Verifying SDG ESG Compliance in Manufacturing Industry Projects by Surveying Sponsors

Abstract

1. Introduction

2. Literature Review

2.1. Theoretical Underpinning

2.2. Sustainable Development Goals and ESG Frameworks

2.3. ESG Integration in Project Management

2.4. Measuring ESG Compliance and Performance

2.5. ESG in the Manufacturing Industry Context

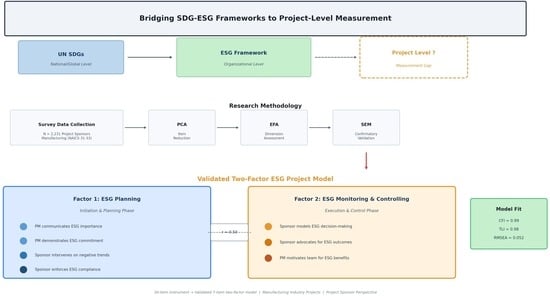

3. Research Methodology

3.1. Research Design

3.2. Sample and Data Collection

3.3. Survey Instrument Development

3.4. Analysis Procedures

3.5. Structural Model Specification

4. Results and Discussion

4.1. Sample Description

4.2. Structural Model Results

4.3. Item Reduction: From 30 Items and Six Factors to Seven Items and Two Factors

4.4. Measurement Model Fit

4.5. Discussion

5. Conclusions

5.1. Summary

5.2. Theoretical Implications

5.3. Practical and Policy Implications

5.4. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bebbington, J.; Unerman, J. Achieving the United Nations Sustainable Development Goals: An enabling role for accounting research. Account. Audit. Account. J. 2018, 31, 2–24. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Investig. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Delgado-Ceballos, J.; Ortiz-De-Mandojana, N.; Antolin-Lopez, R.; Montiel, I. Connecting the Sustainable Development Goals to firm-level sustainability and ESG factors: The need for double materiality. BRQ Bus. Res. Q. 2023, 26, 2–10. [Google Scholar] [CrossRef]

- Carvalho, M.M.; Rabechini, R. Can project sustainability management impact project success? An empirical study applying a contingent approach. Int. J. Proj. Manag. 2017, 35, 1120–1132. [Google Scholar] [CrossRef]

- Silvius, A.; Schipper, R.P. Sustainability in project management: A literature review and impact analysis. Soc. Bus. 2014, 4, 63–96. [Google Scholar] [CrossRef]

- Sabini, L.; Muzio, D.; Alderman, N. 25 years of ‘sustainable projects’. What we know and what the literature says. Int. J. Proj. Manag. 2019, 37, 820–838. [Google Scholar] [CrossRef]

- Chen, H.-M.; Kuo, T.-C.; Chen, J.-L. Impacts on the ESG and financial performances of companies in the manufacturing industry based on the climate change related risks. J. Clean. Prod. 2022, 380, 134951. [Google Scholar] [CrossRef]

- Abdul-Rashid, S.H.; Sakundarini, N.; Raja Ghazilla, R.A.; Thurasamy, R. The impact of sustainable manufacturing practices on sustainability performance: Empirical evidence from Malaysia. Int. J. Oper. Prod. Manag. 2017, 37, 182–204. [Google Scholar] [CrossRef]

- Eskerod, P.; Huemann, M. Sustainable development and project stakeholder management: What standards say. Int. J. Manag. Proj. Bus. 2013, 6, 36–50. [Google Scholar] [CrossRef]

- Kivila, J.; Martinsuo, M.; Vuorinen, L. Sustainable project management through project control in infrastructure projects. Int. J. Proj. Manag. 2017, 35, 1167–1183. [Google Scholar] [CrossRef]

- Anelli, D.; Morano, P.; Fariello, F.; Sabatelli, E. Environmental, Social and Governance (ESG) Assessment with a Two-Phase Goal-Programming-Based Optimization Model: A Comparative Study of Envipark and Kalundborg Eco-Industrial Parks. Front. Built Environ. 2026, 12, 1731282. [Google Scholar] [CrossRef]

- Martens, M.L.; Carvalho, M.M. Key factors of sustainability in project management context: A survey exploring the project managers’ perspective. Int. J. Proj. Manag. 2017, 35, 1084–1102. [Google Scholar] [CrossRef]

- van Zanten, J.A.; van Tulder, R. Multinational enterprises and the Sustainable Development Goals: An institutional approach to corporate engagement. J. Int. Bus. Policy 2018, 1, 208–233. [Google Scholar] [CrossRef]

- van Zanten, J.A.; van Tulder, R. Analyzing companies’ interactions with the Sustainable Development Goals through network analysis: Four corporate sustainability imperatives. Bus. Strategy Environ. 2021, 30, 2396–2420. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The impact of corporate sustainability on organizational processes and performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef]

- Messaoudi, L.; Seba, L.; Jahmane, A. A quadratic goal programming for portfolio selection based on ESG factors. J. Organ. Change Manag. 2025, 38, 605–624. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef]

- Marcelino-Sadaba, S.; Gonzalez-Jaen, L.F.; Perez-Ezcurdia, A. Using project management as a way to sustainability. From a comprehensive review to a framework definition. J. Clean. Prod. 2015, 99, 1–16. [Google Scholar] [CrossRef]

- Sanchez, M.A. Integrating sustainability issues into project management. J. Clean. Prod. 2015, 96, 319–330. [Google Scholar] [CrossRef]

- Christensen, H.B.; Hail, L.; Leuz, C. Mandatory CSR and Sustainability Reporting: Economic Analysis and Literature Review; ECGI: Brussels, Belgium, 2019. [Google Scholar]

- Berg, F.; Kolbel, J.F.; Rigobon, R. Aggregate Confusion: The Divergence of ESG Ratings. Rev. Financ. 2022, 26, 1315–1344. [Google Scholar] [CrossRef]

- Khan, M.; Serafeim, G.; Yoon, A. Corporate Sustainability: First Evidence on Materiality. Account. Rev. 2016, 91, 1697–1724. [Google Scholar] [CrossRef]

- Acerbi, F.; Taisch, M. A literature review on circular economy adoption in the manufacturing sector. J. Clean. Prod. 2020, 273, 123086. [Google Scholar] [CrossRef]

- Lieder, M.; Rashid, A. Towards circular economy implementation: A comprehensive review in context of manufacturing industry. J. Clean. Prod. 2016, 115, 36–51. [Google Scholar] [CrossRef]

- Yang, J.; Shen, G.Q.; Ho, M.; Drew, D.S.; Chan, A.P.C. Exploring critical success factors for stakeholder management in construction projects. J. Civ. Eng. Manag. 2009, 15, 337–348. [Google Scholar] [CrossRef]

- Mansell, P.; Philbin, S.P.; Broyd, T.; Nicholson, I. Assessing the impact of infrastructure projects on global sustainable development goals. Proc. Inst. Civ. Eng. Eng. Sustain. 2019, 173, 196–212. [Google Scholar] [CrossRef]

- Eskerod, P.; Huemann, M.; Savage, G. Project Stakeholder Management-Past and Present. Proj. Manag. J. 2015, 46, 6–14. [Google Scholar] [CrossRef]

- Wang, J.; Hong, Z.; Long, H. Digital Transformation Empowers ESG Performance in the Manufacturing Industry: From ESG to DESG. Sage Open 2023, 13, 21582440231204158. [Google Scholar] [CrossRef]

- Costello, A.B.; Osborne, J. Best practices in exploratory factor analysis: Four recommendations for getting the most from your analysis. Pract. Assess. Res. Eval. 2005, 10, 7. [Google Scholar]

- Hu, L.t.; Bentler, P.M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Struct. Equ. Model. Multidiscip. J. 1999, 6, 1–55. [Google Scholar] [CrossRef]

{kind=link}

| Code | Item Text | Source | EFA Loading | CFA Loading |

|---|---|---|---|---|

| SA1 | The project manager ensured ESG goals were explicitly included in the project charter. | Silvius & Schipper [5] | — | — |

| SA2 | The project manager aligned project ESG objectives with organizational ESG strategy. | Silvius & Schipper [5] | — | — |

| SA3 | The project manager communicated the importance of ESG outcomes to the project team. | Silvius & Schipper [5]; Mansell et al. [26] | 0.58 | 0.71 |

| SA4 | The project manager required ESG considerations in scope, schedule, and budget decisions. | Silvius & Schipper [5] | 0.41 | — |

| SA5 | The project manager demonstrated visible commitment to ESG transformation. | Silvius & Schipper [5]; Yang et al. [25] | 0.63 | 0.74 |

| RP1 | The project manager planned a sufficient budget for ESG activities and measurement. | Mansell et al. [26] | — | — |

| RP2 | The project sponsor ensured access to ESG expertise (internal or external). | Mansell et al. [26] | — | — |

| RP3 | The project manager employed tools for tracking ESG scope compliance. | Mansell et al. [26] | 0.38 | — |

| RP4 | The project manager made ESG training available for the project team. | Silvius & Schipper [5] | — | — |

| RP5 | The project sponsor removed organizational barriers to ESG implementation. | Silvius & Schipper [5] | 0.35 | — |

| GV1 | The project sponsor required ESG KPIs in governance dashboards and stage-gates. | Mansell et al. [26] | 0.43 | — |

| GV2 | The project manager ensured environmental, social, and regulatory risks were tracked. | Silvius & Schipper [5] | 0.42 | — |

| GV3 | The project manager intervened when ESG metrics trended negatively. | Silvius & Schipper [5]; Yang et al. [25] | 0.60 | 0.68 |

| GV4 | The project sponsor enforced compliance with ESG standards and reporting frameworks. | Mansell et al. [26] | 0.67 | 0.72 |

| GV5 | The project manager ensured ESG considerations influenced major decisions. | Silvius & Schipper [5] | 0.40 | — |

| SC1 | The project sponsor encouraged engagement with affected communities. | Yang et al. [25] | — | — |

| SC2 | The project sponsor approved time and budget for community consultations. | Yang et al. [25] | — | — |

| SC3 | The project sponsor supported inclusive design and DEI-related project goals. | Yang et al. [25] | — | — |

| SC4 | The project manager ensured transparency with stakeholders regarding ESG outcomes. | Eskerod et al. [27] | 0.29 | — |

| SC5 | The project sponsor supported partnerships with NGOs or community organizations. | Yang et al. [25] | — | — |

| MN1 | The project manager required regular reporting of ESG KPIs. | Mansell et al. [26] | 0.44 | — |

| MN2 | The project manager validated the accuracy of ESG data before reporting. | Mansell et al. [26] | 0.31 | — |

| MN3 | The project manager supported digital tools for real-time ESG tracking. | Wang et al. [28] | 0.28 | — |

| MN4 | The project manager encouraged lessons-learned capture for ESG practices. | Kivilä et al. [10] | 0.32 | — |

| MN5 | The project manager promoted transparency to avoid greenwashing. | Silvius & Schipper [5] | — | — |

| LB1 | The project sponsor modeled ESG-aligned decision-making. | Silvius & Schipper [5]; Yang et al. [25] | 0.71 | 0.78 |

| LB2 | The project sponsor advocated for ESG outcomes in executive forums. | Silvius & Schipper [5] | 0.68 | 0.75 |

| LB3 | The project manager motivated the team to pursue ESG benefits. | Martens & Carvalho [12] | 0.62 | 0.70 |

| LB4 | The project sponsor supported long-term ESG value over short-term efficiency. | Silvius & Schipper [5] | 0.35 | — |

| LB5 | The project sponsor reinforced the legitimacy of ESG goals when challenged. | Silvius & Schipper [5] | 0.38 | — |

| Item | Reason for Exclusion | Stage of Elimination |

|---|---|---|

| SA1 | Negative loading in PCA; communality = 0.18 | Dropped at PCA stage |

| SA2 | Cross-loading on two factors (Δ < 0.10); communality = 0.24 | Dropped at PCA stage |

| SA4 | Primary loading = 0.41; cross-loading > 0.30 | Dropped at EFA stage |

| RP1 | Communality = 0.22; negative EFA loading | Dropped at PCA stage |

| RP2 | Primary loading = 0.38; communality = 0.21 | Dropped at PCA stage |

| RP3 | Cross-loading; primary loading = 0.38 | Dropped at EFA stage |

| RP4 | Communality = 0.19; weak primary loading | Dropped at PCA stage |

| RP5 | Primary loading = 0.35; communality = 0.28 | Dropped at EFA stage |

| GV1 | Cross-loading; primary loading = 0.43 | Dropped at EFA stage |

| GV2 | Cross-loading on Factor 1 and Factor 2 (Δ = 0.08) | Dropped at EFA stage |

| GV5 | Primary loading = 0.40; communality = 0.26 | Dropped at EFA stage |

| SC1 | Communality = 0.16; weak primary loading | Dropped at PCA stage |

| SC2 | Communality = 0.18; negative loading | Dropped at PCA stage |

| SC3 | Communality = 0.17; primary loading = 0.27 | Dropped at PCA stage |

| SC4 | Primary loading = 0.29; below communality threshold | Dropped at EFA stage |

| SC5 | Communality = 0.14; negative loading | Dropped at PCA stage |

| MN1 | Cross-loading; primary loading = 0.44 | Dropped at EFA stage |

| MN2 | Primary loading = 0.31; communality = 0.23 | Dropped at EFA stage |

| MN3 | Communality = 0.28; primary loading = 0.28 | Dropped at PCA stage |

| MN4 | Primary loading = 0.32; communality = 0.25 | Dropped at EFA stage |

| MN5 | Negative loading; communality = 0.15 | Dropped at PCA stage |

| LB4 | Primary loading = 0.35; cross-loading | Dropped at EFA stage |

| LB5 | Primary loading = 0.38; cross-loading | Dropped at EFA stage |

| Characteristic/Category | n | % | Notes |

|---|---|---|---|

| Gender: Male | 1495 | 67.0% | |

| Gender: Female | 736 | 33.0% | |

| Education: Grade/Vocational | 222 | 9.9% | |

| Education: Associate | 245 | 11.0% | 1 = Associate |

| Education: Bachelor | 1071 | 48.0% | 2 = Bachelor |

| Education: Master | 357 | 16.0% | 3 = Master |

| Education: Advanced/Specialist | 336 | 15.1% | 4 = Advanced |

| NAICS 31: Food, Beverage & Textile Mfg. | 603 | 27.0% | |

| NAICS 32: Chemical, Plastics & Paper Mfg. | 692 | 31.0% | |

| NAICS 33: Metals, Electronics & Transport Mfg. | 936 | 42.0% | |

| Firm Size: Small (<100 employees) | 446 | 20.0% | |

| Firm Size: Medium (100–999) | 826 | 37.0% | |

| Firm Size: Large (1000+) | 959 | 43.0% | |

| Respondent Age: Mean (SD) | 29.5 (11.0) | — | Range: 18–86 |

| Role: Project Sponsor | 1048 | 47.0% | |

| Role: Project Manager/PM Lead | 804 | 36.0% | |

| Role: Executive/C-Suite | 379 | 17.0% | |

| Total | 2231 | 100% |

| Factor | Item | Item Text | Unstd. Loading | SE | z-Value | p | Std. Load. |

|---|---|---|---|---|---|---|---|

| ESG PM Planning | SA3 | The project manager communicated the importance of ESG outcomes to the project team. | 1.000 (ref) | 0.000 | — | — | 0.71 |

| ESG PM Planning | SA5 | The project manager demonstrated visible commitment to ESG transformation. | 1.185 | 0.042 | 27.888 | <0.001 | 0.74 |

| ESG PM Planning | GV3 | The project manager intervened when ESG metrics trended negatively. | 0.872 | 0.034 | 25.812 | <0.001 | 0.68 |

| ESG PM Planning | GV4 | The project sponsor enforced compliance with ESG standards and reporting frameworks. | 1.052 | 0.037 | 28.704 | <0.001 | 0.72 |

| ESG PM Controlling | LB1 | The project sponsor modeled ESG-aligned decision-making. | 1.029 | 0.022 | 46.618 | <0.001 | 0.78 |

| ESG PM Controlling | LB2 | The project sponsor advocated for ESG outcomes in executive forums. | 1.000 (ref) | 0.000 | — | — | 0.75 |

| ESG PM Controlling | LB3 | The project manager motivated the team to pursue ESG benefits. | 0.795 | 0.018 | 44.686 | <0.001 | 0.70 |

| Fit Index | Value |

|---|---|

| Comparative Fit Index (CFI) | 0.992 |

| Tucker–Lewis Index (TLI) | 0.987 |

| Bentler-Bonett Non-normed Fit Index (NNFI) | 0.987 |

| Root Mean Square Error of Approximation (RMSEA) | 0.052 |

| RMSEA 90% CI | [0.043, 0.063] |

| Standardized Root Mean Square Residual (SRMR) | 0.035 |

| Goodness of Fit Index (GFI) | 0.998 |

| McDonald Fit Index (MFI) | 0.988 |

| Hoelter Critical N (α = 0.05) | 762.316 |

| Inter-factor Correlation (r) | ≈0.50 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.

Share and Cite

Strang, K.D.; Vajjhala, N.R. Verifying SDG ESG Compliance in Manufacturing Industry Projects by Surveying Sponsors. Information 2026, 17, 311. https://doi.org/10.3390/info17040311

Strang KD, Vajjhala NR. Verifying SDG ESG Compliance in Manufacturing Industry Projects by Surveying Sponsors. Information. 2026; 17(4):311. https://doi.org/10.3390/info17040311

Chicago/Turabian StyleStrang, Kenneth David, and Narasimha Rao Vajjhala. 2026. "Verifying SDG ESG Compliance in Manufacturing Industry Projects by Surveying Sponsors" Information 17, no. 4: 311. https://doi.org/10.3390/info17040311

APA StyleStrang, K. D., & Vajjhala, N. R. (2026). Verifying SDG ESG Compliance in Manufacturing Industry Projects by Surveying Sponsors. Information, 17(4), 311. https://doi.org/10.3390/info17040311