Supply Risk Considerations for the Elements in Nickel-Based Superalloys

Abstract

1. Introduction

2. Characteristics of Ni-Based Superalloy Types

3. Supply Risk Assessment Method

4. Results and Discussions

4.1. Supply Risk Data

4.2. Normalization and Weighting

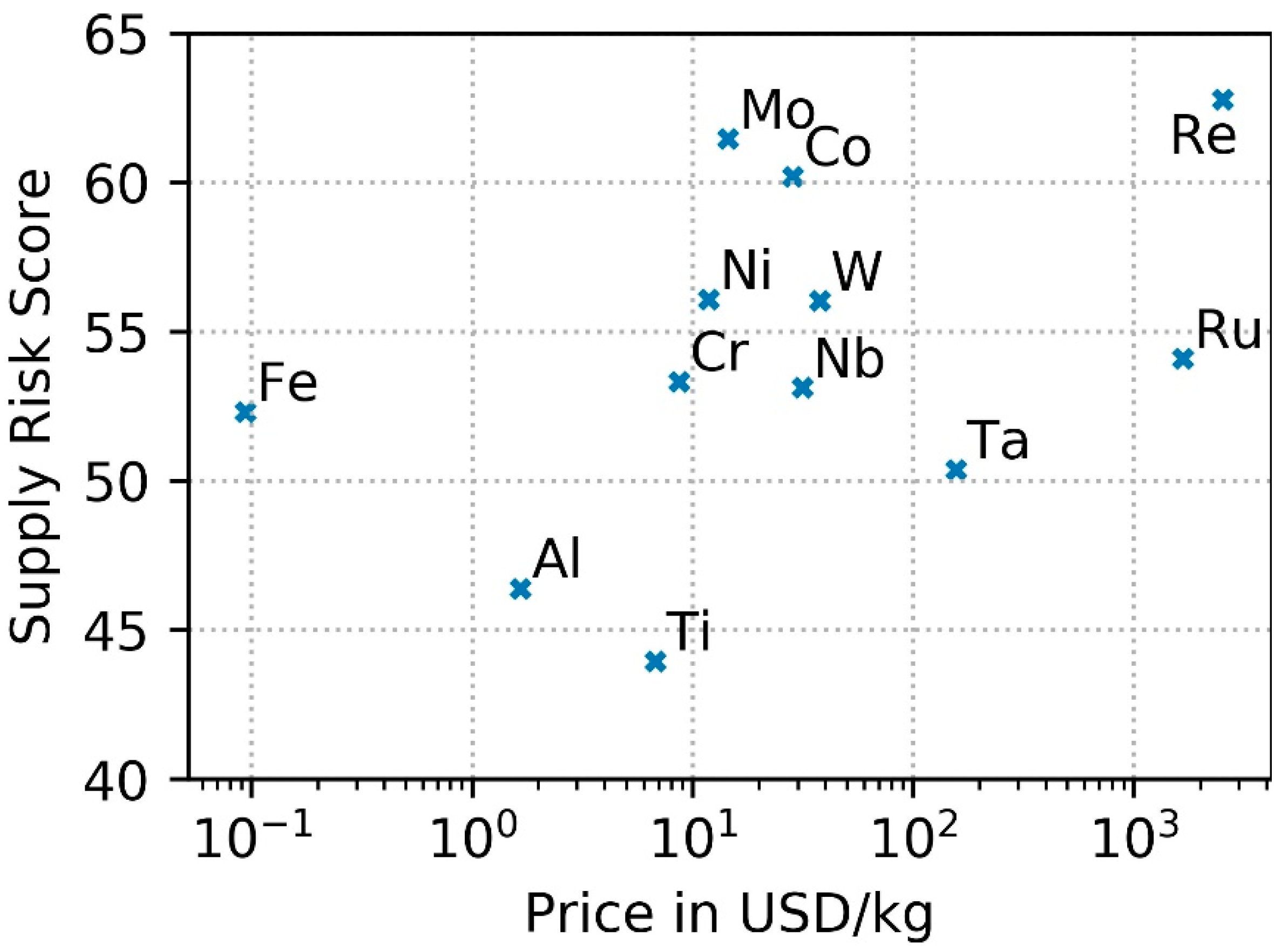

4.3. Supply Risk on the Elemental Level

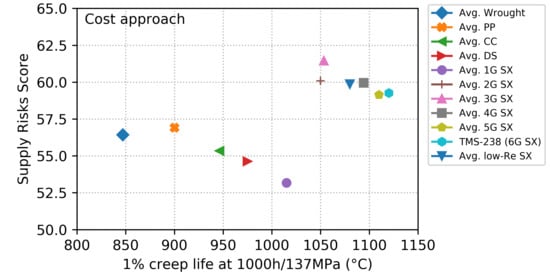

4.4. Supply Risk on the Alloy Level

4.5. Limitations

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Langston, L. Each blade a single crystal. Am. Sci. 2015, 103, 30. [Google Scholar] [CrossRef]

- Darolia, R. Development of strong, oxidation and corrosion resistant nickel-based superalloys: Critical review of challenges, progress and prospects. Int. Mater. Rev. 2019, 64, 355–380. [Google Scholar] [CrossRef]

- Reed, R.C. The Superalloys: Fundamentals and Applications; Cambridge University Press: Cambridge, UK, 2006; ISBN 9780521859042. [Google Scholar]

- Pollock, T.M.; Tin, S. Nickel-based superalloys for advanced turbine engines: Chemistry, microstructure, and properties. J. Propuls. Power 2006, 22, 361–374. [Google Scholar] [CrossRef]

- Langston, L.S. Single-crystal turbine blades earn ASME milestone status. Mach. Des. 2018, 90, 46–52. [Google Scholar]

- The Jet Engine; Rolls-Royce Plc: Manchester, UK, 2005.

- Airbus Airbus Forecasts Need for over 39,000 New Aircraft in the Next 20 Years. Available online: https://www.airbus.com/newsroom/press-releases/en/2019/09/airbus-forecasts-need-for-over-39000-new-aircraft-in-the-next-20-years.html (accessed on 12 February 2020).

- Schafrik, R.; Sprague, R. Superalloy technology—A perspective on critical innovations for turbine engines. Key Eng. Mater. 2008, 380, 113–134. [Google Scholar] [CrossRef]

- Steibel, J. Ceramic matrix composites taking flight at GE Aviation. Am. Ceram. Soc. Bull. 2019, 98, 30–33. [Google Scholar]

- Long, H.; Mao, S.; Liu, Y.; Zhang, Z.; Han, X. Microstructural and compositional design of Ni-based single crystalline superalloys―A review. J. Alloy. Compd. 2018, 743, 203–220. [Google Scholar] [CrossRef]

- Xu, L.; Bo, S.; Hongde, Y.; Lei, W. Evolution of rolls-royce air-cooled turbine blades and feature analysis. Procedia Eng. 2015, 99, 1482–1491. [Google Scholar] [CrossRef]

- Perepezko, J.H. The hotter the engine, the better. Science 2009, 326, 1068–1069. [Google Scholar] [CrossRef]

- Kharina, S.; Rutherford, D. Fuel Efficiency Trends for New Commercial Jet Aircraft: 1960 to 2014; International Council on Clean Transportation: Washington, DC, USA, 2015. [Google Scholar]

- Schafrik, R.E. Materials for a non-steady-state world. Metall. Mater. Trans. B 2016, 47, 1505–1515. [Google Scholar] [CrossRef][Green Version]

- Pollock, T.M. Alloy design for aircraft engines. Nat. Mater. 2016, 15, 809–815. [Google Scholar] [CrossRef] [PubMed]

- Millensiffer, T.A.; Sinclair, D.; Jonasson, I.; Lipmann, A. Rhenium. In Critical Metals Handbook; Gunn, G., Ed.; John Wiley & Sons Ltd.: Hoboken, NJ, USA, 2014; pp. 340–360. [Google Scholar]

- Griffin, G.; Gaustad, G.; Badami, K. A framework for firm-level critical material supply management and mitigation. Resour. Policy 2019, 60, 262–276. [Google Scholar] [CrossRef]

- Ku, A.Y.; Loudis, J.; Duclos, S.J. The impact of technological innovation on critical materials risk dynamics. Sustain. Mater. Technol. 2018, 15, 19–26. [Google Scholar] [CrossRef]

- Ku, A.Y.; Hung, S. Manage Raw Material Supply Risks. Chem. Eng. Prog. 2014, 110, 28–35. [Google Scholar]

- Duclos, S.J.; Otto, J.P.; Konitzer, D.G. Design in an era of constrained resources: As global competition for materials strains the supply chain, companies must know where a shortage can hurt and then plan around it. Mech. Eng. 2010, 132, 36–40. [Google Scholar] [CrossRef]

- Wahl, J.B.; Harris, K. New single crystal superalloys, CMSX®-8 and CMSX®-7. Proc. ASME Turbo Expo 2014, 6, 179–188. [Google Scholar] [CrossRef]

- Lipmann, A. Pratt & Whitney/Molymet Write Largest Deal in Rhenium History. Available online: https://www.lipmann.co.uk/articles/metal-matters/pratt-whitney-molymet-write-largest-deal-in-rhenium-history/ (accessed on 12 February 2020).

- Graedel, T.E.; Nuss, P. Employing considerations of criticality in product design. JOM 2014, 66, 2360–2366. [Google Scholar] [CrossRef]

- Helbig, C.; Bradshaw, A.M.; Kolotzek, C.; Thorenz, A.; Tuma, A. Supply risks associated with CdTe and CIGS thin-film photovoltaics. Appl. Energy 2016, 178, 422–433. [Google Scholar] [CrossRef]

- Helbig, C.; Bradshaw, A.M.; Wietschel, L.; Thorenz, A.; Tuma, A. Supply risks associated with lithium-ion battery materials. J. Clean. Prod. 2018, 172, 274–286. [Google Scholar] [CrossRef]

- Goddin, J.R.J. Identifying supply chain risks for critical and strategic materials. In Critical Materials-Underlying Causes and Sustainable Mitigation Strategies; World Scientific Publishing Co. Pte. Ltd.: Singapore, 2019; pp. 117–150. [Google Scholar]

- Mota, R.M.O.; Graedel, T.E.; Pekarskaya, E.; Schroers, J. Criticality in bulk metallic glass constituent elements. JOM 2017, 69, 2156–2163. [Google Scholar] [CrossRef]

- Sato, A.; Harada, H.; Yeh, A.-C.; Kawagishi, K.; Kobayashi, T.; Koizumi, Y.; Yokokawa, T.; Zhang, J.-X. A 5th generation sc superalloy with balanced high temperature properties and processability. In Proceedings of the Superalloys 2008 (Eleventh International Symposium), Seven Springs, PA, USA, 14–18 September 2008; pp. 131–138. [Google Scholar]

- Caron, P.; Khan, T. Evolution of Ni-based superalloys for single crystal gas turbine blade applications. Aerosp. Sci. Technol. 1999, 3, 513–523. [Google Scholar] [CrossRef]

- Kawagishi, K.; Yeh, A.; Yokokawa, T.; Kobayashi, T.; Koizumi, Y.; Harada, H. Development of an oxidation-resistant high-strength sixth-generation single-crystal superalloy TMS-238. In Proceedings of the Superalloys 2012, Seven Springs, PA, USA, 9–13 September 2012; pp. 189–195. [Google Scholar]

- Bloomberg. Available online: www.bloomberg.com (accessed on 14 December 2019).

- Fastmarkets Metal Bulletin. Available online: www.metalbulletin.com (accessed on 14 December 2019).

- Fink, P.J.; Miller, J.L.; Konitzer, D.G. Rhenium reduction—Alloy design using an economically strategic element. JOM 2010, 62, 55–57. [Google Scholar] [CrossRef]

- Roskill Rhenium Outlook to 2029, 11th Edition. Available online: https://roskill.com/market-report/rhenium/ (accessed on 12 February 2020).

- Kolotzek, C.; Helbig, C.; Thorenz, A.; Reller, A.; Tuma, A. A company-oriented model for the assessment of raw material supply risks, environmental impact and social implications. J. Clean. Prod. 2018, 176, 566–580. [Google Scholar] [CrossRef]

- Helbig, C.; Kolotzek, C.; Thorenz, A.; Reller, A.; Tuma, A.; Schafnitzel, M.; Krohns, S. Benefits of resource strategy for sustainable materials research and development. Sustain. Mater. Technol. 2017, 12, 1–8. [Google Scholar] [CrossRef]

- Helbig, C. Metalle im Spannungsfeld technoökonomischen Handelns: Eine Bewertung der Versorgungsrisiken und der dissipativen Verluste mit Methoden der Industrial Ecology; Universität Augsburg: Augsburg, Germany, 2019. [Google Scholar]

- USGS. Mineral Commodity Summaries 2018; U.S. Geological Survey: Reston, VA, USA, 2018.

- Graedel, T.E.; Allwood, J.M.; Birat, J.-P.; Reck, B.K.; Sibley, S.F.; Sonnemann, G.; Buchert, M.; Hagelüken, C. Recycling Rates of Metals—A Status Report, A Report of the Working Group on the Global Metal Flows to the International Resource Panel; UNEP: Nairobi, Kenya, 2011. [Google Scholar]

- Marscheider-Weidemann, F.; Langkau, S.; Hummen, T.; Erdmann, L.; Tercero Espinoza, L.A.; Angerer, G.; Marwede, M.; Benecke, S. Rohstoffe für Zukunftstechnologien 2016; Deutsche Rohstoffagentur (DERA): Berlin, Germany, 2016. [Google Scholar]

- Nassar, N.T.; Graedel, T.E.; Harper, E.M. By-product metals are technologically essential but have problematic supply. Sci. Adv. 2015, 1, e1400180. [Google Scholar] [CrossRef] [PubMed]

- Graedel, T.E.; Harper, E.M.; Nassar, N.T.; Reck, B.K. On the materials basis of modern society. Proc. Natl. Acad. Sci. USA 2015, 112, 6295–6300. [Google Scholar] [CrossRef] [PubMed]

- Herfindahl, O.C. Concentration in the US Steel Industry; Columbia University: New York, NY, USA, 1950. [Google Scholar]

- Hirschman, A.O. National Power and the Structure of Foreign Trade; University of California Press: Berkeley, CA, USA, 1980; ISBN 9780520040823. [Google Scholar]

- Buchholz, P.; Huy, D.; Liedtke, M.; Schmidt, M. DERA-Rohstoffliste 2014; Deutsche Rohstoffagentur (DERA): Berlin, Germany, 2015. [Google Scholar]

- Kaufmann, D.; Kraay, A. Worldwide Governance Indicators. Available online: http://info.worldbank.org/governance/wgi/index.aspx (accessed on 1 December 2015).

- Jackson, T.; Green, K.P. Annual Survey of Mining Companies 2016; Fraser Institute: Vancouver, BC, Canada, 2017. [Google Scholar]

- UNDP. Human Development Report 2015; UNDP: New York, NY, USA, 2015. [Google Scholar]

- Frenzel, M.; Kullik, J.; Reuter, M.A.; Gutzmer, J. Raw material ‘criticality’—Sense or nonsense? J. Phys. D Appl. Phys. 2017, 50, 123002. [Google Scholar] [CrossRef]

- Schrijvers, D.; Hool, A.; Blengini, G.A.; Chen, W.-Q.; Dewulf, J.; Eggert, R.; van Ellen, L.; Gauss, R.; Goddin, J.; Habib, K.; et al. A review of methods and data to determine raw material criticality. Resour. Conserv. Recycl. 2020, 155, 104617. [Google Scholar] [CrossRef]

- Helbig, C.; Bradshaw, A.M.; Wietschel, L.; Thorenz, A.; Tuma, A. Corrigendum to “Supply risks associated with lithium-ion battery materials”. J. Clean. Prod. 2019, 221, 899–903. [Google Scholar] [CrossRef]

- Tilton, J.E. On Borrowed Time: Assessing the Threat of Mineral Depletion; Resources for the Future: Washington, DC, USA, 2002. [Google Scholar]

- Chopra, S.; Sodhi, M.S. Managing risk to avoid supply-chain breakdown. MIT Sloan Management Review, 15 October 2004. [Google Scholar]

- Erdmann, L.; Graedel, T.E. Criticality of non-fuel minerals: A review of major approaches and analyses. Environ. Sci. Technol. 2011, 45, 7620–7630. [Google Scholar] [CrossRef]

- Achzet, B.; Helbig, C. How to evaluate raw material supply risks—An overview. Resour. Policy 2013, 38, 435–447. [Google Scholar] [CrossRef]

- Yuan, Y.; Yellishetty, M.; Mudd, G.M.; Muñoz, M.A.; Northey, S.A.; Werner, T.T. Toward dynamic evaluations of materials criticality: A systems framework applied to platinum. Resour. Conserv. Recycl. 2020, 152, 104532. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Category | ID | Indicator | Normalization | Weightings |

|---|---|---|---|---|

| Risk of Supply Reduction | S1 | Static Reach Reserves | 1/12 = 8.3% | |

| S2 | Static Reach Resources | 1/12 = 8.3% | ||

| S3 | End-of-Life Recycling Input Rate | 1/12 = 8.3% | ||

| Risk of Demand Increase | D1 | Future Technology Demand | 1/16 = 6.3% | |

| D2 | By-Product Dependence | 1/16 = 6.3% | ||

| D3 | Sector Competition | 1/16 = 6.3% | ||

| D4 | Substitutability | 1/16 = 6.3% | ||

| Market Concentration Risk | C1 | Country Concentration | 1/8 = 12.5% | |

| C2 | Company Concentration | 1/8 = 12.5% | ||

| Political Risk | P1 | Political Stability (WGI-PV) | 1/12 = 8.3% | |

| P2 | Policy Perception (PPI) | 1/12 = 8.3% | ||

| P3 | Regulation (HDI) | 1/12 = 8.3% |

| Indicator | Dimension | Risk | Al | Ti | Cr | Fe | Co | Ni | Nb | Mo | Ru | Ta | W | Re |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| S1 | years | ⊖ | 94 | 107 | 16 | 60 | 58 | 36 | 68 | 52 | 1029 | 84 | 35 | 50 |

| S2 | years | ⊖ | 184 | 258 | 384 | 161 | 1201 | 60 | >200 | 68 | >200 | >200 | 306 | 221 |

| S3 | % | ⊖ | 16 | 6 | 13 | 22 | 16 | 27 | 10 | 11 | 11 | 1 | 37 | 9 |

| D1 | % | ⊕ | 0 | 20 | 0 | 0 | 90 | 0 | 2 | 0 | 3 | 120 | 0 | 150 |

| D2 | % | ⊕ | 0 | 0 | 2 | 1 | 85 | 2 | 2 | 46 | 100 | 28 | 5 | 100 |

| D3 | qualitative | ⊖ | 28 | 42 | 20 | 24 | 42 | 29 | 20 | 28 | 43 | 44 | 35 | 48 |

| D4 | qualitative | ⊖ | 44 | 63 | 76 | 57 | 54 | 62 | 42 | 70 | 63 | 41 | 53 | 90 |

| C1 | HHI | ⊕ | 3057 | 1221 | 3033 | 3321 | 3141 | 1450 | 8266 | 2889 | 6958 | 2346 | 6679 | 3374 |

| C2 | HHI | ⊕ | 2221 | 1317 | 1854 | 2269 | 1902 | 1191 | 6441 | 2183 | 1373 | 2002 | 6920 | 2533 |

| P1 | qualitative | ⊖ | −0.24 | −0.21 | −0.36 | −0.33 | −1.20 | −0.21 | −0.20 | −0.15 | −0.29 | −1.04 | −0.44 | −0.44 |

| P2 | qualitative | ⊖ | 61 | 51 | 58 | 68 | 50 | 56 | 59 | 62 | 51 | 49 | 47 | 73 |

| P3 | qualitative | ⊕ | 0.79 | 0.72 | 0.73 | 0.82 | 0.78 | 0.81 | 0.79 | 0.79 | 0.70 | 0.53 | 0.75 | 0.84 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Helbig, C.; Bradshaw, A.M.; Thorenz, A.; Tuma, A. Supply Risk Considerations for the Elements in Nickel-Based Superalloys. Resources 2020, 9, 106. https://doi.org/10.3390/resources9090106

Helbig C, Bradshaw AM, Thorenz A, Tuma A. Supply Risk Considerations for the Elements in Nickel-Based Superalloys. Resources. 2020; 9(9):106. https://doi.org/10.3390/resources9090106

Chicago/Turabian StyleHelbig, Christoph, Alex M. Bradshaw, Andrea Thorenz, and Axel Tuma. 2020. "Supply Risk Considerations for the Elements in Nickel-Based Superalloys" Resources 9, no. 9: 106. https://doi.org/10.3390/resources9090106

APA StyleHelbig, C., Bradshaw, A. M., Thorenz, A., & Tuma, A. (2020). Supply Risk Considerations for the Elements in Nickel-Based Superalloys. Resources, 9(9), 106. https://doi.org/10.3390/resources9090106