Abstract

There has been recent proliferation of entrepreneurship theorizing involving the true uncertainty of a system—most often labeled as Knightian. This has been noted in both individual papers and in the main partial theories that attempt to explain entrepreneurial activity more holistically. We detect a danger in this work involving such true uncertainty—defined by the condition that decisions plagued by it are non-optimizable by every interested party. It is that all the recent theorizing misinterprets that uncertainty in one of two ways: with a logical contradiction (i.e., that the non-optimizable is actually optimizable); or with a misrepresentation (i.e., that an uncertainty consisting of a knowable unknown that can be made known through known means by the time the decision must be made is true). Our concern is that such misinterpretations create unnecessary costs to academics and practitioners who are struggling to define the system they are managing. We explain this concern and its costs, detail the underlying premises, illustrate it with several examples, and then offer various specific directions to improve the theorizing over such uncertainty in entrepreneurship.

1. Introduction

The greatest opportunities and threats arise from uncertainty. That observation not only applies to the histories of incumbent firms and new ventures but also to the research that focuses on their strategic decisions. In this paper, we identify a fundamental problem with the way that true uncertainty is modeled in the management literature, and especially in the entrepreneurship field. The existence of that problem matters because it harms both academia and practice: it leads to flawed theorizing, a loss of scientific legitimacy, and unnecessary opportunity costs (e.g., in that alterative and non-flawed ideas are ignored); and it leads to firms wasting their scarce resources either treating untreatable uncertainties or failing to treat the treatable ones or misunderstanding the systems they are tasked with managing. To address this problem, we analyze examples to determine recognizable patterns of mismodeling that can then be used as a basis for recommending remedies.

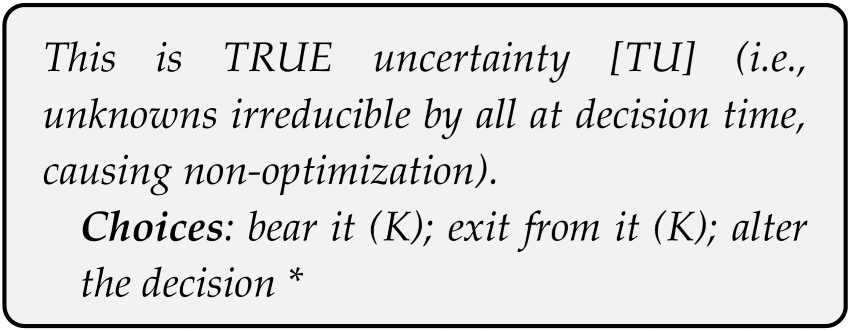

True uncertainty (denoted TU henceforth) is a condition defined by the existence of one or more unknowns that make the focal decision problem impossible to optimize (i.e., where the decision-maker cannot compute the expected values of all relevant choice options in a system). Such unknowns could involve missing options, outcomes or goals, or undefined outcome probabilities and their distributions, but the important thing is that such given unknowns remain unknowable at the time the focal decision must be made. Note that when the expected values of the relevant choices cannot be computed, the decision problem is also theoretically uninsurable—given that the risk of any one outcome based on those choices is then unknown (e.g., as the probability distribution for a specific outcome is unreliable and incomplete). Also note that this is a strict condition of the definition (i.e., that no decision-maker has a feasible way to discover or mitigate the given unknown prior to having to choose a major course of action).

TU can be difficult to fully comprehend; there may be temptation to believe that science or the normal course of events will uncover all truths over a reasonable amount of time, especially if humankind focuses its efforts there. However, TU does remain a very real condition. It is a real condition based on evidence (e.g., given there is regrettably still no cure for all cancers and no full understanding of the origin of the universe or of quantum entanglements and given that even well-informed business decision-makers are surprised regularly). And it is a condition that has been explicitly acknowledged by peers, both recently [1] and over a century ago [2]. Our interest in TU here is specific; however, it is not to prove that such a theoretical and practical condition exists but to analyze how it is treated when it is modeled or alluded to in the literature (whether involving systems thinking or other approaches to problem-solving practiced by entrepreneurs and managers). It is because TU embodies a powerful (informational) market failure—one upon which entrepreneurship has arguably existentially relied (in the version of TU labeled as Knightian uncertainty)—that this exercise is worth undertaking.

Without conducting the exercise, we expect that current harm will continue. Papers that suggest TU is treatable contain a logical flaw, given TU is not, by definition, treatable. Any paper that treats a different uncertainty but confuses it with TU is solving a different problem. In either case, when such inconsistencies are eventually discovered, then negative spillovers can result, including affecting the peer work that actually follows good practice (i.e., entails no inconsistencies). Such cases are also bad for practice because, when the suggestions made by those papers are followed in the real world, they do not provide the value they advertise. And, that disappointment is likely to lead to wasted resources and efforts, if not the creation of resentment within an affected organization when employees lose confidence in its leadership. Further, the distribution of such flawed work can lead to more of it. This is because such work—work that includes promises of impossible benefits (i.e., treatments for untreatable conditions)—is often of high interest and is rewarded by more cites, which then makes even more such work likely to be pursued, with even more harm done. Thus, we suggest better ways forward.

In order to achieve our remedies, however, we must follow a deliberate path: we complete our definition of TU, explaining several important implications; we compare TU to the related concept of Knightian uncertainty (denoted as KU henceforth); we explain TU as a key part of the entrepreneurship model; we assess several sets of recent works on uncertainties and their treatments, focusing on TU; we build a set of remedies based on that assessment; and then we put the exercise in perspective with concluding thoughts.

2. Theoretical Background

2.1. True Uncertainty

Prior to rounding out the initial definition of TU (above) by describing its two most important logical implications, it is worthwhile to reiterate that we are not introducing a wholly new concept. TU, regardless of the label, has been recognized for over a century, and has been acknowledged academically by a significant proportion of the field recently [1,3,4]. This type of uncertainty has also been acknowledged practically through the real-world reporting of the existence of unknown unknowns; the existence of known-to-be-unknowable values (e.g., due to the Heisenberg principle); realizations of surprise by individuals, organizations, and markets alike; and the admittance by a wide spectrum of thinkers (from philosophers to physicists to musicians to politicians) that humankind will never know everything about the past, present, or future. Indeed, there are many possible reasons for the non-optimizability that TU brings. The existence of both unknown unknowns and known unknowns with unknowable values is often attributed to the non-linearity and non-stationarity of complex systems, to the bounded rationality of decision-makers, and to the innate inability to prove even basic mathematical premises (see Gödel’s theorem).

With the establishment of TU in theory and in practice, we now turn to two important implications of its definition. TU requires an irreducible unknownness that is experienced by all interested parties. It is easiest to understand the irreducibility implication by imagining if it were violated, because its hypothetical violation leads to two mutually exclusive and collectively exhaustive cases: In the first case, the reduction in the uncertainty makes the decision optimizable, and so it is, at the end of that process, actually a problem of risk and not of uncertainty. In the second case, the reduction in the uncertainty leaves the decision as remaining non-optimizable after eliminating any of given unknowns that were knowable (leaving only the unknowable ones). Now, consider what that means in the standard theoretical world (e.g., of micro-economics) where every decision-maker is super-rational, and no other market failures or frictions exist—in that world, if the given problem included a reducible component, then all the decision-makers would know that and do the reduction costlessly, completely, and immediately. In proper modeling, we tend to focus on only the simplest meaningful version of the problem—here, that is where the decision entails only the truly irreducible unknowns because all other reductions that could have been performed were already performed1. The by all implication is a logical conclusion. If the focal unknowns—the ones that make the decision non-optimizable—were actually reduceable to the point that the decision could be optimized by even one party, then that decision would obviously no longer be non-optimizable by at least that one decision-maker, if not more. Note that not only would that outcome require an additional modeling assumption (i.e., to explain the heterogeneity among decision-maker abilities to allow that one party to optimize the decision but others not to), but even if it did occur, that one privileged party may profitably offer insurance to the other parties, making the problem optimizable by many, by leaving them only (insurable) risk rather than uncertainty to contend with. To be clear then, true uncertainty entails problems where the unknowns cannot be made (more) knowable (e.g., through knowledge acquisition) by any relevant party prior to the focal decision point.

To proceed, then, it must be clear that TU necessitates non-optimizability of a decision to all. Thus, TU cannot, in any way, be treated or addressed directly, as given, other than by bearing it [2], bearing it by making a choice and taking an irreversible action in full light of one’s ignorance and then hoping for the best.

2.2. Knightian Uncertainties

Knight [2] (p. 233) famously delineated uncertainty from risk in the context of making a decision. His underlying premise was that uncertain decisions are uninsurable because, at a minimum, the expected values of all possible choices cannot be computed with sufficient confidence. This is equivalent to stating that such a decision is non-optimizable (i.e., involves TU). That characterization is found in one part of his widely cited book, a book, unfortunately, that is also full of inconsistencies and contradictions. For example, in later sections of his book, he speaks to uncertainties in ways that contradict that non-optimizability and uninsurability characterizations. We leave it to historians and others interested in parsing century-old words written in a century-old context under whatever pressures were applied to have the text provide some treatments to what were the treatable (e.g., diversifiable, controllable, predictable), known-to-be-knowable-but-unknown-as-originally-provided conditions. To be clear, then, to the extent that we draw from Knight [2], we are simply taking one idea rather than trying to interpret a book full of inconsistent thoughts. We leverage that one core idea—the idea that some decision-problems do involve unknowable unknowns at the time the choice must be made, unknowns that make it impossible to calculate the expected values for all relevant choices, making the decision non-optimizable and uninsurable (i.e., as defined by TU and often referred to as KU). And we do this while noting a limitation in his expression of that idea—that while Knight [2] focused on probabilities being unknown, many other decision elements could also be unknown and generate that non-optimizable condition (e.g., options; raw payoffs; utilities; goals; and so on).

2.3. True Uncertainty in the Entrepreneurship Model

Most recent theories of entrepreneurship invoke uncertainty. The ones that do do so to explain how opportunities emerge, a subset of which are more likely to be exploited specifically by new ventures or by differentiated persons labeled as entrepreneurs. Such theories assume, at a minimum, both dynamics and heterogeneity: dynamics in the form of changes, some unpredicted, occurring over time that provide openings for new products and processes to find success; and heterogeneity in the form of specific differences between firms that favor the entrants’ new products or processes2. As such, the dynamics require decision-makers being forced to act at one point in time based on beliefs about what occurs at a future point in time, beliefs afflicted by uncertainty as the given informational market failure in the system. When that uncertainty is a TU, then it is very likely that the strategic choices made by the potential entrepreneur and its rivals will differ, given there is, by definition, no best action to take and any firm bearing the uncertainty will do so based on its own idiosyncratic beliefs or ‘gut feel’, thus providing a non-null possibility that the opportunity will be exploited first by the entrepreneur alone. (Note that this is not the case when the future is knowable—i.e., where the best choice is known to be knowable through known means by several entities, where incumbents are likely to have a resource and experience advantage over any new entrant.) These theories carry the implicit assumption that the lucky entrepreneur will be able to recoup the costs of bearing the uncertainty with revenues based on any realized advantage that was produced by such bearing (e.g., emerging from some better understanding of an underlying, previously mysterious process, or from an actualized outcome in the form of a successfully tested new technology or product). Essentially, there is an assumed monetizable first-mover advantage involved.

In such a story, TU has an existential relationship with entrepreneurship. It provides one, and perhaps ‘the’, essential explanation for new entry: When the choice over a strategic decision about the future is non-optimizable, then there is no reason why any one firm (e.g., an incumbent) would choose to act the same way as any other (e.g., a potential entrepreneur), given there is no objectively rational basis for choosing any specific action3, and so when one firm gets lucky with its choice and that firm is new, it theoretically has a distinctive basis for successful entry and sustained profitability (e.g., until the uncertainty is resolved and the incumbents can react). TU alone provides the basis for a complete story for such entrepreneurial activity by being an explanation for both why a firm could get lucky and be the only one to do so. It is important to note that TU eliminates incumbent advantages that are normally be assumed to exist when the entrant chooses the same path as the incumbents because, here, they choose different paths of investment and action4.

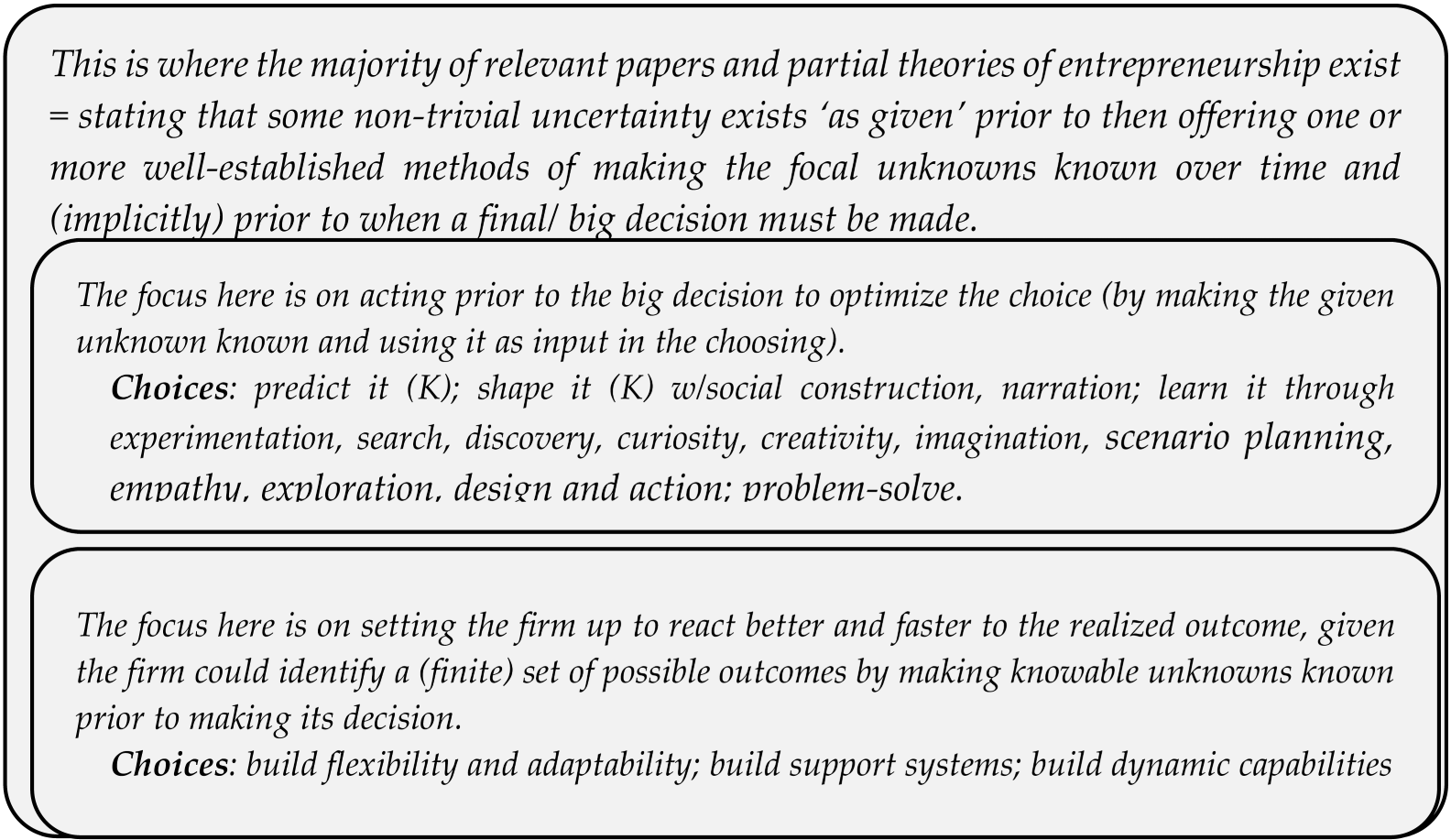

Based on our definition of TU, then logically there exist two separate contexts that are relevant to entrepreneurship: decisions that are vexed by TU—being non-optimizable by all—and so provide opportunities for new entry; and decisions that are not vexed by TU—being treatable (e.g., optimizable), possibly by several means and by several rivals—that do not provide such opportunities (at least, without additional modeling assumptions having to be made). Prescribing treatments (for optimization) to the former, or confusing the latter with the former, is each unhelpful; but we observe that is exactly what has been occurring in the recent literature. One reason is that such past work has not conformed to the simple typology our definition of TU suggests—i.e., that either an unknown is TU or it is not. However, that is not surprising, given there are alternative typologies of uncertainties in the literature—including Milliken’s [7] and Packard et al.’s [3]—but with none of those properly categorizing the term uncertainty in relation to its applicable optimizability5.

3. Assessing the Recent Resurgence of Work Addressing Uncertainties

With the described relevant background in hand, an informed assessment of the recent uncertainty literature is now possible. It is an assessment pursued not for the purpose of pointing out errors but instead for the ultimate purpose of identifying a set of remedies to whatever ailment patterns it uncovers. Specifically, here, we are interested in determining whether, when TU is acknowledged as the system’s context, there is an explicit understanding of the situation as being untreatable (i.e., non-optimizable); and, when the focal unknowns modeled are treated, then these are not misrepresented as being TU.

Our interest in these two concerns arises because a violation of either possibility offers a tempting path to publication, regardless of any underlying intention. That is, when a paper promises to solve the unsolvable—here, by describing the characteristics of a TU situation and then advocating an implementable treatment—then that paper is quite likely to see print. While one or two of these papers may not raise any red flags, the recent surge in such publications does; as it seems highly unlikely that suddenly there is a wide array of treatments for untreatable conditions without any coincidentally new logical, empirical, or mathematical breakthroughs. So, part of our contribution lies in capturing and analyzing the relevant recent literature all in one place—to best illustrate that the concern here is not simply an idiosyncratic, small-scale thing. We show how the concern spills over to multiple outlets, from general to field-specific, as well as how it has infiltrated the set of current theories of entrepreneurship. To do so, however, requires the short explanations of two preliminary issues: the first about why we target theorizing work and the second about how we target specific papers.

3.1. The Need to Target Theory Pieces

We focus on theory papers specifically, not only because there has been the recent resurgence of theorizing about uncertainty but also because distinctive theory is relatively more important to an arguably less-established, less-independent field like entrepreneurship, and uncertainty-related theorizing holds the promise of offering such distinction. Further, there is a cleanness to dissecting theory, as, arguably, the flaws are more identifiable and separable than with empirical studies.

Given this focus, it is worthwhile to restate that a theoretical world is relative to the real world; the former is highly simplified, and its simplifying assumptions often lead to quite unrealistic but logical outcomes from which important points can be made about benchmark cases (e.g., like about perfect competition versus monopolies). It is standard in the management- and entrepreneurship-theorizing literature to adopt a set of well-established, micro-economics-based simplifying assumptions about decision-makers and their abilities—i.e., that all firms are homogeneous, super-rational, and fully informed, unless otherwise explicitly stated. This means that all firms are the same, and act instantaneously on new information that is simultaneously and immediately disseminated to all parties in a frictionless environment6. So, it follows that if one firm identifies a way to reduce some unknowns, all do, and those unknowns are instantaneously reduced7.

Our concern with the recent literature arises from its modeling of TU. When a paper makes an assumption that a TU exists in its model, then there are two implications of interest: The first is that, despite the knowledge of other important elements relevant to the decision, the TU-vexed decision is non-optimizable. The second is that luck alone can drive performance differences among firms. In the real world, at least as evidenced by empirical studies, firm performance is not simply based on an idiosyncratic windfall, but rather attributed to complementary resources and capabilities, including to managerial skill [9]. However, in the theoretical (frictionless) world, luck may be the only thing that matters to realized performance outcomes, unless some other factor is explicitly modeled to explain the difference, such as an assumed initial heterogeneity or market failure.

3.2. How Papers Are Targeted

In our review, we target the ideas of the individual papers and not any paper’s authors8. As such, we are not making any accusations of bad intentionality on the part of any persons involved in the publication of those papers9. We make our assessments and arguments to provoke debate over the core ideas and expectations for a positive reason—to improve the health and impact of the affected academic fields. This exercise is pursued with a larger goal in mind—to remedy confusions over uncertainties in order to reduce their harm. We base any specific critiques on the actual uncertainties that a targeted paper itself portrays. If a labeled uncertainty is used in a paper, however, then we go by what that implies is being assumed unless otherwise explicitly expressed as not being assumed; so, if the term KU is invoked to imply uninsurability, then we assume TU is present unless otherwise explicitly delineated in that paper.

We target relevant work in the recent field-specific papers—those published in high-quality entrepreneurship journals. We focused on the recent bump in uncertainty-related theorizing—from 2020 to 2023—when a dozen papers were published in AMR, using the Business Source Complete database to search in JBV, SEJ, SBE, and ETP for papers that contained the keyword uncertain* in at least two of three fields (i.e., title, abstract, and subject term) as well as one of the keywords Knightian or judgment in the text. There were seven results. (It should be noted that the dozen AMR papers follow the same pattern as the papers in entrepreneurship regarding their treatment of uncertainty.) After the review of these singular journal papers, which we acknowledge limit the scope of the review by time and journal title, we then move to a wider and deeper target to partially compensate. We do so by assessing the related set of partial theories that are the often-cited, uncertainty-centered ideas that have cut across multiple papers in the entrepreneurship literature.

3.3. True Uncertainty Work in the Entrepreneurship Field

We now consider the recent record of theorizing over TU in the entrepreneurship field journals (i.e., SEJ, JBV, and SBE). We provide brief summaries of how several papers have described uncertainty and addressed it. As above, the papers refer to KU almost exclusively when a label is used, implying the uninsurable type of uncertainty (i.e., TU); further, most also describe characteristics of their uncertainty that align with TU (e.g., referencing unimaginable futures, unknown and/or unknowable factors, unpredictability, and so on).

Klein’s [10] paper describes uncertainty as arising when possible outcomes and probabilities are unimaginable (i.e., TU) and then suggests as viable solutions the use of intuition, gut feelings, empathy, or understanding (as judgment) to anticipate the unknown future; heuristics to make a decision; and experimentation to learn across time. Andries and colleagues’ paper [11] describes KU as the condition when relevant variables and their functional relationships are unknown, making the future unpredictable (i.e., TU) and then suggests that scenario-driven thinking and experimentation can provide an advantage. Giménez-Roche and Calcei’s [12] paper considers substantive and fundamental uncertainty to exist when future market conditions cannot be inferred from present ones (i.e., TU) and then suggests that such uncertainty can be reduced by means of (triggering) emergent demand routines or by means of creativity. Rapp and Olbrich’s [13] paper describes KU as entailing focal outcomes and probabilities that are unknown and unknowable (i.e., as TU) and then suggests that the application of various forms of judgment through heuristic problem-solving (i.e., involving splitting a problem into steps and satisficing) will provide benefits. Miozzo and DiVito’s [14] empirical paper begins by defining uncertainty as Knightian (e.g., with outcomes and probabilities unknown), with some Keynesian ideas, but then measures it as problem-solving competence gaps, judging criteria variety and losses of confidence. It is treated through envisioning scenarios, pooling of information, staging of investments, and requests for more information—i.e., treating the specific subjective unknowns and feelings as things that are knowable over time using standard processes. Angus and colleagues’ [15] empirical study focuses on expanding on the obvious point that objective uncertainty (as the impossibility of prediction or the unknowability of future outcomes) differs from subjective uncertainty (as personal doubts about outcomes or the private assessment of the possibility of surprise). They then appear to measure each ex post of the actions (writing a business plan, prototype testing, product updates) and outcomes. So, measures do not match definitions (at a minimum, temporally), and treatments were standard processes (e.g., planning, experimenting, adapting) for knowable unknowns (and risk). Refreshingly, Ramoglou’s paper [4] states explicitly that KU involves the state of unknowability to all (i.e., TU), but then later some hesitation appears when it implies that knowing some knowable opportunity characteristics will somehow help increase the chances of success in dealing with a KU-plagued decision (versus only in dealing with real business issues in general—where, yes, more information is almost always better).

3.4. Interpreting the Analysis Results

Every recent paper describes uncertainty as we do—observed in their authors’ own words—as TU (or implied as such by the use of the KU label without any explicit restrictions or statements to the effect that it does not cover uninsurability). What is alarming is that they all have also violated what TU embodies—by suggesting it can be successfully treated. Many further, and without explanation, state that such treatments advantage entrepreneurs. There are many possible explanations for this odd pattern of suggestions, including the complexity of the TU concept; a confusion between the hypothetical and real worlds when suggesting prescriptions10; the perceived requirement to ‘offer solutions’ to problems in order to be published (e.g., rather than arguing that luck is the ultimate explanation); the temptation to offer solutions when practitioner demand and the substantive peer optimism exists [4]; and, the desire to continue the rich history of story-telling about the ‘uncertainty-exploiting entrepreneur’ [16]. One seemingly simple explanation—that combines several of the preceding ones—is that the authors are imagining a longer-term process: instead of focusing on a strategic decision that must be made by a specific time (i.e., one that involves big performance stakes and irreversible resource commitments); the authors are assuming that many smaller decisions can be made with subsequent actions taken and then with feedback provided and learning happening, all prior to that big strategic decision having to be made. Of course, that drawn-out process is not what Knight [2] had in mind when describing uncertainty as uninsurable, what is captured in our definition of TU, nor what is ever fully modeled in any of those papers we assessed11 (i.e., given that none explain the competitive race to reduce reducible unknowns).

Table 1 offers a summary of the assessments thus far, providing an organized picture of the state of the relevant literature by delineating the different uncertainty definitions and different dynamics embodied in the papers. The columns refer to a paper’s definition of the uncertainty their decision-makers are given; the definitions range from an explicit characterization of TU, to an implied TU (e.g., due to the unrestricted use of the KU label), and to a description of an unknown as not-TU (e.g., instead being a risk or an informational asymmetry). The rows refer to a paper’s assumption of the timing of the focal strategic decision—as being either a one-shot, one-deadline decision, or a multi-shot process with a delayed final decision. The latter is further delineated into two types: (i) papers that either focus more on winning through actions taken prior to the big decision—ones that reduce the uncertainty over time so a better decision can be made; and (ii) papers that focus more on winning through having better reactions to whatever outcomes the focal uncertainty produces by building contingencies, options, and other flexibilities—ones based on more accurate predictions made by also taking some actions prior to the decision that increase the understanding of the focal uncertainty and its effects. None of the assessed papers addresses TU (i.e., the cell denoted by the first column and first row). However, over a century ago, Knight [2] did, suggesting that some decision-makers will choose to bear that uncertainty if they wish to succeed as what he called ‘entrepreneurs’12.

Table 1.

A Mapping of the Recent Literature that Theorizes on Uncertainty, Its Dynamics, and How to Address It.

Almost all the relevant research is located in the first two columns and the last two rows. With the exception of one paper located in the last column, the remainder either explicitly characterizes their uncertainties consistent with TU, or they apply the KU label with the unchallenged implication that the uncertainty is uninsurable (i.e., is TU). Further, all these papers speak to some lengthy process of making given unknowns known using some known and feasible learning routine—essentially delaying the big decision until more information is gathered. Such processes repeat some version of the set of learning methods suggested by Knight and others a century ago or more. These are all treatments for uncovering the focal unknown value of a key known factor (e.g., the value being the ‘level’ of the factor ‘future demand’; the value being the ‘viability’ of the factor ‘new technology’), doing so within a finite period of time. Such treatments include scientific experimentation, rational search, controlled influence on other parties, and learning-based-on-feedback, more generally. When such learning-about-unknowns prior to the big decision does not optimize choices alone, there are papers that apply whatever was learned in order to narrow the wide scope of possible outcomes to a known finite set that then can be used to construct a comprehensive reaction strategy—with contingencies ready for leveraging any realized, pre-identified outcomes. (Such contingencies may involve investments in flexibility, in adaptive systems, in real options, and in dynamic capabilities).

Overall, Table 1 indicates that the recent uncertainty theory work provides useful but non-novel prescriptions for non-TU problems—for decisions vexed by known unknowns that are, in fact, open to being made knowable through known and feasible means. That said, none of the papers actually provides a complete model of those means—at least in terms of specifying what the actual competition-to-make-the-unknown-known-first looks like in that system. Even though each paper infers their prescription will make the entrepreneurial decision-maker successful, none detail the reasons why their venture wins in those learning races, at what costs, and based on which first-mover advantages. For those reasons, it is unlikely that such papers offer much value to academia or to practice. Most at issue for this paper, though, is the fact that none take TU and its non-optimizability seriously; each past work either contradicts the definition of TU by attempting to provide a treatment for it or confuses TU with an uncertainty that is not TU. So, where does that leave us? It leaves us to consider the set of more fundamental theorizing over uncertainty-based entrepreneurship that many of these papers refer to, in order to see if the better understandings of TU lie there.

3.5. True Uncertainty in the Current Set of Partial Theories of Entrepreneurship

The most visible (current) theories of entrepreneurship all involve uncertainty, mainly conceptualized on some interpretation of Knight’s [2] work [1] (p. 453). So, if we are going to suggest remedies for the concerns over TU, then we need to consider the deeper ways it has been leveraged in the field by going beyond the assessment of single, recent papers on the subject that we have completed above. Table 2 summarizes how the main partial theories of entrepreneurship acknowledge and seek to address uncertainty. In that table, for each of the five theories considered in the first column, we briefly describe how it embodies and addresses uncertainty—and TU specifically—in the second column, and then we assess its underlying model in the third column, providing specific suggestions for improvements relevant to uncertainty and/or entrepreneurship.

Table 2.

Assessing the current set of partial entrepreneurship theories and their relationships with true uncertainty.

All the theories identify uncertainty as a significant issue. All then propose ways to treat their described uncertainty. Most recognize TU specifically by explicitly describing how unknowable factors, or unknowable values of core known factors, exist in their focal contexts. That said, not all explicitly recognize that such unknowns exist at the time the focal decision must be made but instead suggest that the key unknowns are convertible to knowns by that time, just as most of the recent papers do. However, when they do recognize that the unknowns remain, there is still an implementable solution offered to treat the described-as-immitigable uncertainty which, in some cases, just boils down to simply bearing it and being lucky, regardless of the label applied (e.g., entrepreneurial judgment). The other theories—the ones that do not define their uncertainty rigorously enough to rule out their uncertainty as embodying TU—also provide solutions, making it unclear whether they do in fact, and erroneously, apply to TU. As such, all of these theories either explicitly, or implicitly by failing to rule it out, suffer from the same concerns as the set of papers assessed do, because they either contain a core logical contradiction of the TU definition, or misrepresent something that is not TU as TU.

As with the majority of the recent papers, almost all of the current theories assume that whatever is unknown ‘as given’ can and will be made sufficiently knowable when the focal decision really needs to be made. These theories further assume that the process for identifying the best choice is also known or knowable, especially to entrepreneurs. These multi-step treatments to address the focal uncertainties—the uncertainties that seem to vex incumbents—are often presented as the main contribution of the theory. Such treatments include experimentation, learning, search, influence, scenario-planning, building real options, and applying heuristics. But there is no rationale for why such treatments favor entrepreneurs, given all of these approaches are available to incumbents, incumbents that would likely have more expertise and experience in pursuing them (e.g., conducting scenario-planning) as well as more resources to apply in so doing. That then raises the question of why the entrepreneur would ever win. That question is not answered, however, either at the level of simply identifying the uncertainty treatment or in the description of the actual mechanics of applying the treatment. To the latter point, none of those partial theories explicitly models the competitive process of applying the prescribed treatment in a manner that explains who wins. The winning implied in these theories seems to involve the assumption that the firm that makes the given unknown known first can make the best decision first and so gain some at-least-temporary relative advantage. Even the implied premise that being first to make the unknown known will be advantageous implied is under-explained, as none of these theories prove that acting first matters in the face of whatever they define as uncertainty, because there is no logic given in either the papers or in the partial theories that deduces any necessary second-mover disadvantage.

4. Consequent Remedies

We now draw from our assessments of the relevant ideas presented in recent work (i.e., in both the papers and the partial theories) to suggest a set of remedies to improve the future study of uncertainty, and especially of TU. We begin by suggesting remedies to the main concerns raised in our assessment of individual papers and reviews, then move to remedies that address concerns related to the current set of partial entrepreneurship theories, and finish with general takeaways for research on uncertainty and other complex and exploitable systems concepts.

Two major concerns are apparent in the depiction of TU within the recent set of papers and reviews: One is that many of the pieces not only provide a description of untreatable uncertainty (i.e., TU) but then follow it by suggesting a logically inconsistent treatment for it. The other is that most of the remaining pieces describe a reasonable treatment for a given uncertainty that is not TU but then imply either that the uncertainty is TU, or that TU is also covered by that treatment in an unintended misrepresentation of the decision-problem.

We suggest four remedies to address these concerns: First, in papers whose main contribution involves uncertainty, there needs to be a full clarification of the type of uncertainty being addressed, so the confusion over important characteristics, such as its inherent treatability or dynamics, can be mitigated. Significant care and space need to be spent in such a paper on clarifying the decision problem, especially its dynamics and how that affects the ability to learn about any unknowns prior to a strategic action having to be made. Second, in papers whose main contribution is prescribing a treatment for an uncertainty, there needs to be an explicit delineation of the novelty of such a treatment, given the sizable set of existing and well-known suggestions. Third, in papers whose main contribution is a prescription for winning by outperforming rivals also facing decisions vexed by the same uncertainty, there needs to be a full modeling of how the proposed treatment must favor the decision-maker, especially when their firm is normally at a disadvantage against better-resourced rivals. For example, in papers that involve a learning-based treatment, the requirement would involve an explicit statement of the heterogeneity of the winner to others in that learning race and an explanation of why winning that race would matter by identifying the first-mover advantages involved. Fourth, in papers that suggest ‘solving’ the given decision-problem by changing it and so changing the uncertainty involved (e.g., so now only risk is at play), there needs to be much more explicit clarification about that original problem being no longer addressed, how that alteration affects the firm (e.g., in switching its goal from optimization of value to maximin), and what the altered problem then means to all the other relevant parties involved (e.g., to rivals or partners)13.

Two major concerns also became apparent in the depiction of TU in the current set of partial theories of entrepreneurship: One is that the most recent theories lack explicit boundaries of their application as they fail to specify under which exact circumstances, and most importantly under which exact uncertainties, the theory does not work. The second concern is that these theories lack an explicit specification of the minimum set of drivers needed to accomplish the successful outcomes they predict. None detail exactly what core market failures and heterogeneities exist that lead to an expectation of new entry and its sustained performance advantage or even of whatever definition of entrepreneurship they use.

We suggest three remedies to address these concerns: First, at a minimum, each theory needs to provide explicit boundaries relating to any uncertainties it involves, because uncertainty remains an often-confused, poorly labeled, and complex concept. Each theory needs to specify where their predictions and prescriptions do not apply (e.g., they cannot apply to decisions involving unknown unknowns). If the theory insists that it applies to TU, then it needs to provide a careful explanation of how the logical contradiction over non-optimizability is avoided. Second, each theory needs to delineate and highlight the underlying drivers of advantage for their entrepreneurs, clearly detailing the set of underlying differences between the focal entrepreneur and the other entities that provide the performance advantage, specifically here, in terms of exploiting any unknowns in the given system context. Third, each theory needs to explicitly separate out what is controllable by, and therefore prescribable to, the entrepreneur in these contexts. This may require a section be included in those theories devoted to the explicit acknowledgment of luck (e.g., in endowments, windfalls, or heterogeneity) and its impacts on the predicted long-term outcomes. We speak here to bridging a current gap in the entrepreneurship theories—i.e., where no existing theory has succeeded in not holding contradictory assumptions about uncertainty. A new theory needs to be built that is wholly true to its implicit and explicit premises, especially about unknowns and their unknowableness.

Besides these sets of specific remedies to the relevant research on uncertainty, and especially on TU, we add two more general recommendations: One is aimed at improving research on this kind of topic—a topic that is complex and confused. The other is aimed at improving this kind of research—the kind that seems to offer a ‘rule for riches’.

To deconfuse complex research topics, such as uncertainty, we recommend finding agreement on a clear typology of the concept so that work can build on a solid foundation. Without such a typology and without clear definitions, we will continue to see the logical errors we have identified in the recent literature, like the attempted treatment of untreatable uncertainty and the treatment of treatable uncertainties that are mislabeled as untreatable. Given that such errors are harmful to both academia and practice, it is paramount to have our field agree upon some standard definitions of the main types of uncertainty to help avoid those errors. Here, at a minimum, a consensus typology needs to delineate between treatable and untreatable uncertainties—i.e., between the decisions that are optimizable despite being plagued by some focal unknowns and the decisions that not optimizable due to the unknowns. If we do not clarify the definitions (e.g., of risk, ambiguity, uncertainty, ignorance, and so on), then the current confusion will continue. And it is a costly confusion—the lack of scientific-level precision of constructs and concepts causes miscommunication, impedes the building upon and testing of each other’s work, and makes the identification of redundancies, inconsistencies, and gaps in the research more difficult. It is also an unnecessary confusion at this stage in the study of these uncertainty-related phenomena, let alone at this stage of the evolution of the entrepreneurship field. We should make a concerted effort to provide clarity rather than allowing the confusion to continue to exist and even to be exploited14.

With the specification of the unknown’s type—even ex post—comes the ability to determine what could be, or could have been, done regarding the focal decision. For example, if the unknown turned out to be an unknown unknown (i.e., a factor that could not have been known at the time the decision had to be made), then there was nothing that could have been done to make the situation better; it was completely out of the decision-maker’s control. However, if the unknown was an unknown value of a known factor (e.g., an unknowable future demand level; the unknowable future net benefit level of a new technology), then there are some things that one could have possibly done even when such things could not have, by definition, solved the ‘given’ decision problem. For example, actions are sometimes available to alter the given decision into a new but related one that can be optimized. For example, perhaps the probability information that allows the calculation of expected values for each and every option is unknowable, but there is still sufficient information that allows the calculation of all worst possible outcomes for each option; in that case, one can alter the decision’s maximand to one of maximizing the minimum outcome and then successfully optimize that new, but different, decision. And that itself might be valuable to the firm. So, for research topics that remain confusing in the literature, we strongly suggest coming to an agreement on a solid, logically coherent typology so that work can then build on consistent ideas rather than flounder on reinventions and misinterpretations of what are usually basic distinctions (e.g., about whether an uncertainty is treatable or not).

Our second recommendation is aimed at improving the kind of research that seems to offer a ‘rule for riches’. We need to avoid implying that ‘we in academia’ can do the impossible, no matter how privately attractive that is. It is publicly costly for any field to have any hint of selling ‘rules for riches’, and it is especially harmful to the legitimacy of any peer work that does not follow suit due to the negative spillovers involved. However, such rules are not uncommonly sold in the history of business research, and, arguably, the recent array of papers that imply there has been some breakthrough for treating untreatable uncertainties serves as but one example. Entrepreneurship, and strategic management more generally, both have a history of promoting various gimmicks and fads [23]. Desperate and lazy managers alike want to believe that ‘ten-dollar bills are lying around on the streets’ and are encouraged to believe so when they read about various successful serial entrepreneurs and firms enjoying sustained superior profitability. Rather than interpreting those cases as outliers (e.g., as lottery winners, or as having special access to rare factors, or as being able to cheat the system by abusing market power), they ignore the high underlying failure rates and choose to believe that such magic really exists, feeling the pressure to imbibe in it for fear of missing out. One reason for such behavior is that academia has often promoted such naïve narratives, and happily and self-servingly fed them, because it is privately profitable15. It is certainly a better story to tell than admitting that all major theories of rents clearly regress back to luck as the original source of relative or absolute advantage (e.g., in obtaining a windfall of better resources, capabilities, knowledge, market power, factors, ideas, and so on—see [26,27,28]).

5. A Concluding Perspective

This paper provides a constructively critical, provocative, evidenced perspective that adds to a lively conversation over the topic of uncertainty, one aimed at improving both its theoretical and practical understanding. In our case, we have contributed to the conversation by arguing a set of recommendations grounded in the concerns raised by assessing the recent surge in uncertainty-focused theorizing in the entrepreneurship literature. We stress that our core argument involves the need for logical consistency in theorizing (e.g., that we cannot allow papers that define a phenomenon as untreatable only to then propose treatments).Our overall message aligns well with Ramoglou’s analysis and critique [4] of the use of the word uncertainty—and specifically the KU label—in the papers that have proposed opportunity-related paradoxes in recent entrepreneurship theory. It also aligns well with Arend’s critical work [29,30,31], including his recommendation for the field to focus on the analysis of very specific problems plagued by very specific uncertainties and bounded by very specific knowns to better determine any appropriate actions, and for the field to address the many impediments that plague the clarification of the uncertainty concept (see also [1,4]).

The need to clarify what uncertainty is also raises a possibly uncomfortable and substantial shift in conceptualizing exactly what entrepreneurship is. If we admit that TU is untreatable—that decisions plagued by it are non-optimizable by all—then there is almost no role for an entrepreneur’s skill in dealing with such decisions other than to efficiently bear the uncertainty and hope for the best. That admission then means that truly skilled entrepreneurship can only arise outside of decisions vexed by TU; it implies that what the field is left studying are simply competitive learning races—races to identify and leverage a known factor’s unknown value in feasible ways (e.g., by learning quickly about a new product’s precise future demand level or a new patent’s maximum gross benefits). That kind of entrepreneurship would consequently mean a focus on the known path(s) for determining the initially unknown value of that key factor over time. That focus is quite different from exploring the more exciting question of how something unknowable affects a strategic decision, the decision-maker’s actions, and the outcomes. Further, that focus on the ‘learning race version of entrepreneurial activity’ would overlap heavily with the rich literature on analogous models16—where entities partake in a number of risky experiments that may or may not lead to private profitability17. So, a big question is then raised over whether the entrepreneurship field can be satisfied almost solely by celebrating the interesting, perhaps even creative, ways that such experimentation and learning occurs in small and real (e.g., boundedly rational) new ventures through the use of various modes of prodding reactions from stakeholders, including customers and investors, even when such paths are mainly predictable in nature? We doubt it (see note 1).

Of course, entrepreneurship involves more than just the old, hypothetical, Knightian story about bearing uncertainty when others do not; it also involves all the practical challenges of bringing new ideas to market in a real world full of economic frictions and temporary informational gaps. For example, it can include the need to secure financing in contexts embodying significant informational asymmetries [33]; negotiate asymmetric partnerships in contexts ripe for capture and exploitation by larger entities [34]; build barriers to imitation when a first-mover advantage is realized [35]; construct options over scale and next-generation technologies [36]; and so on. Perhaps it is to these implementation challenges that the new ‘big’ theories and research will shift, and possibly with more impact and clarity?

Regardless of whether that shift happens, we as a field must admit to the fact that we have not done nearly as good a job as we could have on clarifying uncertainty, even at the most basic level of delineating which can and cannot be treated (i.e., on recognizing TU). We know that we need to do a better job—a more explicit job—of studying which uncertainties can and cannot be addressed and by which means the latter can be. When we fail to do so, especially within our core theorizing, then we do a great disservice to all the entrepreneurs who actually deal with the various forms of uncertainty that exist—treatable and not—because we end up misleading rather than helping them. We hope that the illustrated and organized assessments of the recent uncertainty research provided here, and the recommendations that we made that are grounded in them, will lead to an increased and useful understanding of the many uncertainties—including TU—that vex the strategic decisions that confront our varied and interested audiences.

Funding

This research received no external funding.

Data Availability Statement

No new data were generated for this review.

Conflicts of Interest

The author declares no conflicts of interest.

Notes

| 1 | A few clarifications: In the real world, making the reductions can be meaningful, but that is not what we are concerned about for this paper focused on uncertainty theorizing. Note that just because the focal decision is non-optimizable due to one or more irreducible unknowns, that does not mean that anything else is unknown. And just because the decision is non-optimizable does not mean it cannot be acted upon—e.g., Knight is explicit that entrepreneurs can ‘bear’ TU by acting on the decision regardless, and hoping for the best. |

| 2 | In micro-economic models, this heterogeneity is often embodied in asymmetric costs or in constrained choices based on historic conditions (e.g., as with Judo tactics being viable due to single-price markets—see [5]). |

| 3 | Note that the asymmetry here arises not from any directly assumed ex ante heterogeneity between the focal entrepreneur and its rivals; instead, it arises from the fact that TU’s non-optimizability produces different choices among the decision-makers willing to bear it given the theoretically infinite set of actions a firm could take in light of an unknowable future, where no one choice is guaranteed a better expected result than the other (of the set of possible actions remaining after all dominated options and arbitrages are eliminated). |

| 4 | When a decision (e.g., over a possible investment) can be made using standard operating procedures (e.g., using prediction, control, or options-building), or can be covered through insurance, diversification, sharing agreements, or any other means normally available to an incumbent, then the incumbent should have an advantage over the new entrant, all else being equal. However, when all else is not equal—when asymmetries exist between an entrant and incumbents, like that a possible failure of a risky investment entails more negative spillover to the incumbent, or the entrepreneur’s bankruptcy costs are lower, or the internalizable learning costs are higher to the incumbent (see [6])—then entry may still be possible even without TU. |

| 5 | An exception is the detailed typology described and tabled in Arend’s [8] new book on uncertainty. |

| 6 | That is not to say that the ultimate actions could not differ amongst decision-makers. For example, although the randomization mechanism over a choice may be the same (e.g., all firms roll a multi-sided die), luck would provide differences in the actual choices enacted. This is what we explained in the TU-based entrepreneurship story regarding it not requiring a separate heterogeneity assumption. |

| 7 | This situation differs in the real world—a world full of market failures and heterogeneity—where it is expected that each firm would likely have a different version of an optimal solution, one that seeks to maximize its own unique set of costs, utility, and so on. |

| 8 | These are separate things. Any author can have multiple ideas, even conflicting ones, across papers, making it inappropriate to conflate the two. Furthermore, it is a paper’s idea that is normally the reason for a citation, not the author, and so it is the former that is clearly the focus of any assessment here. |

| 9 | We assume honorable intentions of our peers, given we are all striving to increase the understanding of uncertainty. So, when we raise concerns with recent work, we do so knowing unintended errors can occur and real disagreements over premises can arise. Uncertainty is a complex phenomenon, and so, for example, an offered analysis and prescription can sometimes confound an abstract, theoretical context with the real, practical one. Further, given most of the recent papers draw on Knight’s [2] work, and given he is inconsistent in his use of the term uncertainty in that book—at times referring to, or implying TU, and at times not—we can understand some confusion over terminology and definitions. |

| 10 | Even Knight [2] waffled back and forth between the hypothetical and the real (e.g., regarding observed uncertainty—p. 317). |

| 11 | Even the most recent relevant work does little to clarify such issues. While it is good that some research appears to recognize that there are uncertainties that are untreatable [17], most other research has ignored fundamental concerns and instead been swept up in the ‘so what does this mean for AI?’ calls for opinion pieces [1,18]. While interesting, such uncertainty+AI papers appear to suffer from two problems: first, they fail to seriously consider the should-have-been-predicted ethical problems that AI can pose (e.g., the Facebook algorithm’s culpability in the 2016/17 Myanmar atrocities—see [19]); and, second, they fail to recognize research outside their micro-tribe (e.g., as each chose not to cite a recent book chapter specifically tackling the relationship of uncertainty to AI—see [8]). |

| 12 | Note that there are two alternative actions also listed in this cell. The first—exiting from a TU—does not directly address the problem; it just offers a way out of the problem for a decision-maker (i.e., it only offers a way of dealing with the situation of having the problem—but with not the problem itself). The second—altering the problem to a wholly different problem that is addressable—also does not address the original problem. For example, changing the goal from optimization to maximin—because the available information is available for the latter but not the former—does not actually address the given problem, it just changes the situation. Note that altering the problem is only pursued when it is likely to benefit at least one party vexed by the original problem (net of the costs to doing so); game theory provides a wide and deep literature on how to alter many decisions in beneficial ways [20]. But to be clear, it does not make the original unknowns known but instead substitutes knowables for the unknowns. Also note, no paper assessed here says it is explicitly solving a different problem, implying instead it is solving the original (TU-vexed) problem, which it is not. Finally, note that some research does exist that is explicit on how such uncertainty-vexed problem-altering can work in specific instances [21]. |

| 13 | Perhaps one step towards addressing some of these concerns about how TU is considered in the literature is for the affected fields to begin to be more accepting of theoretical models that involve assumptions that lead to the impossibility of an optimal problem treatment. Such logically coherent but uncomfortable (e.g., Pareto-inefficient) outcomes are not unusual in micro-economics—where they are observed in many expanding-pie games and rivalry models, including the prisoner’s dilemma. This would be a healthier stance to take than the current one, which seems to point at real-world situations where better-than-expected outcomes are achieved, even if solely by luck, and then promoting theories that try to explain it but cannot (e.g., because TU is involved). |

| 14 | We believe that providing clarity begins with agreeing on and enforcing a sharp, over-arching definition for TU, like the one we have suggested, followed by a categorization of phenomena within that definition. TU types could be defined by what the unknown thing is that is causing the non-optimizability of the decision, and that would be useful, assuming that with more knowledge about what is known and not known about the decision comes a greater the understanding is of what can and cannot be achieved with it, as holistic systems thinking advises. There have been attempts at such a typology in recent journal papers [3] but the most comprehensive and clearly delineated one appears in a book [8]. |

| 15 | One way to deter this kind of questionable science would be to improve accountability for those involved. But that is difficult for an academia that has no professional certification, no governing board with any power to discipline its members, and no top journals with paid, professional editors. So, such behavior is expected to continue, if not worsen, with public trust in our research justifiably eroding as a result [24,25]. We have a scientific (and often a public service) responsibility to do better. We should individually and collectively use pressures and policies to mitigate the harmful behaviors in our journals, academies and institutions, in order to defend the sanctity of science with its fundamental premise of seeking truths that lead to deeper understandings of the mechanics of focal phenomena, and to more efficient means to predict and control outcomes. |

| 16 | Such models include patent races, ones that are often mathematically depicted in memoryless Poisson, or in cumulative, or in multi-stage structures, many of which enjoy empirical support. |

| 17 | If we are going to focus on ‘treating the treatables’ and implying that the treatment can be successful, then we must also model the competitive game involved to explain who will win and why, given other firms will also apply the same treatment. Note that such an exercise often requires a whole other paper (e.g., Gavetti et al. [32] provide an example of a model of competitive shaping using an NKES/NKC landscape simulation, but even it remains a long way from dealing with anything deeply uncertain, given it assumes rational agents, static choices among known values performed sequentially, and predictable outcomes [given the model itself proves that the path and equilibrium are predictable and not uncertain]). |

References

- Townsend, D.M.; Hunt, R.R.A.; Rady, J.; Manocha, P.; Jin, J.H. Do Androids Dream of Entrepreneurial Possibilities? A Reply to Ramoglou et al.’s “Artificial Intelligence Forces Us to Rethink Knightian Uncertainty”. Acad. Manag. Rev. 2024; epub ahead of print. [Google Scholar] [CrossRef]

- Knight, F.H. Risk, Uncertainty, and Profit; Houghton Mifflin: Boston, MA, USA, 1921. [Google Scholar]

- Packard, M.D.; Clark, B.B.; Klein, P.G. Uncertainty types and transitions in the entrepreneurial process. Organ. Sci. 2017, 28, 840–856. [Google Scholar] [CrossRef]

- Ramoglou, S. Knowable opportunities in an unknowable future? On the epistemological paradoxes of entrepreneurship theory. J. Bus. Ventur. 2021, 36, 106090. [Google Scholar] [CrossRef]

- Gelman, J.R.; Salop, S.C. Judo economics: Capacity limitation and coupon competition. Bell J. Econ. 1983, 14, 315–325. [Google Scholar] [CrossRef]

- Covin, J.G.; Garrett, R.P.; Kuratko, D.F.; Bolinger, M. Internal corporate venture planning autonomy, strategic evolution, and venture performance. Small Bus. Econ. 2021, 56, 293–310. [Google Scholar] [CrossRef]

- Milliken, F.J. Three types of perceived uncertainty about the environment: State, effect, and response uncertainty. Acad. Manag. Rev. 1987, 12, 133–143. [Google Scholar] [CrossRef]

- Arend, R.J. Uncertainty in Strategic Decision Making: Analysis, Categorization, Causation and Resolution; Springer Nature: Cham, Switzerland, 2024. [Google Scholar]

- Teece, D.J. Profiting from technological innovation: Implications for integration, collaboration, licensing and public policy. Res. Policy 1986, 15, 285–305. [Google Scholar] [CrossRef]

- Klein, P.G. Uncertainty and entrepreneurial judgment during a health crisis. Strateg. Entrep. J. 2020, 14, 563–565. [Google Scholar] [CrossRef]

- Andries, P.; Debackere, K.; Van Looy, B. Simultaneous experimentation as a learning strategy: Business model development under uncertainty—Relevance in times of COVID-19 and beyond. Strateg. Entrep. J. 2020, 14, 556–559. [Google Scholar] [CrossRef]

- Giménez Roche, G.A.; Calcei, D. The role of demand routines in entrepreneurial judgment. Small Bus. Econ. 2021, 56, 209–235. [Google Scholar] [CrossRef]

- Rapp, D.J.; Olbrich, M. From Knightian uncertainty to real-structuredness: Further opening the judgment black box. Strateg. Entrep. J. 2023, 17, 186–209. [Google Scholar]

- Miozzo, M.; DiVito, L. Productive opportunities, uncertainty, and science-based firm emergence. Small Bus. Econ. 2020, 54, 539–560. [Google Scholar]

- Angus, R.W.; Packard, M.D.; Clark, B.B. Distinguishing unpredictability from uncertainty in entrepreneurial action theory. Small Bus. Econ. 2023, 60, 1147–1169. [Google Scholar]

- Brattström, A.; Wennberg, K. The entrepreneurial story and its implications for research. Entrep. Theory Pract. 2022, 46, 1443–1468. [Google Scholar] [CrossRef]

- Clark, D.R.; Hunt, R.A. The Challenge and Opportunity of a Quantum Mechanics Metaphor in Organization and Management Research: A Response to Shelef, Wuebker, and Barney’s “Heisenberg Effects in Experiments on Business Ideas”. Acad. Manag. Rev. 2024; epub ahead of print. [Google Scholar] [CrossRef]

- Ramoglou, S.; Schaefer, R.; Chandra, Y.; McMullen, J.S. Artificial intelligence forces us to rethink Knightian uncertainty: A commentary on Townsend et al.’s “Are the Futures Computable?”. Acad. Manag. Rev. 2024; epub ahead of print. [Google Scholar] [CrossRef]

- Harari, Y.N. Nexus: A Brief History of Information Networks from the Stone Age to AI; Signal: Oxford, UK, 2024. [Google Scholar]

- Brandenburger, A.; Nalebuff, B. Co-Opetition; Broadway Business: New York, NY, USA, 1996. [Google Scholar]

- Arend, R.J. Strategic decision-making under ambiguity: A new problem space and a proposed optimization approach. Bus. Res. 2020, 13, 1231–1251. [Google Scholar] [CrossRef]

- Savage, L.J. The Foundations of Statistics; John Wiley & Sons: London, UK, 1954. [Google Scholar]

- Mintzberg, H.; Pascale, R.T.; Goold, M.; Rumelt, R.P. CMR forum: The “Honda effect” revisited. Calif. Manag. Rev. 1996, 38, 77–117. [Google Scholar]

- Alvesson, M.; Gabriel, Y.; Paulsen, R. Return to Meaning: A Social Science with Something to Say; Oxford University Press: Oxford, UK, 2017. [Google Scholar]

- Tourish, D. Management Studies in Crisis: Fraud, Deception and Meaningless Research; Cambridge University Press: Cambridge, UK, 2019. [Google Scholar]

- Arend, R.J. Mobuis’ Edge: Infinite Regress in the Resource-Based and Dynamic Capabilities View. Strateg. Organ. 2015, 13, 75–85. [Google Scholar]

- Barney, J.B. Strategic factor markets: Expectations, luck, and business strategy. Manag. Sci. 1986, 32, 1231–1241. [Google Scholar]

- Barney, J.B. Is the resource-based “view” a useful perspective for strategic management research? Yes. Acad. Manag. Rev. 2001, 26, 41–56. [Google Scholar]

- Arend, R.J. On the irony of being certain on how to deal with uncertainty. Acad. Manag. Rev. 2020, 45, 702–704. [Google Scholar] [CrossRef]

- Arend, R.J. Confronting when uncertainty-as-unknowability is mismodelled in entrepreneurship. J. Bus. Ventur. Insights 2022, 18, e00334. [Google Scholar] [CrossRef]

- Arend, R.J. Uncertainty and entrepreneurship: A critical review of the research, with implications for the field. Found. Trends Entrep. 2024, 20, 109–244. [Google Scholar]

- Gavetti, G.; Helfat, C.E.; Marengo, L. Searching, shaping, and the quest for superior performance. Strategy Sci. 2017, 2, 194–209. [Google Scholar] [CrossRef]

- Amit, R.H.; Glosten, L.; Muller, E. Does venture capital foster the most promising entrepreneurial firms? Calif. Manag. Rev. 1990, 32, 102–111. [Google Scholar]

- Arend, R.J. SME–supplier alliance activity in manufacturing: Contingent benefits and perceptions. Strateg. Manag. J. 2006, 27, 741–763. [Google Scholar]

- Lieberman, M.B.; Montgomery, D.B. First-mover advantages. Strateg. Manag. J. 1988, 9, 41–58. [Google Scholar]

- McGrath, R.G. Falling forward: Real options reasoning and entrepreneurial failure. Acad. Manag. Rev. 1999, 24, 13–30. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).