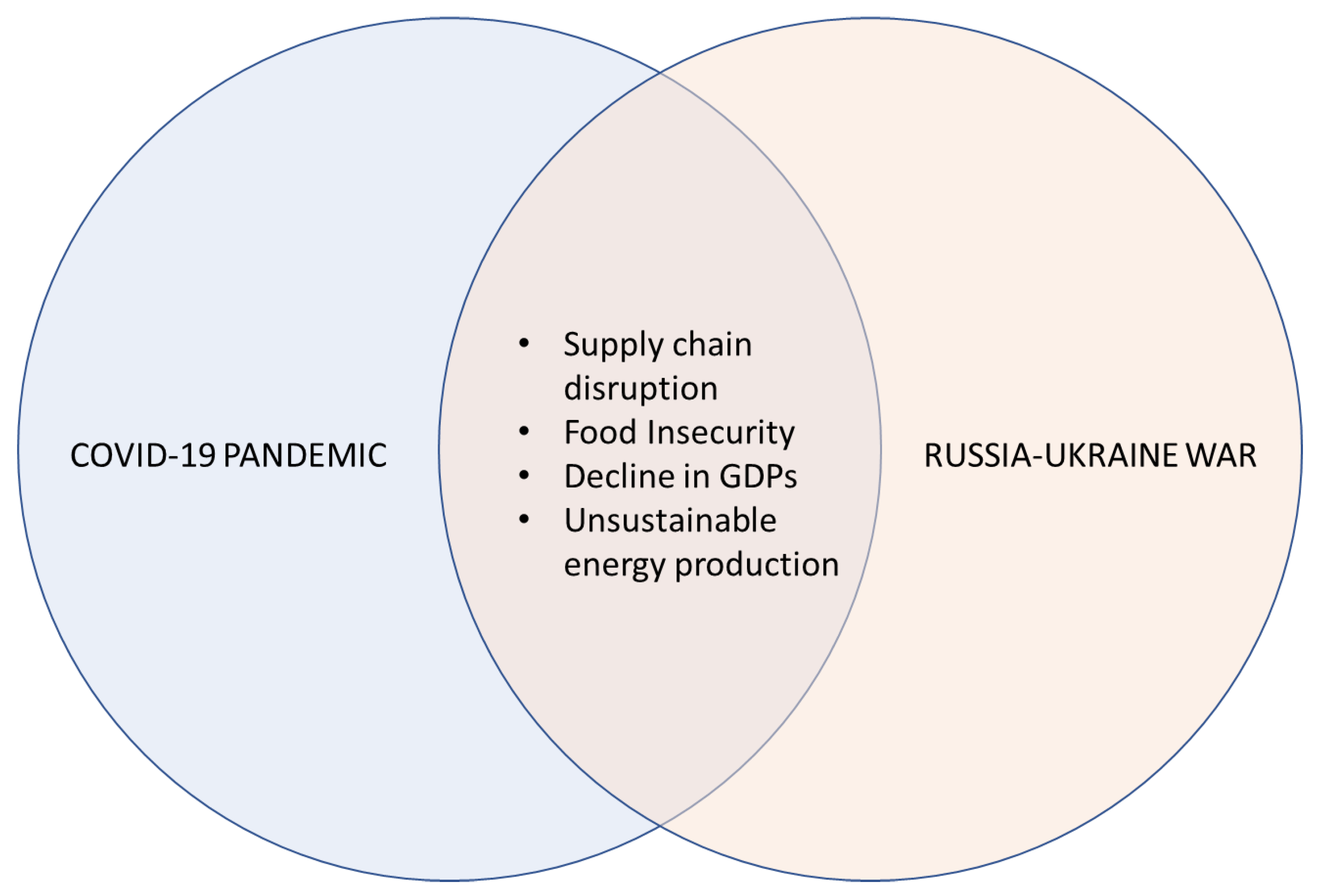

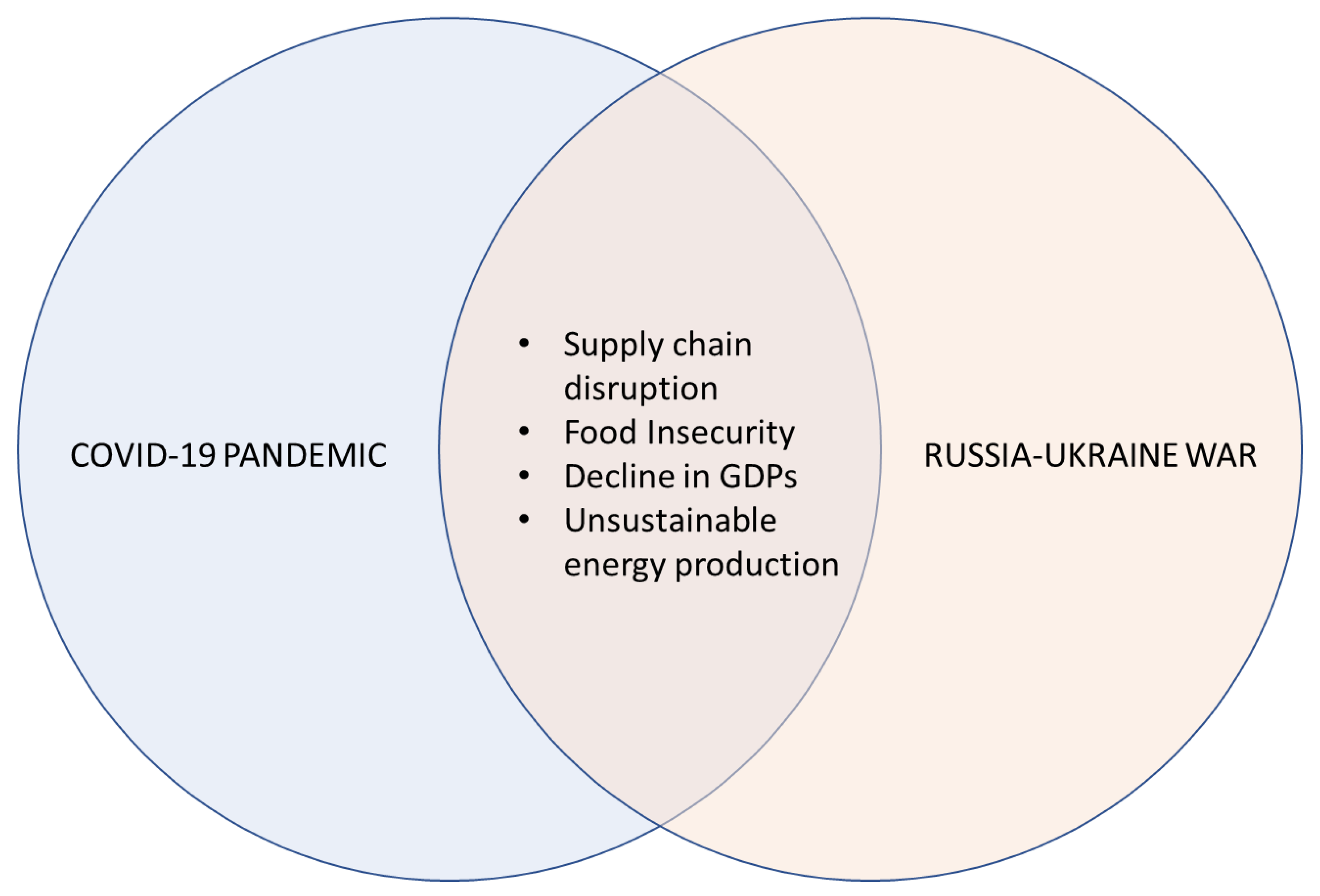

The Rising Impacts of the COVID-19 Pandemic and the Russia–Ukraine War: Energy Transition, Climate Justice, Global Inequality, and Supply Chain Disruption

{kind=link}

Abstract

:1. Introduction

2. The Link between Sustainability Transitions and Resource Management

3. Impacts on Global Supply Chains

3.1. The Case of the COVID-19 Pandemic

3.2. The Case of the Russia–Ukraine War

4. The Challenges of Green Premiums Additionally, Access to Green Technology

5. Discussions

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- IPCC. Climate Change 2022: Impacts, Adaptation and Vulnerability; Intergovernmental Panel on Climate Change: 2022. Available online: https://www.ipcc.ch/report/ar6/wg2/ (accessed on 1 September 2022).

- Ray, D.K.; West, P.C.; Clark, M.; Gerber, J.S.; Prishchepov, A.V.; Chatterjee, S. Climate change has likely already affected global food production. PLoS ONE 2019, 14, e0217148. [Google Scholar] [CrossRef]

- Burrell, A.L.; Evans, J.P.; De Kauwe, M.G. Anthropogenic climate change has driven over 5 million km2 of drylands towards desertification. Nat. Commun. 2020, 11, 3853. [Google Scholar] [CrossRef] [PubMed]

- Behlert, B.; Diekjobst, R.; Felgentreff, C.; Manandhar, T.; Mucket, P.; Pries, L.; Radtke, K.; Welle, D. World Riks Report 2020. Focus: Forced Displacement and Migration; Relief Web: 2020. Available online: https://reliefweb.int/attachments/30ab4c7d-59bc-327d-87da-8d86f265ebcc/WorldRiskReport-2020.pdf (accessed on 1 September 2022).

- UNFCCC. Glasgow Climate Pact; UNFCCC: 2021; pp. 1–10. Available online: https://unfccc.int/sites/default/files/resource/cma2021_10_add1_adv.pdf (accessed on 1 September 2022).

- Kling, G.; Lo, Y.; Murinde, V.; Volz, U. Climate Vulnerability and the Cost of Debt. SSRN Electron. J. 2018, 1–30. [Google Scholar] [CrossRef] [Green Version]

- Were, A. Debt Trap? Chinese Loans and Africa’s Development Options. S. Afr. Insittute Int. Aff. Policy Insights 2018, 66, 1–13. [Google Scholar]

- Gurara, D.; Klyuev, V.; Mwase, N.; Presbitero, A.; Xu, X.C.; Bannister, G. Trends and Challenges in Infrastructure Investment in Low-Income Developing Countries; WP/17/233; International Monetary Fund: Washington, DC, USA, 2017. [Google Scholar]

- The World Bank. Unprecedented Impacts of Climate Change Disproportionately Burdening Developing Countries, Delegate Stresses, as Second Committee Concludes General Debate. Available online: https://www.un.org/press/en/2019/gaef3516.doc.htm (accessed on 20 April 2022).

- UNCTAD. Developing Country External Debt: From Growing Sustainability Concerns to Potential Crisis in the Time of COVID-19. Available online: https://sdgpulse.unctad.org/debt-sustainability/ (accessed on 2 November 2021).

- Adeoti, T.; Fantini, C.; Morgan, G.; Thacker, S.; Ceppi, P.; Bhikhoo, N.; Kumar, S.; Crosskey, S.; O’Regan, N. Infrastructure for Small Island Developing States: The Role of Infrastructure in Enabling Sustainable, Resilient and Inclusive Development in SIDS; UNOPS: Copenhagen, Denmark, 2020; pp. 1–39. [Google Scholar]

- Sandford, A. Coronavirus: Half of Humanity Now on Lockdown as 90 Countries Call for Confinement. Available online: https://www.euronews.com/2020/04/02/coronavirus-in-europe-spain-s-death-toll-hits-10-000-after-record-950-new-deaths-in-24-hou (accessed on 15 April 2020).

- Guan, D.; Wang, D.; Hallegatte, S.; Davis, S.J.; Huo, J.; Li, S.; Bai, Y.; Lei, T.; Xue, Q.; Coffman, D.M.; et al. Global supply-chain effects of COVID-19 control measures. Nat. Hum. Behav. 2020, 4, 577–587. [Google Scholar] [CrossRef] [PubMed]

- DHL. Understanding the “New Normal” Supply Chain Risks in 2022 and Beyond. Available online: https://www.dhl.com/global-en/delivered/globalization/supply-chain-risks-in-2022.html (accessed on 18 April 2022).

- Goshwami, S. 4th Wave of COVID-19 in USA, India, China and Other Countries. Available online: https://dmerharyana.org/4th-wave-of-covid-19/ (accessed on 19 April 2022).

- Bond, I.; Cornago, E.; Mortera-Martinez, C.; Scazzieri, L. Russia’s War on Ukraine: There is Worse to Come (for the West as Well). Available online: https://www.cer.eu/insights/russias-war-ukraine-worse-west (accessed on 26 March 2022).

- Connolly, K. Nord Stream 1: Russia Switches off Gas Pipeline Citing Maintenance. Available online: https://www.theguardian.com/business/2022/aug/31/nord-stream-1-russia-switches-off-gas-pipeline-citing-maintenance (accessed on 18 October 2022).

- United Nations. Global Impact of War in Ukraine on Food, Energy and Finance Systems; United Nations: New York, NY, USA, 2022; pp. 1–22. [Google Scholar]

- UNFCCC. Nationally determined contributions under the Paris Agreement: Synthesis report by the secretariat. In Proceedings of the Conference of the Parties Serving as the Meeting of the Parties to the Paris Agreement, Glasgow, UK, 17 September 2021. [Google Scholar]

- Talens Peiró, L.; Martin, N.; Villalba Méndez, G.; Madrid-López, C. Integration of raw materials indicators of energy technologies into energy system models. Appl. Energy 2022, 307, 118150. [Google Scholar] [CrossRef]

- Palmer, M.; Truong, Y. The Impact of Technological Green New Product Introductions on Firm Profitability. Ecol. Econ. 2017, 136, 86–93. [Google Scholar] [CrossRef] [Green Version]

- Bibri, S.E. Data-driven smart eco-cities of the future: An empirically informed integrated model for strategic sustainable urban development. World Futur. 2021, 1–44. [Google Scholar] [CrossRef]

- Deloitte. Sustainable Manufacturing: From Vision to Action; Deloitte: London, UK, 2021; p. 28. [Google Scholar]

- Jelti, F.; Allouhi, A.; Büker, M.S.; Saadani, R.; Jamil, A. Renewable Power Generation: A Supply Chain Perspective. Sustainability 2021, 13, 1271. [Google Scholar] [CrossRef]

- Kong, L.; Li, H.; Luo, H.; Ding, L.; Zhang, X. Sustainable performance of just-in-time (JIT) management in time-dependent batch delivery scheduling of precast construction. J. Clean. Prod. 2018, 193, 684–701. [Google Scholar] [CrossRef]

- Lotfi, M.; Walker, H.; Rendon-Sanchez, J. Supply Chains’ Failure in Workers’ Rights with Regards to the SDG Compass: A Doughnut Theory Perspective. Sustainability 2021, 13, 2526. [Google Scholar] [CrossRef]

- FAO. The Den Bosch Declaration and Agenda for Action on Sustainable Agriculture and Rural Development: Report of the Conference. In Proceedings of the FAO Netherlands Conference on Agriculture and the Environment, S’Hertogenbosch, The Netherlands, 15–19 April 1991. [Google Scholar]

- Saada, R. Green Transportation in Green Supply Chain Management. In Green Supply Chain-Competitiveness and Sustainability; Bányai, T., Kaczmar, I., Eds.; IntechOpen, 2020. [Google Scholar] [CrossRef]

- Andersen, I. The Circularity Transition: Leaving No One Behind. Available online: https://www.unep.org/news-and-stories/speech/circularity-transition-leaving-no-one-behind (accessed on 25 August 2021).

- Yu, Y.; Zhu, W.; Tian, Y. Green Supply Chain Management, Environmental Degradation, and Energy: Evidence from Asian Countries. Discret. Dyn. Nat. Soc. 2021, 2021, 5179964. [Google Scholar] [CrossRef]

- Allam, Z. The first 50 days of COVID-19: A detailed chronological timeline and extensive review of literature documenting the pandemic. Surveying the COVID-19 Pandemic and Its Implications: Urban Health, Data Technology and Political Economy; Elsevier: Amsterdam, The Netherlands, 2020; pp. 41–69. [Google Scholar]

- Meyer, A.; Walter, W.; Seuring, S. The Impact of the Coronavirus Pandemic on Supply Chains and Their Sustainability: A Text Mining Approach. Front. Sustain. 2021, 2. [Google Scholar] [CrossRef]

- Allam, Z. Chapter 9—Oil, Health Equipment, and Trade: Revisiting Political Economy and International Relations During the COVID-19 Pandemic. In Surveying the Covid-19 Pandemic and Its Implications; Allam, Z., Ed.; Elsevier: Amsterdam, The Netherlands, 2020; pp. 119–127. [Google Scholar]

- Allam, Z.; Jones, D.S. Pandemic stricken cities on lockdown. Where are our planning and design professionals [now, then and into the future]? Land Use Policy 2020, 97, 104805. [Google Scholar] [CrossRef] [PubMed]

- IATA. The Impact of COVID-19 on Aviation. Available online: https://airlines.iata.org/news/the-impact-of-covid-19-on-aviation (accessed on 19 April 2022).

- WTW. COVID-19 Impact on the Air Cargo Industry. Available online: https://www.wtwco.com/en-VN/Insights/2021/01/covid-19-impact-on-the-air-cargo-industry (accessed on 19 April 2022).

- Pallis, A.A. COVID-19 and Maritime Transport: Impact and Responses; UNCTAD: Geneva, Switzerland, 2021. [Google Scholar]

- Freight Right. Congestion All Around, from COVID in China to Gridlocks in L.A. Available online: https://www.freightright.com/news/congestion-all-around-from-covid-in-china-to-gridlocks-in-la (accessed on 19 April 2022).

- Morris, C. Warning Shipping Delay Problems to Continue This Year. Available online: https://www.bbc.com/news/business-60131947 (accessed on 19 April 2022).

- Van der Merwe, B. Weekly Data: How COVID-19 Disrupted Global Shipping. Available online: https://www.investmentmonitor.ai/analysis/covid-global-shipping-container-shortage (accessed on 19 April 2022).

- UNCTAD. Shipping during COVID-19: Why Container Freight Rates Have Surged. Available online: https://unctad.org/news/shipping-during-covid-19-why-container-freight-rates-have-surged (accessed on 19 April 2022).

- Business Wire. Just-in-Time Made the World Tardy: COVID-19 Revealed Manufacturing Cost Cutting Strategies May Have Gone Too Far. Available online: https://www.businesswire.com/news/home/20210628005038/en/Just-In-Time-Made-the-World-Tardy-COVID-19-Revealed-Manufacturing-Cost-Cutting-Strategies-May-Have-Gone-Too-Far-According-to-Pricefx (accessed on 19 April 2022).

- Carrière-Swallow, Y.; Deb, P.; Furceri, D.; Jiménez, D.; Ostry, J.D. How Soaring Shipping Costs Raise Prices Around the World. Available online: https://blogs.imf.org/2022/03/28/how-soaring-shipping-costs-raise-prices-around-the-world/ (accessed on 19 April 2022).

- Ben Hassen, T.; El Bilali, H. Impacts of the Russia-Ukraine War on Global Food Security: Towards More Sustainable and Resilient Food Systems? Foods 2022, 11, 2301. [Google Scholar] [CrossRef]

- Kadosh, O.; Milhalter, G.; Ochoa, A. A Summary of the Latest Sanctions Against Russia. Available online: https://www.pearlcohen.com/a-summary-of-the-latest-sanctions-against-russia-2/ (accessed on 20 April 2022).

- European Commission. REPowerEU: Joint European Action for More Affordable, Secure and Sustainable Energy. Available online: https://ec.europa.eu/commission/presscorner/detail/en/ip_22_1511 (accessed on 20 April 2022).

- White House. FACT SHEET: United States Bans Imports of Russian Oil, Liquefied Natural Gas, and Coal. Available online: https://www.whitehouse.gov/briefing-room/statements-releases/2022/03/08/fact-sheet-united-states-bans-imports-of-russian-oil-liquefied-natural-gas-and-coal/ (accessed on 20 April 2022).

- Eurostat. EU Imports of Energy Products—Recent Developments. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=EU_imports_of_energy_products_-_recent_developments&oldid=558719#Overview (accessed on 20 April 2022).

- International Energy Agency (IEA). Russia’s War on Ukraine: Analysing the Impacts of Russia’s Invasion of Ukraine on Global Energy Markets and International Energy Security. Available online: https://www.iea.org/topics/russia-s-war-on-ukraine (accessed on 20 April 2022).

- Duggal, H.; Haddad, M. Infographic: Russia, Ukraine and the Global Wheat Supply. Available online: https://www.aljazeera.com/news/2022/2/17/infographic-russia-ukraine-and-the-global-wheat-supply-interactive (accessed on 21 April 2022).

- Schiffling, S.; Kanellos, N.V. Five Essential Commodities That Will Be Hit by War in Ukraine. Available online: https://theconversation.com/five-essential-commodities-that-will-be-hit-by-war-in-ukraine-177845 (accessed on 20 April 2022).

- European Commission. Supply Shock Caused by Russian Invasion of Ukraine Puts Strain on Various EU Agri-Food Sectors. Available online: https://ec.europa.eu/info/news/supply-shock-caused-russian-invasion-ukraine-puts-strain-various-eu-agri-food-sectors-2022-apr-05_en (accessed on 21 April 2022).

- UN Food and Agriculture Organisation (FAO). FAO Food Price Index Rises to Record High in February. Available online: https://www.fao.org/newsroom/detail/fao-food-price-index-rises-to-record-high-in-february/en (accessed on 21 April 2022).

- Office for National Statistics. Average Weekly Earnings in Great Britain: March 2022. Available online: https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/bulletins/averageweeklyearningsingreatbritain/march2022 (accessed on 21 April 2022).

- Office for National Statistics. Average Weekly Earnings in Great Britain: April 2022. Available online: https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/bulletins/averageweeklyearningsingreatbritain/april2022 (accessed on 21 April 2022).

- Ratha, D.; Kim, E.J. Russia-Ukraine Conflict: Implications for Remittance Flows to Ukraine and Central Asia. Available online: https://blogs.worldbank.org/peoplemove/russia-ukraine-conflict-implications-remittance-flows-ukraine-and-central-asia (accessed on 21 April 2022).

- Behnassi, M.; El Haiba, M. Implications of the Russia–Ukraine war for global food security. Nat. Hum. Behav. 2022, 6, 754–755. [Google Scholar] [CrossRef] [PubMed]

- Pickson, R.B.; Boateng, E. Climate change: A friend or foe to food security in Africa? Environ. Dev. Sustain. 2022, 24, 4387–4412. [Google Scholar] [CrossRef] [PubMed]

- Clapp, J. Concentration and crises: Exploring the deep roots of vulnerability in the global industrial food system. J. Peasant Stud. 2022, 1–25. [Google Scholar] [CrossRef]

- Bibri, S.E.; Krogstie, J. Environmentally data-driven smart sustainable cities: Applied innovative solutions for energy efficiency, pollution reduction, and urban metabolism. Energy Inform. 2020, 3, 29. [Google Scholar] [CrossRef]

- Hess, D.J.; Sovacool, B.K. Sociotechnical matters: Reviewing and integrating science and technology studies with energy social science. Energy Res. Soc. Sci. 2020, 65, 101462. [Google Scholar] [CrossRef]

- Bibri, S.E.; Allam, Z. The Metaverse as a Virtual Form of Data-Driven Smart Urbanism: On Post-Pandemic Governance through the Prism of the Logic of Surveillance Capitalism. Smart Cities 2022, in press. [CrossRef]

- Geels, F.W. Technological Transitions and System Innovations: Aco-Evolutionary and Socio-Technical Analysis; Edward Elgar: Cheltenham, UK, 2005. [Google Scholar]

- Smith, A. Transforming technological regimes for sustainable development: A role for alternative technology niches? Sci. Public Policy 2003, 30, 127–135. [Google Scholar] [CrossRef]

- Markard, J.; Raven, R.; Truffer, B. Sustainability transitions: An emerging field of research and its prospects. Res. Policy 2012, 41, 955–967. [Google Scholar] [CrossRef]

- Hansen, T.; Coenen, L. The geography of sustainability transitions: Review, synthesis and reflections on an emergent research field. Environ. Innov. Soc. Transit. 2015, 17, 92–109. [Google Scholar] [CrossRef] [Green Version]

- Coenen, L.; Hansen, T.; Glasmeier, A.; Hassink, R. Regional foundations of energy transitions. Camb. J. Reg. Econ. Soc. 2021, 14, 219–233. [Google Scholar] [CrossRef]

- Bridge, G.; Bourzarovski, S.; Bradshaw, M.; Eyre, N. Geographies of energy transition: Space, place and the low-carbon economy. Energy Policy 2013, 53, 331–340. [Google Scholar] [CrossRef]

- Carvalho, L.; Mingardo, G.; Van Haaren, J. Green Urban Transport Policies and Cleantech Innovations: Evidence from Curitiba, Göteborg and Hamburg. Eur. Plan. Stud. 2012, 20, 375–396. [Google Scholar] [CrossRef]

- McCauley, S.M.; Stephens, J.C. Green energy clusters and socio-technical transitions: Analysis of a sustainable energy cluster for regional economic development in Central Massachusetts, USA. Sustain. Sci. 2012, 7, 213–225. [Google Scholar] [CrossRef]

- Bibri, S.E. Introduction: The rise of sustainability, ICT, and urbanization and the materialization of smart sustainable cities. In Smart Sustainable Cities of the Future: The Untapped Potential of Big Data Analytics and Context–Aware Computing for Advancing Sustainability; Springer: Berlin/Heidelberg, Germany, 2018. [Google Scholar] [CrossRef]

- Smith, A. Green Niches in Sustainable Development: The Case of Organic Food in the United Kingdom. Environ. Plan. C Gov. Policy 2006, 24, 439–458. [Google Scholar] [CrossRef]

- McCann, P.; Ortega-Argilés, R. Smart Specialization, Regional Growth and Applications to European Union Cohesion Policy. Reg. Stud. 2015, 49, 1291–1302. [Google Scholar] [CrossRef]

- Lawhon, M.; Murphy, J.T. Socio-technical regimes and sustainability transitions: Insights from political ecology. Prog. Hum. Geogr. 2011, 36, 354–378. [Google Scholar] [CrossRef]

- Bibri, S.E.; Krogstie, J. Towards A Novel Model for Smart Sustainable City Planning and Development: A Scholarly Backcasting Approach. J. Futures Stu. 2019, 24, 45–62. [Google Scholar] [CrossRef]

- Lagendijk, A.; Boertjes, S. Light Rail: All change please! A post-structural perspective on the global mushrooming of a transport concept. Plan. Theory 2012, 12, 290–310. [Google Scholar] [CrossRef]

- Hodson, M.; Marvin, S. Mediating Low-Carbon Urban Transitions? Forms of Organization, Knowledge and Action. Eur. Plan. Stud. 2012, 20, 421–439. [Google Scholar] [CrossRef] [Green Version]

- African Development Bank. Historic Alliance Launches at COP26 to Accelerate a Transition to Renewable Energy, Access to Energy for All, and Jobs. Available online: https://www.afdb.org/en/news-and-events/historic-alliance-launches-cop26-accelerate-transition-renewable-energy-access-energy-all-and-jobs-46557 (accessed on 20 April 2022).

- Rockefeller Foundation. Transforming the Power System in Energy-Poor Countries; The Global Energy Alliance for People and Planet (GEAPP): 2022. Available online: https://www.rockefellerfoundation.org/initiative/global-energy-alliance-for-people-and-planet-geapp/ (accessed on 1 September 2022).

- Allam, Z.; Jones, D.S.; Roös, P. Addressing Knowledge Gaps for Global Climate Justice. Geographies 2022, 2, 14. [Google Scholar] [CrossRef]

- Gates, B. How to Avoid a Climate Disaster; Knopf: New York, NY, USA, 2021. [Google Scholar]

- Cheney, C. How Blended Finance Might Help Low ‘the Green Premium’. Available online: https://www.devex.com/news/how-blended-finance-might-help-lower-the-green-premium-101997 (accessed on 20 April 2021).

- Oyedokun, T.B. Green premium as a driver of green-labelled commercial buildings in the developing countries: Lessons from the UK and US. Int. J. Sustain. Built Environ. 2017, 6, 723–733. [Google Scholar] [CrossRef]

- Conte, N. Green New Deal. Available online: https://wtpartnership.co/green-new-deal/ (accessed on 24 February 2021).

- London Assembly. A Green New Deal. Available online: https://www.london.gov.uk/coronavirus/londons-recovery-coronavirus-crisis/recovery-context/green-new-deal (accessed on 25 August 2021).

- Filatoff, N. A Green New Deal for Australia? Available online: https://www.pv-magazine.com/2020/01/06/a-green-new-deal-for-australia/ (accessed on 25 August 2021).

- Allam, Z.; Sharifi, A.; Giurco, D.; Sharpe, S.A. Green new deals could be the answer to COP26’s deep decarbonisation needs. Sustain. Horiz. 2022, 1, 100006. [Google Scholar] [CrossRef]

- Allam, Z.; Sharifi, A.; Giurco, D.; Sharpe, S.A. On the Theoretical Conceptualisations, Knowledge Structures and Trends of Green New Deals. Sustainability 2021, 13, 12529. [Google Scholar] [CrossRef]

- United Nations Framework Convention on Climate Change. Status of Ratification of the Convention. Available online: https://unfccc.int/process-and-meetings/the-convention/status-of-ratification/status-of-ratification-of-the-convention (accessed on 8 August 2021).

- United Nations Framework Convention on Climate Change. Kyoto Protocol to the United Nations Framework Conventon on Climate Change. Available online: https://unfccc.int/resource/docs/convkp/kpeng.pdf (accessed on 8 August 2021).

- United Nations Framework Convention on Climate Change. Paris Agreement. Available online: https://unfccc.int/sites/default/files/english_paris_agreement.pdf (accessed on 8 August 2021).

- Heubl, B. Global Carbon Emissions: The World Keeps Polluting after COVID-19. Available online: https://eandt.theiet.org/content/articles/2021/06/global-carbon-emissions-the-world-keeps-polluting-after-covid-19/ (accessed on 24 September 2021).

- UN Environment. Cities and Climate Change. Available online: https://www.unenvironment.org/explore-topics/resource-efficiency/what-we-do/cities/cities-and-climate-change (accessed on 3 September 2019).

- Kim, H.-e. Changing Climate, Changing Culture: Adding the Climate Change Dimension to the Protection of Intangible Cultural Heritage. Int. J. Cult. Prop. 2011, 28, 259–290. [Google Scholar] [CrossRef]

- Leal Filho, W. Will climate change disrupt the tourism sector? Int. J. Clim. Chang. Strateg. Manag. 2022, 14, 212–217. [Google Scholar] [CrossRef]

- European Environment Agency (EEA). Economic Losses and Fatalities from Weather-and Climate-Related Events in Europe. Available online: https://www.eea.europa.eu/publications/economic-losses-and-fatalities-from (accessed on 20 April 2022).

- So, K.; Hardin, S.; Extreme Weather Cost U.S. Taxpayers $99 Billion Last Year, and It Is Getting Worse. Available online: https://www.americanprogress.org/article/extreme-weather-cost-u-s-taxpayers-99-billion-last-year-getting-worse/ (accessed on 20 April 2022).

- Flavelle, C. Climate Change Could Cut World Economy by $23 Trillion in 2050, Insurance Giant Warns. Available online: https://www.nytimes.com/2021/04/22/climate/climate-change-economy.html#:~:text=the%20main%20story-,Climate%20Change%20Could%20Cut%20World%20Economy%20by%20%2423%20Trillion%20in,and%20invests%20its%20mammoth%20portfolios (accessed on 1 May 2022).

- Ahmed, K. Inflation Bites Hardest in Developing World as Ukraine War Raises Prices. Available online: https://www.theguardian.com/global-development/2022/apr/29/inflation-bites-hardest-in-developing-world-as-ukraine-war-raises-prices (accessed on 15 October 2022).

- Dennison, S. Green Peace: How Europe’s Climate Policy Can Survice the War in Ukraine. Available online: https://ecfr.eu/publication/green-peace-how-europes-climate-policy-can-survive-the-war-in-ukraine/ (accessed on 15 October 2022).

- Guivarch, C.; Taconet, N.; Méjean, A. Linking Climate and Inequality. Available online: https://www.imf.org/Publications/fandd/issues/2021/09/climate-change-and-inequality-guivarch-mejean-taconet (accessed on 20 April 2022).

- UNEP. Emerging Issues for Small Island Developing States; UNEP: Nairobi, Kenya, 2014. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Allam, Z.; Bibri, S.E.; Sharpe, S.A. The Rising Impacts of the COVID-19 Pandemic and the Russia–Ukraine War: Energy Transition, Climate Justice, Global Inequality, and Supply Chain Disruption. Resources 2022, 11, 99. https://doi.org/10.3390/resources11110099

Allam Z, Bibri SE, Sharpe SA. The Rising Impacts of the COVID-19 Pandemic and the Russia–Ukraine War: Energy Transition, Climate Justice, Global Inequality, and Supply Chain Disruption. Resources. 2022; 11(11):99. https://doi.org/10.3390/resources11110099

Chicago/Turabian StyleAllam, Zaheer, Simon Elias Bibri, and Samantha A. Sharpe. 2022. "The Rising Impacts of the COVID-19 Pandemic and the Russia–Ukraine War: Energy Transition, Climate Justice, Global Inequality, and Supply Chain Disruption" Resources 11, no. 11: 99. https://doi.org/10.3390/resources11110099

APA StyleAllam, Z., Bibri, S. E., & Sharpe, S. A. (2022). The Rising Impacts of the COVID-19 Pandemic and the Russia–Ukraine War: Energy Transition, Climate Justice, Global Inequality, and Supply Chain Disruption. Resources, 11(11), 99. https://doi.org/10.3390/resources11110099