Blockchain, Enterprise Resource Planning (ERP) and Accounting Information Systems (AIS): Research on e-Procurement and System Integration

Abstract

1. Introduction

2. Literature Review and Related Work

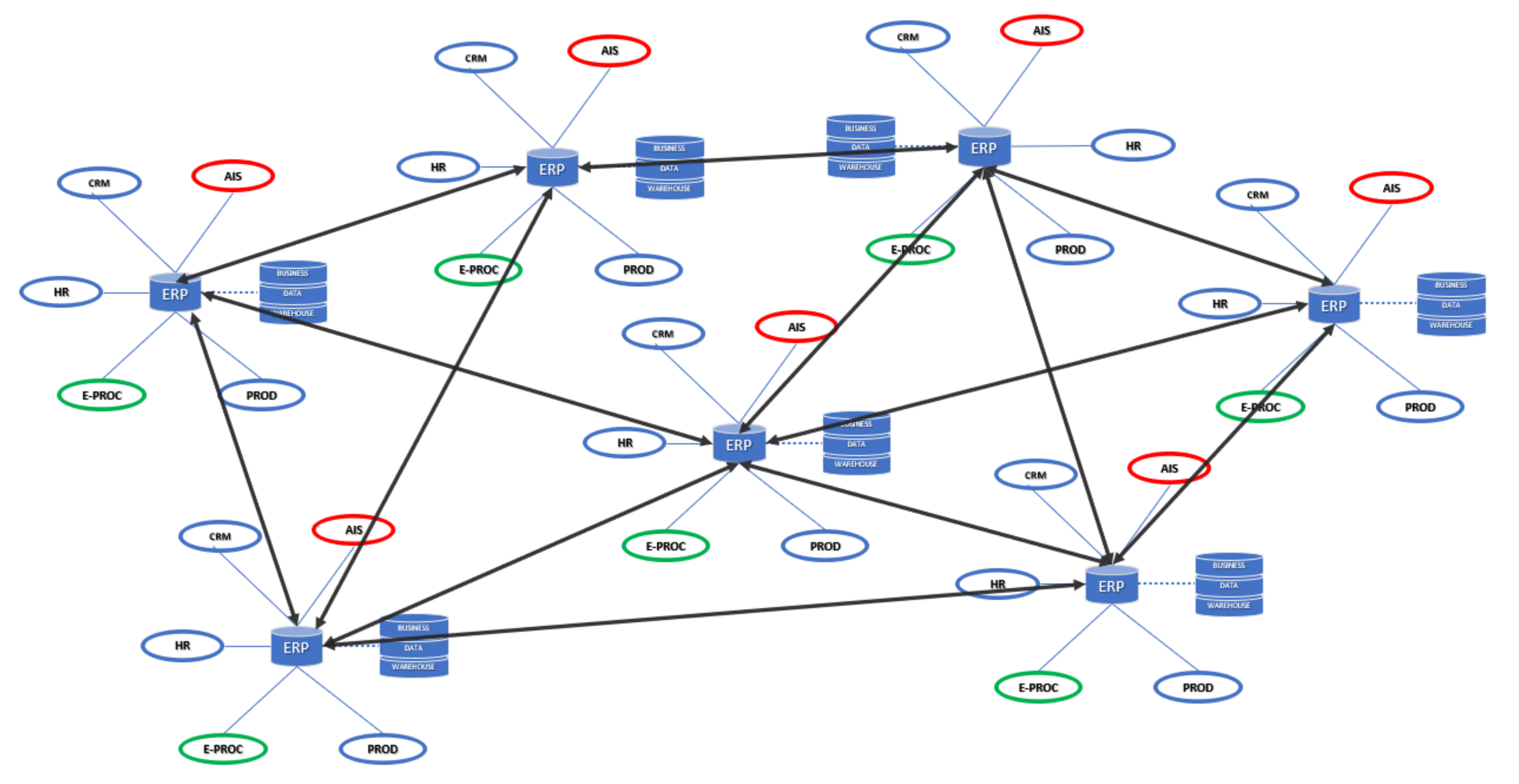

2.1. Accounting, AIS and ERP and DLT

2.2. Blockchain

2.3. Blockchain Applications in Business Areas Other Than Accounting

- Verifiability of data: Applications in this category use the properties of immutability and transparency of blockchain technology by recording some characteristics of data or documents on it. These are visible and verifiable by other ecosystem players or third parties. Among these projects, there are applications commonly known as “notarisation”. For example, a document is timestamped to make verifiable the date of creation and the fact that it has not been modified over time. Many projects of this type have been developed in agrifood to offer more significant guarantees to the final consumer on the traceability of products [71].

- Data coordination: Most of the use cases implement blockchain and distributed ledger technologies in data sharing processes, not only by notarising information but also by exploiting smart contracts to bring data exchange on-chain, allowing more effective coordination and efficiency between the different actors. These applications are developed mainly to reconcile information maintained by other actors, avoiding the emergence of divergences and conflicts. In these projects, blockchain often replaces the role of intermediaries [72].

- The realisation of reliable processes. This is the category in which the most ambitious projects fall, aiming to run entire business processes on blockchain to ensure that every step is verifiable. In these projects, the business process is coded through smart contracts using a blockchain platform. It is also clearly the most complex and challenging application scenario to be implemented [73].

3. Methods

- (1)

- ERP and AIS systems can benefit from decentralised architecture and blockchain;

- (2)

- E-Procurement can facilitate the integration of ERP and AIS systems;

- (3)

- The integration of these systems.

- -

- Which are the particular benefits from blockchain applications on ERP, AIS and e-procurement in particular?

- -

- Does FinTech provide benefits and generate value?

- -

- Is DeFI an effective way to integrate systems and applications?

4. Case Study Analysis and Results

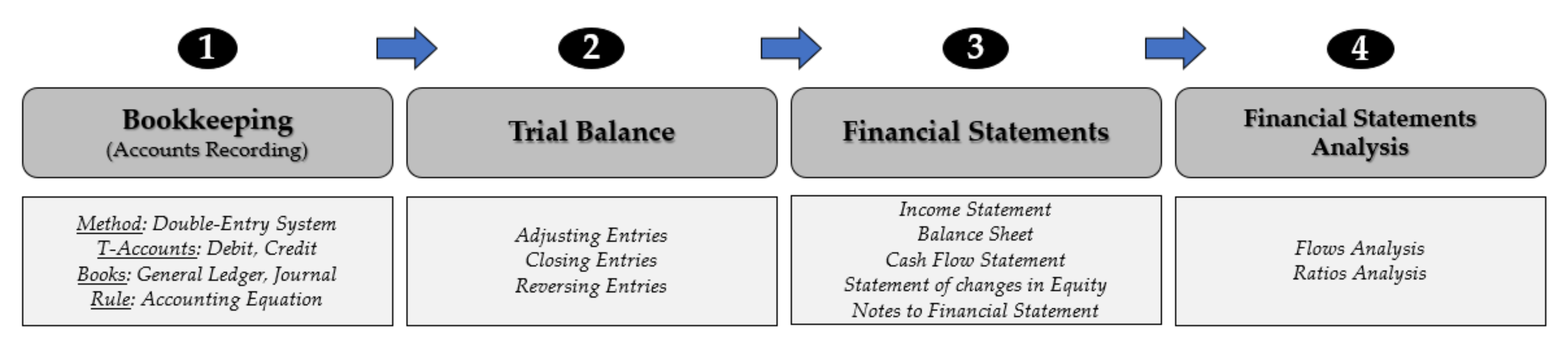

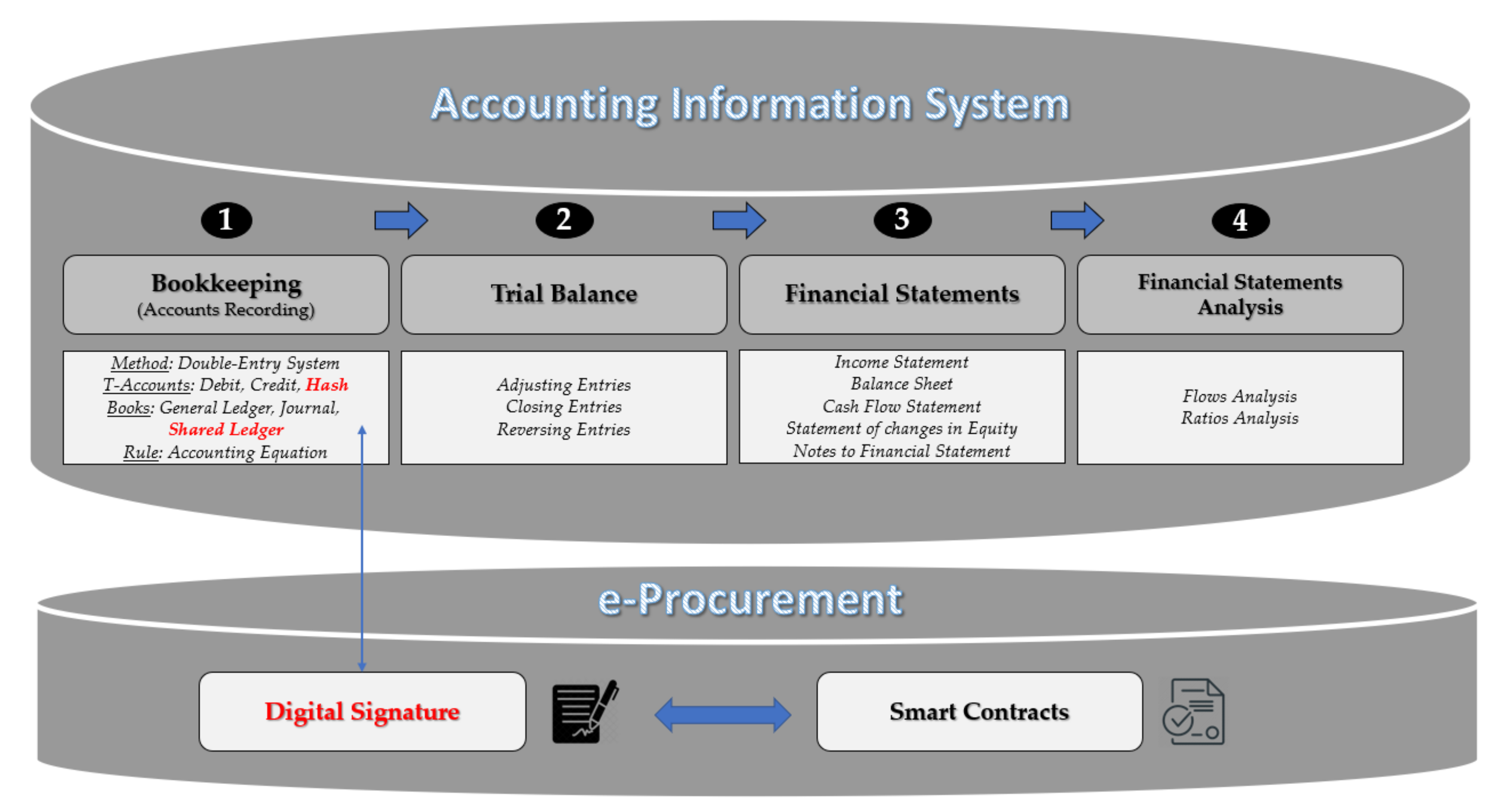

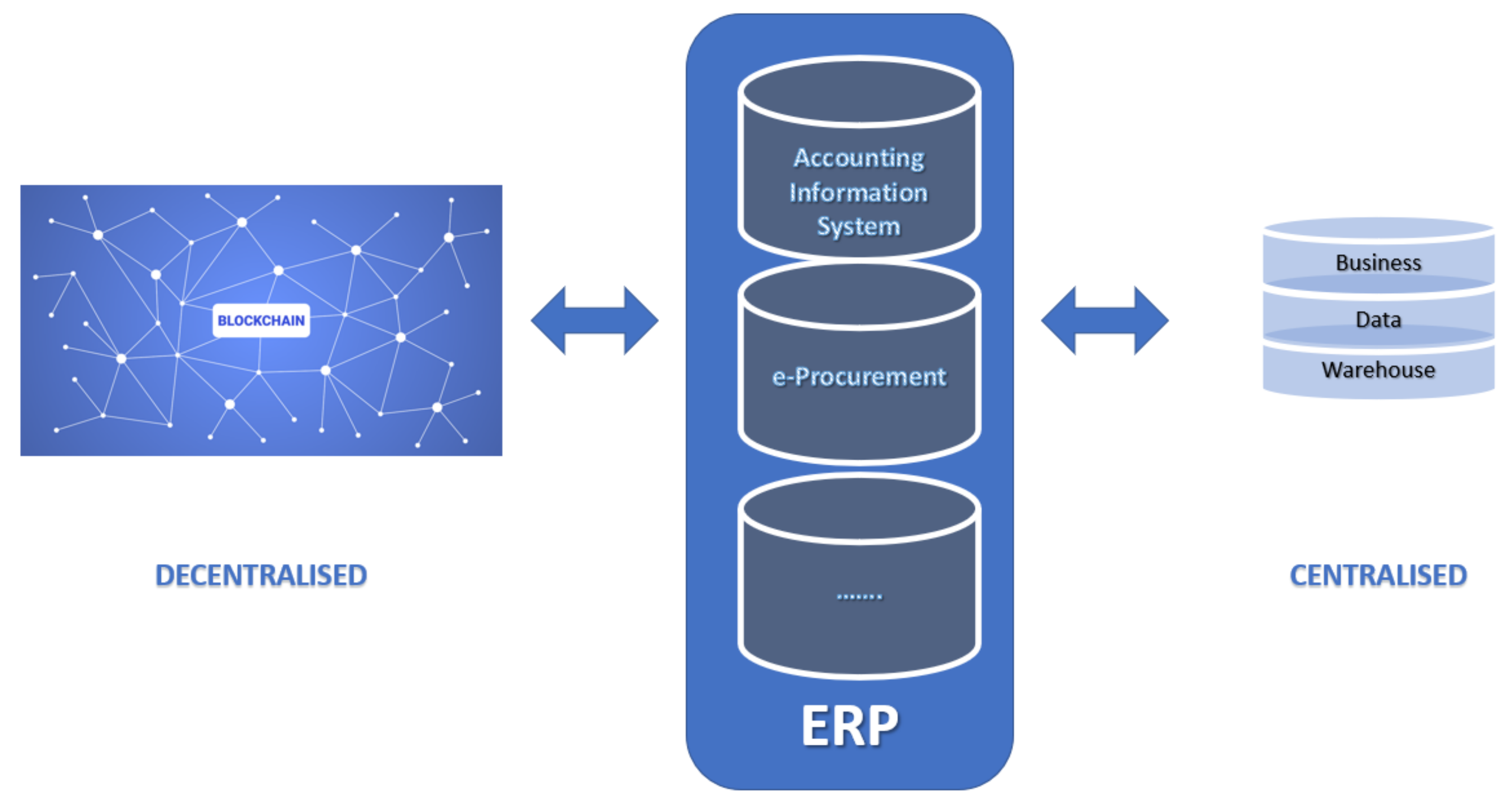

4.1. ERP Mapping

- -

- It allows combining each area of the company because all data is collected in a shared database.

- -

- It has a modular structure that we will deepen below.

- -

- It is customisable. That is, it presents a prescriptive approach that favours business process reengineering. This means that the program itself is implemented in such a way as to adapt it to the needs of individual companies and the particular function it will perform.

- -

- Improves business efficiency from an operational point of view, reducing costs and increasing control over company management.

- -

- The risk is lowered thanks to the integrity of the data and thanks to a more significant number of financial controls.

- -

- They increased management efficiency. The data are readily available as they are present in a single database. This allows to speed up and make business and decision-making processes more reliable and reduce the costs related to operational management.

- -

- The shared system allows more users to access a more significant number of information.

- -

- There is better management of human resources such as workers and employees.

4.2. The Benefits in E-Procurement and Blockchain Applications

- -

- Reduced procurement time and efficiency. Compared to traditional methods, the management of online purchases allows to speed up communication times between buyers and suppliers and improve order processing and thus efficiency.

- -

- IT automation and productivity. The automation of procurement processes with the related alert system allows you to drastically reduce the preparation time of purchase orders and the management of requests by the various company departments concerned. This can substantially save time and increase productivity.

- -

- Costs reduction. The cost reduction is significant in many respects: from paper savings to optimising the personnel involved in managing the practices to reduce inventories and warehouse waste.

- -

- Security, reliability and safety. The e-procurement systems guarantee the transfer and retention of data in compliance with the stringent privacy regulations in force. Furthermore, the reliability of data transmissions (via VPN and encrypted) is ensured by a timely and system-wide security check.

- -

- Flexibility and quality. Thanks to e-procurement platforms, the accessibility of information, the analysis and verification of offers, and the timely management and control of tenders are much more flexible and effective. Furthermore, to reduce the margin of errors and facilitate the use of the platform, there is also a dedicated service desk able to provide operational and functional support in real-time [106,107,108].

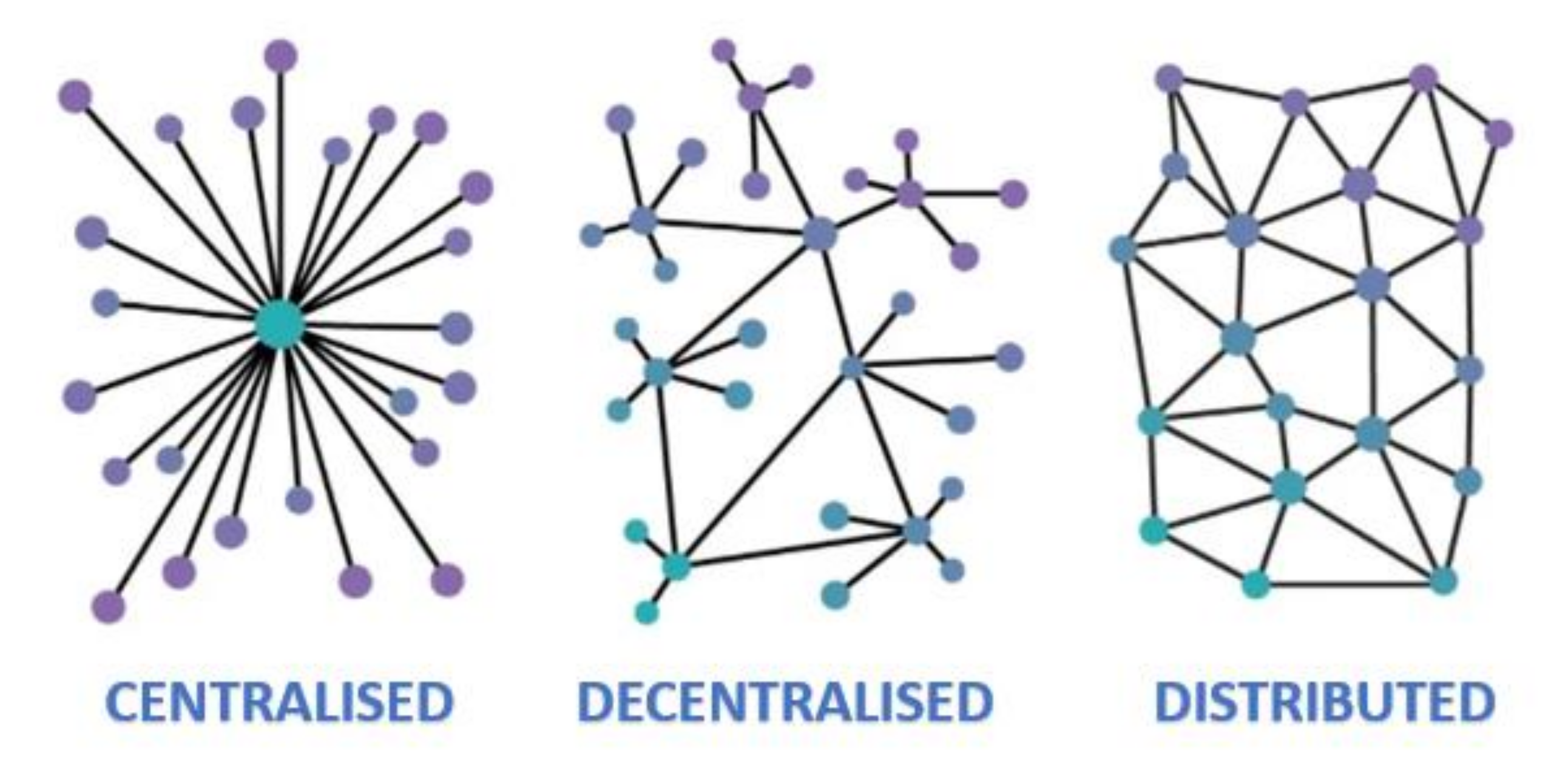

4.3. Blockchain and Decentralisation

4.4. Financial Technology and Decentralized Finance Applications and Integration

5. Discussion and Conclusions

6. Limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Uddin, M.; Alam, M.S.; Mamun, A.A.; Khan, T.U.Z.; Akter, A. A study of the adoption and implementation of enterprise resource planning (ERP): Identification of moderators and mediator. J. Open Innov. Technol. Mark. Complex. 2020, 6, 2. [Google Scholar] [CrossRef]

- Elabdallaoui, H.E.; Elfazziki, A.; Sadgal, M. A Blockchain-Based Platform for the e-Procurement Management in the Public Sector. In International Conference on Model and Data Engineering; Springer: Berlin/Heidelberg, Germany, 2021; pp. 213–223. [Google Scholar]

- Jelassi, T.; Martínez-López, F.J. Interaction with Suppliers: E-Procurement. In Strategies for e-Business; Springer: Berlin/Heidelberg, Germany, 2020; pp. 275–305. [Google Scholar]

- Definition of Enterprise Resource Planning (ERP). Available online: https://www.oracle.com/uk/erp/what-is-erp/ (accessed on 23 July 2021).

- Turner, L.; Weickgenannt, A.B.; Copeland, M.K. Accounting Information Systems: Controls and Processes; John Wiley & Sons: Hoboken, NJ, USA, 2020. [Google Scholar]

- Cleary, P. Introduction to Accounting Information Systems. In The Routledge Companion to Accounting Information Systems; Routledge: London, UK, 2017; pp. 3–12. [Google Scholar]

- Curtis, G.; Cobham, D.; Cobham, D.P. Business Information Systems: Analysis, Design and Practice; Pearson Education: London, UK, 2008. [Google Scholar]

- Romney, M.B.; Steinbart, P.J.; Cushing, B.E. Accounting Information Systems; Prentice-Hall: Upper Saddle River, NJ, USA, 2000. [Google Scholar]

- Brecht, H.D.; Martin, M.P. Accounting information systems: The challenge of extending their scope to business and information strategy. Account. Horiz. 1996, 10, 16. [Google Scholar]

- Kocsis, D. A conceptual foundation of design and implementation research in accounting information systems. Int. J. Account. Inf. Syst. 2019, 34, 100420. [Google Scholar] [CrossRef]

- Teittinen, H.; Pellinen, J.; Järvenpää, M. ERP in action—Challenges and benefits for management control in SME context. Int. J. Account. Inf. Syst. 2013, 14, 278–296. [Google Scholar] [CrossRef]

- Mahmood, F.; Khan, A.Z.; Bokhari, R.H. ERP issues and challenges: A research synthesis. Kybernetes 2019, 49, 629–659. [Google Scholar] [CrossRef]

- Petratos, P.; Faccia, A. Accounting Information Systems and System of Systems: Assessing Security with Attack Surface Methodology. In Proceedings of the 2019 3rd International Conference on Cloud and Big Data Computing, Oxford, UK, 28 August 2019; pp. 100–105. [Google Scholar]

- Rizkiana, A.K.; Ritchi, H.; Adrianto, Z. Critical Success Factors Enterprise Resource Planning (ERP) Implementation in Higher Education. J. Account. Audit. Bus. 2021, 4, 54–65. [Google Scholar] [CrossRef]

- Haddara, M. ERP systems selection in multinational enterprises: A practical guide. Int. J. Inf. Syst. Proj. Manag. 2018, 6, 43–57. [Google Scholar]

- Demi, S.; Haddara, M. Do cloud ERP systems retire? An ERP lifecycle perspective. Procedia Comput. Sci. 2018, 138, 587–594. [Google Scholar] [CrossRef]

- Zhezhnych, P.; Tarasov, D. Methods of data processing restriction in ERP systems. In Proceedings of the 2018 IEEE 13th International Scientific and Technical Conference on Computer Sciences and Information Technologies (CSIT), Lviv, Ukraine, 11–14 September 2018. [Google Scholar]

- Hadidi, M.; Hadidi, S. ERP Security Based on Web Services. Glob. J. Comput. Sci. Technol. 2020, 20, 23–25. [Google Scholar]

- Bondarevskiy, A.S.; Lebedev, A.V. Pseudo-control in ERP control systems. In Proceedings of the Global Science, Montpellier, France, 25 December 2018. [Google Scholar]

- Parthasarathy, S.; Sharma, S. Efficiency analysis of ERP packages—A customisation perspective. Comput. Ind. 2016, 82, 19–27. [Google Scholar] [CrossRef]

- Faccia, A.; Moşteanu, N.R.; Fahed, M.; Capitanio, F. Accounting Information Systems and ERP in the UAE: An Assessment of the Current and Future Challenges to Handle Big Data. In Proceedings of the 2019 3rd International Conference on Cloud and Big Data Computing, Oxford, UK, 28 August 2019; pp. 90–94. [Google Scholar]

- Al-Hashimy, H.N.H.; Al Jubair, A.S.; Jasim, E.T. The effect of accounting information systems (AIS) on enterprise resource planning (ERP). J. Southwest Jiaotong Univ. 2019, 54. [Google Scholar] [CrossRef]

- Grabski, S.V.; Leech, S.A.; Schmidt, P.J. A review of ERP research: A future agenda for accounting information systems. J. Inf. Syst. 2011, 25, 37–78. [Google Scholar] [CrossRef]

- Porras-Gonzalez, E.R.; Martín-Martín, J.M.; Guaita-Martínez, J.M. A critical analysis of the advantages brought by blockchain technology to the global economy. Int. J. Intellect. Prop. Manag. 2019, 9, 166–184. [Google Scholar] [CrossRef]

- Golosova, J.; Romanovs, A. The advantages and disadvantages of the blockchain technology. In Proceedings of the 2018 IEEE 6th workshop on advances in information, electronic and electrical engineering (AIEEE), Vilnius, Lithuania, 8–10 November 2018. [Google Scholar]

- Huang, H.; Lin, J.; Zheng, B.; Zheng, Z.; Bian, J. When Blockchain meets distributed file systems: An overview, challenges, and open issues. IEEE Access 2020, 8, 50574–50586. [Google Scholar] [CrossRef]

- Banerjee, A. Blockchain technology: Supply chain insights from ERP. In Advances in Computers; Elsevier: Amsterdam, The Netherlands, 2020; pp. 69–98. [Google Scholar]

- Parikh, T. The ERP of the future: Blockchain of things. Int. J. Sci. Res. Sci. Eng. Technol. 2018, 4, 1341–1348. [Google Scholar]

- Hader, M.; Elmhamedi, A.; Abouabdellah, A. Blockchain Integrated ERP Fora Bette Supply Chain Management. In Proceedings of the 2020 IEEE 7th International Conference on Industrial Engineering and Applications (ICIEA), Bangkok, Thailand, 16–18 April 2020. [Google Scholar]

- Dai, J.; Vasarhelyi, M.A. Toward blockchain-based accounting and assurance. J. Inf. Syst. 2017, 31, 5–21. [Google Scholar] [CrossRef]

- Shraideh, M.; Drieschner, C.; Betzwieser, B.; Kienegger, H.; Utesch, M.; Krcmar, H. Using a project-based learning approach for teaching emerging technologies: An example of a practical course for introducing SAP Leonardo and SAP HANA. In Proceedings of the 2018 IEEE Global Engineering Education Conference (EDUCON), Canary Islands, Spain, 18–20 April 2018. [Google Scholar]

- Ibañez, J.I.; Bayer, C.N.; Tasca, P.; Xu, J. Triple-Entry Accounting, Blockchain and Next of Kin: Towards a Standardisation of Ledger Terminology. 2021. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3760220 (accessed on 23 July 2021).

- Ibañez, J.I.; Bayer, C.N.; Tasca, P.; Xu, J. Triple-entry accounting: A typology. arXiv 2021, arXiv:2101.02632. [Google Scholar]

- Faccia, A.; Moşteanu, N.R. Accounting and blockchain technology: From double-entry to triple-entry. Bus. Manag. Rev. 2019, 10, 108–116. [Google Scholar]

- Moşteanu, N.R.; Faccia, A. x Digital Systems and New Challenges of Financial Management–FinTech, XBRL, Blockchain and Cryptocurrencies. Qual. Access Success J. 2019, 21, 159–166. [Google Scholar]

- Mosteanu, N.R.; Faccia, A. Fintech Frontiers in Quantum Computing, Fractals, and Blockchain Distributed Ledger: Paradigm Shifts and Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 19. [Google Scholar] [CrossRef]

- Davila, A.; Gupta, M.; Palmer, R. Moving procurement systems to the Internet: The adoption and use of e-procurement technology models. Eur. Manag. J. 2003, 21, 11–23. [Google Scholar] [CrossRef]

- Johnson, P.F.; Klassen, R.D. E-procurement. MIT Sloan Manag. Rev. 2005, 46, 7. [Google Scholar]

- Postmes, P.; Exalto-Sijbrands, M.; Ravesteyn, P. E-Procurement as digital collaboration in an integrated coalition limited by EU regulation. In International Conference on Management, Leadership & Governance; Academic Conferences International Limited: Reading, UK, 2018. [Google Scholar]

- Panayiotou, N.A.; Gayialis, S.P.; Tatsiopoulos, I.P. An e-procurement system for governmental purchasing. Int. J. Prod. Econ. 2004, 90, 79–102. [Google Scholar] [CrossRef]

- Bof, F.; Previtali, P. Organisational pre-conditions for e-procurement in governments: The Italian experience in the public health care sector. Electron. J. E-Gov. 2007, 5, 1–10. [Google Scholar]

- McCue, C.; Roman, A.V. E-procurement: Myth or reality. J. Public Procure. 2012, 12, 221–248. [Google Scholar] [CrossRef]

- Seong, S.K.; Lee, J.Y. Developing e-procurement systems: A case study on the government e-procurement systems in Korea. Public Financ. Manag. 2004, 4, 138–166. [Google Scholar]

- Roman, A.V. Challenges in maximising transformative impacts: Public policy and financial management through e-procurement. J. Public Procure 2013, 13, 337–363. [Google Scholar] [CrossRef]

- Bendoly, E.; Schoenherr, T. ERP system and implementation-process benefits: Implications for B2B e-procurement. Int. J. Oper. Prod. Manag. 2005, 25, 304–319. [Google Scholar] [CrossRef]

- Rajkumar, T.M. E-procurement: Business and technical issues. IS Manag. Handb. 2001, 18, 52–60. [Google Scholar] [CrossRef]

- Soliman, K.S.; Janz, B.D.; Puschmann, T.; Alt, R. Successful use of e-procurement in supply chains. Supply Chain Manag. Int. J. 2005, 10, 122–133. [Google Scholar]

- Mital, M.; Pani, A.; Ramesh, R. Determinants of choice of semantic web based Software as a Service: An integrative framework in the context of e-procurement and ERP. Comput. Ind. 2014, 65, 821–827. [Google Scholar] [CrossRef]

- Grilo, A.; Jardim-Goncalves, R.; Ghimire, S. E-procurement in the era of cloud computing. In 4th international conference on IS management and evaluation (ICIME 2013), Ho Chi Minh City, Vietnam, 13–14 May 2013. [Google Scholar]

- Oliveira, L.M.; Amorim, P.P. Public e-procurement. Int. Financ. Law Rev. 2001, 2001, 43. [Google Scholar]

- Kaur, R.; Kaur, A. Digital signature. In Proceedings of the 2012 International Conference on Computing Sciences, Phagwara, India, 14–15 September 2012. [Google Scholar]

- Arruñada, B. Mandatory accounting disclosure by small private companies. Eur. J. Law Econ. 2011, 32, 377–413. [Google Scholar] [CrossRef]

- Brewster, M. Unaccountable: How the Accounting Profession Forfeited a Public Trust; John Wiley & Sons: Hoboken, NJ, USA, 2009. [Google Scholar]

- Padhi, S.N. SAP® ERP Financials and FICO Handbook; Jones & Bartlett Learning: London, UK, 2009. [Google Scholar]

- Weidner, S.; Koch, B.; Bernhardt, C. Introduction to SAP; SAP University: Beijing, China, 2015. [Google Scholar]

- Faccia, A.; Al Naqbi, M.Y.K.; Lootah, S.A. Integrated Cloud Financial Accounting Cycle: How Artificial Intelligence, Blockchain, and XBRL will Change the Accounting, Fiscal and Auditing Practices. In Proceedings of the 2019 3rd International Conference on Cloud and Big Data Computing, Oxford, UK, 28 August 2019. [Google Scholar]

- Faccia, A.; Manni, F.; Capitanio, F. The possible combination of mandatory ESG reporting and XBRL taxonomies. ESG Ratings and Income Statement, a sustainable value-added disclosure. Sustainability 2021, in press. [Google Scholar]

- Purcinelli, L.M.; Abreu, R.; Vasconcelos, A.L. Sustainable and Smart System: Rethinking Accounting and Taxation in Portugal. In Governance and Sustainability; Springer: Singapore, 2020. [Google Scholar]

- Linh, N.T.M.; Phuong, T.B. Mandatory of E-invoice: Adaption Process of Vietnam. In Proceedings of the 2020 International Conference on Management of e-Commerce and e-Government, Jeju, Korea, 1 July 2020. [Google Scholar]

- Salmony, M.; Harald, B. E-invoicing in Europe: Now and the future. J. Paym. Strategy Syst. 2010, 4, 371–380. [Google Scholar]

- Duong, T.; Chepurnoy, A.; Fan, L.; Zhou, H.S. Twinscoin: A cryptocurrency via proof-of-work and proof-of-stake. In Proceedings of the 2nd ACM Workshop on Blockchains Cryptocurrencies, and Contracts, Incheon, Korea, 22 May 2018. [Google Scholar]

- Mori, T. Financial technology: Blockchain and securities settlement. J. Secur. Oper. Custody 2016, 8, 208–227. [Google Scholar]

- Demi, S.; Colomo-Palacios, R.; Sánchez-Gordón, M. Software Engineering Applications Enabled by Blockchain Technology: A Systematic Mapping Study. Appl. Sci. 2021, 11, 2960. [Google Scholar] [CrossRef]

- Pilkington, M. Blockchain technology: Principles and applications. In Research Handbook on Digital Transformations; Edward Elgar Publishing: Cheltenham, UK, 2016. [Google Scholar]

- Zheng, Z.; Xie, S.; Dai, H.; Chen, X.; Wang, H. An overview of blockchain technology: Architecture, consensus, and future trends. In Proceedings of the 2017 IEEE International Congress on Big Data (Big Data Congress), Boston, MA, USA, 11–14 December 2017. [Google Scholar]

- Onik, M.M.H.; Miraz, M.H. Performance analytical comparison of blockchain-as-a-service (baas) platforms. In Proceedings of the International Conference for Emerging Technologies in Computing, London, UK, 19–21 August 2019. [Google Scholar]

- Treiblmaier, H.; Sillaber, C. A case study of blockchain-induced digital transformation in the public sector. In Blockchain and Distributed Ledger Technology Use Cases; Springer: Berlin/Heidelberg, Germany, 2020. [Google Scholar]

- Swan, M. Blockchain economics: “Ripple for ERP”. Eur. Financ. Rev. 2018, Vol. 2, 24–27. [Google Scholar]

- De Vries, P.D. An analysis of cryptocurrency, bitcoin, and the future. Int. J. Bus. Manag. Commer. 2016, 1, 1–9. [Google Scholar]

- Maull, R.; Godsiff, P.; Mulligan, C.; Brown, A.; Kewell, B. Distributed ledger technology: Applications and implications. Strateg. Chang. 2017, 26, 481–489. [Google Scholar] [CrossRef]

- Benčić, F.M.; Skočir, P.; Žarko, I.P. DL-Tags: DLT and smart tags for decentralised, privacy-preserving, and verifiable supply chain management. IEEE Access 2019, 7, 46198–46209. [Google Scholar] [CrossRef]

- Arslan, S.S.; Jurdak, R.; Jelitto, J.; Krishnamachari, B. Advancements in Distributed Ledger Technology for Internet of Things; Elsevier: Amsterdam, The Netherlands, 2020. [Google Scholar]

- Dietzmann, C.; Heines, R.; Alt, R. The convergence of distributed ledger technology and artificial intelligence: An end-to-end reference lending process for financial services. In Proceedings of the Twenty-Eighth European Conference on Information Systems (ECIS2020), Vitual Conference; 2020. [Google Scholar]

- Wang, D.; Zhao, J.; Mu, C. Research on Blockchain-Based E-Bidding System. Appl. Sci. 2021, 11, 4011. [Google Scholar]

- Elbahri, F.M.; Al-Sanjary, O.I.; Ali, M.A.; Naif, Z.A.; Ibrahim, O.A.; Mohammed, M.N. Difference comparison of SAP, Oracle, and Microsoft solutions based on cloud ERP systems: A review. In Proceedings of the 2019 IEEE 15th International Colloquium on Signal Processing & Its Applications (CSPA), Penang, Malaysia, 8–9 March 2019. [Google Scholar]

- Singla, A.R.; Goyal, D.P. Success factors in ERP systems design implementation: An empirical investigation of the Indian industry. Int. J. Bus. Inf. Syst. 2007, 2, 444–464. [Google Scholar] [CrossRef]

- Preger, R. The Oracle Story, Part 1: 1977-1986. IEEE Ann. Hist. Comput. 2012, 34, 51–57. [Google Scholar] [CrossRef]

- Gargeya, V.B.; Brady, C. Success and failure factors of adopting SAP in ERP system implementation. Bus. Process Manag. J. 2005, 11, 501–516. [Google Scholar] [CrossRef]

- Singh, N.P. Critical analysis of expansion strategies of SAP, IBM, Oracle and Microsoft in the area of business intelligence. Int. J. Strateg. Inf. Technol. Appl. 2011, 2, 23–43. [Google Scholar] [CrossRef][Green Version]

- Adams, K.; Piazzoni, E.; Suh, I.S. Comparative Analysis of ERP Vendors: SAP, Oracle, and Microsoft; School of Business and Economics, Indiana University South Bend: South Bend, IN, USA, 2008. [Google Scholar]

- Mounla, R. Microsoft Dynamics 365 Extensions Cookbook; Packt Publishing Ltd.: New York, NY, USA, 2017. [Google Scholar]

- Implementation of SAP, Oracle and Microsoft Solutions. Available online: https://home.kpmg/hu/en/home/services/advisory/management/it/erp-advisory/solution-implementation.html (accessed on 23 July 2021).

- Hoch, D.J.; Roeding, C.; Lindner, S.K.; Purkert, G. Secrets of software success.; Boston: Harvard Business School Press: Boston, MA, USA, 2000. [Google Scholar]

- Cristea, A.D.; Prostean, O.; Muschalik, T.; Tirian, O. The advantages of using SAP NetWeaver platform to implement a multidisciplinary project. In Proceedings of the 2010 International Joint Conference on Computational Cybernetics and Technical Informatics, Timisoara, Romania, 27–29 May 2010. [Google Scholar]

- Jones, P.; Burger, J. Configuring SAP ERP Financials and Controlling; Wiley: Hoboken, NJ, USA, 2009. [Google Scholar]

- Korkmaz, A. Financial Reporting with SAP; Galileo Press: Bonn, Germany, 2008. [Google Scholar]

- Pinsonneault, A.; Kraemer, K. Survey research methodology in management information systems: An assessment. J. Manag. Inf. Syst. 1993, 10, 75–105. [Google Scholar] [CrossRef]

- Haddadi, A.; Hosseini, A.; Johansen, A.; Olsson, N. Pursuing value creation in construction by research-A study of applied research methodologies. Procedia Comput. Sci. 2017, 121, 1080–1087. [Google Scholar] [CrossRef]

- Nunamaker, J.F., Jr.; Chen, M.; Purdin, T.D. Systems development in information systems research. J. Manag. Inf. Syst. 1990, 7, 89–106. [Google Scholar] [CrossRef]

- Hustad, E.; Haddara, M.; Kalvenes, B. ERP and organisational misfits: An ERP customisation journey. Procedia Comput. Sci. 1990, 100, 429–439. [Google Scholar] [CrossRef][Green Version]

- Viorel-Costin, B. SAP MM/WMS-implementation of an ERP system-analysis and recommendations in the IT unit testing phase. A case study (III). Ann. Econ. Ser. 2020, 1, 16–21. [Google Scholar]

- Billyan, B.F.; Irawan, M.I. Analysis of Technology Acceptance of Enterprise Resource Planning (ERP) System in The Regional Office of PT. XYZ Throughout Indonesia. J. Phys.Conf. Ser. 2021, 1844, 012008. [Google Scholar] [CrossRef]

- Savchuk, R.R.; Kirsta, N.A. Managing of the Business Processes in Enterprise by Moving to SAP ERP System. In Proceedings of the 2019 IEEE Conference of Russian Young Researchers in Electrical and Electronic Engineering (EIConRus), Saint Petersburg, Russia, 28–31 January 2019. [Google Scholar]

- SAP Products from A-Z. Available online: https://www.sap.com/products-a-z.html (accessed on 23 July 2021).

- SAP ERP Technical & Functional Modules Complete List. Available online: https://www.guru99.com/sap-modules.html (accessed on 23 July 2021).

- SAP Modules—Complete List of ERP SAP R/3 Modules. Available online: https://www.tutorialkart.com/sap/sap-modules-list/ (accessed on 23 July 2021).

- SAP ERP Modules: Complete List (SAP ERP Components). Available online: https://inui.io/sap-erp-modules/ (accessed on 23 July 2021).

- Cocca, P.; Marciano, F.; Rossi, D.; Alberti, M. Business software offer for industry 4.0: The SAP case. IFAC Pap. 2018, 51, 1200–1205. [Google Scholar] [CrossRef]

- Gräther, W.; Kolvenbach, S.; Ruland, R.; Schütte, J.; Torres, C.; Wendland, F. Blockchain for education: Lifelong learning passport. In Proceedings of the 1st ERCIM Blockchain Workshop 2018, European Society for Socially Embedded Technologies (EUSSET), Amsterdam, The Netherlands, 8–9 May 2018. [Google Scholar]

- SAP Unveils Blockchain Service in the Cloud. Available online: https://www.cnbc.com/2017/05/17/sap-unveils-blockchain-service-in-the-cloud.html (accessed on 23 July 2021).

- Our 2019 Observation: SAP Leonardo is Now Dead. Available online: https://www.brightworkresearch.com/our-2019-observation-sap-leonardo-is-now-dead/ (accessed on 23 July 2021).

- Action Required: Migrate your Azure Blockchain Service Data by 10 September. 2021. Available online: https://azure.microsoft.com/en-us/updates/action-required-migrate-your-azure-blockchain-service-data-by-10-september-2021/ (accessed on 23 July 2021).

- Kappauf, J.; Lauterbach, B.; Koch, M. Logistic Core Operations with SAP: Procurement, Production and Distribution Logistics; Springer: Berlin/Heidelberg, Germany, 2011. [Google Scholar]

- Yarramalli, S.S.; Ponnam, R.S.M.; Rao, G.R.K.; Fathimabi, S.K.; Madasu, P. Digital Procurement on Systems Applications and Products (SAP) Cloud Solutions. In Proceedings of the 2020 Second International Conference on Inventive Research in Computing Applications (ICIRCA), Coimbatore, India, 15–17 July 2020. [Google Scholar]

- Ghattamneni, M.R. Future of B2B networks based on ERP (Enterprise Resource Package) packages like SAP, Ariba. Int. J. Manag. IT Eng. 2016, 6, 122–126. [Google Scholar]

- Ageshin, E.A. E-procurement at work: A case study. Prod. Inventory Manag. J. 2001, 42, 48–53. [Google Scholar]

- Ferreira, I.; Amaral, L.A. Public e-procurement: Advantages, limitations and technological” pitfalls”. In Proceedings of the 9th International Conference on Theory and Practice of Electronic Governance, Montevideo, Uruguay, 1–3 March 2016. [Google Scholar]

- Roche, J. Are you ready for e-procurement? Strateg. Financ. 2001, 83, 56. [Google Scholar]

- Cappiello, B.; Carullo, G. Introduction: The Challenges and Opportunities of Blockchain Technologies. In Blockchain, Law and Governance; Springer: Cham, Swizterland, 2021; pp. 1–9. [Google Scholar]

- Cong, L.W.; He, Z. Blockchain disruption and smart contracts. Rev. Financ. Stud. 2019, 32, 1754–1797. [Google Scholar] [CrossRef]

- Cieplak, J.; Leefatt, S. Smart contracts: A smart way to automate performance. Georget. Law Technol. Rev. 2017, 1, 417–427. [Google Scholar]

- He, M.D.; Leckow, M.R.B.; Haksar, M.V.; Griffoli, M.T.M.; Jenkinson, N.; Kashima, M.M.; Khiaonarong, T.; Rochon, M.C.; Tourpe, H. Fintech and Financial Services: Initial Considerations; International Monetary Fund: Washington, DC, USA, 2017. [Google Scholar]

- Khan, M.K.; He, Y.; Akram, U.; Zulfiqar, S.; Usman, M. Firms’ technology innovation activity: Does financial structure matter? Asia-Pac. J. Financ. Stud. 2018, 47, 329–353. [Google Scholar] [CrossRef]

- Alshawi, S.; Themistocleous, M.; Almadani, R. Integrating diverse ERP systems: A case study. J. Enterp. Inf. Manag. 2004, 17, 454–462. [Google Scholar] [CrossRef]

- Bouveret, A. Cyber Risk for the Financial Sector: A Framework for Quantitative Assessment; International Monetary Fund: Washington, DC, USA, 2018. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Module Code | Business Function | Module Code | Business Function |

|---|---|---|---|

| FI | Financial Accounting | CO | Controlling |

| TR | Treasury Management | RE | Real Estate Management |

| EC | Enterprise Controlling | IM | Investment Management |

| SCM | Supply Chain Management | APO | Advanced Planning Optimization |

| MM | Material Management | LE | Logistics Execution |

| SD | Sales Distribution | CS | Customer Service |

| PP | Production Management | EHS | Environment Health and Safety |

| QM | Quality Management | LO | Logistics General |

| SRM | Supply Relationship Management | PM | Plant Management |

| PLM | Product Lifecycle Management | HR/HCM | Human Capital Management |

| ESS | Employee Self Service | MSS | Management Self Service |

| CRM | Customer Relationship Mgmt | FSCM | Financial Supply Chain Mgmt |

| GCR | Governance Risk Compliance | CPM | Corporate Performance Mgmt |

| PS | Project System | IS | Industry Specific |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Faccia, A.; Petratos, P. Blockchain, Enterprise Resource Planning (ERP) and Accounting Information Systems (AIS): Research on e-Procurement and System Integration. Appl. Sci. 2021, 11, 6792. https://doi.org/10.3390/app11156792

Faccia A, Petratos P. Blockchain, Enterprise Resource Planning (ERP) and Accounting Information Systems (AIS): Research on e-Procurement and System Integration. Applied Sciences. 2021; 11(15):6792. https://doi.org/10.3390/app11156792

Chicago/Turabian StyleFaccia, Alessio, and Pythagoras Petratos. 2021. "Blockchain, Enterprise Resource Planning (ERP) and Accounting Information Systems (AIS): Research on e-Procurement and System Integration" Applied Sciences 11, no. 15: 6792. https://doi.org/10.3390/app11156792

APA StyleFaccia, A., & Petratos, P. (2021). Blockchain, Enterprise Resource Planning (ERP) and Accounting Information Systems (AIS): Research on e-Procurement and System Integration. Applied Sciences, 11(15), 6792. https://doi.org/10.3390/app11156792