Symbolic or Substantive? The Effects of the Digital Transformation Process on Environmental Disclosure

Abstract

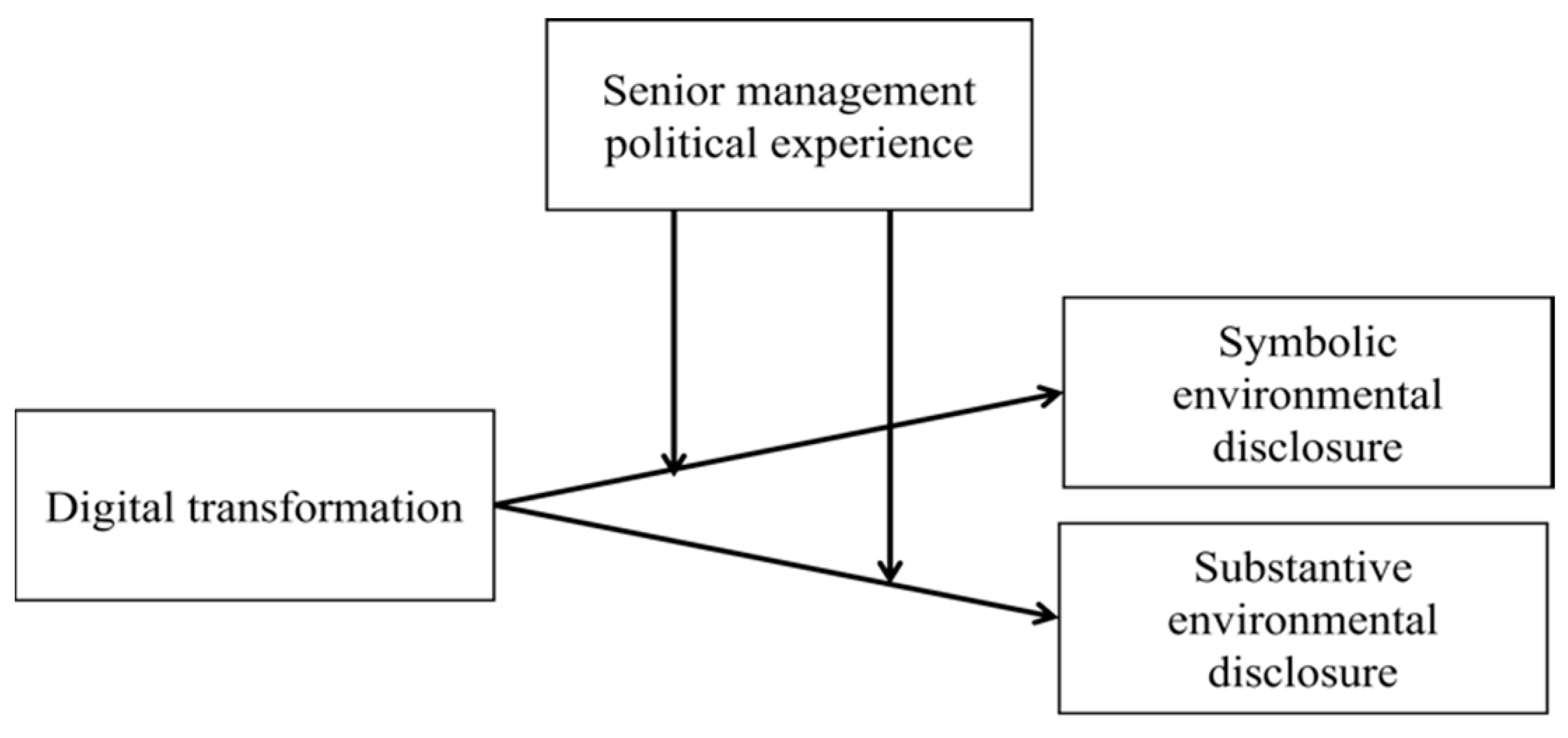

1. Introduction

2. Literature Review and Hypotheses

2.1. Environmental Disclosure as a Strategic Response

2.2. Digital Transformation Efforts and Environmental Disclosure

2.3. Moderating Role of Senior Managers’ Political Experience

3. Methodologies

3.1. Sample Data

3.2. Measures

3.2.1. Dependent Variables: Symbolic and Substantive Environmental Disclosure

3.2.2. Independent Variable: Digital Transformation

3.2.3. Moderating Variable: Senior Managers’ Political Experience

3.2.4. Control Variables

3.3. Models

4. Results

4.1. Descriptive Statistics

4.2. Regression Analysis

4.3. Robustness Analysis

4.4. Additional Analyses

5. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| Variables | Key words |

| Symbolic environmental disclosure | Consistent with environmental policies, compliance with the environmental pollution emission standards, increasing production and reducing pollution, increasing production without reducing pollution, low consumption (low energy consumption), “low pollution, high recycling”, comprehensive resource utilization policies/planning, principles of coordinated environmental and economic development, sustainable development, environmental coordination, coordinated development of production and the environment, integration of economic and environmental benefits, environmental education (environmental propaganda, environmental protection education, and overall environmental awareness), environmental planning, environmental protection technology research (resource utilization technology research, comprehensive utilization technology research of waste), environmental monitoring, identification of pollution sources, environmental protection measures, environmental pre-assessment, environmental assessment (environmental evaluation) |

| Substantive environmental disclosure | Sewage charges (pollutant discharge charges), effluent charges, exhaust gas charges (air pollution prevention charges), solid waste charges, hazardous waste charges, charges for exceeding noise limits (noise abatement charges), centralized waste disposal charges, acquisition of environmental protection equipment, maintenance fees, coal-fired boiler remediation fees, retirement obligations, industries’ conversion development funds, clean production processes, comprehensive utilization of “three wastes”, clean production technologies, standard emissions, purification treatments, environmental construction projects, production safety costs, production protection costs, labor protection fees, environmental recovery and governance bonds, environmental restoration costs, greening fees, environmental administration expenses, pollution prevention and control costs, key pollution source prevention and control costs, regional pollution prevention and control costs, environmental monitoring fees, environmental research fees, environmental management fees |

References

- Perez-Batres, L.A.; Doh, J.P.; Miller, V.V.; Pisani, M.J. Stakeholder Pressures as Determinants of CSR Strategic Choice: Why do Firms Choose Symbolic Versus Substantive Self-Regulatory Codes of Conduct? J. Bus. Ethics 2012, 110, 157–172. [Google Scholar] [CrossRef]

- Gong, G.; Xu, S.; Gong, X. On the Value of Corporate Social Responsibility Disclosure: An Empirical Investigation of Corporate Bond Issues in China. J. Bus. Ethics 2016, 150, 227–258. [Google Scholar] [CrossRef]

- Tashman, P.; Marano, V.; Kostova, T. Walking the walk or talking the talk? Corporate social responsibility decoupling in emerging market multinationals. J. Int. Bus. Stud. 2019, 50, 153–171. [Google Scholar] [CrossRef]

- Cho, C.H.; Roberts, R.W.; Patten, D.M. The language of US corporate environmental disclosure. Account. Org. Soc. 2010, 35, 431–443. [Google Scholar] [CrossRef]

- Cho, C.H.; Laine, M.; Roberts, R.W.; Rodrigue, M. Organized hypocrisy, organizational façades, and sustainability reporting. Account. Org. Soc. 2015, 40, 78–94. [Google Scholar] [CrossRef]

- Shu, C.; Zhou, K.Z.; Xiao, Y.; Gao, S. How Green Management Influences Product Innovation in China: The Role of Institutional Benefits. J. Bus. Ethics 2016, 133, 471–485. [Google Scholar] [CrossRef]

- Luo, X.R.; Wang, D.; Zhang, J. Whose Call to Answer: Institutional Complexity and Firms’ CSR Reporting. Acad. Manag. J. 2017, 60, 321–344. [Google Scholar] [CrossRef]

- Manes-Rossi, F.; Nicolo, G. Exploring sustainable development goals reporting practices: From symbolic to substantive approaches—Evidence from the energy sector. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1799–1815. [Google Scholar] [CrossRef]

- Truong, Y.; Mazloomi, H.; Berrone, P. Understanding the impact of symbolic and substantive environmental actions on organizational reputation. Ind. Mark. Manag. 2021, 92, 307–320. [Google Scholar] [CrossRef]

- Xu, G.; Zhou, Y.; Ji, H. How Can Government Promote Technology Diffusion in Manufacturing Paradigm Shift? Evidence From China. IEEE Trans. Eng. Manag. 2023, 70, 1547–1559. [Google Scholar] [CrossRef]

- Zhou, J.; Li, P.; Zhou, Y.; Wang, B.; Zang, J.; Meng, L. Toward New-Generation Intelligent Manufacturing. Engineering 2018, 4, 11–20. [Google Scholar] [CrossRef]

- Lin, B.; Zhang, Q. Corporate environmental responsibility in polluting firms: Does digital transformation matter? Corp. Soc. Responsib. Environ. Manag. 2023, 30, 2234–2246. [Google Scholar] [CrossRef]

- Chen, P.; Hao, Y. Digital transformation and corporate environmental performance: The moderating role of board characteristics. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1757–1767. [Google Scholar] [CrossRef]

- Xv, Q.; Li, X.; Guo, F. Digital transformation and environmental performance: Evidence from Chinese resource-based enterprises. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 1816–1840. [Google Scholar]

- Lu, Y.; Xu, C.; Zhu, B.; Sun, Y. Digitalization transformation and ESG performance: Evidence from China. Bus. Strateg. Environ. 2024, 33, 352–368. [Google Scholar] [CrossRef]

- Zhang, W.; Zhao, J. Digital transformation, environmental disclosure, and environmental performance: An examination based on listed companies in heavy-pollution industries in China. Int. Rev. Econ. Financ. 2023, 87, 505–518. [Google Scholar] [CrossRef]

- Mariani, M.M.; Machado, I.; Magrelli, V.; Dwivedi, Y.K. Artificial intelligence in innovation research: A systematic review, conceptual framework, and future research directions. Technovation 2023, 122, 102623. [Google Scholar] [CrossRef]

- Blichfeldt, H.; Faullant, R. Performance effects of digital technology adoption and product & service innovation—A process-industry perspective. Technovation 2021, 105, 102275. [Google Scholar]

- Frank, A.G.; Mendes, G.H.S.; Ayala, N.F.; Ghezzi, A. Servitization and Industry 4.0 convergence in the digital transformation of product firms: A business model innovation perspective. Technol. Forecast. Soc. 2019, 141, 341–351. [Google Scholar] [CrossRef]

- Vial, G. Understanding digital transformation: A review and a research agenda. J. Strateg. Inf. Syst. 2019, 28, 118–144. [Google Scholar] [CrossRef]

- Usai, A.; Fiano, F.; Messeni Petruzzelli, A.; Paoloni, P.; Farina Briamonte, M.; Orlando, B. Unveiling the impact of the adoption of digital technologies on firms’ innovation performance. J. Bus. Res. 2021, 133, 327–336. [Google Scholar] [CrossRef]

- Sun, Z.; Sun, X.; Wang, W.; Wang, W. Digital transformation and greenwashing in environmental, social, and governance disclosure: Does investor attention matter? Bus. Ethics 2023, 1–22. [Google Scholar] [CrossRef]

- Bai, C.; Dallasega, P.; Orzes, G.; Sarkis, J. Industry 4.0 technologies assessment: A sustainability perspective. Int. J. Prod. Econ. 2020, 229, 107776. [Google Scholar] [CrossRef]

- Zhou, Y.; Zang, J.; Miao, Z.; Minshall, T. Upgrading Pathways of Intelligent Manufacturing in China: Transitioning across Technological Paradigms. Engineering 2019, 5, 691–701. [Google Scholar] [CrossRef]

- Duanmu, J.-L.; Bu, M.; Pittman, R. Does market competition dampen environmental performance? Evidence from China. Strateg. Manag. J. 2018, 39, 3006–3030. [Google Scholar] [CrossRef]

- Zimmerman, M.A.; Zeitz, G.J. Beyond Survival: Achieving New Venture Growth by Building Legitimacy. Acad. Manag. Rev. 2002, 27, 414–431. [Google Scholar] [CrossRef]

- Greenwood, R.; Raynard, M.; Kodeih, F.; Micelotta, E.R.; Lounsbury, M. Institutional Complexity and Organizational Responses. Acad. Manag. Ann. 2011, 5, 317–371. [Google Scholar] [CrossRef]

- Jackson, G.; Bartosch, J.; Avetisyan, E.; Kinderman, D.; Knudsen, J.S. Mandatory Non-financial Disclosure and Its Influence on CSR: An International Comparison. J. Bus. Ethics 2019, 162, 323–342. [Google Scholar] [CrossRef]

- Perez-Batres, L.A.; Miller, V.V.; Pisani, M.J. CSR, Sustainability and the Meaning of Global Reporting for Latin American Corporations. J. Bus. Ethics 2010, 91, 193–209. [Google Scholar] [CrossRef]

- del Mar Alonso-Almeida, M.; Llach, J.; Marimon, F. A Closer Look at the ‘Global Reporting Initiative’ Sustainability Reporting as a Tool to Implement Environmental and Social Policies: A Worldwide Sector Analysis. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 318–335. [Google Scholar] [CrossRef]

- Hess, D. The Three Pillars of Corporate Social Reporting as New Governance Regulation: Disclosure, Dialogue, and Development. Bus. Ethics Q. 2008, 18, 447–482. [Google Scholar] [CrossRef]

- Wedari, L.K.; Jubb, C.; Moradi-Motlagh, A. Corporate climate-related voluntary disclosures: Does potential greenwash exist among Australian high emitters reports? Bus. Strateg. Environ. 2021, 30, 3721–3739. [Google Scholar] [CrossRef]

- Zhao, M. CSR-Based Political Legitimacy Strategy: Managing the State by Doing Good in China and Russia. J. Bus. Ethics 2012, 111, 439–460. [Google Scholar] [CrossRef]

- Sharma, S. Managerial Interpretations and Organizational Context as Predictors of Corporate Choice of Environmental Strategy. Acad. Manag. J. 2000, 43, 681–697. [Google Scholar] [CrossRef]

- Oliver, C. Strategic Responses to Institutional Processes. Acad. Manag. Rev. 1991, 16, 145–179. [Google Scholar] [CrossRef]

- Meng, X.; Zeng, S.; Xie, X.; Zou, H. Beyond symbolic and substantive: Strategic disclosure of corporate environmental information in China. Bus. Strateg. Environ. 2019, 28, 403–417. [Google Scholar] [CrossRef]

- Shabana, K.M.; Ravlin, E.C. Corporate Social Responsibility Reporting as Substantive and Symbolic Behavior: A Multilevel Theoretical Analysis. Bus. Soc. Rev. 2016, 121, 297–327. [Google Scholar] [CrossRef]

- Bromley, P.; Powell, W.W. From Smoke and Mirrors to Walking the Talk: Decoupling in the Contemporary World. Acad. Manag. Ann. 2012, 6, 483–530. [Google Scholar] [CrossRef]

- Lyon, T.P.; Maxwell, J.W. Greenwash: Corporate Environmental Disclosure under Threat of Audit. J. Econ. Manag. Strategy 2011, 20, 3–41. [Google Scholar] [CrossRef]

- Berrone, P.; Fosfuri, A.; Gelabert, L. Does Greenwashing Pay Off? Understanding the Relationship Between Environmental Actions and Environmental Legitimacy. J. Bus. Ethics 2015, 144, 363–379. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Org. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Rodrigue, M.; Magnan, M.; Cho, C.H. Is Environmental Governance Substantive or Symbolic? An Empirical Investigation. J. Bus. Ethics 2012, 114, 107–129. [Google Scholar] [CrossRef]

- Kunkel, S.; Matthess, M. Digital transformation and environmental sustainability in industry: Putting expectations in Asian and African policies into perspective. Environ. Sci. Policy 2020, 112, 318–329. [Google Scholar] [CrossRef]

- Cardinali, P.G.; De Giovanni, P. Responsible digitalization through digital technologies and green practices. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 984–995. [Google Scholar] [CrossRef]

- Rammer, C.; Fernández, G.P.; Czarnitzki, D. Artificial intelligence and industrial innovation: Evidence from German firm-level data. Res. Policy 2022, 51, 104555. [Google Scholar] [CrossRef]

- Liu, J.; Chang, H.; Forrest, J.Y.-L.; Yang, B. Influence of artificial intelligence on technological innovation: Evidence from the panel data of china’s manufacturing sectors. Technol. Forecast. Soc. 2020, 158, 120142. [Google Scholar] [CrossRef]

- Dalenogare, L.S.; Benitez, G.B.; Ayala, N.F.; Frank, A.G. The expected contribution of Industry 4.0 technologies for industrial performance. Int. J. Prod. Econ. 2018, 204, 383–394. [Google Scholar] [CrossRef]

- Wang, S.; Wan, J.; Zhang, D.; Li, D.; Zhang, C. Towards smart factory for industry 4.0: A self-organized multi-agent system with big data based feedback and coordination. Comput. Netw. 2016, 101, 158–168. [Google Scholar] [CrossRef]

- Cugno, M.; Castagnoli, R.; Büchi, G. Openness to Industry 4.0 and performance: The impact of barriers and incentives. Technol. Forecast. Soc. 2021, 168, 120756. [Google Scholar] [CrossRef]

- Hughes, L.; Dwivedi, Y.K.; Rana, N.P.; Williams, M.D.; Raghavan, V. Perspectives on the future of manufacturing within the Industry 4.0 era. Prod. Plan. Control 2020, 33, 138–158. [Google Scholar] [CrossRef]

- Ghobakhloo, M. Determinants of information and digital technology implementation for smart manufacturing. Int. J. Prod. Res. 2019, 58, 2384–2405. [Google Scholar] [CrossRef]

- Ji, H.; Miao, Z.; Wan, J.; Lin, L. Digital transformation and financial performance: The moderating role of entrepreneurs’ social capital. Technol. Anal. Strategy 2022, 1–18. [Google Scholar] [CrossRef]

- Guinan, P.J.; Parise, S.; Langowitz, N. Creating an innovative digital project team: Levers to enable digital transformation. Bus. Horiz. 2019, 62, 717–727. [Google Scholar] [CrossRef]

- Yuan, Y.; Tian, G.; Lu, L.Y.; Yu, Y. CEO Ability and Corporate Social Responsibility. J. Bus. Ethics 2017, 157, 391–411. [Google Scholar] [CrossRef]

- García-Sánchez, I.-M.; Aibar-Guzmán, B.; Aibar-Guzmán, C.; Azevedo, T.-C. CEO ability and sustainability disclosures: The mediating effect of corporate social responsibility performance. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1565–1577. [Google Scholar] [CrossRef]

- Lashitew, A.A. When businesses go digital: The role of CEO attributes in technology adoption and utilization during the COVID-19 pandemic. Technol. Forecast. Soc. 2023, 189, 122324. [Google Scholar] [CrossRef] [PubMed]

- Lewis, B.W.; Walls, J.L.; Dowell, G.W.S. Difference in degrees: CEO characteristics and firm environmental disclosure. Strateg. Manag. J. 2014, 35, 712–722. [Google Scholar] [CrossRef]

- Sheng, H.; Feng, T.; Liu, L. The influence of digital transformation on low-carbon operations management practices and performance: Does CEO ambivalence matter? Int. J. Prod. Res. 2023, 61, 6215–6229. [Google Scholar] [CrossRef]

- Babiak, K.; Trendafilova, S. CSR and environmental responsibility: Motives and pressures to adopt green management practices. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 11–24. [Google Scholar] [CrossRef]

- Pacheco, D.F.; Dean, T.J.; Payne, D.S. Escaping the green prison: Entrepreneurship and the creation of opportunities for sustainable development. J. Bus. Ventur. 2010, 25, 464–480. [Google Scholar] [CrossRef]

- Sheng, S.; Zhou, K.Z.; Li, J.J. The Effects of Business and Political Ties on Firm Performance: Evidence from China. J. Mark. 2011, 75, 1–15. [Google Scholar] [CrossRef]

- Ji, H.; Miao, Z. Corporate social responsibility and collaborative innovation: The role of government support. J. Clean. Prod. 2020, 260, 121028. [Google Scholar] [CrossRef]

- Zhang, Y.; Yang, Z.; Zhang, T. Strategic resource decisions to enhance the performance of global engineering services. Int. Bus. Rev. 2018, 27, 678–700. [Google Scholar] [CrossRef]

- Zhou, Y.; Miao, Z.; Urban, F. China’s leadership in the hydropower sector: Identifying green windows of opportunity for technological catch-up. Ind. Corp. Chang. 2020, 29, 1319–1343. [Google Scholar] [CrossRef]

- Li, Z. Will Cheap Talk on Environmental responsibility Get Punished? J. World Econ. 2018, 41, 167–188. [Google Scholar]

- Li, Z.; Wenhan, W.; Yao, W. Firms’ Environmental Responsibility Performance and Government Subsidies Empirical Evidence Based on Text Analysis. J. Financ. Econ. 2022, 48, 78–92+108. [Google Scholar]

- Loughran, T.; McDonald, B. When Is a Liability Not a Liability? Textual Analysis, Dictionaries, and 10-Ks. J. Financ. 2011, 66, 35–65. [Google Scholar] [CrossRef]

- He, K.; Chen, W.; Zhang, L. Senior management’s academic experience and corporate green innovation. Technol. Forecast. Soc. 2021, 166, 120664. [Google Scholar] [CrossRef]

- Lu, Y.; Abeysekera, I. Stakeholders’ power, corporate characteristics, and social and environmental disclosure: Evidence from China. J. Clean. Prod. 2014, 64, 426–436. [Google Scholar] [CrossRef]

- White, H. A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity. Econometrica 1980, 48, 817–838. [Google Scholar] [CrossRef]

- Stornelli, A.; Ozcan, S.; Simms, C. Advanced manufacturing technology adoption and innovation: A systematic literature review on barriers, enablers, and innovation types. Res. Policy 2021, 50, 104229. [Google Scholar] [CrossRef]

- Verhoef, P.C.; Broekhuizen, T.; Bart, Y.; Bhattacharya, A.; Qi Dong, J.; Fabian, N.; Haenlein, M. Digital transformation: A multidisciplinary reflection and research agenda. J. Bus. Res. 2021, 122, 889–901. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Bourke, J.; Roper, S. AMT adoption and innovation: An investigation of dynamic and complementary effects. Technovation 2016, 55–56, 42–55. [Google Scholar] [CrossRef]

- Santamaría, L.; Nieto, M.J.; Barge-Gil, A. Beyond formal R&D: Taking advantage of other sources of innovation in low- and medium-technology industries. Res. Policy 2009, 38, 507–517. [Google Scholar]

- Xie, X.; Huo, J.; Zou, H. Green process innovation, green product innovation, and corporate financial performance: A content analysis method. J. Bus. Res. 2019, 101, 697–706. [Google Scholar] [CrossRef]

- Chai, S.; Zhang, K.; Wei, W.; Ma, W.; Abedin, M.Z. The impact of green credit policy on enterprises’ financing behavior: Evidence from Chinese heavily-polluting listed companies. J. Clean. Prod. 2022, 363, 132458. [Google Scholar] [CrossRef]

- Suoniemi, S.; Meyer-Waarden, L.; Munzel, A.; Zablah, A.R.; Straub, D. Big data and firm performance: The roles of market-directed capabilities and business strategy. Inform. Manag. 2020, 57, 103365. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Measurement |

|---|---|

| Symbolic environmental disclosure | Please refer to “dependent variables” section for details |

| Substantive environmental disclosure | Please refer to “dependent variables” section for details |

| Digital transformation | Please refer to “independent variables” section for details |

| Senior managers’ political experience | Please refer to “moderating variables” section for details |

| Firm size | Ln (total assets) |

| Asset/liability ratio | Total liabilities/total assets |

| Chairman’s shareholdings | Shareholding ratio of chairman |

| Firm growth | Growth rate of return on net assets |

| Board size | Ln (numbers of boards members) |

| Duality | 1 if chairman serves as CEO, 0 otherwise |

| Ownership | 1 if firm is state-owned, 0 otherwise |

| Variable | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|

| Symbolic environmental disclosure | 0.604 | 0.698 | 0 | 6.899 |

| Substantive environmental disclosure | 0.860 | 1.065 | 0 | 6.197 |

| Digital transformation | 2.173 | 3.279 | 0 | 16.018 |

| Senior managers’ political experience | 0.444 | 0.497 | 0 | 1 |

| Firm size | 21.844 | 1.145 | 18.760 | 25.306 |

| Asset/liability ratio | 0.373 | 0.188 | 0.025 | 0.804 |

| Chairman shareholdings | 0.115 | 0.161 | 0 | 0.093 |

| Firm growth | 0.010 | 0.033 | 0 | 0.249 |

| Board size | 2.190 | 0.225 | 1.386 | 3.219 |

| Duality | 0.315 | 0.464 | 0 | 1 |

| Ownership | 0.281 | 0.449 | 0 | 1 |

| High-tech industries | 0.513 | 0.500 | 0 | 1 |

| Heavily polluting industries | 0.436 | 0.496 | 0 | 1 |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Symbolic environmental disclosure | 1.000 | ||||||||||

| 2. Substantive environmental disclosure | 0.175 *** | 1.000 | |||||||||

| 3. Digital transformation | −0.017 *** | −0.136 *** | 1.000 | ||||||||

| 4. Square of digital transformation | −0.024 ** | −0.136 *** | 0.935 *** | 1.000 | |||||||

| 5. Senior managers’ political experience | −0.002 | −0.001 | −0.032 *** | −0.031 *** | 1.000 | ||||||

| 6. Firm size | 0.062 *** | 0.245 *** | 0.066 *** | 0.037 *** | 0.041 *** | 1.000 | |||||

| 7. Asset/liability ratio | 0.015 * | 0.147 *** | −0.038 *** | −0.037 *** | −0.009 | 0.536 *** | 1.000 | ||||

| 8. Chairman shareholdings | −0.016 * | −0.122 *** | 0.048 *** | 0.043 *** | −0.017 ** | −0.336 *** | −0.267 *** | 1.000 | |||

| 9. Firm growth | −0.015 * | 0.008 | 0.034 *** | 0.032 *** | −0.029 *** | −0.002 | 0.076 *** | −0.057 *** | 1.000 | ||

| 10. Board size | 0.020 *** | 0.121 *** | −0.051 *** | −0.048 *** | 0.062 *** | 0.231 *** | 0.149 *** | −0.228 *** | 0.028 *** | 1.000 | |

| 11. Duality | −0.023 *** | −0.109 *** | 0.070 *** | 0.055 *** | −0.033 *** | −0.171 *** | −0.148 *** | 0.275 *** | −0.027 *** | −0.153 *** | 1.000 |

| 12. Ownership | 0.022 *** | 0.193 *** | −0.100 *** | −0.077 *** | 0.016 ** | 0.351 *** | 0.311 *** | −0.422 *** | 0.100 *** | 0.244 *** | −0.277 *** |

| Symbolic Environmental Disclosure | Substantive Environmental Disclosure | |||||

|---|---|---|---|---|---|---|

| Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

| Firm size | 0.040 *** | 0.041 *** | 0.041 *** | 0.106 *** | 0.113 *** | 0.112 *** |

| (3.45) | (3.51) | (3.49) | (5.62) | (−6.00) | (−5.99) | |

| Asset/liability ratio | −0.072 | −0.073 | −0.073 | 0.068 | 0.054 | 0.054 |

| (−1.19) | (−1.21) | (−1.21) | (0.68) | (−0.54) | (−0.54) | |

| Chairman shareholdings | 0.000 | 0.000 | 0.001 | −0.001 | −0.001 | −0.001 |

| (0.11) | (0.11) | (0.09) | (−0.28) | (−1.09) | (−1.10) | |

| Firm growth | −0.001 | −0.001 | −0.001 | 0.001 | 0.001 | 0.001 |

| (−0.62) | (−0.58) | (−0.59) | (1.11) | (0.45) | (0.45) | |

| Board size | 0.012 | 0.012 | 0.011 | 0.178 *** | 0.177 *** | 0.177 *** |

| (0.30) | (0.30) | (0.27) | (3.11) | (3.12) | (3.11) | |

| Duality | −0.011 | −0.010 | −0.010 | −0.084 *** | −0.082 *** | −0.082 *** |

| (−0.51) | (−0.49) | (−0.48) | (−2.77) | (−2.72) | (−2.72) | |

| Ownership | 0.005 | 0.005 | 0.003 | 0.232 *** | 0.230 *** | 0.229 *** |

| (0.17) | (0.16) | (0.10) | (4.73) | (4.71) | (4.69) | |

| Senior managers’ political experience | 0.013 | 0.013 | 0.013 | −0.004 | −0.004 | −0.004 |

| (0.67) | (0.67) | (0.67) | (−0.15) | (−0.14) | (−0.14) | |

| Digital transformation | −0.003 | −0.002 | −0.017 ** | −0.015 ** | ||

| (−0.92) | (−0.88) | (−2.47) | (−2.35) | |||

| Square of digital transformation | −0.001 | −0.001 | ||||

| (−1.58) | (−1.60) | |||||

| Interaction term | 0.011 ** | 0.005 | ||||

| (2.41) | (0.80) | |||||

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Firm | Yes | Yes | Yes | Yes | Yes | Yes |

| Adjusted R2 | 0.057 | 0.057 | 0.057 | 0.238 | 0.242 | 0.242 |

| Observations | 14841 | 14841 | 14841 | 14841 | 14841 | 14841 |

| Variable | Symbolic Environmental Disclosure | Substantive Environmental Disclosure |

|---|---|---|

| Digital transformation | 0.000 | −0.001 * |

| (−0.21) | (−1.79) | |

| Square of digital transformation | −0.001 | |

| (−0.42) | ||

| Controls | Yes | Yes |

| Year | Yes | Yes |

| Firm | Yes | Yes |

| Adjusted R2 | 0.028 | 0.219 |

| Observations | 14355 | 14509 |

| First Stage | Second Stage | |

|---|---|---|

| Variables | Digital Transformation | Substantive Environmental Disclosure |

| Fitted_Digital transformation | −0.048 *** | |

| (−3.15) | ||

| Instrumental variable | 0.542 *** (33.72) | |

| Observations | 14434 | 14434 |

| Kleibergen–Paap rk LM statistic (Underidentification test) | 429.155 (p = 0.000) | |

| Cragg–Donald Wald F statistic (Weak identification test) | 2932.571 |

| Variables | Symbolic Environmental Disclosure | Substantive Environmental Disclosure |

|---|---|---|

| Technology-oriented digital transformation | 0.010 * | −0.009 |

| (1.74) | (−0.99) | |

| Market-oriented digital transformation | −0.015 ** | −0.019 *** |

| (−2.53) | (−2.55) | |

| Controls | Yes | Yes |

| Year | Yes | Yes |

| Firm | Yes | Yes |

| Adjusted R2 | 0.058 | 0.242 |

| Observations | 14,841 | 14,841 |

| Variables | HT Industries | LMT Industries | ||

|---|---|---|---|---|

| Symbolic Environmental Disclosure | Substantive Environmental Disclosure | Symbolic Environmental Disclosure | Substantive Environmental Disclosure | |

| Digital transformation | −0.004 | −0.060 ** | −0.009 *** | −0.065 *** |

| (−1.18) | (−7.62) | (−2.34) | (−7.22) | |

| Square of digital transformation | 0.001 | 0.002 | ||

| (0.97) | (1.27) | |||

| Controls | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| Firm | Yes | Yes | Yes | Yes |

| Adjusted R2 | 0.010 | 0.123 | 0.014 | 0.148 |

| Observations | 7677 | 7677 | 6757 | 6757 |

| Variables | Heavily Polluting Industries | Other Manufacturing Industries | ||

|---|---|---|---|---|

| Symbolic Environmental Disclosure | Substantive Environmental Disclosure | Symbolic Environmental Disclosure | Substantive Environmental Disclosure | |

| Digital transformation | −0.001 | −0.060 *** | −0.011 *** | −0.043 *** |

| (−0.34) | (−6.35) | (−2.70) | (−4.18) | |

| Square of digital transformation | 0.003 ** | −0.002 | ||

| (2.23) | (−0.94) | |||

| Controls | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes |

| Adjusted R2 | 0.008 | 0.129 | 0.020 | 0.113 |

| Observations | 6316 | 6316 | 8118 | 8118 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ji, H.; Sheng, S.; Wan, J. Symbolic or Substantive? The Effects of the Digital Transformation Process on Environmental Disclosure. Systems 2024, 12, 197. https://doi.org/10.3390/systems12060197

Ji H, Sheng S, Wan J. Symbolic or Substantive? The Effects of the Digital Transformation Process on Environmental Disclosure. Systems. 2024; 12(6):197. https://doi.org/10.3390/systems12060197

Chicago/Turabian StyleJi, Huanyong, Shuya Sheng, and Jun Wan. 2024. "Symbolic or Substantive? The Effects of the Digital Transformation Process on Environmental Disclosure" Systems 12, no. 6: 197. https://doi.org/10.3390/systems12060197

APA StyleJi, H., Sheng, S., & Wan, J. (2024). Symbolic or Substantive? The Effects of the Digital Transformation Process on Environmental Disclosure. Systems, 12(6), 197. https://doi.org/10.3390/systems12060197