Mitigating Financial Distress by Engaging in Digital Transformation: The Moderating Role of Life Cycles

Abstract

1. Introduction

2. Literature Review and Theoretical Framework

2.1. Financial Distress

2.2. Digital Transformation

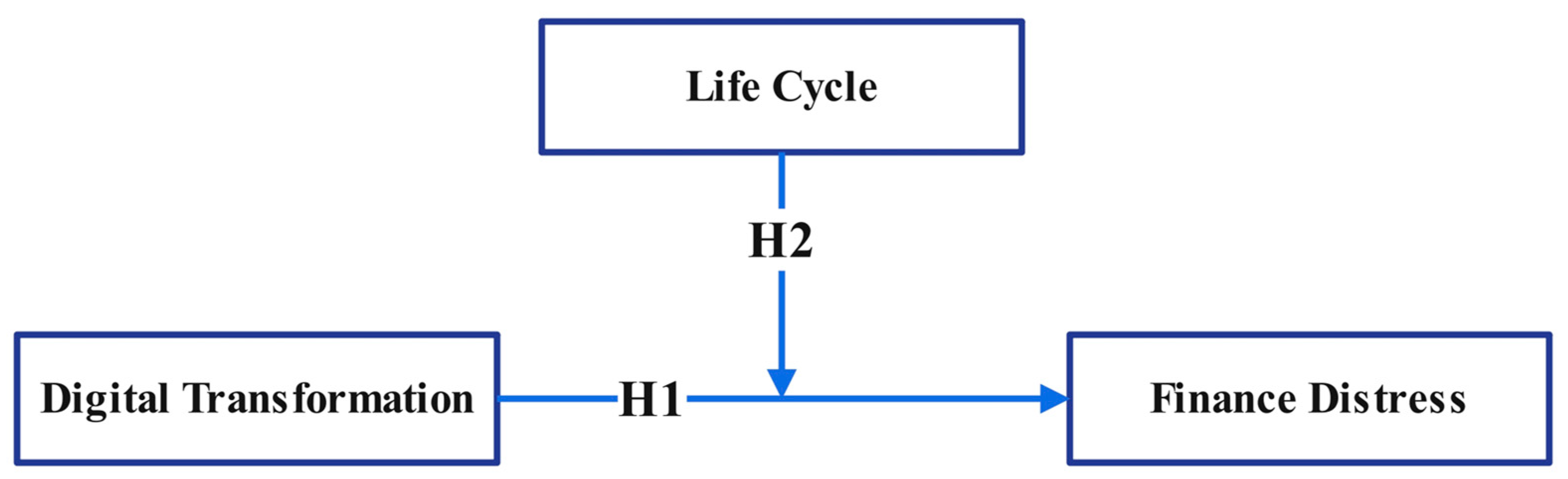

2.3. Theoretical Framework and Hypotheses Development

2.3.1. A Perspective on Digital Transformation and Financial Distress

2.3.2. The Moderating Role of Life Cycle

3. Methodology

3.1. Sample and Data Collection

3.2. Variables

3.2.1. Financial Distress

3.2.2. Digital Transformation

3.2.3. Life Cycle

3.2.4. Control Variable

3.3. Analysis

4. Results

Main Results

5. Discussion

5.1. Theoretical Implications

5.2. Practical Implications

5.3. Limitations and Future Research Prospects

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Purnanandam, A. Financial distress and corporate risk management: Theory and evidence. J. Financ. Econ. 2008, 87, 706–739. [Google Scholar] [CrossRef]

- Aiyar, S.; Calomiris, C.W.; Wieladek, T. Bank capital regulation: Theory, empirics, and policy. IMF Econ. Rev. 2015, 63, 955–983. [Google Scholar] [CrossRef]

- Delis, M.; Galariotis, E.; Monne, J. Economic condition and financial cognition. J. Bank. Financ. 2021, 123, 106035. [Google Scholar] [CrossRef]

- Madrid-Guijarro, A.; García-Pérez-de-Lema, D.; Van Auken, H. An analysis of non-financial factors associated with financial distress. Entrep. Reg. Dev. 2011, 23, 159–186. [Google Scholar] [CrossRef]

- Hanelt, A.; Bohnsack, R.; Marz, D.; Antunes Marante, C. A systematic review of the literature on digital transformation: Insights and implications for strategy and organizational change. J. Manag. Stud. 2021, 58, 1159–1197. [Google Scholar] [CrossRef]

- Hess, T.; Matt, C.; Benlian, A.; Wiesböck, F. Options for formulating a digital transformation strategy. MIS Q. Exec. 2016, 15, 123. [Google Scholar]

- Zhu, Y.; Yu, D. Digital transformation and firms’ bargaining power: Evidence from China. J. Bus. Res. 2024, 183, 114851. [Google Scholar] [CrossRef]

- Van Nguyen, T.; Pham, H.T.; Ha, H.M.; Tran, T.T.T. An integrated model of supply chain quality management, Industry 3.5 and innovation to improve manufacturers’ performance—A case study of Vietnam. Int. J. Logist. Res. Appl. 2024, 27, 261–283. [Google Scholar] [CrossRef]

- Vogel, R.; Güttel, W.H. The dynamic capability view in strategic management: A bibliometric review. Int. J. Manag. Rev. 2013, 15, 426–446. [Google Scholar] [CrossRef]

- Knudsen, D.R. Elusive boundaries, power relations, and knowledge production: A systematic review of the literature on digitalization in accounting. Int. J. Account. Inf. Syst. 2020, 36, 100441. [Google Scholar] [CrossRef]

- Kraus, S.; Durst, S.; Ferreira, J.J.; Veiga, P.; Kailer, N.; Weinmann, A. Digital transformation in business and management research: An overview of the current status quo. Int. J. Inf. Manag. 2022, 63, 102466. [Google Scholar] [CrossRef]

- Matarazzo, M.; Penco, L.; Profumo, G.; Quaglia, R. Digital transformation and customer value creation in Made in Italy SMEs: A dynamic capabilities perspective. J. Bus. Res. 2021, 123, 642–656. [Google Scholar] [CrossRef]

- Warner, K.S.; Wäger, M. Building dynamic capabilities for digital transformation: An ongoing process of strategic renewal. Long Range Plan. 2019, 52, 326–349. [Google Scholar] [CrossRef]

- Atif, M.; Liu, B.; Nadarajah, S. The effect of corporate environmental, social and governance disclosure on cash holdings: Life-cycle perspective. Bus. Strategy Environ. 2022, 31, 2193–2212. [Google Scholar] [CrossRef]

- Durana, P.; Michalkova, L.; Privara, A.; Marousek, J.; Tumpach, M. Does the life cycle affect earnings management and bankruptcy? Oeconomia Copernic. 2021, 12, 425–461. [Google Scholar] [CrossRef]

- Phelps, R.; Adams, R.; Bessant, J. Life cycles of growing organizations: A review with implications for knowledge and learning. Int. J. Manag. Rev. 2007, 9, 1–30. [Google Scholar] [CrossRef]

- Trkman, P. The critical success factors of business process management. Int. J. Inf. Manag. 2010, 30, 125–134. [Google Scholar] [CrossRef]

- Liu, Y.; Wei, H. Digital transformation and enterprise financial asset allocation. Appl. Econ. 2024, 1–18. [Google Scholar] [CrossRef]

- Zhao, X.; Huang, Q.; Zhang, H.; Zhao, L. Can digital transformation in manufacturing enterprises mitigate financial distress? Technol. Anal. Strateg. Manag. 2023, 1–17. [Google Scholar] [CrossRef]

- Liu, F.; Fang, M.; Xiao, S.; Shi, Y. Mitigating bullwhip effect in supply chains by engaging in digital transformation: The moderating role of customer concentration. Ann. Oper. Res. 2024, 1–22. [Google Scholar] [CrossRef]

- Fang, M.; Liu, F.; Xiao, S.; Park, K. Hedging the bet on digital transformation in strategic supply chain management: A theoretical integration and an empirical test. Int. J. Phys. Distrib. Logist. Manag. 2023, 53, 512–531. [Google Scholar] [CrossRef]

- Huang, Y.P.; Yen, M.F. A new perspective of performance comparison among machine learning algorithms for financial distress prediction. Appl. Soft Comput. 2019, 83, 105663. [Google Scholar] [CrossRef]

- Mselmi, N.; Lahiani, A.; Hamza, T. Financial distress prediction: The case of French small and medium-sized firms. Int. Rev. Financ. Anal. 2017, 50, 67–80. [Google Scholar] [CrossRef]

- Peng, Y.; Tao, C. Can digital transformation promote enterprise performance?—From the perspective of public policy and innovation. J. Innov. Knowl. 2022, 7, 100198. [Google Scholar] [CrossRef]

- Zhuo, C.; Chen, J. Can digital transformation overcome the enterprise innovation dilemma: Effect, mechanism and effective boundary. Technol. Forecast. Soc. Change 2023, 190, 122378. [Google Scholar] [CrossRef]

- Liu, W.; Liu, C.; Luo, J.; Liu, F. How does digital transformation promote total factor productivity? Strategy, technology, and application. Manag. Decis. Econ. 2024, 45, 2739–2750. [Google Scholar] [CrossRef]

- Fang, M.; Yu, Y.; Park, K.; Liu, F.; Xiao, S.S.; Shi, Y. Supply chain relationship dependencies and circular economy performance: The contingency role of digitalization capability. J. Purch. Supply Manag. 2024, 30, 100902. [Google Scholar] [CrossRef]

- Wang, M.; Yu, Y.; Liu, F. Does digital transformation curb the formation of zombie firms? A machine learning approach. Technol. Anal. Strateg. Manag. 2023, 1–17. [Google Scholar] [CrossRef]

- Xu, J.; Haris, M.; Liu, F. Intellectual capital efficiency and firms’ financial performance based on business life cycle. J. Intellect. Cap. 2022, 24, 653–682. [Google Scholar] [CrossRef]

- Gordon, M.J. Towards a theory of financial distress. J. Financ. 1971, 26, 347–356. [Google Scholar] [CrossRef]

- Johnston, R.; Markov, S.; Ramnath, S. Sell-side debt analysts. J. Account. Econ. 2009, 47, 91–107. [Google Scholar] [CrossRef]

- White, M.J. The corporate bankruptcy decision. J. Econ. Perspect. 1989, 3, 129–151.e10. [Google Scholar] [CrossRef]

- Bhamra, H.S.; Fisher, A.J.; Kuehn, L.A. Monetary policy and corporate default. J. Monet. Econ. 2011, 58, 480–494. [Google Scholar] [CrossRef]

- Benmelech, E.; Frydman, C.; Papanikolaou, D. Financial frictions and employment during the great depression. J. Financ. Econ. 2019, 133, 541–563. [Google Scholar] [CrossRef]

- Demirguc-Kunt, A.; Love, I.; Maksimovic, V. Business environment and the incorporation decision. J. Bank. Financ. 2006, 30, 2967–2993. [Google Scholar] [CrossRef]

- Alves, P.; Couto, E.B.; Francisco, P.M. Board of directors’ composition and capital structure. Res. Int. Bus. Financ. 2015, 35, 1–32. [Google Scholar] [CrossRef]

- Garlappi, L.; Yan, H. Financial distress and the cross-section of equity returns. J. Financ. 2011, 66, 789–822. [Google Scholar] [CrossRef]

- Cathcart, L.; Dufour, A.; Rossi, L.; Varotto, S. The differential impact of leverage on the default risk of small and large firms. J. Corp. Financ. 2020, 60, 101541. [Google Scholar] [CrossRef]

- Kim, S.Y.; Upneja, A. Predicting restaurant financial distress using decision tree and AdaBoosted decision tree models. Econ. Model. 2014, 36, 354–362. [Google Scholar] [CrossRef]

- Brodeur, J.; Pellerin, R.; Deschamps, I. Collaborative approach to digital transformation (CADT) model for manufacturing SMEs. J. Manuf. Technol. Manag. 2022, 33, 61–83. [Google Scholar] [CrossRef]

- Richard, P.J.; Devinney, T.M. Modular strategies: B2B technology and architectural knowledge. Calif. Manag. Rev. 2005, 47, 86–113. [Google Scholar] [CrossRef]

- AlNuaimi, B.K.; Singh, S.K.; Ren, S.; Budhwar, P.; Vorobyev, D. Mastering digital transformation: The nexus between leadership, agility, and digital strategy. J. Bus. Res. 2022, 145, 636–648. [Google Scholar] [CrossRef]

- Tan, T.F.; Netessine, S. At your service on the table: Impact of tabletop technology on restaurant performance. Manag. Sci. 2020, 66, 4496–4515. [Google Scholar] [CrossRef]

- Aben, T.A.; van der Valk, W.; Roehrich, J.K.; Selviaridis, K. Managing information asymmetry in public–private relationships undergoing a digital transformation: The role of contractual and relational governance. Int. J. Oper. Prod. Manag. 2021, 41, 1145–1191. [Google Scholar] [CrossRef]

- Li, L. Digital transformation and sustainable performance: The moderating role of market turbulence. Ind. Mark. Manag. 2022, 104, 28–37. [Google Scholar] [CrossRef]

- Ghosh, S.; Hughes, M.; Hodgkinson, I.; Hughes, P. Digital transformation of industrial businesses: A dynamic capability approach. Technovation 2022, 113, 102414. [Google Scholar] [CrossRef]

- Lütjen, H.; Schultz, C.; Tietze, F.; Urmetzer, F. Managing ecosystems for service innovation: A dynamic capability view. J. Bus. Res. 2019, 104, 506–519. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef]

- Kroh, J.; Luetjen, H.; Globocnik, D.; Schultz, C. Use and efficacy of information technology in innovation processes: The specific role of servitization. J. Prod. Innov. Manag. 2018, 35, 720–741. [Google Scholar] [CrossRef]

- Sestino, A.; Prete, M.I.; Piper, L.; Guido, G. Internet of Things and Big Data as enablers for business digitalization strategies. Technovation 2020, 98, 102173. [Google Scholar] [CrossRef]

- Livdan, D.; Sapriza, H.; Zhang, L. Financially constrained stock returns. J. Financ. 2009, 64, 1827–1862. [Google Scholar] [CrossRef]

- Lu, Y.; Zhou, L.; Bruton, G.; Li, W. Capabilities as a mediator linking resources and the international performance of entrepreneurial firms in an emerging economy. J. Int. Bus. Stud. 2010, 41, 419–436. [Google Scholar] [CrossRef]

- Atzmon, M.B.; Vanderstraeten, J.; Albers, S. Small-firm growth-enabling capabilities: A framework for young technology-based firms. Technovation 2022, 117, 102542. [Google Scholar] [CrossRef]

- Yang, G.; Nie, Y.; Li, H.; Wang, H. Digital transformation and low-carbon technology innovation in manufacturing firms: The mediating role of dynamic capabilities. Int. J. Prod. Econ. 2023, 263, 108969. [Google Scholar] [CrossRef]

- Barua, A.; Konana, P.; Whinston, A.B.; Yin, F. An empirical investigation of net-enabled business value. MIS Q. 2004, 28, 585–620. [Google Scholar] [CrossRef]

- Cassiman, B.; Golovko, E. Innovation and internationalization through exports. J. Int. Bus. Stud. 2011, 42, 56–75. [Google Scholar] [CrossRef]

- Gopalakrishna-Remani, V.; Byun, K.A.; Doty, D.H. The impact of employees’ perceptions about top management engagement on sustainability development efforts and firm performance. Bus. Strategy Environ. 2022, 31, 2964–2977. [Google Scholar] [CrossRef]

- Jones, C.I.; Tonetti, C. Nonrivalry and the Economics of Data. Am. Econ. Rev. 2020, 110, 2819–2858. [Google Scholar] [CrossRef]

- Lynall, M.D.; Golden, B.R.; Hillman, A.J. Board composition from adolescence to maturity: A multitheoretic view. Acad. Manag. Rev. 2003, 28, 416–431. [Google Scholar] [CrossRef]

- Thietart, R.A.; Vivas, R. An empirical investigation of success strategies for businesses along the product life cycle. Manag. Sci. 1984, 30, 1405–1423. [Google Scholar] [CrossRef]

- Kliestik, T.; Novak Sedlackova, A.; Bugaj, M.; Novak, A. Stability of profits and earnings management in the transport sector of Visegrad countries. Oeconomia Copernic. 2022, 13, 475–509. [Google Scholar] [CrossRef]

- Dickinson, V. Cash flow patterns as a proxy for firm life cycle. Account. Rev. 2011, 86, 1969–1994. [Google Scholar] [CrossRef]

- Park, S.M. The Effects of Personnel Reform Systems on Georgia State Employees’ Attitudes: An empirical analysis from a principal–agent theoretical perspective. Public Manag. Rev. 2010, 12, 403–437. [Google Scholar] [CrossRef]

- Ceipek, R.; Hautz, J.; De Massis, A.; Matzler, K.; Ardito, L. Digital transformation through exploratory and exploitative internet of things innovations: The impact of family management and technological diversification. J. Prod. Innov. Manag. 2021, 38, 142–165. [Google Scholar] [CrossRef]

- Menz, M.; Kunisch, S.; Birkinshaw, J.; Collis, D.J.; Foss, N.J.; Hoskisson, R.E.; Prescott, J.E. Corporate Strategy and the Theory of the Firm in the Digital Age. J. Manag. Stud. 2021, 58, 1695–1720. [Google Scholar] [CrossRef]

- Carnes, C.M.; Chirico, F.; Hitt, M.A.; Huh, D.W.; Pisano, V. Resource orchestration for innovation: Structuring and bundling resources in growth-and maturity-stage firms. Long Range Plan. 2017, 50, 472–486. [Google Scholar] [CrossRef]

- Doha, A.; Das, A.; Pagell, M. The influence of product life cycle on the efficacy of purchasing practices. Int. J. Oper. Prod. Manag. 2013, 33, 470–498. [Google Scholar] [CrossRef]

- Karniouchina, E.V.; Carson, S.J.; Short, J.C.; Ketchen, D.J., Jr. Extending the firm vs. industry debate: Does industry life cycle stage matter? Strateg. Manag. J. 2013, 34, 1010–1018. [Google Scholar] [CrossRef]

- Zhai, H.; Yang, M.; Chan, K.C. Does digital transformation enhance a firm’s performance? Evidence from China. Technol. Soc. 2022, 68, 101841. [Google Scholar] [CrossRef]

- La Rocca, M.; La Rocca, T.; Cariola, A. Capital structure decisions during a firm’s life cycle. Small Bus. Econ. 2011, 37, 107–130. [Google Scholar] [CrossRef]

- Berger, A.N.; EI Ghoul, S.; Guedhami, O.; Roman, R.A. Internationalization and bank risk. Manag. Sci. 2017, 63, 2283–2301. [Google Scholar] [CrossRef]

- Karolyi, S.A. Personal lending relationships. J. Financ. 2018, 73, 5–49. [Google Scholar] [CrossRef]

- Campa, D. Earnings management strategies during financial difficulties: A comparison between listed and unlisted French companies. Res. Int. Bus. Financ. 2019, 50, 457–471. [Google Scholar] [CrossRef]

- Ding, S.; Cui, T.; Bellotti, A.G.; Abedin, M.Z.; Lucey, B. The role of feature importance in predicting corporate financial distress in pre and post COVID periods: Evidence from China. Int. Rev. Financ. Anal. 2023, 90, 102851. [Google Scholar] [CrossRef]

- Lukason, O.; Laitinen, E.K. Firm failure processes and components of failure risk: An analysis of European bankrupt firms. J. Bus. Res. 2019, 98, 380–390. [Google Scholar] [CrossRef]

- Altman, E.I.; Iwanicz-Drozdowska, M.; Laitinen, E.K.; Suvas, A. Financial distress prediction in an international context: A review and empirical analysis of Altman’s Z-score model. J. Int. Financ. Manag. Account. 2017, 28, 131–171. [Google Scholar] [CrossRef]

- Almamy, J.; Aston, J.; Ngwa, L.N. An evaluation of Altman’s Z-score using cash flow ratio to predict corporate failure amid the recent financial crisis: Evidence from the UK. J. Corp. Financ. 2016, 36, 278–285. [Google Scholar] [CrossRef]

- García, C.J.; Herrero, B. Female directors, capital structure, and financial distress. J. Bus. Res. 2021, 136, 592–601. [Google Scholar] [CrossRef]

- Tinoco, M.H.; Wilson, N. Financial distress and bankruptcy prediction among listed companies using accounting, market and macroeconomic variables. Int. Rev. Financ. Anal. 2013, 30, 394–419. [Google Scholar] [CrossRef]

- Ellinger, A.E.; Natarajarathinam, M.; Adams, F.G.; Gray, J.B.; Hofman, D.; O’Marah, K. Supply chain management competency and firm financial success. J. Bus. Logist. 2011, 32, 214–226. [Google Scholar] [CrossRef]

- Grice, J.S.; Ingram, R.W. Tests of the generalizability of Altman’s bankruptcy prediction model. J. Bus. Res. 2001, 54, 53–61. [Google Scholar] [CrossRef]

- Zhong, X.; Ren, G. Independent and joint effects of CSR and CSI on the effectiveness of digital transformation for transition economy firms. J. Bus. Res. 2023, 156, 113478. [Google Scholar] [CrossRef]

- Aizawa, A. An information-theoretic perspective of tf–idf measures. Inf. Process. Manag. 2003, 39, 45–65. [Google Scholar] [CrossRef]

- Akter, S.; Michael, K.; Uddin, M.R.; McCarthy, G.; Rahman, M. Transforming business using digital innovations: The application of AI, blockchain, cloud and data analytics. Ann. Oper. Res. 2022, 308, 7–39. [Google Scholar] [CrossRef]

- Fang, M.; Liu, F.; Park, K. Is inventory performance helping to improve SME credit ratings? The moderating role of supply chain concentration. Appl. Econ. Lett. 2022, 31, 880–884. [Google Scholar] [CrossRef]

- Johnson, M.; Albizri, A.; Harfouche, A.; Fosso-Wamba, S. Integrating human knowledge into artificial intelligence for complex and ill-structured problems: Informed artificial intelligence. Int. J. Inf. Manag. 2022, 64, 102479. [Google Scholar] [CrossRef]

- Lu, Q.; Chesbrough, H. Measuring open innovation practices through topic modelling: Revisiting their impact on firm financial performance. Technovation 2022, 114, 102434. [Google Scholar] [CrossRef]

- Oliveira, M.; Kadapakkam, P.R.; Beyhaghi, M. Effects of customer financial distress on supplier capital structure. J. Corp. Financ. 2017, 42, 131–149. [Google Scholar] [CrossRef]

- Hoy, F. The complicating factor of life cycles in corporate venturing. Entrep. Theory Pract. 2006, 30, 831–836. [Google Scholar] [CrossRef]

- Correia, S. REGHDFE: Stata Module to Perform Linear or Instrumental-Variable Regression Absorbing Any Number of High-Dimensional Fixed Effects. Boston College Department of Economics. 2023. Available online: https://ideas.repec.org/c/boc/bocode/s457874.html (accessed on 20 April 2024).

- Blanc, S.M.; Setzer, T. Analytical debiasing of corporate cash flow forecasts. Eur. J. Oper. Res. 2015, 243, 1004–1015. [Google Scholar] [CrossRef]

- Fresard, L. Financial strength and product market behavior: The real effects of corporate cash holdings. J. Financ. 2010, 65, 1097–1122. [Google Scholar] [CrossRef]

- Geng, R.; Bose, I.; Chen, X. Prediction of financial distress: An empirical study of listed Chinese companies using data mining. Eur. J. Oper. Res. 2015, 1, 236–247. [Google Scholar] [CrossRef]

- Broccardo, L.; Tenucci, A.; Agarwal, R.; Alshibani, S.M. Steering digitalization and management control maturity in small and medium enterprises (SMEs). Technol. Forecast. Soc. Change 2024, 204, 123446. [Google Scholar] [CrossRef]

- Chouaibi, S.; Festa, G.; Quaglia, R.; Rossi, M. The risky impact of digital transformation on organizational performance–evidence from Tunisia. Technol. Forecast. Soc. Change 2022, 178, 121571. [Google Scholar] [CrossRef]

- ElBannan, M.A. On the prediction of financial distress in emerging markets: What matters more? Empirical evidence from Arab spring countries. Emerg. Mark. Rev. 2021, 47, 100806. [Google Scholar] [CrossRef]

- Gökalp, E.; Martinez, V. Digital transformation capability maturity model enabling the assessment of industrial manufacturers. Comput. Ind. 2021, 132, 103522. [Google Scholar] [CrossRef]

- Pindado, J.; Rodrigues, L.; De la Torre, C. Estimating financial distress likelihood. J. Bus. Res. 2008, 61, 995–1003. [Google Scholar] [CrossRef]

- Dang, V.A.; Gao, N.; Yu, T. Climate policy risk and corporate financial decisions: Evidence from the NOx budget trading program. Manag. Sci. 2023, 69, 7517–7539. [Google Scholar] [CrossRef]

- Gupta, N.; Sardana, D.; Lee, R. Dynamic capabilities that matter for business failure versus survival. Ind. Mark. Manag. 2024, 116, 40–50. [Google Scholar] [CrossRef]

- Bresciani, S.; Huarng, K.H.; Malhotra, A.; Ferraris, A. Digital transformation as a springboard for product, process and business model innovation. J. Bus. Res. 2021, 128, 204–210. [Google Scholar] [CrossRef]

- Fernandez-Vidal, J.; Perotti, F.A.; Gonzalez, R.; Gasco, J. Managing digital transformation: The view from the top. J. Bus. Res. 2022, 152, 29–41. [Google Scholar] [CrossRef]

- Kretschmer, T.; Khashabi, P. Digital transformation and organization design: An integrated approach. Calif. Manag. Rev. 2020, 62, 86–104. [Google Scholar] [CrossRef]

- Dal Mas, F.; Massaro, M.; Ndou, V.; Raguseo, E. Blockchain technologies for sustainability in the agrifood sector: A literature review of academic research and business perspectives. Technol. Forecast. Soc. Change 2023, 187, 122155. [Google Scholar] [CrossRef]

- .Queiroz, M.M.; Wamba, S.F. Blockchain adoption challenges in supply chain: An empirical investigation of the main drivers in India and the USA. Int. J. Inf. Manag. 2019, 46, 70–82. [Google Scholar] [CrossRef]

- Ribeiro-Navarrete, B.; Calderon-Monge, E.; Simón-Moya, V. Digitalisation and digital transformation in the social economy: The cases of Anecoop and Consum. Br. Food J. 2023, 125, 3489–3505. [Google Scholar] [CrossRef]

- Alqahtani, J.; Duong, L.; Taylor, G.; Eulaiwi, B. Outside directors, firm life cycle, corporate financial decisions and firm performance. Emerg. Mark. Rev. 2022, 50, 100820. [Google Scholar] [CrossRef]

- Arikan, A.M.; Stulz, R.M. Corporate acquisitions, diversification, and the firm’s life cycle. J. Financ. 2016, 71, 139–194. [Google Scholar] [CrossRef]

- Nauhaus, S.; Luger, J.; Raisch, S. Strategic decision making in the digital age: Expert sentiment and corporate capital allocation. J. Manag. Stud. 2021, 58, 1933–1961. [Google Scholar] [CrossRef]

- Vittori, D.; Natalicchio, A.; Panniello, U.; Petruzzelli, A.M.; Cupertino, F. Business Model Innovation between the embryonic and growth stages of industry lifecycle. Technovation 2022, 117, 102592. [Google Scholar] [CrossRef]

- Liu, F.; Dutta, D.K.; Park, K. From external knowledge to competitive advantage: Absorptive capacity, firm performance, and the mediating role of labour productivity. Technol. Anal. Strateg. Manag. 2021, 33, 18–30. [Google Scholar] [CrossRef]

- Chanias, S.; Myers, M.D.; Hess, T. Digital transformation strategy making in pre-digital organizations: The case of a financial services provider. J. Strateg. Inf. Syst. 2019, 28, 17–33. [Google Scholar] [CrossRef]

- Chen, M.Y. Predicting corporate financial distress based on integration of decision tree classification and logistic regression. Expert Syst. Appl. 2011, 38, 11261–11272. [Google Scholar] [CrossRef]

- Chen, Y.J.; Chen, Y.M. Forecasting corporate credit ratings using big data from social media. Expert Syst. Appl. 2022, 207, 118042. [Google Scholar] [CrossRef]

- Huang, Y.; Wang, Z.; Jiang, C. Diagnosis with incomplete multi-view data: A variational deep financial distress prediction method. Technol. Forecast. Soc. Change 2024, 201, 123269. [Google Scholar] [CrossRef]

- Zhang, Z.; Wu, C.; Qu, S.; Chen, X. An explainable artificial intelligence approach for financial distress prediction. Inf. Process. Manag. 2022, 59, 102988. [Google Scholar] [CrossRef]

{kind=link}

| Dimension | Category | Keywords |

|---|---|---|

| Strategy | Digital Transformation Strategy | Business digitalization; Digital age; Digital capability; Digital change; Digital management; Digital technology; Digitalization strategy; DT; Industrial digitalization; Information digitalization |

| Technology | Artificial Intelligence | Artificial intelligence; Business intelligence; Deep learning; Face recognition; Image understanding; Intelligent data analysis; Machine learning; Natural language processing; Robotic process automation; Semantic search; Smart robot; Speech recognition |

| Blockchain | Alliance chain; Blockchain; Differential Privacy; Digital currency; Distributed computing; Interconnected chain; Test chain | |

| Cloud Computing | Brain-like computing; Cloud computing; Cognitive computing; Cyber-physical systems; Fusion architecture; Graph computing; Green computing; In-memory computing; Multi-party secure computing; Stream computing | |

| Big Data | Bata mining; Big data; Data center; Data visualization; Hadoop; Multi-source heterogeneous data; Text mining | |

| Application | Digital Transformation Application | Digital marketing; Digital platform; Industrial internet; Industry 4.0; Intelligent manufacturing; Internet of things; Smart factory |

| Category | Variable | Definition |

|---|---|---|

| Dependent Variable | Financial distress | Equals one if the Z-score of a company is less than 1.81, and zero if the Z-score of a company is more than 2.67 |

| Independent Variable | Digital transformation | Use keywords about digital transformation in the annual reports published by the companies and analyses the degree of word specificity and its word frequency based on the TF-IDF method |

| Moderator Variable | Growth stage | Equals one if a firm’s investment cash flows are negative and financing cash flows are positive and zero otherwise |

| Maturity stage | Equals one if a firm’s operating cash flows are positive, investing cash flows are negative, negative financing cash flows, and zero otherwise | |

| Declining stage | Equals one (1) if a firm is not in the growth or maturity stage | |

| Control Variable | Size | The natural logarithm of the firm’s total assets. |

| Age | The number of years since a firm was established. | |

| Leverage | Total liabilities/total assets | |

| Profitability | Net profit/total assets | |

| Current | Current assets/current liabilities | |

| Cash | (Monetary funds + trading financial assets)/current liabilities | |

| Quick | (Current assets-net inventory)/current liabilities | |

| Concentration | The percentage of ownership held by the largest shareholder |

| Variables | Mean | S.D. | Min | Max |

|---|---|---|---|---|

| Financial Distress | 0.1813 | 0.3853 | 0 | 1 |

| Digital Transformation | 1.5584 | 3.3156 | 0 | 18.6 |

| Growth stage | 0.4702 | 0.4991 | 0 | 1 |

| Maturity stage | 0.3508 | 0.4772 | 0 | 1 |

| Declining stage | 0.1791 | 0.3834 | 0 | 1 |

| Size | 7.5827 | 1.1236 | 5.1591 | 10.6879 |

| Age | 17.5052 | 5.5832 | 7 | 35 |

| Leverage | 0.3716 | 0.2035 | 0.0491 | 0.9444 |

| Profitability | 0.0670 | 0.0741 | −0.2254 | 0.2779 |

| Current | 3.0272 | 3.0878 | 0.3894 | 18.4989 |

| Cash | 1.2972 | 2.0430 | 0.0427 | 12.5255 |

| Quick | 2.4534 | 2.8218 | 0.2175 | 17.0209 |

| Concentration | 0.3407 | 0.1422 | 0.0908 | 0.7341 |

| Variables | Financial Distress | Digital Transformation | Growth Stage | Maturity Stage | Declining Stage | Size | Age |

|---|---|---|---|---|---|---|---|

| Financial Distress | 1 | ||||||

| Digital Transformation | −0.0210 * | 1 | |||||

| Growth stage | 0.0253 * | 0.0271 * | 1 | ||||

| Maturity stage | −0.0581 * | −0.0458 * | −0.6924 * | 1 | |||

| Declining stage | 0.0393 * | 0.0217 * | −0.4399 * | −0.3433 * | 1 | ||

| Size | 0.3124 * | 0.0183 * | 0.0052 | 0.0899 * | −0.1186 * | 1 | |

| Age | 0.1257 * | 0.0459 * | −0.1450 * | 0.0657 * | 0.1070 * | 0.1248 * | 1 |

| Leverage | 0.6792 * | 0.0030 | 0.0989 * | −0.0999 * | −0.0044 | 0.4302 * | 0.1461 * |

| Profitability | −0.3967 * | −0.045 * | 0.0296 * | 0.1017 * | −0.1652 * | 0.0393 * | −0.1039 * |

| Current | −0.3094 * | −0.0259 * | −0.0566 * | 0.0352 * | 0.0299 * | −0.3954 * | −0.1457 * |

| Cash | −0.2348 * | −0.0265 * | −0.0275 * | 0.0179 * | 0.0135 | −0.3286 * | −0.1412 * |

| Quick | −0.2899 * | −0.0164 * | −0.0477 * | 0.0304 * | 0.0244 * | −0.3912 * | −0.1479 * |

| Concentration | −0.0363 * | −0.0567 * | −0.0186 * | 0.0641 * | −0.0556 * | 0.1423 * | −0.1339 * |

| Variables | Leverage | Profitability | Current | Cash | Quick | Concentration | |

| Financial Distress | |||||||

| Digital Transformation | |||||||

| Growth stage | |||||||

| Maturity stage | |||||||

| Declining stage | |||||||

| Size | |||||||

| Age | |||||||

| Leverage | 1 | ||||||

| Profitability | −0.3458 * | 1 | |||||

| Current | −0.6537 * | 0.2071 * | 1 | ||||

| Cash | −0.5434 * | 0.1836 * | 0.8989 * | 1 | |||

| Quick | −0.6308 * | 0.2071 * | 0.9883 * | 0.9148 * | 1 | ||

| Concentration | −0.0285 * | 0.1631 * | 0.0281 * | 0.0343 * | 0.0232 * | 1 |

| Variables | Financial Distress | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Digital Transformation | −0.0378 *** | −0.0384 *** | −0.0080 | −0.0393 *** | −0.0382 *** | −0.0379 *** | −0.0543 *** | |

| (0.013) | (0.013) | (0.019) | (0.013) | (0.014) | (0.013) | (0.015) | ||

| Growth stage | 0.1471 * | 0.2320 *** | ||||||

| (0.080) | (0.088) | |||||||

| Digital Transformation × Growth stage | −0.0529 ** | |||||||

| (0.023) | ||||||||

| Maturity stage | −0.3524 *** | −0.3445 *** | ||||||

| (0.087) | (0.096) | |||||||

| Digital Transformation × Maturity stage | −0.0054 | |||||||

| (0.027) | ||||||||

| Declining stage | 0.2701 ** | 0.1297 | ||||||

| (0.106) | (0.117) | |||||||

| Digital Transformation × Declining stage | 0.0815 *** | |||||||

| (0.029) | ||||||||

| Control Variable | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | −12.4464 *** | −12.5989 *** | −12.6953 *** | −12.7336 *** | −12.6094 *** | −12.6139 *** | −12.6993 *** | −12.6880 *** |

| (0.552) | (0.556) | (0.559) | (0.559) | (0.557) | (0.558) | (0.558) | (0.558) | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 |

| R2 | 0.710 | 0.711 | 0.711 | 0.711 | 0.712 | 0.712 | 0.711 | 0.712 |

| Variables | Financial Distress | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Digital Transformation Strategy | −0.2567 *** | −0.2580 *** | −0.1973 ** | −0.2600 *** | −0.2438 *** | −0.2570 *** | −0.2760 *** | |

| (0.090) | (0.090) | (0.093) | (0.090) | (0.092) | (0.091) | (0.092) | ||

| Growth stage | 0.1439 * | 0.2319 *** | ||||||

| (0.080) | (0.085) | |||||||

| Digital Transformation Strategy × Growth stage | −0.0521 *** | |||||||

| (0.017) | ||||||||

| Maturity stage | −0.3488 *** | −0.3178 *** | ||||||

| (0.087) | (0.095) | |||||||

| Digital Transformation Strategy × Maturity stage | −0.0209 | |||||||

| (0.025) | ||||||||

| Declining stage | 0.2709 ** | 0.1892 | ||||||

| (0.106) | (0.116) | |||||||

| Digital Transformation Strategy × Declining stage | 0.0463 * | |||||||

| (0.026) | ||||||||

| Control Variable | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | −12.4464 *** | −12.5670 *** | −12.6595 *** | −12.7906 *** | −12.5727 *** | −12.6010 *** | −12.6675 *** | −12.6309 *** |

| (0.552) | (0.555) | (0.558) | (0.560) | (0.556) | (0.557) | (0.557) | (0.557) | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 |

| R2 | 0.710 | 0.711 | 0.711 | 0.711 | 0.712 | 0.712 | 0.711 | 0.711 |

| Variables | Financial Distress | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Digital Transformation Application | −0.0305 | −0.0318 | 0.0196 | −0.0329 | −0.0266 | −0.0300 | −0.0425 ** | |

| (0.020) | (0.020) | (0.025) | (0.020) | (0.021) | (0.020) | (0.022) | ||

| Growth stage | 0.1452 * | 0.2562 *** | ||||||

| (0.080) | (0.086) | |||||||

| Digital Transformation Application × Growth stage | −0.0691 *** | |||||||

| (0.020) | ||||||||

| Maturity stage | −0.3494 *** | −0.3118 *** | ||||||

| (0.087) | (0.095) | |||||||

| Digital Transformation Application × Maturity stage | −0.0251 | |||||||

| (0.026) | ||||||||

| Declining stage | 0.2689 ** | 0.1744 | ||||||

| (0.106) | (0.117) | |||||||

| Digital Transformation Application × Declining stage | 0.0534 ** | |||||||

| (0.027) | ||||||||

| Control Variable | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | −12.4464 *** | −12.5191 *** | −12.6137 *** | −12.7043 *** | −12.5259 *** | −12.5531 *** | −12.6172 *** | −12.5912 *** |

| (0.552) | (0.555) | (0.558) | (0.559) | (0.556) | (0.557) | (0.557) | (0.557) | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 |

| R2 | 0.710 | 0.710 | 0.710 | 0.711 | 0.711 | 0.711 | 0.711 | 0.711 |

| Variables | Financial Distress | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| AI | −0.2430 *** | −0.2433 *** | −0.1945 *** | −0.2447 *** | −0.2393 *** | −0.2436 *** | −0.2727 *** | |

| (0.056) | (0.056) | (0.061) | (0.056) | (0.057) | (0.056) | (0.058) | ||

| Growth stage | 0.1419 * | 0.2004 ** | ||||||

| (0.080) | (0.085) | |||||||

| AI × Growth stage | −0.0350 * | |||||||

| (0.018) | ||||||||

| Maturity stage | −0.3484 *** | −0.3315 *** | ||||||

| (0.087) | (0.095) | |||||||

| AI × Maturity stage | −0.0117 | |||||||

| (0.026) | ||||||||

| Declining stage | 0.2736 ** | 0.1581 | ||||||

| (0.106) | (0.116) | |||||||

| AI × Declining stage | 0.0688 ** | |||||||

| (0.027) | ||||||||

| Control Variable | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | −12.4464 *** | −12.6486 *** | −12.7390 *** | −12.8034 *** | −12.6550 *** | −12.6707 *** | −12.7523 *** | −12.7204 *** |

| (0.552) | (0.555) | (0.558) | (0.560) | (0.557) | (0.558) | (0.558) | (0.558) | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 |

| R2 | 0.710 | 0.711 | 0.712 | 0.712 | 0.712 | 0.712 | 0.712 | 0.712 |

| Variables | Financial Distress | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Blockchain | 0.1559 | 0.1642 | 0.2925 | 0.1680 | 0.2135 | 0.1486 | 0.1072 | |

| (0.228) | (0.228) | (0.231) | (0.227) | (0.228) | (0.227) | (0.228) | ||

| Growth stage | 0.1419 * | 0.2503 *** | ||||||

| (0.080) | (0.085) | |||||||

| Blockchain × Growth stage | −0.0628 *** | |||||||

| (0.017) | ||||||||

| Maturity stage | −0.3463 *** | −0.2907 *** | ||||||

| (0.087) | (0.094) | |||||||

| Blockchain × Maturity stage | −0.0380 | |||||||

| (0.025) | ||||||||

| Declining stage | 0.2700 ** | 0.2071 * | ||||||

| (0.106) | (0.116) | |||||||

| Blockchain × Declining stage | 0.0359 | |||||||

| (0.026) | ||||||||

| Control Variable | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | −12.4464 *** | −12.4527 *** | −12.5420 *** | −12.7444 *** | −12.4540 *** | −12.5193 *** | −12.5532 *** | −12.5161 *** |

| (0.552) | (0.552) | (0.555) | (0.559) | (0.554) | (0.556) | (0.555) | (0.555) | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 |

| R2 | 0.710 | 0.710 | 0.710 | 0.711 | 0.711 | 0.711 | 0.711 | 0.711 |

| Variables | Financial Distress | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Cloud Computing | −0.1120 | −0.1139 | 0.0170 | −0.1177 | −0.0997 | −0.1128 | −0.1390 * | |

| (0.079) | (0.079) | (0.088) | (0.079) | (0.081) | (0.079) | (0.081) | ||

| Growth stage | 0.1424 * | 0.2454 *** | ||||||

| (0.080) | (0.085) | |||||||

| Cloud Computing × Growth stage | −0.0615 *** | |||||||

| (0.018) | ||||||||

| Maturity stage | −0.3476 *** | −0.3051 *** | ||||||

| (0.087) | (0.095) | |||||||

| Cloud Computing × Maturity stage | −0.0289 | |||||||

| (0.026) | ||||||||

| Declining stage | 0.2713 ** | 0.1908 * | ||||||

| (0.106) | (0.116) | |||||||

| Cloud Computing × Declining stage | 0.0462 * | |||||||

| (0.026) | ||||||||

| Control Variable | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | −12.4464 *** | −12.4781 *** | −12.5685 *** | −12.7231 *** | −12.4829 *** | −12.5265 *** | −12.5802 *** | −12.5444 *** |

| (0.552) | (0.553) | (0.556) | (0.559) | (0.554) | (0.556) | (0.556) | (0.556) | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 |

| R2 | 0.710 | 0.710 | 0.710 | 0.711 | 0.711 | 0.711 | 0.711 | 0.711 |

| Variables | Financial Distress | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Big data | −0.0595 * | −0.0599 * | −0.0049 | −0.0610 * | −0.0529 | −0.0600 * | −0.0777 ** | |

| (0.033) | (0.033) | (0.036) | (0.033) | (0.034) | (0.033) | (0.034) | ||

| Growth stage | 0.1417 * | 0.2410 *** | ||||||

| (0.080) | (0.086) | |||||||

| Big data × Growth stage | −0.0588 *** | |||||||

| (0.019) | ||||||||

| Maturity stage | −0.3471 *** | −0.3113 *** | ||||||

| (0.087) | (0.095) | |||||||

| Big data × Maturity stage | −0.0246 | |||||||

| (0.026) | ||||||||

| Declining stage | 0.2719 ** | 0.1775 | ||||||

| (0.106) | (0.116) | |||||||

| Big data × Declining stage | 0.0551 ** | |||||||

| (0.027) | ||||||||

| Control Variable | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | −12.4464 *** | −12.4791 *** | −12.5683 *** | −12.7220 *** | −12.4830 *** | −12.5199 *** | −12.5821 *** | −12.5429 *** |

| (0.552) | (0.553) | (0.556) | (0.559) | (0.554) | (0.556) | (0.556) | (0.556) | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 | 16,589 |

| R2 | 0.710 | 0.710 | 0.711 | 0.711 | 0.711 | 0.711 | 0.711 | 0.711 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, J.; Yu, Y.; Wei, Z.; Shen, J.; Zhang, Z.; Sun, Z. Mitigating Financial Distress by Engaging in Digital Transformation: The Moderating Role of Life Cycles. Systems 2024, 12, 513. https://doi.org/10.3390/systems12120513

Zhang J, Yu Y, Wei Z, Shen J, Zhang Z, Sun Z. Mitigating Financial Distress by Engaging in Digital Transformation: The Moderating Role of Life Cycles. Systems. 2024; 12(12):513. https://doi.org/10.3390/systems12120513

Chicago/Turabian StyleZhang, Jianbo, Yaoyi Yu, Zhuoqiong Wei, Jie Shen, Zhiping Zhang, and Zichun Sun. 2024. "Mitigating Financial Distress by Engaging in Digital Transformation: The Moderating Role of Life Cycles" Systems 12, no. 12: 513. https://doi.org/10.3390/systems12120513

APA StyleZhang, J., Yu, Y., Wei, Z., Shen, J., Zhang, Z., & Sun, Z. (2024). Mitigating Financial Distress by Engaging in Digital Transformation: The Moderating Role of Life Cycles. Systems, 12(12), 513. https://doi.org/10.3390/systems12120513