M.; Schminke, M. Assembling fragments into a lens: A review, critique, and proposed research agenda for the organizational work climate literature. J. Manag. 2009, 35, 634–717. [Google Scholar] [CrossRef]

- Norton, T.; Zacher, H.; Ashkanasy, N. Organisational sustainability policies and employee green behaviour: The mediating role of work climate perceptions. J. Environ. Psychol. 2014, 38, 49–54. [Google Scholar] [CrossRef]

- Norton, T.; Parker, S.; Zacher, H.; Ashkanasy, N. Employee green behavior: A theoretical framework, multilevel review, and future research agenda. Organ. Environ. 2015, 28, 103–125. [Google Scholar] [CrossRef]

- Tian, H.; Zhang, J.; Li, J. The relationship between pro-environmental attitude and employee green behavior: The role of motivational states and green work climate perceptions. Environ. Sci. Pollut. Res. 2020, 27, 7341–7352. [Google Scholar] [CrossRef]

- Hasebrook, J.; Michalak, L.; Wessels, A.; Koenig, S.; Spierling, S.; Kirmsse, S. Green behavior: Factors influencing behavioral intention and actual environmental behavior of employees in the financial service sector. Sustainability 2022, 14, 10814. [Google Scholar] [CrossRef]

- Kartadjumena, E.; Rodgers, W. Executive compensation, sustainability, climate, environmental concerns, and company financial performance: Evidence from Indonesian commercial banks. Sustainability 2019, 11, 1673. [Google Scholar] [CrossRef]

- Burhan, A.; Rahmanti, W. The impact of sustainability reporting on company performance. J. Econ. Bus. Account. Ventur. 2012, 15, 257–272. [Google Scholar] [CrossRef]

- Barnett, M.; Archuleta, W.; Cantu, C. Politics, concern for future generations, and the environment: Generativity mediates political conservatism and environmental attitudes. J. Appl. Soc. Psychol. 2019, 49, 647–654. [Google Scholar] [CrossRef]

- Lagoarde-Segot, T. Sustainable finance. A critical realist perspective. Res. Int. Bus. Financ. 2019, 47, 1–9. [Google Scholar] [CrossRef]

- Syropoulos, S.; Markowitz, E. Our responsibility to future generations: The case for intergenerational approaches to the study of climate change. J. Environ. Psychol. 2023, 87, 102006. [Google Scholar] [CrossRef]

- Syropoulos, S.; Markowitz, E. Perceived responsibility towards future generations and environmental concern: Convergent evidence across multiple outcomes in a large, nationally representative sample. J. Environ. Psychol. 2021, 76, 101651. [Google Scholar] [CrossRef]

- Dienes, C. Actions and intentions to pay for climate change mitigation: Environmental concern and the role of economic factors. Ecol. Econ. 2015, 109, 122–129. [Google Scholar] [CrossRef]

- Masud, M.; Akhtar, R.; Afroz, R.; Al-Amin, A.; Kari, F. Pro-environmental behavior and public understanding of climate change. Mitig. Adapt. Strateg. Glob. Change 2015, 20, 591–600. [Google Scholar] [CrossRef]

- Yilmaz, V.; Can, Y. Impact of knowledge, concern and awareness about global warming and global climatic change on environmental behavior. Environ. Dev. Sustain. 2020, 22, 6245–6260. [Google Scholar] [CrossRef]

- Duijndam, S.; Beukering, P. Understanding public concern about climate change in Europe, 2008–2017: The influence of economic factors and right-wing populism. Clim. Policy 2021, 21, 353–367. [Google Scholar] [CrossRef]

- Katz, I.; Rauvola, R.; Rudolph, C.; Zacher, H. Employee green behavior: A meta-analysis. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1146–1157. [Google Scholar] [CrossRef]

- Rahman, M. Role of agriculture in Bangladesh economy: Uncovering the problems and challenges. Int. J. Bus. Manag. Invent. 2017, 6, 36–46. [Google Scholar]

- Husain, A.; Hossain, M. Bangladesh’s agricultural growth and development over fifty years. In Towards a Sustainable Economy: The Case of Bangladesh; Hossain, M., Ahmad, Q., Islam, M., Eds.; Routledge: London, UK, 2022; pp. 171–190. [Google Scholar]

- Yeasmin, S.; Haque, S.; Adnan, K.; Parvin, M.; Rahman, M.; Rahman, K.; Salman, M.; Hossain, M. Factors influencing demand for, and supply of, agricultural credit: A study from Bangladesh. J. Agric. Food Res. 2024, 16, 101173. [Google Scholar] [CrossRef]

- Kamal, Y. The development of banking sector in Bangladesh. Southeast Univ. J. Bus. Stud. 2006, 2, 241–251. [Google Scholar]

- Suzuki, Y.; Adhikary, B. A ‘bank rent’ approach to understanding the development of the banking system in Bangladesh. Contemp. South Asia 2010, 18, 155–173. [Google Scholar] [CrossRef]

- BB. Agricultural & Rural Credit Policy and Programme for the FY 2013–2014; Technical Report; Bangladesh Bank: Dhaka, Bangladesh, 2014. [Google Scholar]

- BB. Annual Report 2022–2023; Technical Report; Bangladesh Bank: Dhaka, Bangladesh, 2023. [Google Scholar]

- Azad, A.; Choudhury, N.; Wadood, S. Impact of agricultural credit on agricultural production: Evidence from Bangladesh. Soc. Sci. Rev. 2023, 40, 109–128. [Google Scholar] [CrossRef]

- Bandura, A. Social cognitive theory: An agentic perspective. Annu. Rev. Psychol. 2001, 52, 1–26. [Google Scholar] [CrossRef]

- Harris, J.; Carins, J.; Rundle-Thiele, S. Can social cognitive theory influence breakfast frequency in an institutional context: A qualitative study. Int. J. Environ. Res. Public Health 2021, 18, 11270. [Google Scholar] [CrossRef] [PubMed]

- Teo, S.; Gao, C.; Brennan, N.; Fava, N.; Simmons, M.; Baker, D.; Zbukvic, I.; Rickwood, D.; Brown, E.; Smith, C.; et al. Climate change concerns impact on young Australians’ psychological distress and outlook for the future. J. Environ. Psychol. 2024, 93, 102209. [Google Scholar] [CrossRef]

- Stern, P.; Dietz, T.; Abel, T.; Guagnano, G.; Kalof, L. A value-belief-norm theory of support for social movements: The case of environmentalism. Hum. Ecol. Rev. 1999, 6, 81–97. [Google Scholar]

- Stren, P. Toward a coherent theory of environmentally significant behaviour. J. Soc. Issues 2000, 56, 407–424. [Google Scholar] [CrossRef]

- Ghazali, E.; Nguyen, B.; Mutum, D.; Yap, S. Pro-environmental behaviours and value-belief-norm theory: Assessing unobserved heterogeneity of two ethnic groups. Sustainability 2019, 11, 3237. [Google Scholar] [CrossRef]

- Van der Linden, S. The social-psychological determinants of climate change risk perceptions: Towards a comprehensive model. J. Environ. Psychol. 2015, 41, 112–124. [Google Scholar] [CrossRef]

- Brügger, A.; Demski, C.; Capstick, S. How personal experience affects perception of and decisions related to climate change: A psychological view. Weather Clim. Soc. 2021, 13, 397–408. [Google Scholar] [CrossRef]

- Kluckhohn, F.; Strodtbeck, F. Variations in Value Orientations; Row, Peterson: New York, NY, USA, 1961. [Google Scholar]

- Gajanayake, R.; Johnson, L.; Daronkola, H.; Perera, C. Impact of households’ future orientation and values on their willingness to install solar photovoltaic systems. Sustainability 2024, 16, 8143. [Google Scholar] [CrossRef]

- Mostafizur, R.; Asma, K.; Islam, M.; Kotani, K. Drivers for sustainable food purchase intentions: Prosocial attitudes for future generations and environmental concerns. Future Foods 2025, 11, 100609. [Google Scholar] [CrossRef]

- ADB. Bangladesh Climate and Disaster Risk Atlas: Hazards—Volume 1; Technical Report; Planning Commission, Ministry of Planning and Asian Development Bank: Dhaka, Bangladesh; Manila, Philippines, 2021. [Google Scholar]

- Rahaman, K.; Ahmed, F.; Nazrul, I. Modeling on climate induced drought of north-western region, Bangladesh. Model. Earth Syst. Environ. 2016, 2, 1–21. [Google Scholar] [CrossRef]

- BBS. Report on Agriculture and Rural Statistics 2018; Technical Report; Bangladesh Bureau of Statistics, Statistics and Informatics Division, Ministry of Planning: Dhaka, Bangladesh, 2019. [Google Scholar]

- BB. Introduction—Bangladesh Bank; Technical Report; Bangladesh Bank: Dhaka, Bangladesh, 2015. [Google Scholar]

- Bujang, M.; Sa’at, N.; Bakar, T.; Joo, L. Sample size guidelines for logistic regression from observational studies with large population: Eemphasis on the accuracy between statistics and parameters based on real life clinical data. Malays. J. Med. Sci. 2018, 25, 122. [Google Scholar] [CrossRef] [PubMed]

- Morselli, D.; Passini, S. Measuring prosocial attitudes for future generations: The social generativity scale. J. Adult Dev. 2015, 22, 173–182. [Google Scholar] [CrossRef]

- Barnett, M.; Vleet, S.; Cantu, C. Gratitude mediates perceptions of previous generations’ prosocial behaviors and prosocial attitudes toward future generations. J. Posit. Psychol. 2021, 16, 54–59. [Google Scholar] [CrossRef]

- Nunnally, J. Psychometric Theory, 2nd ed.; McGraw-Hill: New York, NY, USA, 1978. [Google Scholar]

- Schmitt, N. Uses and abuses of coefficient alpha. Psychol. Assess. 1996, 8, 350. [Google Scholar] [CrossRef]

- Briggs, S.; Cheek, J. The role of factor analysis in the development and evaluation of personality scales. J. Personal. 1986, 54, 106–148. [Google Scholar] [CrossRef]

- Field, A. Discovering Statistics Using SPSS, 4th ed.; SAGE: London, UK, 2013. [Google Scholar]

- Wooldridge, J. Econometric Analysis of Cross Section and Panel Data; MIT Press: Cambridge, MA, USA, 2010. [Google Scholar]

- Wooldridge, J. Introductory Econometrics: A Modern Approach; Cengage Learning: Boston, MA, USA, 2019. [Google Scholar]

- Cameron, A.; Trivedi, P. Microeconometrics Using Stata: Cross-Sectional and Panel Regression Methods; Stata Press: College Station, TX, USA, 2022; Volume I. [Google Scholar]

- Long, J.; Freese, J. Regression Models for Categorical Dependent Variables Using Stata; Stata Press: College Station, TX, USA, 2006; Volume 7. [Google Scholar]

- Islam, M.; Kotani, K.; Managi, S. Nature dependence and seasonality change perceptions for climate adaptation and mitigation. Econ. Anal. Policy 2024, 81, 34–44. [Google Scholar] [CrossRef]

- Zhao, Y.; Liu, Y.; Dong, L.; Sun, Y.; Zhang, N. The effect of climate change on firms’ debt financing costs: Evidence from China. J. Clean. Prod. 2024, 434, 140018. [Google Scholar] [CrossRef]

- Wu, Q.; Shahbaz, M.; Kyriakou, I. Temperature fluctuations, climate uncertainty, and financing hindrance. J. Reg. Sci. 2025, 65, 112–134. [Google Scholar] [CrossRef]

- Barbier, E. The economic determinants of land degradation in developing countries. Philos. Trans. R. Soc. Lond. Ser. Biol. Sci. 1997, 352, 891–899. [Google Scholar] [CrossRef]

- Islam, M.; Kotani, K. Changing seasonality in Bangladesh. Reg. Environ. Change 2016, 16, 585–590. [Google Scholar] [CrossRef]

- Cadilha, S.; Vaz, S. Prospection as a sustainability virtue: Imagining futures for intergenerational ethics. Z. Ethik Moralphilosophie 2023, 6, 293–309. [Google Scholar] [CrossRef]

- Barberis, N. Thirty years of prospect theory in economics: A review and assessment. J. Econ. Perspect. 2013, 27, 173–196. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. Prospect theory: An analysis of decision under risk. In Handbook of the Fundamentals of Financial Decision Making: Part I; World Scientific: Singapore, 2013; pp. 99–127. [Google Scholar]

- Osberghaus, D. Prospect theory, mitigation and adaptation to climate change. J. Risk Res. 2017, 20, 909–930. [Google Scholar] [CrossRef]

- Gonzalez-Ramirez, J.; Arora, P.; Podesta, G. Using insights from prospect theory to enhance sustainable decision making by agribusinesses in Argentina. Sustainability 2018, 10, 2693. [Google Scholar] [CrossRef]

- Godefroid, M.; Plattfaut, R.; Niehaves, B. How to measure the status quo bias? A review of current literature. Manag. Rev. Q. 2023, 73, 1667–1711. [Google Scholar] [CrossRef]

- Mazutis, D.; Eckardt, A. Sleepwalking into catastrophe: Cognitive biases and corporate climate change inertia. Calif. Manag. Rev. 2017, 59, 74–108. [Google Scholar] [CrossRef]

- Keh, H.; Foo, M.; Lim, B. Opportunity evaluation under risky conditions: The cognitive processes of entrepreneurs. Entrep. Theory Pract. 2002, 27, 125–148. [Google Scholar] [CrossRef]

- McFadden, C. Implicit bias training is dead, long live implicit bias training: The evolving role of human resource development in combatting implicit bias within organisations. In The Emerald Handbook of Work, Workplaces and Disruptive Issues in HRM; Emerald Publishing Limited: Bingley, UK, 2022; pp. 381–396. [Google Scholar]

- Enke, B.; Gneezy, U.; Hall, B.; Martin, D.; Nelidov, V.; Offerman, T.; Van, J. Cognitive biases: Mistakes or missing stakes? Rev. Econ. Stat. 2023, 105, 818–832. [Google Scholar] [CrossRef]

- Sprengel, D.; Busch, T. Stakeholder engagement and environmental strategy—The case of climate change. Bus. Strategy Environ. 2011, 20, 351–364. [Google Scholar] [CrossRef]

- Dixon-Fowler, H.; Slater, D.; Johnson, J.; Ellstrand, A.; Romi, A. Beyond “Does it pay to be green?” A meta-analysis of moderators of the CEP—CFP relationship. J. Bus. Ethics 2013, 112, 353–366. [Google Scholar] [CrossRef]

- Bătae, O.; Dragomir, V.; Feleagă, L. The relationship between environmental, social, and financial performance in the banking sector: A European study. J. Environ. Psychol. 2021, 290, 125791. [Google Scholar] [CrossRef]

- Grosbois, D.; Fennell, D. Determinants of climate change disclosure practices of global hotel companies: Application of institutional and stakeholder theories. Tour. Manag. 2022, 88, 104404. [Google Scholar] [CrossRef]

- Zakhem, A.; Palmer, D. Normative stakeholder theory. In Stakeholder Management (Business and Society 360); Emerald Publishing Limited: Bingley, UK, 2017; Volume 1, Chapter 3; pp. 49–73. [Google Scholar]

- Valentinov, V.; Hajdu, A. Integrating instrumental and normative stakeholder theories: A systems theory approach. J. Organ. Change Manag. 2021, 34, 699–712. [Google Scholar] [CrossRef]

- Bell, W. Foundations of Futures Studies: Human Science for a New Era; Transaction Publishers: Piscataway, NJ, USA, 2009; Volume 1. [Google Scholar]

- Van der Helm, R. The vision phenomenon: Towards a theoretical underpinning of visions of the future and the process of envisioning. Futures 2009, 41, 96–104. [Google Scholar] [CrossRef]

- Phdungsilp, A. Futures studies’ backcasting method used for strategic sustainable city planning. Futures 2011, 43, 707–714. [Google Scholar] [CrossRef]

- Amer, M.; Daim, T.; Jetter, A. A review of scenario planning. Futures 2013, 46, 23–40. [Google Scholar] [CrossRef]

- Szpunar, K.; Spreng, R.; Schacter, D. A taxonomy of prospection: Introducing an organizational framework for future-oriented cognition. Proc. Natl. Acad. Sci. USA 2014, 111, 18414–18421. [Google Scholar] [CrossRef]

- González-Ricoy, I.; Gosseries, A. Institutions for Future Generations; Oxford University Press: Oxford, UK, 2016. [Google Scholar]

- Bibri, S.; Krogstie, J. Generating a vision for smart sustainable cities of the future: A scholarly backcasting approach. Eur. J. Futur. Res. 2019, 7, 1–20. [Google Scholar] [CrossRef]

- Ziegler, R.; Oliveira, L. Backcasting for sustainability—An approach to education for sustainable development in management. Int. J. Manag. Educ. 2022, 20, 100701. [Google Scholar] [CrossRef]

- Vecchiato, R. Environmental uncertainty, foresight and strategic decision making: An integrated study. Technol. Forecast. Soc. Change 2012, 79, 436–447. [Google Scholar] [CrossRef]

- Cook, C.; Inayatullah, S.; Burgman, M.; Sutherland, W.; Wintle, B. Strategic foresight: How planning for the unpredictable can improve environmental decision-making. Trends Ecol. Evol. 2014, 29, 531–541. [Google Scholar] [CrossRef]

- Tuominen, A.; Tapio, P.; Varho, V.; Järvi, T.; Banister, D. Pluralistic backcasting: Integrating multiple visions with policy packages for transport climate policy. Futures 2014, 60, 41–58. [Google Scholar] [CrossRef]

- Wodak, J.; Neale, T. A critical review of the application of environmental scenario exercises. Futures 2015, 73, 176–186. [Google Scholar] [CrossRef]

- Soria-Lara, J.; Banister, D. Collaborative backcasting for transport policy scenario building. Futures 2018, 95, 11–21. [Google Scholar] [CrossRef]

- Lacroix, D.; Laurent, L.; Menthière, N.; Schmitt, B.; Béthinger, A.; David, B.; Didier, C.; Châtelet, J. Multiple visions of the future and major environmental scenarios. Technol. Forecast. Soc. Change 2019, 144, 93–102. [Google Scholar] [CrossRef]

- Timilsina, R.; Nakagawa, Y.; Kotani, K. Exploring the possibility of linking and incorporating future design in backcasting and scenario planning. Sustainability 2020, 12, 9907. [Google Scholar] [CrossRef]

- Pandit, A.; Nakagawa, Y.; Timilsina, R.; Kotani, K.; Saijo, T. Taking the perspectives of future generations as an effective method for achieving sustainable waste management. Sustain. Prod. Consum. 2021, 27, 1526–1536. [Google Scholar] [CrossRef]

- Shahen, M.; Kotani, K.; Saijo, T. Intergenerational sustainability is enhanced by taking the perspective of future generations. Sci. Rep. 2021, 11, 2437. [Google Scholar] [CrossRef]

- Haque, M.; Murtaz, M. Green financing in Bangladesh. In Proceedings of the International Conference on Finance for Sustainable Growth and Development; Jahur, M., Uddin, S., Eds.; Department of Finance, Faculty of Business Administration, University of Chittagong: Chittagong, Bangladesh, 2018; pp. 82–89. [Google Scholar]

- Volz, U.; Böhnke, J.; Knierim, L.; Richert, K.; Roeber, G.; Eidt, V. Financing the Green Transformation: How to Make Green Finance Work in Indonesia; Springer: Berlin/Heidelberg, Germany, 2015. [Google Scholar]

- Khairunnessa, F.; Vazquez-Brust, D.; Yakovleva, N. A review of the recent developments of green banking in Bangladesh. Sustainability 2021, 13, 1904. [Google Scholar] [CrossRef]

| Variables | Description |

|---|---|

| Dependent variables | |

| Future agricultural financing (FAF) | If bankers do not disagree about the future profitability of agricultural financing, then the value is 1; otherwise it is 0. |

| Future agricultural development (FAD) | If bankers do not disagree about the future development of agriculture, then the value is 1; otherwise it is 0. |

| Independent variables | |

| Cognitive factors | |

| Climate concerns | |

| Temperature and sunlight | This is a value for measuring concern about temperature and sunlight, ranging from 0 to 5, with a high value indicating high concern. |

| Precipitation | This is a value for measuring concern about precipitation, ranging from 0 to 5, with a high value indicating high concern. |

| Seasonality | This is a value for measuring concern about seasonality, ranging from 0 to 5, with a high value indicating high concern. |

| Topography | This is a value for measuring concern about topography, ranging from 0 to 5, with a high value indicating high concern. |

| Prosocial attitude for future generations | This score is based on 6 questions, with possible total scores ranging from 6 to 30. |

| Climate-change areas (Base group = Low climate-change area) | |

| High hazard-prone area | This variable takes a value of 1 when bankers live in a high hazard-prone area, otherwise 0. |

| High drought-prone area | This variable takes a value of 1 when bankers live in a high drought-prone area, otherwise 0. |

| Sociodemographic & bank characteristics | |

| Age | Age is defined as banker’s age in years. |

| Gender | Gender is a dummy variable that takes a value of 1 when the banker is male, otherwise 0. |

| Educational background | It is a dummy variable that takes a value of 1 if the banker has business-related education, otherwise 0. |

| Bank type | Bank type represents a dummy variable that takes a value of 1 when a banker is from a private bank, otherwise 0. |

| Bank fixed-asset collateral | It is a dummy variable that takes a value of 1 if the bank has a fixed-asset collateral system to provide loans, otherwise 0. |

| Agricultural loan | Total amount of current year loans in BDT a |

| Climate-Change Areas | Overall | p-Value | |||

|---|---|---|---|---|---|

| Low Climate-Change | High Hazard-Prone | High Drought-Prone | |||

| Cognitive factors | |||||

| Climate concerns | |||||

| Temperature and sunlight | |||||

| Average (Median) a | 2.65 (3.00) | 3.39 (4.00) | 3.13 (3.00) | 3.06 (3.00) | |

| SD b | 1.50 | 1.16 | 1.40 | 1.40 | 0.01 c |

| Precipitation | |||||

| Average (Median) | 3.65 (4.00) | 3.80 (4.00) | 4.23 (4.00) | 3.93 (4.00) | |

| SD | 1.21 | 1.15 | 0.80 | 1.07 | 0.01 c |

| Seasonality | |||||

| Average (Median) | 3.46 (4.00) | 3.92 (4.00) | 4.21 (4.00) | 3.90 (4.00) | |

| SD | 1.55 | 0.86 | 0.77 | 1.13 | 0.01 c |

| Topography | |||||

| Average (Median) | 3.79 (4.00) | 3.96 (4.00) | 4.09 (4.00) | 3.96 (4.00) | |

| SD | 1.15 | 1.51 | 1.35 | 1.34 | 0.01 c |

| Prosocial attitude for future generations | |||||

| Average (Median) | 25.14 (25.00) | 25.16 (25.00) | 24.73 (25.00) | 24.97 (25.00) | |

| SD | 2.73 | 1.62 | 1.70 | 2.05 | 0.01 c |

| Sociodemographic & bank characteristics | |||||

| Age | |||||

| Average (Median) | 39.14 (39.00) | 37.17 (37.00) | 38.87 (39.00) | 38.48 (39.00) | |

| SD | 7.25 | 6.05 | 6.02 | 6.47 | 0.02 c |

| Gender () | |||||

| Average (Median) | 0.86 (1.00) | 0.96 (1.00) | 0.95 (1.00) | 0.93 (1.00) | |

| SD | 0.35 | 0.19 | 0.22 | 0.26 | 0.01 d |

| Educational background () | |||||

| Average (Median) | 0.46 (0.00) | 0.49 (0.00) | 0.44 (0.00) | 0.46 (0.00) | |

| SD | 0.50 | 0.50 | 0.50 | 0.50 | 0.60 d |

| Bank type () | |||||

| Average (Median) | 0.72 (1.00) | 0.68 (1.00) | 0.64 (1.00) | 0.68 (1.00) | |

| SD | 0.45 | 0.47 | 0.48 | 0.47 | 0.21 d |

| Bank fixed-asset collateral () | |||||

| Average (Median) | 0.73 (1.00) | 0.84 (1.00) | 0.80 (1.00) | 0.79 (1.00) | |

| SD | 0.45 | 0.36 | 0.40 | 0.41 | 0.03 d |

| Agricultural loan | |||||

| Average (Median) | 5,259,093 (2,000,000) | 10,800,000 (2,800,000) | 44,100,000 (5,603,289) | 23,000,000 (3,500,000) | |

| SD | 8,237,631 | 32,300,000 | 144,000,000 | 96,400,000 | 0.01 c |

| Sample size | 181 | 166 | 249 | 596 | |

| Climate-Change Areas | Overall | |||

|---|---|---|---|---|

| Low Climate-Change Area | High Hazard-Prone Area | High Drought-Prone Area | ||

| Future agricultural financing (FAF) | ||||

| Average | 0.85 | 0.24 | 0.39 | 0.48 |

| Median | 1.00 | 0.00 | 0.00 | 0.00 |

| SD a | 0.36 | 0.43 | 0.49 | 0.50 |

| Min | 0.00 | 0.00 | 0.00 | 0.00 |

| Max | 1.00 | 1.00 | 1.00 | 1.00 |

| Future agricultural development (FAD) | ||||

| Average | 0.89 | 0.22 | 0.40 | 0.49 |

| Median | 1.00 | 0.00 | 0.00 | 0.00 |

| SD | 0.31 | 0.42 | 0.49 | 0.50 |

| Min | 0.00 | 0.00 | 0.00 | 0.00 |

| Max | 1.00 | 1.00 | 1.00 | 1.00 |

| Sample size | 181 | 166 | 249 | 596 |

| Future Agricultural Financing (FAF) | Future Agricultural Development (FAD) | |||||||

|---|---|---|---|---|---|---|---|---|

| Coefficient | ME a | Coefficient | ME | Coefficient | ME | Coefficient | ME | |

| Model 1-1 | Model 1-2 | Model 1-3 | Model 1-4 | Model 2-1 | Model 2-2 | Model 2-3 | Model 2-4 | |

| Cognitive factors | ||||||||

| Climate concerns | ||||||||

| Temperature and sunlight | ** | ** | ** | ** | *** | *** | *** | *** |

| Precipitation | ** | ** | * | * | *** | *** | *** | *** |

| Seasonality | 0.01 | 0.002 | 0.0003 | 0.0001 | ||||

| Topography | *** | *** | *** | *** | *** | *** | *** | *** |

| Prosocial attitude for future generations | 0.17 *** | 0.04 *** | 0.14 ** | 0.03 ** | 0.14 ** | 0.03 ** | 0.11 * | 0.03 * |

| Climate-change areas (r b = Low climate-change area) | ||||||||

| High hazard-prone area | *** | *** | *** | *** | *** | *** | *** | *** |

| High drought-prone area | *** | *** | *** | *** | *** | *** | *** | *** |

| Sociodemographic & bank characteristics | ||||||||

| Age | ||||||||

| Gender () | 0.27 | 0.07 | ||||||

| Educational background () | 0.18 | 0.04 | 0.07 | 0.02 | ||||

| Bank type () | 0.22 | 0.05 | 0.29 | 0.07 | ||||

| Bank fixed-asset collateral () | *** | *** | *** | *** | ||||

| Agricultural loan c | 0.04 | 0.01 | 0.03 | 0.01 | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Asma, K.M.; Masud, M.R.; Kotani, K. How Do Climate Concerns and Value Orientation Among Bankers Influence Agricultural Financing and Development? Climate 2025, 13, 98. https://doi.org/10.3390/cli13050098

Asma KM, Masud MR, Kotani K. How Do Climate Concerns and Value Orientation Among Bankers Influence Agricultural Financing and Development? Climate. 2025; 13(5):98. https://doi.org/10.3390/cli13050098

Chicago/Turabian StyleAsma, Khatun Mst, Md Rony Masud, and Koji Kotani. 2025. "How Do Climate Concerns and Value Orientation Among Bankers Influence Agricultural Financing and Development?" Climate 13, no. 5: 98. https://doi.org/10.3390/cli13050098

APA StyleAsma, K. M., Masud, M. R., & Kotani, K. (2025). How Do Climate Concerns and Value Orientation Among Bankers Influence Agricultural Financing and Development? Climate, 13(5), 98. https://doi.org/10.3390/cli13050098