Regime-Specific Quant Generative Adversarial Network: A Conditional Generative Adversarial Network for Regime-Specific Deepfakes of Financial Time Series

Abstract

:1. Introduction

- The use of a structural breakpoint algorithm, greedy Gaussian segmentation [20], to learn time-dependent class categories (‘regimes’) to be used as embedding conditions and cluster time series data in pre-processing to train the conditional RSQGAN;

- A user-controlled hyper-parameter method in RSQGAN topological design (‘z-clipping’) as originally proposed by Brock et al. [21] in BigGAN, which enables users to directly control the variability of synthetic data outputs; and

- An empirical evaluation of the selection of GAN performance metrics for specifically evaluating synthetic FTS data quality for rarer crisis regimes.

2. Background

Generative Adversarial Networks (GANs)

- Mode collapse. The true data distribution is likely to be high-dimensional and multi-modal. Mode collapse can occur if, during training, the discriminator network overfits in its ability to identify generated fakes. The generator network then responds by restricting fake samples to modes that are less likely to be classified as fakes. The progressive overfitting of the discriminator within this subset causes the density of generated samples to concentrate into a shrinking support space. Despite this, observed generator and discriminator losses continue to shrink but generated samples become invariant. Conversely, another cause of mode collapse could be from vanishing discriminator gradients, which result in stalled learning for the generator network. Methods for dealing with discriminator overfitting include weight regularisation [32], regularisation by discriminator learning from stochastically corrupted inputs [33], using alternative loss functions such as Wasserstein loss (WGAN) [34] and applying gradient penalties in the discriminator learning process (WGAN-GP) [35].

- Training non-convergence. Though convergence may not indicate training success if mode collapse occurs, non-convergence in the adversarial training of vanilla GANs may also indicate failure. The nature of adversarial training and non-convex joint loss functions can lead to oscillatory behaviour. The oscillatory non-convergence of losses may not produce desirable or stable results for the learned DGP. Therefore, increasingly unstable representations of the DGP could be learned. Non-convergence can also be caused by an underfitting discriminator or vanishing discriminator gradient that results in a generator’s failure to learn. Interested readers are referred to GAN meta-studies that examine the effectiveness of discriminator regularisation and loss functions to manage the non-convergence [36] and critical analysis of theoretical supports for reducing mode collapse and non-convergence in the image data domain [23].

- Quality evaluation. As the above discussion argues that the overall GAN performance cannot be reliably judged by observing training losses, other evaluation metrics would be needed. Evaluation metrics would need to consider variability across modes and output quality for each mode. Subjective human evaluation could apply for data domains such as images or sound, though these are not robust measures for model benchmarking. It was argued by Theis et al. [37] that GANs could be used for a number of purposes (e.g., unsupervised feature learning, density estimation, in-filling, etc.), the quality of a GAN should be evaluated based on its originally intended purpose. However, quantitative evaluation metrics and subjective human assessment measures do not necessarily correlate to the performance of the GAN’s objective. For image GANs, quantitative evaluation methods such as inception score [38] and Fréchet inception distance [39] metrics were developed to correlate with performance for image synthesis tasks. For conditional image GANs, the Fréchet joint distance was proposed by DeVries et al. [40] to explicitly metricate inter-mode variability and intra-mode quality over a joint Gaussian distribution in embedded image and conditioning spaces. By contrast, in the FTS data domain, the GAN output quality cannot easily be subjectively judged by visual inspection. Instead, simulated FTS data are judged with reference to a set of market heuristics called stylised facts [41,42,43] as outlined in Section 5.4 below.

3. Related Work

- Stability improvements, which deal with issues such as mode collapse and non-convergence;

- Evaluation improvements, which derive numerical measures to evaluate GAN output quality; and

- Architectural improvements, which aim to improve GAN output quality, applied across domains.

3.1. Stability Improvements

3.2. Evaluation Improvements

3.3. Architectural Improvements

- Conditional GANs (cGANs) [18]—an improvement to ensure deliberate generation from distinct class modes;

- ‘z-skipping’ and ‘z-clipping’ [21]—improvements to class conditional synthetic quality, while giving user control to synthetic data size and the ability to explicitly trade off synthetic fidelity to real training data against synthetic variety, respectively.

4. Related Work: Generative FTS Models

- Density estimation. Though GANs implicitly learn latent data densities, Kondratyev and Schwarz [17] demonstrate that a restricted Boltzmann machine (RBM) with stochastic Bernoulli activations [49] could estimate joint densities and higher moments of the DGP for multivariate FX log-return data, as well as reproduce desired autocorrelation and non-stationary behaviours via a controlled early stopping ‘thermalisation’ parameter.

- Generating synthetic data. Other approaches explored for generative FTS modelling included denoising autoencoders and style transfer for FX data [50] and multivariate Gaussian sequence mixtures [51]. FTS GAN models in the literature used various network topologies for generator and discriminator networks. Takahashi et al. [11] developed FIN-GAN, which used an ensemble product of CNN and MLP outputs to model US equities. Wiese et al. [12] developed Quant GAN, which used a TCN with skip layers to jointly learn generative models for drift and volatility stochastic processes akin to GARCH model classes for the S&P500. Only a few papers [13,14,15] applied cGANs for FTS generative modelling. Koshiyama et al. [13] used single-hidden-layer MLP networks to train cGANs conditioned on 1 year (252 days) of historical returns to generate 5 years of synthetic data (1260 days) for 573 different assets spanning equities, fixed income, and FX. de Meer Pardo [14] used deep CNNs with combinations of WGAN-GP [35] and relativistic average critic losses (RaGAN) [52] and conditioning on the previous 100 days of S&P500 returns to jointly simulate 100 days of S&P500 and VIX synthetic data. Fu et al. [15] used a three-layer MLP architecture with WGAN [33] critic loss and conditioning on regime category (normal versus crisis) to generate next-day synthetic data for two US financial stocks. More recently, Marti [16] explored the generative modelling of very-high-dimensional FTS correlation matrices using a deep convolutional GAN (DCGAN) [24]. As of the time of writing, it is the only study known to us that has evaluated GAN performance based on its ability to simulate characteristics of empirically studied multivariate FTS behaviour.

5. Methodologies

5.1. Models

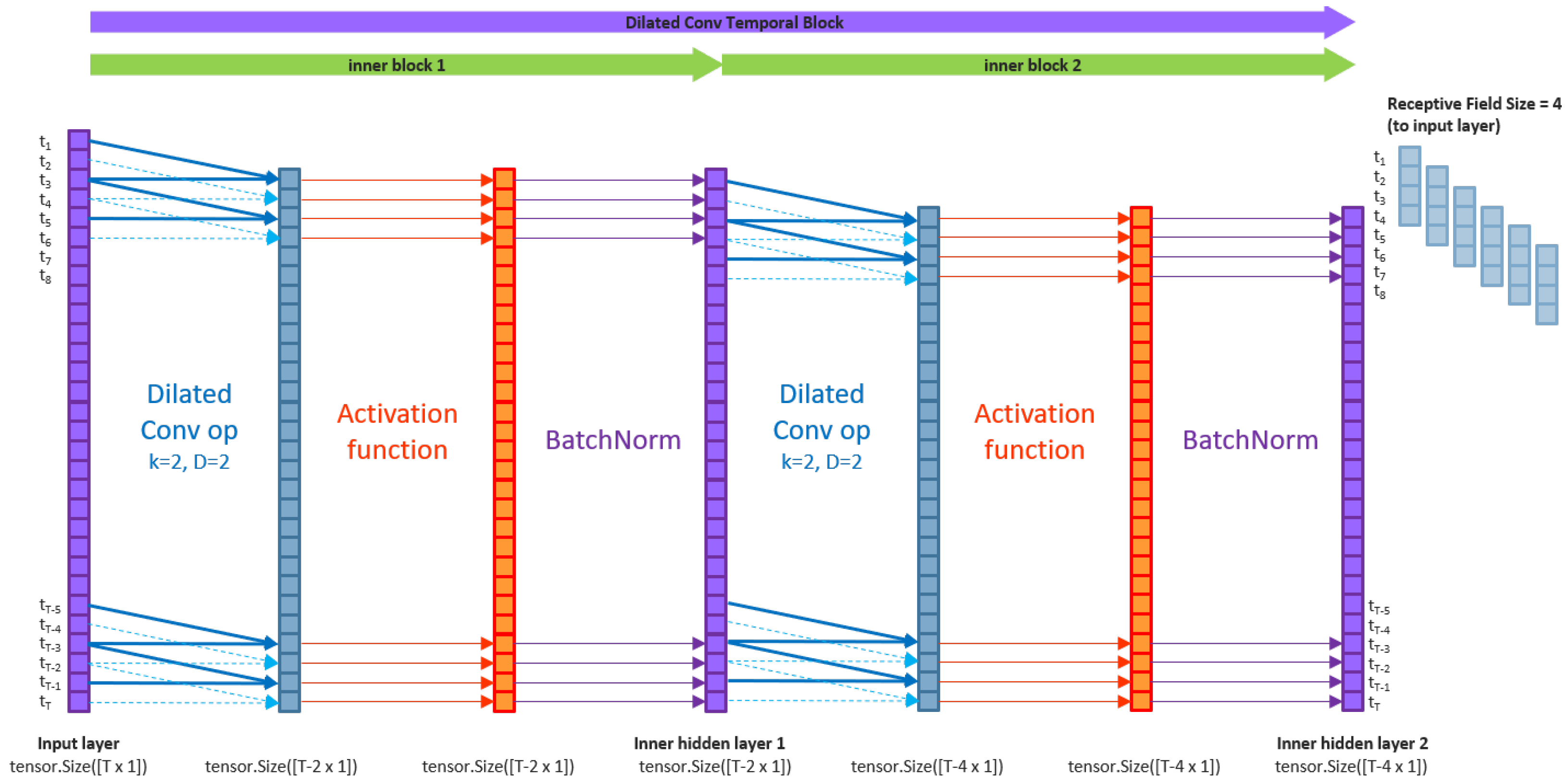

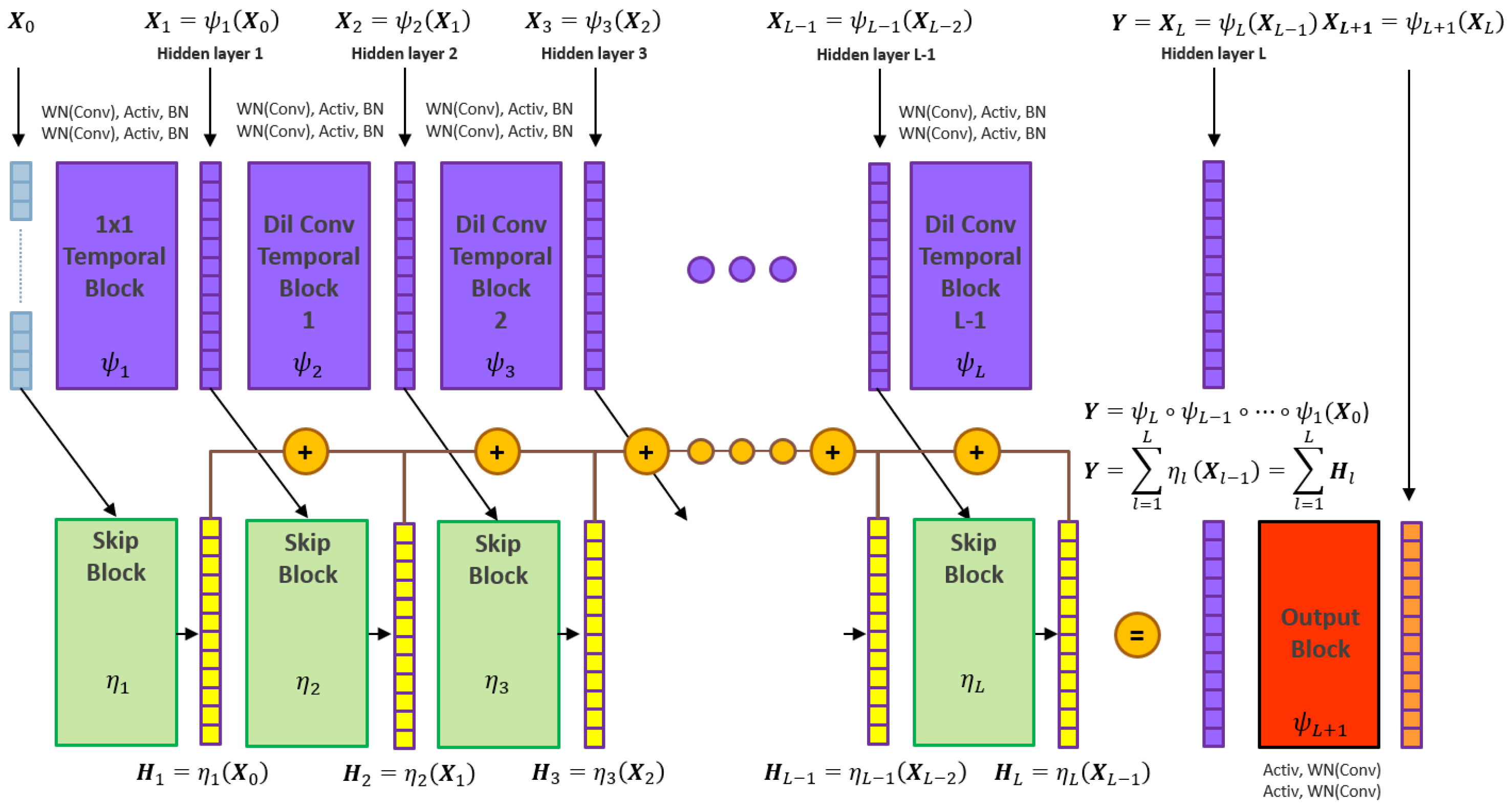

5.1.1. Temporal Convolutional Networks

5.1.2. From TCN to Quant GAN

5.1.3. RSQGAN

5.1.4. RSQGAN Model

5.1.5. RSQGAN Training Procedure

| Algorithm 1: RSQGAN training |

|

5.2. Data

5.3. Experimental Design

5.4. Evaluation by Stylised Facts

- Linear unpredictability [43] refers to the rapid decay of return autocorrelations even over small time lags, which reflects some evidence of market efficiency. This is captured by examining the autocorrelation function (ACF) of returns up to some maximum time lag.

- Heavy-tailed return distribution [43,53] refers to the phenomenon where the return distribution density fits a power, rather than exponential, law function. There is a tendency for very large positive returns for some stocks, which manifest as excess return kurtosis relative to a Gaussian distribution.

- Volatility clustering [42] refers to the phenomenon where periods of high volatility (temporal standard deviation of returns) tend to be autocorrelated with periods of high volatility. This can be observed by fitting the ACF of absolute log-returns to a power-law function with low decay parameter .

- Leverage effect [54,55] refers to the observation that past price returns are negatively correlated with future volatility. It could be observed that the numerator of the lead-lag correlation expression , given by , is negative if, for , , i.e., negative returns predict higher future volatility (and, vice-versa, that positive returns predict lower future volatility).

- Coarse–fine volatility correlation [56,57,58] is a measure of the correlation of the volatility structure observed over a historical period when looking at two different time resolutions. The lower-resolution volatility, coarse volatility, given by , measures the absolute historical returns between time . The fine volatility, measured by , is a measure of the absolute daily return variations between time . The coarse–fine volatility with lag k, , measures the time dependency between fine and k-lagged coarse volatility. The lead lag correlation given by would indicate if a higher historical lead-lag correlation is predictive of a lower lead-lag correlation in the future—a kind of regime-switching behaviour as measured by coarse and fine volatility at total lag .

- Gain/loss asymmetry [59] is the phenomenon where positive total returns take a longer time to accrue than negative absolute returns. In other words, the speed at which return drawdowns occur tends to be faster than the speed at which return accumulation occurs. This is measured by observing the empirical distribution of wait time random variable for upper and lower return threshold (barriers) to be struck.

5.5. Hardware and Software

6. Results

6.1. Evaluation Metrics

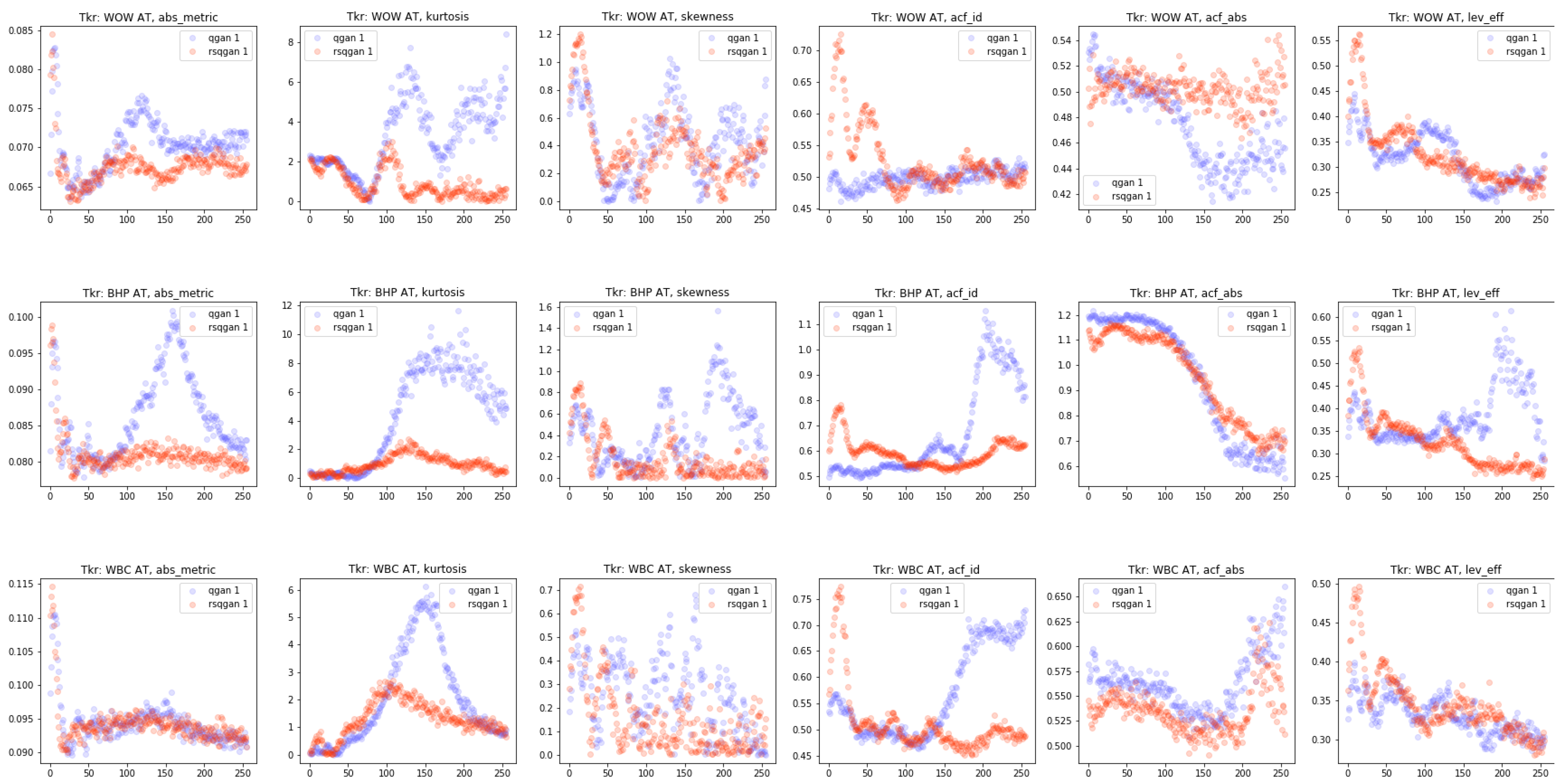

6.2. Key Results

- Minimising crisis regime SF test losses toward zero is not desired.This outcome may be indicative of mode collapse. GANs are susceptible to mode collapse for reasons described in Section 2. High intra-class entropy (variability) is desirable and is a measure of GAN quality. The purpose of RSQGAN in risk management applications is to provide a rich, non-degenerate synthetic density distribution. Hence, hyperparameter choices should focus on the relative improvement over QGAN without aiming to drive crisis regime SF test losses to zero. An equivalent metric for Fréchet joint distance [40] in the image domain that balances fidelity versus variety does not yet exist for the FTS domain. The investigation will be left for future work.

- GAN training is notoriously unstable, leading to performance variations sensitive to the number of training epochs.SF test losses can be unstable due to the instability of learned generator representations during training. Potential approaches to dealing with this were discussed in Section 3.1. Hence, the results shown in these tables do not include RSQGAN improvements that could be captured through the use of improved GAN objective loss functions or research into the calibration of early stopping criteria. This has been left for future work.

7. Discussion

- The QGAN and RSQGAN performance can be highly variable between assets and regimes for fixed topology and hyperparameter settings. The baseline settings used were the same architectural and hyperparameter settings as the QGAN open-source implementation by Wiese et al. [12]. Unsurprisingly, these settings resulted in a mixed performance across all stocks and regimes. Baseline QGAN settings consisted of six hidden layers and skip layer connections of 50 nodes each while using fixed discriminator and generator learning rates of and , respectively. On the training stock set, RSQGAN outperformed QGAN on all four crisis-sensitive SF test metrics. However, on the validation stock set, RSQGAN only outperformed on the loss CDF stoptime distribution. By construction, the conditional RSQGAN, which is trained by learning from average class losses, performs similarly to the average of multiple QGANs each trained on single-regime datasets. But due to regime class imbalance, it outperforms the minority crisis regime class at the expense of the performance on the ‘normal’ regime classes. However, as the performance was observed to be highly variable across stock and regime conditions, this suggests that additional model flexibility is required to deal with different regime lengths or stock-specific behaviour. Choosing an appropriate receptive field size (and hence network depth) is an important hyperparameter for simulating different regime lengths in a single model. Selecting an RFS that is too short could lead to longer-term time independence in simulations than is justifiable. Selecting an RFS that is too long would reduce the effective training dataset while increasing learnable parameters. The receptive field size should be consistent with the intended simulation horizon. Despite selecting training and validation stock sets from the same long-term correlation cluster, the mixed performance between stocks and regimes highlights that the same RSQGAN topology was not sufficiently rich to learn stock-specific features that could be applied from one stock (e.g., BHP) and to expect a similarly strong performance in a highly correlated stock (e.g., RIO). Thus, a richer topology such as a joint drift and volatility GAN, such as the stochastic volatility neural network (SVNN) model by Wiese et al. [12], could be extended to the conditional case in the future. A single-drift topology in isolation will underperform in simulating stocks that show strong momentum characteristics (i.e., a negative leverage effect) where high returns predict lower future volatility. An additional approach to potentially learning stock-specific features and improving the RSQGAN performance is to jointly condition regime categorical classes with continuous variables such as rolling volatility, correlation, or recent historical time series such as that demonstrated by Koshiyama et al. [13], de Meer Pardo [14], Fu et al. [15].

- A higher-capacity topology appears to further improve the RSQGAN performance relative to QGAN.A larger-capacity RSQGAN/QGAN network with seven hidden layers and skip layer connections of 60 nodes each led to RSQGAN outperforming in nine out of nine SF test metrics for the training stock set. However, RSQGAN outperformed in only two out of nine SF test metrics for the validation stock set. An examination of training losses indicates that this was partially due to training instability, which could be rectified by improved objective loss functions and early stopping criteria. This is left for future investigation. A poor performance on the validation stock set could also be due to the RSQGAN topology not being flexible enough to learn necessary stock-specific features (see the point above).

- The choice of early stopping criteria for training QGAN and RSQGAN is a significant area for further improvement.The original early stopping criteria in the open-source implementation by Wiese et al. [12] was used. The early stopping of QGAN and RSQGAN training occurred if the mean absolute deviation of the ACF of log-returns and the ACF of absolute returns both fell below preset thresholds.Figure 16 below shows that, during training for a given regime, none of the six possible stopping criteria uniformly converge for any of the three training stocks. This could be due to a number of causes—a topology without the sufficient capacity to simultaneously learn all SF behaviours and/or unstable training. Further, it is not necessarily desirable for convergence over all SF behaviours, as it may suggest mode collapse. No experiments were conducted to explore if there were reliable heuristics for setting early stopping conditions and understanding trade-offs between individual SF test metrics. This remains an open problem and is left for future work.

- A modest z-clipping of noise prior to in training and in generation appeared to improve the performance further.Experiments with a ‘crude’ implementation of z-clipping and skip-z layers from the BigGAN paper by Brock et al. [21] showed that modest z-clipping could produce synthetic data with higher initial fidelity to real data.The ‘crude’ RSQGAN implementation only applied skip-z layers to the first hidden layer of the generator and discriminator networks rather than learnable embeddings at all hidden layers. Further, it did not include the authors’ suggestion to implement an orthogonal regularisation of the generator. Despite the crude implementation, modest but mixed performance improvements were observed across SF test losses when a modest z-clipping of in training and in generation were applied.However, an experiment that used a more extreme clipping parameter in training and in generation appeared to degrade the relative performance of RSQGAN relative to QGAN. A full implementation of z-clipping and skip-z layers and further experiments are left to future work.

- RSQGAN produced synthetic data from crisis regimes with improved SF evaluation measures.It is reasonable to expect an RSQGAN outperformance for the minority crisis regime, as the RSQGAN training procedure corrects for regime class imbalance and enables shared parameter learning across all classes in a single model representation. This is a useful property for crisis risk management applications where fewer historical crisis data are observable.Improving simulations for the expected decay of the ACF of absolute returns or volatility could be useful for assessing the value of options instruments. By similar arguments, an improved simulation of expected future volatility based on recent returns or simulating multiperiod (coarse) or intraday (fine) volatility with a lag given observed coarse or fine volatility could assist with risk decision making. Further knowledge of the time distribution for different loss thresholds could assist with a trading strategy. SF test metrics corresponding to these actionable concepts are volatility clustering ACF, leverage effect, coarse–fine volatility lag, and loss stoptime CDF.

8. Future Work

9. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix A.1. Temporal Convolutional Networks

Appendix A.1.1. Multilayer Perceptron

Appendix A.1.2. TCN Model Definition

Appendix A.2. Quant GAN

Quant GAN Model

Appendix A.3. Quant GAN Training Procedure

| Algorithm A1: Quant GAN training [12] |

|

Appendix A.4. Greedy Gaussian Segmentation

Regime Classes—Greedy Gaussian Segmentation

| Algorithm A2: Split interval [20] |

|

| Algorithm A3: Greedy Gaussian Segmentation [20] |

|

References

- Hu, Z.; Zhao, Y.; Khushi, M. A Survey of Forex and Stock Price Prediction Using Deep Learning. Appl. Syst. Innov. 2021, 4, 9. [Google Scholar] [CrossRef]

- Gu, S.; Kelly, B.; Xiu, D. Empirical Asset Pricing via Machine Learning; Technical report; National Bureau of Economic Research: Cambridge, MA, USA, 2018. [Google Scholar]

- De Prado, M.L. Tactical Investment Algorithms. 2019. Available online: https://ssrn.com/abstract=3459866 (accessed on 1 August 2023).

- Kingma, D.P.; Welling, M. Auto-encoding variational bayes. arXiv 2013, arXiv:1312.6114. [Google Scholar]

- Vincent, P.; Larochelle, H.; Bengio, Y.; Manzagol, P.A. Extracting and composing robust features with denoising autoencoders. In Proceedings of the 25th International Conference on Machine Learning, Helsinki, Finland, 5–9 July 2008; pp. 1096–1103. [Google Scholar]

- Goodfellow, I.; Pouget-Abadie, J.; Mirza, M.; Xu, B.; Warde-Farley, D.; Ozair, S.; Courville, A.; Bengio, Y. Generative adversarial nets. In Proceedings of the Advances in Neural Information Processing Systems, Montreal, QC, Canada, 8–13 December 2014; pp. 2672–2680. [Google Scholar]

- Larsen, A.B.L.; Sønderby, S.K.; Larochelle, H.; Winther, O. Autoencoding beyond pixels using a learned similarity metric. In Proceedings of the International Conference on Machine Learning, PMLR, New York, NY, USA, 20–22 June 2016; pp. 1558–1566. [Google Scholar]

- Huang, H.; Li, Z.; He, R.; Sun, Z.; Tan, T. Introvae: Introspective variational autoencoders for photographic image synthesis. arXiv 2018, arXiv:1807.06358. [Google Scholar]

- Zhou, X.; Pan, Z.; Hu, G.; Tang, S.; Zhao, C. Stock market prediction on high-frequency data using generative adversarial nets. Math. Probl. Eng. 2018, 2018, 4907423. [Google Scholar] [CrossRef]

- Zhang, K.; Zhong, G.; Dong, J.; Wang, S.; Wang, Y. Stock Market Prediction Based on Generative Adversarial Network. Procedia Comput. Sci. 2019, 147, 400–406. [Google Scholar] [CrossRef]

- Takahashi, S.; Chen, Y.; Tanaka-Ishii, K. Modeling financial time-series with generative adversarial networks. Phys. A Stat. Mech. Its Appl. 2019, 527, 121261. [Google Scholar] [CrossRef]

- Wiese, M.; Knobloch, R.; Korn, R.; Kretschmer, P. Quant GANs: Deep generation of financial time series. Quant. Financ. 2020, 20, 1419–1440. [Google Scholar] [CrossRef]

- Koshiyama, A.; Firoozye, N.; Treleaven, P. Generative Adversarial Networks for Financial Trading Strategies Fine-Tuning and Combination. arXiv 2019, arXiv:1901.01751. [Google Scholar] [CrossRef]

- de Meer Pardo, F. Enriching Financial Datasets with Generative Adversarial Networks. 2019. Working Paper. Available online: http://resolver.tudelft.nl/uuid:51d69925-fb7b-4e82-9ba6-f8295f96705c (accessed on 1 August 2023).

- Fu, R.; Chen, J.; Zeng, S.; Zhuang, Y.; Sudjianto, A. Time Series Simulation by Conditional Generative Adversarial Net. arXiv 2019, arXiv:1904.11419. [Google Scholar] [CrossRef]

- Marti, G. CorrGAN: Sampling Realistic Financial Correlation Matrices Using Generative Adversarial Networks. In Proceedings of the ICASSP 2020–2020 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), Barcelona, Spain, 4–8 May 2020; pp. 8459–8463. [Google Scholar]

- Kondratyev, A.; Schwarz, C. The Market Generator. 2019. Available online: https://ssrn.com/abstract=3384948 (accessed on 1 August 2023).

- Mirza, M.; Osindero, S. Conditional generative adversarial nets. arXiv 2014, arXiv:1411.1784. [Google Scholar]

- Esteban, C.; Hyland, S.L.; Rätsch, G. Real-valued (medical) time series generation with recurrent conditional gans. arXiv 2017, arXiv:1706.02633. [Google Scholar]

- Hallac, D.; Nystrup, P.; Boyd, S. Greedy Gaussian segmentation of multivariate time series. Adv. Data Anal. Classif. 2019, 13, 727–751. [Google Scholar] [CrossRef]

- Brock, A.; Donahue, J.; Simonyan, K. Large scale gan training for high fidelity natural image synthesis. arXiv 2018, arXiv:1809.11096. [Google Scholar]

- Mohamed, S.; Lakshminarayanan, B. Learning in implicit generative models. arXiv 2016, arXiv:1610.03483. [Google Scholar]

- Manisha, P.; Gujar, S. Generative Adversarial Networks (GANs): What it can generate and What it cannot? arXiv 2018, arXiv:1804.00140. [Google Scholar]

- Radford, A.; Metz, L.; Chintala, S. Unsupervised representation learning with deep convolutional generative adversarial networks. arXiv 2015, arXiv:1511.06434. [Google Scholar]

- Karras, T.; Aila, T.; Laine, S.; Lehtinen, J. Progressive growing of gans for improved quality, stability, and variation. arXiv 2017, arXiv:1710.10196. [Google Scholar]

- Oord, A.v.d.; Dieleman, S.; Zen, H.; Simonyan, K.; Vinyals, O.; Graves, A.; Kalchbrenner, N.; Senior, A.; Kavukcuoglu, K. Wavenet: A generative model for raw audio. arXiv 2016, arXiv:1609.03499. [Google Scholar]

- Zhang, Y.; Gan, Z.; Carin, L. Generating text via adversarial training. In Proceedings of the NIPS Workshop on Adversarial Training, Online, 25 November 2016; Volume 21. [Google Scholar]

- d’Autume, C.d.M.; Rosca, M.; Rae, J.; Mohamed, S. Training language gans from scratch. arXiv 2019, arXiv:1905.09922. [Google Scholar]

- Choi, E.; Biswal, S.; Malin, B.; Duke, J.; Stewart, W.F.; Sun, J. Generating multi-label discrete patient records using generative adversarial networks. arXiv 2017, arXiv:1703.06490. [Google Scholar]

- Acharya, D.; Huang, Z.; Paudel, D.P.; Van Gool, L. Towards high resolution video generation with progressive growing of sliced Wasserstein GANs. arXiv 2018, arXiv:1810.02419. [Google Scholar]

- Clark, A.; Donahue, J.; Simonyan, K. Efficient video generation on complex datasets. arXiv 2019, arXiv:1907.06571. [Google Scholar]

- Roth, K.; Lucchi, A.; Nowozin, S.; Hofmann, T. Stabilizing training of generative adversarial networks through regularization. In Proceedings of the Advances in Neural Information Processing Systems, Long Beach, CA, USA, 4–9 December 2017; pp. 2018–2028. [Google Scholar]

- Arjovsky, M.; Bottou, L. Towards principled methods for training generative adversarial networks. arXiv 2017, arXiv:1701.04862. [Google Scholar]

- Arjovsky, M.; Chintala, S.; Bottou, L. Wasserstein gan. arXiv 2017, arXiv:1701.07875. [Google Scholar]

- Gulrajani, I.; Ahmed, F.; Arjovsky, M.; Dumoulin, V.; Courville, A.C. Improved training of wasserstein gans. In Proceedings of the Advances in Neural Information Processing Systems, Long Beach, CA, USA, 4–9 December 2017; pp. 5767–5777. [Google Scholar]

- Mescheder, L.; Geiger, A.; Nowozin, S. Which training methods for GANs do actually converge? arXiv 2018, arXiv:1801.04406. [Google Scholar]

- Theis, L.; Oord, A.v.d.; Bethge, M. A note on the evaluation of generative models. arXiv 2015, arXiv:1511.01844. [Google Scholar]

- Salimans, T.; Goodfellow, I.; Zaremba, W.; Cheung, V.; Radford, A.; Chen, X. Improved Techniques for Training Gans. In Proceedings of the Advances in Neural Information Processing Systems, Barcelona, Spain, 5–10 December 2016; pp. 2234–2242. [Google Scholar]

- Heusel, M.; Ramsauer, H.; Unterthiner, T.; Nessler, B.; Hochreiter, S. Gans trained by a two time-scale update rule converge to a local nash equilibrium. In Proceedings of the Advances in Neural Information Processing Systems, Long Beach, CA, USA, 4–9 December 2017; pp. 6626–6637. [Google Scholar]

- DeVries, T.; Romero, A.; Pineda, L.; Taylor, G.W.; Drozdzal, M. On the evaluation of conditional gans. arXiv 2019, arXiv:1907.08175. [Google Scholar]

- Cont, R. Empirical properties of asset returns: Stylized facts and statistical issues. J. Quant. Financ. 2001, 1, 223. [Google Scholar] [CrossRef]

- Cont, R. Volatility clustering in financial markets: Empirical facts and agent-based models. In Long Memory in Economics; Springer: Berlin/Heidelberg, Germany, 2007; pp. 289–309. [Google Scholar]

- Chakraborti, A.; Toke, I.M.; Patriarca, M.; Abergel, F. Econophysics review: I. Empirical facts. Quant. Financ. 2011, 11, 991–1012. [Google Scholar] [CrossRef]

- Villani, C. Optimal Transport: Old and New; Springer Science & Business Media; Springer: Berlin/Heidelberg, Germany, 2008; Volume 338. [Google Scholar]

- Szegedy, C.; Vanhoucke, V.; Ioffe, S.; Shlens, J.; Wojna, Z. Rethinking the inception architecture for computer vision. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, Las Vegas, NV, USA, 26 June–1 July 2016; pp. 2818–2826. [Google Scholar]

- Bai, S.; Kolter, J.Z.; Koltun, V. An empirical evaluation of generic convolutional and recurrent networks for sequence modeling. arXiv 2018, arXiv:1803.01271. [Google Scholar]

- He, K.; Zhang, X.; Ren, S.; Sun, J. Deep residual learning for image recognition. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, Las Vegas, NV, USA, 26 June–1 July 2016; pp. 770–778. [Google Scholar]

- Brock, A.; Lim, T.; Ritchie, J.M.; Weston, N. Neural photo editing with introspective adversarial networks. arXiv 2016, arXiv:1609.07093. [Google Scholar]

- Smolensky, P. Information Processing in Dynamical Systems: Foundations of Harmony Theory; Technical report; Colorado Univ at Boulder Dept of Computer Science: Boulder, CO, USA, 1986. [Google Scholar]

- Da Silva, B.; Shi, S.S. Towards Improved Generalization in Financial Markets with Synthetic Data Generation. arXiv 2019, arXiv:1906.03232. [Google Scholar]

- Franco-Pedroso, J.; Gonzalez-Rodriguez, J.; Cubero, J.; Planas, M.; Cobo, R.; Pablos, F. Generating virtual scenarios of multivariate financial data for quantitative trading applications. J. Financ. Data Sci. 2019, 1, 55–77. [Google Scholar] [CrossRef]

- Jolicoeur-Martineau, A. The relativistic discriminator: A key element missing from standard GAN. arXiv 2018, arXiv:1807.00734. [Google Scholar]

- Liu, Y.; Gopikrishnan, P.; Stanley, H.E. Statistical properties of the volatility of price fluctuations. Phys. Rev. E 1999, 60, 1390. [Google Scholar] [CrossRef] [PubMed]

- Bouchaud, J.P.; Matacz, A.; Potters, M. Leverage effect in financial markets: The retarded volatility model. Phys. Rev. Lett. 2001, 87, 228701. [Google Scholar] [CrossRef]

- Qiu, T.; Zheng, B.; Ren, F.; Trimper, S. Return-volatility correlation in financial dynamics. Phys. Rev. E 2006, 73, 065103. [Google Scholar] [CrossRef]

- Müller, U.A.; Dacorogna, M.M.; Davé, R.D.; Olsen, R.B.; Pictet, O.V.; Von Weizsäcker, J.E. Volatilities of different time resolutions—Analyzing the dynamics of market components. J. Empir. Financ. 1997, 4, 213–239. [Google Scholar] [CrossRef]

- Rydberg, T.H. Realistic statistical modelling of financial data. Int. Stat. Rev. 2000, 68, 233–258. [Google Scholar] [CrossRef]

- Gavrishchaka, V.V.; Ganguli, S.B. Volatility forecasting from multiscale and high-dimensional market data. Neurocomputing 2003, 55, 285–305. [Google Scholar] [CrossRef]

- Jensen, M.H.; Johansen, A.; Simonsen, I. Inverse statistics in economics: The gain–loss asymmetry. Phys. A Stat. Mech. Its Appl. 2003, 324, 338–343. [Google Scholar] [CrossRef]

- Box, G.E.; Jenkins, G.M.; Reinsel, G.C.; Ljung, G.M. Time Series Analysis: Forecasting and Control; John Wiley & Sons: London, UK, 2015. [Google Scholar]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef]

- Engle, R.F.; Granger, C.W. Co-integration and error correction: Representation, estimation, and testing. Econom. J. Econom. Soc. 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Dumoulin, V.; Visin, F. A guide to convolution arithmetic for deep learning. arXiv 2016, arXiv:1603.07285. [Google Scholar]

- Ioffe, S.; Szegedy, C. Batch normalization: Accelerating deep network training by reducing internal covariate shift. arXiv 2015, arXiv:1502.03167. [Google Scholar]

- Miyato, T.; Kataoka, T.; Koyama, M.; Yoshida, Y. Spectral normalization for generative adversarial networks. arXiv 2018, arXiv:1802.05957. [Google Scholar]

- Loshchilov, I.; Hutter, F. Sgdr: Stochastic gradient descent with warm restarts. arXiv 2016, arXiv:1608.03983. [Google Scholar]

- Kingma, D.P.; Ba, J. Adam: A method for stochastic optimization. arXiv 2014, arXiv:1412.6980. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Stylised Fact (SF) | Evaluation Metric |

|---|---|

| 1. Linear unpredictability | |

| 2. Heavy-tailed distribution | is the p.d.f of R, |

| 3. Volatility clustering | up to large k, small |

| 4. Leverage effect | for |

| 5. Coarse–fine vol correlation | for some |

| 6. Gain/loss asymmetry | = |

| SF Test Losses | Interpretation and Sources | Expression |

|---|---|---|

| acf | ST unpredictability Chakraborti et al. [43] | |

| Return density Chakraborti et al. [43] Liu et al. [53] | ||

| vc_acf* | Volatility clustering Cont [42] | |

| vc_pdf | Abs. return density Cont [42] | |

| leveff* | Loss future vol lag Bouchaud et al. [54] Qiu et al. [55] | |

| cfvol* | Coarse–fine vol lag Müller et al. [56] Rydberg [57] Gavrishchaka and Ganguli [58] | |

| cfvol_diff | Coarse–fine vol skew Müller et al. [56] Rydberg [57] Gavrishchaka and Ganguli [58] | |

| gain_cdf_ | Gain stoptime CDF Jensen et al. [59] | |

| loss_cdf_* | Loss stoptime CDF Jensen et al. [59] |

| All Regimes | Crisis Regime | ||

|---|---|---|---|

| acf | rsqgan | 2.135 | 2.757 |

| qgan | 2.030 | 3.197 | |

| rsqgan | 0.641 | 0.770 | |

| qgan | 0.588 | 0.671 | |

| vc_acf* | rsqgan | 2.351 | 3.213 |

| qgan | 2.566 | 3.111 | |

| vc_pdf | rsqgan | 0.396 | 0.479 |

| qgan | 0.347 | 0.502 | |

| leveff* | rsqgan | 1924.233 | 1463.868 |

| qgan | 1607.904 | 1835.097 | |

| cfvol* | rsqgan | 4.749 | 6.202 |

| qgan | 5.199 | 6.327 | |

| cfvol_diff | rsqgan | 2.430 | 3.886 |

| qgan | 2.386 | 3.840 | |

| gain_cdf_12_5 | rsqgan | 21.826 | 19.622 |

| qgan | 23.052 | 19.119 | |

| loss_cdf_12_5* | rsqgan | 24.968 | 20.450 |

| qgan | 24.259 | 21.305 |

| All Regimes | Crisis Regime | ||

|---|---|---|---|

| acf | rsqgan | 1.824 | 2.619 |

| qgan | 1.779 | 2.723 | |

| rsqgan | 0.826 | 0.953 | |

| qgan | 0.712 | 0.838 | |

| vc_acf* | rsqgan | 2.548 | 3.619 |

| qgan | 2.794 | 3.685 | |

| vc_pdf | rsqgan | 0.393 | 0.582 |

| qgan | 0.375 | 0.503 | |

| leveff* | rsqgan | 2091.035 | 2718.220 |

| qgan | 1726.681 | 2139.719 | |

| cfvol* | rsqgan | 4.743 | 6.181 |

| qgan | 5.086 | 6.305 | |

| cfvol_diff | rsqgan | 2.310 | 3.743 |

| qgan | 2.311 | 3.735 | |

| gain_cdf_12_5 | rsqgan | 24.841 | 13.825 |

| qgan | 24.338 | 12.592 | |

| loss_cdf_12_5* | rsqgan | 31.333 | 15.159 |

| qgan | 32.698 | 16.431 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huang, A.; Khushi, M.; Suleiman, B. Regime-Specific Quant Generative Adversarial Network: A Conditional Generative Adversarial Network for Regime-Specific Deepfakes of Financial Time Series. Appl. Sci. 2023, 13, 10639. https://doi.org/10.3390/app131910639

Huang A, Khushi M, Suleiman B. Regime-Specific Quant Generative Adversarial Network: A Conditional Generative Adversarial Network for Regime-Specific Deepfakes of Financial Time Series. Applied Sciences. 2023; 13(19):10639. https://doi.org/10.3390/app131910639

Chicago/Turabian StyleHuang, Andrew, Matloob Khushi, and Basem Suleiman. 2023. "Regime-Specific Quant Generative Adversarial Network: A Conditional Generative Adversarial Network for Regime-Specific Deepfakes of Financial Time Series" Applied Sciences 13, no. 19: 10639. https://doi.org/10.3390/app131910639

APA StyleHuang, A., Khushi, M., & Suleiman, B. (2023). Regime-Specific Quant Generative Adversarial Network: A Conditional Generative Adversarial Network for Regime-Specific Deepfakes of Financial Time Series. Applied Sciences, 13(19), 10639. https://doi.org/10.3390/app131910639