A Better Integration of Industrial Robots in Romanian Enterprises and the Labour Market

Abstract

:1. Introduction

“To overcome these adverse circumstances and pursue sustainable growth, both SMEs and large companies prepare long-term growth strategies to strengthen their technological innovation capability; overall, SMEs are in a relatively unfavorable condition to improve their performance and pursue continuous growth through technological innovation” [8].

“Technology innovation capability is a combination of technology innovation and capability; it is the organizational ability to carry out the process of developing, introducing, and adopting ideas and technologies for new products, services, and production processes” [9].

2. Recent Evolutions in the Robotics Market

2.1. The Intensive Use of Automation, Artificial Intelligence, and Robots

2.2. Filling the Gap between Automation and Robotics

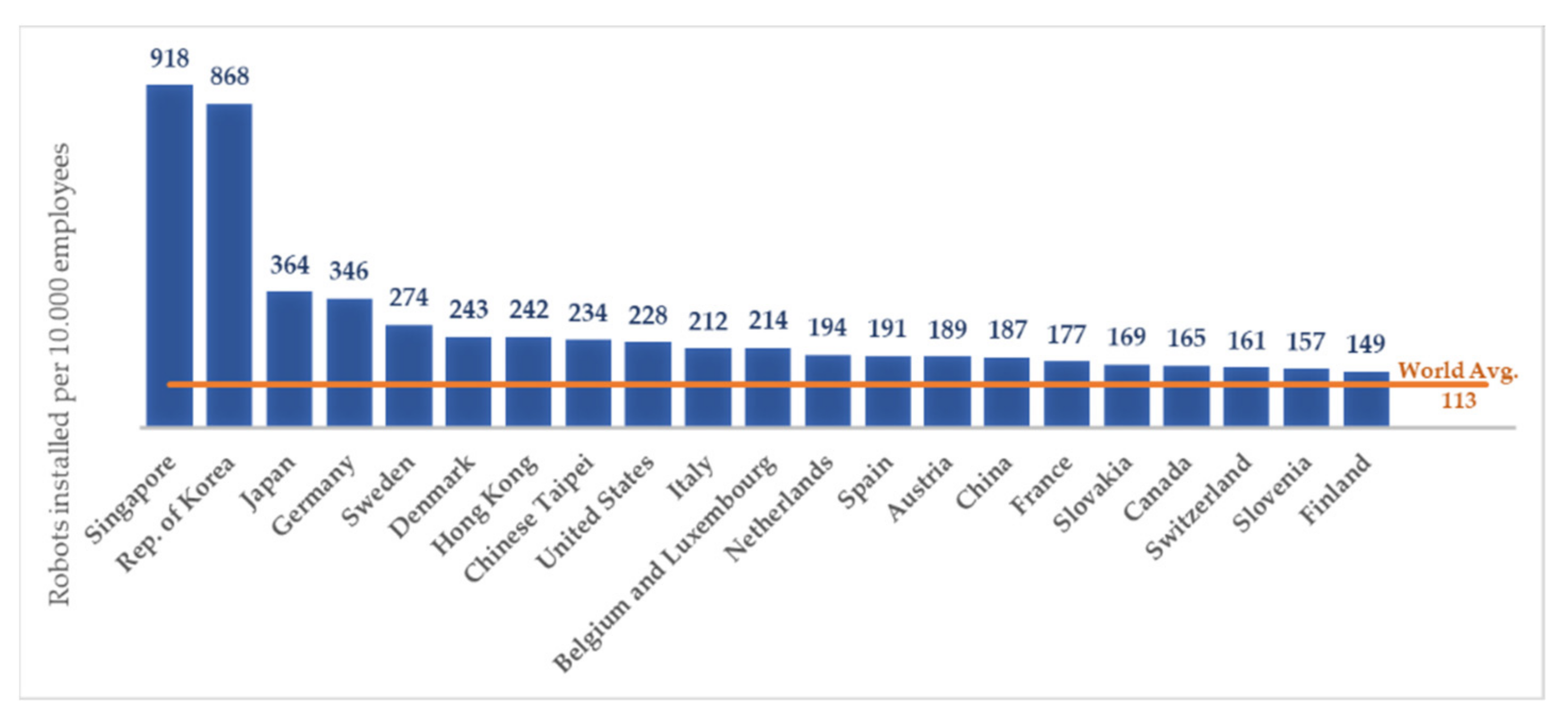

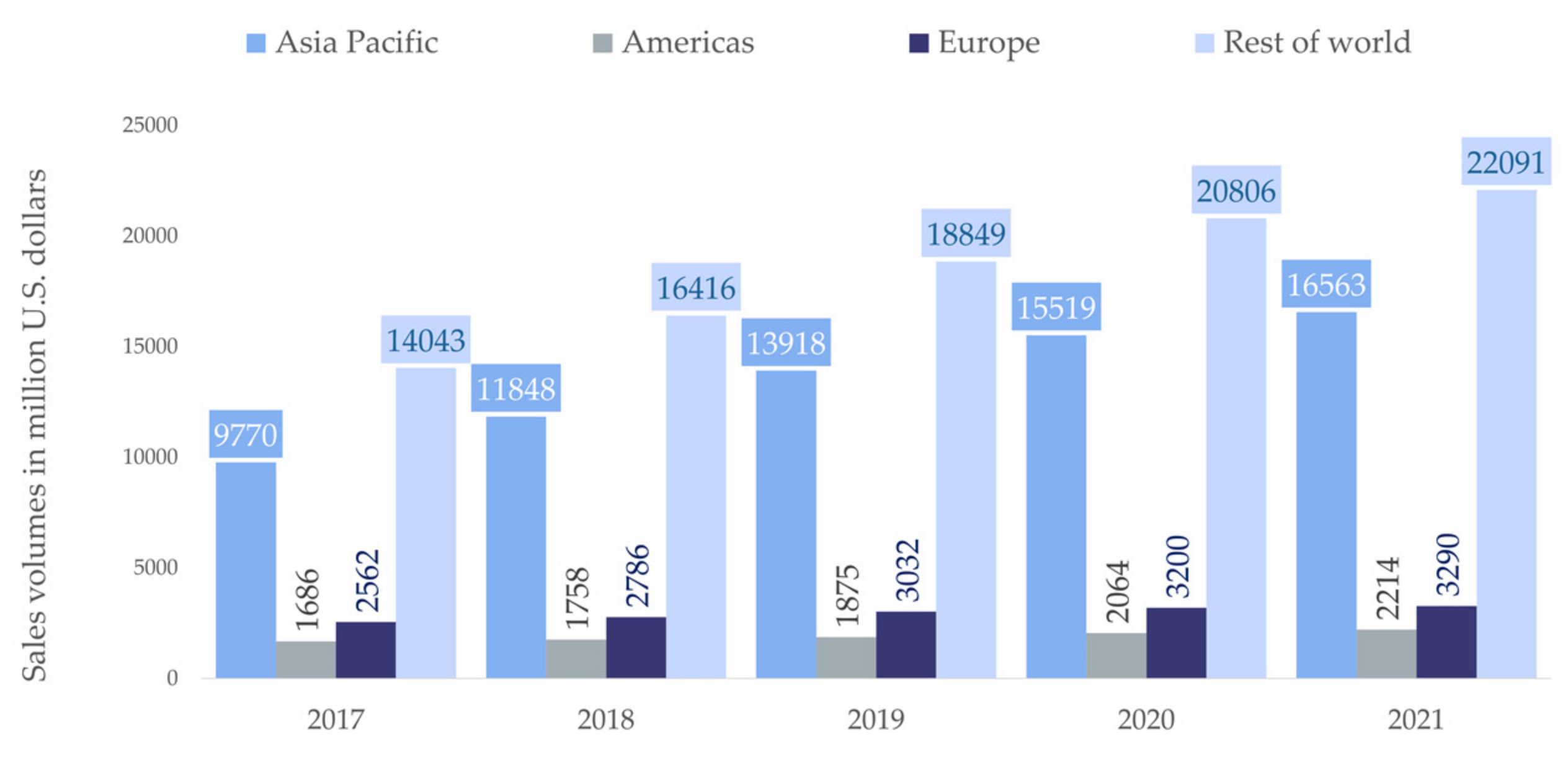

2.3. Global Robotics Market: Main Dimensions, Considerations, and Impact

2.4. The Added Value of Robotics: A Marketing Perspective for Increasing Competitiveness

3. Modelling Data Regarding Enterprises’ Use of Industrial Robots: Key Findings and Main Results

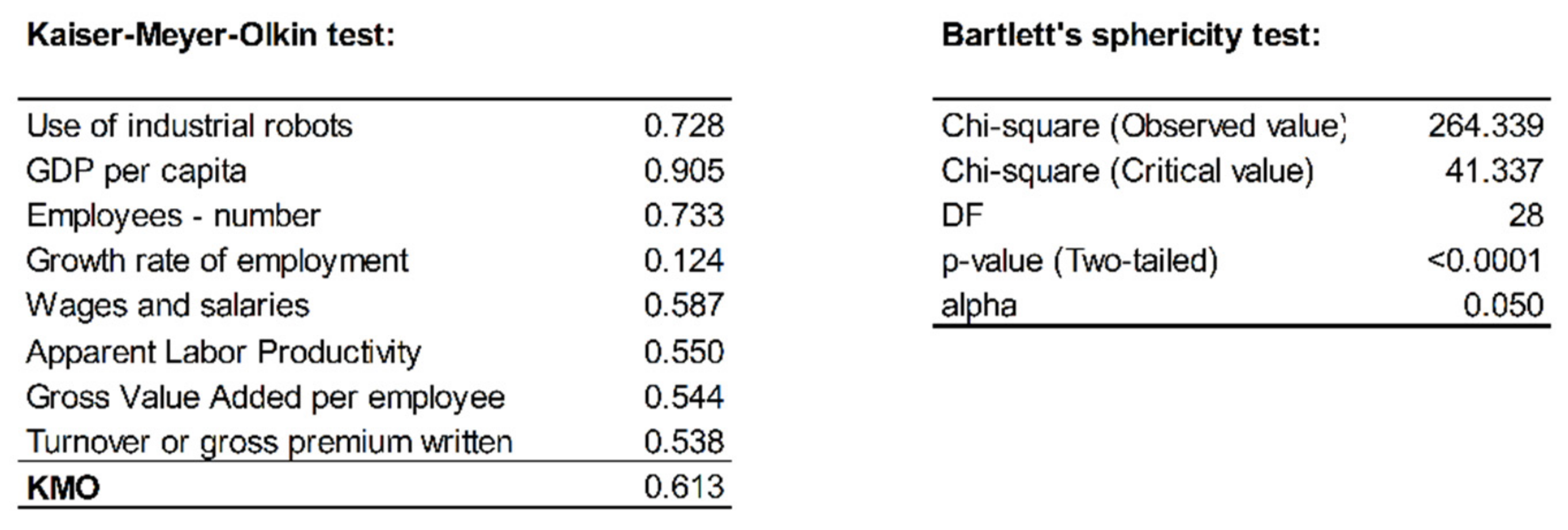

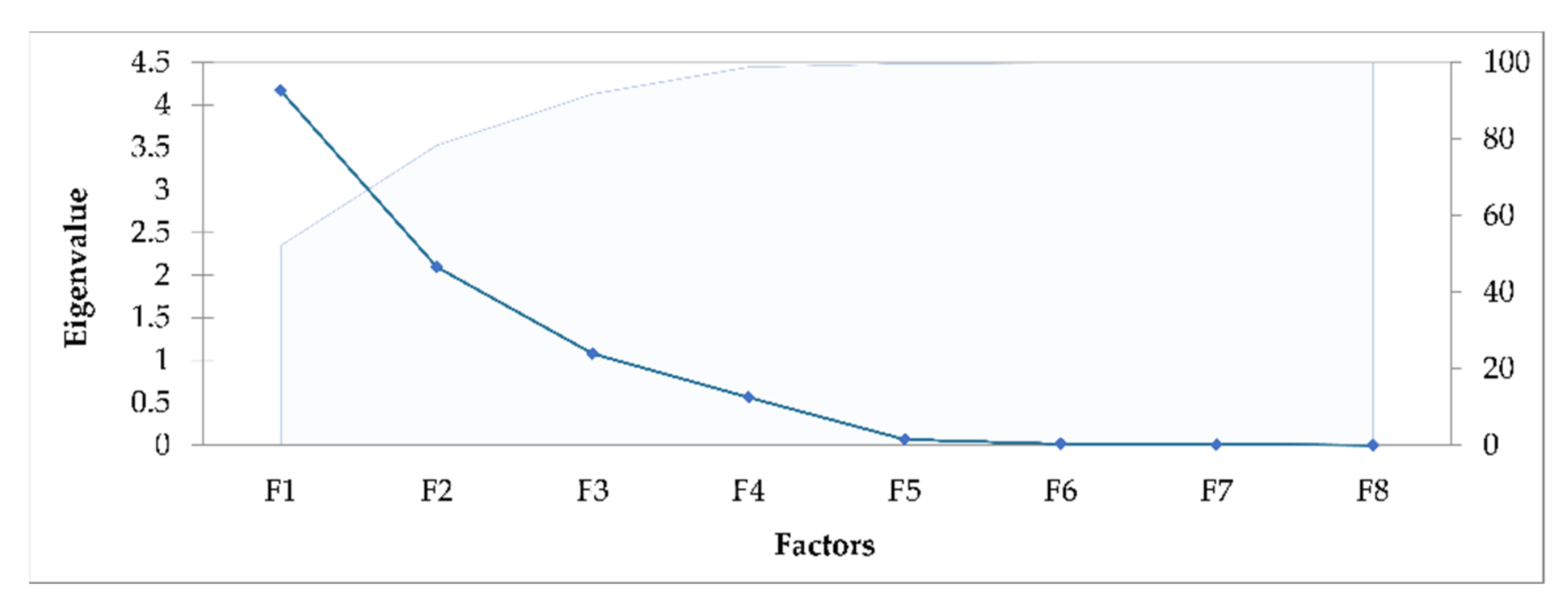

3.1. Data Collection

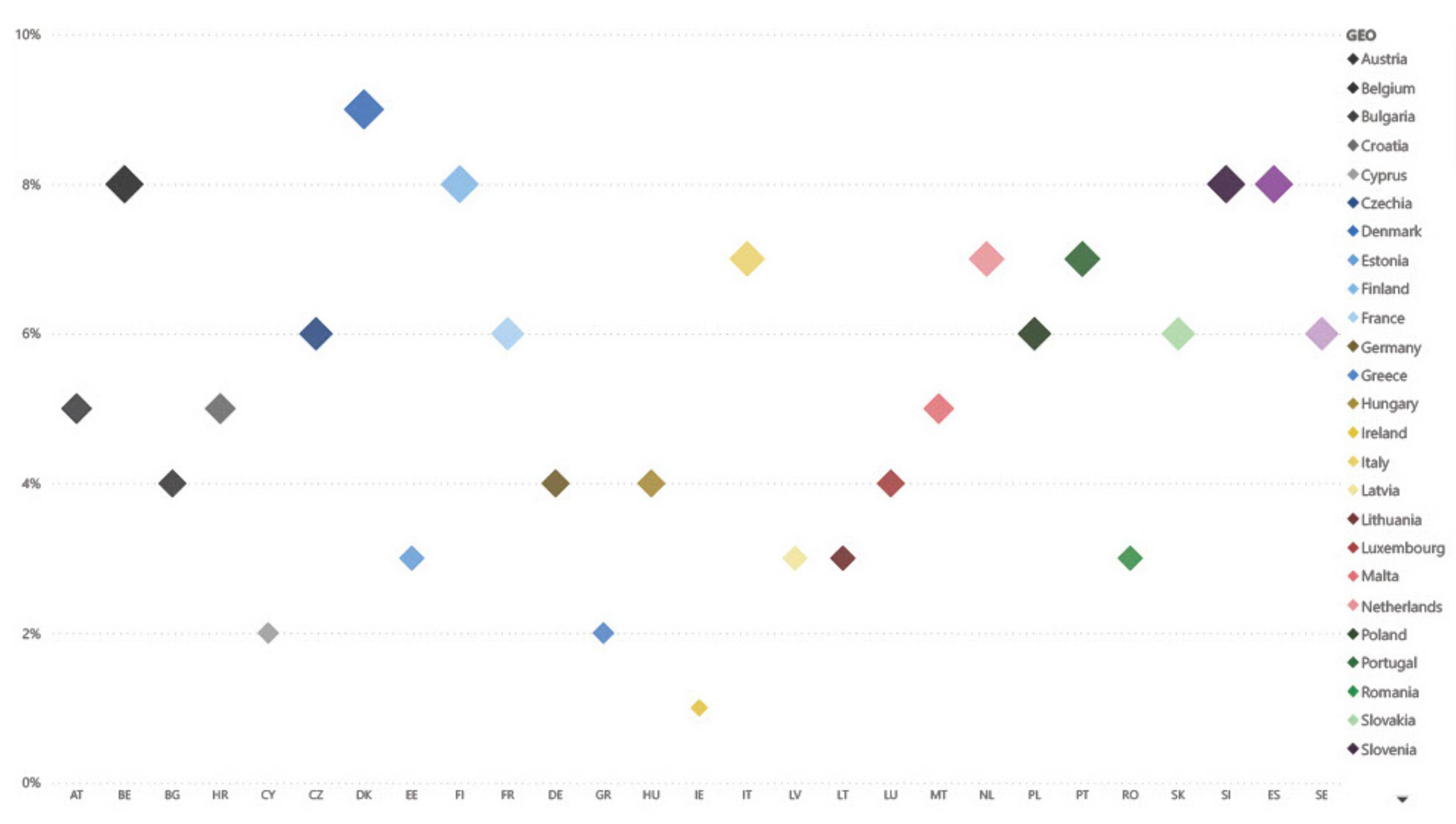

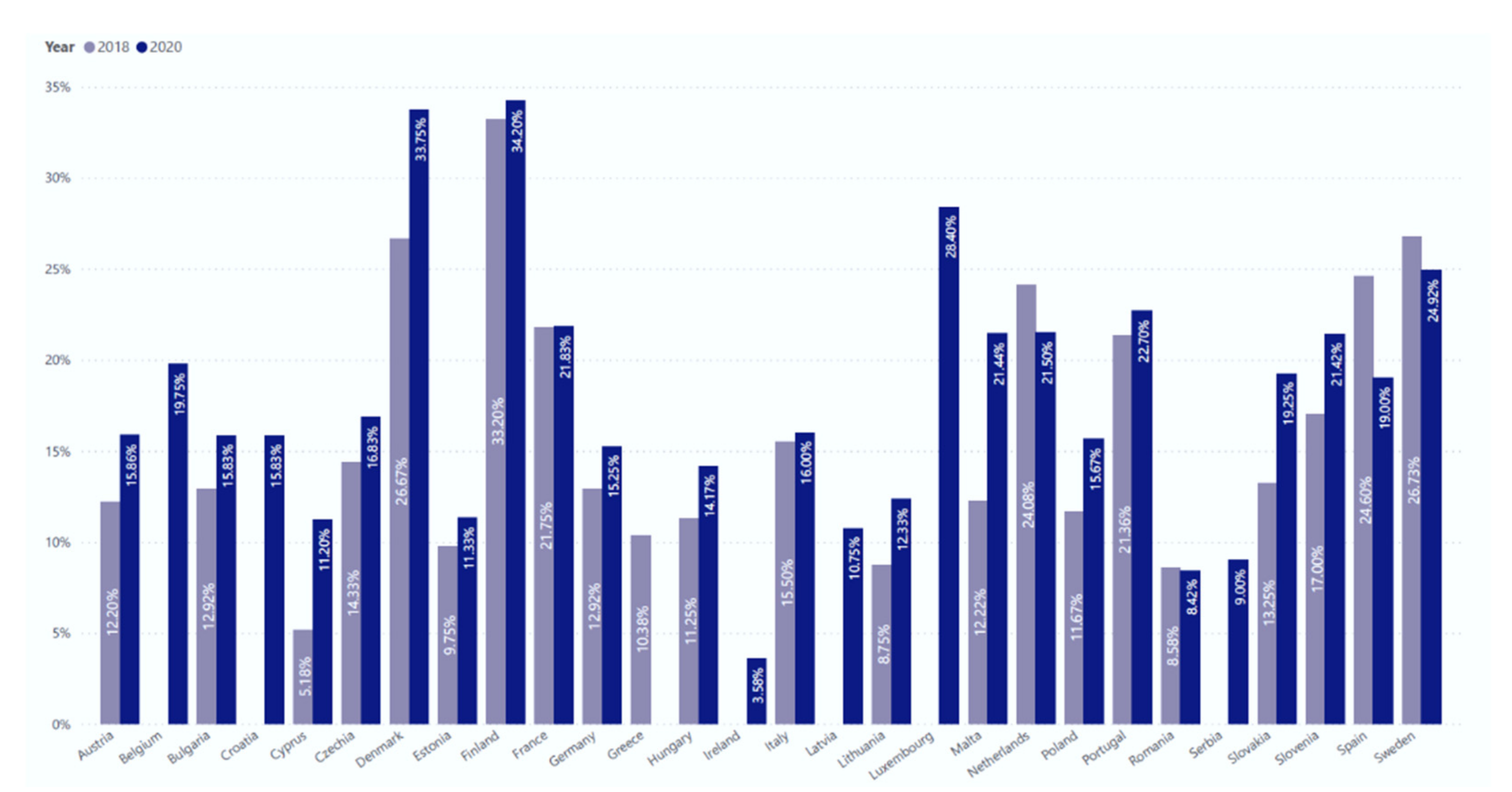

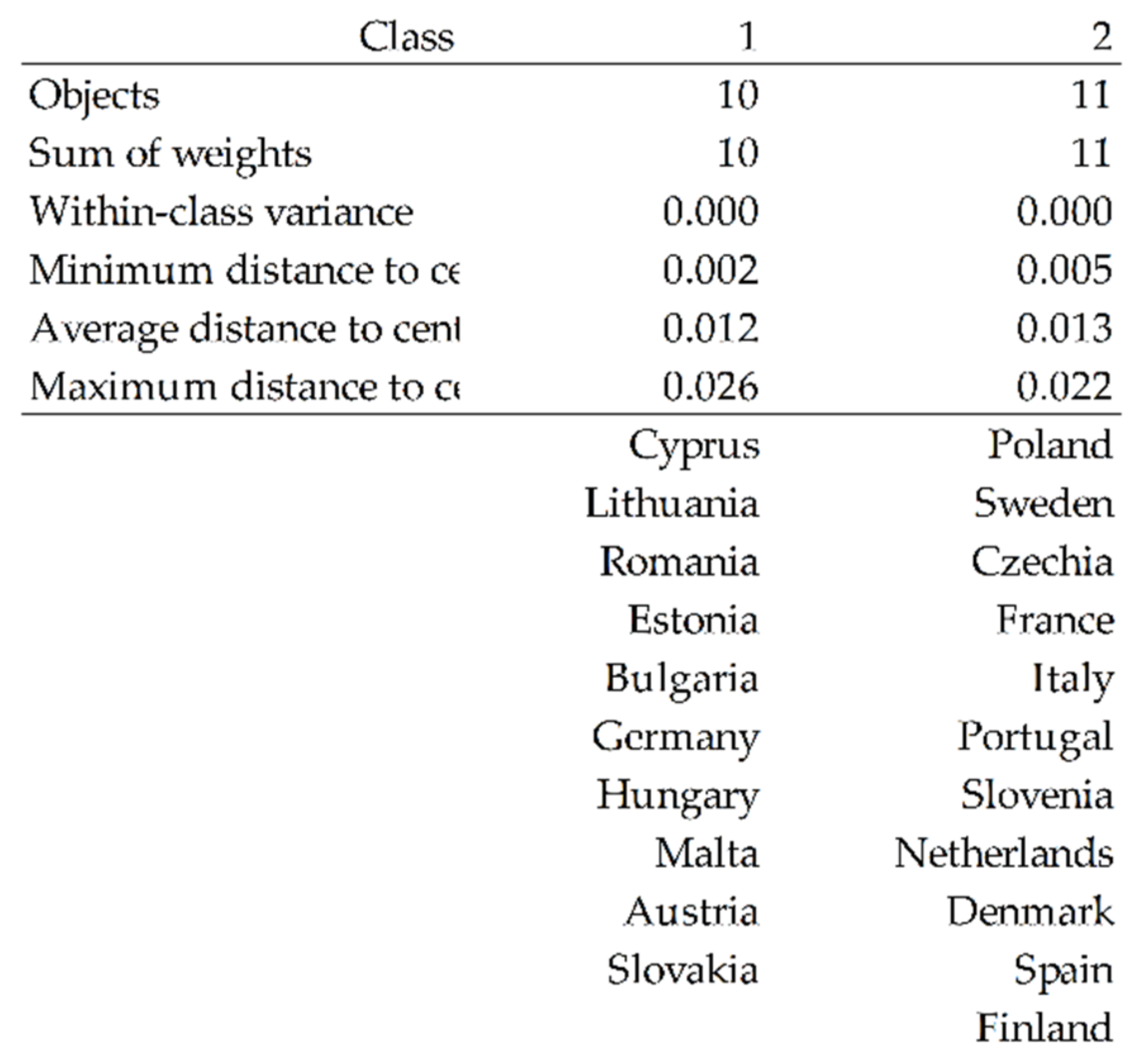

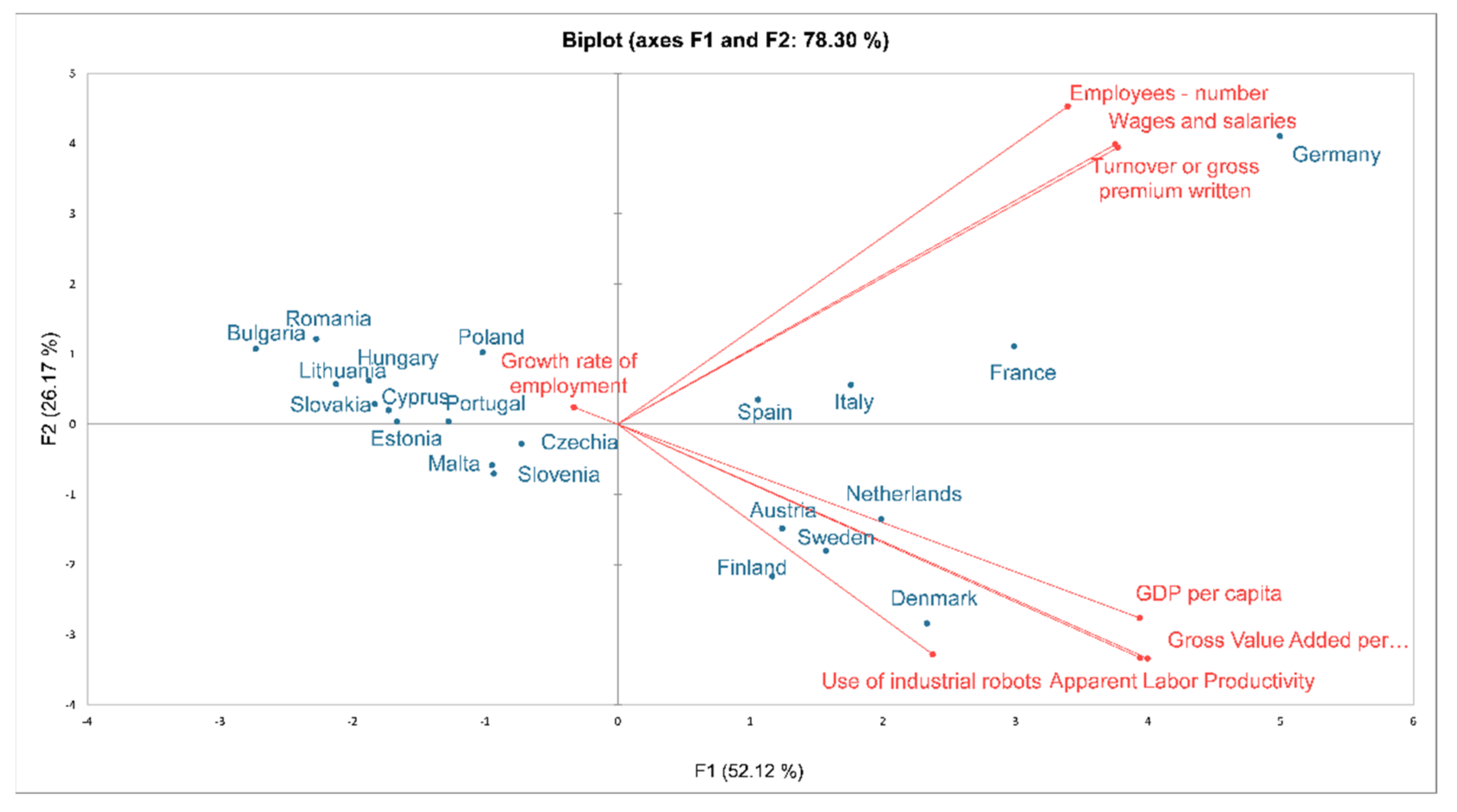

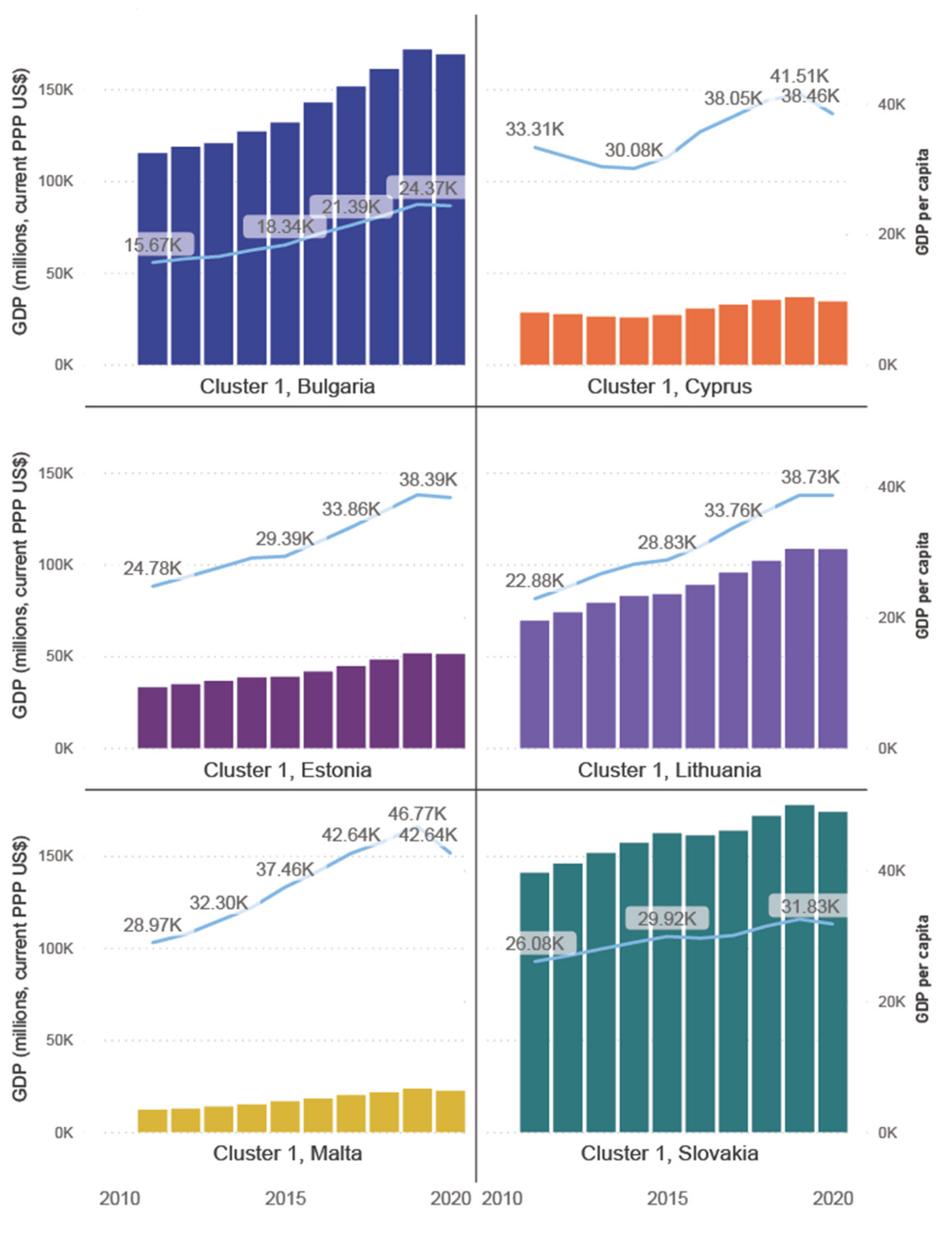

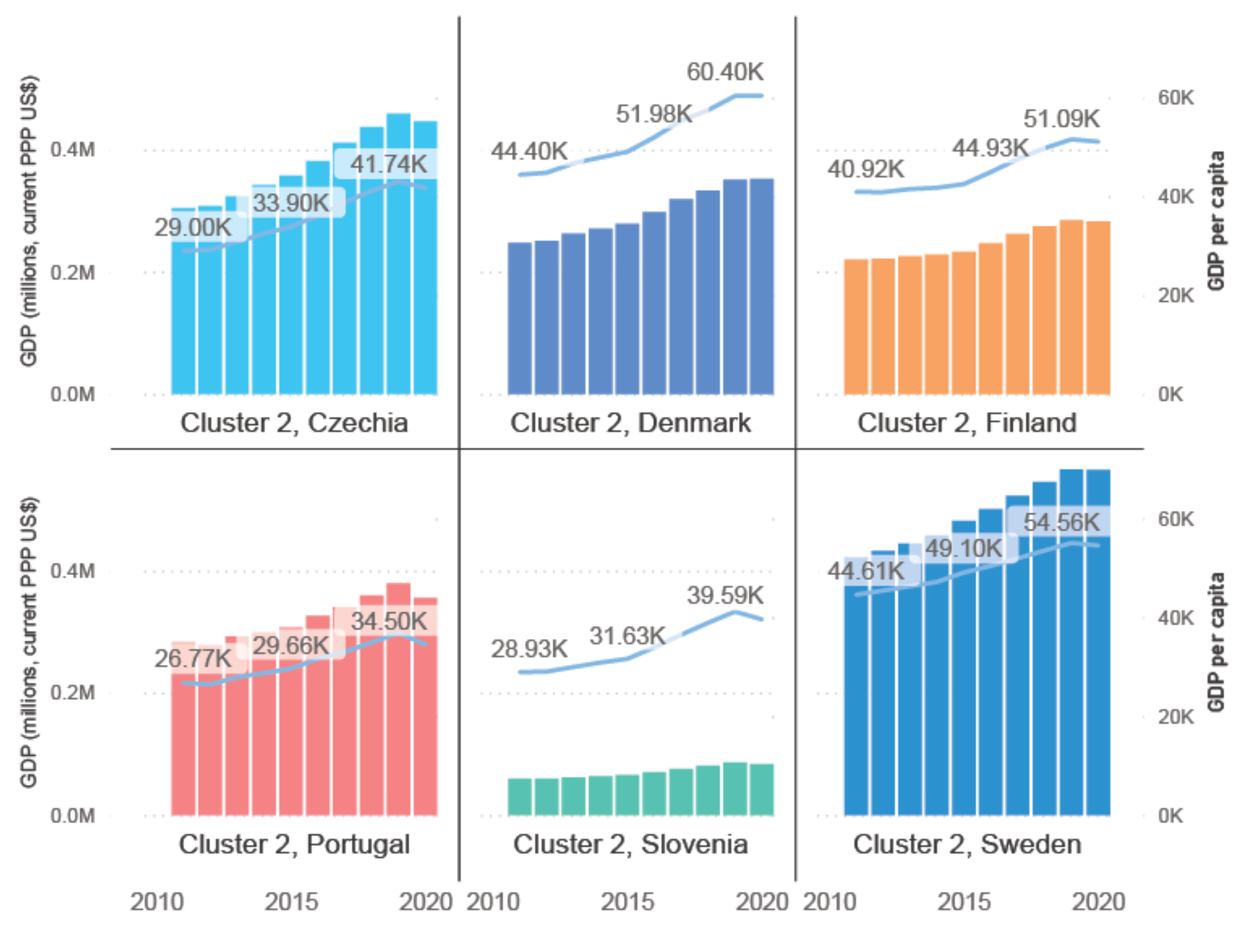

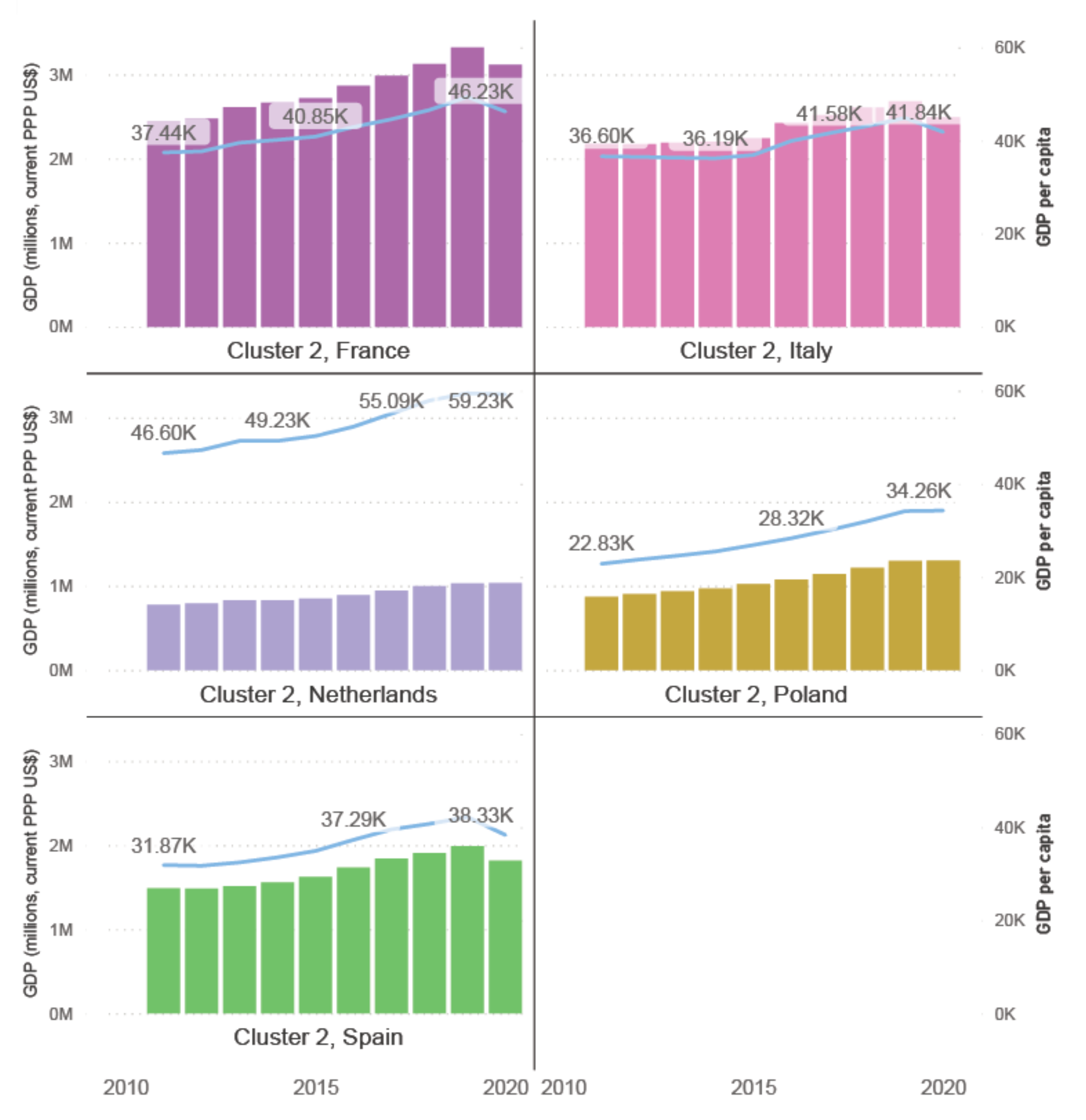

3.2. Clustering Analysis of Countries’ Distribution Based on the Share of Enterprises That Are Using Industrial Robots

- Countries with a low-to-moderate use of industrial robots in enterprises.

- Countries with intense use of industrial robots in enterprises.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Class | Year | Use of Industrial Robots | GDP per Capita | Employees-Number | Growth Rate of Employment | Wages and Salaries | Apparent Labor Productivity | Gross Value Added per Employee | Turnover or Gross Premium Written |

|---|---|---|---|---|---|---|---|---|---|---|

| Austria | 1 | 2018 | 4.0% | 57,050.35 | 2,606,757 | 2.7 | 96,271.3 | 68.9 | 77.3 | 737,701 |

| Bulgaria | 1 | 2018 | 3.0% | 22,911.30 | 1,755,308 | 0.9 | 12,626.4 | 14.5 | 16.7 | 141,152 |

| Cyprus | 1 | 2018 | 1.0% | 40,476.39 | 255,930 | 8.4 | 4623.6 | 35.3 | 37.2 | 33,708 |

| Germany | 1 | 2018 | 3.0% | 54,954.85 | 28,392,620 | 4.5 | 966,659.3 | 59.7 | 65.4 | 6,830,401 |

| Hungary | 1 | 2018 | 3.0% | 31,831.98 | 2,430,651 | 4.3 | 29,833.8 | 25.2 | 29.4 | 324,310 |

| Estonia | 1 | 2018 | 3.0% | 36,326.80 | 406,082 | 1 | 5860.6 | 31 | 33.4 | 64,982 |

| Lithuania | 1 | 2018 | 2.0% | 36,346.40 | 888,691 | 1.8 | 9010.1 | 21.3 | 23.6 | 91,926 |

| Malta | 1 | 2018 | 3.0% | 44,482.24 | 133,811 | 6.5 | 2709.2 | 42 | 49.6 | 24,471 |

| Slovakia | 1 | 2018 | 4.0% | 31,505.06 | 1,265,837 | 2.8 | 16,547.9 | 24.3 | 31.7 | 212,337 |

| Romania | 1 | 2018 | 2.0% | 29,248.81 | 3,944,656 | 1 | 38,575.2 | 18.4 | 18.9 | 313,933 |

| Czechia | 2 | 2018 | 6.0% | 41,134.09 | 2,917,924 | 1.5 | 43,711.2 | 29.7 | 38.5 | 541,087 |

| Denmark | 2 | 2018 | 7.0% | 57,462.78 | 1,706,138 | 3.4 | 82,813.0 | 92.8 | 98.4 | 545,569 |

| Finland | 2 | 2018 | 8.0% | 49,755.14 | 1,406,385 | 1.9 | 52,513.6 | 68.9 | 74.3 | 402,031 |

| France | 2 | 2018 | 6.0% | 46,569.02 | 14,610,108 | 0.5 | 528,720.8 | 63.7 | 68.9 | 3,830,389 |

| Italy | 2 | 2018 | 6.0% | 43,123.61 | 10,979,755 | 1.5 | 295,949.6 | 49.8 | 68.5 | 3,033,061 |

| Netherlands | 2 | 2018 | 7.0% | 57,901.10 | 5,194,758 | 3.6 | 168,480.0 | 64.8 | 74.9 | 1,644,839 |

| Poland | 2 | 2018 | 5.0% | 31,978.53 | 8,035,391 | 6.4 | 99,261.4 | 25.2 | 30.8 | 1,124,830 |

| Portugal | 2 | 2018 | 6.0% | 34,931.78 | 2,804,351 | 4.5 | 40,277.2 | 26 | 31.8 | 375,645 |

| Slovenia | 2 | 2018 | 6.0% | 38,915.64 | 560,885 | 4.2 | 12,147.8 | 36.8 | 43 | 102,384 |

| Spain | 2 | 2018 | 8.0% | 40,720.19 | 10,438,323 | 3.9 | 252,581.7 | 42.2 | 50.8 | 2,055,805 |

| Sweden | 2 | 2018 | 6.0% | 53,553.31 | 2,820,065 | 2.4 | 106,466.3 | 70.7 | 84.8 | 842,503 |

4. Conclusions and Potential Limitations

4.1. Conclusions

4.2. Limitations of the Study

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

References

- Phelps, E.S. The Robot Question. Proj. Synd. 2020. Available online: https://www.project-syndicate.org/commentary/economics-of-ai-robot-labor-by-edmund-s-phelps-2020-08?referral=d461cf&barrier=accesspaylog (accessed on 10 February 2022).

- OECD. Coronavirus (COVID-19): SME Policy Responses. In Policy Responses to Coronavirus; OECD: Paris, France, 2020; Available online: https://read.oecd-ilibrary.org/view/?ref=119_119680-di6h3qgi4x&title=Covid-19_SME_Policy_Responses (accessed on 21 February 2022). [CrossRef]

- Shen, Y.; Guo, D.; Long, F.; Mateos, L.A.; Ding, H.; Xiu, Z.; Hellman, R.B.; King, A.; Chen, S.; Zhang, C.; et al. Robots under COVID-19 Pandemic: A Comprehensive Survey. IEEE Access 2020, 9, 1590–1615. [Google Scholar] [CrossRef] [PubMed]

- Acemoglu, D.; Pascual, R. Artificial Intelligence, Automation, and Work. In The Economics of Artificial Intelligence: An Agenda; Ajay, A., Joshua, G., Avi, G., Eds.; University of Chicago Press: Chicago, IL, USA; National Bureau of Economic Research, Inc.: Middlesex County, MA, USA, 2019; pp. 197–236. Available online: http://www.nber.org/chapters/c14027 (accessed on 15 March 2022).

- Akpan, I.J.; Udoh, E.A.P.; Adebisi, B. Small business awareness and adoption of state-of-the-art technologies in emerging and developing markets, and lessons from the COVID-19 pandemic. J. Small Bus. Entrep. 2020, 34, 123–140. [Google Scholar] [CrossRef]

- Barbierato, E.; Zamponi, M.E. Shifting Perspectives on AI Evaluation: The Increasing Role of Ethics in Cooperation. AI 2022, 3, 331–352. [Google Scholar] [CrossRef]

- Al Suwaidi, F.; Alshurideh, M.; Al Kurdi, B.; Salloum, S.A. The Impact of Innovation Management in SMEs Performance: A Systematic Review. In Proceedings of the International Conference on Advanced Intelligent Systems and Informatics Systems Frontiers 2020 (AISI 2020), Cairo, Egypt, 19–21 October 2020; Advances in Intelligent Systems and, Computing. Hassanien, A.E., Slowik, A., Snášel, V., El-Deeb, H., Tolba, F.M., Eds.; Springer: Cham, Switzerland, 2020; Volume 1261, pp. 720–730. [Google Scholar] [CrossRef]

- Yoo, W.-J.; Choo, H.H.; Lee, S.J. A Study on the Sustainable Growth of SMEs: The Mediating Role of Organizational Metacognition. Sustainability 2018, 10, 2829. [Google Scholar] [CrossRef] [Green Version]

- Rhodes, J.; Cheng, V.; Sadeghinejad, Z.; Lok, P. The relationship between management team (TMT) metacognition, entrepreneurial orientations and small and medium enterprises (SMEs) firm performance. Int. J. Manag. Pract. 2018, 11, 111–140. [Google Scholar] [CrossRef]

- Hawksworth, J.; Berriman, R.; Goel, S. Will Robots Really Steal Our Jobs? An International Analysis of the Potential Long-Term Impact of Automation; Price Waterhouse Coopers: London, UK, 2018; Available online: https://www.pwc.com/hu/hu/kiadvanyok/assets/pdf/impact_of_automation_on_jobs.pdf (accessed on 19 February 2022).

- Schwab, K. The Fourth Industrial Revolution; World Economic Forum: Geneva, Switzerland, 2016; ISBN 1944835008. [Google Scholar]

- Deane, P.M. The First Industrial Revolution; Cambridge University Press: Cambridge, UK, 1965; pp. 238–254. ISBN 0521048028. [Google Scholar]

- Wahlster, W. Director and CEO of the German Research Center for Artificial Intelligence. In Proceedings of the Hannover Messe, Industry 4.0, Hannover Fair, Hannover, Germany, 4–8 April 2011. [Google Scholar]

- Somayya, M.; Rajesh, M.H.; Durgesh, K.J. The Future Digital Work Force: Robotic Process Automation (RPA). J. Inf. Syst. Technol. Manag. 2019, 16, e201916001. Available online: https://www.scielo.br/pdf/jistm/v16/1807-1775-jistm-16-e201916001.pdf (accessed on 19 February 2022).

- Tom, M.M.; Hill, M. Machine Learning Definition, 1st ed.; McGraw-Hill: New York, NY, USA, 1997; Available online: http://www.cs.cmu.edu/afs/cs.cmu.edu/user/mitchell/ftp/mlbook.html (accessed on 19 February 2022).

- European Commission. European Enterprise Survey on the Use of Technologies Based on Artificial Intelligence; Final Report; Ipsos Belgium and International Centre for Innovation Technology and Education, Solvay Brussels School of Economics, Management, Eds.; Publications Office of the European Union: Luxembourg, 2020; ISBN1 978-92-76-20108-3. Available online: https://ec.europa.eu/digital-single-market/en/news/european-enterprise-survey-use-technologies-based-artificial-intelligence& (accessed on 10 January 2022)ISBN2 978-92-76-20108-3.

- Gerlind, W.; Biacabe, B.T.; Bormann, U.; Muntz, A.; Niehaus, G.; Soler, G.J.; Brauchitsch, B.V. Artificial Intelligence and Robotics and Their Impact on the Workplace. IBA Glob. Employ. Inst. 2017, 11, 49–57. Available online: https://www.ibanet.org/Article/NewDetail.aspx?ArticleUid=012a3473-007f-4519-827c-7da56d7e3509 (accessed on 14 March 2022).

- Ben-Ari, M.; Mondada, F. Robots and Their Applications. In Elements of Robotics; Springer: Cham, Switzerland, 2018. [Google Scholar] [CrossRef]

- Tractica Research. Robotics Market Forecasts; Informa Tech.: London, UK, 2019; Available online: https://omdia.tech.informa.com/OM000845/Robotics-Market-Forecasts (accessed on 10 January 2022).

- Robot Race: The World´s Top 10 Automated Countries; International Federation of Robots: Frankfurt, Germany. 2020. Available online: https://ifr.org/ifr-press-releases/news/robot-race-the-worlds-top-10-automated-countries (accessed on 12 January 2022).

- International Federation of Robots. Positioning Paper: The Impact of Robots on Productivity, Employment and Jobs; International Federation of Robots: Frankfurt, Germany, 2018; Available online: https://ifr.org/img/office/IFR_The_Impact_of_Robots_on_Employment.pdf (accessed on 12 January 2022).

- Thacher, T.D.; Pludowski, P.; Shaw, N.J.; Mughal, M.Z.; Munns, C.F.; Högler, W. Nutritional rickets in immigrant and refugee children. Public Health Rev. 2016, 37, 3. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Georgieff, A.; Milanez, A. Correlation between average percentage change in employment by country and percentage change in the use of industrial robots during the period 2012–2019. In What Happened to Jobs at High Risk of Automation; OECD Publishing: Paris, France, 2021. [Google Scholar]

- Graetz, G.; Michaels, G. Robots at Work. Rev. Econ. Stat. 2018, 100, 753–768. [Google Scholar] [CrossRef] [Green Version]

- Mazachek, K. Robots and the Economy. The Role of Automation in Driving Productivity Growth; Ascendant Program Services LLC for Select USA , Ed.; Department of Commerce: Washington, DC, USA, 2020. Available online: https://www.selectusa.gov/servlet/servlet.FileDownload?file=015t0000000kyXN (accessed on 9 January 2022).

- Timmer, M.; van Moergastel, T.; Stuivenwold, E.; Ypma, G. EUKLEMS Report—European Union Capital, Labor, Energy, Materials and Services Database. Available online: http://www.euklems.net/data/euklems_growth_and_productivity_accounts_part_i_methodology.pdf (accessed on 12 February 2022).

- Deepan, P.; Simon, P. IDC FutureScape: Worldwide Future of Work 2021 Predictions—Asia/Pacific (Excluding Japan) Implications, IDC Future Scape Reports. 2020. Available online: https://www.idc.com/getdoc.jsp?containerId=AP45873020 (accessed on 10 January 2022).

- International Federation of Robots.Executive Summary World Robotics 2021-Service Robots, World Robotics R&D Programs. 2021. Available online: https://ifr.org/img/worldrobotics/Executive_Summary_WR_Service_Robots_2021.pdf (accessed on 12 January 2022).

- Zhao, X.; Wu, C.; Liu, D. Comparative Analysis of the Life-Cycle Cost of Robot Substitution: A Case of Automobile Welding Production in China. Symmetry 2021, 13, 226. [Google Scholar] [CrossRef]

- Belanche, D.; Casaló, L.V.; Flavián, C. Frontline robots in tourism and hospitality: Service enhancement or cost reduction? Electron. Mark. 2020, 31, 477–492. [Google Scholar] [CrossRef]

- Chui, M.; Manyika, J.; Miremadi, M. Where Machines Could Replace Humans—And Where They Can’t (Yet); Mckinsey: Chicago, IL, USA, 2016; Available online: https://www.mckinsey.com/business-functions/digital-mckinsey/our-insights/where-machines-could-replace-humans-and-where-they-cant-yet (accessed on 20 January 2022).

- Wirtz, J.; Zeithaml, V. Cost-effective service excellence. J. Acad. Mark. Sci. 2017, 46, 59–80. [Google Scholar] [CrossRef] [Green Version]

- Xiao, L.; Kumar, V. Robotics for Customer Service: A Useful Complement or an Ultimate Substitute? J. Serv. Res. 2019, 24, 9–29. [Google Scholar] [CrossRef]

- Eurostat. Products Eurostat News. 25% of Large Enterprises in the EU Use Robots. Available online: https://ec.europa.eu/info/sites/info/files/file_import/2019-european-semester-country-reportromania_en.pdf (accessed on 20 January 2022).

- Eurostat. Annual Enterprise Statistics for Special Aggregates of Activities. Available online: https://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=sbs_na_sca_r2&lang=en (accessed on 9 January 2022).

- International Comparison Program. World Bank, World Development Indicators Database. World Bank, Eurostat-OECD PPP Programme. Available online: https://data.worldbank.org/indicator/NY.GDP.PCAP.PP.CD (accessed on 10 March 2022).

- Stiglitz, E.; Joseph, A.S.; Jean-Paul, F. Mismeasuring Our Lives: Why GDP Doesn’t Add Up: The Report; ReadHowYouWant: New York, NY, USA, 2010. [Google Scholar]

- Statista. Statista’s Most Important Companies in the Manufacturing Industry in Romania in 2019, by Revenue Report. Available online: https://www.statista.com/statistics/1115921/romania-companies-in-the-manufacturing-industry-by-revenue/; https://www.statista.com/study/64326/robotics/ (accessed on 19 March 2022).

| ° | F1 | F2 | F3 | F4 | F5 | F6 | F7 | F8 |

|---|---|---|---|---|---|---|---|---|

| Eigenvalue | 4.170 | 2.094 | 1.077 | 0.563 | 0.069 | 0.016 | 0.010 | 0.002 |

| Variability (%) | 52.122 | 26.174 | 13.456 | 7.041 | 0.860 | 0.204 | 0.119 | 0.024 |

| Cumulative % | 52.122 | 78.296 | 91.752 | 98.793 | 99.652 | 99.856 | 99.976 | 100.000 |

| Component | |||

|---|---|---|---|

| Factor | D1 | D2 | D3 |

| Use of industrial robots | 0.667 | −0.028 | −0.401 |

| GDP per capita | 0.918 | 0.237 | 0.121 |

| Employees-number | 0.088 | 0.987 | −0.011 |

| Growth rate of employment | 0.022 | −0.041 | 0.957 |

| Wages and salaries | 0.200 | 0.976 | −0.008 |

| Apparent Labor Productivity | 0.962 | 0.177 | −0.014 |

| Gross Value Added per employee | 0.969 | 0.184 | −0.041 |

| Turnover or gross premium written | 0.205 | 0.975 | −0.034 |

| Enterprise Name | General Industry |

|---|---|

| Astra Bus S.R.L | Automotive |

| Automobile Dacia S.A | Automotive |

| C&I Eurotrans XXI | Automotive |

| El Car Igescu S.N.C. | Automotive |

| Ford Romania | Automotive |

| ROMAN S.A. | Automotive |

| Continental AG | Automotive |

| KIRCHHOFF Automotive Romania SRL | Automotive |

| Daimler AG | Automotive |

| Greiner Packaging | Packaging manufacturer |

| Electroplast | Manufacturing of cables and electric cords |

| Braiconf | Manufacturing of textiles |

| Confind | Manufacturing of equipment |

| Noriel | Toy manufacturing |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Stoica, I.; Zaman, G.; Suciu, M.-C.; Purcărea, V.-L.; Jude, C.-R.; Radu, A.-V.; Catană, A.; Radu, A.-C. A Better Integration of Industrial Robots in Romanian Enterprises and the Labour Market. Appl. Sci. 2022, 12, 6014. https://doi.org/10.3390/app12126014

Stoica I, Zaman G, Suciu M-C, Purcărea V-L, Jude C-R, Radu A-V, Catană A, Radu A-C. A Better Integration of Industrial Robots in Romanian Enterprises and the Labour Market. Applied Sciences. 2022; 12(12):6014. https://doi.org/10.3390/app12126014

Chicago/Turabian StyleStoica (Răpan), Ivona, Gheorghe Zaman, Marta-Christina Suciu, Victor-Lorin Purcărea, Cornelia-Rodica Jude, Andra-Victoria Radu, Aida Catană, and Anamaria-Cătălina Radu. 2022. "A Better Integration of Industrial Robots in Romanian Enterprises and the Labour Market" Applied Sciences 12, no. 12: 6014. https://doi.org/10.3390/app12126014

APA StyleStoica, I., Zaman, G., Suciu, M.-C., Purcărea, V.-L., Jude, C.-R., Radu, A.-V., Catană, A., & Radu, A.-C. (2022). A Better Integration of Industrial Robots in Romanian Enterprises and the Labour Market. Applied Sciences, 12(12), 6014. https://doi.org/10.3390/app12126014