5.1.1. Level Effect of Single Factor

(1) Level effect of low-frequency variables

Table 3 and

Table 4 give the estimation results of the mixed model for the level value of a single factor.

reflects the level effect of each influencing factor on the long-term component of the high-frequency volatility, and

reflects the optimal estimation weight in the single-factor mixed level value model. The coefficients

examine the impact of the level of individual factors or the increase in the rate of return on the volatility of the crude oil market; that is, when

is positive and statistically significant, the increase of the factor will promote the Brent crude oil futures market fluctuation. When

is negative and statistically significant, the increase in this factor will reduce the volatility of the Brent crude oil futures market.

From the estimated results in

Table 3, we can see the following:

① From the point of view of H value: based on the level effect model of US crude oil inventory (Inventory) and Australia’s Newcastle port spot offshore price of thermal coal (Cspp), the H value is 0.0182 and 0.0155, respectively, which is closer to 1%. That is to say, the level effect model based on the above two variables is more stable. The H value of WTI crude oil noncommercial arbitrage holdings is the largest, and the estimation result is poor.

② From the perspective of BIC value, the BIC value of Inventory, GasSpotPrice, and Cspp models is the smallest. From the perspective of LLH (Log likelihood), the Inventory and GasSpotPrice models have the smallest LLH value, indicating that the Inventory and GasSpotPrice models have improved accuracy and simplicity.

From the results of coefficient estimation, we can see the following:

① The coefficients of US crude oil inventory (Inventory), OPEC crude oil production (OPEC), OECD crude oil consumption (OECD), and the Henry Hub natural gas spot price (GasSpotPrice) are statistically significant. The coefficients of the FOB spot price of thermal coal in Port Canius, Australia (Cspp) and WTI crude oil noncommercial arbitrage holdings (Wtioi) are not significant. The values of the US crude oil inventories, the OECD crude oil consumption, the natural gas spot prices, the spot price of thermal coal at the Port of Cannes, Australia, and the WTI crude oil noncommercial arbitrage positions are greater than zero, while the value of OPEC crude oil production is less than zero.

② The crude oil inventory coefficient is significantly greater than zero, and the US crude oil inventory level is positively correlated with the volatility of crude oil futures prices. Crude oil inventory is a part of the crude oil demand and the potential supply of crude oil next year. The higher its value, the higher the volatility of crude oil futures prices. Similarly, the OECD is the main demand representative of the crude oil market. The increase in OECD crude oil consumption will cause a significant increase in crude oil market volatility, which is consistent with economic theory.

③ As a kind of clean energy, natural gas has a wider scope of promotion. As one of the important substitutes for oil, the increase in natural gas prices is also one of the factors driving the fluctuation of crude oil prices. Similar to natural gas, coal is also an important substitute for oil. It has a positive impact on the fluctuation of crude oil prices. Due to coal’s substitution role for crude oil requires conditions, its advantage of replacing crude oil will not exist when the price of coal gradually increases. Therefore, it can be seen from the estimation results that the impact is not sufficiently significant, the coal price level has which on the fluctuation of crude oil prices in the long run.

④ Crude oil noncommercial arbitrage holdings represent speculative factors in the crude oil futures market. From the estimation results, the coefficient of Wtioi is greater than zero, but the statistics are not significant, indicating that speculative factors are not important factors for international oil price fluctuations for the global crude oil market.

⑤ Unlike others, the coefficient of OPEC crude oil production is less than zero and statistically significant, indicating that the increase in OPEC crude oil production will weaken the volatility of Brent crude oil futures. OPEC crude oil production, as the main supplier of the oil market, has a significant impact on price fluctuations in the international crude oil market. When the OPEC crude oil production value is high, the global crude oil market is adequately supplied, and international oil prices which has the effect of stabilizing oil prices will be more stable.

Based on the above analysis, in terms of horizontal effects, crude oil production, consumption, inventory, and natural gas prices are the main factors that have a major impact on the fluctuation of Brent crude oil futures prices after the financial crisis in addition to coal spot prices and speculative factors.

(2) Level effect analysis of high-frequency variables

In the process of selecting explanatory variables, in addition to considering low-frequency variables, the influence of high-frequency variables is also considered in order to increase the sufficiency of the explanation.

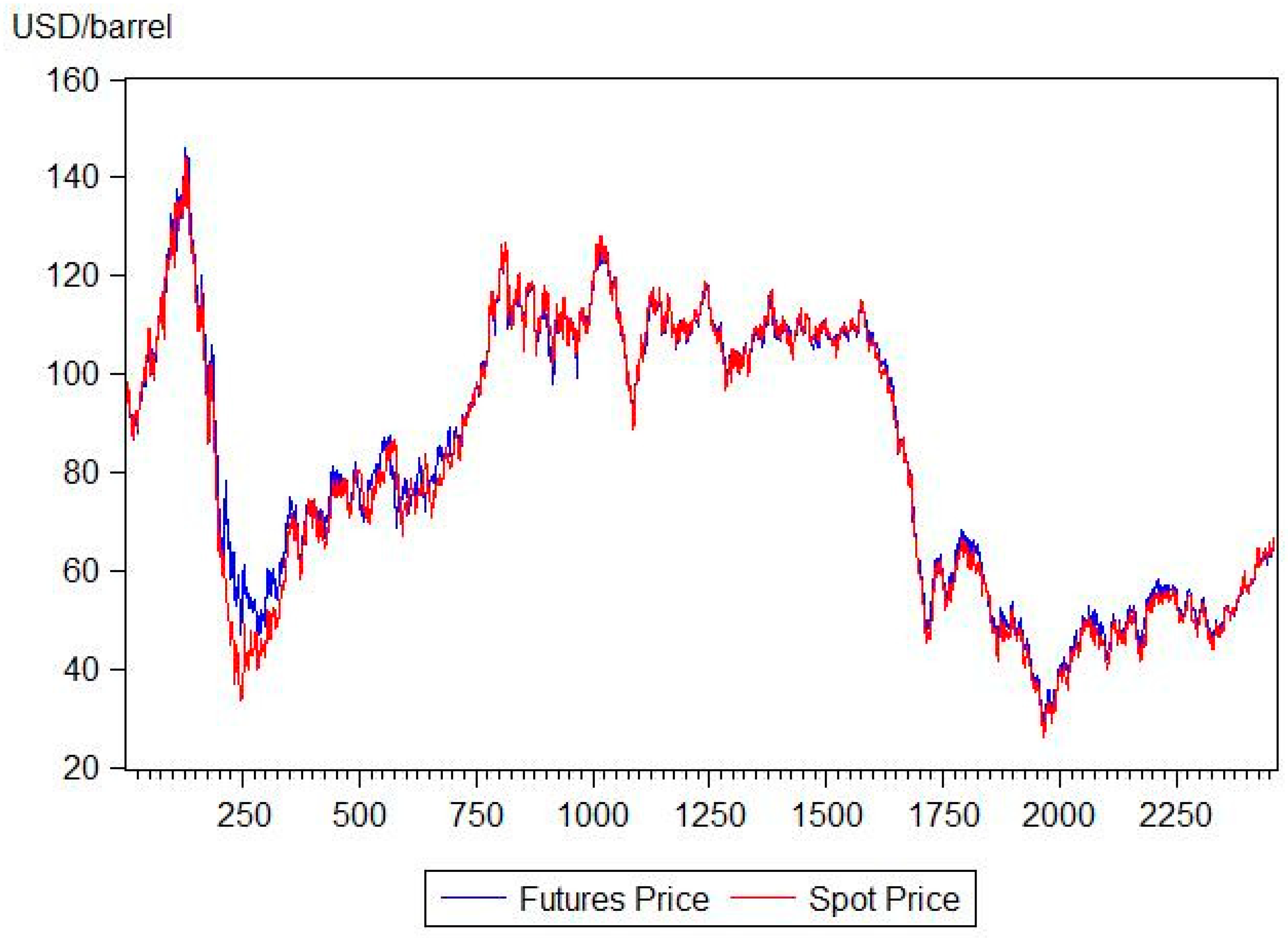

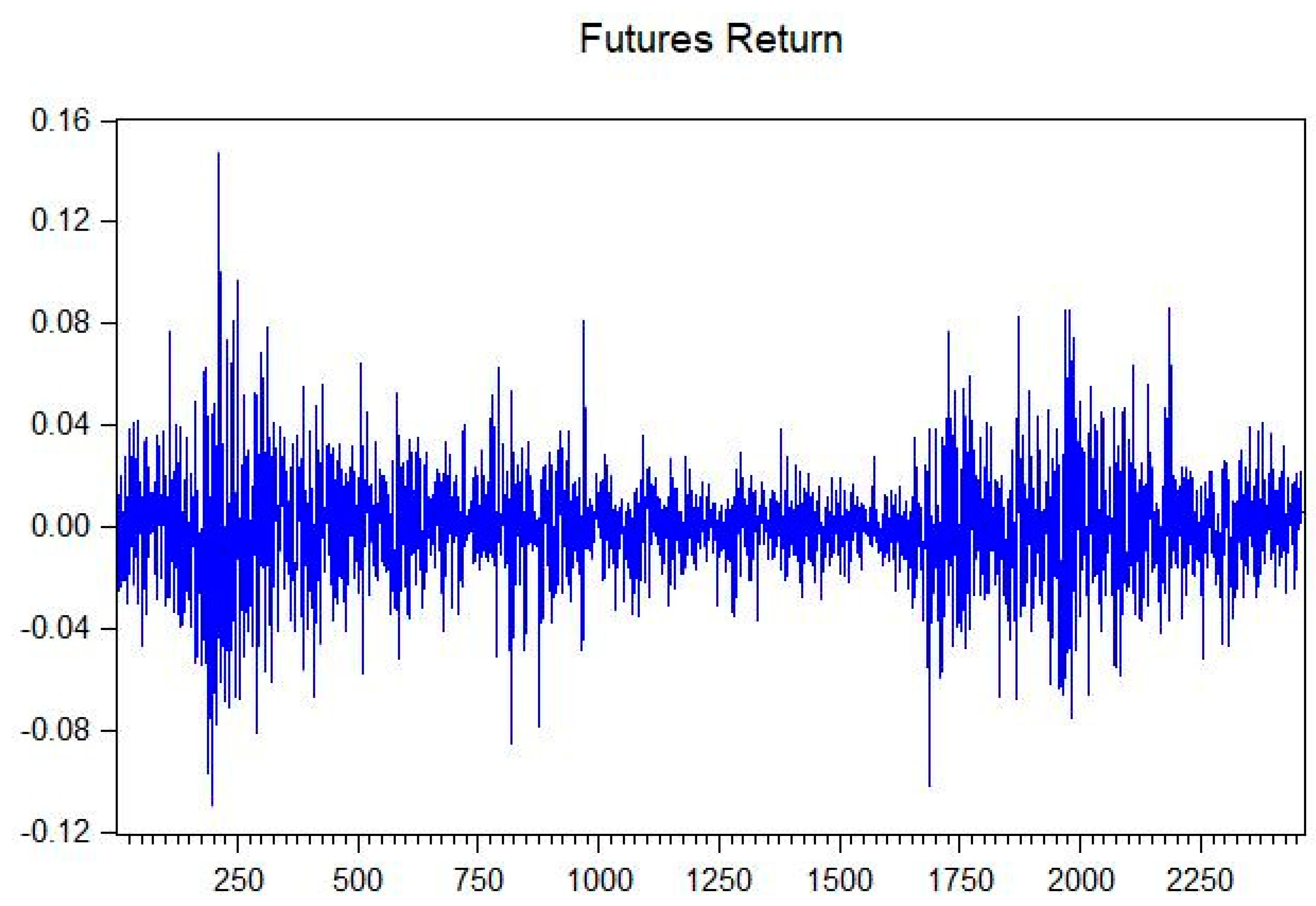

This article combines indicator correlation and data availability and selects five high-frequency variables including the closing price of the US dollar index (USD), Brent crude oil futures trading volume (10,000 lots), Brent crude oil futures open interest (short orders) (10,000 lots), Henry Hub Natural Gas Spot Price (Dollars per Million Btu), and Europe Brent Spot Price FOB (Dollars per Barrel) as explanatory variables. Among them, the US dollar index, Brent crude oil spot prices, and natural gas prices represent high-frequency factors outside the market; trading volume and open interest represent high-frequency factors on the market.

From the estimated results in

Table 4, we can see the following:

① From the point of view of H value: the H value of the Brent crude oil spot price (PS) model is the lowest, at 0.0111, and the H value of the natural gas price (GS) model is the highest, at 0.0195, while that of the Brent crude oil futures volume (V) and the dollar index (the H value of DI) and Brent crude oil futures’ open interest (OI) is 0.0188. Thus, the spot price model is relatively more stable, while the natural gas price model is the worst.

② Based on MAE and RMSE criteria, the estimation effect of each model is basically the same.

③ The BIC and LLH values of the Brent crude oil futures trading volume (V), US dollar index (DI), and Brent crude oil futures open interest (OI) are better than other variables.

Judging from the

coefficient estimation results in

Table 4, the following can be concluded:

① The values of the Brent crude oil futures trading volume and Brent crude oil spot price is statistically significant. Other statistics such as the Brent crude oil futures open interest, the US dollar index, and the natural gas daily price are not statistically significant. The values of the spot price, the open interest, and the dollar index are negative, and the values of the other two high-frequency factors are positive.

② Trading volume is a high-frequency factor in the field affecting the market, reflecting market liquidity and trading activity. The trading volume coefficient is greater than zero and statistically significant, indicating that the trading volume on the market is an important factor affecting price fluctuations. However, when the daily trading volume is high, the volatility of Brent crude oil futures prices becomes stronger, and vice versa. Unlike trading volume, Brent crude oil futures open interest has a nonsignificant negative effect on the volatility of Brent crude oil futures. This is consistent with the results of the same frequency analysis. Different from the securities market, open interest is a statistical quantity unique to the futures market, reflecting the flow of funds on and off the market. An increase in open interest indicates that funds have entered the market, and a decrease in open interest indicates that funds have flowed out of the market. At the same time, there is a complicated correspondence between trading volume and open interest. The higher the open interest, the larger the market capital, and the weaker the relative market volatility.

③ The value of natural gas price is greater than zero, but it is not statistically significant. The analysis result of the daily price level effect of natural gas is similar to the analysis result of the monthly low-frequency data of natural gas, and both are nonsignificant positive relationships.

④ The value of the US dollar exchange rate is less than zero. The US dollar exchange rate represents the price of the US dollar. As a unit of calculation of crude oil futures, it has a certain impact on the price of crude oil. From the estimation results, when the exchange rate of the US dollar decreases, the volatility of oil prices increases as the marked price is only the nominal price of the crude oil, while the actual value of crude oil remains unchanged. When the value of the US dollar decreases, the price of crude oil will increase. When the price of the US dollar increases, the price unit of crude oil will decrease, so it has the effect of stabilizing oil prices.

⑤ The Brent futures price is representative of the expected Brent spot price, and the spot price is the basis of the futures price. Based on the estimation results, the Brent crude oil spot price income has a significant negative effect on the futures price fluctuation; that is, the spot price is negatively correlated to the volatility of the futures market, especially when the spot price is high, the futures price will also be high, and the relative volatility will be weaker.

Therefore, from the analysis results of high-frequency factors, the trading volume in the high-frequency factors on the market and the spot price in the high-frequency factors outside the market have a significant explanatory effect on the price volatility of the Brent crude oil futures market.

In addition, based on the estimation results in

Table 3 and

Table 4, the Brent crude oil futures market has a strong GARCH effect. Various GARCH-MIDAS models reflect the adaptability of the mixed level model in describing the fluctuations of the Brent crude oil futures market.

5.1.2. Single Factor Volatility Effect

Table 5 and

Table 6 are the estimation results of the volatility effect of low-frequency and high-frequency variables, respectively. The coefficients

in each equation examine the volatility of a single factor or the impact of increased volatility on the volatility of the crude oil futures market; that is, when

is positive and statistically significant, the increase in the volatility of this factor will promote the volatility of the crude oil futures market. When

is negative and statistically significant, the increase in the volatility of this factor will reduce the volatility of the crude oil futures market.

(1) Analysis of volatility effects of low-frequency variables

The volatility effects of low-frequency variables are estimated as shown in

Table 5.

From the estimated results in

Table 5, we can see the following:

① The α + β values of each model are very close to 1, indicating that each model has a relatively strong ARCH effect and volatility persistence.

② In terms of BIC and LLH standards, except for the volatility effect model of the spot offshore price of thermal coal (Cspp) in the Port of Cannes, Australia, the comparison results of other models are relatively consistent. Relatively speaking, the estimated accuracy of the OPEC, OECD, and Wtioi models is slightly higher. Regarding the H value, the estimation accuracy of the thermal coal spot offshore price (Cspp) model of Canusl Port, Australia, is slightly higher, followed by the Inventory, OPEC, and OECD volatility effect models, while the H value of WTI crude oil noncommercial arbitrage holdings is the largest, and the estimation result is poor. There is almost no difference in the MAE and RMSE values of each model.

③ In addition, the volatility effect model of low-frequency factors is compared with the level effect model of low-frequency factors: Although the corresponding models have advantages and disadvantages from the criteria of BIC, LLH, H, MAE, and RMSE, the volatility model generally outperforms the level effect model. Based on the average value of each indicator of the five models, the BIC, LLH, H, MAE, and RMSE values of the horizontal effect model are −7.0128, −4967.73, 0.0188, 0.0005, and 0.0008, and the five types of indicator values of the volatility effect model are −7.0268, −5217.56, 0.0187, 0.0005, and 0.0008, so overall the volatility effect model slightly outperforms the horizontal effect model.

④ The coefficient estimation values of all low-frequency factors are greater than zero, indicating that the volatility of the six low-frequency factors is positively correlated with the volatility of Brent crude oil futures returns, but the values of the coal spot price and natural gas spot price model are not statistically significant.

⑤ The increase in the volatility of crude oil inventories, crude oil consumption, crude oil production, substitute prices, and speculative factors will increase the volatility of the Brent crude oil futures market. Relatively speaking, the impact of substitutes is not sufficiently obvious.

(2) Analysis of volatility effects of high-frequency variables

The volatility effects of high-frequency variables are estimated as shown in

Table 6.

From the estimated results in

Table 6, we can see the following:

① Similar to the low-frequency variable volatility effect model, the α + β value of each model of the high-frequency variable volatility effect is very close to 1, indicating that each model has a relatively strong ARCH effect and relatively strong volatility persistence. In addition, the H value of the trading volume and natural gas price fluctuation effect model is 0.0173, the H value of the open interest and the dollar index fluctuation effect model is slightly higher, and the value of the spot price fluctuation effect model is the largest. Regarding LLH, the natural gas price model has the highest accuracy, but its BIC value is the largest, so from these two standards, the evaluation results are inconsistent, indicating that the stability of this model is poor. The MAE and RMSE values of each model have almost no difference.

② In addition, based on the comparison between the high-frequency factors volatility effect model and the high-frequency factors horizontal effect model, although the corresponding models have advantages and disadvantages based on the BIC, LLH, and H criteria, the volatility model generally outperforms the level effects model. From the average value of the indicators of the five models, the BIC, LLH, and H values of the horizontal effect model are −7.0226, −5280.11, and 0.0174, and the five types of indicators of the volatility effect model are −7.0230, −5333.10, and 0.0177, respectively. Therefore, in general, the volatility effect model of high-frequency factors slightly outperforms the horizontal effect model.

③ Judging from the parameter values of various variables, whether it is the high-frequency factors on the market or the high-frequency factors outside the market, all the coefficients are greater than zero, indicating that the increase in volatility will increase the volatility of Brent crude oil futures prices. Judging from the significance of the coefficients of each variable, the coefficients of the next three factors are statistically significant, except for the position volume and the dollar index. This shows that the volatility of high-frequency factors is also an important factor affecting the volatility of Brent crude oil futures.

{kind=link}

{kind=link}