Characteristics of the Supply Chain of Tobacco and Tobacco Products: Evidence from Serbia

Abstract

:1. Introduction

- Through excise taxes, the state affects the price of cigarettes, thus collecting revenues and potentially reducing consumption, which implies a reduction in the demand for raw tobacco.

- It determines the game’s rules in this market through the appropriate legal regulation.

- In some cases, its agricultural policy measures affect tobacco production by providing various support to tobacco producers.

- This research examined the entire supply chain of tobacco, and thus fills the gap in the literature, especially in the European territory.

- Based on the results, all participants in the supply chain can adjust their operations so that the supply chain remains sustainable.

- Based on the research, it is possible to determine the critical problems within the chain and give adequate recommendations to the creators of economic policies.

2. Literature Review

3. Materials and Methods

4. Results

5. Discussion

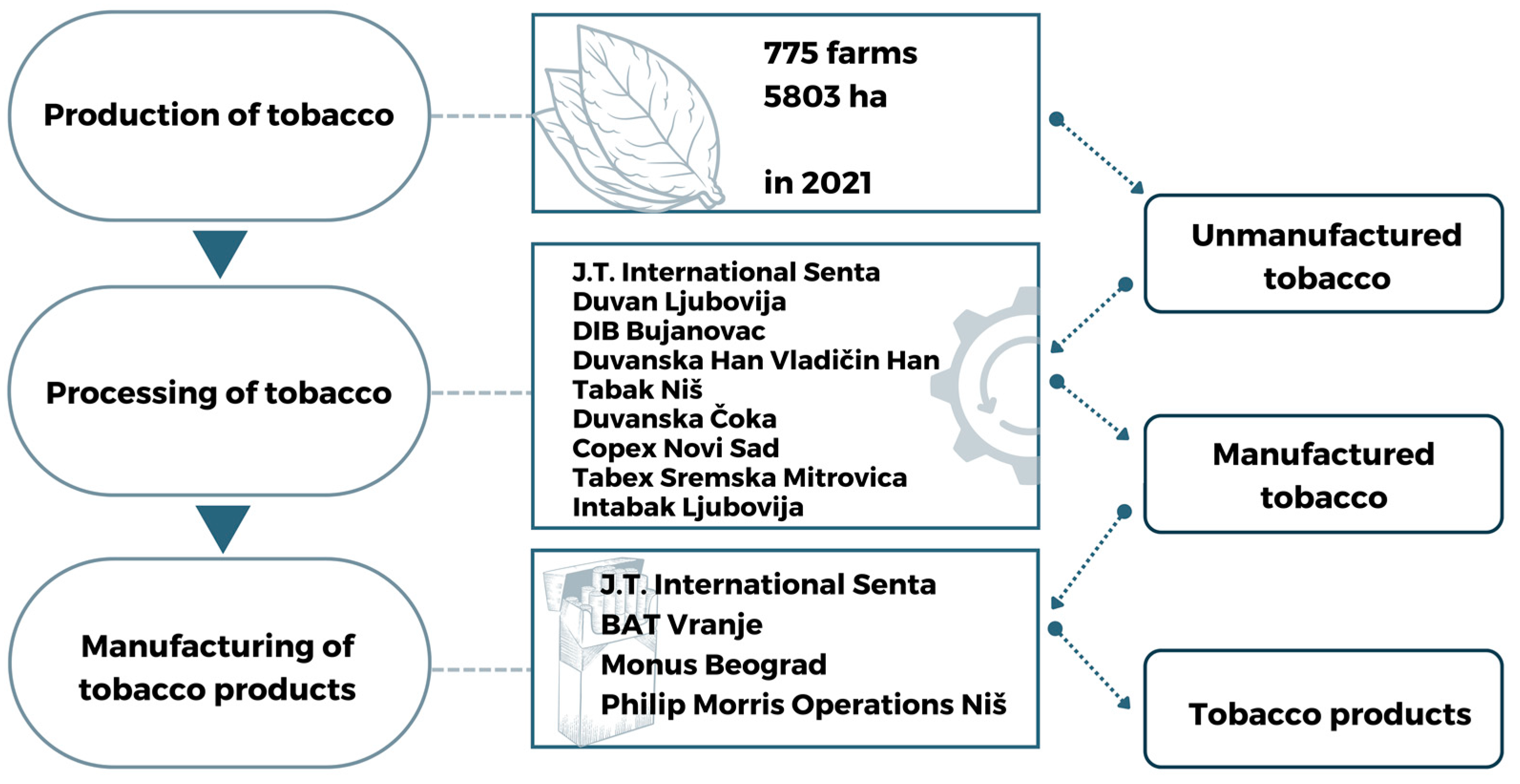

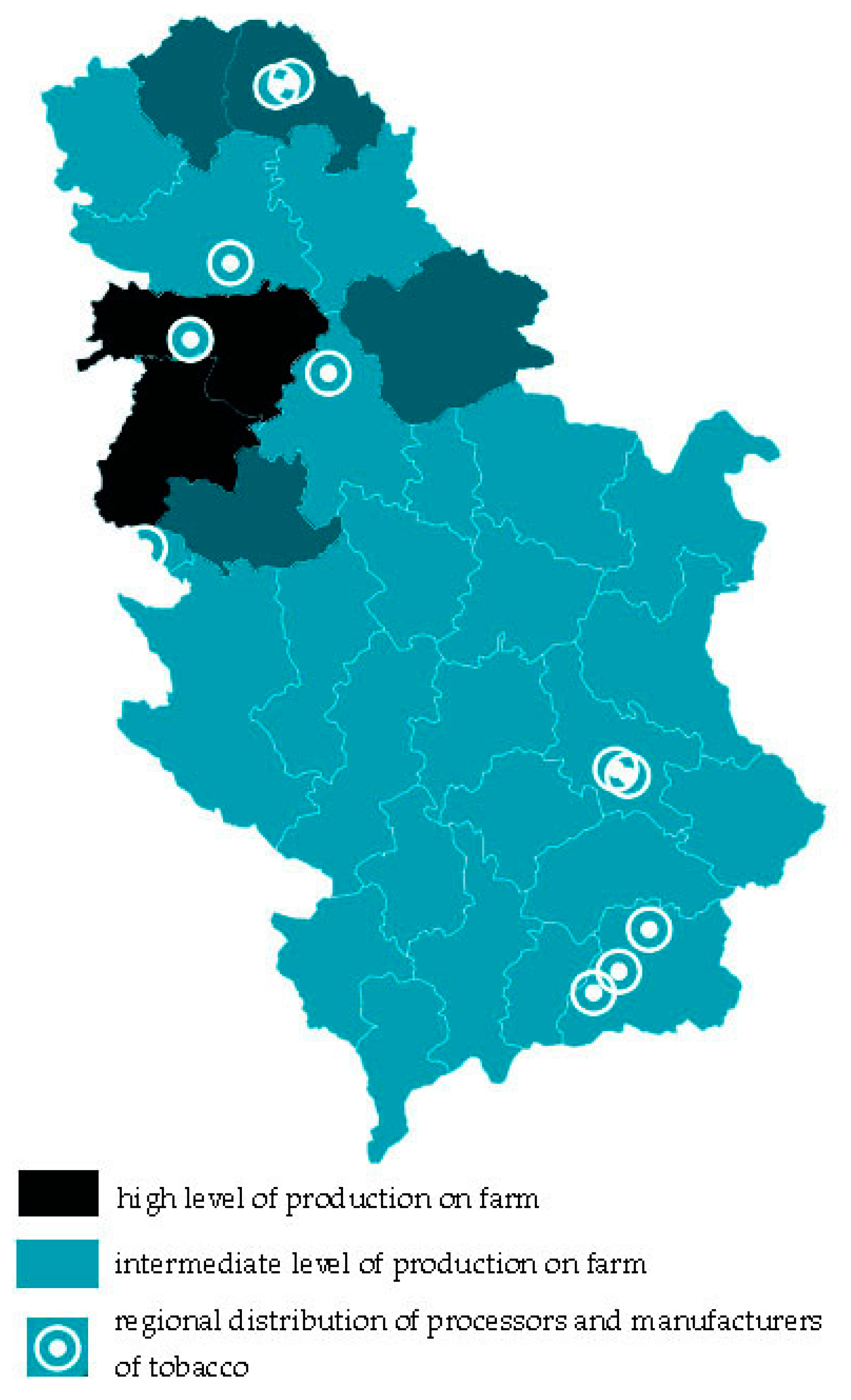

- The producers are in a poor negotiating position due to market concentration conditioned by the relatively low price of tobacco (Figure A3). Also, according to the Law on Tobacco [6], agricultural farms are obliged to enter a contract with tobacco processors and to sell tobacco to processors by the end of the current year. This kind of law puts farmers in a worse position than processors because the free sale of tobacco on the market is impossible.

- As already mentioned, farms perform the process of drying and packaging tobacco, which requires additional capital investments to purchase dryers. The energy consumption for drying is relatively high (natural gas is used most often), which increases production costs, especially in cases of shocks in the energy market, which was a characteristic of the observed period.

- Tobacco production requires a relatively large number of seasonal workers, which is a limiting factor. With the economic development in Serbia, there has been a significant labor force migration toward industry, while specific technological solutions are still expensive for producers. Indeed, reducing the number of farms is a characteristic of Serbian agriculture in the transition period, which also affected the tobacco production sector.

6. Conclusions

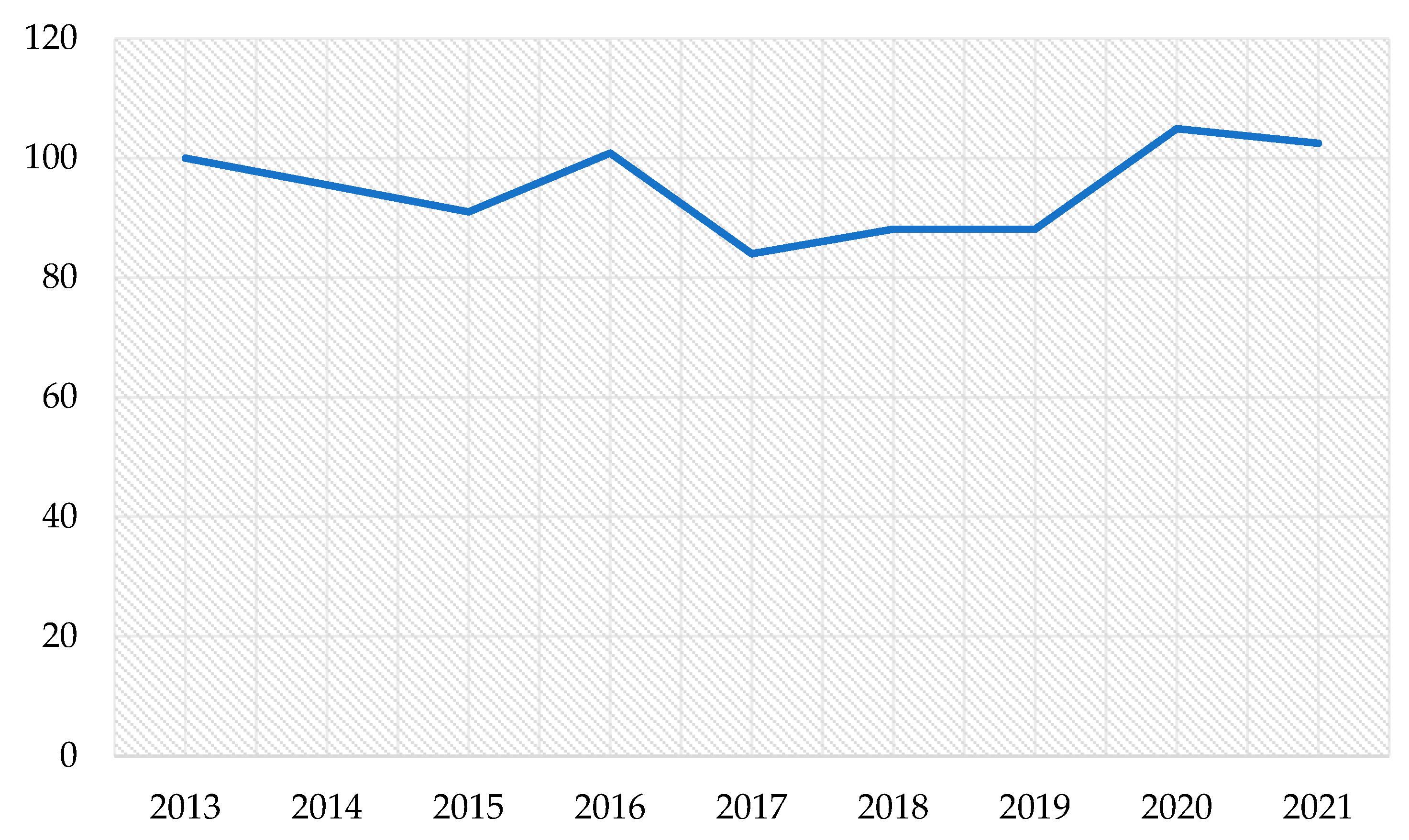

- Serbia was the only country in Europe where tobacco production was increasing. The key reasons were the presence of the largest multinational companies and weaker state regulations than in the EU.

- The number of farms producing tobacco decreased in the previous period, which, along with the production growth, suggests that the most efficient farms survived on the market. The further survival of these farms was threatened mainly due to a worse negotiating position on the market, which affected the relatively low price of tobacco and the increase in production costs due to the unstable global energy market. One of the solutions is a change in state regulations that will allow farms to sell tobacco freely on the market and encourage the association of producers.

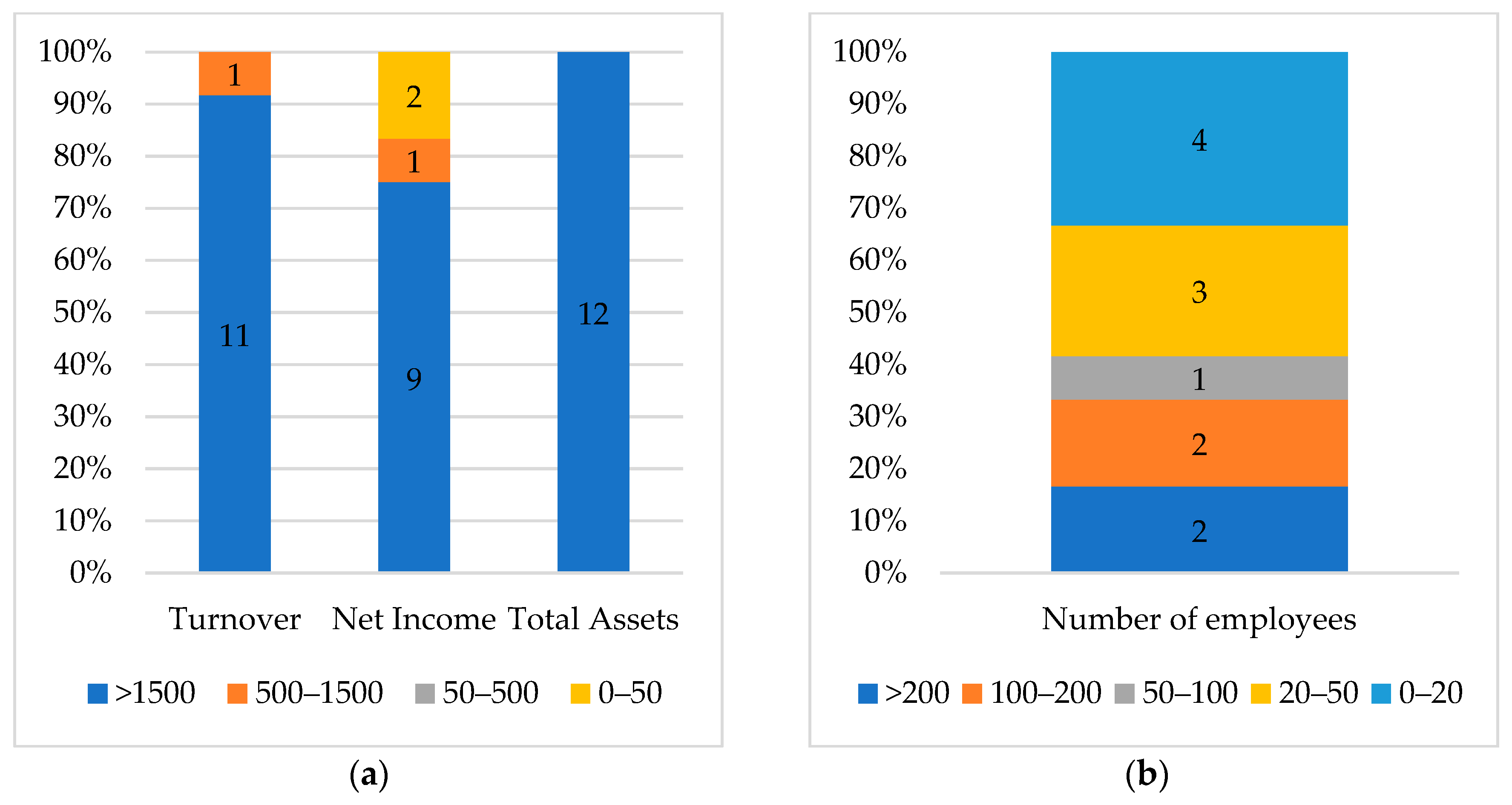

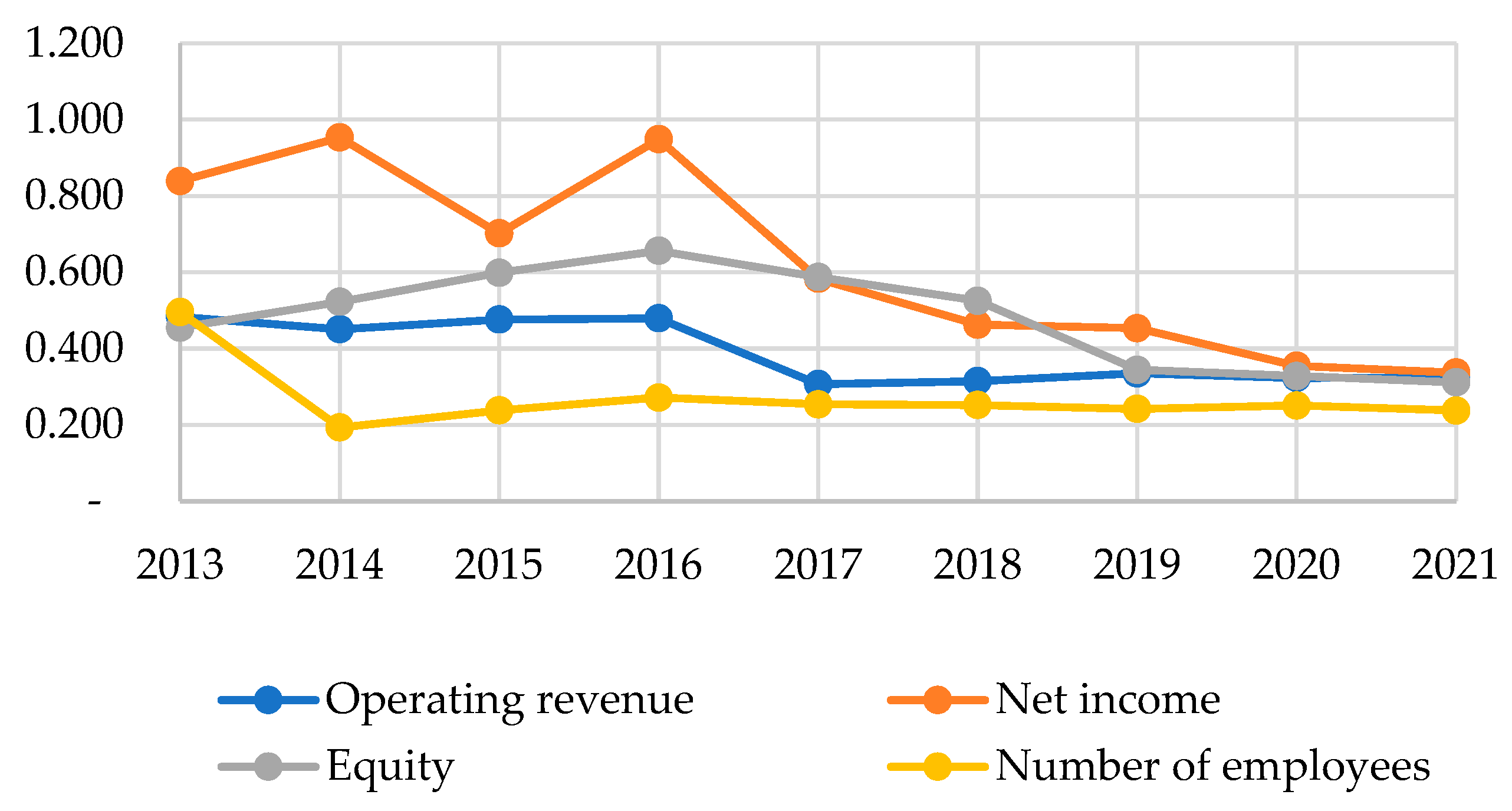

- There was a high market concentration in the Serbian tobacco industry. In the long term, this can potentially impact welfare losses primarily due to the manipulative abilities of oligopoly or oligopsony participants.

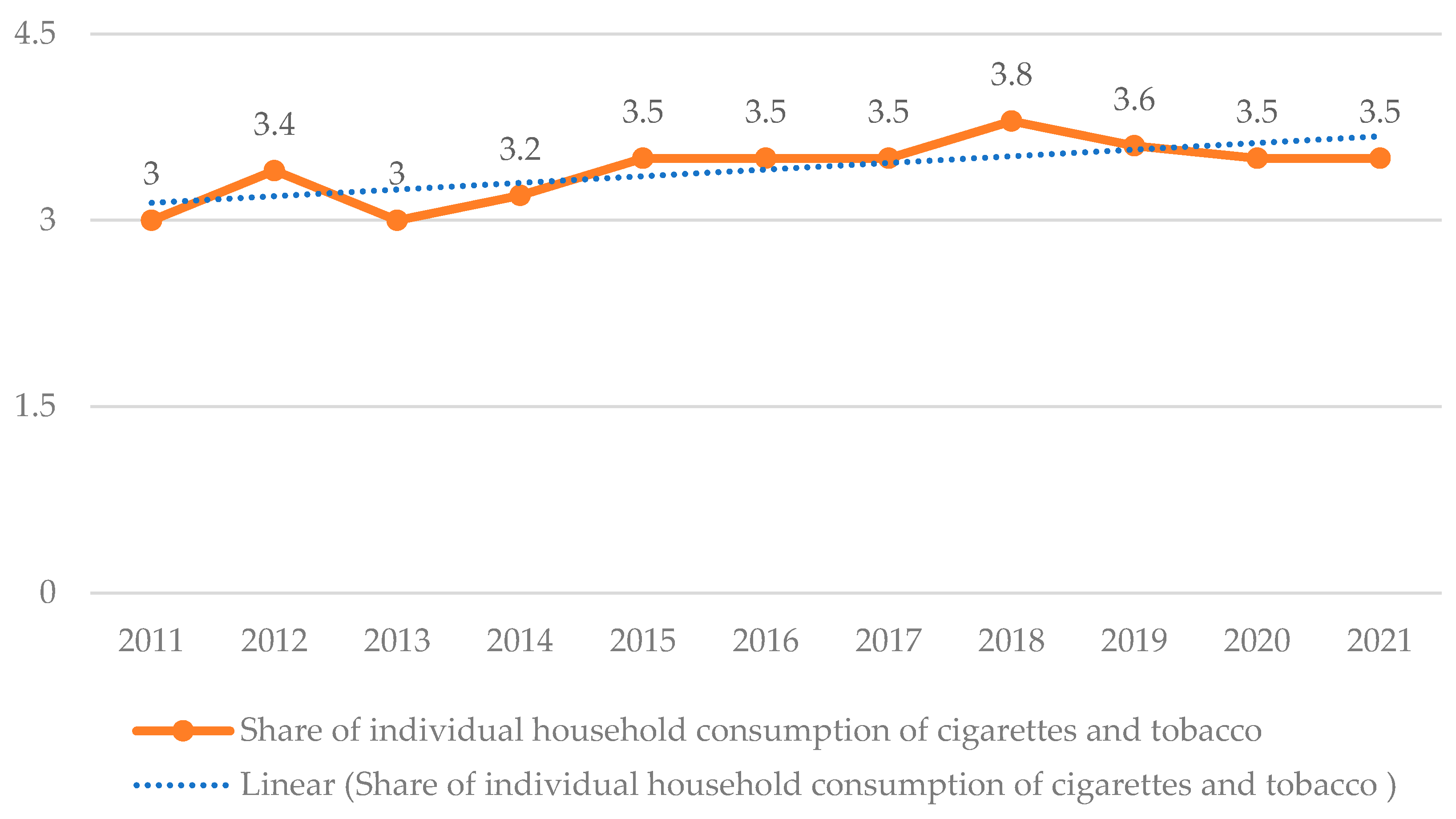

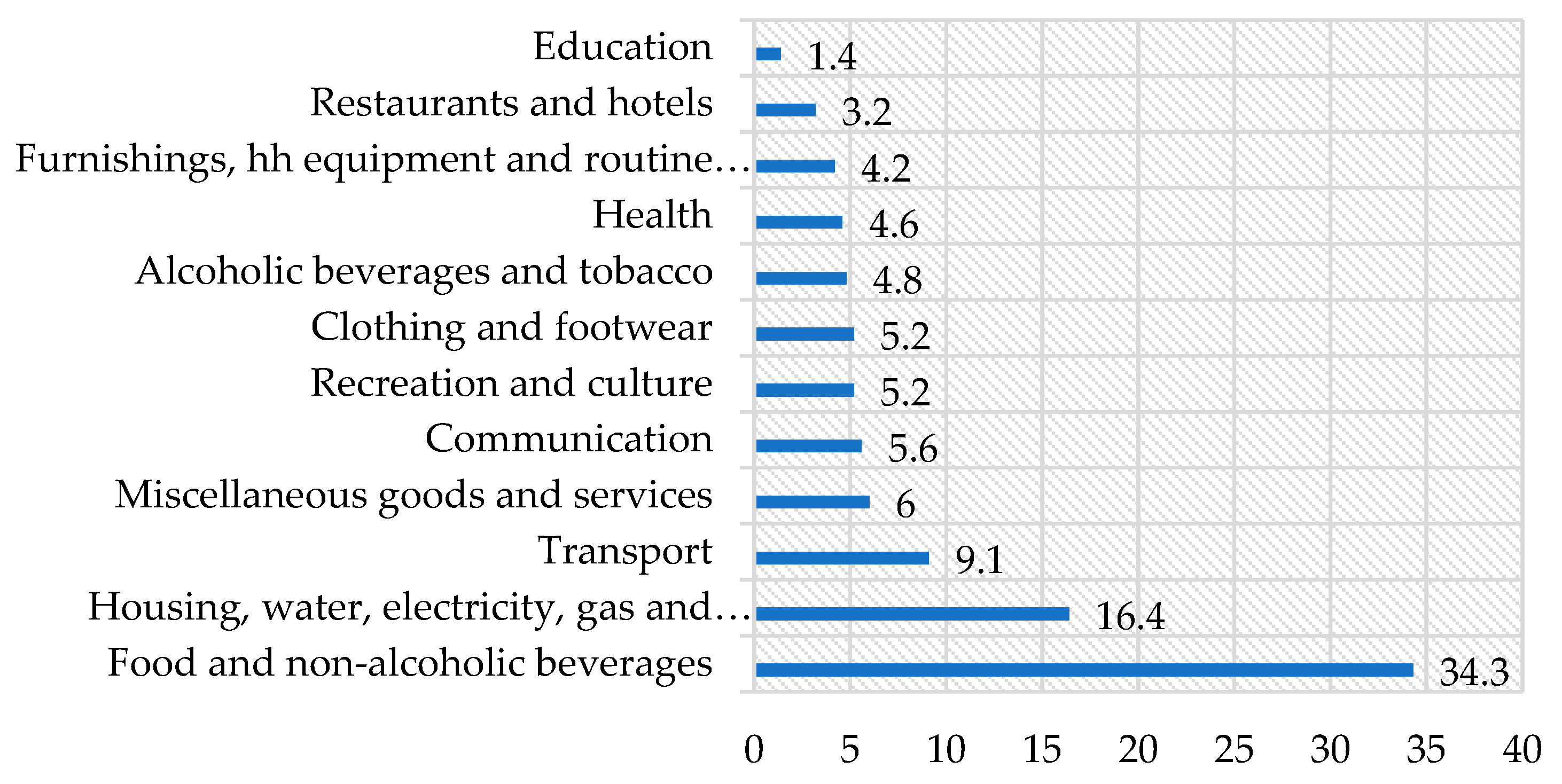

- The consumption of cigarettes was very high in Serbia. As tobacco products harm health, government policy must focus on measures that will reduce consumption. An adequate tax policy could affect this reduction and provide additional fiscal revenues.

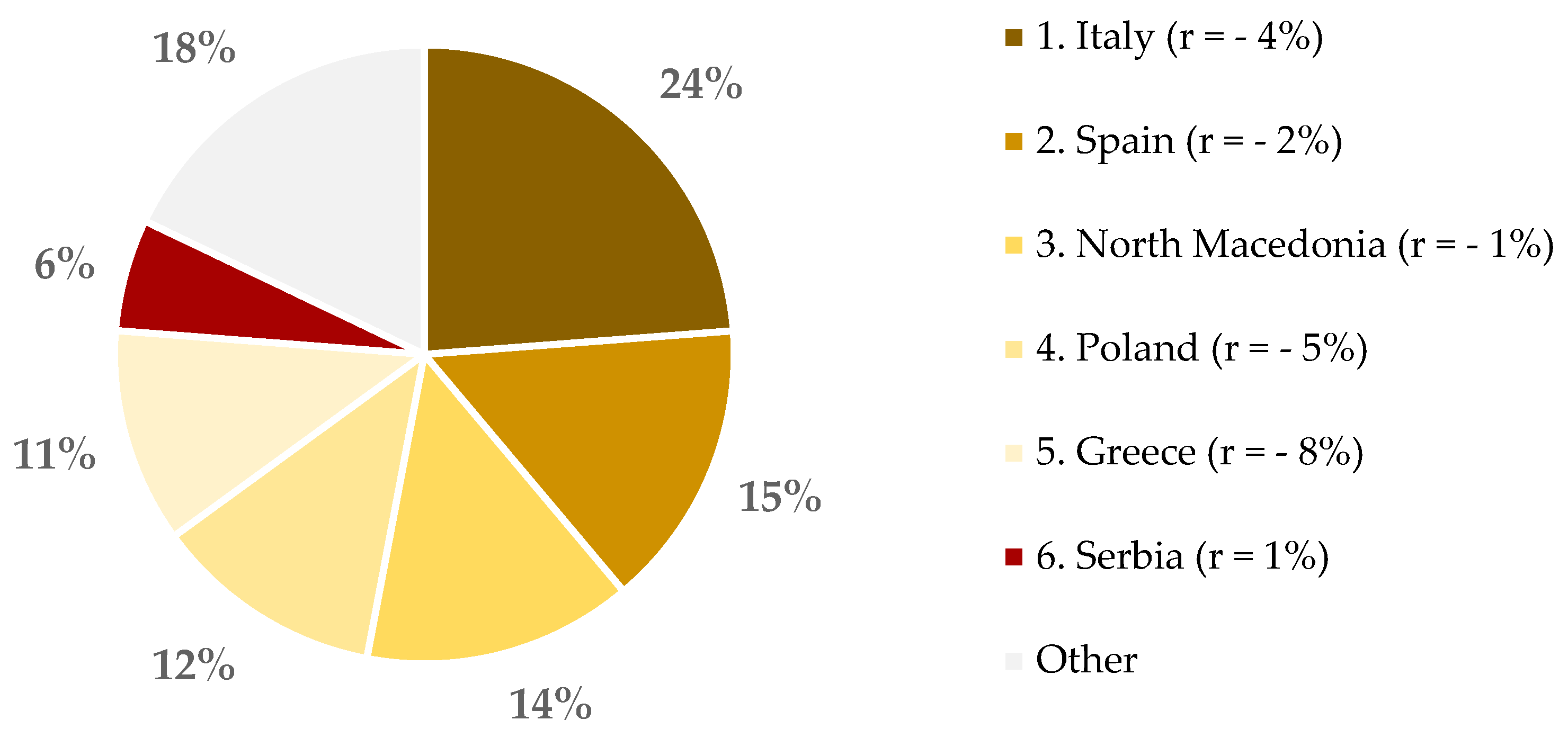

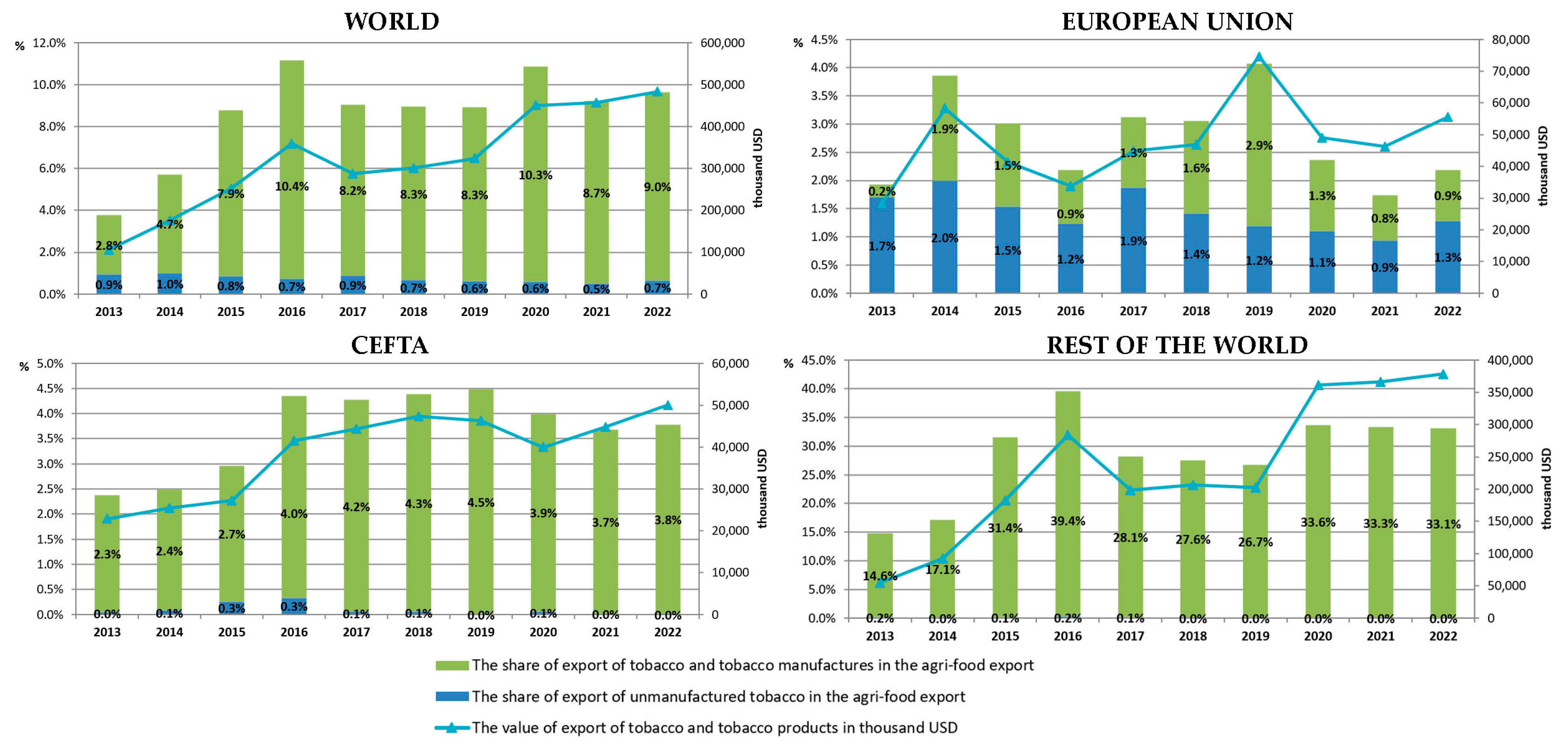

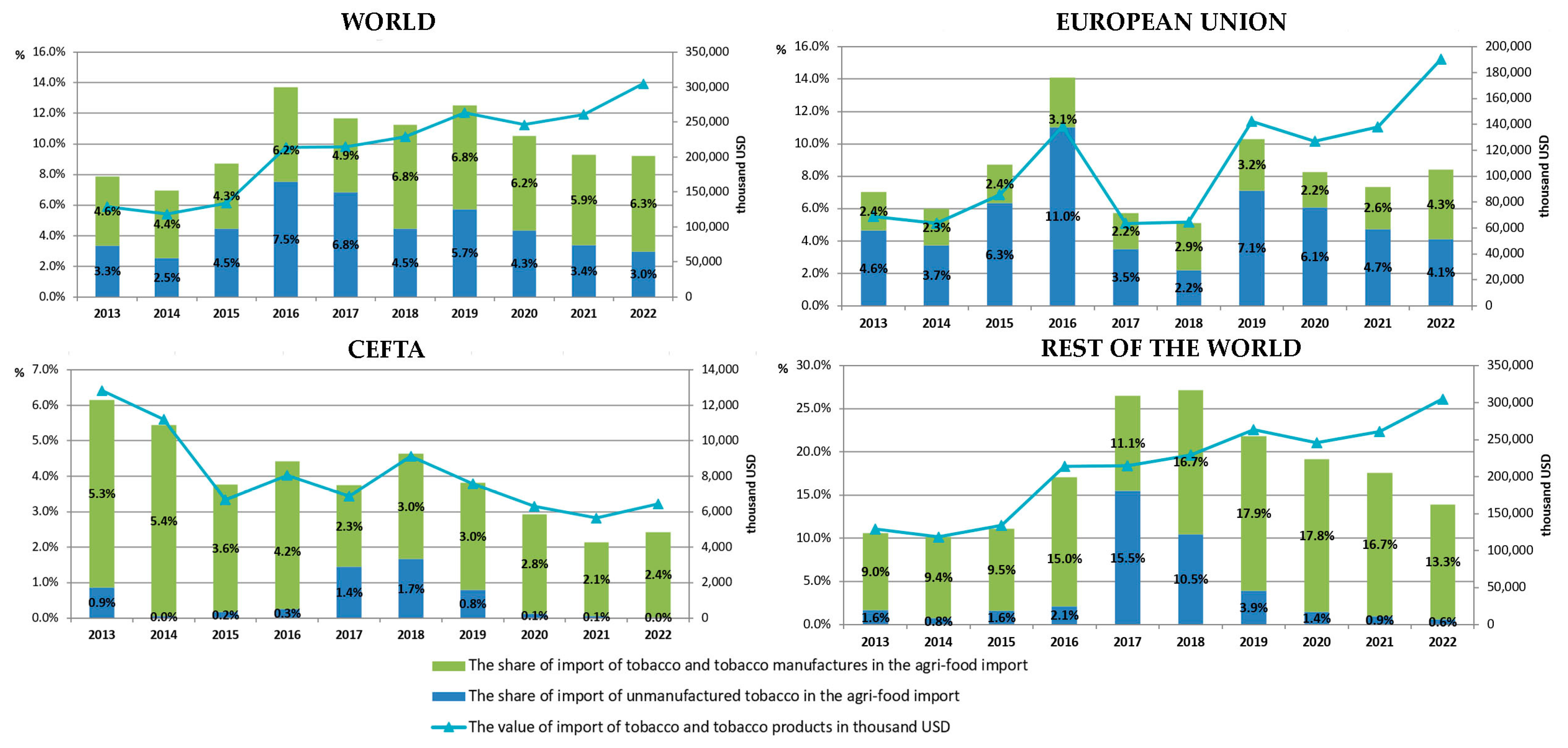

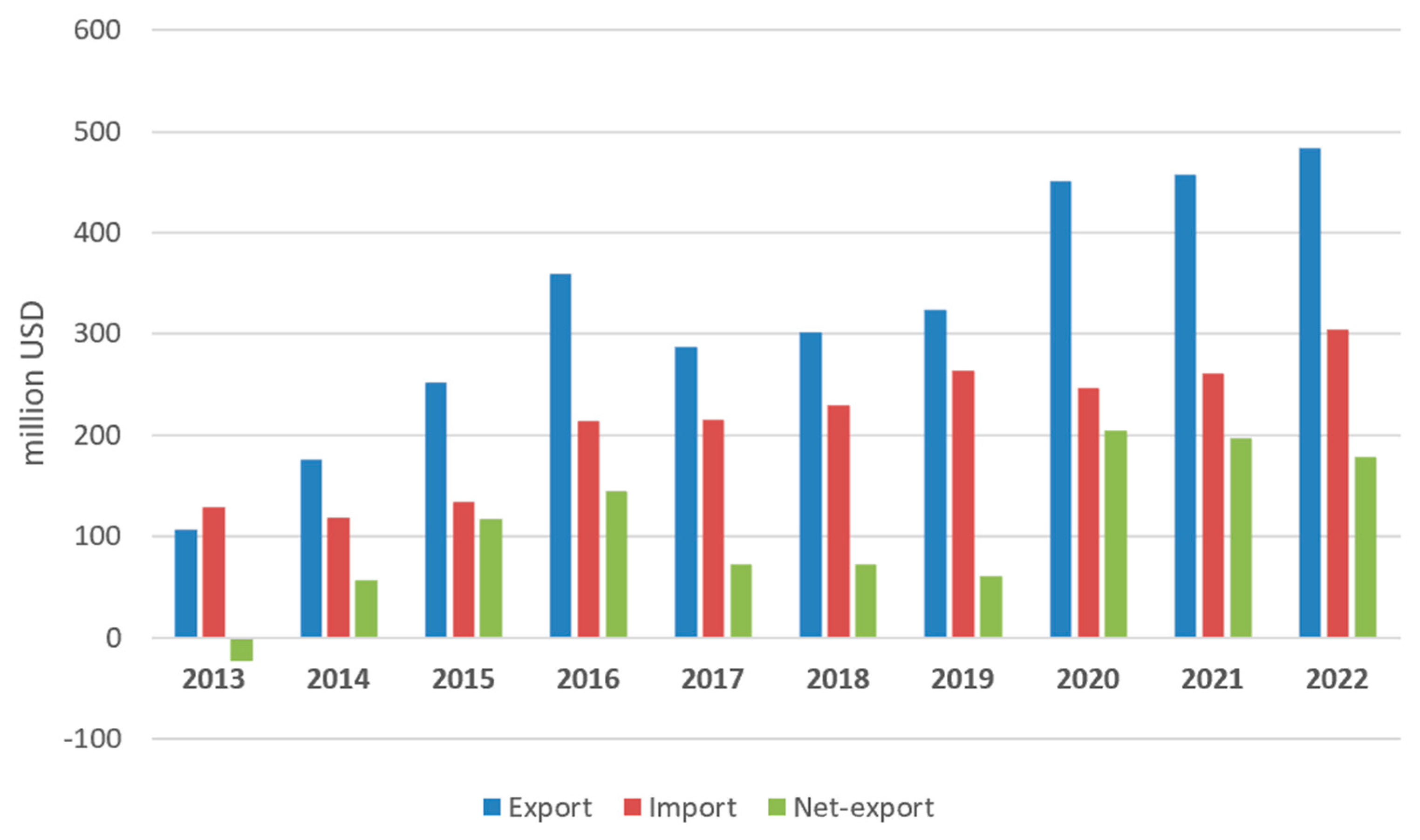

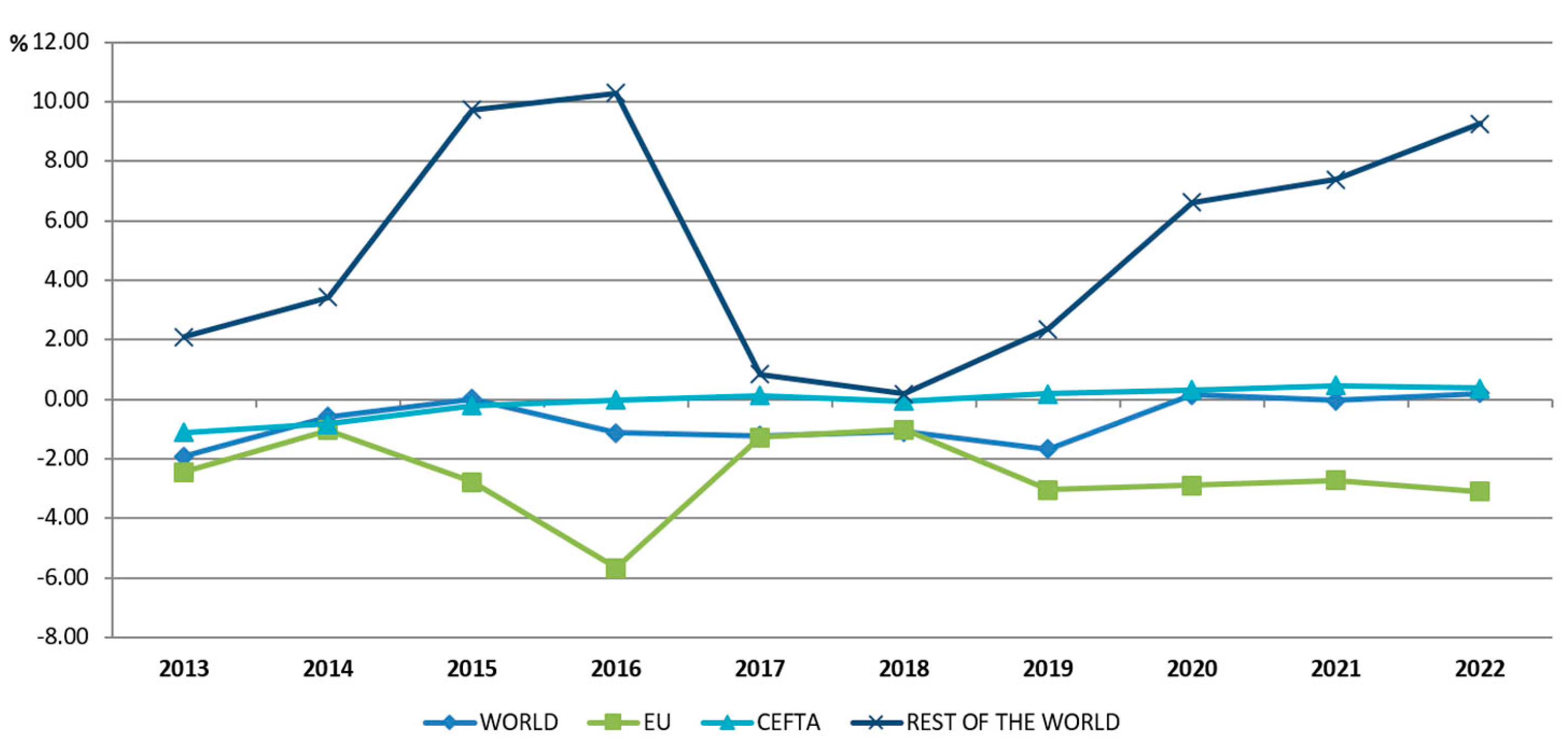

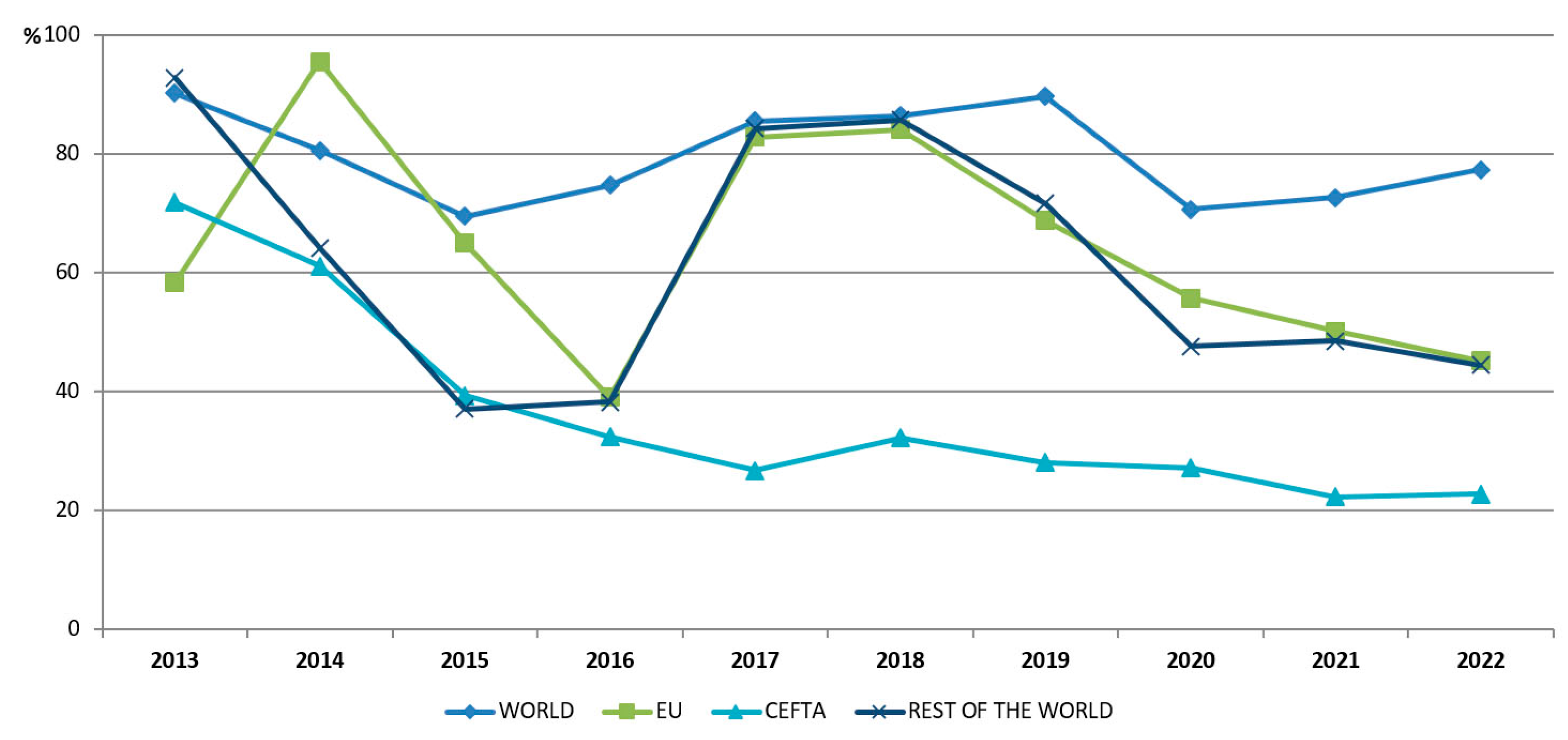

- Regarding foreign trade, there was a significant intensification, tobacco products were mainly exported to non-traditional markets (Algeria), and exports were dominated by one company—PMI. The tobacco and tobacco products market in Serbia was generally well integrated with the world market, but the level of revealed comparative advantages was low.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Appau, A.; Drope, J.; Witoelar, F.; Chavez, J.J.; Lencucha, R. Why Do Farmers Grow Tobacco? A Qualitative Exploration of Farmers Perspectives in Indonesia and Philippines. Int. J. Environ. Res. Public Health 2019, 16, 2330. [Google Scholar] [CrossRef]

- FAOSTAT. Available online: https://www.fao.org/faostat/en/ (accessed on 16 June 2023).

- Gallus, S.; Borroni, E.; Odone, A.; van den Brandt, P.A.; Gorini, G.; Spizzichino, L.; Pacifici, R.; Lugo, A. The Role of Novel (Tobacco) Products on Tobacco Control in Italy. Int. J. Environ. Res. Public Health 2021, 18, 1895. [Google Scholar] [CrossRef]

- Crop Productions and Plant-Based Products. Available online: https://agriculture.ec.europa.eu/farming/crop-productions-and-plant-based-products_en (accessed on 10 June 2023).

- Vladisavljevic, M.; Zubović, J.; Đukić, M.; Jovanović, O. Tobacco Price Elasticity in Serbia: Evidence from a Middle-Income Country with High Prevalence and Low Tobacco Prices. Tob. Control 2020, 29 (Suppl. S5), s331–s336. [Google Scholar] [CrossRef] [PubMed]

- Official Gazette of the Republic of Serbia. Zakon o Duvanu. Available online: https://www.paragraf.rs/propisi/zakon_o_duvanu.html (accessed on 10 June 2023).

- Statistical Office of Republic of Serbia. Statistical Yearbook. Available online: https://publikacije.stat.gov.rs/G2022/PdfE/G20222055.pdf (accessed on 5 June 2023).

- Statistical Office of Republic of Serbia. Statistical Calendar of Republic of Serbia 2023. Available online: https://publikacije.stat.gov.rs/G2023/Pdf/G202317016.pdf (accessed on 5 June 2023).

- Zubović, J.; Đukić, J.; Jovanović, O. Economic Aspects of Tobacco Control and Empirical Findings in Serbia; Institute of Economic Science: Belgrade, Republic of Serbia, 2020; Volume 180–181. [Google Scholar]

- Official Gazette of the Republic of Serbia no. 121/2021 and 18/2022). Uredba o Usklađivanju Nomenklature Carinske Tarife za 2022. Godinu. Available online: https://www.mfin.gov.rs/propisi/uredba-o-usklaivanju-nomenklature-carinske-tarife-za-2022-godinu-slubeni-glasnik-rs-broj-12121 (accessed on 5 June 2023).

- Appau, A.; Drope, J.; Goma, F.; Magati, P.; Labonte, R.; Makoka, D.; Zulu, R.; Li, Q.; Lencucha, R. Explaining Why Farmers Grow Tobacco: Evidence From Malawi, Kenya, and Zambia. Nicotine Tob. Res. 2020, 22, 2238–2245. [Google Scholar] [CrossRef] [PubMed]

- Chingosho, R.; Dare, C.; Walbeek, C. van. Tobacco Farming and Current Debt Status among Smallholder Farmers in Manicaland Province in Zimbabwe. Tob. Control 2021, 30, 610–615. [Google Scholar] [CrossRef]

- Rahman, M.S.; Ahmed, N.A.M.F.; Ali, M.; Abedin, M.M.; Islam, M.S. Determinants of Tobacco Cultivation in Bangladesh. Tob. Control 2020, 29, 692–694. [Google Scholar] [CrossRef]

- Bertollini, R.; Ribeiro, S.; Mauer-Stender, K.; Galea, G. Tobacco Control in Europe: A Policy Review. Eur. Respir. Rev. Off. J. Eur. Respir. Soc. 2016, 25, 151–157. [Google Scholar] [CrossRef]

- Straarup, M.S.; O’Donovan, F.; Lambrou, A.; Weber, C.; Gebetsberger-Hartleitner, I.; Solimini, R.; Labarbe, B.; Lange, C.C.; Stærmose, S.; Staal, Y.C.M.; et al. The Joint Action on Tobacco Control: A Cooperation Project for Strengthening Tobacco Control in Europe. Tob. Prev. Cessat. 2022, 8, 26. [Google Scholar] [CrossRef]

- Matkovski, B.; Đokić, D. Podrška Proizvodnji Duvana u Srbiji. Agroekonomika 2014, 43, 154–164. [Google Scholar]

- Matkovski, B.; Kalaš, B.; Zekić, S.; Jeremić, M. Agri-Food Competitiveness in South East Europe. Outlook Agric. 2019, 48, 326–335. [Google Scholar] [CrossRef]

- Matkovski, B.; Zekić, S.; Đokić, D.; Jurjević, Ž.; Đurić, I. Export Competitiveness of Agri-Food Sector during the EU Integration Process: Evidence from the Western Balkans. Foods 2022, 11, 10. [Google Scholar] [CrossRef]

- Božić, D.; Nikolić, M. Foreign Trade and Comparative Advantages of Agrarian Sector of Serbia and Neighboring Countries. Ekon. Poljopr. 2019, 66, 737–753. [Google Scholar] [CrossRef]

- Tuna, E.; Georgiev, N.; Nacka, M. Competitiveness Analysis of the Tobacco Sub-Sector in the Republic of Macedonia. Agroecon. Croat. 2013, 3, 53–60. [Google Scholar]

- Zekić, S.; Matkovski, B.; Đokić, D.; Kleut, Ž. Competitiveness of Tobacco and Tobacco Products: The Case of Serbia. Custos E Agronegocio 2016, 12, 191–211. [Google Scholar]

- Božić, D.; Nikolić, M.M. Obeležja Spoljnotrgovinske Razmene Poljoprivredno-Prehrambenih Proizvoda Srbije: Characteristics of Serbian Foreign Trade of Agricultural and Food Products. Marketing 2016, 47, 293–304. [Google Scholar] [CrossRef]

- Matkovski, B.; Lovre, K.; Zekic, S. The Foreign Trade Liberalization and Export of Agri-Food Products of Serbia. Agric. Econ. Zemědělská Ekon. 2017, 63, 331–345. [Google Scholar] [CrossRef]

- Birovljev, J.; Matkovski, B.; Ćetković, B. The Competitiveness of the Serbian Agri-Food Products on the Market of Countries in the Region. Anali Ekon. Fak. U Subotici 2015, 33, 61–78. [Google Scholar]

- Blažková, I. Convergence of Market Concentration: Evidence from Czech Food Processing Sectors. Agris Line Pap. Econ. Inform. 2016, 4, 25–36. [Google Scholar] [CrossRef]

- Swinnen, J.F.M.; Vandeplas, A. Market Power and Rents in Global Supply Chains. Agric. Econ. 2010, 41, 109–120. [Google Scholar] [CrossRef]

- Vuković, B.; Mijić, K.; Spahić, N. Concetracion of Tobacco Market: Evidence from Serbia. Econ. Agric. 2015, 62, 385–398. [Google Scholar] [CrossRef]

- Mirović, V.; Andrašić, J.; Kalaš, B. Impact of the Market Concentration on Trading Chains’ Performance in Serbia. Šk. Biznisa 2019, 1, 1–14. [Google Scholar] [CrossRef]

- Pjanić, M.; Vuković, B.; Mijić, K. Analysis of the Market Concentration of Agricultural Enterprises in AP Vojvodina. Strateg. Manag. 2018, 23, 40–45. [Google Scholar] [CrossRef]

- Kastratović, R.; Lončar, D.; Milošević, S. Market concentration and profitability: The empirical evidence from Serbian manufacturing industry. Zb. Rad. Ekon. Fak. U Rijeci Časopis Za Ekon. Teor. Praksu 2019, 37, 213–233. [Google Scholar] [CrossRef]

- Grullon, G.; Larkin, Y.; Michaely, R. Are U.S. Industries Becoming More Concentrated? Rev. Financ. 2018, 23, 697–743. [Google Scholar] [CrossRef]

- Flor, L.S.; Reitsma, M.B.; Gupta, V.; Ng, M.; Gakidou, E. The Effects of Tobacco Control Policies on Global Smoking Prevalence. Nat. Med. 2021, 27, 239–243. [Google Scholar] [CrossRef]

- WHO Report on the Global Tobacco Epidemic 2021: Addressing New and Emerging Products. Available online: https://www.who.int/publications-detail-redirect/9789240032095 (accessed on 10 June 2023).

- Nargis, N.; Stoklosa, M.; Shang, C.; Drope, J. Price, Income, and Affordability as the Determinants of Tobacco Consumption: A Practitioner’s Guide to Tobacco Taxation. Nicotine Tob. Res. 2021, 23, 40–47. [Google Scholar] [CrossRef]

- Ministry of Finance, Republic of Serbia. Website. Tobacco Administration. Available online: https://www.duvan.gov.rs/ (accessed on 20 June 2023).

- TP Catalyst. Database. Available online: https://tpcatalyst.bvdinfo.com/202305/version-20230602092050/TpCatalyst/Companies/Login?returnUrl=%2F202305%2Fversion-20230602092204%2FTpCatalyst%2FCompanies (accessed on 20 June 2023).

- Statistical Office of the Republic of Serbia. Database. Available online: https://www.stat.gov.rs/en-US/ (accessed on 20 May 2023).

- Standard International Trade Classification. United Nations Statistics Division—Trade Statistics. Available online: https://unstats.un.org/unsd/trade/sitcrev4.htm (accessed on 1 July 2023).

- Krstić, M.; Gawel, A. Improving the competitiveness—Determinants and solutions for quality of local business conditions. Int. J. Qual. Res. 2023, 17, 529–554. [Google Scholar] [CrossRef]

- Balassa, B. Trade Liberalisation and “Revealed” Comparative Advantage1. Manch. Sch. 1965, 33, 99–123. [Google Scholar] [CrossRef]

- Lafay, G. The Measurement of Revealed Comparative Advantages. In International Trade Modelling; Springer: Berlin/Heidelberg, Germany, 1992. [Google Scholar]

- Matkovski, B.; Zekić, S.; Jurjević, Ž.; Đokić, D. The Agribusiness Sector as a Regional Export Opportunity: Evidence for the Vojvodina Region. Int. J. Emerg. Mark. 2021, 17, 2468–2489. [Google Scholar] [CrossRef]

- Burianová, J.; Belová, A. The Competitiveness of Agricultural Foreign Trade Commodities of the CR Assessed by Way of the Lafay Index. Agris Line Pap. Econ. Inform. 2012, 4, 27–36. [Google Scholar]

- Grubel, H.G.; Loyd, P.J. Intra-Industry Trade: The Theory and Measurement of International Trade in Differentiated Product. Econ. J. 1975, 85, 646–648. [Google Scholar]

- Hou, K.; Robinson, D.T. Industry Concentration and Average Stock Returns. J. Financ. 2006, 61, 1927–1956. [Google Scholar] [CrossRef]

- Lado-Sestayo, R.; Otero-González, L.; Vivel-Búa, M.; Martorell-Cunill, O. Impact of Location on Profitability in the Spanish Hotel Sector. Tour. Manag. 2016, 52, 405–415. [Google Scholar] [CrossRef]

- Krivokapic, R.; Njegomir, V.; Stojic, D. Effects of Corporate Diversification on Firm Performance: Evidence from the Serbian Insurance Industry. Econ. Res. Ekon. Istraživanja 2017, 30, 1224–1236. [Google Scholar] [CrossRef]

- Stojanović, B.; Kostić, M. Competition Policy and the Impact of Market Structure on Companies’ Profitability. Ekon. Preduz. 2013, 61, 325–338. [Google Scholar] [CrossRef]

- Vojinović, Ž.; Milutinović, S.; Sertić, D.; Leković, B. Determinants of Sustainable Profitability of the Serbian Insurance Industry: Panel Data Investigation. Sustainability 2022, 14, 5190. [Google Scholar] [CrossRef]

- Arian, A.; Sands, J.; Tooley, S. Industry and Stakeholder Impacts on Corporate Social Responsibility (CSR) and Financial Performance: Consumer vs. Industrial Sectors. Sustainability 2023, 15, 12254. [Google Scholar] [CrossRef]

- Basdekis, C.; Katsampoxakis, I.; Anathreptakis, K. Women’s Participation in Firms’ Management and Their Impact on Financial Performance: Pre-COVID-19 and COVID-19 Period Evidence. Sustainability 2023, 15, 8686. [Google Scholar] [CrossRef]

- Bui, T.N.; Nguyen, X.H.; Pham, K.T. The Effect of Capital Structure on Firm Value: A Study of Companies Listed on the Vietnamese Stock Market. Int. J. Financ. Stud. 2023, 11, 100. [Google Scholar] [CrossRef]

- Mahssouni, R.; Makhroute, M.; Touijer, M.N.; Elabjani, A. Dual Perspectives on Financial Performance: Analyzing the Impact of Digital Transformation and COVID-19 on European Listed Companies. J. Risk Financ. Manag. 2023, 16, 371. [Google Scholar] [CrossRef]

- Tarighi, H.; Hosseiny, Z.N.; Akbari, M.; Mohammadhosseini, E. The Moderating Effect of the COVID-19 Pandemic on the Relation between Corporate Governance and Firm Performance. J. Risk Financ. Manag. 2023, 16, 306. [Google Scholar] [CrossRef]

- Tekić, D.; Mutavdžić, B.; Milić, D.; Matkovski, B.; Đokić, D.; Novaković, T. Profitability Determinants of Small Agricultural and Food Companies in the Republic of Serbia. Custos E Agronegocio 2022, 18, 124–145. [Google Scholar]

- Jambor, A.; Babu, S. Competitiveness of Global Agriculture; Springer International Publishing: Cham, Switzerland, 2016. [Google Scholar] [CrossRef]

- Hamad, H.A.; Cek, K. The Moderating Effects of Corporate Social Responsibility on Corporate Financial Performance: Evidence from OECD Countries. Sustainability 2023, 15, 8901. [Google Scholar] [CrossRef]

- Parzonko, A.; Parzonko, A.J.; Bórawski, P.; Wicki, L. Return on Equity in Dairy Farms from Selected EU Countries: Assessment Based on the DuPont Model in Years 2004–2020. Agriculture 2023, 13, 1403. [Google Scholar] [CrossRef]

- Walsh, J.; Parsons, R.; Wang, Q.; Conner, D. What Makes an Organic Dairy Farm Profitable in the United States? Evidence from 10 Years of Farm Level Data in Vermont. Agriculture 2020, 10, 17. [Google Scholar] [CrossRef]

- Dakić, S.; Mijić, K.; Jakšić, D. Multiple Regression Approach to Modelling Determinants of Business Success Based on Financial Statements: Evidence from Food Processing Companies in the Republic of Serbia. Custos E Agronegocio 2019, 15, 485–501. [Google Scholar]

- Vuković, B.; Milutinović, S.; Mijić, K.; Krsmanović, B.; Jakšić, D. Analysis of Financial Performance Determinants: Evidence from the European Agricultural Companies. Custos E Agronegocio 2022, 18, 285–306. [Google Scholar]

- U.S. Department of Justice and the Federal Trade Commission. Horizontal Merger Guidelines. 2010. Available online: https://www.justice.gov/sites/default/files/atr/legacy/2010/08/19/hmg-2010.pdf (accessed on 7 June 2023).

- European Commission. Guidelines on the Assessment of Horizontal Mergers under the Council Regulation on the Control of Concentrations between Undertakings. 2004. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=celex%3A52004XC0205%2802%29 (accessed on 5 June 2023).

- Das, P. Econometrics in Theory and Practice: Analysis of Cross Section, Time Series and Panel Data with Stata 15.1|SpringerLink. Available online: https://link.springer.com/book/10.1007/978-981-32-9019-8 (accessed on 17 August 2023).

- Hsiao, C. (Ed.) Analysis of Panel Data; Econometric Society Monographs; Cambridge University Press: Cambridge, UK, 2022; pp. 469–497. [Google Scholar] [CrossRef]

- Ahmed, A.M.; Nugraha, D.P.; Hágen, I. The Relationship between Capital Structure and Firm Performance: The Moderating Role of Agency Cost. Risks 2023, 11, 102. [Google Scholar] [CrossRef]

- Ahmed, A.M.; Sharif, N.A.; Ali, M.N.; Hágen, I. Effect of Firm Size on the Association between Capital Structure and Profitability. Sustainability 2023, 15, 11196. [Google Scholar] [CrossRef]

- Eurostat. Tobacco Consumption Statistics. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Tobacco_consumption_statistics (accessed on 4 June 2023).

- Statistical Office of the Republic of Serbia. Household Budget Survey. Available online: https://www.stat.gov.rs/en-us/oblasti/potrosnja-prihodi-i-uslovi-zivota/potrosnja-domacinstva/ (accessed on 20 June 2023).

- Kilibarda, B.; Nikolić, N.; Krstev, S.; Šović, N.; Gudelj Rakić, J. Global Survey of Tobacco Use among Young People Aged 13–15 in Serbia in 2017; Institute for Public Health of Serbia “Dr. Milan Jovanović Batut”: Belgrade, Serbia, 2018. [Google Scholar]

- Official Gazette of the Republic of Serbia. Zakon o Zaštiti Stanovništva od Izloženosti Duvanskom Dimu. Available online: https://www.paragraf.rs/propisi/zakon_o_zastiti_stanovnistva_od_izlozenosti_duvanskom_dimu.html (accessed on 21 June 2023).

- Official Gazette of the Republic of Serbia. Zakon o Oglašavanju. Available online: https://www.paragraf.rs/propisi/zakon_o_oglasavanju.html (accessed on 21 June 2023).

- O’Rourke, M.; Djukic, J. Welcome to Serbia: Feel Free to Smoke. Tob. Control 2008, 17, 428–430. [Google Scholar] [CrossRef]

- Checkpoint. Database. Available online: https://www.checkpoint.rs/ (accessed on 15 July 2023).

- Đokić, D.; Novaković, T.; Tekić, D.; Matkovski, B.; Zekić, S.; Milić, D. Technical Efficiency of Agriculture in the European Union and Western Balkans: SFA Method. Agriculture 2022, 12, 1992. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Notation | Formulation | Indicator | Predicted Effect |

|---|---|---|---|---|

| Profitability | ROA | Net income/Total assets | Company’s capacity to generate profits derived from its assets. | / |

| Market concentration (operating revenue-based) | HHI | Equation (1) | Extent to which a market is dominated by a small number of large companies. | + |

| Liquidity | LIQ | Current assets/Current liabilities | Company’s capacity to fulfill its short-term financial obligations. | − |

| Financial leverage | LEV | Total liabilities/Equity | Company’s indebtedness in relation to equity. | − |

| Debt ratio | DEBT | Total liabilities/Total assets | Company’s indebtedness in relation to total assets. | − |

| Firm size | SIZE | Ln (Total assets) | Size of organization through total assets. | + |

| Tangibility | TANG | Fixed assets/Total assets | Company’s asset structure. | − |

| Total assets turnover | TAT | Sales revenue/Average total assets | Company’s capacity to generate sales derived from its assets. | + |

| Fixed assets turnover | FAT | Sales revenue/Average fixed assets | Company’s capacity to generate sales derived from its fixed assets. | + |

| Current assets turnover | CAT | Sales revenue/Average current assets | Company’s capacity to generate sales derived from its current assets. | + |

| Growth | GRW | Turnover (year t) − Turnover (year t1)/Turnover (year t − 1) | Company’s ability to increase sales between two time periods. | + |

| Profitability | ROA | Net income/Total assets | Company’s capacity to generate profits derived from its assets. | / |

| Market concentration (operating revenue-based) | HHI | Equation (1) | Extent to which a market is dominated by a small number of large companies. | + |

| Liquidity | LIQ | Current assets/Current liabilities | Company’s capacity to fulfill its short-term financial obligations. | − |

| Financial leverage | LEV | Total liabilities/Equity | Company’s indebtedness in relation to equity. | − |

| Debt ratio | DEBT | Total liabilities/Total assets | Company’s indebtedness in relation to total assets. | − |

| Firm size | SIZE | Ln (Total assets) | Size of organization through total assets. | + |

| Tangibility | TANG | Fixed assets/Total assets | Company’s asset structure. | − |

| Total assets turnover | TAT | Sales revenue/Average total assets | Company’s capacity to generate sales derived from its assets. | + |

| Fixed assets turnover | FAT | Sales revenue/Average fixed assets | Company’s capacity to generate sales derived from its fixed assets. | + |

| Current assets turnover | CAT | Sales revenue/Average current assets | Company’s capacity to generate sales derived from its current assets. | + |

| Growth | GRW | Turnover (year t) − Turnover (year t − 1)/Turnover (year t − 1) | Company’s ability to increase sales between two time periods. | + |

| Year | Area (ha) | Total Production (t) | Yield (t/ha) | Number of Farms | Production per Farm (t) | Area per Farm |

|---|---|---|---|---|---|---|

| 2013 | 4939 | 7977 | 1.62 | 1781 | 4.48 | 2.77 |

| 2014 | 4899 | 9341 | 1.91 | 1695 | 5.51 | 2.89 |

| 2015 | 5012 | 8776 | 1.75 | 1235 | 7.11 | 4.06 |

| 2016 | 5256 | 7810 | 1.49 | 959 | 8.14 | 5.48 |

| 2017 | 5069 | 7173 | 1.42 | 983 | 7.30 | 5.16 |

| 2018 | 5762 | 7169 | 1.24 | 992 | 7.23 | 5.81 |

| 2019 | 7023 | 7992 | 1.14 | 885 | 9.03 | 7.94 |

| 2020 | 6745 | 8924 | 1.32 | 900 | 9.92 | 7.49 |

| 2021 | 5803 | 10,097 | 1.74 | 775 | 13.03 | 7.49 |

| Herfindahl–Hirschman Index | Operating Revenue | Net Income | Equity | Number of Employees |

|---|---|---|---|---|

| HHI 2013 | 0.484 | 0.839 | 0.455 | 0.496 |

| HHI 2014 | 0.451 | 0.953 | 0.523 | 0.193 |

| HHI 2015 | 0.476 | 0.702 | 0.599 | 0.238 |

| HHI 2016 | 0.479 | 0.949 | 0.656 | 0.272 |

| HHI 2017 | 0.307 | 0.583 | 0.587 | 0.254 |

| HHI 2018 | 0.314 | 0.463 | 0.525 | 0.252 |

| HHI 2019 | 0.335 | 0.453 | 0.344 | 0.242 |

| HHI 2020 | 0.323 | 0.355 | 0.328 | 0.251 |

| HHI 2021 | 0.324 | 0.337 | 0.312 | 0.238 |

| Test | p-Value | Decision |

|---|---|---|

| Hausman test | 0.9870 | The random effects model was appropriate |

| Time effect | 0.0000 | Time effect included |

| Individual effect | 0.0000 | Individual effect included |

| Variable | VIF | 1/VIF (TOL) |

|---|---|---|

| HHI | 1.19 | 0.8382 |

| LIQ | 1.23 | 0.8152 |

| LEV | 1.17 | 0.8556 |

| DEBT | 1.30 | 0.7695 |

| SIZE | 1.82 | 0.5493 |

| TANG | 3.78 | 0.2645 |

| TAT | 10.82 | 0.0925 |

| FAT | 7.25 | 0.1379 |

| CAT | 4.67 | 0.2142 |

| GRW | 1.23 | 0.8128 |

| Mean VIF | 3.45 | - |

| Test | p-Value | Decision |

|---|---|---|

| Wooldridge test | 0.2556 | Absence of autocorrelation |

| Breusch–Pagan test/Cook–Weisberg test | 0.0022 | Presence of heteroskedasticity |

| ROA | Coefficient | Robust Standard Error | z | P > |z| | 95% Conf. | Interval |

|---|---|---|---|---|---|---|

| HHI | −0.5684 | 0.1872 | −3.04 | 0.002 | −0.9352 | −0.2016 |

| LIQ | −0.0008 | 0.0003 | −2.84 | 0.005 | −0.0014 | −0.0002 |

| LEV | 0.0047 | 0.0025 | 1.91 | 0.057 | −0.0001 | 0.0096 |

| DEBT | −0.0712 | 0.0010 | −7.13 | 0.000 | −0.0907 | −0.0516 |

| SIZE | −0.0124 | 0.0077 | −1.61 | 0.107 | −0.0275 | 0.0027 |

| TANG | −0.1868 | 0.0928 | −2.01 | 0.044 | −0.3686 | −0.0049 |

| TAT | 0.1552 | 0.0633 | 2.45 | 0.014 | 0.0311 | 0.2792 |

| FAT | −0.0235 | 0.0093 | −2.54 | 0.011 | −0.0417 | −0.0053 |

| CAT | 0.0128 | 0.0205 | 0.62 | 0.533 | −0.0273 | 0.0529 |

| GRW | −0.0446 | 0.0111 | −4.00 | 0.000 | −0.0664 | −0.0228 |

| Constant | 0.6091 | 0.2237 | 2.72 | 0.006 | 0.1706 | 1.0477 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tica, T.; Matkovski, B.; Đokić, D.; Jurjević, Ž. Characteristics of the Supply Chain of Tobacco and Tobacco Products: Evidence from Serbia. Agriculture 2023, 13, 1711. https://doi.org/10.3390/agriculture13091711

Tica T, Matkovski B, Đokić D, Jurjević Ž. Characteristics of the Supply Chain of Tobacco and Tobacco Products: Evidence from Serbia. Agriculture. 2023; 13(9):1711. https://doi.org/10.3390/agriculture13091711

Chicago/Turabian StyleTica, Teodora, Bojan Matkovski, Danilo Đokić, and Žana Jurjević. 2023. "Characteristics of the Supply Chain of Tobacco and Tobacco Products: Evidence from Serbia" Agriculture 13, no. 9: 1711. https://doi.org/10.3390/agriculture13091711

APA StyleTica, T., Matkovski, B., Đokić, D., & Jurjević, Ž. (2023). Characteristics of the Supply Chain of Tobacco and Tobacco Products: Evidence from Serbia. Agriculture, 13(9), 1711. https://doi.org/10.3390/agriculture13091711