Measuring Food Loss and Waste Costs in the Italian Potato Chip Industry Using Material Flow Cost Accounting

Abstract

:1. Introduction

2. Literature Review on Food Loss and Waste Measurement Methodologies

3. Materials and Methods

3.1. The Material Flow Cost Accounting Model

3.2. Definitions, Boundaries and Functional Units

3.3. Material Flows, Cost Categories and General Assumptions

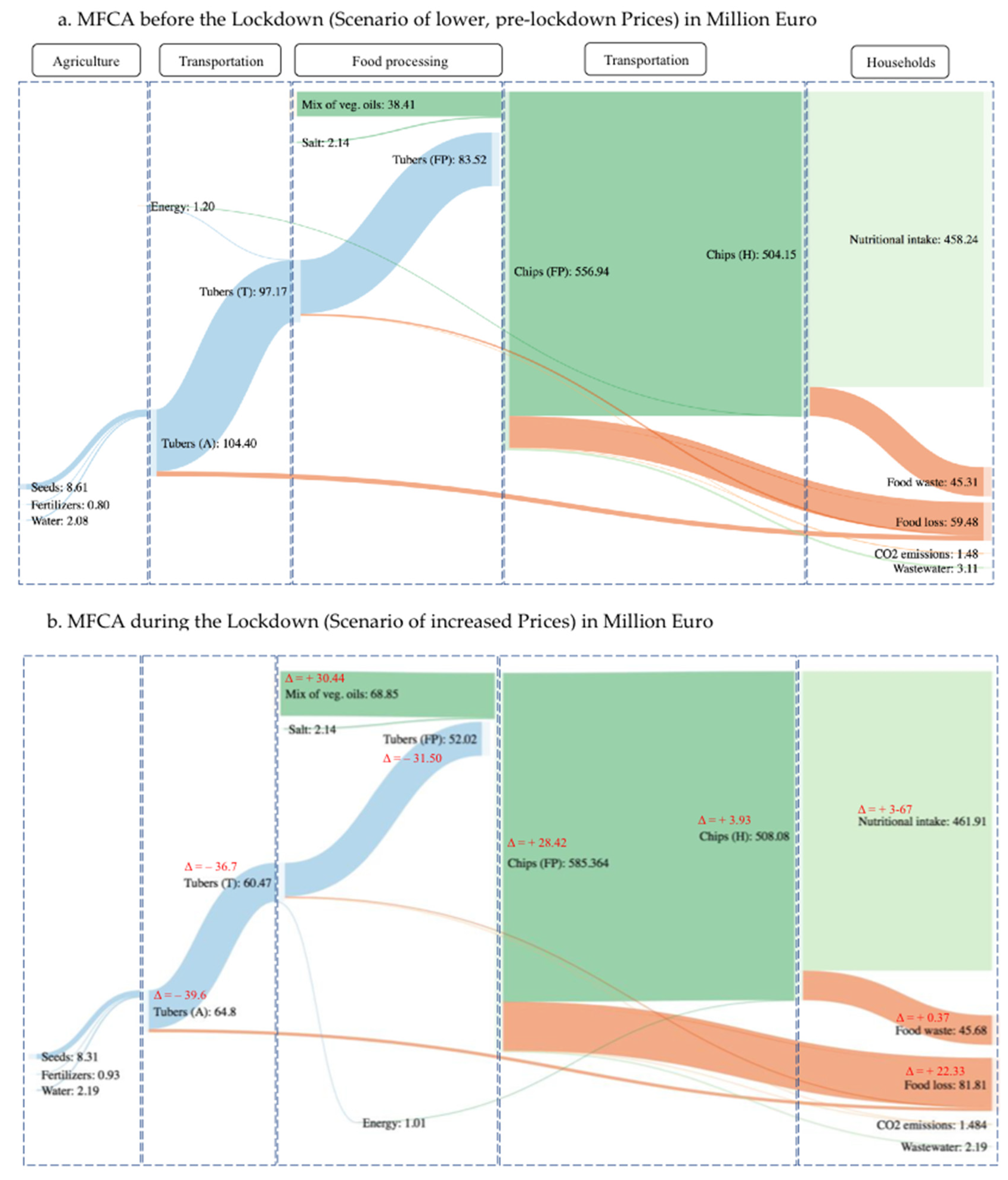

4. Results

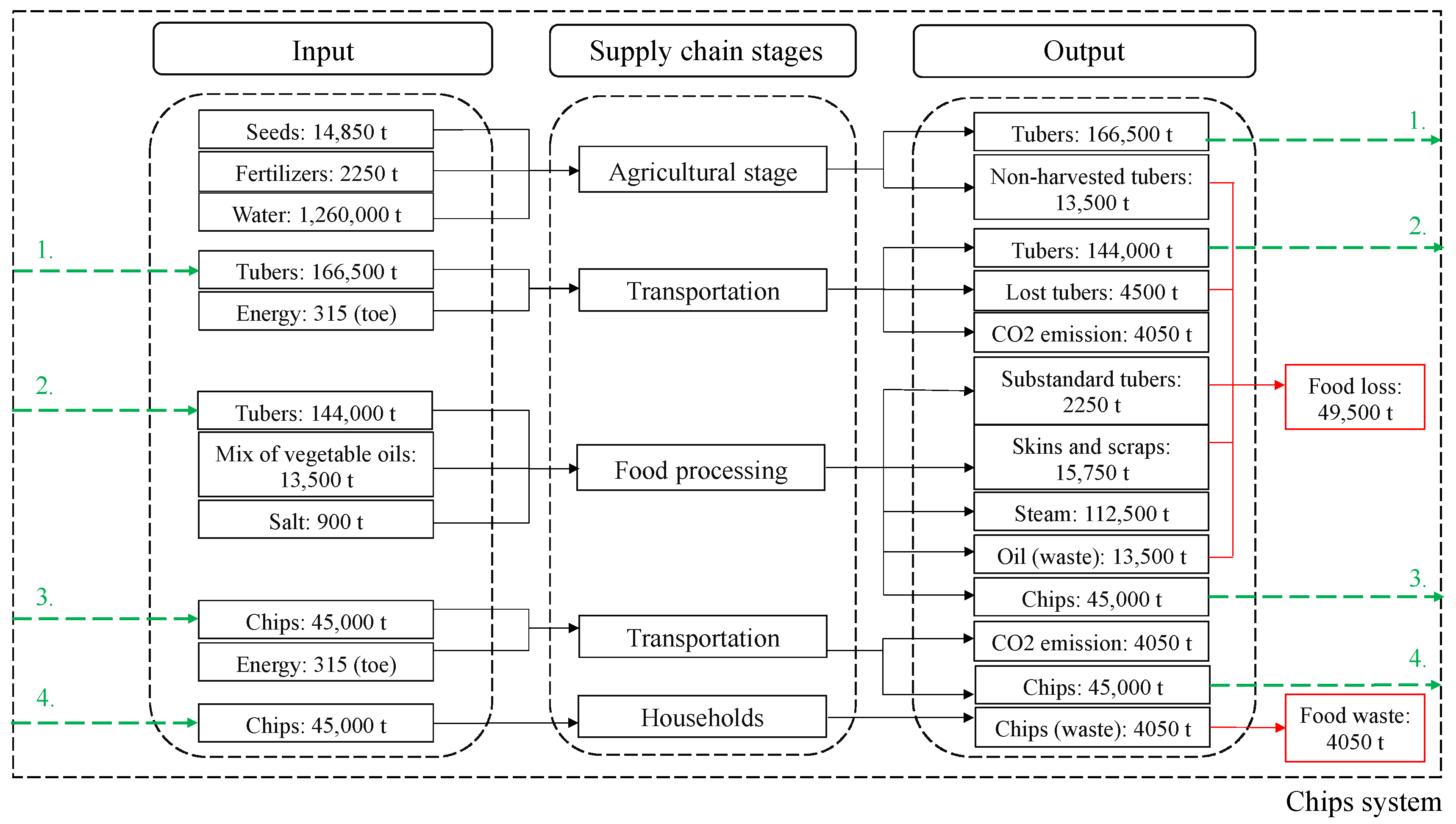

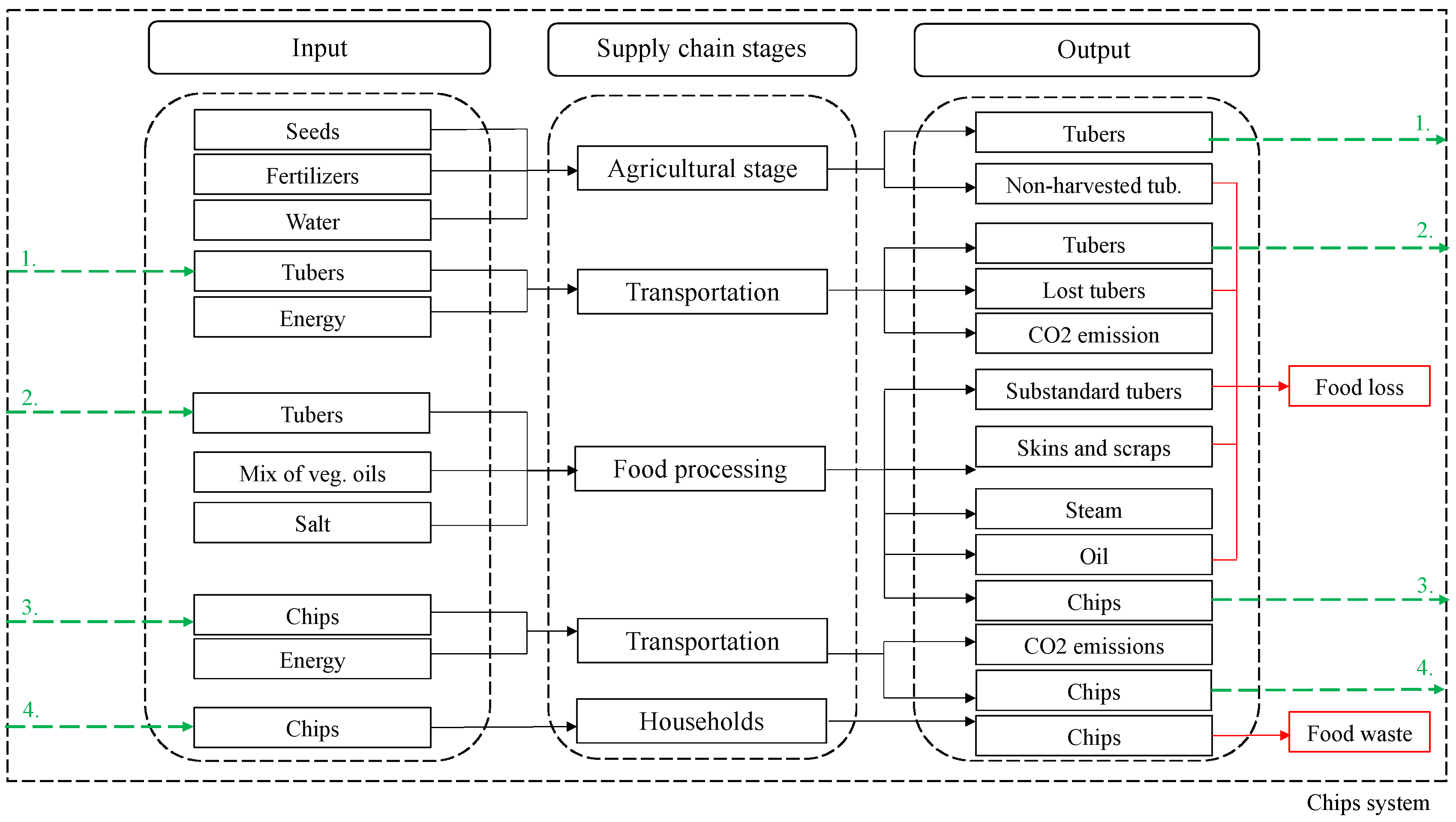

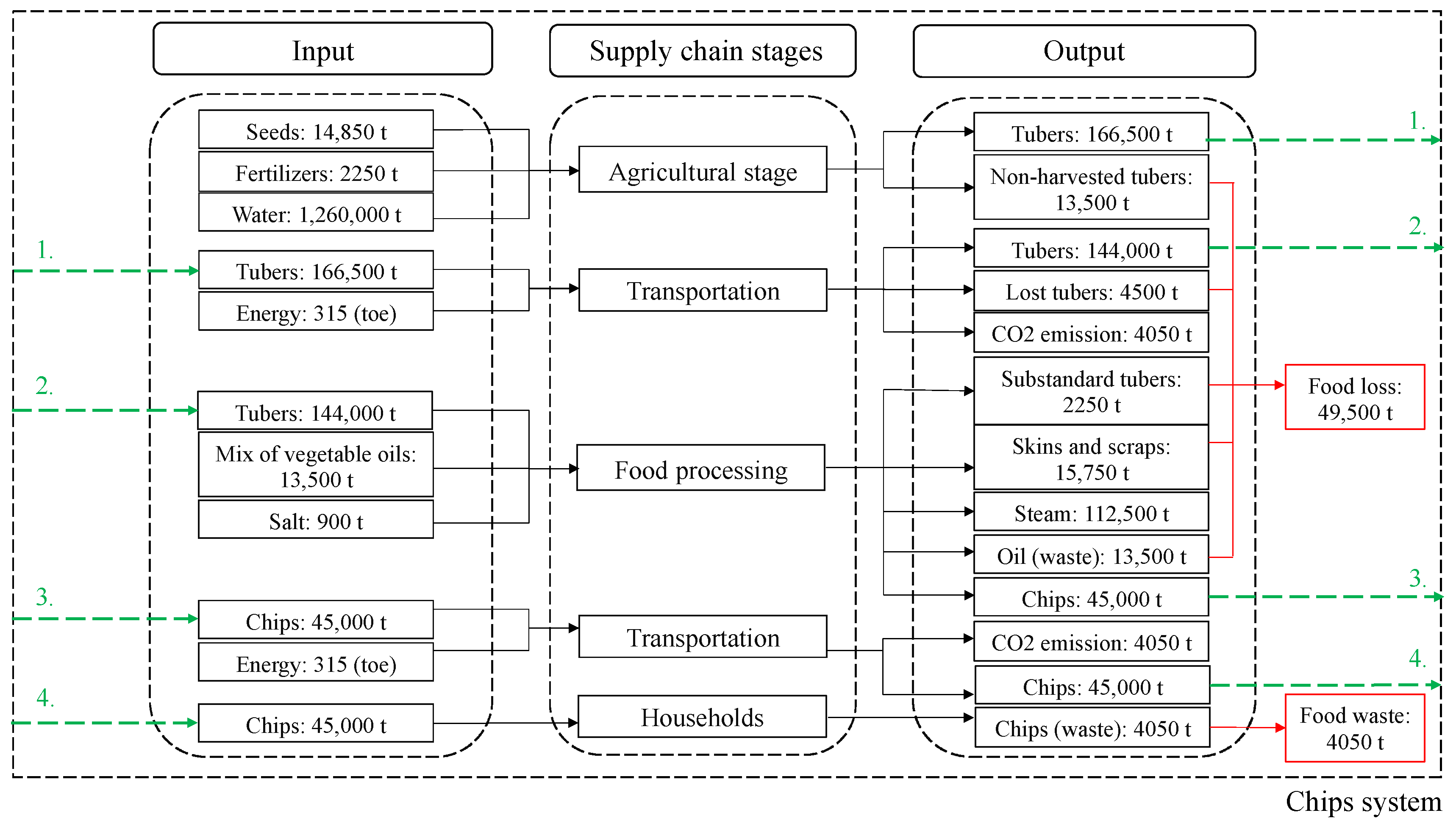

4.1. Material Flow Analysis for the Italian Potato Chip Industry

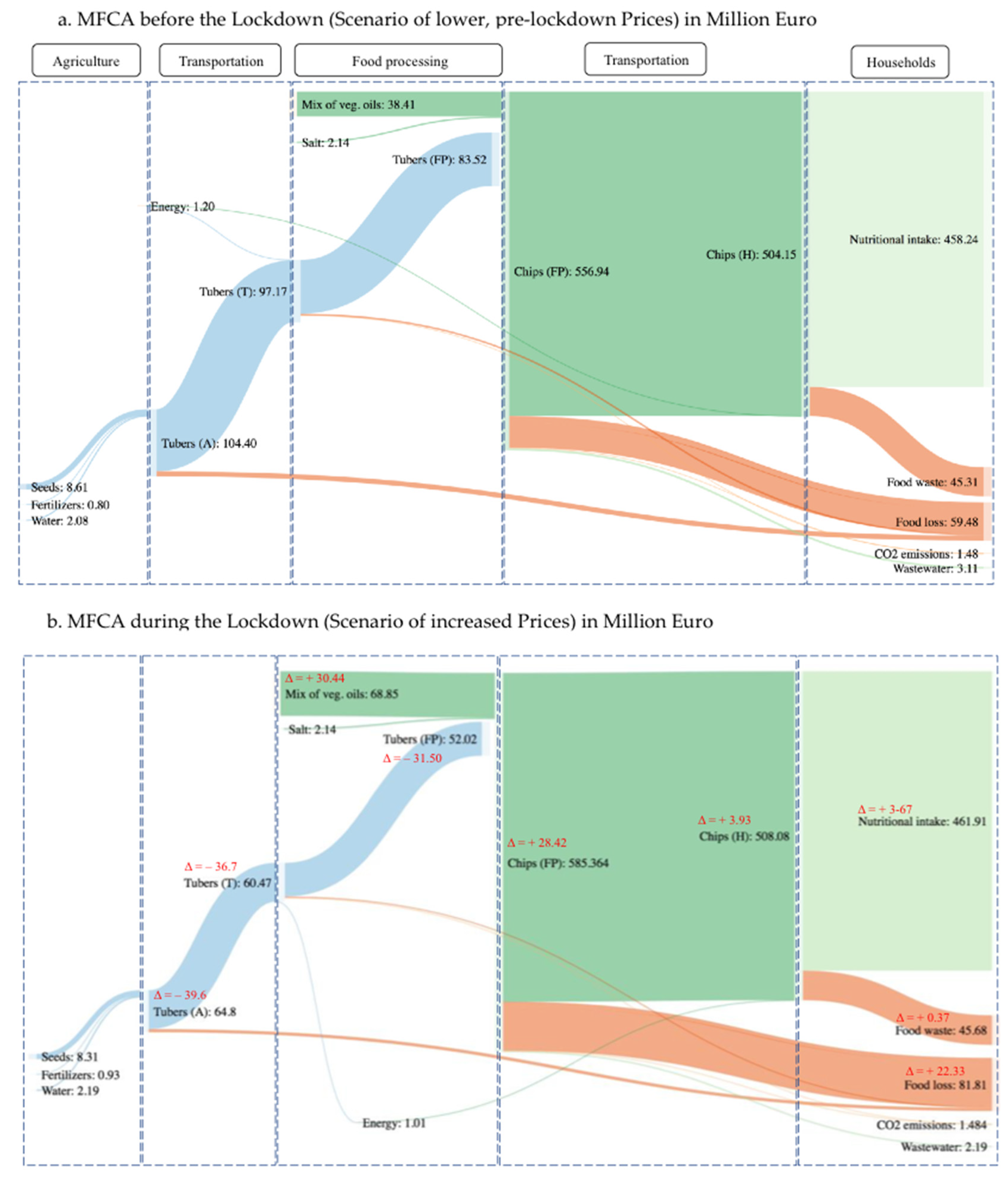

4.2. Material Flow Cost Accounting before and during the Lockdown

5. Discussion

5.1. Managerial Implications

5.2. Public Authorithies’ Implications

5.3. Conceptual Implications

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Zylbersztajn, D. Agribusiness systems analysis: Origin, evolution and research perspectives. Rev. Adm. 2017, 52, 114–117. [Google Scholar] [CrossRef] [Green Version]

- Food and Agriculture Organization of the United Nations. Agriculture Food Systems Transformation: From Strategy to Action; Food and Agriculture Organization of the United Nations: Rome, Italy, 2021. [Google Scholar]

- Food and Agriculture Organization of the United Nations. The Impact of Disasters and Crises on Agriculture and Food Security: 2021; Food and Agriculture Organization of the United Nations: Rome, Italy, 2021. [Google Scholar]

- Pérez-Escamilla, R. Food Security and the 2015-2030 Sustainable Development Goals: From Human to Planetary Health: Perspectives and Opinions. Curr. Dev. Nutr. 2017, 7, e000513. [Google Scholar] [CrossRef]

- Amicarelli, V.; Bux, C. Food waste measurement toward a fair, healthy and environmental-friendly food system: A critical review. Br. Food J. 2020, 123, 2907–2935. [Google Scholar] [CrossRef]

- Edwards, M.R.; Clifford, J.S. Reframing agribusiness: Moving from farm to market centric. J. Agribus. 2005, 23, 57–73. [Google Scholar]

- Ritchie, H.; Roser, M. Environmental Impacts of Food Production. OurWorldInData.org. Available online: https://ourworldindata.org/environmental-impacts-of-food (accessed on 15 July 2021).

- Food and Agriculture Organization of the United Nations. Food Wastage Footprint. Impacts on Natural Resources, Summary Report; Food and Agriculture Organization of the United Nations: Rome, Italy, 2013. [Google Scholar]

- Poore, J.; Nemecek, T. Reducing food’s environmental impacts through producers and consumers. Science 2018, 360, 987–992. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Pellegrini, M.; Ponzo, V.; Rosato, R.; Scumaci, E.; Goitre, I.; Benso, A.; Belcastro, S.; Crespi, C.; De Michieli, F.; Ghigo, E.; et al. Changes in weight and nutritional habits in adults with obesity during the “lockdown” period caused by the COVID-19 virus emergency. Nutrients 2020, 12, 2016. [Google Scholar] [CrossRef] [PubMed]

- Bakaloudi, D.R.; Jeyakumar, D.T.; Jayawardena, R.; Chourdakis, M. The impact of COVID-19 lockdown on snacking habits, fast-food and alcohol consumption: A systematic review of the evidence. Clin. Nutr. 2021. [Google Scholar] [CrossRef]

- Official Journal of European Union. Regulation (EC) No 1069/2009 of the European parliament and of the council of 21 October 2009-laying down health rules as regards animal by-products as derived products not no human consumption and repealing regulation (EU) No 1774/2002 (animal by-products regulation). Off. J. Eur. Un. 2009, 300, 33. [Google Scholar]

- Moraes, N.V.; Lermen, F.H.; Echeveste, M.E.S. A systematic literature review on food waste/loss prevention and minimization methods. J. Environ. Manag. 2021, 286, 112268. [Google Scholar] [CrossRef] [PubMed]

- Giordano, C.; Alboni, F.; Cicatiello, C.; Falasconi, L. Do discount food products end up in the bin? An investigation into the link between deal-prone shopping behavior and quantities of household food waste. Int. J. Consum. Stud. 2019, 43, 199–209. [Google Scholar] [CrossRef]

- Roe, B.E.; Qi, D.; Beyl, R.A.; Neubig, K.E.; Apolzan, J.W.; Martin, C.K. A randomized controlled trial to address consumer food waste with a technology-aided tailored sustainability intervention. Resour. Conserv. Recycl. 2022, 179, 106121. [Google Scholar] [CrossRef]

- Khalid, S.; Naseer, A.; Sahid, M.; Shah, G.M.; Ullah, M.I.; Waqar, A.; Abbas, T.; Imran, M.; Rehman, F. Assessment of nutritionl loss with food waste and factors governing this waste at household level in Pakistan. J. Clean. Prod. 2019, 206, 1015–1024. [Google Scholar] [CrossRef]

- Seabrook, J.A.; Gilliland, J.A. “Reduce Food Waste, Save Money”: Testing a novel intervention to reduce household food waste. Environ. Behav. 2021, 53, 151–183. [Google Scholar]

- Soma, T.; Li, B.; Maclaren, V. Food waste reduction: A test of three consumer awareness interventions. Sustainability 2020, 12, 907. [Google Scholar] [CrossRef] [Green Version]

- Cammarelle, A.; Lombardi, M.; Viscecchia, R. Packaging innovations to reduce food loss and waste: Are Italian manufacturers willing to invest? Sustainability 2021, 13, 1963. [Google Scholar] [CrossRef]

- Katajajuuri, J.M.; Silvennoinen, K.; Hartikainen, H.; Heikkila, L.; Reinikainen, A. Food waste in the Finnish food chain. J. Clean. Prod. 2014, 73, 322–329. [Google Scholar] [CrossRef]

- Tostivint, C.; de Veron, S.; Jan, O.; Lanctuit, H.; Hutton, Z.H.; Loubiere, M. Measuring food waste in a dairy supply chain in Pakistan. J. Clean. Prod. 2017, 145, 221–231. [Google Scholar] [CrossRef]

- Djekic, I.; Operta, S.; Djulancic, N.; Lorenzo, J.M.; Barba, F.J.; Djordjevic, V.; Tomasevic, I. Quantities, environmental footprints and beliefs associated with household food waste in Bosnia and Herzegovina. Waste Manag. Res. 2019, 37, 1250–1260. [Google Scholar] [CrossRef]

- Beretta, C.; Stoessel, F.; Baier, U.; Hellweg, S. Quantifying food losses and the potential for reduction in Switzerland. Waste Manag. 2013, 33, 764–773. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Islam, M.T.; Huda, N. Material flow analysis (MFA) as a strategic tool in E-waste management: Applications, trends and future directions. J. Environ. Manag. 2019, 244, 344–361. [Google Scholar] [CrossRef] [PubMed]

- Villalba, L. Material Flow Analysis (MFA) and waste characterizations for formal and informal performance indicators in Tandil, Argentina: Decision-making implications. J. Environ. Manag. 2020, 264, 110453. [Google Scholar] [CrossRef] [PubMed]

- Yogiswari, N.L.P.P.; Budiasih, I.G.A.N.; Sudana, I.P.; Mimba, N.P.S.H. Implementation of environmental cost accounting during the COVID-19 pandemic in medical waste management. Linguist. Cult. Rev. 2021, 6, 264–276. [Google Scholar] [CrossRef]

- Afshar, R.K.; Dekamin, M. Sustainability assessment of corn production in conventional and conservation tillage systems. J. Clean. Prod. 2022, 351, 131508. [Google Scholar] [CrossRef]

- Bux, C.; Amicarelli, V. Separate collection and bio-waste valorization in the Italian poultry sector by material flow analysis. J. Mater. Cycles Waste Manag. 2022, 24, 811–823. [Google Scholar] [CrossRef]

- United Nations Environment Programme. Food Waste Index. Report 2021; United Nations Environment Programme: Nairobi, Kenya, 2021. [Google Scholar]

- Garcia-Herrero, L.; De Menna, F.; Vittuari, M. Food waste at school. The environmental and cost impact of a canteen meal. Waste Manag. 2019, 100, 249–258. [Google Scholar] [CrossRef] [PubMed]

- Omolayo, Y.; Feingold, B.J.; Neff, R.A.; Romeiko, X.B.X. Life cycle assessment of food loss and waste in the food supply chain. Resour. Conserv. Recycl. 2021, 164, 105119. [Google Scholar] [CrossRef]

- Christ, K.L.; Burritt, R. Material flow cost accounting for food waste in the restaurant industry. Br. Food J. 2017, 119, 600–612. [Google Scholar] [CrossRef]

- May, N.; Guenther, E. Shared benefit by material flow cost accounting in the food supply chain. The case of berry pomace as upcycled by-product of a black currant juice production. J. Clean. Prod. 2020, 245, 118946. [Google Scholar] [CrossRef]

- Piwowar-Sulej, K.; Krzywonos, M.; Kwil, I. Environmental entrepreneurship–Bibliometric and content analysis of the subject literature based on H-Core. J. Clean. Prod. 2021, 295, 126277. [Google Scholar] [CrossRef]

- Herzig, C.; Viere, T.; Schaltegger, S.; Burritt, R.L. Environmental Management Accounting. Case Studies of South-East Asian Companies; Routledge, Taylor & Francis Group: Oxfordshire, UK, 2012. [Google Scholar]

- Arieftiara, D.; Theresa, R.M.; Sari, R. Sustainability in health service industry: The implementation of material flow cost accounting (MFCA) as an eco-efficient analysis. J. Southeast Asian Res. 2021, 2021, 747009. [Google Scholar] [CrossRef]

- Ho, J.Y.; Ng, D.K.S.; Kin Wan, Y.; Andiappan, V. Synthesis of wastewater treatment plant based on minimal waste generation cost: A material flow cost accounting (MFCA) approach. Process Saf. Environ. Prot. 2021, 148, 559–578. [Google Scholar] [CrossRef]

- Dechampai, D.; Homrossukon, S.; Wongthatsanekorn, W.; Ekkachai, K. Applying material flow cost accounting and two-dimensional, irregularly shaped cutting stock problems in the lingerie manufacturing industry. Appl. Sci. 2021, 11, 3142. [Google Scholar] [CrossRef]

- Burritt, R.L.; Hahn, T.; Schaltegger, S. Towards a comprehensive framework for environmental management accounting—Links between business actors and environmental management accounting tools. Aust. Account. Rev. 2008, 12, 39–50. [Google Scholar] [CrossRef]

- ISO 14501:2011; Environmental Management–Material Flow Cost Accounting–General Framework. ISO/TC 207. International Organization for Standardization: Geneva, Switzerland, 2011; pp. 1–38.

- Jasch, C. Environmental and Material Flow Cost Accounting; Springer: Dordrecht, The Netherlands, 2009. [Google Scholar]

- Brunner, P.H.; Rechberger, H. Handbook of Material Flow Analysis. For Environmental, Resource and Waste Engineers, 2nd ed.; CRC Press: Boca Raton, FL, USA; Taylor & Francis Group, LLC: London, UK, 2017. [Google Scholar]

- Jakrawatana, N.; Pingmuangleka, P.; Gheewala, S.H. Material flow management and cleaner production of cassava processing for future food, feed and fuel in Thailand. J. Clean. Prod. 2016, 134, 633–641. [Google Scholar] [CrossRef]

- Wan, Y.K.; Ng, R.T.L.; Ng, D.K.S.; Tan, R.R. Material flow cost accounting (MFCA)–Based approach for prioritisation of waste recovery. J. Clean. Prod. 2015, 107, 602–614. [Google Scholar] [CrossRef]

- Dierkes, S.; Siepelmeyer, D. Production and cost theory-based material flow cost accounting. J. Clean. Prod. 2019, 235, 483–492. [Google Scholar] [CrossRef]

- Kokubu, K.; Kitada, H. Material flow cost accounting and existing management perspectives. J. Clean. Prod. 2015, 108, 1279–1288. [Google Scholar] [CrossRef]

- Sahu, A.K.; Padhy, R.K.; Das, D.; Gautam, A. Improving financial and environmental performance through MFCA: A SME case study. J. Clean. Prod. 2021, 279, 123751. [Google Scholar] [CrossRef]

- Hendriks, C.R.; Obernosterer, D.; Müller, S.; Kytzia, P.; Baccini, P.; Brunner, P.H. Material flow analysis: A tool to support environmental policy decision making. Case-studies on the city of Vienna and the Swiss lowlands. Int. J. Justice Sustain. 2000, 5, 311–328. [Google Scholar] [CrossRef]

- Food and Agriculture Organization of the United Nations. Global Food Losses and Food Waste: Extent, Causes and Prevention; Food and Agriculture Organization of the United Nations: Rome, Italy, 2011. [Google Scholar]

- Hartikainen, H.; Mogensen, L.; Svanes, E.; Franke, U. Food waste quantification in primary production–The Nordic countries as a case study. Waste Manag. 2018, 71, 502–511. [Google Scholar] [CrossRef]

- Rubinstein, R.Y.; Kroese, D.P. Simulation and the Monte Carlo Method, 3rd ed.; Wiley: Hoboken, NJ, USA, 2017. [Google Scholar]

- Principato, L.; Secondi, L.; Cicatiello, C.; Mattia, G. Caring more about food: The unexpected positive effect of the COVID-19 lockdown on household food management and waste. Socio-Econ. Plan. Sci. 2020, 100953, in press. [Google Scholar] [CrossRef]

- Statista. Average Prices of Diesel Fuel in Italy from 2000 to 2021; Statista Research Department: New York, NY, USA, 2021. [Google Scholar]

- U.S. Environmental Protection Agency. Emission Factors for Greenhouse Gas Inventories. Available online: https://www.epa.gov/sites/production/files/2018-03/documents/emission-factors_mar_2018_0.pdf (accessed on 17 July 2021).

- ISMEA. Osservatorio Patate. Prezzi Mensili All’origine. Available online: http://www.ismeamercati.it/flex/cm/pages/ServeBLOB.php/L/IT/IDPagina/4834#MenuV (accessed on 14 July 2021).

- ISTAT. Prezzi Al Consumo. Available online: https://www.istat.it/it/archivio/241413 (accessed on 19 July 2021).

- Camaggio, G.; Lagioia, G. La Trasformazione Industriale Della Patata; Dal Tubero Al Fast Food. Quaderno del Dipartimento di Scienze Merceologiche; Progedit: Bari, Italy, 2002; Volume 27, pp. 1–56. [Google Scholar]

- Hoepli, U. (Ed.) Manuale di Agricoltura, 2nd ed.; Hopeli: Milano, Italy, 1997. [Google Scholar]

- Mouron, P.; Willersinn, C.; Mobius, S.; Lansche, J. Environmental profile of the Swiss supply chain for French fries: Effects of food loss reduction, loss treatments and process modifications. Sustainability 2016, 8, 1214. [Google Scholar] [CrossRef] [Green Version]

- Sablani, S.; Mujumdar, A. Drying of Potato, Sweet Potato, and Other Roots. In Handbook of Industrial Drying, 4th ed.; Taylor & Francis Group, LLC: Boca Raton, FL, USA, 2006. [Google Scholar]

- Gustavsson, J.; Cedeberg, C.; Sonesson, U.; van Otterdijk, R.; Meybeck, A. Global Food Losses and Waste. Extent, Causes, Prevention; Food and Agriculture Organization of the United Nations: Rome, Italy, 2011. [Google Scholar]

- Consorzio Comuni Acquedotto Monferrato. Tariffe in Vigore 01/01/2019. Available online: https://www.ccam.it/tariffe-vigore-01012019 (accessed on 18 July 2021).

- Consorzio Comuni Acquedotto Monferrato. Tariffe in Vigore 01/01/2021. Available online: https://www.ccam.it/tariffe-vigore-01012021 (accessed on 18 July 2021).

- Camera di Commercio Alessandria. Listino Settimanale dei Prezzi All’ingrosso dei Prodotti Agricoli. Available online: http://images.al.camcom.gov.it/f/PriceLists/archive/ListinoPrezzi_1_07-10-2019.pdf (accessed on 18 July 2021).

- Camera di Commercio Alessandria. Listino Settimanale dei Prezzi All’ingrosso dei Prodotti Agricoli (Fertilizzanti). Available online: http://www.al.camcom.gov.it/PriceLists/Pub/Item?id_level_2=10 (accessed on 18 July 2021).

- ISMEA. Oli Vegetali–News Mercati. Available online: http://www.ismeamercati.it/flex/cm/pages/ServeBLOB.php/L/IT/IDPagina/9283 (accessed on 18 July 2021).

- ISMEA. Olio di Semi Raffinati–Prezzi per Piazza All’ingrosso. Available online: http://www.ismeamercati.it/flex/cm/pages/ServeBLOB.php/L/IT/IDPagina/927 (accessed on 18 July 2021).

- OECD. Effective Carbon Rates 2021. Pricing Carbon Emissions through Taxes and Emissions Trading; OECD Publishing: Paris, France, 2021. [Google Scholar]

- Eurostat. Intra EU-28 Export of Potatoes, 2018 (1000 EU, 1000 Tonnes). Eurostat, Statistics Explained, European Union 1995–2021; Eurostat: Luxembourg, 2018. [Google Scholar]

- Eurostat. The EU Potato Sector-Statistics on Production, Prices and Trade, European Union, 1995–2021; Eurostat: Luxembourg, 2021. [Google Scholar]

- Amica Chips. Amica Chips, Una Storia Tutta Italiana. Available online: https://allfoodonline.com/amica-chips-una-storia-tutta-italiana/ (accessed on 28 July 2021).

- Food. Amica Chips Festeggia I Primi 25 Anni. Available online: https://www.foodweb.it/2015/05/amica-chips-festeggia-i-primi-25-anni/ (accessed on 28 July 2021).

- San Carlo. L’azienda. Available online: https://www.sancarlo.it/it/publishing1.asp?ArticleId=9 (accessed on 28 July 2021).

- ISTAT. Nota Mensile Sull’andamento Dell’economia Italiana. Available online: https://www.istat.it/it/files/2020/04/notamensile_marzo_def.pdf (accessed on 28 July 2021).

- Coldiretti. Coronavirus, Balzo Nell’acquisto di Prodotti Alimentari. Available online: https://www.coldiretti.it/economia/coronavirus-balzo-nellacquisto-di-prodotti-alimentari (accessed on 28 July 2021).

- Nielsen. Coronavirus: La Spesa in Quarantena. The NielsenCompany (US). Available online: https://nielseniq.com/global/it/insights/analysis/2020/coronavirus-la-spesa-in-quarantena/ (accessed on 28 July 2021).

- Nielsen. Insights. Largo Consumo e Distribuzione. The NielsenCompany (US). Available online: https://www.nielsen.com/it/it/insights/ (accessed on 28 July 2020).

- STAN (subSTance flow ANalysis), Technische Universtitat Wien, Institute for Water Quality, Resource and Waste Management. Funded by ARA–Altstoff Recycling Austria, Lebensministerium, Federal State of Austria. Available online: https://www.stan2web.net (accessed on 28 July 2020).

- European Central Bank. Consumption Patterns and Inflation Measurement Issues during the COVID-19 Pandemic. Available online: https://www.ecb.europa.eu/pub/economic-bulletin/focus/2020/html/ecb.ebbox202007_03~e4d32ee4e7.en.html (accessed on 18 July 2021).

- Cencic, O. Treatment of Data Uncertainties in MFA. In Handbook of Material Flow Analysis: For Environmental, Resource, and Waste Engineers, 2nd ed.; Brunner, P.H., Rechberger, H., Eds.; CRC Press—Taylor & Francis Group: Boca Raton, FL, USA, 2016; pp. 94–148. [Google Scholar]

- Rechberger, H.; Cencic, O.; Fruhwirth, R. Uncertainty in material flow analysis. J. Ind. Ecol. 2014, 18, 159–160. [Google Scholar] [CrossRef]

- Wang, Y.; Ma, H. Analysis of uncertainty in material flow analysis. J. Clean. Prod. 2018, 170, 1017–1028. [Google Scholar] [CrossRef]

- Scacchi, A.; Catozzi, D.; Boietti, E.; Bert, F.; Siliquini, R. COVID-19 lockdown and self-perceived changes of food choice, waste, impulse buying and their determinants in Italy: QuarantEat, a cross-sectional study. Foods 2021, 10, 306. [Google Scholar] [CrossRef]

- Pappalardo, G.; Cerroni, S.; Nayaga, R.F.; Yang, W. Impact of COVID-19 household food waste: The case of Italy. Front. Nutr. 2020, 7, 585090. [Google Scholar] [CrossRef]

- Cialani, C.; Mortazavi, R. The cost of urban waste management: An empirical analysis of recycling patterns in Italy. Front. Sustain. Cities 2020, 2, 8. [Google Scholar] [CrossRef]

- European Environment Agency. Typical Charge (Gate Fee and Landfill Tax) for Legal Landfilling of Non-Hazardous Municipal Waste in EU Member States and Regions; European Union: Copenhagen, Denmark, 2013. [Google Scholar]

- Schmidt, M.; Nakajima, M. Material flow cost accounting as an approach to improve resource efficiency in manufacturing companies. Resources 2013, 2, 358–369. [Google Scholar] [CrossRef]

- Nishitani, K.; Kokubu, K.; Wu, Q.; Kitada, H.; Guenther, E.; Guenther, T. Material flow cost accounting (MFCA) for the circular economy: An empirical study of the triadic relationship between MFCA, environmental performance, and the economic performance of Japanese companies. J. Environ. Manag. 2022, 303, 114219. [Google Scholar] [CrossRef] [PubMed]

- IFAC. International Guidance Document: Environmental Management Accounting. Available online: https://www.ifac.org/knowledge-gateway/preparing-future-ready-professionals/publications/international-guidance-document-environmental-management-accounting (accessed on 31 March 2022).

- Tran, T.T.; Herzig, C. Improving decision-making through material flow cost accounting: The case of VietGreen bottled mineral water company. Int. Food Agribus. Manag. Rev. 2021, 25, 37–48. [Google Scholar] [CrossRef]

- Närvänen, E.; Mesiranta, N.; Mattila, M.; Heikkine, A. Food Waste Management: Solving the Wicked Problem; Springer Nature: London, UK, 2019. [Google Scholar]

- Amicarelli, V.; Rana, L.R.; Lombardi, M.; Bux, C. Material flow analysis and sustainability of the Italian meat industry. J. Clean. Prod. 2021, 299, 126902. [Google Scholar] [CrossRef]

- Kuiper, M.; Cui, H.D. Using food loss reduction to reach food security and environmental objectives–A search for promising leverage points. Food Policy 2021, 98, 101915. [Google Scholar] [CrossRef]

- Goossens, Y.; Wegner, A.; Schmidt, T. Sustainability assessment of food waste prevention measures: Review of existing evaluation practices. Front. Sustain. Food Syst. 2019, 3, 90. [Google Scholar] [CrossRef]

- Kambanou, M.L.; Lindahl, M. A literature review of life cycle costing in the product-service system context. Proc. CIRP 2016, 47, 186–191. [Google Scholar] [CrossRef] [Green Version]

- Huang, C.H.; Liu, S.M.; Hsu, N.Y. Understanding global food surplus and food waste to tackle economic and environmental sustainability. Sustainability 2020, 12, 2892. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

| Supply Chain Stage | Input | t | Output | t |

|---|---|---|---|---|

| Agricultural stage | Seeds | 0.33 | Non-harvested tubers Tubers | 0.3 4 |

| Fertilizers | 0.05 | |||

| Water | 28 | |||

| Transportation | Energy | 0.007 | CO2 emissions | 0.10 |

| Non-harvested tubers | 0.3 | |||

| Tubers | 4 | Tubers lost | 0.1 | |

| Tubers | 3.6 | |||

| Food processing | Mix of oils | 0.3 | Mix of oils | 0.3 |

| Salt | 0.02 | Steam | 2.2 | |

| Substandard tubers | 0.05 | |||

| Tubers | 3.6 | Skins and scraps | 0.35 | |

| Chips | 1 | |||

| Transportation | Energy | 0.007 | CO2 emissions | 0.10 |

| Chips | 1 | Chips | 1 | |

| Households | Chips | 1 | Food waste (at 9%) | 0.09 |

| Cost Category | Item | Scenario 1 | Scenario 2 | Δ (%) |

|---|---|---|---|---|

| Material costs | Tubers | 580 | 360 | −38% |

| Fertilizers | 355 | 415 | 17% | |

| Seeds | 428 | 560 | 31% | |

| Water | 1.65 | 1.74 | 5% | |

| Mix of veg. oils | 2.86 | 5.1 | 78% | |

| Salt | 160 | 160 | N/A | |

| Chips | 11.19 | 11.28 | 0.80% | |

| Energy costs | Fuel | 1.72 | 1.53 | −10% |

| Waste management costs | Recovery | 15 | 15 | N/A |

| Additional costs | CO2 emissions | 60 | 60 | N/A |

| Scenario 1 | ||||

|---|---|---|---|---|

| Ratios | Input | Tubers (A) | Chips (D) | Chips (H) |

| Food loss | 111.72% | 56.97% | 10.68% | 12.98% |

| Food waste | 85.11% | 43.40% | 8.14% | 9.89% |

| Scenario 2 | ||||

| Ratios | Input | Tubers (A) | Chips (D) | Chips (H) |

| Food loss | 99.26% | 126.25% | 13.98% | 17.71% |

| Food waste | 55.42% | 55.42% | 7.80% | 9.89% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Amicarelli, V.; Roe, B.E.; Bux, C. Measuring Food Loss and Waste Costs in the Italian Potato Chip Industry Using Material Flow Cost Accounting. Agriculture 2022, 12, 523. https://doi.org/10.3390/agriculture12040523

Amicarelli V, Roe BE, Bux C. Measuring Food Loss and Waste Costs in the Italian Potato Chip Industry Using Material Flow Cost Accounting. Agriculture. 2022; 12(4):523. https://doi.org/10.3390/agriculture12040523

Chicago/Turabian StyleAmicarelli, Vera, Brian E. Roe, and Christian Bux. 2022. "Measuring Food Loss and Waste Costs in the Italian Potato Chip Industry Using Material Flow Cost Accounting" Agriculture 12, no. 4: 523. https://doi.org/10.3390/agriculture12040523

APA StyleAmicarelli, V., Roe, B. E., & Bux, C. (2022). Measuring Food Loss and Waste Costs in the Italian Potato Chip Industry Using Material Flow Cost Accounting. Agriculture, 12(4), 523. https://doi.org/10.3390/agriculture12040523