A Study of the Impact of Executive Corruption on Corporate Innovation

Abstract

1. Introduction

2. Materials and Methods

2.1. Literature Review

2.1.1. Influencing Factors of Enterprise Innovation

2.1.2. The Economic Consequences of Executive Corruption

2.1.3. Correlation between Corporate Innovation and Financial Misconduct

2.2. Theory Analysis and Research Hypotheses

2.3. Research Design

2.3.1. Sample Selection and Data Source

2.3.2. Variable Definitions

- Enterprise Innovation

- Executive Corruption

- Financing Constraints

- Internal Control (IC)

- Educational Background of Executives (EDU)

- Nature of the Enterprise (SOE)

- Political Connection (PC)

- Audit Quality (AUDIT)

- Institutional Investor Ownership (INSP)

- Other control variables

2.3.3. Model Design

3. Results

3.1. Descriptive Statistics

3.2. Main Regression Results

3.3. Mediation Effect Test for Financing Constraints

3.4. Analysis of the Moderating Mechanism of Changes in Internal and External Environments

3.5. Endogeneity Test and Robustness Test

3.5.1. Endogeneity Test

- Instrumental Variable Method

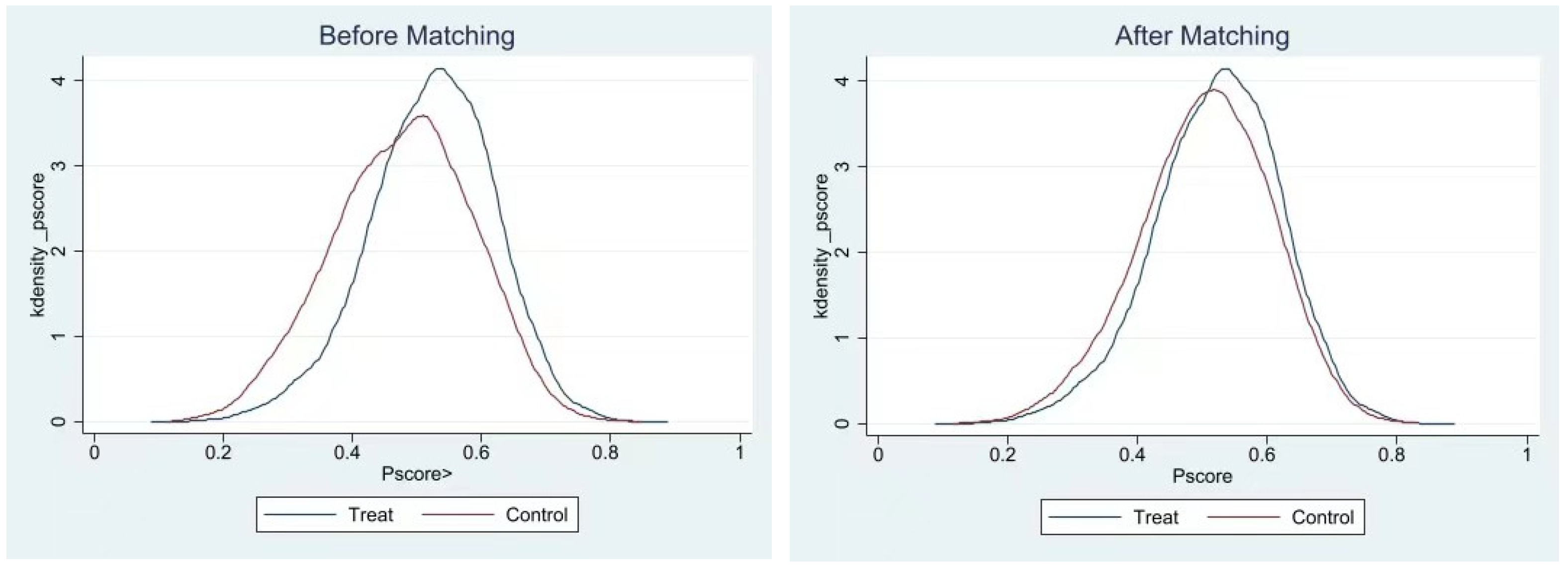

- Propensity Score Matching Analysis (PSM)

3.5.2. Robustness Test

- Variable Replacement

- Regression Method Replacement

4. Discussion

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Rodriguez, P.; Siegel, D.S.; Hillman, A.; Eden, L. Three Lenses on the Multinational Enterprise: Politics, Corruption and Corporate Social Responsibility. J. Int. Bus. Stud. 2006, 37, 733–746. [Google Scholar] [CrossRef]

- Luo, Y. An Organizational Perspective of Corruption. Manag. Organ. Rev. 2004, 1, 119–154. [Google Scholar] [CrossRef]

- Anokhin, S.; Schulze, W. Entrepreneurship, Innovation and Corruption. J. Bus. Ventur. 2009, 24, 465–476. [Google Scholar] [CrossRef]

- He, J.; Tian, X. Finance and corporate innovation: A survey. Asia Pac. J. Financ. Stud. 2018, 47, 165–212. [Google Scholar] [CrossRef]

- Hu, M.; Gan, S. Management power, internal control and executive corruption. J. Zhongnan Univ. Econ. Law 2015, 3, 87–93. [Google Scholar]

- Aidt, T.S.; Dutta, J. Policy Compromises: Corruption and Regulation in A Democracy. Econ. Politics 2008, 20, 335–360. [Google Scholar] [CrossRef]

- Claessens, S.; Laeven, L. Financial Development, Property Rights and Growth. J. Financ. 2003, 58, 24–36. [Google Scholar] [CrossRef]

- Li, H.; Zhang, J. Corruption and corporate innovation: Lubricant or stumbling block. Nankai Econ. Res. 2015, 24–58. [Google Scholar]

- Yang, Q. Enterprise growth: Political affiliation or capacity building? Econ. Res. 2011, 10, 54–66. [Google Scholar]

- Zhou, Y.; Zhao, X. Research on Local Government Competition Patterns—Theoretical and Policy Analysis of Constructing a Benign Competition Order among Local Governments. Manag. World 2002, 12, 52–61. [Google Scholar]

- Chen, D.; Li, O.Z.; Liang, S. Do Managers Perform for Perks; Working Paper; Social Science Electronic Publishing: Rochester, NY, USA, 2009. [Google Scholar]

- Zhou, L. Incentives and cooperation of government officials in the promotion game—Another discussion on the reasons for the persistence of local protectionism and duplicated construction problems in China. Econ. Res. 2004, 6, 33–40. [Google Scholar]

- Xu, X.; Liu, X. Decentralization Reform, Compensation Control and Corporate Executive Corruption. Manag. World 2013, 3, 119–132. [Google Scholar]

- Li, W.; Li, H.; Li, H. Innovation Incentive or Tax Shield?—Research on tax incentives for high-tech enterprises. Res. Manag. 2016, 37, 61–70. [Google Scholar]

- Lv, J.; Yu, D. Government Research and Innovation Subsidies and Enterprise R&D Investment: Extrusion, Substitution or Incentive? China Sci. Technol. Forum 2011, 8, 21–28. [Google Scholar]

- Wu, C.; Tang, G. Intellectual property protection enforcement strength, technological innovation and firm performance—Evidence from Chinese listed companies. Econ. Res. 2016, 51, 125–139. [Google Scholar]

- Li, H.; Zhang, Z. Financial development, intellectual property protection and technological innovation efficiency—The role of financial marketization. Res. Manag. 2014, 35, 160–167. [Google Scholar]

- Williams, H.L. Intellectual Property Rights and Innovation: Evidence from the Human Genome. J. Political Econ. 2010, 121, 1–27. [Google Scholar] [CrossRef] [PubMed]

- Li, M.; Xiao, H.; Zhao, S. A study on the relationship between financial development, technological innovation and economic growth—Based on provincial and municipal panel data in China. China Manag. Sci. 2015, 23, 162–169. [Google Scholar]

- Wang, P.; Wang, K. Digital Finance and Corporate Innovation Output—Moderating Effects Based on Reverse Mixing of Privately Listed Companies. Financ. Account. Mon. 2022, 8. [Google Scholar]

- Jia, J.; Lun, X.; Lin, S. Financial Development, Microenterprise Innovation Output and Economic Growth—An Empirical Analysis Based on the Patent Perspective of Listed Companies. Financ. Res. 2017, 1, 99–113. [Google Scholar]

- He, Y.; Lin, H.; Wang, M. Product market competition, executive incentives and corporate innovation—Empirical evidence based on Chinese listed companies. Financ. Trade Econ. 2015, 2, 125–135. [Google Scholar]

- Thakor, R.T.; Lo, A.W. Competition and R&D Financing Decisions: Evidence from the Biopharmaceutical Industry; Social Science Electronic Publishing: Rochester, NY, USA, 2015. [Google Scholar]

- Ren, H. An empirical study on the relationship between equity structure and corporate R&D investment—A data analysis based on A-share manufacturing listed companies. China Soft Sci. 2010, 5, 126–135. [Google Scholar]

- Yang, J.; Sheng, L. An empirical study on the impact of equity structure on corporate investment in technological innovation. Sci. Res. 2007, 4, 787–792. [Google Scholar]

- Linton, J.D. De–babelizing the language of innovation. Technovation 2009, 29, 729–737. [Google Scholar] [CrossRef]

- Ye, Z.; Zhao, Y. Independent directors, institutional environment and R&D investment. J. Manag. 2017, 14, 1033–1040. [Google Scholar]

- Shen, Y.; Wang, F.; Huang, J.; Ji, R. Do innate characteristics of executives play a role in the IPO market? Manag. World 2017, 9, 141–154. [Google Scholar]

- Yi, J.; Zhang, X.; Wang, H. Firm Heterogeneity, Executive Overconfidence and Firm Innovation Performance. Nankai Manag. Rev. 2015, 18, 101–112. [Google Scholar]

- Galasso, A.; Simcoe, T.S. CEO Overconfidence and Innovation. Manag. Sci. 2011, 57, 1469–1484. [Google Scholar] [CrossRef]

- Yu, S.; Wang, T. A study on the correlation between executives’ professional and technical backgrounds and corporate R&D investment. Econ. Manag. Res. 2014, 5, 14–22. [Google Scholar]

- Manso, G. Motivating Innovation. J. Financ. 2011, 66, 1823–1860. [Google Scholar] [CrossRef]

- Kong, D.; Xu, M.; Kong, G. Internal pay gap and innovation in enterprises. Econ. Res. 2017, 52, 144–157. [Google Scholar]

- Chen, X.; Chen, D.; Wan, H.; Liang, S. Regional differences, compensation control and executive corruption. Manag. World 2009, 11, 130–143. [Google Scholar]

- Wan, L.; Chen, F.; Rao, J. Regional corruption and corporate investment efficiency—An empirical study based on listed companies in China. Financ. Res. 2015, 5, 57–62. [Google Scholar]

- Lin, Y.; Liu, X.; Zhu, J. The impact of anti-corruption on investment efficiency: Based on the perspective of sustainable development. East China Econ. Manag. 2019, 33, 111–123. [Google Scholar]

- Wang, Y. Analysis of executive corruption in state-owned enterprise listed companies and coping strategies. Mod. Bus. Ind. 2011, 23, 133–135. [Google Scholar]

- Pearce, C.L.; Manz, C.C.; Sims, H.P. The roles of vertical and shared leadership in the enactment of executive corruption: Implications for research and practice. Leadersh. Q. 2008, 19, 353–359. [Google Scholar] [CrossRef]

- Mukherjee, A.; Singh, M.; Žaldokas, A. Do corporate taxes hinder innovation? J. Financ. Econ. 2017, 124, 195–221. [Google Scholar] [CrossRef]

- Bange, M.M.; De Bondt, W.F. R&D budgets and corporate earnings targets. J. Corp. Financ. 1998, 4, 153–184. [Google Scholar]

- Kwon, S.S.; Yin, Q.J. Executive compensation, investment opportunities, and earnings management: High-tech firms versus low-tech firms. J. Account. Audit. Financ. 2006, 21, 119–148. [Google Scholar] [CrossRef]

- Shust, E. Does research and development activity increase accrual-based earnings management? J. Account. Audit. Financ. 2015, 30, 373–401. [Google Scholar] [CrossRef]

- Murphy, K.; Shleifer, A.; Vishny, R. Why Is Rent–seeking So Costly to Growth? Am. Econ. Rev. 1993, 83, 409–414. [Google Scholar]

- Shleifer, A.; Vishny, R.W. Corruption. Q. J. Econ. 1993, 108, 599–617. [Google Scholar] [CrossRef]

- Guriev, S. Red Tape and Corruption. J. Dev. Econ. 2004, 73, 489–504. [Google Scholar] [CrossRef]

- Baumol, W. Entrepreneurship: Productive, Unproductive and Destructive. J. Political Econ. 1990, 98, 893–921. [Google Scholar] [CrossRef]

- Lian, Y.; Su, J. Financing constraints, uncertainty and investment efficiency of listed companies. Manag. Rev. 2009, 21, 19–26. [Google Scholar]

- Chen, P.; Yang, M. Research on the impact of financing constraints on R&D investment of small and medium-sized science and technology enterprises. Financ. Account. Newsl. 2018, 26, 57–61. [Google Scholar]

- Wang, Y.; Dai, W. Does internal control inhibit or promote corporate innovation?—The logic of China. Audit. Econ. Res. 2019, 34, 19–32. [Google Scholar]

- Zhang, G.; Zhao, J.; Tian, W. Internal control quality and firm performance: A perspective based on internal agency and signaling theory. World Econ. 2015, 1, 126–153. [Google Scholar]

- Yang, G.; Zhu, Y. Pay control, intra-firm pay gap and innovation: Evidence from the manufacturing industry. J. Econ. 2020, 7, 122–155. [Google Scholar]

- Boubakri, N.; Cosset, J.; Saffar, W. Political Connections of Newly Privatized Firms. J. Corp. Financ. 2008, 14, 654–673. [Google Scholar] [CrossRef]

- Zhao, L.; Sun, T.; Chen, S. Does Political Affiliation Ease the Debt Financing Constraints of Small and Medium-sized Enterprises?—Another discussion on the information value-added role of social auditing. Financ. Account. Newsl. 2019, 30, 125–128. [Google Scholar]

- Song, J.; Zhao, R.; Guo, T. Research on government subsidies, political affiliation and value of private listed companies based on mediation effect model. Soft Sci. 2020, 34, 82–87. [Google Scholar]

- Zhuang, Z. Innovation, entrepreneurial activity allocation and long-term economic growth. Econ. Res. 2007, 8, 82–94. [Google Scholar]

- Quan, X.; Wu, S.; Wen, F. Management power, private earnings and pay manipulation. Econ. Res. 2010, 45, 73–87. [Google Scholar]

- Shi, Q.; Sun, M.; Xie, X. Disclosure of critical audit matters and corporate innovation quality: A perspective on financing constraints under information asymmetry. Account. Econ. Res. 2022, 36, 19–40. [Google Scholar]

- Fisman, R.; Wang, Y. The Mortality Cost of Political Connections; Nber Chinese Economy Working Group: Cambridge, MA, USA, 2013. [Google Scholar]

- Jiang, X. Government decentralization and innovation of state-owned enterprises—A study based on the perspective of pyramid structure of local state-owned enterprises. Manag. World 2016, 9, 120–135. [Google Scholar]

- Quan, X.; Yin, H. Chinese short-selling mechanism and corporate innovation—A natural experiment based on the stepwise expansion of financing and securities. Manag. World 2017, 1, 128–144. [Google Scholar]

- Xu, Y.; Liu, Y.; Cai, G. Executive compensation stickiness and corporate innovation. Account. Res. 2018, 7, 43–49. [Google Scholar]

- Zhou, X.; Cheng, L.; Wang, H. Is the higher the level of technological innovation the better the financial performance of enterprises?—An empirical study based on 16 years of patent application data of Chinese pharmaceutical listed companies. Financ. Res. 2012, 8, 166–179. [Google Scholar]

- Xu, X.; Tang, Q. The effects of RD activities and innovation patents on firm value—A study from Chinese listed companies. Res. Dev. Manag. 2010, 22, 20–29. [Google Scholar]

- Huang, Q. New features of management corruption and new stage of state-owned enterprise reform. China Ind. Econ. 2006, 11, 52–59. [Google Scholar]

- Bai, Z.; Chen, Y.; Wang, L.; Yu, H. Research on the performance of state-owned listed companies and the implicit corruption of executives—Based on the perspective of behavioral economics. Res. Manag. 2018, 2, 100–107. [Google Scholar]

- Zhao, C.; Yang, D.; Cao, W. Administrative power, control power and executive corruption in state-owned enterprises. Financ. Res. 2015, 41, 78–89. [Google Scholar]

- Cai, H.; Fang, H.; Xu, L.C. Eat, Drink, Firms and Government: An Investigation of Corruption from the Entertainment and Travel Costs of Chinese Firms. J. Law Econ. 2011, 54, 55–78. [Google Scholar] [CrossRef]

- Huang, J.; Li, K. Eating and drinking, corruption and corporate orders. Econ. Res. 2013, 48, 71–84. [Google Scholar]

- Yang, Q. Political affiliation and corporate growth. Teach. Res. 2010, 6, 38–43. [Google Scholar]

- Jia, M.; Zhang, Z. Does political affiliation of executives affect corporate philanthropic behavior? Manag. World 2010, 4. [Google Scholar]

- Wen, Z.; Hou, J.; Zhang, L. Comparison and application of moderating and mediating effects. J. Psychol. 2005, 2, 268–274. [Google Scholar]

{kind=link}

| Variable Name | Abridgement | Definition |

|---|---|---|

| Enterprise size | SIZE | Natural logarithm of total assets of the enterprise at the end of the year |

| Years of establishment of the enterprise | AGE | Natural logarithm of the number of years the business has been established |

| Enterprise performance | ROA | Return on assets, i.e., the ratio of net profit for the year to total assets at the end of the year |

| Growth | GROW | Year-on-year growth rate of operating income |

| Financial leverage | LEV | Gearing ratio, which is the ratio of total liabilities to total assets |

| Cash flows | CFO | Net cash flows from operating activities to total assets for the year |

| Tobin’s Q value | TBQ | Tobin’s Q value |

| Shareholding ratio of the largest shareholder | LARST | Shareholding ratio of the largest shareholder |

| Monetary remuneration of executives | COMP | Logarithm of the sum of executive compensation for the first three years of the year |

| Two jobs in one | DUAL | Dummy variable that takes the value of 1 if the current year’s Chairman and Managing Director are both appointed by the same person, and 0 otherwise. |

| Variable Name | Observations | Minimum Value | Maximum Value | Mean Value | Median | Standard Deviation |

|---|---|---|---|---|---|---|

| RDIN | 21,444 | 0.0000 | 0.2535 | 0.0384 | 0.0316 | 0.0434 |

| RDOUT | 21,444 | 0.0000 | 8.5875 | 2.3507 | 0.0000 | 2.6494 |

| Corr | 21,444 | −0.0563 | 0.0905 | 0.0000 | −0.0025 | 0.0215 |

| RDIN | 21,444 | 0.0000 | 0.2535 | 0.0384 | 0.0316 | 0.0434 |

| RDOUT | 21,444 | 0.0000 | 8.5875 | 2.3507 | 0.0000 | 2.6494 |

| Corr | 21,444 | −0.0563 | 0.0905 | 0.0000 | −0.0025 | 0.0215 |

| AGE | 21,444 | 2.4849 | 3.6376 | 3.1685 | 3.1781 | 0.2137 |

| SIZE | 21,444 | 19.7510 | 26.5249 | 22.2751 | 22.0894 | 1.2907 |

| ROA | 21,444 | −0.2926 | 0.2276 | 0.0412 | 0.0379 | 0.0590 |

| LEV | 21,444 | 0.0347 | 0.8923 | 0.4242 | 0.4163 | 0.2016 |

| CFO | 21,444 | −0.1965 | 0.2436 | 0.0489 | 0.0476 | 0.0655 |

| GROW | 21,444 | −0.6576 | 2.5807 | 0.1313 | 0.0902 | 0.3144 |

| TBQ | 21,444 | 0.7908 | 13.3657 | 2.0191 | 1.6059 | 1.3097 |

| LARST | 21,444 | 0.0826 | 0.7579 | 0.3444 | 0.3234 | 0.1472 |

| COMP | 21,444 | 5.4501 | 7.2550 | 6.2702 | 6.2583 | 0.2989 |

| DUAL | 21,444 | 0.0000 | 1.0000 | 0.2459 | 0.0000 | 0.4307 |

| Variables | The Entire Sample (OLS) | Sample Excluding Firms with No R&D Activities (OLS) | ||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| RDIN | RDIN | RDIN | RDIN | |

| Corr | −0.367 *** | −0.297 *** | −0.402 *** | −0.303 *** |

| (−4.34) | (−3.23) | (−3.39) | (−3.38) | |

| AGE | −0.034 *** | −0.026 *** | ||

| (−2.73) | (−3.95) | |||

| SIZE | 0.002 *** | 0.002 *** | ||

| (3.24) | (3.89) | |||

| ROA | 0.083 *** | 0.136 *** | ||

| (5.30) | (5.69) | |||

| LEV | −0.058 *** | −0.067 *** | ||

| (−4.61) | (−5.09) | |||

| CFO | 0.037 *** | 0.058 *** | ||

| (3.66) | (3.73) | |||

| GROW | 0.002 ** | 0.0007 | ||

| (2.53) | (0.45) | |||

| TBQ | 0.005 *** | 0.007 *** | ||

| (3.05) | (3.88) | |||

| LARST | −0.038 *** | −0.034 *** | ||

| (−3.40) | (−3.20) | |||

| COMP | 0.020 *** | 0.026 *** | ||

| (3.65) | (3.28) | |||

| DUAL | 0.007 *** | 0.005 *** | ||

| (3.65) | (3.96) | |||

| Constant | 0.038 *** | 0.094 *** | 0.051 *** | 0.039 *** |

| (3.31) | (3.43) | (3.22) | (3.34) | |

| Observations | 21,444 | 21,444 | 10,504 | 10,504 |

| FIRM/YEAR | NO | YES | NO | YES |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| RDIN | SA | RDIN | |

| Corr | −0.297 *** | 0.619 *** | −0.285 *** |

| (−3.23) | (2.97) | (−3.02) | |

| SA | −0.010 *** | ||

| (−3.58) | |||

| AGE | −0.034 *** | −0.067 *** | −0.034 *** |

| (−2.73) | (−3.37) | (−2.73) | |

| SIZE | 0.002 *** | 1.230 *** | 0.014 *** |

| (3.24) | (6.58) | (4.117) | |

| ROA | 0.083 *** | −0.128 *** | 0.082 *** |

| (5.30) | (−4.43) | (5.04) | |

| LEV | −0.058 *** | −0.031 *** | −0.058 *** |

| (−4.61) | (−3.89) | (−3.40) | |

| CFO | 0.037 *** (3.66) | −0.038 *** (−3.75) | 0.036 *** (8.281) |

| GROW | 0.002 ** | −0.010 *** | 0.002 *** |

| (2.53) | (−4.61) | (2.65) | |

| TBQ | 0.005 *** | 0.016 *** | 0.005 *** |

| (3.05) | (3.25) | (2.92) | |

| LARST | −0.038 *** | 0.052 *** | −0.038 *** |

| (−3.40) | (3.28) | (−2.63) | |

| COMP | 0.020 *** | −0.008 *** | 0.020 *** |

| (3.65) | (−2.93) | (2.72) | |

| DUAL | 0.007 *** | 0.008 *** | 0.006 *** |

| (3.65) | (5.15) | (3.52) | |

| Constant | 0.094 *** | −22.30 *** | 0.312 *** |

| (3.43) | (−3.86) | (5.08) | |

| Observations | 21,444 | 21,444 | 21,444 |

| R-squared | 0.090 | 0.994 | 0.090 |

| FIRM/YEAR | YES | YES | YES |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Weak Internal Control | Strong Internal Control | No Professional Background | Professional Background | Non-State-Owned Enterprise | State-Owned Enterprise | |

| Corr | −0.267 *** | −0.005 | −0.100 | −0.264 *** | −0.006 | −0.229 ** |

| (−3.79) | (−0.58) | (−0.20) | (−4.02) | (−0.08) | (−2.71) | |

| AGE | −0.038 *** | −0.031 *** | −0.028 *** | −0.037 *** | −0.034 *** | −0.024 *** |

| (−3.23) | (−3.37) | (−3.29) | (−4.65) | (−3.28) | (−3.49) | |

| SIZE | −0.001 ** | −0.002 *** | 0.001 * | 0.002 *** | 0.002 *** | 0.001 ** |

| (−2.48) | (−6.19) | (1.88) | (5.94) | (3.86) | (2.37) | |

| ROA | −0.087 *** | −0.082 *** | 0.094 *** | 0.079 *** | 0.092 *** | 0.075 *** |

| (−3.12) | (−2.61) | (3.60) | (3.04) | (3.31) | (3.54) | |

| LEV | −0.060 *** | −0.056 *** | −0.062 *** | −0.057 *** | −0.074 *** | −0.032 *** |

| (−5.08) | (−3.32) | (−2.91) | (−3.66) | (−3.18) | (−4.06) | |

| CFO | −0.040 *** | −0.035 *** | 0.053 *** | 0.030 *** | 0.042 *** | 0.032 *** |

| (−5.94) | (−6.17) | (6.79) | (5.65) | (6.95) | (5.52) | |

| GROW | 0.000 | 0.004 *** | 0.002 | 0.003 ** | 0.001 | 0.004 *** |

| (0.13) | (3.15) | (1.05) | (2.46) | (0.86) | (3.10) | |

| TBQ | 0.004 *** | 0.006 *** | 0.005 *** | 0.005 *** | 0.005 *** | 0.005 *** |

| (2.62) | (3.12) | (3.55) | (3.06) | (7.36) | (5.13) | |

| LARST | −0.035 *** | −0.039 *** | −0.034 *** | −0.040 *** | −0.035 *** | −0.032 *** |

| (−2.61) | (−3.06) | (−5.23) | (−7.69) | (−3.33) | (−3.58) | |

| COMP | 0.021 *** | 0.019 *** | 0.021 *** | 0.020 *** | 0.020 *** | 0.021 *** |

| (3.72) | (3.86) | (4.46) | (6.39) | (3.66) | (4.46) | |

| DUAL | 0.006 *** | 0.007 *** | 0.005 *** | 0.007 *** | 0.005 *** | 0.002 * |

| (7.01) | (8.12) | (5.17) | (3.31) | (6.44) | (1.72) | |

| Constant | 0.084 *** | 0.098 *** | 0.053 *** | 0.104 *** | 0.105 *** | 0.017 |

| (3.01) | (5.14) | (3.84) | (4.46) | (3.16) | (1.51) | |

| Observations | 10,676 | 10,768 | 6650 | 14,794 | 13,213 | 8231 |

| R-squared | 0.219 | 0.269 | 0.236 | 0.244 | 0.225 | 0.178 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| No Political Connection | Political Connection Present | Low Audit Quality | High Audit Quality | Low Institutional Ownership | High Institutional Ownership | |

| Corr | −0.107 * | −0.214 *** | −0.279 *** | −0.081 * | −0.214 *** | −0.001 |

| (−1.57) | (−4.47) | (−3.32) | (−1.17) | (−4.31) | (−0.54) | |

| AGE | −0.037 *** | −0.030 *** | −0.035 *** | −0.020 *** | −0.043 *** | −0.025 *** |

| (−3.97) | (−5.16) | (−6.80) | (−5.78) | (−3.75) | (−2.74) | |

| SIZE | 0.001 *** | 0.003 *** | 0.002 *** | 0.001 | −0.000 | −0.002 *** |

| (3.41) | (6.06) | (5.66) | (0.61) | (−0.60) | (−6.49) | |

| ROA | 0.076 *** | 0.094 *** | 0.083 *** | 0.073 *** | −0.097 *** | −0.056 *** |

| (3.32) | (3.29) | (4.83) | (3.28) | (−3.66) | (−3.32) | |

| LEV | −0.061 *** | −0.052 *** | −0.060 *** | −0.035 *** | −0.079 *** | −0.034 *** |

| (−4.88) | (−2.07) | (−3.97) | (−5.97) | (−5.50) | (−3.13) | |

| CFO | 0.040 *** | 0.029 *** | 0.036 *** | 0.045 *** | −0.037 *** | −0.033 *** |

| (4.20) | (4.19) | (7.85) | (2.95) | (−5.37) | (−6.16) | |

| GROW | 0.002 | 0.003 ** | 0.002 ** | 0.003 | 0.000 | 0.003 *** |

| (1.48) | (2.45) | (2.25) | (0.76) | (0.10) | (2.61) | |

| TBQ | 0.005 *** | 0.006 *** | 0.005 *** | 0.006 *** | 0.005 *** | 0.005 *** |

| (6.85) | (4.31) | (3.24) | (6.24) | (5.46) | (6.54) | |

| LARST | −0.039 *** | −0.036 *** | −0.036 *** | −0.047 *** | −0.023 *** | −0.029 *** |

| (−6.41) | (−2.60) | (−8.65) | (−9.00) | (−3.03) | (−4.52) | |

| COMP | 0.019 *** | 0.021 *** | 0.021 *** | 0.019 *** | 0.023 *** | 0.017 *** |

| (4.46) | (3.16) | (8.76) | (7.37) | (3.87) | (3.92) | |

| DUAL | 0.007 *** | 0.005 *** | 0.006 *** | 0.013 *** | 0.007 *** | 0.003 *** |

| (9.12) | (4.53) | (9.60) | (5.52) | (7.80) | (4.07) | |

| Constant | 0.099 *** | 0.087 *** | 0.095 *** | −0.016 | 0.075 *** | 0.074 *** |

| (3.22) | (4.56) | (4.61) | (−0.66) | (5.48) | (8.11) | |

| Observations | 14,461 | 6983 | 20,201 | 1243 | 10,713 | 10,731 |

| R-squared | 0.242 | 0.241 | 0.236 | 0.276 | 0.234 | 0.197 |

| Variables | (1) | (2) |

|---|---|---|

| First | Second | |

| MCorr | 0.823 *** | |

| (7.86) | ||

| Corr | −2.727 *** | |

| (−6.32) | ||

| Controls | YES | YES |

| FIRM/YEAR | YES | YES |

| Constant | −0.009 ** | 0.111 |

| (−2.11) | (0.01) | |

| Observations | 21,444 | 21,444 |

| Variables | Unmatched | Mean | % Bias | t-Test | ||

|---|---|---|---|---|---|---|

| Matched | Treated | Control | t-Value | p-Value | ||

| SIZE | U | 22.133 | 22.434 | −3.500 | −3.190 | 0.000 |

| M | 22.133 | 22.171 | −2.900 | −2.440 | 0.015 | |

| ROA | U | 0.043 | 0.039 | 2.000 | 2.130 | 0.000 |

| M | 0.043 | 0.044 | −0.400 | −0.250 | 0.803 | |

| GROW | U | 0.114 | 0.148 | −1.900 | −0.950 | 0.000 |

| M | 0.114 | 0.112 | 0.600 | 0.480 | 0.633 | |

| TBQ | U | 2.103 | 1.935 | 2.900 | 1.420 | 0.000 |

| M | 2.101 | 2.123 | −1.700 | −1.210 | 0.226 | |

| AGE | U | 3.170 | 3.166 | 2.100 | 1.540 | 0.124 |

| M | 3.170 | 3.172 | −1.000 | −0.700 | 0.486 | |

| LEV | U | 0.416 | 0.432 | −2.100 | −1.950 | 0.000 |

| M | 0.416 | 0.419 | −1.600 | −1.210 | 0.225 | |

| CFO | U | 0.052 | 0.046 | 1.300 | 1.540 | 0.000 |

| M | 0.052 | 0.054 | −1.900 | −1.360 | 0.174 |

| Variables | (1) | (2) |

|---|---|---|

| Ols | Psm_Ols | |

| Corr | −0.297 *** | −0.300 *** |

| (−3.23) | (−4.46) | |

| AGE | −0.034 *** | −0.033 *** |

| (−2.73) | (−5.12) | |

| SIZE | 0.002 *** | 0.003 *** |

| (3.24) | (6.15) | |

| ROA | 0.083 *** | 0.080 *** |

| (5.30) | (6.91) | |

| LEV | −0.058 *** | −0.059 *** |

| (−4.61) | (−4.33) | |

| CFO | 0.037 *** | 0.035 *** |

| (3.66) | (5.04) | |

| GROW | 0.002 ** | 0.002 |

| (2.53) | (1.25) | |

| TBQ | 0.005 *** | 0.004 *** |

| (3.05) | (7.17) | |

| LARST | −0.038 *** | −0.038 *** |

| (−3.40) | (−3.42) | |

| COMP | 0.020 *** | 0.024 *** |

| (3.65) | (4.24) | |

| DUAL | 0.007 *** | 0.008 *** |

| (3.65) | (6.60) | |

| Constant | 0.094 *** | 0.088 *** |

| (3.43) | (6.59) | |

| Observations | 21,444 | 21,444 |

| FIRM/YEAR | YES | YES |

| Variables | Full Sample (OLS) | Sample Excluding Companies with no R&D Activity (OLS) | ||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| RDOUT | RDOUT | RDOUT | RDOUT | |

| Corr | −0.657 *** | −0.519 *** | −0.689 *** | −0.830 *** |

| (−7.89) | (−6.09) | (−3.14) | (−3.28) | |

| AGE | −2.223 *** | −0.793 *** | ||

| (−6.15) | (−5.70) | |||

| SIZE | 0.021 | 0.415 *** | ||

| (1.04) | (2.80) | |||

| ROA | 1.531 *** | 1.183 *** | ||

| (4.15) | (3.43) | |||

| LEV | −0.853 *** | −0.072 | ||

| (−7.45) | (−0.68) | |||

| CFO | 0.488 | 0.177 | ||

| (1.64) | (0.62) | |||

| GROW | 0.135 ** | 0.087 | ||

| (3.26) | (1.47) | |||

| TBQ | −0.026 * | 0.010 | ||

| (−1.75) | (0.72) | |||

| LARST | −1.165 *** | −0.208 * | ||

| (−9.26) | (−1.85) | |||

| COMP | 0.617 *** | 0.897 *** | ||

| (8.86) | (4.12) | |||

| DUAL | 0.247 *** | 0.210 *** | ||

| (5.89) | (6.10) | |||

| Constant | 2.351 *** | 5.759 *** | 4.767 *** | −7.483 *** |

| (3.16) | (3.25) | (4.52) | (−6.10) | |

| Observations | 21,444 | 21,444 | 10,504 | 10,504 |

| FIRM/YEAR | NO | YES | NO | YES |

| Variables | Tobit Regression | Poisson Regression | Negative Binomial Regression | |||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| RDIN | RDIN | RDOUT | RDOUT | RDOUT | RDOUT | |

| Corr | −0.402 *** | −0.300 *** | −0.272 *** | −0.216 *** | −0.284 *** | −0.215 *** |

| (−5.66) | (−2.74) | (−3.62) | (−3.29) | (−5.44) | (−4.00) | |

| AGE | −0.046 *** | −0.905 *** | −0.996 *** | |||

| (−3.61) | (−4.74) | (−3.63) | ||||

| SIZE | 0.002 *** | 0.012 ** | 0.015 | |||

| (4.77) | (2.30) | (1.19) | ||||

| ROA | 0.090 *** | 0.626 *** | 0.623 *** | |||

| (4.43) | (6.67) | (2.63) | ||||

| LEV | −0.071 *** | −0.408 *** | −0.526 *** | |||

| (−3.09) | (−3.78) | (−6.98) | ||||

| CFO | 0.036 *** | 0.222 *** | 0.252 | |||

| (7.03) | (2.89) | (1.28) | ||||

| GROW | 0.003 *** | 0.056 *** | 0.071 * | |||

| (2.58) | (3.76) | (1.74) | ||||

| TBQ | 0.005 *** | −0.014 *** | −0.024 ** | |||

| (2.72) | (−3.59) | (−2.44) | ||||

| LARST | −0.047 *** | −0.503 *** | −0.493 *** | |||

| (−2.85) | (−5.60) | (−6.26) | ||||

| COMP | 0.022 *** | 0.259 *** | 0.299 *** | |||

| (8.69) | (4.59) | (6.70) | ||||

| DUAL | 0.008 *** | 0.097 *** | 0.105 *** | |||

| (3.15) | (9.59) | (4.13) | ||||

| Constant | 0.034 *** | 0.115 *** | 0.853 *** | 2.127 *** | 0.853 *** | 2.160 *** |

| (8.95) | (3.17) | (9.33) | (6.52) | (7.54) | (6.68) | |

| Observations | 21,444 | 21,444 | 21,444 | 21,444 | 21,444 | 21,444 |

| FIRM/YEAR | NO | YES | NO | YES | NO | YES |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bai, M.; Chen, Y.; Hong, Y.; Yang, Z. A Study of the Impact of Executive Corruption on Corporate Innovation. Systems 2024, 12, 25. https://doi.org/10.3390/systems12010025

Bai M, Chen Y, Hong Y, Yang Z. A Study of the Impact of Executive Corruption on Corporate Innovation. Systems. 2024; 12(1):25. https://doi.org/10.3390/systems12010025

Chicago/Turabian StyleBai, Ming, Yanru Chen, Ye Hong, and Zhongqi Yang. 2024. "A Study of the Impact of Executive Corruption on Corporate Innovation" Systems 12, no. 1: 25. https://doi.org/10.3390/systems12010025

APA StyleBai, M., Chen, Y., Hong, Y., & Yang, Z. (2024). A Study of the Impact of Executive Corruption on Corporate Innovation. Systems, 12(1), 25. https://doi.org/10.3390/systems12010025