Abstract

Using platform self-operation, customer reviews, and compensation commitments as traditional benchmarks, this study foregrounds blockchain traceability as a technology-enabled authenticity signal in cross-border cosmetic e-commerce (CBEC). Using an 8-scenario orthogonal experiment, we test a model in which perceived risk mediates the effects of authenticity signals on purchase intention. We probe blockchain boundary conditions by examining their interactions with traditional signals. Our results show that blockchain is the only signal with a significant direct effect on purchase intention and that it also exerts an indirect effect by reducing perceived risk. While customer reviews show no consistent effect, self-operation and compensation influence purchase intention indirectly via risk reduction. Moderation tests indicate that blockchain is most effective in low-trust settings—i.e., when self-operation, reviews, or compensation safeguards are absent or weak—while this marginal impact declines when such safeguards are strong. These findings refine signaling theory by distinguishing a technology-backed signal from institutional and social signals and by positioning perceived risk as the central mechanism in CBEC cosmetics. Managerially speaking, blockchain should serve as the anchor signal in high-risk contexts and as a reinforcing signal where traditional assurances already exist. Future work should extend to field/transactional data and additional signals (e.g., brand reputation, third-party certifications).

1. Introduction

Cross-border e-commerce (CBEC) has become one of the fastest-growing components of digital trade in recent years. According to the WTO and OECD [1], digital trade, including CBEC transactions, has continued to expand rapidly, driven by greater global connectivity and digital platforms. In China, official customs data show that the total value of CBEC imports and exports reached RMB 2.38 trillion in 2023, representing a 15.6 percent year-on-year increase [2]. Cosmetics are among the leading product categories in CBEC retail imports, accounting for more than 40 percent of transactions in some surveys [3]. As cosmetics are high-value and experience-oriented products closely related to health and appearance, authenticity and safety concerns are particularly salient. Consumer trust has thus become a decisive factor for the sustainable development of CBEC platforms in this sector.

Despite rapid expansion, CBEC faces persistent challenges in fostering consumer confidence. Counterfeit products, inconsistent quality, unreliable logistics, and inadequate post-purchase protection frequently undermine trust, exposing consumers to heightened uncertainty [4,5]. Compared with domestic e-commerce, cross-border transactions exacerbate information asymmetry due to geographic distance and complex global supply chains, which amplify consumers’ perceived risk [4]. High levels of perceived risk have been shown to suppress consumer engagement and reduce purchase intention across e-commerce platforms [6,7]. Addressing these risks through effective trust-building mechanisms is therefore both a managerial necessity and an important avenue of academic inquiry. Perceived risk has long been identified as a key determinant of consumer behavior in digital commerce. Without the ability to physically inspect products, consumers rely on signals and cues to assess authenticity and credibility. High perceived risk amplifies concerns over financial loss, product performance, and security, which suppresses purchase intention [6,8,9]. In CBEC contexts, these concerns are even more pronounced, as consumers also face uncertainties related to customs clearance, delivery reliability, and dispute resolution [4,7]. This makes perceived risk particularly salient in shaping trust and purchase intention in cross-border settings.

To address these challenges, CBEC platforms have increasingly adopted authenticity signals to mitigate consumer concerns. Traditional mechanisms include platform self-operation labels, verified customer reviews, and risk-bearing commitments such as “fake one, pay ten” or unconditional return guarantees (Zhang & Pertheban, 2023) [10]. Grounded in signaling theory (Spence, 1973) [11], these cues reduce information asymmetry and enable consumers to infer product authenticity and seller credibility. Empirical research confirms that platform-backed endorsements, certification labels, and compensation guarantees enhance consumer trust and stimulate purchase intention [12,13]. Similarly, customer reviews function as vital social proof, where review volume, valence, and credibility significantly influence consumer decisions [14,15]. Nevertheless, the reliability of these traditional signals has been brought into question: reviews may be fabricated or manipulated [16], self-operation is costly and difficult to scale, and compensation policies are often inconsistently enforced [17,18]. Recent advances in blockchain technology provide new opportunities for authenticity signaling. Blockchain enables immutable, transparent, and verifiable records of product origins and supply chain processes [19]. In high-risk industries such as luxury goods, pharmaceuticals, and cosmetics, blockchain-based traceability has been shown to enhance consumer trust and willingness to pay [20,21]. Unlike traditional signals that depend on institutional authority, blockchain creates decentralized, technology-driven trust validated through transparent records and smart contracts [22,23]. Its signaling effectiveness is nevertheless not guaranteed. Consumers often lack familiarity with blockchain applications, and the reliability of data inputs remains problematic—if false or incomplete information is entered, blockchain cannot ensure authenticity (“garbage in, garbage out”) [24,25]. Moreover, concerns about privacy and the trade-off between transparency and data protection further limit consumer acceptance [26].

Although signaling theory has been widely applied in e-commerce research, important gaps remain. First, prior studies have predominantly focused on traditional signals such as platform certification, customer reviews, and refund policies [27,28], often without rigorous theoretical grounding regarding how these mechanisms mitigate uncertainty in online exchange environments [29]. Second, while mediating mechanisms such as perceived quality and value have been explored [30], the role of perceived risk—arguably more critical in highly uncertain cross-border contexts—remains underexamined. Third, most prior research relies on surveys rather than controlled experiments, meaning that the question of how signals jointly operate remains unanswered. Finally, although some recent studies have examined the role of external cues in shaping CBEC purchase decisions [31], little is known about how consumers integrate blockchain cues with traditional signals in sensitive product categories such as cosmetics.

This study addresses these gaps by employing a between-subject experimental design grounded in signaling theory, comparing four authenticity signals commonly used in CBEC: blockchain traceability labels, platform self-operation, customer reviews, and compensation guarantees. It examines both the direct effects of these signals on purchase intention and the indirect effects mediated by perceived risk. The contributions of this study are threefold. First, it advances signaling theory by systematically comparing blockchain-based and traditional signals within a unified framework. Second, it empirically demonstrates the mediating role of perceived risk in cross-border contexts, offering a more nuanced understanding of trust formation. Third, it offers practical guidance for CBEC managers in designing multi-signal trust strategies that effectively balance technology-driven and traditional mechanisms to mitigate consumer risk and enhance purchase intention.

2. Theoretical Background and Related Work

2.1. Signaling Theory and Its Role in E-Commerce

Originally introduced by Spence [11], signaling theory provides a powerful framework for understanding how observable cues help reduce market information asymmetry. In contexts where buyers cannot directly evaluate product attributes before purchasing, sellers rely on signals to communicate credibility, authenticity, and quality. Effective signals, which are reliable in shaping buyer perceptions, are typically costly or difficult to imitate.

Within e-commerce research, scholars have frequently drawn on signaling theory to analyze how online sellers and platforms use mechanisms such as certifications, reviews, and guarantees to reduce consumer uncertainty and perceived risk [32]. Empirical evidence confirms that trust signals significantly influence consumers’ perceptions and behaviors: verified reviews and platform labels enhance product credibility, while compensation policies serve as explicit assurances against potential loss (Kim & Peterson, 2017; Stouthuysen et al., 2018) [27,28]. For example, Chevalier and Mayzlin [14] demonstrated how online reviews act as powerful word-of-mouth signals that affect consumer purchase decisions, providing an early foundation for the study of user-generated cues in digital marketplaces.

More recently, the emergence of blockchain as a transparency-enhancing technology introduces new signals that fundamentally differ from conventional cues, relying on technological validation rather than institutional enforcement. This shift opens fertile ground for extending signaling theory by comparing how traditional and technology-based signals function in high-risk environments such as CBEC [25].

2.2. Traditional Authenticity Signals

In CBEC, traditional authenticity signals remain central to building consumer trust, especially when buyers lack familiarity with the seller or product. One prominent institutional signal is platform endorsement, such as self-operation labels or official store badges (e.g., “Tmall Global Supermarket”). These signals represent the platform’s certification of legitimacy and operational reliability, thereby strengthening brand credibility and reducing uncertainty [33,34,35]. Studies also show that such endorsements not only reduce cognitive perceptions of risk but also foster emotional attachment and willingness to pay a premium [36].

A second type of signal is risk-bearing commitments, such as “tenfold compensation for counterfeits” policies or unconditional return guarantees. By explicitly addressing consumer concerns over product quality and post-purchase protection, these commitments provide psychological assurance and encourage transactions in highly uncertain contexts [17,37]. These measures have been found to improve consumer satisfaction, foster loyalty, and increase repeat purchase probability (Li & Liu, 2021; Liu & Chen, 2022) [13,38].

The third key form of authenticity signal is customer reviews, which function as user-generated content providing social proof of product credibility. Review volume, quality, and emotional valence have been shown to influence consumer trust and purchase intention [15,39,40]. However, in CBEC contexts, the prevalence of fake or manipulated reviews raises consumer skepticism and weakens their signaling value. Recent empirical evidence from Tmall Global further demonstrates that while external cues such as reviews significantly shape purchase decisions, their effectiveness diminishes when credibility is questioned [31]. Recent cases of fabricated reviews on leading platforms further challenge their reliability as trust signals, creating an urgent need to re-examine whether consumer reviews are still effective in cross-border markets.

Although these traditional signals play a vital role, they may not fully overcome CBEC’s authenticity challenges. They are vulnerable to manipulation, costly to maintain, and inconsistently enforced; as such, they may fail to provide sufficient reassurance for consumers in high-risk categories such as cosmetics. This limitation underscores the importance of exploring how emerging technology-driven signals, particularly blockchain, can complement or substitute traditional mechanisms.

2.3. Blockchain as an Emerging Signal

Blockchain technology has been increasingly explored as a technology-driven authenticity signal in CBEC. Its core properties—immutability, transparency, and traceability—make it uniquely suited to contexts where consumers are concerned about counterfeit products, supply chain integrity, and data credibility. From a signaling perspective, blockchain generates tamper-proof and auditable records of product origin, production, and distribution, which serve as high-cost, hard-to-fake signals of authenticity [41,42]. Unlike platform-based signals that rely on institutional authority, blockchain provides decentralized verification, thereby enhancing credibility through technical validation [43,44].

Its efficacy has been shown across several sectors. Blockchain makes farm-to-table traceability possible, for example, in the food industry, boosting customer trust in quality and safety [20,21]. By enabling customers to independently confirm the authenticity of premium items, it aids in the fight against counterfeiting [45,46]. By protecting transaction data and guaranteeing compliance, it keeps fake medications out of the pharmaceutical industry’s supply chain [47]. These uses demonstrate how blockchain can function both directly by increasing the legitimacy of technology and indirectly by lowering perceived risk.

Despite these advantages, several barriers hinder blockchain’s signaling effectiveness. Its technical complexity may limit consumers’ understanding of how it ensures authenticity [48]. Moreover, blockchain cannot guarantee data accuracy if the inputs themselves are flawed; garbage in, garbage out remains a critical limitation [24,25]. Consumer skepticism may also arise if blockchain-based features are poorly communicated [49], while low awareness, limited exposure, and privacy concerns further restrict its widespread adoption [26,45]. These challenges indicate that blockchain cannot yet function as a stand-alone solution but may be most effective when combined with traditional authenticity signals. This highlights the importance of investigating multi-signal strategies in CBEC, particularly in sensitive sectors such as cosmetics. Recent empirical studies also highlight blockchain’s role in strengthening consumer trust and purchase intentions in CBEC contexts, while pointing out variations in consumer sensitivity and retailer adoption strategies [46,47,50].

2.4. Research Gaps

Although signaling theory has been widely applied in e-commerce, several important gaps remain in the context of CBEC. Firstly, most studies focus on traditional authenticity signals such as platform labels, customer reviews, and refund policies [27,28]. As such, despite recent calls to examine technology-driven signals in greater depth, there has been limited systematic comparison with blockchain-based mechanisms [46]. Secondly, researchers have previously mainly examined signals in isolation, neglecting how multiple signals may interact or produce substitution and complementarity effects. This omission is noteworthy given emerging evidence that, in CBEC, external cues—such as reviews and platform information—jointly shape consumer decision-making [31]. Thirdly, while mediating mechanisms such as perceived quality and value have been investigated [30], the role of perceived risk—arguably more critical in highly uncertain CBEC contexts—has not been systematically validated, despite recent meta-analytical and review-based evidence emphasizing its decisive role in purchase suppression [45]. Finally, most existing studies rely on survey-based methods, whereas controlled experiments that allow for causal inference remain scarce, particularly in high-risk categories such as cosmetics.

3. Research Hypotheses and Theoretical Model

Building on signaling theory and prior studies examining consumer behavior in CBEC, this study investigates how four authenticity signals—namely blockchain traceability, platform self-operation, customer reviews, and compensation guarantees—shape purchase intention. We specifically look at how they affect consumer decision-making, both directly and indirectly, through perceived risk, a technique that is especially important in highly uncertain CBEC situations like cosmetics.

3.1. Direct Effects of Authenticity Signals on Purchase Intention (H1a–H1d)

Authenticity signals are central mechanisms for reducing information asymmetry between sellers and consumers [11]. In CBEC, consumers often face uncertainty regarding product authenticity, quality, and transaction safety due to the geographical and institutional distance of overseas sellers. Prior research highlights that signals which are observable, credible, and difficult to imitate can directly enhance consumer confidence and increase purchase likelihood [19,32].

O1 (Direct effects).

Authenticity signals can directly influence purchase intention.

Accordingly, we tested direct paths between each signal and purchase intention (H1a–H1d).

3.1.1. Blockchain Traceability

Blockchain offers transparent, unchangeable records of product origin, logistics, and distribution, introducing a technology-based authenticity signal. Blockchain applications in supply chains have been demonstrated to increase perceptions of authenticity, decrease fraud, and improve traceability [20,25]. As such, by allowing customers to confirm product history using tamper-proof data, it is anticipated to provide an immediate boost to purchase intention for CBEC cosmetics.

H1a.

Blockchain traceability has a direct, positive effect on purchase intention.

3.1.2. Platform Self-Operation

Strong platform endorsement and operational control are shown in institutional signals such as platform self-operation (e.g., “Tmall Global Supermarket”). Better after-sales support, more stringent product procurement, and a decreased danger of counterfeit products are all linked to self-operated businesses [10]. Customers are therefore more likely to view self-operation as a reliable assurance of product quality, which, in turn, raises their propensity to buy.

H1b.

Platform self-operation has a direct, positive effect on purchase intention.

3.1.3. Customer Reviews

Customer reviews act as social proof, conveying others’ consumption experiences and helping to resolve information asymmetry in online transactions. Prior research shows that positive reviews can enhance credibility and increase consumers’ willingness to buy [51]. While, in CBEC, concerns about manipulation may attenuate this effect [51], evidence still largely predicts a positive direct association.

H1c.

Customer reviews have a positive, direct effect on purchase intention.

3.1.4. Compensation Guarantees

Compensation mechanisms such as the “fake one, pay ten” policy provide explicit institutional risk-sharing, bolstering sellers’ confidence in product authenticity. Such guarantees not only reduce consumers’ perceived financial loss but also strengthen their confidence in making a purchase [17,37]. Accordingly, compensation commitments are hypothesized to positively influence purchase intention in CBEC cosmetics.

H1d.

Compensation guarantees have a positive, direct effect on purchase intention.

3.2. Mediating Role of Perceived Risk (H2a–H2d)

Perceived risk is widely recognized as a critical mechanism through which authenticity signals influence consumer behavior [52]. In CBEC contexts, uncertainty regarding authenticity, logistics reliability, and transaction safety is heightened compared to domestic e-commerce [8].

O2 (Mediation).

The effects of authenticity signals on purchase intention are mediated by perceived risk.

Accordingly, we examined each signal as mediated via perceived risk (H2a–H2d): if a signal reduces such risk, consumers’ willingness to buy should increase.

3.2.1. Blockchain Traceability

Blockchain technology reduces consumers’ uncertainty by providing verifiable and tamper-proof supply chain data. Prior research demonstrates that blockchain enhances transparency, traceability, and accountability, thereby reducing fraud risks and alleviating consumer concerns about counterfeit goods [20,25]. In CBEC cosmetics, blockchain-driven traceability is expected to lower perceived risk, which, in turn, increases purchase intention.

H2a.

Perceived risk mediates the relationship between blockchain traceability and purchase intention.

3.2.2. Platform Self-Operation

Platform self-operation serves as an institutional guarantee that the seller adheres to rigorous sourcing, distribution, and after-sales standards. Prior studies show that institutional assurances reduce uncertainty and transaction risks, thus encouraging consumers to engage in online purchases [10,17]. In CBEC, self-operated platforms can reduce consumer concerns about counterfeit or substandard cosmetics, indirectly promoting purchase intention via risk reduction.

H2b.

Perceived risk mediates the relationship between platform self-operation and purchase intention.

3.2.3. Customer Reviews

By supplying firsthand information from other buyers, customer reviews act as social proof in online markets, minimizing uncertainty by delivering experienced insights from other buyers [51]. In many e-commerce contexts, reviews have been shown to lower perceived risk; however, due to customer skepticism regarding authenticity and potential manipulation, in CBEC they may be less helpful [51]. Positive assessments can nonetheless reduce risk and, when regarded as trustworthy, indirectly increase purchase intention.

H2c.

It is perceived risk that mediates the relationship between customer reviews and intention to buy.

3.2.4. Compensation Guarantees

Compensation commitments such as the “fake one, pay ten” policy provide consumers with explicit financial assurance against counterfeit products. These mechanisms transfer risk to sellers or platforms, thus directly lowering the perceived financial and psychological risks on the part of consumers [37]. In CBEC cosmetics, compensation guarantees are expected to significantly reduce perceived risk and thereby increase consumers’ likelihood of purchasing.

H2d.

Perceived risk mediates the relationship between compensation guarantees and purchase intention.

3.3. Moderating Effects of Signal Interactions (H3a–H3c)

Signals can interact, and the presence of one cue may amplify or dampen another [11]. In CBEC, blockchain often coexists with traditional assurances (platform self-operation, customer reviews, compensation guarantees). As such, it is important to assess whether blockchain’s impact varies across these conditions, i.e., across institution-based trust devices, social-proof cues, and contractual risk-sharing safeguards [29].

O3 (Moderation).

Consistent with signaling theory’s view that a signal’s marginal diagnosticity is contingent upon the surrounding cue set [11,32], the effect of blockchain traceability depends on traditional assurances (self-operation, reviews, compensation). Accordingly, we specify the following moderation hypotheses (H3a–H3c) to capture these conditional effects.

3.3.1. Platform Self-Operation as a Moderator

Institutional signals such as platform self-operation are perceived as highly credible guarantees. When blockchain traceability is combined with self-operation, its incremental value may be attenuated, as consumers already rely on the institutional trust provided by the platform. Conversely, in the absence of self-operation, blockchain may become more salient as a substitute mechanism for mitigating uncertainty.

Self-operation provides institution-based trust in the form of formal governance and platform-level assurance, reducing perceived risk even before any transaction occurs [11]. When this umbrella is strong, the marginal diagnosticity of an additional technology signal should be lower; when it is absent, users more so rely on hard-to-fake provenance cues.

H3a.

The effect of blockchain traceability on perceived risk and purchase intention is stronger on non-self-operated platforms than on self-operated equivalents.

3.3.2. Customer Reviews as a Moderator

Customer reviews provide social proof [14]; however, their credibility is often questioned in CBEC contexts due to manipulation concerns [53]. When positive reviews are absent, blockchain traceability becomes a critical assurance mechanism. However, when abundant positive reviews are present, consumers may rely more on peer feedback, thereby weakening blockchain’s incremental role [54].

H3b.

The impact of blockchain traceability on perceived risk and purchase intention is stronger when customer reviews are absent than when they are present.

3.3.3. Compensation Guarantees as a Moderator

Compensation commitments act as explicit financial safeguards, directly reducing consumer perceptions of risk. Classic signaling work views warranties/guarantees as costly, credible signals that transfer risk and that can therefore act as substitutes for other credibility cues [32] In online settings, institution-based assurances such as guarantees, escrow, and platform policies reliably lower perceived risk and build trust [12]. When compensation guarantees are available, the marginal impact of blockchain should weaken accordingly, because part of the uncertainty has already been alleviated by the guarantee. Conversely, in the absence of guarantees, blockchain becomes the primary assurance of authenticity.

H3c.

The impact of blockchain traceability on perceived risk and purchase intention is stronger when compensation guarantees are absent than when they are present.

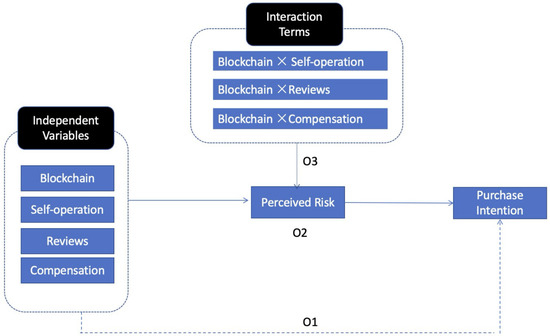

3.4. Theoretical Model

Figure 1 illustrates the proposed conceptual model. Four authenticity signals are used as independent variables: compensation promises, platform self-operation, blockchain traceability, and user reviews. In addition to being a direct result of these signals, perceived risk also acts as a mediator between them and the dependent variable of purchase intention. Thanks to this framework, (1) the direct effects of authenticity signals on purchase intention, (2) the direct effects of authenticity signals on perceived risk, (3) the mediating role of perceived risk between authenticity signals and purchase intention, and (4) the moderating role of traditional signals in influencing the efficacy of blockchain traceability can thus all be empirically tested.

Figure 1.

Conceptual model. O1–O3 are overarching propositions that organize the framework (O1: direct effects; O2: mediation via perceived risk; O3: moderation by traditional assurances—self-operation, reviews, and compensation). Statistical tests are reported for path-level hypotheses H1a–H1d (direct), H2a–H2d (mediation), and H3a–H3c (interactions).

4. Research Methodology

Consistent with the conceptual framework (Figure 1), we organized our empirical tests around three overarching propositions (O1–O3), evaluating path-level hypotheses (H1a–H1d; H2a–H2d; H3a–H3c). O1 concerns direct effects, O2 mediation via perceived risk, and O3 moderation by traditional assurances (self-operation, reviews, and compensation).

4.1. Experimental Design and Stimuli

This study employed an orthogonal experimental design to examine the effects of four authenticity signals—namely blockchain traceability labels, platform self-operation, customer reviews, and compensation guarantees—on perceived risk and purchase intention in the CBEC cosmetics context. Each factor was manipulated at two levels (present versus absent). Figure 2 illustrates an example of the CBEC product page stimulus (Scenario 1, all signals present), with manipulated elements annotated in English. Only participants assigned to Scenario 1 viewed this version, while others saw versions corresponding to their assigned scenario.

Figure 2.

Example stimulus (Scenario 1, all signals present).

The stimuli were simulated CBEC product pages for imported cosmetics. All pages adopted a standardized layout, with variations applied to the authenticity signals: (1) blockchain traceability was presented through a QR code and descriptive text; (2) platform self-operation was indicated by an official “Tmall Supermarket”-style label; (3) positive customer reviews appeared in a dedicated section; and (4) the compensation guarantee (“fake one, pay ten”) was displayed as a badge. Each page was displayed for 45 s to ensure that participants had sufficient time to recognize and process the relevant information.

The orthogonal array reduced the number of scenarios from 16 to 8, which improved design efficiency and minimized unnecessary participant burden at the study level. The design matrix is shown in Table 1.

Table 1.

Orthogonal experimental design with four authenticity signals in the CBEC cosmetics context.

To ensure valid manipulations, a preliminary expert validation was conducted with three scholars specializing in e-commerce and consumer behavior. The experts confirmed that the four authenticity signals were realistic, clearly identifiable, and suitable for the CBEC cosmetics context. Based on their feedback, minor wording adjustments were made to the blockchain and compensation guarantee descriptions for optimal clarity. The 45-s exposure time was determined through preliminary pretests. Although 30 s was sufficient for basic page browsing, extending the duration to 45 s provided participants with more time to fully process the signals while avoiding unnecessary fatigue. This duration, therefore, represents a balanced compromise between adequate information processing and participant efficiency.

Beyond the expert validation used to refine the stimuli, manipulation validity was assessed on participants in the main study. After viewing the assigned page, respondents answered four recognition items—blockchain traceability, platform self-operation, positive reviews, and compensation guarantee—with Yes/No/Not sure options. We pre-specified an exclusion rule: respondents selecting Not sure for any item or misidentifying more than one cue were removed from the analytic sample.

4.2. Participants and Sampling

Participants were recruited through the Jianshu online crowdsourcing platform. To ensure homogeneity and internal validity, the following eligibility criteria were applied:

- Platform credit score ≥ 80;

- Historical task acceptance rate ≥ 80%;

- Female respondents;

- Age between 26 and 30 years;

- Prior CBEC shopping experience.

The selection of young female consumers was based on the sampling options available on the Jianshu crowdsourcing platform, which allows researchers to predefine respondents’ demographic attributes such as gender and age. Among the available age groups, women aged 26–30 were chosen because they represent a core consumer segment in the cosmetics market and are most relevant to the study context. Before participation, participants needed to respond to a preliminary screening item: “Have you previously bought products via CBEC platforms?” Only those that answered “Yes” were included.

A total of 320 questionnaires were distributed evenly and randomly across the eight scenarios (40 per scenario). After data cleaning, which excluded respondents that failed the manipulation check or reported no CBEC shopping experience, 274 valid responses were retained, yielding an effective response rate of 85.6%. Krejcie and Morgan’s [55] sample size determination formula indicates that a sample of approximately 384 is required for large populations. In addition, the SEM literature generally recommends a sample size between 200 and 400 to ensure robust estimation and model stability [56,57].

4.3. Measures

Perceived risk and purchase intention were operationalized using established scales adapted to the CBEC cosmetics context. All constructs were assessed on seven-point Likert-type scales, ranging from 1 (“strongly disagree”) to 7 (“strongly agree”). The measurement items were adapted from validated scales taken from prior studies (see Table 2). A pilot test with 30 respondents confirmed reliability (Cronbach’s α > 0.80) and item clarity.

Table 2.

Measurement items, conceptual definitions, and literature sources.

Perceived risk was defined as consumers’ subjective evaluation of uncertainty, authenticity, and potential financial loss in CBEC cosmetics purchases. Purchase intention was defined as consumers’ likelihood and willingness to purchase the product presented.

4.4. Data Collection

An online questionnaire aligned with the experimental tasks helped us capture the data. Participants were given one of the eight scenarios at random and presented with a product page for consideration for at least 45 s (minimum exposure to discourage inattentive viewing; no upper time limit). Subsequently, the participants completed a questionnaire, which was randomized in order to reduce order effects. As manipulation checks administered to participants in the main study, we asked questions about four recognition items for the cues (blockchain traceability, platform self-operation, positive reviews, and compensation guarantee), presenting Yes/No/Not sure options. We pre-specified an exclusion rule: respondents that chose “Not sure” for any item or misidentified more than one cue were removed. Respondents who misidentified more than one signal were eliminated, as well as those who were unsure.

Of the 320 complete responses received, 274 were considered valid after data cleaning and manipulation check application. The remaining sample size fulfilled the statistical power and SEM requirements, thus confirming the strength of the analysis. All processes followed institutionally set ethical requirements, receiving clearance from the university’s ethics committee. In addition, participants were provided with an informed consent document that detailed their ability to withdraw from participation at any stage without incurring any negative consequences. In addition, participants were also assured that their identities would not be recorded, ensuring anonymity and confidentiality.

4.5. Analytical Strategy

We followed a two-layer testing plan aligned with the framework presented in Figure 1: (i) direct paths (addressing O1) and mediation via perceived risk (addressing O2), and (ii) moderation by traditional assurances on blockchain effects (addressing O3), plus a nested model comparison for model selection.

Mediation (O2). We tested mediation by reporting the direct effect c′, the indirect effect ab through perceived risk, the total effect c′ + ab, and the percentage mediated PM = ab/(c′ + ab). The significance of ab was determined via bias-corrected bootstrap CIs with 5000 resamples; as a robustness check, we additionally report the Sobel z.

Moderation (O3). We followed a uni-directional specification aligned with our technology-led focus: traditional cues (self-operation, reviews, and compensation) were modeled as moderators of blockchain effects on perceived risk and purchase intention. Reciprocal tests were scoped for future work, since our orthogonal design and power analysis were optimized for blockchain-conditional tests rather than for both moderation directions.

For model selection, we contrasted four nested specifications using global fit indices and information criteria: M0 (CFA only), M1 (direct effects; no mediation/moderation), M2 (+mediation via perceived risk), and M3 (+interactions: Blockchain × Self-operation/Reviews/Compensation). We report χ2/df, CFI, TLI, RMSEA, SRMR, AIC, and BIC (Table A1). Accounting for parsimony, lower AIC/BIC indicate better relative fit; absolute-fit thresholds followed common guidelines (e.g., CFI/TLI ≥ 0.95, RMSEA ≤ 0.06–0.08, SRMR ≤ 0.08).

5. Results

5.1. Common Method Bias

We first tested whether a single shared method could account for covariation among indicators (see Table 3). A one-factor CFA did not adequately fit the data (χ2 (104) = 445.216, RMSEA = 0.109, CFI = 0.935, TLI = 0.925, SRMR = 0.039), whereas separating indicators into perceived risk and purchase intention yielded an excellent fit (χ2 (13) = 21.290, RMSEA = 0.048, CFI = 0.995, TLI = 0.992, SRMR = 0.018). The difference test demonstrated a strong preference for the two-factor solution (Δχ2 (91) = 423.926, p < 0.001); thus, material CMB is unlikely.

Table 3.

Common method bias test results.

5.2. Descriptive Statistics

Of the 320 questionnaires distributed, 302 valid responses were collected (response rate = 94.4%). After excluding participants who failed the signal recognition check or lacked CBEC shopping experience, 274 valid responses remained for analysis, yielding an effective rate of 85.6%.Table 4 presents the sample characteristics. All respondents were female, aged 26–30, and had prior CBEC shopping experience, which aligns with the study’s targeted demographic group. Regarding monthly income, most participants reported earnings between CNY 4000 and 7999 (72.2%), and more than 60% indicated purchasing imported cosmetics at least seven times a year. These characteristics confirm that the sample represents the primary consumer group of interest in China’s CBEC cosmetics sector.

Table 4.

Sample characteristics (N = 274).

5.3. Measurement Model Evaluation

Before testing structural relations, we assessed whether the indicators adequately capture their latent constructs [60]. Following established guidelines [61,62], we examined reliability, convergent and discriminant validity, and overall measurement model fit.

5.3.1. Composite Reliability and Convergent Validity

To evaluate the adequacy of our measurement model, we conducted confirmatory factor analysis (CFA) in Mplus (Version 8.3) using the maximum likelihood estimation (MLE) method. Reliability was examined through Cronbach’s alpha and composite reliability (CR), while convergent validity was assessed by inspecting standardized factor loadings and the average variance extracted (AVE). This multi-criteria assessment ensured that the constructs demonstrated both internal consistency and convergent validity, thereby meeting the prerequisites for subsequent structural equation modeling (SEM).

Following widely accepted benchmarks, standardized factor loadings should ideally be ≥0.70 [61]; however, in exploratory contexts, values ≥ 0.50 are considered acceptable [63]. Cronbach’s α values ≥ 0.70 are typically regarded as the minimum threshold for adequate reliability [64]. Similarly, composite reliability (CR) values ≥ 0.70 indicate satisfactory internal consistency [60], while an AVE ≥ 0.50 suggests that the construct captures more than half of the variance of its observed indicators [62]. These criteria are frequently cited in the SEM literature, providing a foundation for judging measurement model adequacy [62,65]. Table 5 reports standardized factor loadings ranging from 0.851 to 0.939, all above the commonly suggested cut-off. Both constructs achieved Cronbach’s alpha values higher than 0.90, with composite reliability (CR) also surpassing 0.90 and average variance extracted (AVE) above 0.80. Taken together, these indicators provide strong evidence that the measurement scales demonstrate high internal consistency, robust reliability, and satisfactory convergent validity.

Table 5.

Reliability and validity measurement construct statistics.

As reported in Table 5, standardized factor loadings ranged from 0.851 to 0.939, which are well above the recommended cut-off and provide strong support for item reliability. Both constructs achieved Cronbach’s alpha values greater than 0.90, reflecting excellent internal consistency. Composite reliability (CR) values also exceeded 0.90, further confirming the robustness of the scales. In addition, the AVE values were all above 0.80, clearly surpassing the 0.50 benchmark and demonstrating that the constructs explain the majority of the variance in their respective indicators.

Taken together, these results provide compelling evidence that the measurement scales demonstrate high internal consistency, robust reliability, and satisfactory convergent validity. The consistently strong performance across all metrics aligns with the recommended thresholds in prior methodological studies [62,65], thereby confirming that the constructs are well-specified and suitable for subsequent structural modeling.

5.3.2. Discriminant Validity

We define discriminant validity as the degree to which constructs within a model remain conceptually and empirically distinct [65]. To assess this property, we employed two established techniques. Firstly, following the Fornell–Larcker criterion, we compared the square root of each construct’s average variance extracted (AVE) with its correlations with other constructs [62]. As reported in Table 6, the AVE square roots for perceived risk (0.906) and purchase intention (0.928) were both higher than their inter-construct correlation (−0.775), thereby confirming discriminant validity.

Table 6.

Discriminant validity.

Second, we adopted the Heterotrait–Monotrait Ratio (HTMT) [66] to evaluate the constructs’ discriminant validity. HTMT compares correlations across different constructs (heterotrait) with those within the same construct (monotrait), thereby indicating how well each is distinguished from others. Following established guidelines, HTMT values above 0.85–0.90 may signal insufficient discriminant validity [67,68]. In our data (see Table 7), the HTMT value between perceived risk and purchase intention was 0.834—below the conservative 0.85 threshold—indicating adequate discriminant validity. We also checked collinearity, finding tolerance > 0.10 and VIF < 5, indicating no multicollinearity.

Table 7.

Heterotrait–Monotrait Ratio.

5.3.3. Model Fit Indices

Using Mplus (Version 8.3) with data from 274 valid responses, the adequacy of the overall measurement model was further examined through a set of widely recognized indices. Evaluating multiple indices rather than a single statistic is essential, as each provides complementary insights into how well the model reproduces the observed covariance matrix [69].

Though it is known to be highly sensitive to sample size, the chi-square (χ2) statistic is the most traditional indicator of model fit. For this reason, researchers typically report the χ2/df ratio instead of relying solely on the raw χ2 value. A ratio of less than 3 is generally taken as evidence of a good fit, while values under 5 may still be considered acceptable in large-sample contexts [69].

The Comparative Fit Index (CFI) evaluates the improvement in the hypothesized model relative to a null model, where all variables are assumed to be uncorrelated. CFI values above 0.90 are usually interpreted as acceptable, with values greater than 0.95 indicating an excellent fit. Alongside this, the Tucker–Lewis Index (TLI)—sometimes referred to as the Non-Normed Fit Index—adjusts for model complexity and the number of estimated parameters. Like the CFI, TLI values above 0.90 represent adequate fit, and values beyond 0.95 reflect a very good model specification.

By penalizing model complexity and taking sample size into account, the Root Mean Square Error of Approximation (RMSEA) provides an absolute measure of approximate fit. RMSEA values below 0.05 are indicative of a close fit, values between 0.05 and 0.08 reflect reasonable approximation error, and values greater than 0.10 suggest poor model fit [70].

The Standardized Root Mean Square Residual (SRMR) complements the above indices by capturing the standardized difference between the observed and predicted correlations. Because it is based on residuals, the SRMR is particularly useful for detecting localized areas of misfit. Values below 0.08 are generally considered acceptable [71].

As presented in Table 8, the proposed model satisfied all recommended benchmarks: χ2 = 97.044, χ2/df = 2.488, CFI = 0.968, TLI = 0.959, RMSEA = 0.074, and SRMR = 0.057. Collectively, these indices demonstrate that the measurement model provides an adequate to excellent fit with the observed data. This confirmation of model adequacy establishes a strong empirical basis for proceeding with structural equation modeling and hypothesis testing.

Table 8.

Structural equation model fit indices.

A nested comparison of alternative structural specifications is reported in Section 5.4 and Appendix A Table A1.

5.4. Model Comparison and Selection

Appendix A Table A1 reports the fit of four nested specifications. The direct-only structural model (M1) fits poorly (χ2/df = 7.46; RMSEA = 0.153; SRMR = 0.297; CFI = 0.846; TLI = 0.802), indicating that a purely direct structure is inadequate. Adding mediation (M2) yields a substantial improvement (χ2/df = 1.06; CFI = 0.999; TLI = 0.998; RMSEA = 0.015; SRMR = 0.019) and markedly lower information criteria (ΔAIC = −252.04; ΔBIC = −233.97 vs. M1), supporting the inclusion of perceived risk as a mediator. Adding interactions (M3) further improves absolute fit (χ2/df = 1.02; CFI = 1.000; TLI = 0.999; RMSEA = 0.008; SRMR = 0.019). AIC favors M3 over M2 (ΔAIC = −4.21), whereas BIC slightly favors M2 (ΔBIC = +17.47) due to the stronger parsimony penalty. Guided by theory (testing blockchain’s boundary conditions) and the improved absolute fit, we retain M3 for hypothesis testing; importantly, all mediation inferences remain the same under M2, indicating robustness.

5.5. Structural Model Analysis

5.5.1. Direct Effects

Table 9 summarizes the SEM path analysis, which shows that the associations between authenticity signals and purchase intention differ across types. More specifically, blockchain traceability had a significant positive influence on purchase intention (β = 0.111, p = 0.007), indicating that technology-driven transparency mechanisms can increase consumers’ willingness to buy in CBEC cosmetics contexts.

Table 9.

Path hypothesis testing.

In contrast, the effect of platform self-operation on purchase intention was not statistically significant (β = 0.074, p = 0.070). Although such signals may provide institutional assurance, their direct influence on consumers’ purchase decisions was not evident in this study.

Likewise, customer reviews did not produce a significant direct impact on purchase intention (β = 0.022, p = 0.594), suggesting that while reviews can serve as social proof in many e-commerce settings, their effectiveness in CBEC cosmetics may be weakened by concerns about review authenticity.

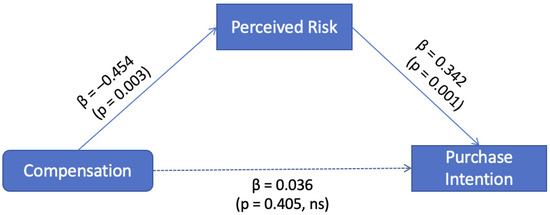

Compensation guarantees likewise showed no significant influence on purchase intention (β = 0.036, p = 0.405). Although such guarantees represent institutional mechanisms of risk transfer, their presence alone does not appear sufficient to directly motivate consumer purchase behavior in this context.

5.5.2. Mediation Effect Testing

Perceived risk was examined as a mediator linking authenticity signals to purchase intention. Direct, indirect, and total effects were computed as c′, ab, and c′ + ab, respectively. Following established mediation procedures, indirect effects were estimated as the product of the paths (a × b) from authenticity signals to purchase intention via perceived risk [72,73]. Significance was assessed using bias-corrected bootstrapping with 5000 resamples; confidence intervals excluding zero indicate statistical significance. For inference convergence, we additionally report the Sobel z test and a Monte Carlo (distribution-of-the-product) check, which yielded the same significance pattern across signals [74,75]. To highlight relative magnitudes, we also report the proportion mediated (PM = ab/(c′ + ab)) and the ab/c′ ratio where interpretable.

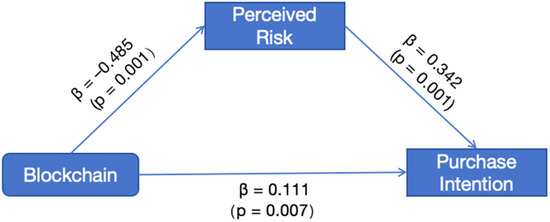

As presented in Table 10, blockchain traceability exhibited a significant indirect effect on purchase intention via perceived risk (β_indirect = 0.166, p = 0.001, 95% CI [0.204, 0.805]; Sobel z = 3.192), while the direct path remained positive (c′ = 0.111, p < 0.01). The indirect effect exceeded the direct equivalent (PM = 0.599; ab/c′ ≈ 1.50), indicating partial mediation and supporting H2a.

Table 10.

Mediation test results: perceived risk as a mediator between authenticity signals and purchase intention.

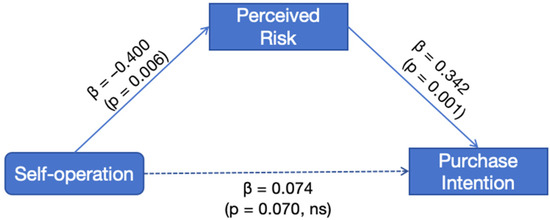

As shown in Table 10, platform self-operation exhibited a significant indirect effect via perceived risk (β_indirect = 0.138, p = 0.006, 95% CI [0.126, 0.699]; Sobel z = 2.755), whereas the direct path was not significant (c′ = 0.074, n.s.). The mediated component dominates (PM = 0.651; ab/c′ ≈ 1.86, indicating indirect-only mediation and lending support to H3b: institutional assurances lower perceived risk, thereby promoting purchase intention.

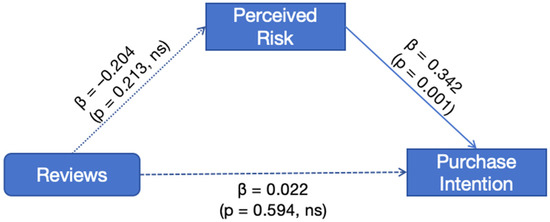

In contrast, customer reviews showed no significant mediation via perceived risk (β_indirect = 0.067, p = 0.213, 95% CI [−0.123, 0.525]; Sobel z = 1.245), thus failing to support H3c. Because the indirect effect is non-significant, PM and ab/c′ab/c′ab/c′ are not interpreted, a pattern consistent with growing consumer skepticism about review authenticity in CBEC contexts.

Finally, compensation guarantees exhibited a significant indirect effect via perceived risk (β_indirect = 0.156, p = 0.003, 95% CI [0.175, 0.767]; Sobel z = 3.007), while the direct path was not significant (c′ = 0.036, n.s.). The mediated pathway dominates (PM = 0.812; ab/c′ ≈ 4.33, indicating indirect-only mediation and confirming H3d. This highlights that explicit institutional risk-bearing commitments lower perceived risk, thereby increasing purchase intention.

Building on Table 10, we detail each signal’s mediation pattern below.

- Blockchain Traceability.

As shown in Table 10 (see Figure 3), blockchain traceability exhibited a significant indirect effect on purchase intention via perceived risk (β_indirect = 0.166, p = 0.001, 95% CI [0.204, 0.805]; Sobel z = 3.192), while the direct path remained positive (c′ = 0.111, p < 0.01). The indirect effect exceeded the direct equivalent (PM = 0.599; ab/c′ ≈ 1.50ab/c′\approx 1.50ab/c′ ≈ 1.50), indicating partial mediation and supporting H2a.

Figure 3.

The mediating role of perceived risk in the relationship between blockchain traceability and purchase intention.

- Platform Self-Operation.

As shown in Table 10 (see Figure 4), platform self-operation exhibited a significant indirect pathway via perceived risk (β_indirect = 0.138, p = 0.006, 95% CI [0.126, 0.699]), while the direct effect was not significant (c′ = 0.074, p = 0.070, n.s.). The mediated component dominated (PM = 0.651; ab/c′ ≈ 1.86), indicating indirect-only mediation and supporting H2b: platform-backed operational assurances lower perceived risk, thereby promoting purchase intention.

Figure 4.

The mediating role of perceived risk in the relationship between platform self-operation and purchase intention.

- Customer Reviews.

In contrast, customer reviews showed no significant mediation via perceived risk (β_indirect = 0.067, p = 0.213, 95% CI [−0.123, 0.525]; Sobel z = 1.245), thus failing to support H2c. Because the indirect effect is non-significant, PM and ab/c′ab/c′ab/c′ are not interpreted, a pattern consistent with growing consumer skepticism about review authenticity in CBEC cosmetics (see Figure 5).

Figure 5.

The mediating role of perceived risk in the relationship between customer reviews and purchase intention.

- Compensation Guarantee.

Compensation commitments yielded a significant indirect effect via perceived risk (β_indirect = 0.156, p = 0.003, 95% CI [0.175, 0.767]; Sobel z = 3.007), while the direct path was not significant (c′ = 0.036, n.s.). The mediated pathway dominated (PM = 0.812; ab/c′ ≈ 4.33) indicating indirect-only mediation and supporting H2d (see Figure 6).

Figure 6.

The mediating role of perceived risk in the relationship between compensation guarantee and purchase intention.

5.5.3. Moderation Analysis: Blockchain Effectiveness Boundary Conditions

To further test blockchain effectiveness boundary conditions, moderation analyses were conducted with platform self-operation, customer reviews, and compensation guarantees as moderators. The conditional indirect effects are reported in Table 11, with the corresponding visualizations presented in Figure 7. This two-step reporting separates the formal interaction test from the more descriptive conditional effects.

Table 11.

Conditional indirect effects of blockchain on purchase intention via perceived risk under different moderator conditions.

Figure 7.

Conditional effects of blockchain under different moderator conditions. Panels (a–f) present total and decomposed effects across platform self-operation, customer reviews, and compensation guarantees. Bars indicate standardized coefficients, with significance codes as follows: ns = not significant.

- (a)

- H3a: Self-operation

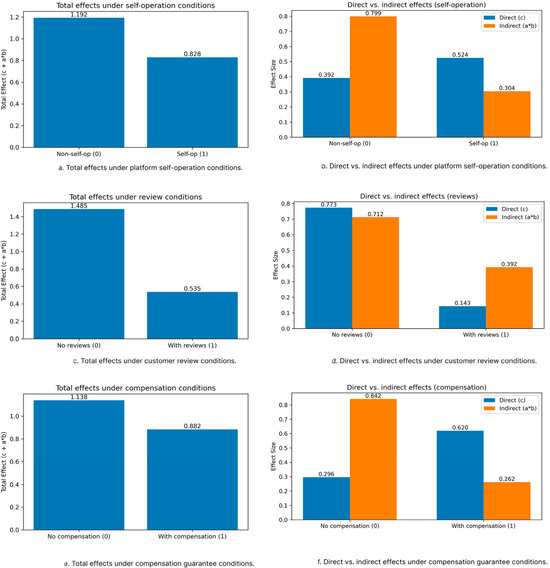

As shown in Table 11 (simple-slope results), under the non-self-operated platform condition (0), blockchain traceability significantly reduces perceived risk (simple slope a = −0.885, p < 0.001), yielding a significant total effect on purchase intention (c + ab = 1.192, p < 0.001). Under the self-operated platform condition (1), the simple slope weakens and becomes non-significant (a = −0.337, n.s.). In this case, purchase intention is more affected by the direct path (c = 0.524, p < 0.05). Consistently, the product-term test shows that Blockchain × Self-operation is positive but only marginally significant (β = 0.189, SE = 0.119, z = 1.594, p = 0.111; StdYX), indicating a weakening tendency rather than a definitive interaction (see Figure 7a,b; interaction coefficients summarized in Table 12).

Table 12.

Interaction terms (product-term tests) on perceived risk.

- (b)

- H3b: Reviews

In the no-review condition (0), blockchain significantly reduces risk and increases purchase intention (total effect = 1.485, p < 0.001); when reviews are present (1), the total effect shrinks markedly (=0.535, p < 0.05) and the indirect effect is only marginal (†). The corresponding product-term test shows that Blockchain × Reviews is non-significant (β = 0.158, SE = 0.174, z = 0.908, p = 0.364; StdYX); we therefore treat this moderation as directional evidence to be interpreted with caution (see Figure 7c,d; see Table 12).

- (c)

- H3c: Compensation

In the no-compensation-guarantee condition (0), blockchain’s risk-suppressing effect is strongest and the total effect is significant (=1.138, p < 0.001); when a compensation guarantee is present (1), the effect weakens and relies more on the direct component (total effect = 0.882, p < 0.01). The product-term test indicates that Blockchain × Compensation is marginally significant (β = 0.221, SE = 0.133, z = 1.658, p = 0.097; StdYX), again suggesting attenuation that does not reach conventional significance thresholds (see Figure 7e,f; see Table 12).

6. Discussion

6.1. Summary of Key Findings

This research aimed to examine how the four authenticity signals of blockchain traceability, self-operated platforms, customer reviews, and compensation commitments influence purchase intention within the CBEC cosmetics industry, with perceived risk as a potential mediating factor.

Firstly, purchase intention is significantly influenced by blockchain traceability (β = 0.111, p < 0.01), lending support to H1a. However, no significant direct effects were established for self-operated platforms, customer reviews, and compensation guarantees (H1b, H1c, and H1d).

Secondly, perceived risk is significantly diminished by blockchain self-operation and compensation guarantees, while customer reviews have no effect. Thirdly, mediation analyses demonstrated that perceived risk was the mediating factor for the effects of blockchain self-operation and compensation guarantees on purchase intention. Notably, purchase intention is influenced by blockchain traceability through direct and indirect pathways, highlighting its role as a signaling mechanism.

Lastly, moderation analyses suggest that blockchain’s efficacy appears stronger in low-trust settings—on non-self-operated platforms without reviews or reimbursement assurances—where total effects are largest (1.192, 1.485, and 1.138, all p < 0.001 from conditional effects). However, product-term tests (Table 12) did not reach conventional significance (α = 0.05) for H3a–H3c, indicating that these patterns should be interpreted as directional (attenuating/diminishing returns) rather than definitive interactions. In other words, while some direct impacts remain sizable, blockchain’s marginal contribution tends to shrink when traditional assurances are present.

6.2. Theoretical Implications

These findings extend signaling theory in several ways. Firstly, they demonstrate that not all authenticity signals operate through the same mechanisms. Blockchain functions as both a direct and indirect signal, whereas self-operation and compensation guarantees work by lowering risk perceptions indirectly. This diverges from earlier studies that typically regarded signals as uniformly indirect mechanisms of reducing uncertainty [32]. In addition, our results suggest that signaling theory can be enriched by incorporating insights from transaction cost economics. By reducing monitoring and verification costs, blockchain may serve not only as a signal but also as an institutional mechanism that lowers the overall market exchange cost. This dual role highlights the need to expand the boundaries of signaling theory from purely communicative functions to include efficiency-enhancing roles in digital markets. Importantly, the interaction terms were not significant at α = 0.05 (Table 12); as such, the moderation patterns should be interpreted as suggestive rather than conclusive.

Secondly, our results highlight the centrality of perceived risk as a mediating mechanism in CBEC. While prior studies emphasized perceived quality or trust [30], our findings show that, in high-risk categories such as cosmetics, reducing risk is a more immediate determinant of purchase intention. In particular, our results differ from those of Treiblmaier and Garaus [30], who reported a full mediation model in the food supply chain: in their study, blockchain enhanced purchase intention only indirectly through perceived quality, with no significant direct effect. In contrast, our study identifies a partial mediation structure in CBEC cosmetics, where blockchain not only reduces perceived risk by indirectly increasing purchase intention, but also exerts a direct effect. This contrast underscores the importance of product category context: in food, consumers prioritize quality assurance, whereas in cosmetics, concerns about counterfeiting and product safety render risk reduction the dominant pathway. Further extending this logic to luxury goods, blockchain may act as a credibility enhancer tied to exclusivity, while in pharmaceuticals it may function as a safeguard against life-threatening risks. This product-specific heterogeneity demonstrates that signaling theory must be contextualized within category-specific consumer priorities, which opens up new avenues for comparative studies across industries.

Thirdly, the insignificance of customer reviews raises theoretical questions about the erosion of UGC as a trust signal. Whereas earlier work identified reviews as strong predictors of purchase behavior [15,39], our findings suggest that their signaling value may be contextually limited in cross-border settings, where skepticism regarding authenticity is high. This points to the possibility of a broader theoretical shift: signals originating from consumers (UGC) may be losing their relative strength compared with institutionally validated signals such as blockchain. In an era where fake reviews and manipulated ratings are pervasive, authenticity signals backed by technological or contractual enforcement may become the dominant drivers of trust. Future signaling theory research should therefore consider the dynamic evolution of signal credibility, recognizing that signal effectiveness may change over time depending on technological, institutional, and cultural developments.

Finally, the moderation patterns contribute to signaling theory by indicating possible substitution/diminishing returns between blockchain and traditional signals. When institutional (self-operation), contractual (compensation), or social (reviews) assurances are absent, blockchain seems to act as a “safeguard signal,” compensating for missing credibility cues; when these are present, blockchain’s marginal impact declines. However, because the product-term tests for H3a–H3c were not significant (Table 12), we frame this as a directional refinement rather than a definitive interaction, consistent with Spence’s view that signal value depends on the broader signaling environment. Overall, our study underscores how authenticity signals are heterogeneous and interdependent, even if their statistical interactions are not always detected. Furthermore, we did not test the inverse direction, i.e., whether social proof (reviews) changes in effectiveness when blockchain is present (vs. absent). Our orthogonal design and power analysis were optimized for blockchain-conditional tests, rather than for both directions of moderation (see Section 4.5). We therefore view reciprocal moderation as theoretically informative and recommend it as a research avenue for future studies that are adequately powered for symmetrical tests.

6.3. Managerial Implications

Our findings imply two platform archetypes requiring different portfolios of authenticity signals, with blockchain’s main effect robust across contexts even though formal interaction tests were not significant. For emerging or low-trust platforms—typically with a high share of third-party sellers and weaker brand equity—ex ante verifiability should be the first line of defense. Blockchain traceability offers the largest marginal reduction in perceived risk and the greatest boost for purchase intention, particularly when other assurances are weak or absent. A pragmatic rollout would be to prioritize high-risk SKUs and sellers, implement one-click verification with a transparent provenance timeline, and link fast-track compensation to completed on-chain checks; when reviews are sparse, the product page should foreground a combined traceability + guarantee badge to substitute for this missing social proof. For mature or high-trust platforms with sizeable self-operation and strong reputations, blockchain is best positioned as an enhancement rather than as the primary signal. Selective batch-level coverage controls unit costs while preserving credibility in sensitive or high-value categories; reviews remain important but should be tightly governed (e.g., “verified purchase” and, where applicable, “verified via traceability” tags) so that experience feedback is distinguished from authenticity claims.

Order of investment and economics: In low-trust settings, expected returns typically rank as follows: blockchain traceability → compensation guarantees → self-operation → review curation. In high-trust settings, review governance and self-operation move up in priority, while blockchain becomes a targeted tool for categories where authenticity is pivotal. Economically speaking, blockchain involves front-loaded, asset-building costs, whereas compensation is a post-event expense with the potential for abuse and adjudication frictions; in price-sensitive categories, low prices plus an accessible guarantee can raise first-purchase conversion. However, repeat purchases hinge on verifiable rather than purely contractual signals.

Repositioning reviews: Without blockchain, the visibility and weight of credible reviews and curated third-party tests should be increased to substitute for missing traceability; with blockchain, reviews should be shifted toward usage and performance and marked as coming from traceability-verified buyers to saliently divide roles.

Execution and measurement: Risk-perception metrics (verification click-through and completion, conversion uplift after verification, share of counterfeit-related complaints), unit economics (on-chain cost per item, compensation cost as %GMV, fraudulent-claim rate), and loyalty indicators (repeat-purchase for traceable items, add-to-cart/save rates, NPS, positive word-of-mouth) should be tracked. To diagnose substitution vs. complementarity between signals, A/B/C tests should be run on matched items (review-salient page vs. blockchain-salient page vs. combined page) and both first- and second-purchase outcomes compared.

Presentation matters (insights from prior work): Finally, diverging from the authors of [30], we suggest that how blockchain is presented is consequential: their food-sector study reported indirect-only effects (no significant direct path). In cosmetics, however, we find a partial-mediation structure. This difference may reflect category priorities and signal format (QR-only vs. QR code plus textual explanation), implying that effectiveness is maximized when presentation is simple, interactive, and aligned with category-specific concerns.

6.4. Limitations and Future Research Directions

The limitations of this study open up avenues for further inquiry. Firstly, the sample was restricted to female consumers aged 26–30 with CBEC shopping experience, limiting our study’s generalizability. Future research should test more diverse demographics and cross-cultural samples. Secondly, the study relied on experimental scenarios and self-reported purchase intentions. The incorporation of field experiments or transaction-level data could provide stronger evidence of real consumer behavior. Thirdly, although four major signals were examined, other factors such as brand reputation, third-party certifications, or logistics performance were not included. Future studies could explore interactions between blockchain and these alternative signals. Fourthly, the moderation findings highlight the need to explore signal substitution and complementarity further. Future research could adopt multi-group analysis to examine whether blockchain’s role differs across platform types, product categories, or cultural contexts. Longitudinal designs may also clarify whether the erosion of review credibility is temporary or structural. Finally, because our moderation design was uni-directional in construction, and because statistical power was optimized for blockchain-conditional tests (see Section 4.5), future research should employ adequately powered, symmetrical designs to detect reciprocal moderation (e.g., reviews × blockchain presence) and compare substitution versus complementarity across categories.

7. Conclusions

This study investigates when a technology signal (blockchain traceability) outperforms traditional cues in cross-border cosmetic e-commerce. Three results stand out. O1 (Direct effects): Blockchain is the only signal with a significant direct effect on purchase intention; self-operation and compensation do not show reliable direct effects, and reviews show no consistent effect.

O2 (Mediation): Perceived risk is the central mechanism. While blockchain also boosts purchase intention indirectly by lowering risk, self-operation and compensation influence intention only via risk reduction; reviews, however, do not show a mediating effect.

O3 (Moderation): Blockchain’s impact is context-dependent; it is strongest when traditional assurances are weak or absent (non-self-operated platforms, no reviews, no compensation) and its marginal contribution shrinks when such safeguards are present, indicating substitution rather than simple complementarity.

Theoretically, these findings refine signaling theory by demonstrating the heterogeneity of authenticity signals (direct vs. indirect pathways), establishing perceived risk as a central mediator in CBEC cosmetics and highlighting that a signal’s value depends on the broader signaling environment. Practically, blockchain should be deployed as the primary signal where trust is thin and redeployed as a focused credibility booster where institutional safeguards are strong; the overall signal portfolio should be tailored to the platform’s maturity and the product category’s authenticity risk profile.

While limitations concerning sample composition and experimental design remain, such shortcomings open up avenues for future work using more diverse populations, field or transactional data, and additional signals (e.g., brand reputation, third-party certifications). Longitudinal study designs could also assess whether the waning signaling value of reviews is temporary or structural across product categories.

Author Contributions

Conceptualization, X.L.; methodology, X.L.; formal analysis, X.L.; investigation, X.L.; data curation, X.L.; writing—original draft preparation, X.L.; writing—review and editing, A.Y.D.; supervision, A.Y.D. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

The study was conducted in accordance with the Declaration of Helsinki. According to the policies of the Human Research Ethics Committee, Research Administration Center, Chiang Mai University (CMU-HREC), formal ethical approval was waived because the survey was anonymous, did not collect personal identifiers, and posed no more than minimal risk to participants.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data that support the findings of this study are available on request from the corresponding author. The data are not publicly available due to privacy or ethical restrictions.

Conflicts of Interest

There are no conflicts of interest to declare.

Appendix A

Table A1.

Nested-model comparison and global fit indices (SEM).

Table A1.

Nested-model comparison and global fit indices (SEM).

| Model | Description | χ2/df | CFI | TLI | RMSEA | SRMR | AIC | BIC | ΔAIC vs. Prev | ΔBIC vs. Prev |

|---|---|---|---|---|---|---|---|---|---|---|

| M0 | CFA only | 1.64 | 0.995 | 0.992 | 0.048 | 0.018 | 5507.564 | 5587.053 | – | – |

| M1 | Direct effects (no mediation/moderation) | 7.46 | 0.846 | 0.802 | 0.153 | 0.297 | 5722.223 | 5812.551 | – | – |

| M2 | +Mediation (Risk) | 1.06 | 0.999 | 0.998 | 0.015 | 0.019 | 5470.187 | 5578.580 | ↓ 252.04 | ↓ 233.97 |

| M3 | +Interactions (Blockchain × SO/REV/COMP) | 1.02 | 1.000 | 0.999 | 0.008 | 0.019 | 5465.974 | 5596.047 | ↓ 4.21 | ↑ 17.47 |

Note: ↓ = decrease; ↑ = increase. Lower AIC/BIC values indicate better fit.

References

- World Trade Organization. Organisation for Economic Co-Operation and Development. Digital Trade 2023; WTO: Geneva, Switzerland, 2023. [Google Scholar]

- People’s Daily Online. China’s Cross-Border E-Commerce Imports and Exports Hit 2.38 Trillion Yuan in 2023. 2024. Available online: http://en.people.cn/n3/2024/0124/c90000-20126122.html (accessed on 15 August 2025).

- Mitsui Global Strategic Studies Institute. The Expansion of Cross-Border E-Commerce in China. 2021. Available online: https://www.mitsui.com/mgssi/en/report/detail/__icsFiles/afieldfile/2021/12/22/2111c_takahashi_e.pdf (accessed on 15 August 2025).

- Giuffrida, M.; Jiang, H.; Mangiaracina, R. Investigating the relationships between uncertainty types and risk management strategies in cross-border e-commerce logistics. Int. J. Logist. Manag. 2021, 32, 1406–1433. [Google Scholar] [CrossRef]

- Lee, H.; Yeon, C. Blockchain-Based Traceability for Anti-Counterfeit in Cross-Border E-Commerce Transactions. Sustainability 2021, 13, 11057. [Google Scholar] [CrossRef]

- Phamthi, V.A.; Nagy, Á.; Ngo, T.M. The influence of perceived risk on purchase intention in e-commerce—Systematic review and research agenda. Int. J. Consum. Stud. 2024, 48, e13067. [Google Scholar] [CrossRef]

- Wang, C.; Liu, T.; Zhu, Y.; Wang, H.; Wang, X.; Zhao, S. The influence of consumer perception on purchase intention: Evidence from cross-border E-commerce platforms. Heliyon 2023, 9, e21617. [Google Scholar] [CrossRef] [PubMed]

- Forsythe, S.M.; Shi, B. Consumer patronage and risk perceptions in Internet shopping. J. Bus. Res. 2003, 56, 867–875. [Google Scholar] [CrossRef]

- Martins, C.; Oliveira, T.; Popovič, A. Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int. J. Inf. Manag. 2014, 34, 1–13. [Google Scholar] [CrossRef]

- Zhang, X.; Pertheban, T.R. Exploring the Factors Affecting Consumer Trust in Cross-Border E-Commerce: A Comparative Study. Acad. J. Bus. Manag. 2023, 5, 51–57. [Google Scholar]

- Spence, M. Job Market Signaling. Q. J. Econ. 1973, 87, 355. [Google Scholar] [CrossRef]

- Kim, D.J.; Ferrin, D.L.; Rao, H.R. A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decis. Support Syst. 2008, 44, 544–564. [Google Scholar] [CrossRef]

- Quintus, M.; Mayr, K.; Hofer, K.M.; Chiu, Y.T. Managing consumer trust in e-commerce: Evidence from advanced versus emerging markets. Int. J. Retail Distrib. Manag. 2024, 52, 1038–1056. [Google Scholar] [CrossRef]

- Chevalier, J.A.; Mayzlin, D. The effect of word of mouth on sales: Online book reviews. J. Mark. Res. 2006, 43, 345–354. [Google Scholar] [CrossRef]

- Hwang, Y.; Yoo, J. The effects of eWOM volume and valence on consumer decision-making: The moderating role of brand familiarity. Asia Pac. J. Mark. Logist. 2021, 33, 1331–1348. [Google Scholar]

- Luca, M. Reviews, Reputation, and Revenue: The Case of Yelp.com. 2016; NOM Unit Working; Harvard Business School: Boston, MA, USA, 2011. [Google Scholar]

- Järvenpää, S.L.; Tractinsky, N.; Saarinen, L. Consumer Trust in an Internet Store: A Cross-Cultural Validation. J. Comput.-Mediat. Commun. 2006, 5, JCMC526. [Google Scholar] [CrossRef]

- Yuan, M. The Impact of Blockchain Technology on E-Commerce Product Development: Case Studies of Walmart and LVMH. Adv. Econ. Manag. Political Sci. 2024, 109, 137–142. [Google Scholar] [CrossRef]

- Menon, S.; Jain, K. Blockchain Technology for Transparency in Agri-Food Supply Chain: Use Cases, Limitations, and Future Directions. IEEE Trans. Eng. Manag. 2024, 71, 106–120. [Google Scholar] [CrossRef]

- Hastig, G.M.; Sodhi, M.S. Blockchain for Supply Chain Traceability: Business Requirements and Critical Success Factors. Prod. Oper. Manag. 2020, 29, 935–954. [Google Scholar] [CrossRef]

- Kamilaris, A.; Fonts, A.; Prenafeta-Boldú, F.X. The Rise of Blockchain Technology in Agriculture and Food Supply Chains. Trends Food Sci. Technol. 2019, 91, 640–652. [Google Scholar] [CrossRef]

- Duong, C.D.; Nguyen, T.H.; Ngo, T.V.N.; Thanh, T.T.H.; Tran, N.M. Blockchain Technology and Consumers’ Organic Food Consumption: A Moderated Mediation Model of Blockchain-Based Trust and Perceived Blockchain-Related Information Transparency. J. Asia Bus. Stud. 2024, 19, 54–78. [Google Scholar] [CrossRef]

- Pun, H.; Zhang, J.; Zhao, X. The role of blockchain in combating counterfeit luxury products. Decis. Sci. 2021, 52, 1069–1100. [Google Scholar]

- Rejeb, A.; Keogh, J.G.; Treiblmaier, H.; Rejeb, K. Blockchain technology in the food industry: A review of potentials and challenges. Int. J. Prod. Res. 2020, 58, 2142–2162. [Google Scholar]

- Treiblmaier, H. Toward more rigorous blockchain research: Recommendations for writing blockchain case studies. Front. Blockchain 2019, 2, 3. [Google Scholar] [CrossRef]

- Kumar, A.; Liu, R.; Shan, Z. Is blockchain a silver bullet for supply chain management? Technical challenges and research opportunities. Decis. Sci. 2022, 53, 647–671. [Google Scholar] [CrossRef]

- Kim, Y.; Peterson, R.A. A Meta-analysis of Online Trust Relationships in E-commerce. J. Interact. Mark. 2017, 38, 44–54. [Google Scholar] [CrossRef]

- Stouthuysen, K.; Teunis, I.; Reusen, E.; Slabbinck, H. Initial Trust and Intentions to Buy: The Effect of Vendor-Specific Guarantees, Customer Reviews and the Role of Online Shopping Experience☆. Electron. Commer. Res. Appl. 2018, 27, 23–38. [Google Scholar] [CrossRef]

- Pavlou, P.A.; Liang, H.; Xue, Y. Understanding and Mitigating Uncertainty in Online Exchange Relationships: A Principal–Agent Perspective. MIS Q. 2007, 31, 105–136. [Google Scholar] [CrossRef]

- Treiblmaier, H.; Garaus, M. Using blockchain to signal quality in the food supply chain: The impact on consumer purchase intentions and the moderating effect of brand familiarity. Int. J. Inf. Manag. 2023, 68, 102514. [Google Scholar] [CrossRef]

- Fang, M.; Deng, Z.; Guo, J. The effects of external cues on cross-border e-commerce product sales: An application of the elaboration likelihood model. Abbas AF, editor. PLoS ONE. 2023, 18, e0293462. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signaling Theory: A Review and Assessment. J. Manag. 2010, 37, 39–67. [Google Scholar] [CrossRef]

- Kim, R.B.; Yan, C. Effects of Brand Experience, Brand Image and Brand Trust on Brand Building Process: The Case of Chinese Millennial Generation Consumers. J. Int. Stud. 2019, 12, 9–21. [Google Scholar] [CrossRef]

- Kurnia, P.R.; Lepar, P.S.; Sitio, R.P. Marketing Communication Tools, Emotional Connection, and Brand Choice: Evidence From Healthy Food Industry. Int. J. Digit. Entrep. Bus. 2023, 4, 37–48. [Google Scholar] [CrossRef]

- Morhart, F.; Malär, L.; Guèvremont, A.; Girardin, F.; Grohmann, B. Brand Authenticity: An Integrative Framework and Measurement Scale. J. Consum. Psychol. 2014, 25, 200–218. [Google Scholar] [CrossRef]

- Assiouras, I.; Liapati, G.; Kouletsis, G.; Koniordos, M. The Impact of Brand Authenticity on Brand Attachment in the Food Industry. Br. Food J. 2015, 117, 538–552. [Google Scholar] [CrossRef]

- Dwyer, F.R.; Schurr, P.H.; Oh, S. Developing Buyer-Seller Relationships. J. Mark. 1987, 51, 11. [Google Scholar] [CrossRef]

- Liu, Y.; Chen, N. Dynamic Pricing With Money-Back Guarantees. Prod. Oper. Manag. 2022, 31, 941–962. [Google Scholar] [CrossRef]

- Aditya, A.R.; Alversia, Y. The Influence of Online Review on Consumers’ Purchase Intention. GATR J. Manag. Mark. Rev. 2019, 4, 194–201. [Google Scholar] [CrossRef]