1. Introduction

In recent years, the travel and tourism industry has been identified as a prominent contributor to greenhouse gas emissions via air, sea, and road transportation. The United Nations World Tourism Organization reports that tourism-related transport emissions represented 22% of global transport emissions in 2016 [

1]. Luggage and travel bags are an inseparable feature to all travellers that add to the environmental burden of the travel industry. With an estimated 4.5 billion passengers carried by scheduled flights in 2019 [

2] and a luggage market estimated at USD 22 billion in 2019 [

3], luggage requires a closer examination.

Indeed, as a product category, luggage has failed to receive adequate academic attention in terms of environmental impacts and sustainability issues, presumably because the impact of carbon emissions associated with travel, especially air travel, dwarfs that of the luggage industry, which is arguably smaller. Nonetheless, structured luggage and travel bags are usually composed of moulded polymer components, aluminium tubes, plastic zippers, and synthetic rubber wheels, which are combined mechanically and chemically with synthetic textiles and various reinforcement materials. When these composite products reach their end-of-life (EoL) stage, they can be quite problematic to collect and manage. In addition, according to the authors’ understanding of waste management, luggage is not easily classified into either disassembling and recycling or recovery processes.

In the USA, luggage waste is classified under Miscellaneous Durable Goods for waste management, and of this category, only 2% was recycled in 2018 [

4]. In the EU, luggage and travel bag waste fall into the broader category of municipal solid waste (MSW), which is considered to be recycled at an average rate of 48% [

5]. However, the European MSW recycling rate accounts for the management of recyclable waste materials (i.e., plastics, metals, glass, paper/cardboard) and organic waste (e.g., food waste, grass clippings, leaves) that are easily distinguished and can be separated at the source (e.g., household). Bulky waste, a category to which luggage is likely attributed, is not properly classified, and therefore anecdotal evidence suggests that any attempt to correctly process it using the European List of Wastes (LoW) [

6] is futile. This could explain the lack of detailed statistics on individual bulky waste categories, including luggage, which hinders the generation of any insights into luggage and travel bag waste management. Local councils in the UK offer bulky waste collection at a price; however, specific guidelines for the disposal of luggage are not readily available. Often, the luggage collected is transferred to a Household Waste Recycling Centre (HWRC) where it would become part of the same waste code as other mixed rigid plastics (e.g., garden furniture, code: 20 01 39), or it is mixed with other bulky waste (with the LoW code 20 03 07) of which the fate of depends on the waste management practices employed by different authorities and HWRCs; in the UK, the majority of bulky waste almost certainly goes to either landfills or incineration (the likelihood of either varies in other countries). This, unfortunately, leaves consumers with little clarity as to whether luggage may be recycled [

7].

Aside from their design characteristics and EoL management, luggage as a product category can be characterised by an intertwined relationship between different stakeholders (including the owner)

vis à vis its use and handling. During the luggage’s use phase, the owner is seldom in control, or even in sight of their luggage, having agreed to the responsibility and liability for carriage to airlines, upon ticket purchase for air travel. When not in use, luggage is kept in storage for short, medium, and even long periods, seeing infrequent use [

8]. This presents certain specific challenges as luggage use pertains to factors outside of the control of the user, such as the occasional damages occurring when the luggage is under the airlines’ control; as well as accidental damage due to weather conditions, and so on.

The changes brought about by the COVID-19 pandemic, where business-related travel is being questioned and the adoption of online video conferencing becomes ubiquitous [

9,

10], have urged the travel sector to rethink their business models. Some of the main questions that arise relate to how luggage can be utilised more intensively and efficiently, for longer periods, and how they can become more sustainable in the future. As a product, luggage is designed to offer a service, lending itself to the development of a new business model that could create value for consumers and businesses alike through its reuse [

11,

12,

13], a practice that is increasingly gaining traction.

To this end, product-service systems (PSS) can provide a means with which to promote reusability in the luggage industry, and in turn, monitor and prevent waste generation and promote dematerialisation and resource efficiency through circular economy principles [

14,

15]. PSSs are business models (BMs) that can offer the opportunity to decouple the ownership of materials, components, and products from the provision of function. This can lead to reduced primary resources and energy consumption, improved resource management, and optimisation in value chains [

12]. However, despite the potential for PSSs to help drive the sustainability agenda, the adoption of such models remains limited [

16,

17], especially in business-to-consumer (B2C) commercial relationships [

16,

18].

Globally recognised brands such as IKEA are helping to re-frame the narrative on the re-sale of furniture and homewares [

19] instigating the transition. Many high-end fashion and luxury brands are now offering their versions of PSS. One such example is the ThredUp—Rent the Runway (RtR) partnership, a US-based apparel rental and subscription service that uses the PSS model to encourage swapping; from clothes to inspiration and ideas. ThredUp successfully began trading on the NASDAQ in March 2021 [

20], becoming the first largest online consignment and thrift shop. This booming economic growth via the PSS model could potentially drive more interest in the long-term product maintenance and repairability, with the travel goods industry potentially wanting to grasp opportunities to generate revenue.

The use of PSSs in the travel goods industry is wide-ranging in the literature on luggage (or baggage) inspection techniques and airport security scanning systems research [

21,

22], and occasionally on luggage design with a focus on polymer composites, design-engineering and ergonomics studies [

23,

24,

25]. However, academic research into the production, distribution, usage and EoL of luggage and travel goods within a PSS framework is lacking. While a PSS can create the conditions for sustainable luggage handling and management [

26,

27], it will not necessarily lead to better environmental or market outcomes as these depend on the context and PSS adoption and implementation [

28,

29]. Meanwhile, PSS implementation could lead to capability development in the travel-goods industry, providing businesses with certain strategic advantages [

30]. This points to a research gap, which this study aims to fill in by exploring the feasibility of PSS models in the luggage and travel goods industry in a European context, and their potential to instigate sustainability. Mont [

11] outlines three main areas of uncertainty with regard to PSS feasibility: (i) the readiness of companies to adopt; (ii) the readiness of consumers to accept; and (iii) associated environmental implications.

Following that, the study proposes a typology of pathways to PSS adoption in the luggage sector and investigates their potential implementation in the future towards promoting sustainability. Using a mixed-methods approach, the study gathers qualitative data from consumers and luggage manufacturers, to shed light on two main areas: the readiness of consumers to adopt the PSS concept, and the industry’s perceptions and attitudes that could promote or impede PSS adoption in the luggage sector. The data collected are critically assessed in their usefulness in creating the appropriate socio-economic and business conditions, to support the emergence of PSSs that could unlock environmental, social, and economic benefits promoting a sustainable circularity in the travel goods industry.

2. Literature Review

PSS models have been developed from servitisation concepts from the late 1980s and 1990s [

14,

31,

32]. A concise and often-cited definition of a PSS is “

a system of products, services, supporting networks and infrastructures that are designed to be competitive, satisfy customer needs and have a lower environmental impact than traditional business models” [

11]. PSSs are also known by the terms Integrated Product Service Offering (IPSO) [

29], and Sustainable Product-Service System (S.PSS) [

33,

34].

As described by Manzini and Vezzoli [

35], there are three main categories of PSS: (i) services that add value to a product life cycle, e.g., by extending its use; (ii) services that provide enabling platforms for customers, e.g., for mobility or accommodation functions; and (iii) services that provide a result to a customer, e.g., clean laundry, or heated water. Tukker [

28] provides a clearer definition of these three primary categories and some sub-categories of PSSs in a diagrammatic form, shown here in

Figure 1, which are

product-oriented,

use-oriented and

results-oriented. These, have since become common nomenclature.

A

product-oriented PSS is largely based on the conventional sale, purchase, and ownership transfer of a product, but with additional services added. These services could be maintenance contracts, take-back agreements at the product’s EoL stage, and advice or consultancy on how best to utilise the product [

28]. An example of a product-oriented PSS is purchasing office equipment with an after-sales service agreement that involves on-site checks and repairs to keep the equipment in good working order.

The

use-oriented PSS is sometimes referred to as an

access-based consumption (ABC) model [

36] or a

user-oriented model, and is generally represented via product leasing, renting or sharing, and pooling schemes. In all three schemes, both the ownership of the product and responsibility for its maintenance and take-back remain with the provider. The customer can only purchase the use of, or access to, the product. Leasing usually allows the user (or user group) to have unlimited access to the product within a time frame (e.g., leasing office equipment across a period of many months or years), whereas renting or sharing requires that the product be used sequentially by multiple users (e.g., renting a car for a few days). Product pooling allows the product to be used simultaneously between users (e.g., car-pooling with multiple passengers) [

28].

A results-oriented PSS can be described as a model where service is sold, with the products involved in the provision of the service identified by the provider and not necessarily by the customer. For example, this could be the provision of ambient lighting to office space, without specifying the exact type or amount of lighting elements to be installed.

Regarding the feasibility of a given PSS, a barrier to the success of business-to-business (B2B) PSS models, which often involve industrial equipment and other investment goods [

37,

38,

39] is their translation to B2C models. Another barrier to the adoption of PSSs by businesses and consumers is the potential for

rebound effects, where the positive effects of a PSS are cancelled by unintended negative effects [

40,

41]. Rebound effects are usually associated with environmental impacts. Goedkoop et al. [

12] conclude that for PSS to be truly sustainable and avoid rebound effects via alternative consumption, the perceived value must be high in combination with low environmental impact. In effect, any newly launched PSS should be priced such that there are no savings made which could then be spent elsewhere on energy and material-consuming goods and services.

Further barriers to use-oriented PSS uptake are the environmental impacts of leasing and rental models [

42,

43]. The amount of energy and emissions related to delivery and pick-up services, dry cleaning and sterilisation, and potential repairs, is likely to negate any impact reduction through the manufacture of fewer physical products. By way of example, Johnson and Plepys [

43] measured the environmental impacts of a fashion rental BM in Sweden, using Life Cycle Analysis (LCA), and presented several stark implications for consumer behaviour. They state that “

Consumers who rent clothing should fully replace their purchasing needs and avoid partial substitution” [

43] in addition to wearing the rented garments multiple times during the rented period [

43]. The delivery and pick-up aspects could be addressed partly by the P2P sharing BM typology, where consumers can lend and borrow their luggage to those within their geographic area, ideally exchanging via public transport or on foot. Currently, though, this is not something attracting consumers to engage with, despite studies showing that familiarity with digital sharing culture and service (e.g., smartphone apps, social media platforms and online ordering) can be a driver of commercial success in PSS [

44].

3. Methods

A blend of empirical and secondary research data were compiled in a largely inductive process to explore the entrenched thinking and emerging sentiments from consumers and experts alike on the reusability of travel goods via the PSS. The data collection took place in two stages. In the first stage, we employed an explorative survey targeting consumers; in the second stage, we conducted in-depth semi-structured interviews with experts working in the travel goods industry to identify consumers and experts, leading to critical discussion points on PSS feasibility.

The academic literature about the various facets of PSS was explored via widely known online search engines and academic platforms (e.g., Web of Sciences, Scopus, ScienceDirect). For up-to-date statistics relating to travel goods and associated markets, various sources were accessed such as websites of the European Union, US and British government sites, and business statistics sites such as Forbes and Statista. Conventional and emergent BMs within the travel-goods market were identified, researched and mapped into four discrete PSS BM types to make sense of their potential implementation.

3.1. Online Explorative Survey

The online consumer sentiment explorative survey was conducted via an anonymous online questionnaire to collect data from luggage-owning travellers living in the UK and Europe. The survey was restricted to adults over 18 and the purpose of the questionnaire was to understand perceptions towards both product-oriented and use-oriented PSSs. The questionnaire was composed of 37 questions using the Qualtrics XM platform [

45] and was divided into four sections: demographics, current luggage ownership, and use, maintenance and disposal, and luggage rental and leasing. Instead of focusing only on consumer behaviours, the study collected data on perceptions of luggage leasing and renting potential. Ranking-style questions were employed within the questionnaire, to elicit sentiment and preference, and, also, to gauge the relative popularity of each response (see

Supplementary Material). Qualtrics XM was selected as it is a trusted online survey platform in higher education organisations in Europe and the US [

46] and is also used by the National Health Service (NHS) in the UK [

47]. The questionnaire was distributed via email, web, SMS, and social media.

The survey took an average of 10 min to complete. The survey was launched on 1 July and it automatically closed at 11:59 p.m. on 3 August 2021. The data were anonymised before their analysis, including deleting the postcode. Participation in the online survey was promoted via social media accounts on LinkedIn, Facebook and Instagram and via snowballing. Facebook and Instagram were among the top four most popular social media platforms in the UK in 2019; hence, their selection.

3.2. In-Depth Expert Interviews

A sample of 10 experts from across 10 different brands and nationalities (British, German, French, Chinese) was selected to capture the views of senior product development and marketing managers within the travel-goods industry. The experts were selected based on the following criteria: (1) had a direct professional association with the travel-good industry, working for one of the brands explored in the survey; (2) represented a specific speciality, e.g., sales management, marketing-communications, product-marketing and new product development; (3) had a direct relationship with the sustainability team with the business they represented.

The purpose of the interviews was to gauge the experts’ opinions regarding the existence of servitisation in the industry and thoughts on how PSS could be adapted to the travel sector in the future (see

Supplementary Materials). Five experts were finally recruited via professional associations and former working relationships—the rest were unresponsive. Employing Bogner and Menz’s [

48] typology of interview strategies, the semi-structured interviews with the experts were classified as

Interviewer as Co-Expert, within a type of interaction specified as

the theory-generating expert interview. The specialist competence is similar and specialist knowledge and vocabulary are shared to develop a theory through induction, while revealing knowledge and insights within the given thematic framework [

48,

49].

All interviews were conducted between 12 and 28 August 2021. The interviews lasted about one hour each, they were conducted over Zoom with the auto-caption function enabled and were audio-recorded to allow for automatic transcription, which was then checked for accuracy before thematic analysis. During the interviews, participants answered a series of questions about their understanding of sustainability in the travel-goods industry, the customer needs, and the potential application and barriers to PSS adoption (such as renting and leasing) in the travel goods/luggage market and their impact on their business. The interview protocol can be found in

Supplementary Materials. It contains seven specific questions (Q#) and one open-ended question. Q1 and Q2 were designed with the aim to identify the company’s priorities in terms of sustainability and whether such considerations have started to gain precedence in the travel-goods industry. Q3 was designed to investigate customer needs and how the company captures and utilises this knowledge in designing its strategy. Q4–Q6 were aimed at gathering the views of the industry on the likelihood of adopting the PSS in their business, the degree of adoption needed to improve their sustainability credentials, and the barriers perceived in doing so. Q7 was designed to investigate the challenges related to the “if” and “how” of PSS adoption. Finally, the open-ended question was designed to investigate the company’s ideas, insights and concerns with sustainability and the need for changing their BM.

4. Results

4.1. PSS BM Typology

PSS business model types were assessed for relevancy, and four hypothetical models were created using evidence from the literature. The typology presented in

Figure 2, (diagrams 1–4) combines visual aspects of systematic flow charts with graphical value mapping to give a depiction of product, data, and value flow, along with centres of energy and resource consumption via various processes, such as cleaning the luggage and EoL management. The intention is to create a visual structure for analysis and comparison. For clarity, the diagrams cannot be entirely comprehensive in terms of data ownership and transfer within each model which, as discussed, is an important aspect of use-oriented PSS BMs.

Typologies 1 and 2 describe the relationship a luggage manufacturer/brand owner could have with a customer across the life cycle of a product, with a product-oriented PSS (Typology 1) and a use-oriented PSS (Typology 2). Both concentrate on a notional ‘Direct to Consumer’ (DTC) brand (as opposed to wholesale) with vertically integrated production (i.e., the luggage manufacturer/brand owner owns its production facilities, usually ensuring a shorter supply chain). The potential outsourcing of production, cleaning and EoL management from the luggage manufacturer/brand owner to other stakeholders in the system (e.g., materials, components and product suppliers) is shown below the diagrams in pale grey. This is to indicate the additional levels of complexity involved in the processes depicted, given the prevalence of outsourced production in the travel-goods industry. Typologies 3 and 4 are elaborations of use-oriented PSSs, enabled and distributed largely by online digital technologies. They indicate how intermediary rental companies can create BMs with value propositions utilising their online platforms with, the physical products of separate luggage brands (Typology 3), and through users sharing their physical products (Typology 4).

Typology 1 shows that ownership is transferred to the customer, but the luggage manufacturer has full responsibility for the cleaning and maintenance and eventually the EoL processes. With each transfer of the product from the customer to the luggage manufacturer/brand owner, data are collected about user habits or potential physical weak points on the product. Shown as a dotted line box between the manufacturer/brand owner and the customer (and in other areas on other typology diagrams) is the logistics provider (for example DHL or FedEx) that can benefit economically from deliveries to and from the customer.

Typology 2 describes the relationship between the luggage brand and multiple customers who could lease (or rent) a piece of luggage for a pre-agreed period. As with Typology 1, the luggage manufacturer has full responsibility for the maintenance, cleaning and EoL processes. Again, it is quite likely that the brand would engage third parties (i.e., suppliers) to carry out these processes (shown below in pale grey). Significant here is that each time a piece of luggage is transferred between the manufacturer/brand owner and customer, both economic value and data (which has a value) are also transferred.

Typology 3 depicts a situation where a rental/leasing intermediary purchases products from a luggage manufacturer/brand owner to then rent or lease out to customers. It becomes the rental company’s responsibility to manage the cleaning and maintenance of products coming back and forth from customers, and to manage the EoL process. Herein, we assume luggage returns to the manufacturer/brand owner at the EoL stage. Notable here is the potential for multiple transfers of data and economic value between the rental platform and customer, but only a single transaction between luggage manufacturer and customer (the rental agency in this case).

Typology 4 is a peer-to-peer (P2P) rent-share network, managed by an intermediary. In this situation, consumers borrow a piece of luggage from other customers (i.e., consumers) via an online platform with pricing set by the consumer themself. The product delivery and return method are agreed upon between the lender and borrower, as are cleaning and maintenance. The online intermediary provides the platform for communication between parties, takes a percentage of the rental fee from both the borrower and lender, and provides a method of insuring both parties to encourage correct usage and return of the product. If the sharing is carried out within a radius that does not require private motorised transport (i.e., the exchange is completed on foot or by public transport) then this typology could indeed have positive environmental impact benefits.

These typologies were examined through discussion with industry experts (in

Section 4.2). They were found to be relevant if not convincing to the experts for largely economic reasons. It was generally perceived that typologies 3 and 4 would not currently be commercially viable for most existing luggage brands, whereas typologies 1 and 2 could potentially return economic value and were thus preferred.

4.2. Expert Interviews

The group of five industry experts interviewed represented two brands within one of the world’s largest luggage manufacturing groups, a company within a global luxury conglomerate, and one global premium lifestyle brand that is also part of a larger commercial group, and which produces a range of products in addition to luggage. While all interviewees are high-level managers and directors within their respective companies and have high degrees of control over product development and related activities, none are board-level ‘C-suite’ directors (e.g., Chief Executive Officer, Chief Operating Officer).

The first interview question centred on the travel industry’s reaction to a reported increase in sustainability concerns among travellers following the outbreak of COVID-19. This drew a wide selection of responses; from the identification of recycled materials as a primary action to carbon-neutral declarations, discussion of product quality and durability, and travel frequencies that may be more prevalent in the coming years. Regarding the specific nature of the question and the mixed views elicited, it was clear that no industry-wide perspective on sustainability currently exists.

Discussing major factors driving the luggage industry towards greater environmental sustainability, the risk versus opportunity and shareholder value featured as the most important themes. As both brands represented belong to publicly listed companies, there was a recognition of share price and the need to develop and comply with corporate social responsibility (CSR) guidelines to attract and maintain investment. Some of this communication on compliance was described as greenwashing. It was noted that the development of corporate communication strategies for sustainability is now a necessity for all brands, whether or not these strategies lead to measurably effective actions.

The potential for government-driven regulatory action that might force change within the industry was acknowledged as a slight possibility but was seen as less likely to drive change in the short term compared to profit-imperatives related to sales, as well as other forms of commercial pressure. To this end, a comment was made that large retailers (in Europe and UK) are now introducing measures to stock only products that adhere to their own “Green-Label” product sustainability guidelines, possibly to facilitate their own CSR compliance. If future regulations in the form of manufacturer take-back directives were to occur, it was agreed that this would prove difficult for most of the industry in the West to cope with, due to the prevalence of Far-East production, fragmented supply chains, and wholesale distribution. Potential take-back directives were deemed more achievable in vertically integrated and DTC businesses, where a brand owns the means of production (finished goods factories) and distribution (online/offline stores). It was also mentioned by most interviewees that luggage brands would need to rethink their product design approach towards embracing design for disassembly, but how achievable this might be was not elaborated on.

When asked whether customers were in search of new or enhanced services within the luggage market, the issues of logistics and distribution consistently came up as an important factor—more so than sustainability issues. One manager called the high consumer expectations for near-instantaneous delivery after their online purchase, “The Amazon mentality”. For the more premium brands represented, the trend for mass-customisation in consumer products (Horizon 2020 European Commission, 2021) was mentioned as something sought after by their customers. It appears, however, that product-oriented and use-oriented PSS models are not being actively considered by luggage brands, nor requested by consumers. One manager noted that where their brand had implemented a product-oriented PSS in the form of an extended warranty programme with sustainability goals promoted, the consumer take-up had been limited.

Managers from the more premium brands also claimed that their customer care programmes, including product warranty, have been offering a sustainability-oriented service already, by concentrating on maintaining and extending product life. This type of Value-Retention Process [

50], could encourage customers to question the value of product warranties more carefully and avoid (what one interviewed expert called)

spurious guarantees. Further on questions into use-oriented PSSs, it was identified that retail price points for luggage were rarely high enough to encourage the consideration of use-based models (unlike car rentals, where purchase prices are considerably higher). Consumers can always find luggage at a price that suits them, irrespective of the related environmental issues. According to all managers, their brands had explored use-oriented PSSs to some extent (some beginning around 2010) and had concluded that the price-value equation did not work well enough for either consumer or provider, to warrant the actual implementation of actual schemes.

Regarding rental and/or leasing, hygiene was consistently highlighted as a barrier to adoption and seen to be most likely the consumer’s primary concern. Beyond the emotional and hygiene aspects of ownership versus access, two further themes were evident here. The physical logistics of providing a reliable rental system was cited as something very difficult and probably not commercially viable at this moment, and secondly, the business proposition of access-based consumption was in almost direct opposition to the conventional purchase-with-warranty proposition, i.e., requiring a comprehensive business model transformation.

4.3. Consumer Sentiment Survey

The survey generated an overall sample size of 110 respondents. Whilst it is acknowledged that the sample size is not large, the responses still provide meaningful insights into the research. A demographic breakdown shows the sample is 55% female, 40% male, with 5% non-binary or preferring not to say. The sample is well distributed across age groups, with 11% of respondents being from the 18–25 age group, 20% from the 26–35 age group, 42% from the 36–45 age group, 18% from the 46–55 age group, and 7% from the older than 56 age group; 2% of the respondents preferred not to say. The sample is 60% UK and 35% EU and Non-EU European nations, with 5% preferring not to say. The sample is more than 60% in full-time employment and very well-educated, with more than 85% of respondents holding a bachelor’s degree or higher, 31% with master’s degrees or higher and 8.5% with doctorates. These levels of education are much higher than national averages in EU European countries and the UK [

51] however, when cross-sectional filtering was performed between the higher and lower educational levels attained, the variation in results was not significant.

Also, to be noted is that 15% of respondents have worked or are working in the travel-goods industry, and there were certain respondents who could be termed as either “frequent travellers” or occasional travellers by frequency, but again these groupings showed no meaningful differences within results. Various other filters were applied to detect data categories beyond what was visible through demographic grouping and the most notable difference between respondents who claimed interest in use-oriented PSS and those who did not. While the data suggest there may be two different mindsets at play here, it is too simplistic to suggest that the PSS-interested respondents are aware or concerned with sustainability issues per se. Responses to certain other questions, especially those related to the repair and disposal of luggage, reveal contradictory opinions from both groups.

Participants were asked to answer travel frequency-related questions based on their pre-COVID-19 travel experience to gain an understanding of ownership of luggage types and travel habits. Respondents across all demographics thought they would be travelling a similar amount when COVID-19 pandemic restrictions were lifted, although 34% believed they would be taking fewer trips for longer. An overwhelming 95% and 97% of participants owned pieces of both small cabin-size and large check-in-size luggage, respectively. Cabin-sized luggage was used up to 10 times per year by 81% of people, whereas large check-in size luggage was used less than 5 times per year by 83%, which clearly shows there are long periods where large luggage sits unused. When asked about ownership by brand, over 40% were able to name a single well-known brand as their primary luggage used, with all other brands recording 5% or less, with 12% of respondents not knowing their brand of luggage.

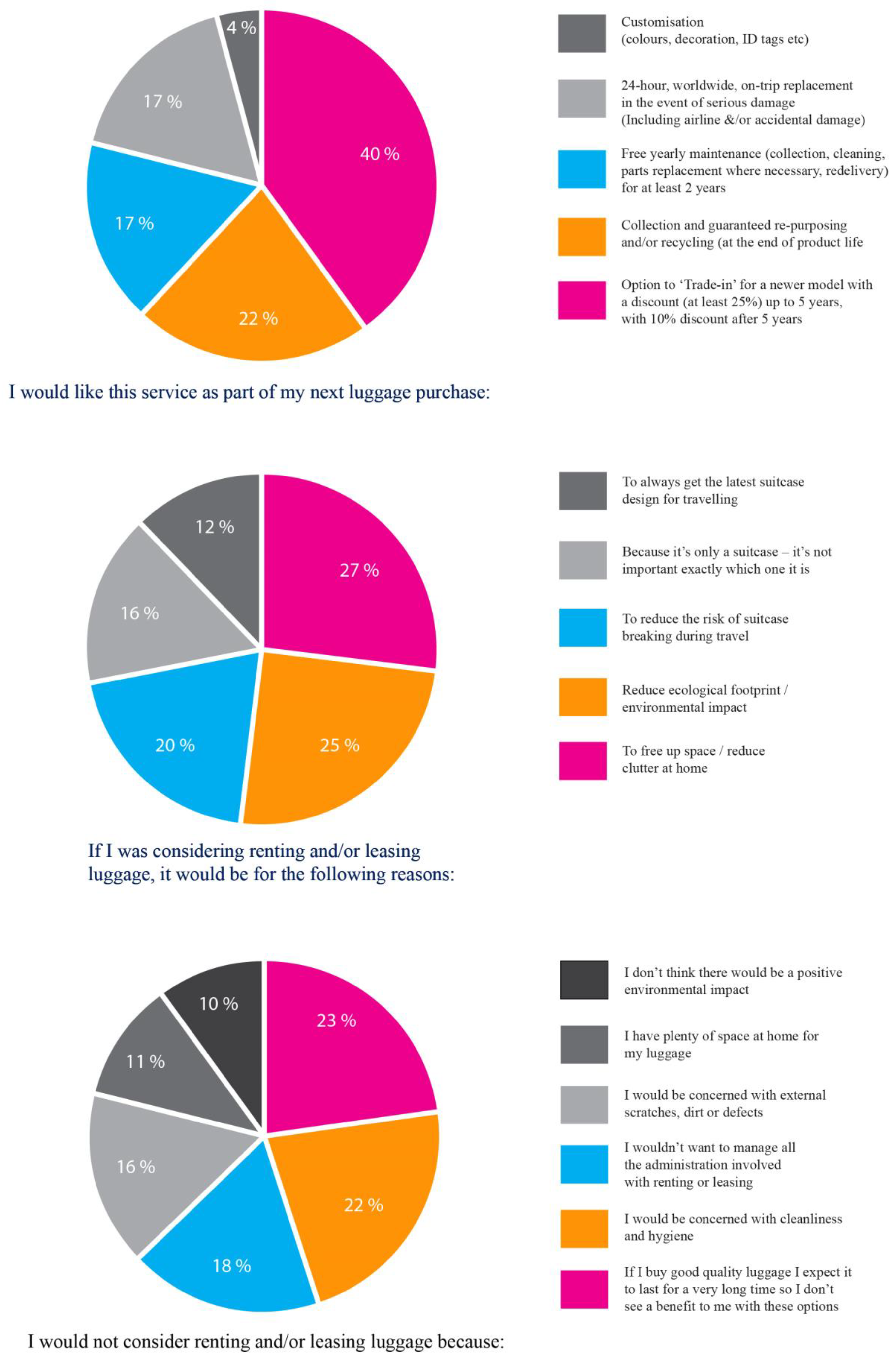

Users’ sentiments toward their luggage, in terms of warranty value, repair status, and disposal methods, were the focus of the third section of the survey. Less than 14% of participants bought their current luggage with the warranty as a primary consideration, and 57% were neutral (‘neither agree nor disagree’) when asked whether their warranty represented good value, suggesting a lack of interest or concern in this area. A clear majority (70%) would be more likely to repair large luggage than cabin-size luggage, despite cabin luggage being used much more frequently. Around 54% of respondents stated that they have never had their luggage repaired, and 12% even claimed they wouldn’t repair their luggage. Around 55% of the respondents claimed that they have left broken luggage for municipal waste collection as the most common form of disposal, with 31% disposing of still-functional luggage the same way (with municipal solid waste) suggesting that this was due to the luggage being unwanted. When given options for product-oriented services associated with a new luggage purchase, 40% of all respondents chose a trade-in for a discount on a new item. Following this option, a guaranteed re-purposing–recycling EoL service proved narrowly more interesting to consumers than maintenance and repair services (

Figure 3). Notable is that customisation was the lowest priority by far, despite several experts interviewed for the study claiming this as an important area of commercial consideration. Interestingly, when comparing the answers of PSS-interested and un-interested respondents, the trade-in option was preferred by 54% and 26%, respectively, suggesting very different views on this point.

In the final section of the questionnaire, participants were asked to rate their interest in use-oriented PSS models such as renting, leasing, subscription, and P2P sharing models for luggage usage. A sizeable 30–45% (exact percentages vary depending on the model in question) of total respondents were not interested; however, the remaining majority of around 60% showed some level of interest in these models. Around 25% of those interested in renting or leasing cited the reduction of environmental impact as their top consideration. This came narrowly behind saving space and reducing clutter in the home at 27%. Avoiding management of damaged or broken luggage was the third priority in this category (see

Figure 3). For the general sample, the least popular form of PSS was the P2P model. However, 45% of those who had already professed interest in use-oriented PSSs still gave a positive response to the idea of renting their luggage to others through a P2P platform and 58% to the idea of renting luggage from others via the same method.

The questionnaire contained several questions regarding potential pricing for renting, leasing and subscription, and although these data should be approached with caution due to the limited sample size, there are some interesting results nonetheless. Whether reflecting on renting (short term) or leasing (longer term), respondents were twice as likely to be interested in large-size luggage than small. When given a sliding scale of price options (where renting or leasing becomes cheaper with longer contracts), the most popular rental options for large luggage were GBP 2/EUR 2 per day (51%) followed by GBP 5/EUR 5 per day (38%) and the most popular leasing option was GBP 25/EUR 25 for 1 year (at 41%). While the rental figures are not entirely economically unrealistic in 2021 (depending on rental periods), they suggest that many people cannot fully conceive a reasonable price-value equation for this typology of PSSs, compared to a conventional purchase-ownership transaction.

When measuring total responses, and when filtering for those claiming an interest, the two primary barriers to the adoption of use-oriented PSSs were hygiene concerns, and the belief that purchasing good quality luggage makes the proposed alternatives irrelevant (see

Figure 3). These two answers accounted for 22% and 23%, respectively, of all responses. The third reason was the concern that there would be too much administration and hassle involved in the use-oriented systems at 18%, although this third reason was slightly less a factor when filtering for younger respondents.

Only 10% believed that there would not be a positive environmental impact on the use-oriented PSS models although this may reflect a lack of reliable offers and reliable sustainability information available in this area. The final question raised additional associations of buying good quality luggage and clarified that much of the total sample preferred the idea of purchasing second-hand or re-sale refurbished luggage from a trusted brand, rather than renting or leasing luggage. Measuring the responses of those interested in use-oriented PSS with those not interested, here again, there was a notable disparity, with 67% of interested respondents preferring the re-sale option compared to 54% of not interested.

6. Conclusions

Major stakeholders in the luggage industry are aware of the sustainability issues associated with their business, but do not have a clear nor shared vision of how to manage these issues. This seems partly due to a viewpoint that commercial aviation, which plays a measurably larger role in global carbon emissions than the comparatively small luggage industry, will remain a dominant form of travel. Many consumers, despite the implications of continuing to travel as before, appear open to engaging in new and potentially more sustainable models of usage and ownership; however, there is a distinct lack of attractive offers available in this space, as well as issues associated with the perceived risk of damage accountability and hygiene.

Nonetheless, the use-oriented PSS typology in the luggage industry can be a catalyst for change. Luggage is a product that is often moderately or rarely used, it takes up space and, most importantly, it can be detached from possession as the infrequent use reduces the sense of ownership. Confidence in sharing luggage needs to be developed based on customer-brand trust to maintain a relationship that will drive the rollout of this model and increase loyalty. This can be supported by online sharing platforms and technologies such as distributed ledgers, where higher-value luggage production with a smaller overall pool of products will become possible. Effectively, this would be disrupting the current norms and push through for clever design, use of durable materials, and convenient maintenance and repair services in the luggage industry as well as other product manufacturing sectors. Advanced leasing and sharing model(s) that suit different needs and match people’s demands and expectations is a way to transition to circularity. While achieving this presents organisational and logistical challenges, it is likely to initiate a paradigm shift in current BMs away from a reliance on product ownership and towards greater levels of service provision that can generate a diverse pool of revenues. The challenge for the industry is to capture and allocate economic value through this shift, supporting the circular economy principles whilst avoiding negative externalities, and promoting greater resource efficiency and reduced environmental impacts.

Notwithstanding the challenges to PSS implementation, the luggage industry is ripe for disruption. The USD 22 billion scale of the luggage market [

3], which is dominated by only a few international groups and brands [

58] suggests that there is scope for emergent, innovative business models to succeed [

59]. Whether it be an established manufacturer changing their approach, an emergent brand or a digital platform, the stakeholder that will find the right mix of product and service should appeal to a customer base that is willing to engage. Environmentally, PSS in the travel industry appears to make sense due to decreases in resource use, energy use and carbon emissions across the entire system. The likelihood of negative rebound effects, along with the complex logistics-related impacts, will need to be further explored to prevent unintended consequences. Yet, a novel PSS that questions the very need for owning the luggage to begin with could still take flight. A recent Japan Airlines initiative to rent clothing to visitors to Japan without the need for luggage [

60] echoes a concept by Rent the Runway and TripAdvisor in the US in 2021 [

61]. These can be refreshingly disruptive and can potentially promote change. This jump to a results-oriented PSS has the potential to shake up the entire industry, and if such a scheme could be designed to measurably reduce environmental impacts at scale—then it could be an extremely important step towards sustainable travel.

{kind=link}

{kind=link}

{kind=link}