Sustainability and Continuous Improvement of Organization: Review of Process-Oriented Performance Indicators

Abstract

1. Introduction

2. Methodology

- (1)

- Key Performance Indicator AND sustainable development AND identification AND review. In total, 4 relevant publications were retrieved.

- (2)

- Performance indicator AND measurement AND metrics AND objectives AND quality AND review. In total, 9 relevant publications were retrieved.

- (1)

- Key performance Indicator AND business. In total, 10 relevant publications were retrieved.

- (2)

- Performance indicator AND measurement AND metrics AND review. In total 7 relevant publications were retrieved.

- (3)

- Sustainability AND Benchmarking AND Key Performance Indicators LIMIT TO (open access). In total 5 relevant publications were retrieved.

3. The Concept of Sustainable Development

4. Measuring the Organization’s Sustainable Development

5. Analysing the Performance of the Organization

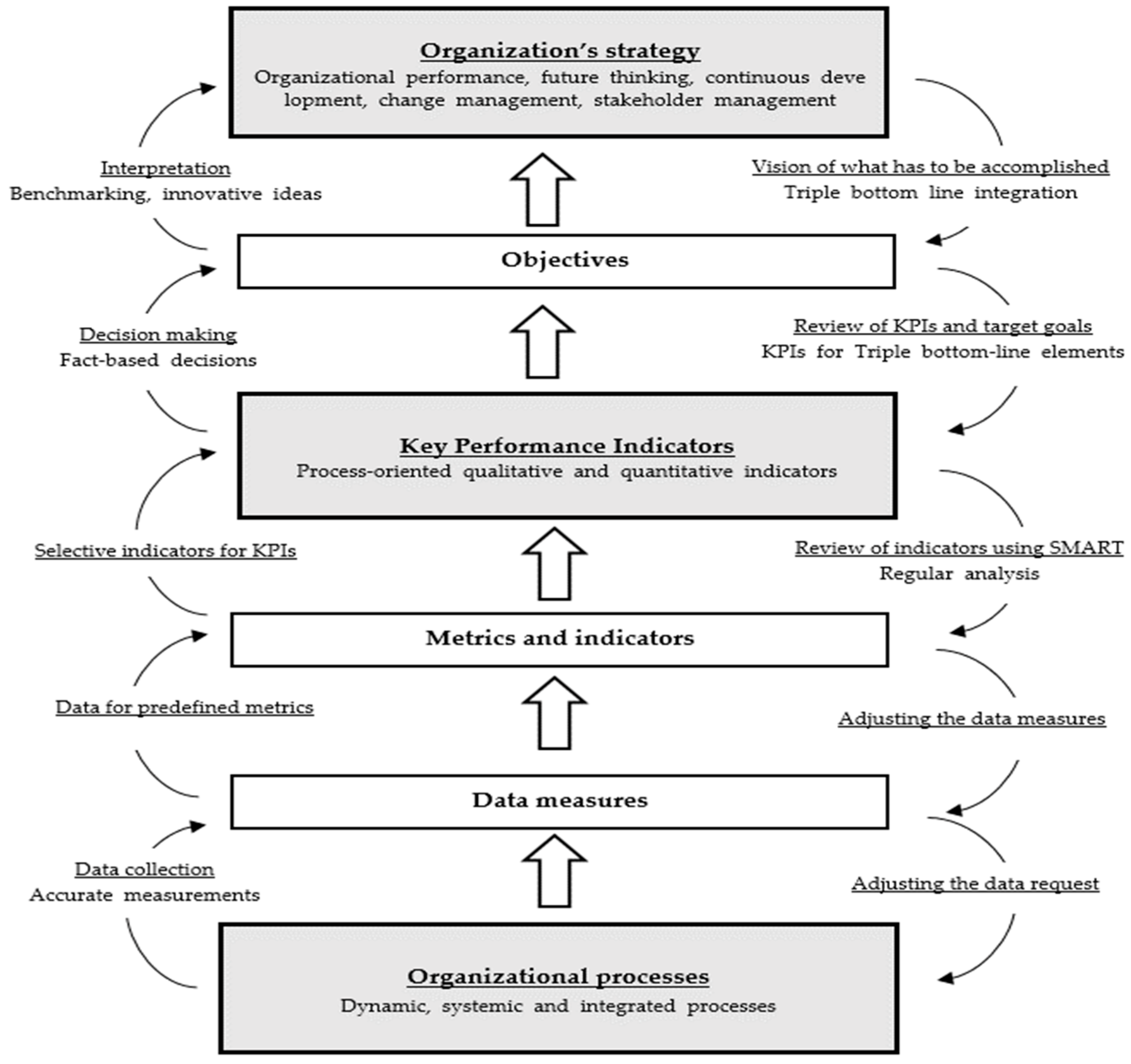

6. The Linkage between the Organization’s Strategy, KPIs and Processes

7. Conclusions, Discussions and Further Studies

Author Contributions

Funding

Conflicts of Interest

References

- Bonsón, E.; Bednárová, M. CSR Reporting Practices of Eurozone Companies. Rev. Contab. 2015. [Google Scholar] [CrossRef]

- White, G.R.T.; James, P. Extension of Process Mapping to Identify “Green Waste”. Benchmarking 2014, 21, 835–850. [Google Scholar] [CrossRef]

- Rao, P.; Singh, A.K.; La O’Castillo, O.; Intal, P.S.; Sajid, A. A Metric for Corporate Environmental Indicators for Small and Medium Enterprises in the Philippines. Bus. Strategy Environ. 2009, 18, 14–31. [Google Scholar] [CrossRef]

- Yun, J.H.J.; Yigitcanlar, T. Open Innovation in Value Chain for Sustainability of Firms. Sustain 2017, 9, 811. [Google Scholar] [CrossRef]

- Roša, A.; Lace, N. The Open Innovation Model of Coaching Interaction in Organisations for Sustainable Performance within the Life Cycle. Sustainability 2018, 10, 3516. [Google Scholar] [CrossRef]

- Danileviciene, I.; Lace, N. The Features of Economic Growth in the Case of Latvia and Lithuania. J. Open Innov. Technol. Mark. Complex. 2017, 3. [Google Scholar] [CrossRef]

- Athanasopoulou, A.; Selsky, J.W. The Social Context of Corporate Social Responsibility: Enriching Research With Multiple Perspectives and Multiple Levels. Bus. Soc. 2015. [Google Scholar] [CrossRef]

- Keeble, J.J.; Topiol, S.; Berkeley, S. Using Indicators to Measure Sustainability Performance at a Corporate and Project Level. J. Bus. Ethics 2003, 44, 149–158. [Google Scholar] [CrossRef]

- Santos, J.B.; Brito, L.A.L. Toward a Subjective Measurement Model for Firm Performance. BAR Braz. Adm. Rev. 2012, 9, 95–117. [Google Scholar] [CrossRef]

- Dubickis, M.; Gaile-Sarkane, E. Transfer of Know-How Based on Learning Outcomes for Development of Open Innovation. J. Open Innov. Technol. Mark. Complex. 2017, 3. [Google Scholar] [CrossRef]

- Barone, D.; Jiang, L.; Amyot, D.; Mylopoulos, J. Reasoning with Key Performance Indicators. Lect. Notes Bus. Inf. Process. 2011, 92, 82–96. [Google Scholar] [CrossRef]

- Laufer, W.S. Social Accountability and Corporate Greenwashing. J. Bus. Ethics 2003, 43, 253–261. [Google Scholar] [CrossRef]

- Nigri, G.; Del Baldo, M. Sustainability Reporting and Performance Measurement Systems: How Do Small- and Medium Sized Benefit Corporations Manage Integration? Sustainability 2018, 10, 4499. [Google Scholar] [CrossRef]

- World Commission on Environment and Development. (S1) Report of the World Commission on Environment and Development: Our Common Future. Med. Confl. Surviv. 1987. [Google Scholar] [CrossRef]

- Bansal, P.; DesJardine, M.R. Business sustainability: It is about time. Strateg. Organ. 2014, 12, 70–78. [Google Scholar] [CrossRef]

- Rocha-Lona, L.; Garza-Reyes, J.A.; Lim, M.K.; Kumar, V. Corporate Sustainability and Business Excellence. In Proceedings of the IEOM 2015—5th International Conference on Industrial Engineering and Operations Management, Dubai, UAE, 3–5 March 2015. [Google Scholar] [CrossRef]

- Moldavanova, A.; Goerdel, H.T. Understanding the puzzle of organizational sustainability: Toward a conceptual framework of organizational social connectedness and sustainability. Public Manag. Rev. 2017, 1–27. [Google Scholar] [CrossRef]

- Thomas, T.E.; Lamm, E. Legitimacy and organizational sustainability. J. Bus. Ethics 2012, 110, 191–203. [Google Scholar] [CrossRef]

- Zeps, A.; Ribickis, L. Setting Innovations as a Strategic Aim for Technical Universities. J. Bus. Econ. 2016, 7, 507–517. [Google Scholar] [CrossRef]

- Thomas, D.; Preston, L.E. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar]

- Dowling, J.; Pfeffer, J. Organizational legitimacy: Social values and organizational behavior. Pac. Sociol. Rev. 1975, 18, 122–136. [Google Scholar] [CrossRef]

- Maletič, M.; Maletič, D.; Dahlgaard, J.J.; Dahlgaard-Park, S.M.; Gomišček, B. Effect of Sustainability-Oriented Innovation Practices on the Overall Organisational Performance: An Empirical Examination. Total Qual. Manag. Bus. Excell. 2016. [Google Scholar] [CrossRef]

- Brundage, M.P.; Bernstein, W.Z.; Morris, K.C.; Horst, J.A. Using Graph-Based Visualizations to Explore Key Performance Indicator Relationships for Manufacturing Production Systems. Procedia CIRP 2017, 61, 451–456. [Google Scholar] [CrossRef]

- Fonseca, L.M.; Lima, V.M. Countries Three Wise Men: Sustainability Innovation, and Competitiveness. J. Ind. Eng. Manag. 2015, 8, 1288–1302. [Google Scholar] [CrossRef]

- Havas, A. Social and Business Innovations: Are Common Measurement Approaches Possible? Foresight STI Gov. 2017, 10, 58–80. [Google Scholar] [CrossRef]

- Ivanov, C.-I.; Avasilcăi, S. Measuring the Performance of Innovation Processes: A Balanced Scorecard Perspective. Procedia Soc. Behav. Sci. 2014. [Google Scholar] [CrossRef]

- Copernicus-Campus. COPERNICUS-Guidelines for Sustainable Development in the European Higher Education Area. Available online: http://www.unece.org/fileadmin/DAM/env/esd/information/COPERNICUS%20Guidelines.pdf (accessed on 26 July 2019).

- Gough, S.; Scott, W. Higher Education and Sustainable Development: Paradox and Possibility; Routledge: Abingdon, UK, 2008. [Google Scholar]

- Technical Commitee ISO/TC176/SC2 Quality Systems. ISO 9001:2015—Quality Management Systems—Requirements; ISO: Geneva, Switzerland, 2015. [Google Scholar]

- Mulder, K.F.; Segalàs, J.; Ferrer-Balas, D. How to Educate Engineers for/in Sustainable Development. Int. J. Sustain. High. Educ. 2012, 13, 211–218. [Google Scholar] [CrossRef]

- Nemetz, P.N. Business and the Sustainability Challenge; Routledge: Abingdon, UK, 2014. [Google Scholar] [CrossRef]

- Isaksson, R. Total Quality Management for Sustainable Development—Focus on Processes; Lulea University of Technology: Luleå, Sweden, 2004. [Google Scholar]

- GRI. Consolidated Set of GRI Sustainability Reporting Standards; GRI: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Asif, M.; Searcy, C.; Zutshi, A.; Fisscher, O.A.M. An Integrated Management Systems Approach to Corporate Social Responsibility. J. Clean. Prod. 2013. [Google Scholar] [CrossRef]

- Varsei, M.; Soosay, C.; Fahimnia, B.; Sarkis, J. Framing Sustainability Performance of Supply Chains with Multidimensional Indicators. Supply Chain Manag. 2014, 19, 242–257. [Google Scholar] [CrossRef]

- Avram, E.; Avasilcai, S. Business Performance Measurement in Relation to Corporate Social Responsibility: A Conceptual Model Development. Procedia Soc. Behav. Sci. 2014, 109, 1142–1146. [Google Scholar] [CrossRef][Green Version]

- Doyle, E.; Perez-Alaniz, M. From the Concept to the Measurement of Sustainable Competitiveness: Social and Environmental Aspects. Entrep. Bus. Econ. Rev. 2018, 5, 35–59. [Google Scholar] [CrossRef]

- Sahimi, N.S.; Turan, F.M.; Johan, K. Development of Sustainability Assessment Framework in Hydropower Sector. IOP Conf. Ser. Mater. Sci. Eng. 2017, 226. [Google Scholar] [CrossRef]

- Pohludka, M.; Stverkova, H.; Ślusarczyk, B. Implementation and Unification of the ERP System in a Global Company as a Strategic Decision for Sustainable Entrepreneurship. Sustainability 2018, 10, 2916. [Google Scholar] [CrossRef]

- Demartini, M.; Pinna, C.; Aliakbarian, B.; Tonelli, F.; Terzi, S. Soft Drink Supply Chain Sustainability: A Case Based Approach to Identify and Explain Best Practices and Key Performance Indicators. Sustainability 2018, 10, 3540. [Google Scholar] [CrossRef]

- De Menna, F.; Dietershagen, J.; Loubiere, M.; Vittuari, M. Life Cycle Costing of Food Waste: A Review of Methodological Approaches. Waste Manag. 2018. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard: Translating Strategy into Action; Proceedings of the IEEE; Harvard Business Review Press: Boston, MA, USA, 1996. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard—Measures That Drive Performance; Harvard Business Review Press: Boston, MA, USA, 1992. [Google Scholar]

- Gibbons, R.; Kaplan, R.S. Formal Measures in Informal Management: Can a Balanced Scorecard Change a Culture? Am. Econ. Rev. 2015. [Google Scholar] [CrossRef]

- Parmenter, D. Key Performance Indicators: Developing, Implementing and Using Winning KPIs, 3rd ed.; Wiley & Sons, Inc.: Hoboken, NJ, USA, 2010. [Google Scholar]

- Hlyal, M.; Chahid, M.T.; Soulhi, A.; Alami, J.E.; Alami, N.E. Supplier’s Selection for the Moroccan Textile Sector by Using Performance Measurement System. Mod. Appl. Sci. 2015, 9, 102–116. [Google Scholar] [CrossRef]

- Kibira, D.; Morris, K.; Kumaraguru, S. Methods and Tools for Performance Assurance of Smart Manufacturing Systems. J. Res. Natl. Inst. Stand. Technol. 2016, 121, 287. [Google Scholar] [CrossRef]

- Moges Kasie, F.; Moges Belay, A. The Impact of Multi-Criteria Performance Measurement on Business Performance Improvement. J. Ind. Eng. Manag. 2013. [Google Scholar] [CrossRef]

- Podgórski, D. Measuring Operational Performance of OSH Management System—A Demonstration of AHP-Based Selection of Leading Key Performance Indicators. Saf. Sci. 2015, 73, 146–166. [Google Scholar] [CrossRef]

- Van Looy, A.; Shafagatova, A. Business Process Performance Measurement: A Structured Literature Review of Indicators, Measures and Metrics. Springerplus 2016, 5, 1–24. [Google Scholar] [CrossRef]

- Zemguliene, J.; Valukonis, M. Structured Literature Review on Business Process Performance Analysis and Evaluation. Entrep. Sustain. Issues 2018, 6, 226–252. [Google Scholar] [CrossRef]

- Álvarez, C.; Rodríguez, V.; Ortega, F.; Villanueva, J. A Scorecard Framework Proposal for Improving Software Factories’ Sustainability: A Case Study of a Spanish Firm in the Financial Sector. Sustainability 2015, 7, 15999–16021. [Google Scholar] [CrossRef]

- Bengo, I.; Arena, M.; Azzone, G.; Calderini, M. Indicators and Metrics for Social Business: A Review of Current Approaches. J. Soc. Entrep. 2016. [Google Scholar] [CrossRef]

- Bingol, B.N.; Polat, G. Measuring Managerial Capability of Subcontractors Using a KPI Model. Procedia Eng. 2017, 196, 68–75. [Google Scholar] [CrossRef]

- Milichovský, F. Financial Key Performance Indicators in Engineering Companies. Period. Polytech. Soc. Manag. Sci. 2015, 23, 60–67. [Google Scholar] [CrossRef]

- Rodrigues, V.P.; Pigosso, D.C.A.; Andersen, J.W.; McAloone, T.C. Evaluating the Potential Business Benefits of Ecodesign Implementation: A Logic Model Approach. Sustainability 2018, 10, 2011. [Google Scholar] [CrossRef]

- Sabbagha, O.; Rahman, M.N.A.; Ismail, W.R.; Hussain, W.M.H.W. Impact of Quality Management Systems and After-Sales Key Performance Indicators on Automotive Industry: A Literature Review. Procedia Soc. Behav. Sci. 2016, 224, 68–75. [Google Scholar] [CrossRef]

- Fantini, P.; Palasciano, C.; Taisch, M. Back to Intuition: Proposal for a Performance Indicators Framework to Facilitate Eco-Factories Management and Benchmarking. Procedia CIRP 2015, 26, 1–6. [Google Scholar] [CrossRef]

- Marquardt, K.; Olaru, M.; Ceausu, I. Study on the Development of Quality Measurements Models for Steering Business Services. Amfiteatru Econ. 2017, 19, 95–110. [Google Scholar]

- Yun, S.; Jung, W. Benchmarking Sustainability Practices Use throughout Industrial Construction Project Delivery. Sustainability 2017, 9, 1007. [Google Scholar] [CrossRef]

- Povolná, L. Innovation Strategy in Small and Medium Sized Enterprises (SMEs) in the Context of Growth and Recession Indicators. J. Open Innov. Technol. Mark. Complex. 2019, 5, 32. [Google Scholar] [CrossRef]

- Kwon, Y.-I.; Son, J.-K. A Case Study on the Promising Product Selection Indicators for Small and Medium-Sized Enterprises (SMEs). J. Open Innov. Technol. Mark. Complex. 2018, 4, 56. [Google Scholar] [CrossRef]

- Rostoka, Z.; Locovs, J.; Gaile-Sarkane, E. Open Innovation of New Emerging Small Economies Based on University-Construction Industry Cooperation. J. Open Innov. Technol. Mark. Complex. 2019, 5, 10. [Google Scholar] [CrossRef]

- Mazais, J.; Lapiņa, I.; Liepiņa, R. Process Management for Quality Assurance: Case of Universities. In Proceedings of the 8th European Conference on Management, Leadership and Governance, Cyprus, Pafos, 8–9 November 2012; Neapolis University Pafos: Pafos, Cyprus, 2012; pp. 522–530. [Google Scholar]

- Yusr, M.M. Innovation capability and its role in enhancing the relationship between TQM practices and innovation performance. J. Open Innov. Technol. Mark. Complex. 2016, 2, 6. [Google Scholar] [CrossRef]

- Liepiņa, R.; Lapiņa, I.; Janauska, J.; Mazais, J. Innovations, Standards and Quality Management Systems: Analysis of Interrelation. In Proceedings of the 8th European Conference on Innovation and Entrepreneurship, Brussels, Belgium, 19–20 September 2013; Academic Conferences and Publishing International Limited: Brussels, Belgium, 2013; pp. 723–730. [Google Scholar]

- Leydesdorff, L.; Ivanova, I. “Open innovation” and “triple helix” models of innovation: Can synergy in innovation systems be measured? J. Open Innov. Technol. Mark. Complex. 2016, 2, 11. [Google Scholar] [CrossRef]

- Yun, J.H.J.; Won, D.K.; Park, K. Dynamics from open innovation to evolutionary change. J. Open Innov. Technol. Mark. Complex. 2016, 2, 7. [Google Scholar] [CrossRef]

{kind=link}

| Time | Sustainable Development | Sustainability Focus |

|---|---|---|

| 1987 | Seeks to meet the needs and aspirations of the present without compromising the ability to meet those of the future [14]. | Future thinking |

| 2005 | As a principle and a practice brings added value to the content and process. Sustainable development can only be progressed—or indeed achieved—through a critical understanding of its complementary parts—environmental, socio-political and economic factors [27]. | Triple bottom line |

| 2008 | At the general level is a continuous process that is essentially sustainable, influenced by three factors: environment, economy and society [28]. | Continuous process; Triple bottom line |

| 2009 and 2015 | Achieving a balance between the environment, society and the economy (triple bottom line (TBL)) is considered essential to meet the needs of the present without compromising the ability of future generations to meet their needs [29]. | Triple bottom line |

| 2012 | Based on continuous change, systemic thinking, integrated and dynamic processes, as well as a change in the organization’s internal culture and strategy [30]. | Continuous change; Systemic management; Integrated and dynamic process management |

| 2014 | Ensures the need for more accurate measurement and regular analysis of existing resources (environmental, human, physical) in order to ensure fact-based decision making [31]. | Accurate measurements; Regular analysis; Fact-based decision making |

| 2014 | Sustainability and responsibility must be one of the values of the organization in order to be able to define sustainable development. Future generations must be one of the considered stakeholders [32]. | Future thinking; Stakeholder management |

| 2016 | Based on clear understanding of the organization’s key sustainability factors—economic, environmental and social. Sustainability is based on innovative ideas, focus on stakeholders and benchmarking [33]. | Triple bottom line; Innovative ideas; Benchmarking |

| Year | Themes of Measuring the Organization’s Sustainable Development | Authors |

|---|---|---|

| 2011 | Viewed through Corporate Social Responsibility (CSR) indicators that measure internal and external stakeholder expectations. | [34] |

| 2014 | Using multidimensional indicators to measure sustainable development. | [35] |

| 2014 | Using Balanced Scorecard (BSC) method for Corporate Social Responsibility indicators. Introducing the environmental dimension in the BSC. | [36] |

| 2014 | Benchmarking other organizations’ sustainable development. | [2] |

| 2015 | Triple bottom line (TBL) (social, environmental and economic) reporting. Comparing and using GRIs and AECA. | [1] |

| 2015 | Coloration of sustainability, innovation, and competitiveness at organizational and business level. | [24] |

| 2017 | Sustainable competitiveness includes several interrelated aspects of the concept of sustainable development. | [37] |

| 2017 | Sustainability concept of the “Triple P” (planet, people and profit) used in the Systematic Sustainability Assessment (SSA) tool for improving business performance | [38] |

| 2018 | The Enterprise Resource Planning (ERP) system for sustainable development of the organization. | [39] |

| 2018 | Defining sustainable Key Performance Indicators with the aim to control sustainability-related issues. Using the best sustainable practices in the business field. | [13,40] |

| 2018 | The Life Cycle Sustainability Assessment framework used for measuring the economic dimension of sustainable development. | [41] |

| Element | Description | Authors |

|---|---|---|

| Data Measures | Data measures are based on organizational performance and consist of data sets and numbers that are analysed together with performance indicators. These measures have to be quantifiable and reliable. | [49] |

| KPIs are based on data measures of physical characteristics of a system or process, it could be challenging, for example when measuring the key aspects of the innovation process in the organization. | [23,24,25,26] | |

| Data performance measures need to be as dynamic as the rapidly changing business environment. This indicates real time measures as an important factor. | [48] | |

| Good performance measures are quantitative, objective and not subjective. They are simple, understandable, practical, and consistent with appropriate scales and clear, timely objectives. | [46] | |

| Measurements are the magnitude or values of actual data gathered from the process based upon a standard or unit of measurement. | [47] |

| Element | Description | Authors |

|---|---|---|

| Indicators | Indicators in the process perspective are analysed as lagging (outcome) and leading indicators. Most benchmarking approaches use lagging indicators to measure the performance outcomes. | [49,60] |

| Measuring indicators are used to measure and improve the organization’s performance. These indicators need to be aligned with the organization’s strategy. | [45] | |

| There is a wide range of indicators that describe the system or process, but not all of them are related to performance. | [23] | |

| The relationship between business performance and performance measures often leads to a large number of indicators. For process management it is important to incorporate financial and non-financial indicators in balanced proportions. | [48] | |

| The Performance Measurement System (PMS) should be balanced and include indicators that are necessary and sufficient. PMS allows to identify critical performance areas and helps to define KPIs. | [13,46,54] | |

| An indicator is a parameter, which points to, provides information about, or describes the state of a phenomenon with significance and relevance to performance objectives. | [47] | |

| Companies usually use inappropriate or poorly classified indicators or compare own results with previous periods, where there were different conditions for organizations’ achievements. | [55] |

| Element | Description | Authors |

|---|---|---|

| Key Performance Indicators | Key Performance Indicators is a set of carefully selected indicators that describe the organization’s main business objectives. | [49] |

| It is important to develop the relationship between the inherent Key Performance Indicators and the particular process. KPIs are crucial for measuring and improving processes. | [23] | |

| Key Performance Indicators (KPIs) represent a set of measures focusing on those kinds of organizational performance that are most relevant to the effectiveness of current and future design of the organization or key success factors. | [46,56] | |

| KPI is one that is critical to the current and future success of the organization. Indicators should, among other things, be numerically and precisely quantifiable. | [47] | |

| The correct choice of performance indicators is an important part of the corporate strategic process and quality management, because well-defined and weighted KPIs can help realise strategic plans. | [39,55,57,59] | |

| KPIs are directly linked to business success, but defining an effective KPI that shows business benefits is not always easy. To develop a set of indicators, it is necessary to include the name, owner, formula, justification and description of KPIs. | [52,58] |

| Element | Description | Authors |

|---|---|---|

| Objectives | Objectives are set for a system, process or action. They are linked to the business strategy and they have to be relevant and achievable in a specific time period. | [49,50] |

| The key aspect is to develop balanced process improvement objectives that are described by the set of KPIs. | [23,51] | |

| Performance targets and objectives in the organization are introduced with the top to bottom approach. Performance objectives need to be realistic and measurable. | [48] | |

| There are two types of expressions of process or system performance: identifying the degrees reached in different objectives and synthesis of performance in terms of overall objectives. | [46] | |

| Organizations pursue KPIs that are defined by today’s performance objectives. Performance measurement is followed by performance analysis so that critical factors governing performance are identified and decisions are made for improvement. | [47,63] | |

| Many organizations are defining not only process objectives but also overall objectives and metrics for the organization’s sustainability and benchmarking. | [2,52,60,64] |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Medne, A.; Lapina, I. Sustainability and Continuous Improvement of Organization: Review of Process-Oriented Performance Indicators. J. Open Innov. Technol. Mark. Complex. 2019, 5, 49. https://doi.org/10.3390/joitmc5030049

Medne A, Lapina I. Sustainability and Continuous Improvement of Organization: Review of Process-Oriented Performance Indicators. Journal of Open Innovation: Technology, Market, and Complexity. 2019; 5(3):49. https://doi.org/10.3390/joitmc5030049

Chicago/Turabian StyleMedne, Aija, and Inga Lapina. 2019. "Sustainability and Continuous Improvement of Organization: Review of Process-Oriented Performance Indicators" Journal of Open Innovation: Technology, Market, and Complexity 5, no. 3: 49. https://doi.org/10.3390/joitmc5030049

APA StyleMedne, A., & Lapina, I. (2019). Sustainability and Continuous Improvement of Organization: Review of Process-Oriented Performance Indicators. Journal of Open Innovation: Technology, Market, and Complexity, 5(3), 49. https://doi.org/10.3390/joitmc5030049