1. Introduction

Elliott (1998) and

Cavanagh et al. (1995) investigated the test on a coefficient of a cointegrating relation in the presence of a near unit root in a bivariate cointegrating regression. They show convincingly that when inference on the coefficient is performed as if the process has a unit root, then the size distortion is serious, see top panel of

Figure A1 for a reproduction of their results. This paper analyses the

p-dimensional cointegrated VAR model with

r cointegrating relations under local alternatives

where

are

and

is i.i.d.

. It is assumed that

and

are known

matrices of rank

and

c is

and an unknown parameter, such that the model allows for a whole matrix,

of near unit roots. We consider below the likelihood ratio test,

for a given value of

calculated as if

that is, as if we have a CVAR with rank

The properties of the test

can be very bad, when the actual data generating process (DGP) is a slight perturbation of the process generated by the model specified by

. The matrix

describes a surface in the space of

matrices of dimension

. Therefore a model is formulated that in some particular “directions”, given by the matrix

has a small perturbation of the order of

and

extra parameters,

c, that are used to describe the near unit roots.

A similar model could be suggested for near unit roots in the

model, see

Di Iorio et al. (2016), but this will not be attempted here.

The model (

1) contains as a special case the DGP used for the simulations in

Elliott (1998), whe the errors are i.i.d. Gaussian and no deterministic components are present. The likelihood ratio test,

for

equal to a given value, is derived assuming that

and analyzed when in fact near unit roots are present,

. The parameters

and

can be estimated consistently, but

c cannot, and this is what causes the bad behaviour of

The matrix

is an invertible function of the

parameters

see Lemma 1, so that the Gaussian maximum likelihood estimator in model (

1) is least squares, and their limit distributions are found in Theorem 2. The main contribution of this paper, however, is a simulation study for the bivariate VAR with

,

It is shown that two of the methods introduced by

McCloskey (2017, Theorems Bonf and Bonf -Adj), for allowing the critical value for

to depend on the estimator of

give a much better solution to inference on

in the case of a near unit root. The results of

McCloskey (2017) also allow for multivariate parameters and for more complex adjustments, but in the present paper we focus for the simulations on the case with

and

so there is only one parameter in

c. In case

the matrix

is linear in

and for

it has an extra unit root. Therefore there is a near unit root for

, and we choose the vector

such

corresponds to the non-explosive near unit roots of interest.

The assumption that

and

are known is satisfied under the null, in the DGP analyzed by Elliott, see (

15) and (16). This is of course convenient, because

as free parameters, are not estimable.

Let

denote the parameters

and

and let

and

denote the maximum likelihood estimators in model (

1). For a given

(here

or

the quantile

is defined by

. Simulations show that the quantile is increasing in

and solving the inequality for

a

confidence interval,

is defined for

c. For given

(here

or

the quantile

is defined by

and

McCloskey (2017) suggests replacing the critical value

by the stochastic critical value

or introducing the optimal

by solving the equation

for a given nominal size

(here 10%).

These methods are explained and implemented by a simulation study, and it is shown that they offer a solution to the problem of inference on in the presence of a near unit root.

3. Critical Value Adjustment for Test on in the CVAR with near Unit Roots

3.1. Bonferroni Bounds

In this section the method of

McCloskey (2017, Theorem Bonf) is illustrated by a number of simulation experiments. The simulations are performed with data generated by a bivariate model (

1), where

and

The direction

is chosen such that

The test

for a given value of

is calculated assuming

, see (

6). The simulations of

Elliott (1998), see

Section 3.3, show that there may be serious size distortions of the test, depending on the value of

c and

, if the test is based on the quantiles from the asymptotic

distribution.

The methods of

McCloskey (2017) consists in this case of replacing the

critical value with a stochastic critical value depending on

in order to control the rejection probability under the null hypothesis.

Let

and let

denote the probability measure corresponding to the parameters

The method consists of finding the

quantile of

see (5) with

replaced by

, as defined by

for

or

say, and the

quantile

of

as defined by

for

or

say.

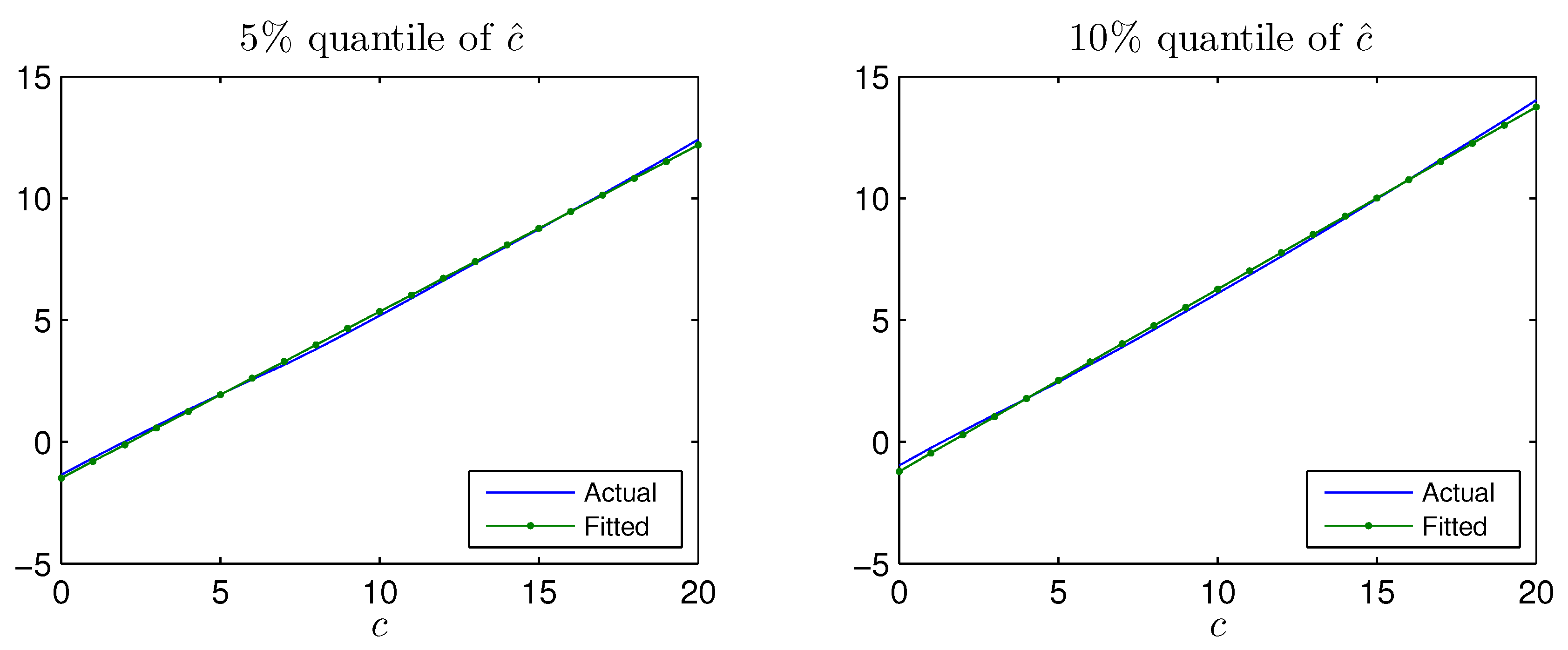

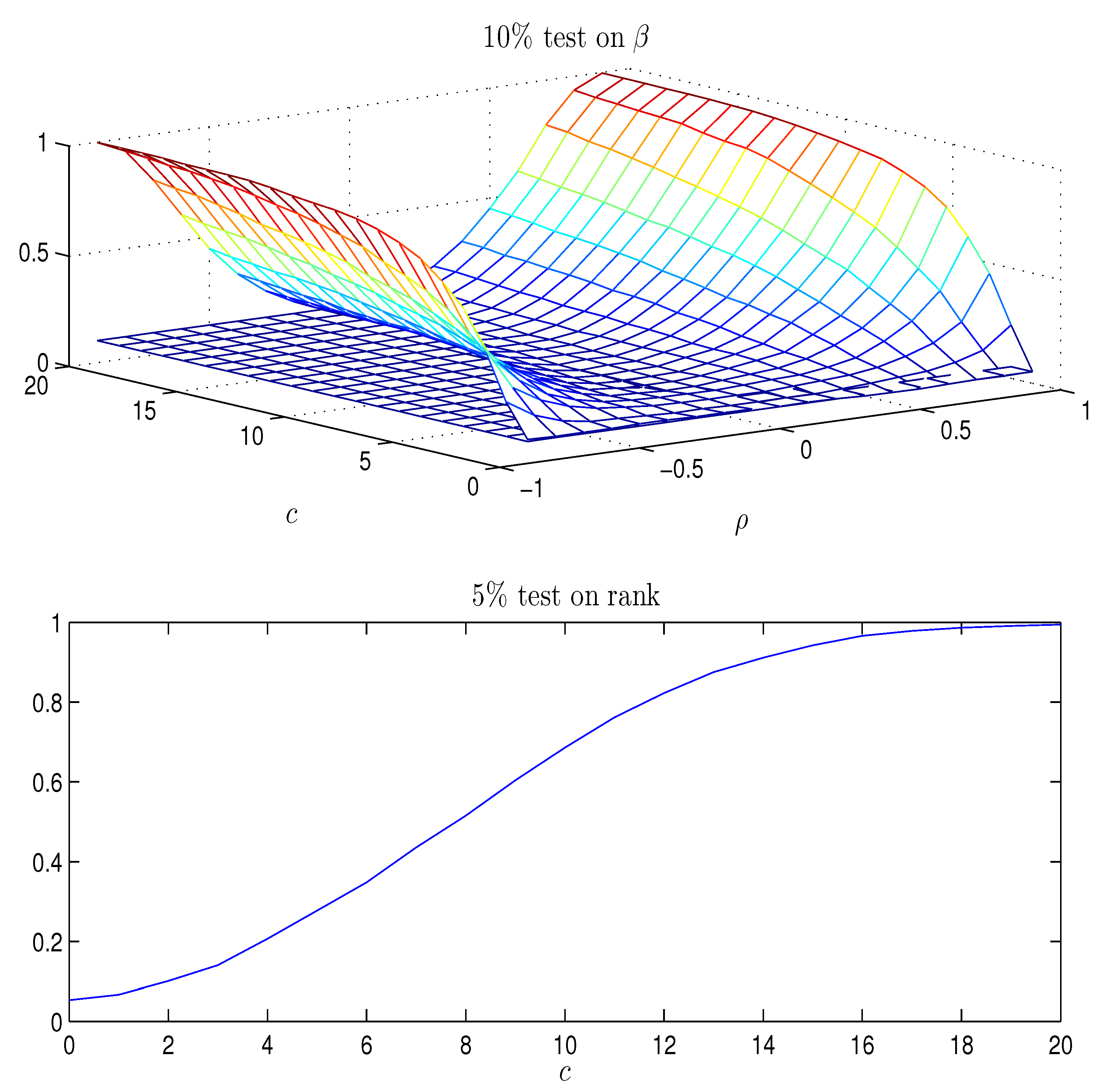

By simulation for given

and a grid of given of values

the quantiles

and

are determined. It turns out, that both

and

are increasing in

see

Figure A2. Therefore, a solution

can be found such that

This gives a

confidence interval

for

c, based on the estimator

. Note that for

it holds by monotonicity of

that

such that

but we also have

such that

In the paper from

McCloskey (2017) it is proved under suitable conditions that we have the much stronger result

Thus, the limiting rejection probability, for given of the test on calculated as if but replacing the quantile by the estimated stochastic quantile lies between and In the simulations we set and , so that the limiting rejection probability is bounded by

Note that

is replaced by the consistent estimator

It obviously simplifies matters that in all the examples we simulate, it turns out that

is approximately linear and increasing in

and

is approximately quadratic and increasing in

c for the relevant values of

c, see

Figure A2.

3.2. Adjusted Bonferroni Bounds

McCloskey (2017, Theorem Bonf-Adj) suggests determining by simulation on a grid of values of

c and

the quantitity

It turns out that

is monotone in

and we can determine for a given nominal size

(here 10%)

The Adjusted Bonferroni quantile is then

and we find

The result of

McCloskey (2017, Theorem Bonf-Adj) is that under suitable assumptions

where we illustrate the upper bound.

3.3. The Simulation Study of Elliott (1998)

The DGP is defined by the equations,

It is assumed that

are i.i.d.

with

and the initial values are

The data

are generated from (

15) and (16), and the test statistic

for the hypothesis

is calculated using (

6).

The DGP defined by (

15) and (16) is contained in model (

1) for

. Note that

such that

where the sign on

has been chosen such that

Finally

and

and therefore

For the process is and is stationary, and if is close to zero, has a near unit root.

Applying Corollary 1 to the DGP (

15) and (16), the expectation of the test statistic

is found to be

which increases approximately linearly in

Based on

simulations of errors

,

, the data

, are constructed from the DGP for each combination of the parameters

where

indicates the interval from

a to

c with step

b. Based on each simulation,

and the test

for

are calculated.

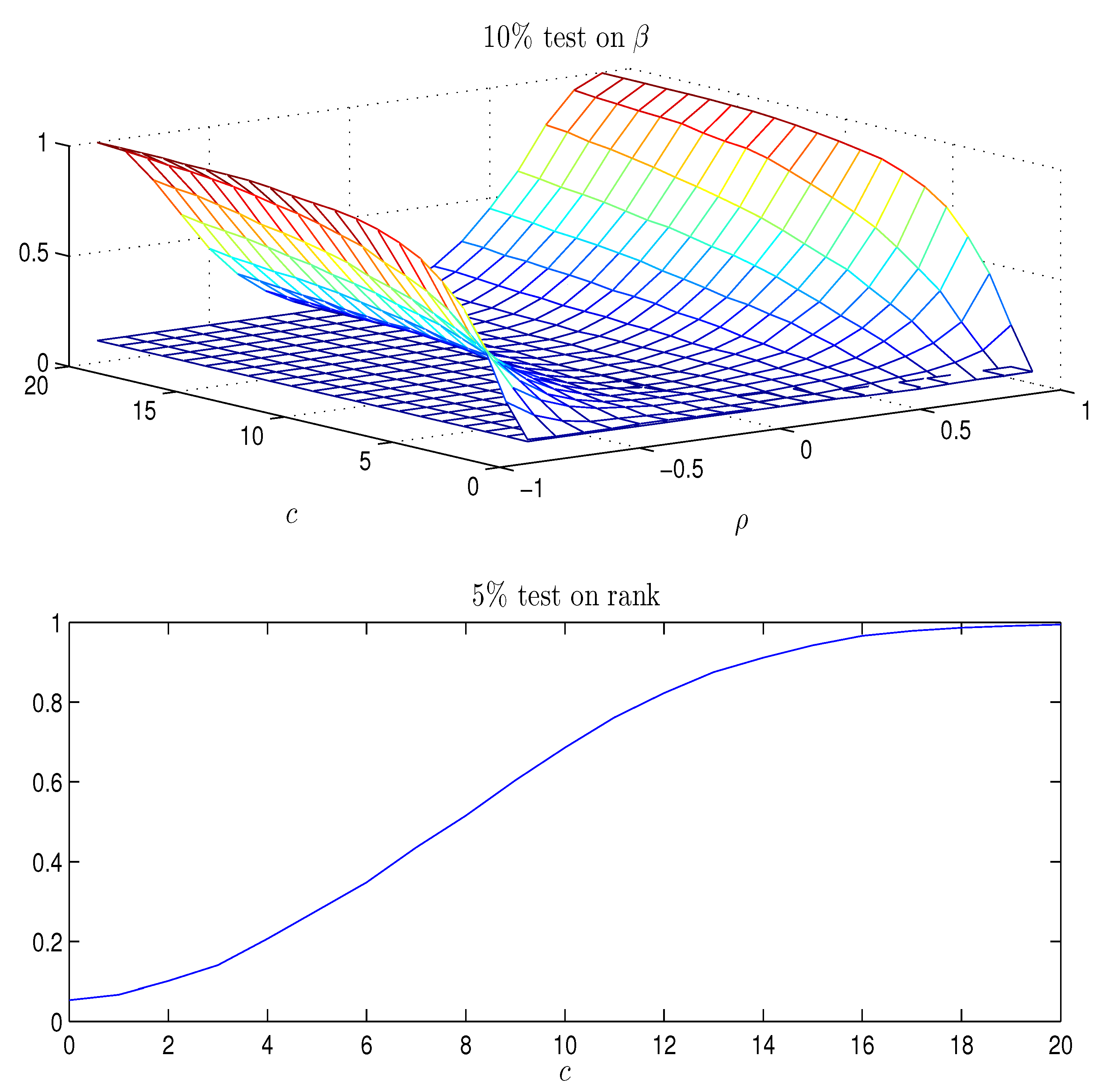

Top panel of

Figure A1 shows the rejection probabilities of the test

as a function of

, using the asymptotic critical value,

for a nominal rejection probability of

. The rejection probability increases with

and with

c. When

(corresponding to an autoregressive coefficient of

) and

, the size of the test

is around

, as found in

Elliott (1998). The results are analogous across models with an unrestricted constant term, or with a constant restricted to the cointegrating space. In the paper by

Elliott (1998) a number of tests are analyzed, and it was found that they were quite similar in their performance and similar to the above likelihood ratio test

from the CVAR with rank equal to 1.

3.4. Results with Bonferroni Quantiles and Adjusted Bonferroni Quantiles for

Data are simulated as above and first the rank test statistic,

, see

Johansen (

1996, chp. 11) for rank equal to 1, is calculated. The rejection probabilities for a 5% test using

are given in the bottom panel of

Figure A1 and they show that for

the hypothesis that the rank is 1, is practically certain to be rejected. If

the probability of rejecting that the rank is 1 is around

, so that plotting the rejection probabilities for

covers the relevant values, see

Figure A3.

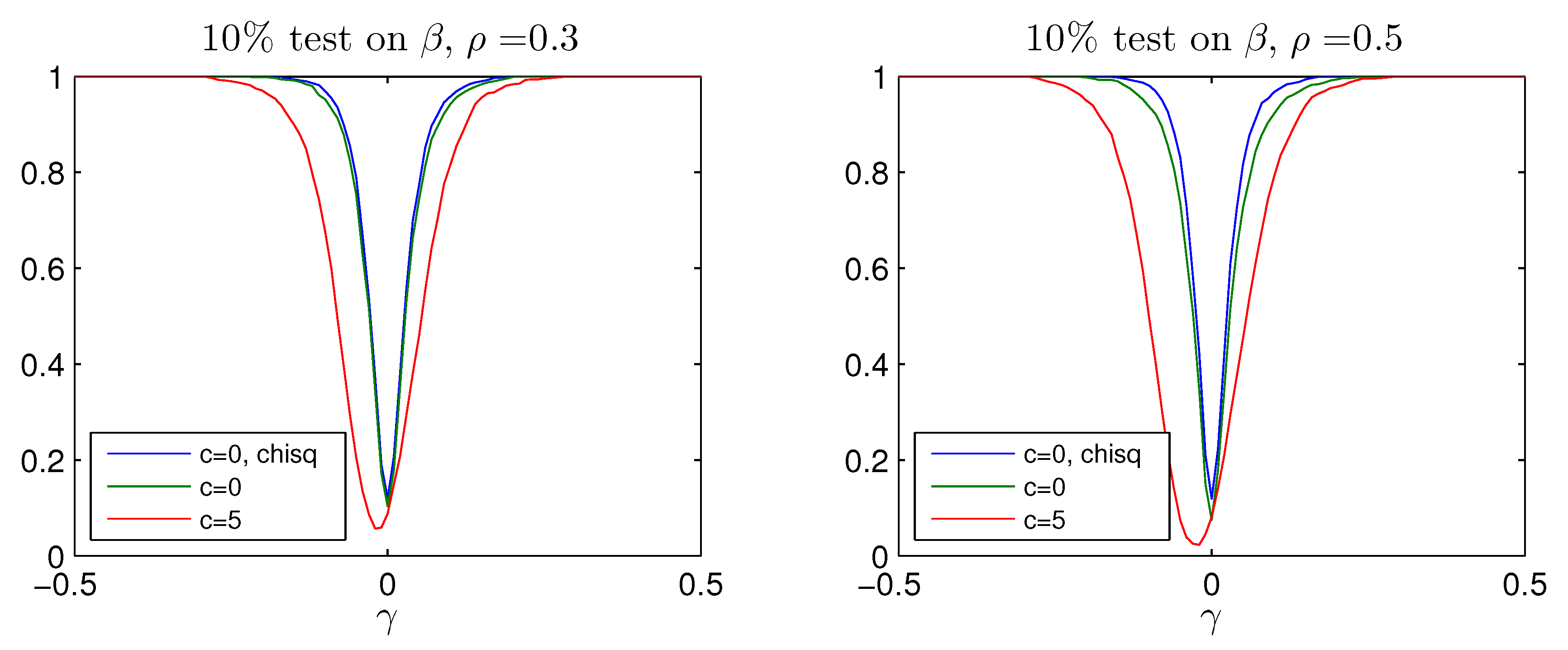

For

and

the quantiles

of

are reported in

Figure A2 as a function of

c. The quantiles

are nearly linear in

and they are approximated by

where the coefficients

depend on

, which is used to construct the upper confidence limit in (

14) as

For

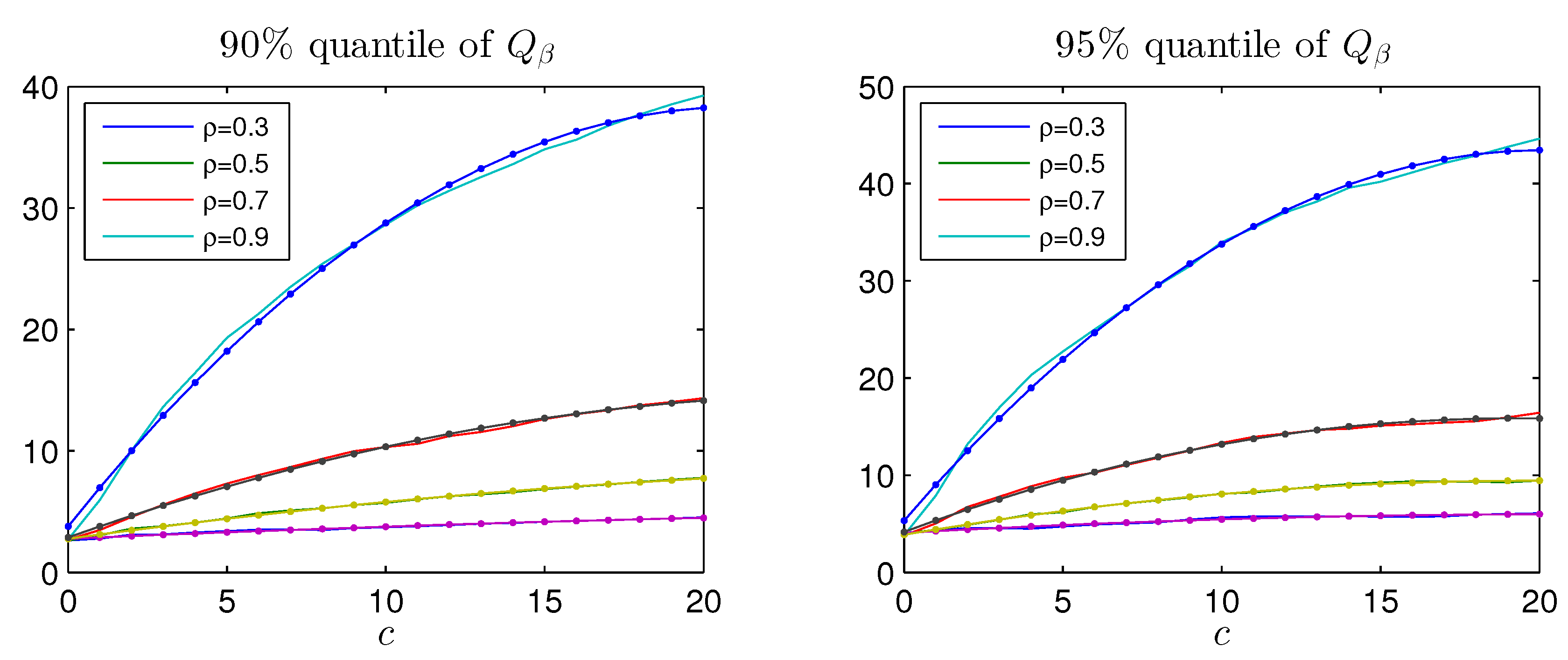

and

the quantiles

of

are reported in

Figure A2 as function of

c for four values of

. It is seen that for given

, the quantiles

are monotone and quadratic in

c, for relevant values of

and hence they can be approximated by

where the coefficients

depend on

and

. The modified critical value is then constructed replacing

by

in (

19), and thus one finds the adjusted critical value

which depends on estimated values,

and

, and on discretionary values,

and

.

The adjusted Bonferroni quantile is explained in

Section 3.2. Simulations show that

is linear in

and the solution of the equation

where

is the nominal size of the test, determines

; the adjusted Bonferroni

q-quantile is then found like (

20) as

where

.

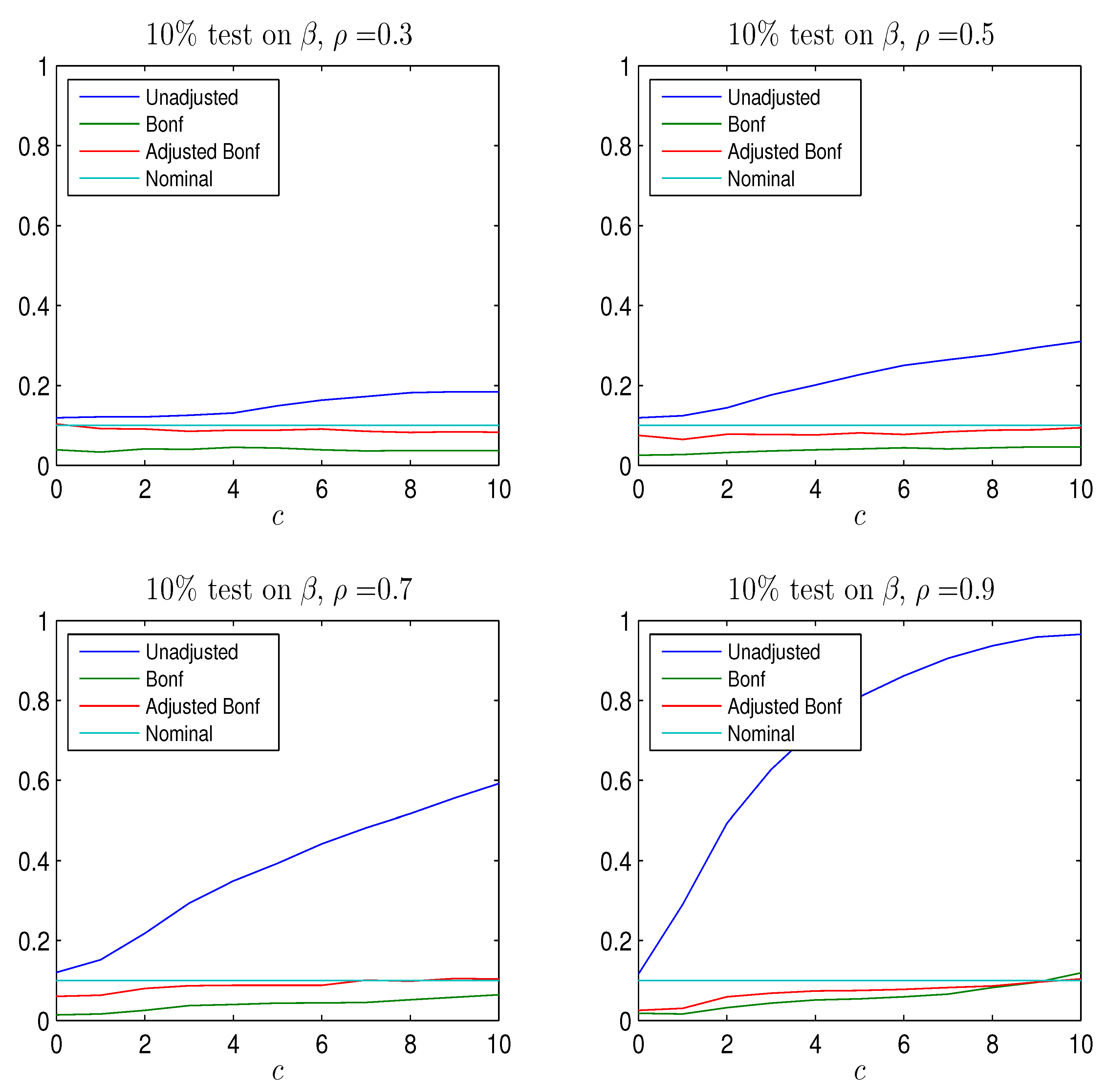

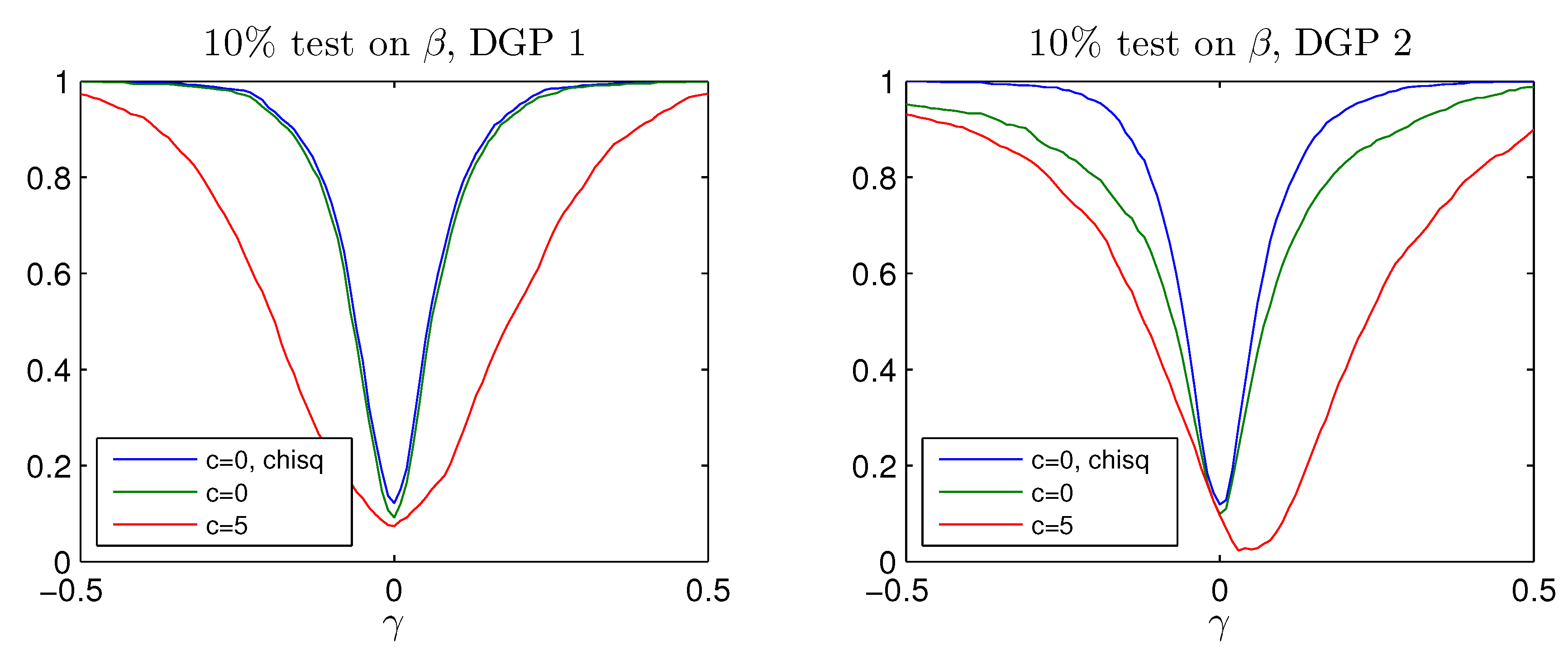

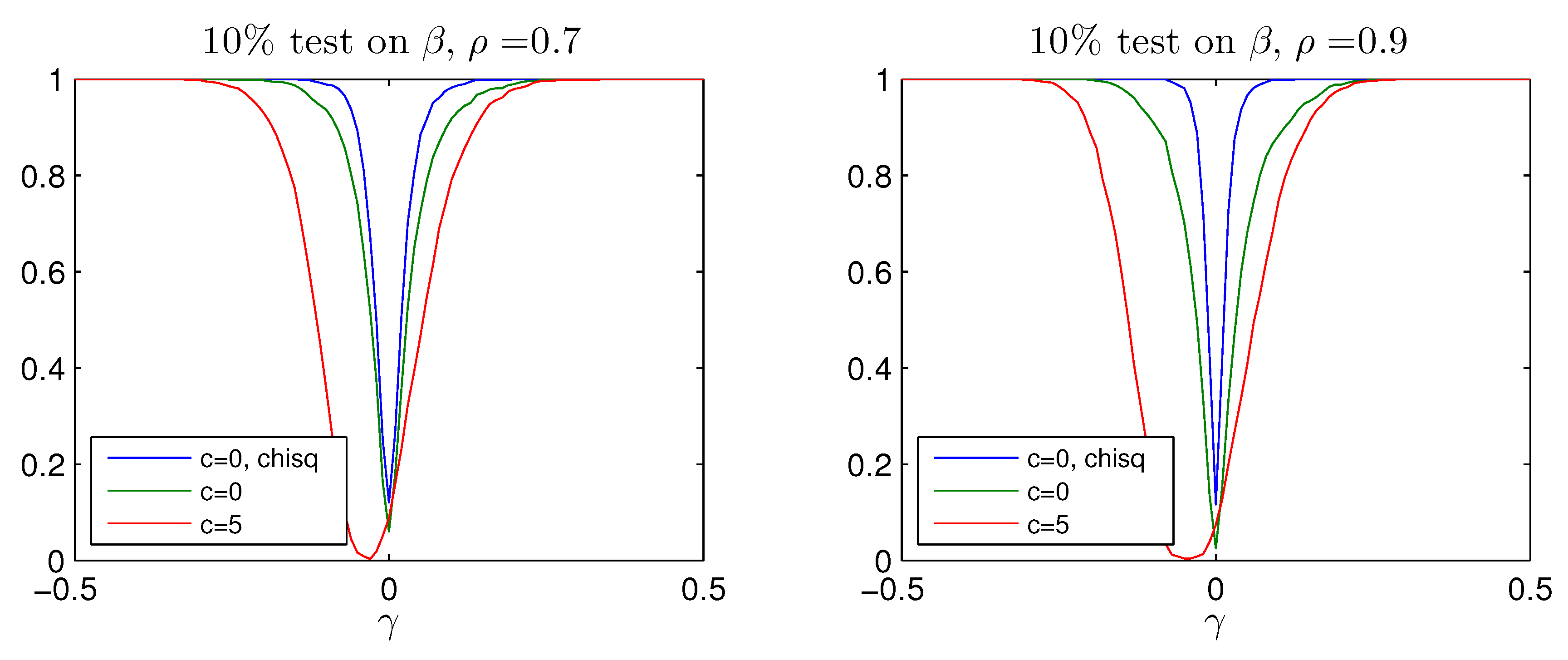

The rejection frequency of

the test for

calculated using the

quantile, the Bonferroni quantile in (

20) for

and

and the adjusted Bonferroni quantile in (

21) for

is reported as a function of

c for four values of

in

Figure A3. For both corrections the rejection frequency is below the nominal size of

; hence both procedures are able to eliminate the serious size-distortions of the

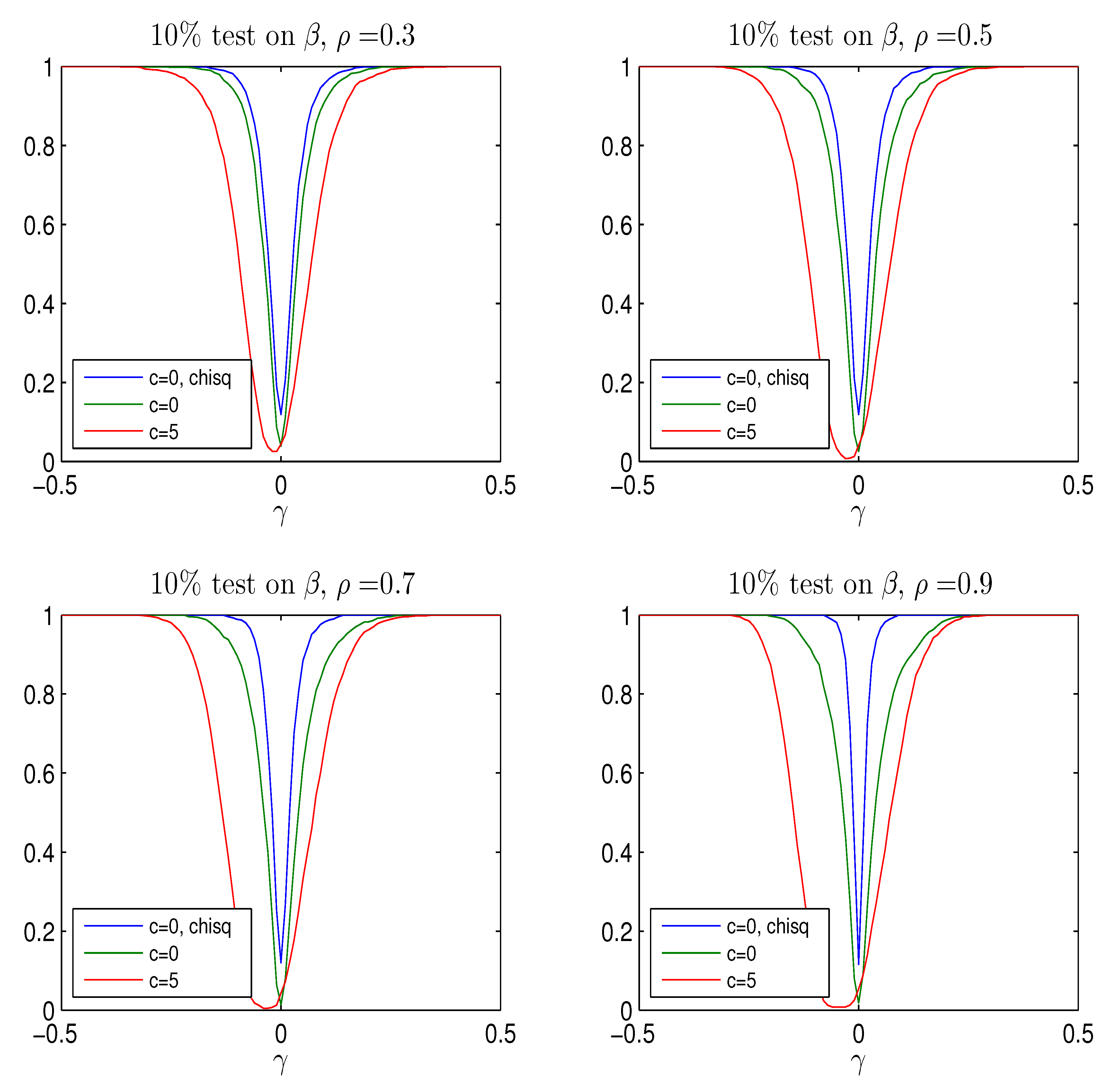

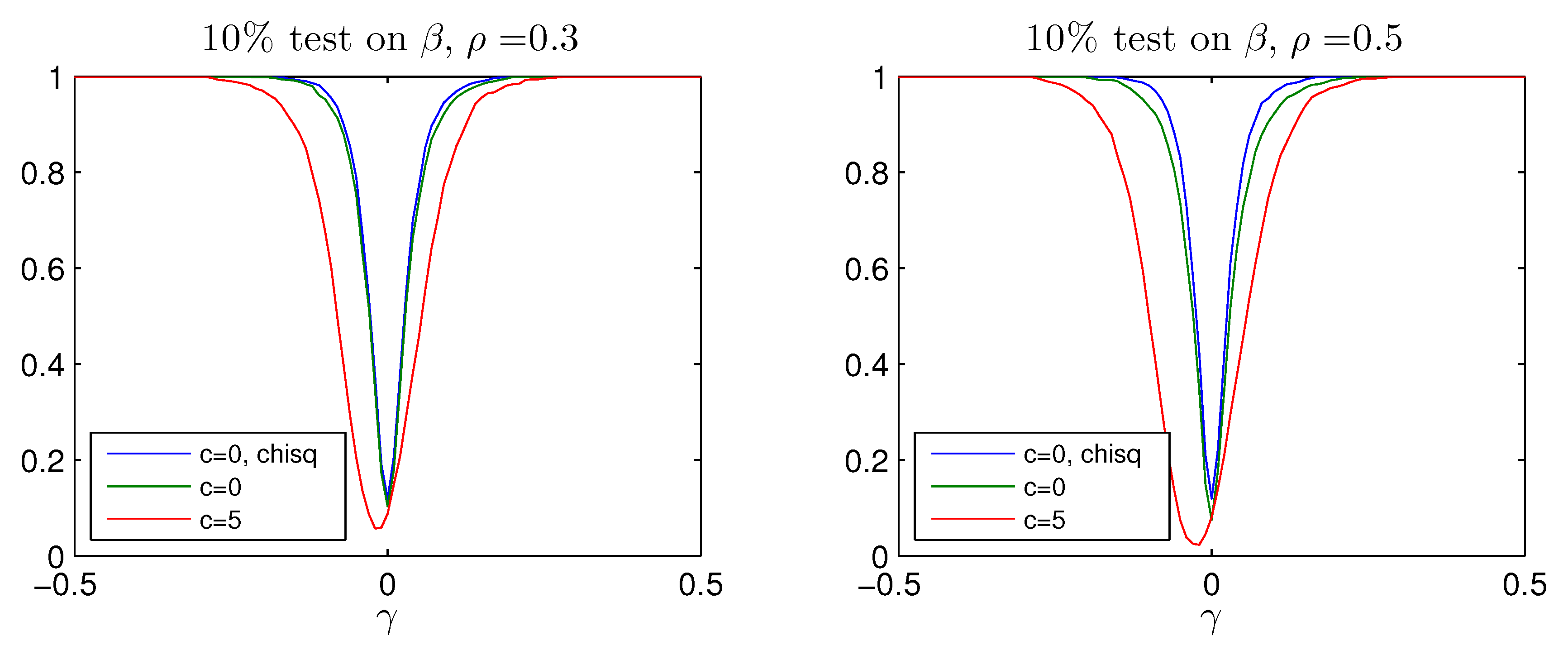

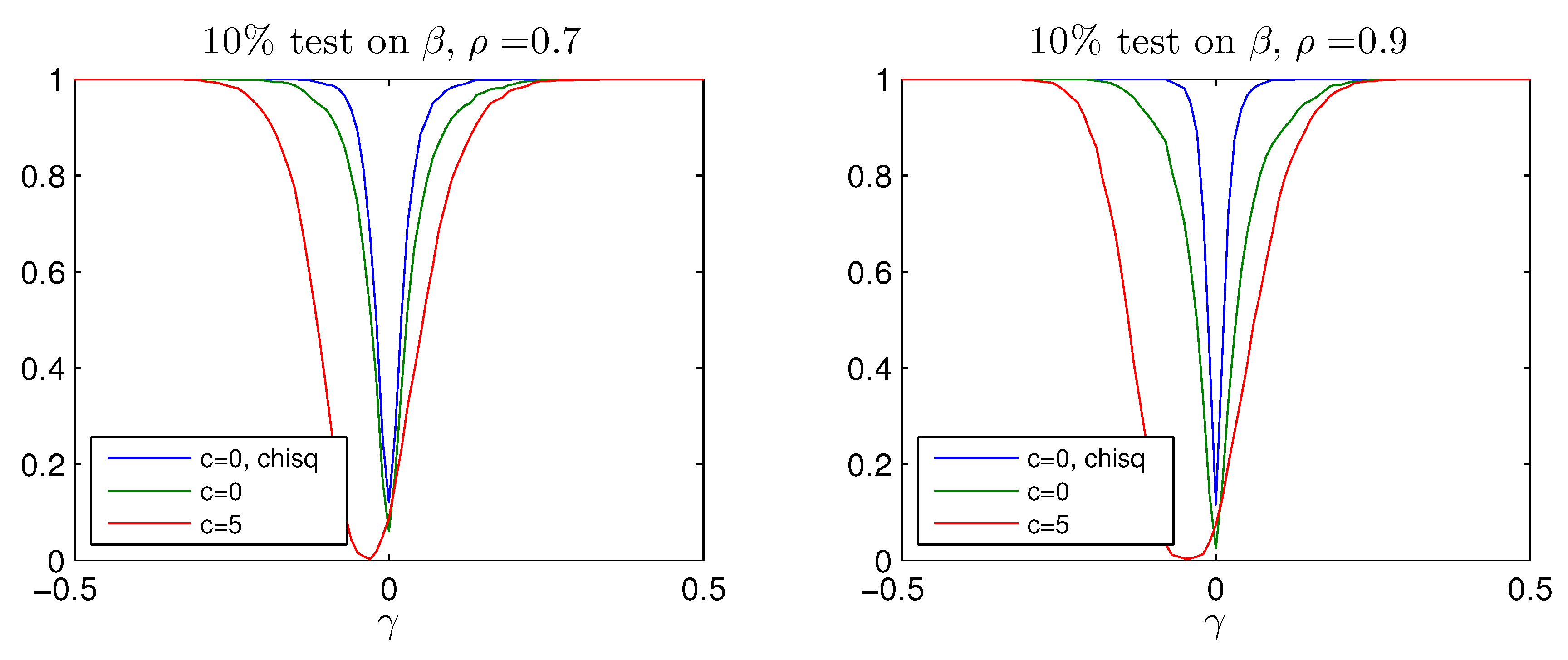

test. While the Bonferroni adjustment leads to rather conservative test with rejection frequency well below the nominal size, the adjusted Bonferroni procedure is closer to the nominal value. The power of the two procedures is shown in

Figure A4 and

Figure A5 for values of

It is seen that the better rejection probabilities in

Figure A3 are achieved together with a reasonable power for

where the probability of rejecting the hypothesis of

is around

, see bottom panel of

Figure A1. Notice that both tests become slightly biased, that is, the power functions are not flat around the null

.

In conclusion, the simulations indicate that the adjusted Bonferroni procedure works better than the simple Bonferroni, the reason being that the former relies on the joint distribution of and .

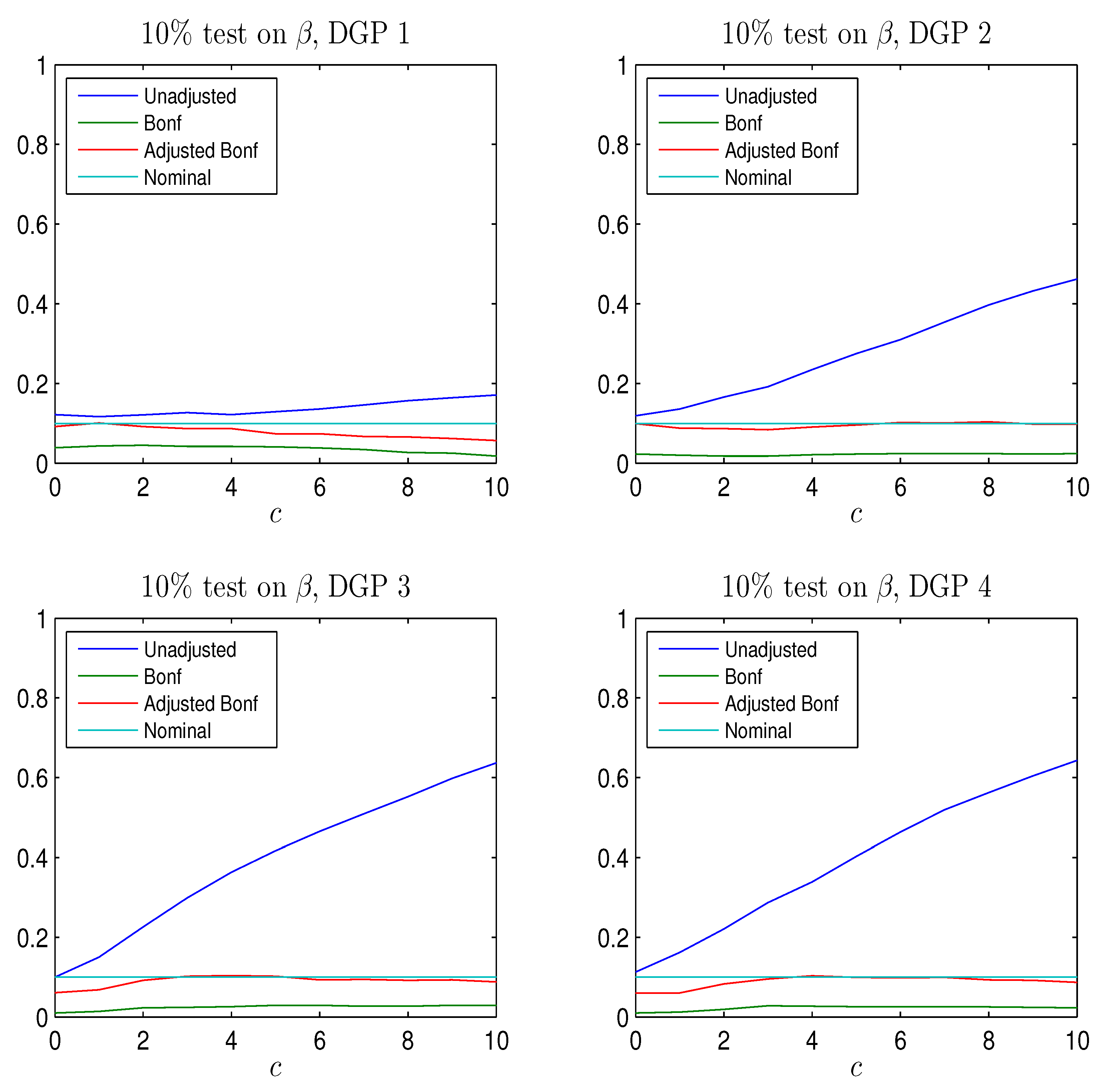

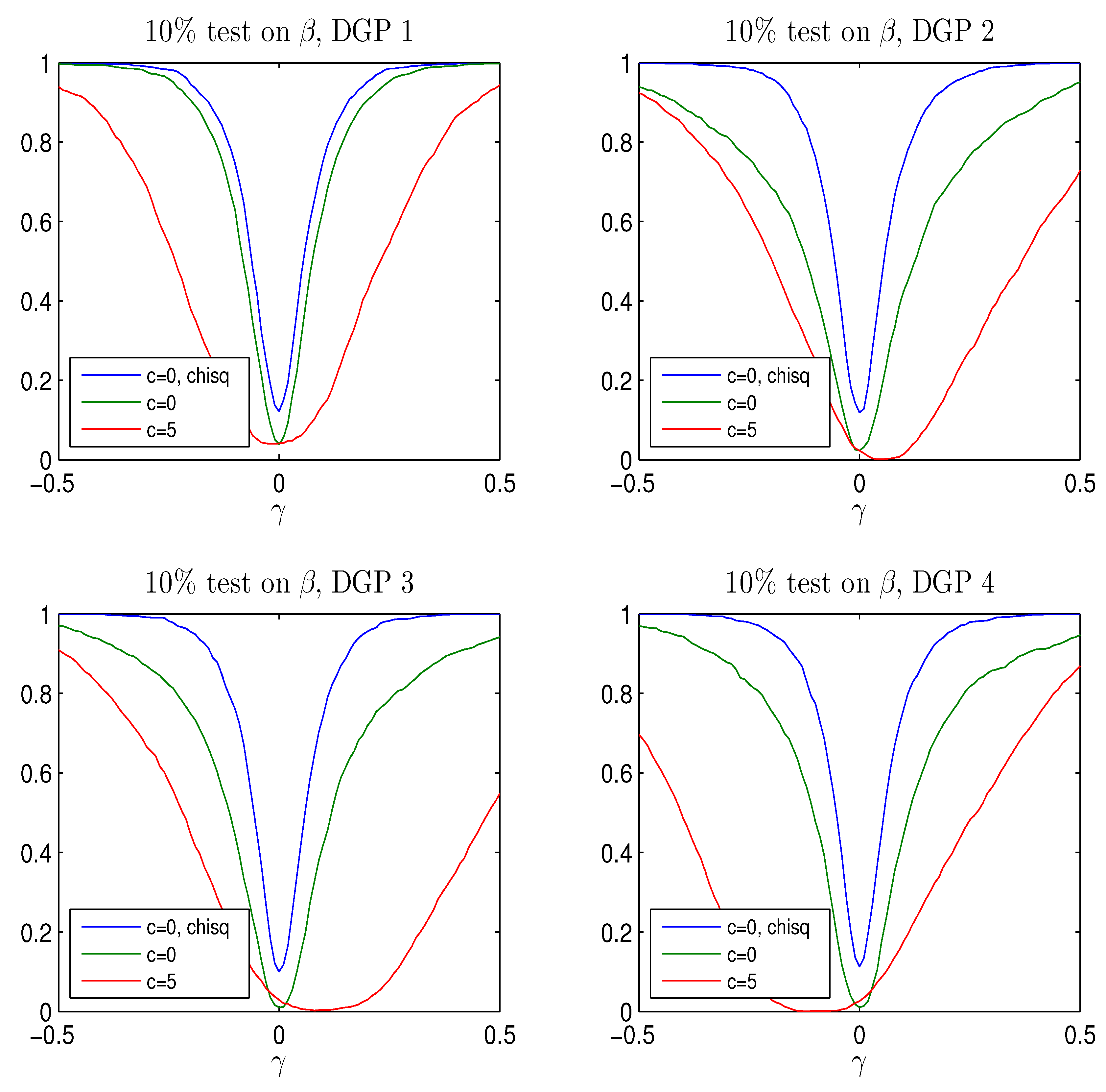

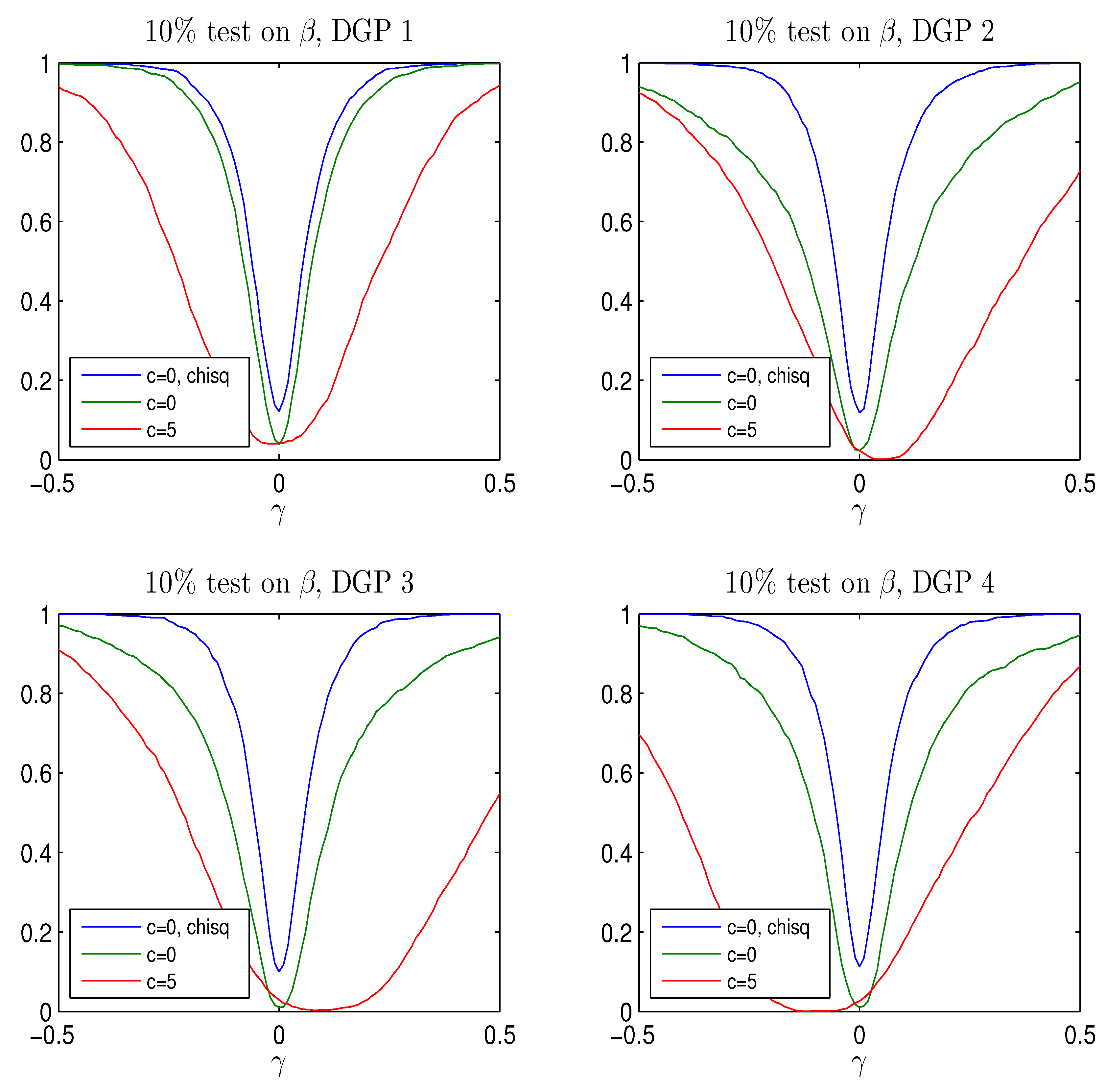

3.5. A Few Examples of Other DGPs

Four other data generating processes are defined in

Table 1, to investigate the role of different choices of

and

for the results on improving the rejection probabilities for test on

under the null and alternative. The DGPs all have

. The vectors

and

are chosen to investigate different positions of the near unit root in the DGP.

The choice of DGP turns out to be important also for the test, for In fact the probability of rejecting is around for DGP 1 if , for DGP 2 if , whereas for DGP 3 and 4 the value value is 8.

The rejection probabilities in

Figure A6 are plotted for

to cover the most relevant values.

The results are summarized in

Figure A6,

Figure A7 and

Figure A8. It is seen that the conclusions from the study of the DGP analyzed by Elliott seem to be valid also for other DGPs. For moderate values of

using the Bonferroni quantiles gives a rather conservative test while the adjusted Bonferroni procedure is closer to the nominal size and the power curves look reasonable for

although the tests are slightly biased, except for DGP 1. For this DGP,

such that

which means that the asymptotic distribution of

is

see Theorem 3, despite the near unit root. It is seen from

Figure A6, there is only moderate distortion of the rejection probability in this case and in

Figure A7 and

Figure A8, the power curves are symmetric around

so the tests are approximately unbiased.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}