1. Introduction

The American Statistical Association statement on “Statistical Significance and

P-values” (

Wasserstein and Lazar 2016) aimed at reminding the statistics community about a number of pitfalls that are commonly fallen into, in the everyday use of

p-values. The statement and accompanying introduction also pointed to the rich history of the statisticians who have articulated the issues, providing a long list of references. This raises a question: If no one has listened before, will they be swayed by this latest exhortation? Perhaps a numerical example might be more convincing—an example that illustrates that the issue is less that the common use of

p-values is philosophically misguided, and more that the numbers can just be completely wrong (for evidence that these issues are of real, applied importance in economics and finance see

Kim and Ji (

2015).

One way in which to understand the misuse of the p-value is as a misapplication of the modus tollens argument. Suppose we had data that would prove a null hypothesis to be true or false, with certainty. If the null hypothesis is true, then the data would support the null with certainty. So if the data did not support the null, we would know that the null is false. However, such logic does not apply to statistical reasoning, where the data does not give answers with certainty. If the null is true, then a small p-value is unlikely. The fallacy of applying modus tollens is that it may be that if the null is false, then a small p-value is also unlikely.

Problems with the misuse of

p-values have been understand for a very long time—at least in principle. The purpose here is to provide a new-but-simple example of the disconnect between a

p-value and the probability that a null hypothesis is true—adding to the long list of existing examples. Beginning with a quick review of what has been said in the past may be useful. There are a number of concerns with regard to

p-values, which have been discussed at least as far back as

Berkson (

1942), and as recently as

Wasserstein and Lazar (

2016). The latter also includes many references. I focus here solely on the issue that a

p-value is not designed to speak to the relative merits of a null hypothesis versus the alternative.

Nickerson (

2000) explains the problem, and gives many further references.

Trafimow (

2003) puts the matter succinctly, “although one can calculate the probability of obtaining a finding given that the null hypothesis is true, this is not equivalent to calculating the probability that the null hypothesis is true given that one has obtained a finding.”

1 Trafimow (

2005) is more pointed, writing, “A

p-value can be a dramatic overestimate or underestimate of the desired posterior probability of the null hypothesis depending on the prior probability of the null hypothesis and the probability of the finding given that the null hypothesis is not true.”

Dickey (

1977) points out that the area under the tail is not, in general, a good approximation to the Bayes factor.

Berger and Sellke (

1987) summarize the issue nicely, writing that “actual evidence against a null (as measured, say, by posterior probability or comparative likelihood) can differ by an order of magnitude from the

p-value. … The overall conclusion is that

p-values can be highly misleading measures of the evidence provided by the data against the null hypothesis”

Trafimow and Rice (

2009) show that the

p-value need not even be very highly correlated with the true probability of the null hypothesis.

The point addressed here is the ASA’s second principle, “

P-values do not measure the probability that the studied hypothesis is true…” Or as

E.S. Pearson (

1938) wrote eight decades ago, “Gosset … had a tremendous influence on the … idea which has formed the basis of all the…researches of Neyman and myself. It is the simple suggestion that the only valid reason for rejecting a statistical hypothesis is that some alternative hypothesis explains the events with a greater degree of probability.”

Hubbard and Bayarri (

2003) explain the difference between Fisher’s advocacy of the

p-value and the idea of Neyman and Pearson to compare a null hypothesis to an alternative, offering historical perspectives as well.

Robinson and Wainer (

2002) discuss a number of issues with the use of

p-values, including the point that “… many users of NHST [Null Hypothesis Significance Testing] interpret the result as the probability of the null hypothesis based on the data observed. … This error suggests that users really want to make a different kind of inference—a probabilistic statement of the likelihood of the hypothesis”, which is the point that we pursue below.

2 Hubbard and Lindsay (

2008) write that “

P-Values Exaggerate the Evidence Against the Null Hypothesis”. This is the most damning criticism of the

p-value as a measure of evidence.” (Emphasis in the original). We shall see, however, that it is also possible for a

p-value to understate the evidence against the null.

2. The General Problem

Wasserstein and Lazar (

2016) succinctly remind everyone that “Informally, a

p-value is the probability under a specified statistical model that a statistical summary of the data … would be equal to or more extreme than its observed value.” Following

Trafimow (

2005), suppose that we call finding that probability to be equal to or more extreme to be the “finding”, or simply,

. The “philosophical” problem is that

p-values summarize

, while we are, with rare exception, interested in

. The two are related by Bayes’ Theorem, but they are not the same. Pointedly, they need not even be close. As a reminder, the

p-value is calculated by assuming that the null hypothesis is true, and then calculating the probability that some observed outcome would come about under the null hypothesis. The classic case is to calculate the probability that an estimated parameter should be as far or farther from a point that is specified by the null, as is the observed estimate. The

p-value is

, but from Bayes’ theorem:

The generic reason that the p-value need not be close to the conditional probability of the hypothesis is that the p-value is missing the other two elements in Equation (1). Since this is obvious, it is probably worth commenting on why the deployment of the p-value remains nearly pervasive. The requirement to specify is sometimes viewed as non-scientific, as it comes from something other than the data at hand. Also, the specification of generally requires considerable information about the alternative hypothesis, certainly much more than merely the idea that the alternative is anything other than the null.

The notion that the p-value summarizes is an oversimplification, of course, as it ignores conditioning on the econometric specification of the entire estimate. Really, the p-value gives . Conditioning on specification carries through to the left side of Equation (1), but in what follows, I will omit it for the sake of brevity. In addition, when one applies Bayes’ Theorem, the result is really conditioned on the prior specified, although this is traditionally omitted from the notation. It is also true that frequentists and Bayesians sometimes disagree over the entire nature of the statistical enterprise, including even the meaning of “probability.” Nothing in what follows speaks to these deeper issues.

3. A Simple Example of the Problem

Consider the decision of whether a coin is fair or not, based on the number of heads, , observed after tosses. If there are 26 heads out of 64 tosses, the p-value is 0.08 (so the null seems very unlikely). Though a bit short of the magic number 0.05, that’s a sufficiently low p-value that a sympathetic editor might consider publication. Doing the Bayes’ Theorem calculation requires some additional assumptions, but arguably innocuous assumptions suggest that the coin is more likely than not, fair, —a strikingly different conclusion (“Arguably innocuous” being taken here as the prior odds for the coin being fair being 50/50, and that if the coin is not fair, all we know is that the probability of a head is between zero and one). Note that since the posterior is not far from the prior, we would conclude that the data is not very informative, which is probably not the conclusion one would draw from looking at the 0.08 p-value.

In this example, the studied hypothesis is that the mean chance of a head is

, and that the

p-value is

, where

is the cdf (cumulative distribution function) of the binomial distribution. Bayes Theorem gives us

as a function of the binomial probability mass function

, and a prior over

,

.

Unlike the formula for calculating the

p-value, here, the answer requires some extra inputs. Most researchers would probably agree that the probability of a head is between zero and one, so that outside that range,

equals zero. Beyond that, we probably want to put some finite mass onto the studied hypothesis.

might be thought of as neutral.

3 Also, we might be as ignorant as possible about alternative values, by spreading the rest of the mass uniformly between the limits, so between zero and one,

. This gives:

Using these assumptions gives us the

value given above. Of course, varying counts of heads give different probabilities and

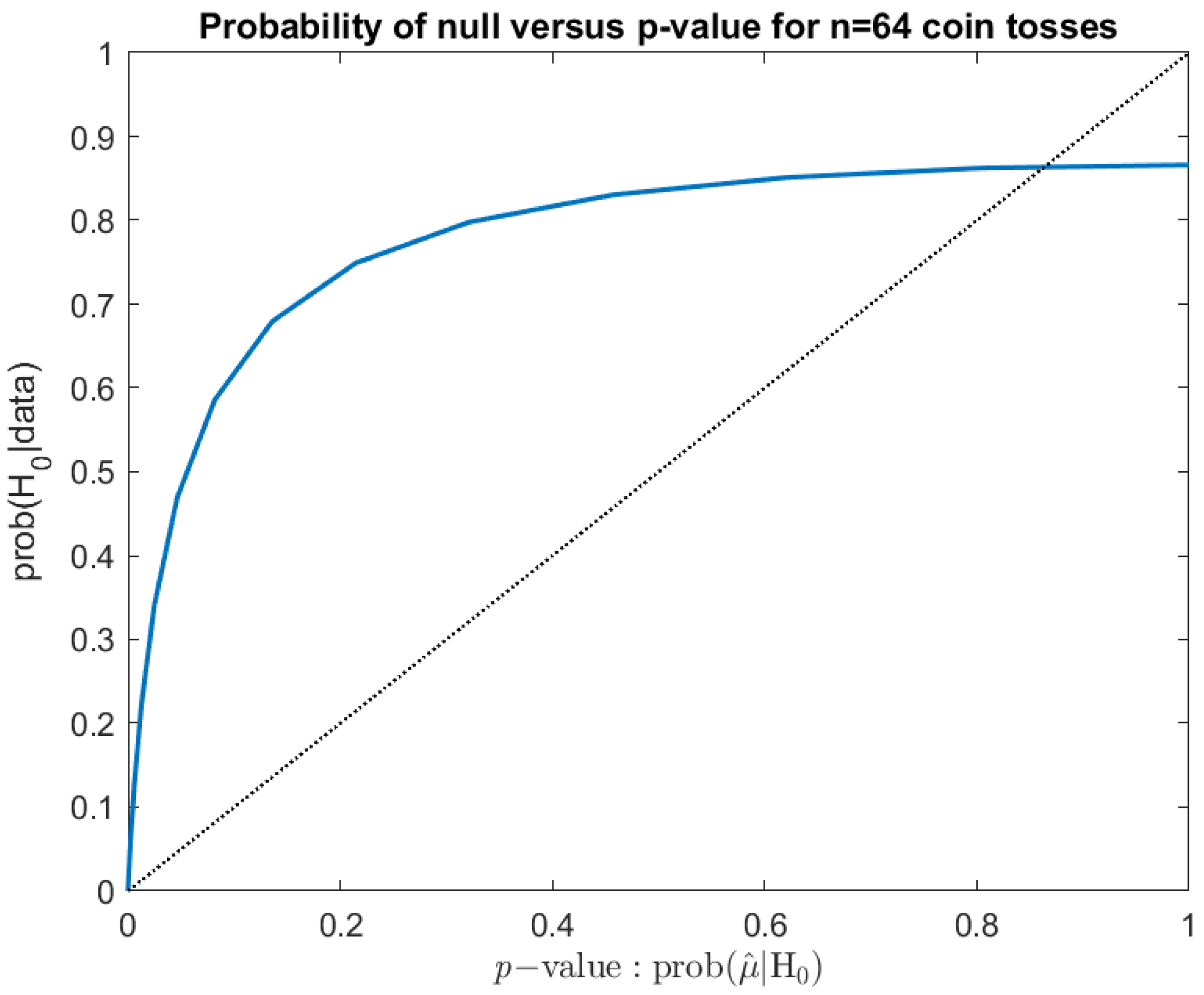

p-values, with the relation between the two for the 64 coin tosses shown in

Figure 1. If the

p-value gave the probability that the hypothesis were true, the plot would lie along the 45° line. However, it does not do so. Regardless, the more important lesson is that the curve is often very far from the 45° line, and indeed, it can lie either above or below.

Different priors do give different probabilities for the studied hypothesis, so there may well be a prior for which the p-value does coincide with the correct probability for the studied hypothesis. In the example here, if we put a prior weight, , on the fair coin that is equal to 0.04, we obtain a probability that is equal to the 0.08 p-value. Still, it seems likely that a p-valuista who rejects a fair coin did not intend to declare a prior of 96 percent against the coin being fair.

{kind=link}