1. Introduction

Organizations routinely seek to improve their performance by serving customers more effectively and thus improving profitability. However, in endeavouring to realize greater profits, organizations may take only a few factors into account or may engage in change-management processes that purport to be comprehensive but are limited in scope. In the present study, the focus is on investigating the potential of the balanced scorecard (BSC) approach to describing organizational performance and discovering opportunities for meaningful, effective change that encompasses multiple organizational functions and concerns.

The study focus is a logistics industry organization, a national postal service, in Saudi Arabia selected as an instructive example in light of Saudi Arabia’s relatively recent efforts to reduce its economic dependence on oil. In this context, Vision 2030, announced in 2016, includes a strategic focus on exploiting the country’s geographical location. As a result, the Saudi logistics sector has become critically important to decision makers and the government has introduced multiple plans to advance this sector. In particular, given that the infrastructure of Saudi Arabia is generally held to be insufficient such that the challenge of transforming it has yet to be met, the development and implementation of a sound and feasible strategic plan to improve the logistics industry is viewed as the backbone of Vision 2030. For this reason, the government’s plans focus on strengthening the logistic competencies of agencies in this sector. It is in this context that the research presented herein was conducted.

The study focuses on two related questions explored through several hypotheses. How and to what extent can all four of the perspectives—learning and growth, internal business process, customer, financial performance—comprising the BSC approach be used to advance organizational performance? What are the relationships between these perspectives and can considering them in a holistic way be beneficial to business outcomes?

One of the most well-known tools used in strategic management is the balanced scorecard (BSC) introduced by

Kaplan and Norton (

1992). In fact, the BSC has gained recognition in both academia and industry. Many organizations, for profit, non-profit and public-sector, have embraced the BSC concept as constituting an effective method within an overall strategic management system and, therefore, as a way to improve performance. There is no doubt that the BSC can be used to transform the business strategies of any organization into initiatives with manageable objectives that can be measured using key performance indicators (KPIs)—including by focusing simultaneously on the financial perspective and multiple non-financial perspectives (i.e., the customer, internal business process and learning and growth perspectives).

Kaplan and Norton (

1996,

2001) suggest that the unique structure of the BSC means that it can be used as a strategic tool to guide organizations toward achieving sustained long-term profitability. Further,

Kaplan (

2012) noted that the BSC model can provide rich information about any organization type including in regard to determining the perspectives most appropriate to a given organization. Another concept associated with the BSC is the strategy map (

Kaplan and Norton 2004b), a visual framework that prescribes several cause-and-effect relationships between various aspects of an organization’s strategy in concert with the integration of BSC perspectives. Strategy maps are used to foster employees’ understanding of their organization’s strategies and on this basis to involve the entire organization in pursuing and supporting the organization strategically. Many researchers (

Banker et al. 2011;

Cheng and Humphreys 2012) have indicated that the use of strategy maps enables employees to understand how with their organization’s objectives is linked to organizational strategy.

Many studies focus mainly on assessing the implications of using a strategy map to assist managers in more effectively set strategic objectives and/or to identify the measures in the strategy map on which managers should focus. However, there is only limited research on testing the causal links in the BSC strategy map and the interdependence between these perspectives.

Thakkar et al. (

2006) and

Wu (

2012) explored several interrelationships between BSC perspectives and showed that feedback relationships exist among them.

In the present study, all the causal relationships (both direct and indirect) within the BSC perspective are investigated in order to help managers further their understanding of how these perspectives are connected and whether a feedback relationship is in operation, as suggested by

Thakkar et al. (

2006) and

Wu (

2012). Factor analysis is used to determine the reliability of the instrument used herein and structural equation modelling (SEM) is used to determine the significance of the paths in the BSC strategy map. The focal example investigated is the Saudi Postal Corporation, an organization in the logistics industry that depends on efficient operations to handle postal services in Saudi Arabia.

The importance of this study lies in the fact that understanding all the direct and indirect causal relationships between the BSC perspectives has the potential to deepen the field’s understanding of how these perspectives relate to each other. On this basis, paths to improved operations within organizations can be identified and pursued in a coordinated way instead of with a focus on only one or a few perspectives.

The rest of the paper proceeds as follows: In

Section 2, an account of the theoretical background and the development of the hypotheses is presented. In

Section 3, the research methodology, including the data collection and participants, are discussed along with variable measures. The focus of

Section 4 is the main findings, including the reliability measures of the instrument used and the results of the structural model. Concluding remarks and a discussion of the practical implications of the results are presented in

Section 5.

3. Research Methodology

3.1. Data Collection and Participants

One of the oldest service institutions in Saudi Arabia, the Saudi Postal Corporation both provides and regulates the country’s postal service. The postal service in Saudi has gone through significant development in recent years. In particular, in June 2002, the Saudi Postal Corporation became a public institution, operating in accordance with the philosophy of the private sector. With this transformation, the Saudi Postal Corporation opened a postal processing centre in every region of Saudi Arabia with three main centres in Riyadh, Jeddah and Dammam.

One of these three main centres, the Jeddah Post Processing Centre specializes in handling registered mail, consignments, e-commerce shipments and other mail to which the conditions of registered mail apply. This type of mail has a tracking number that the customer can use to follow a given piece of mail as it makes its way through Saudi Post locations to his/her door at a price that is competitive with the cost of other private carriers in the country for a similar service. The centre has eleven departments, including administrative departments and field sections, as well as a technical section focused on maintaining the postal machinery. As of 2018, the Jeddah Treatment Centre employed a total of 201 people.

In summer 2018, to collect data for the present study, a questionnaire was distributed to all the employees at the Jeddah Treatment Centre and 101 complete questionnaires were returned. The respondents represent a diverse sample in terms of educational level, work experience and age. As shown in

Table 1, most of the respondents were older than 35 years of age (70.6%), held a diploma or a bachelor’s degree (52.5%) as their highest level of formal educational attainment and had more than 20 years’ work experience (47.5%).

3.2. Variables Measures

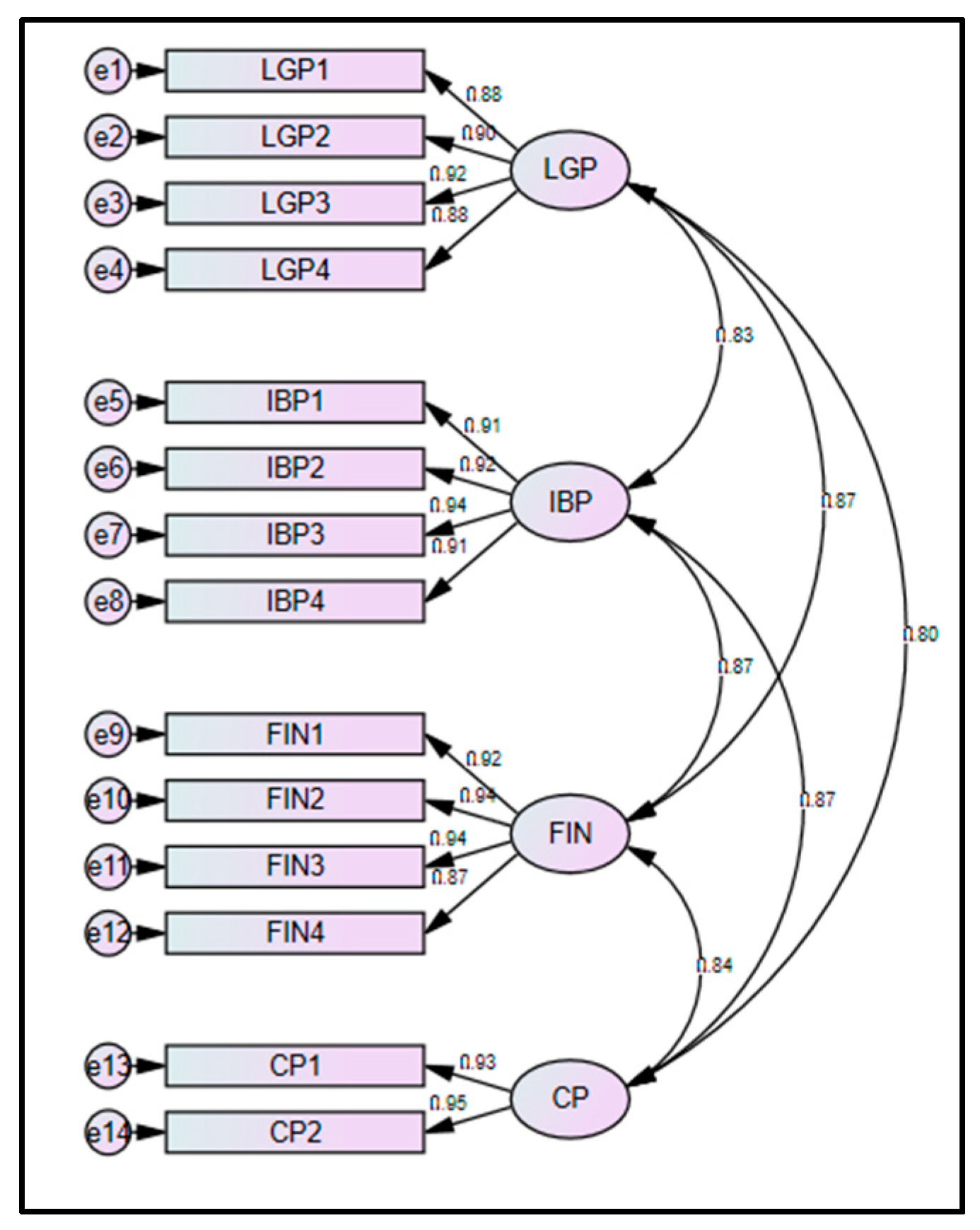

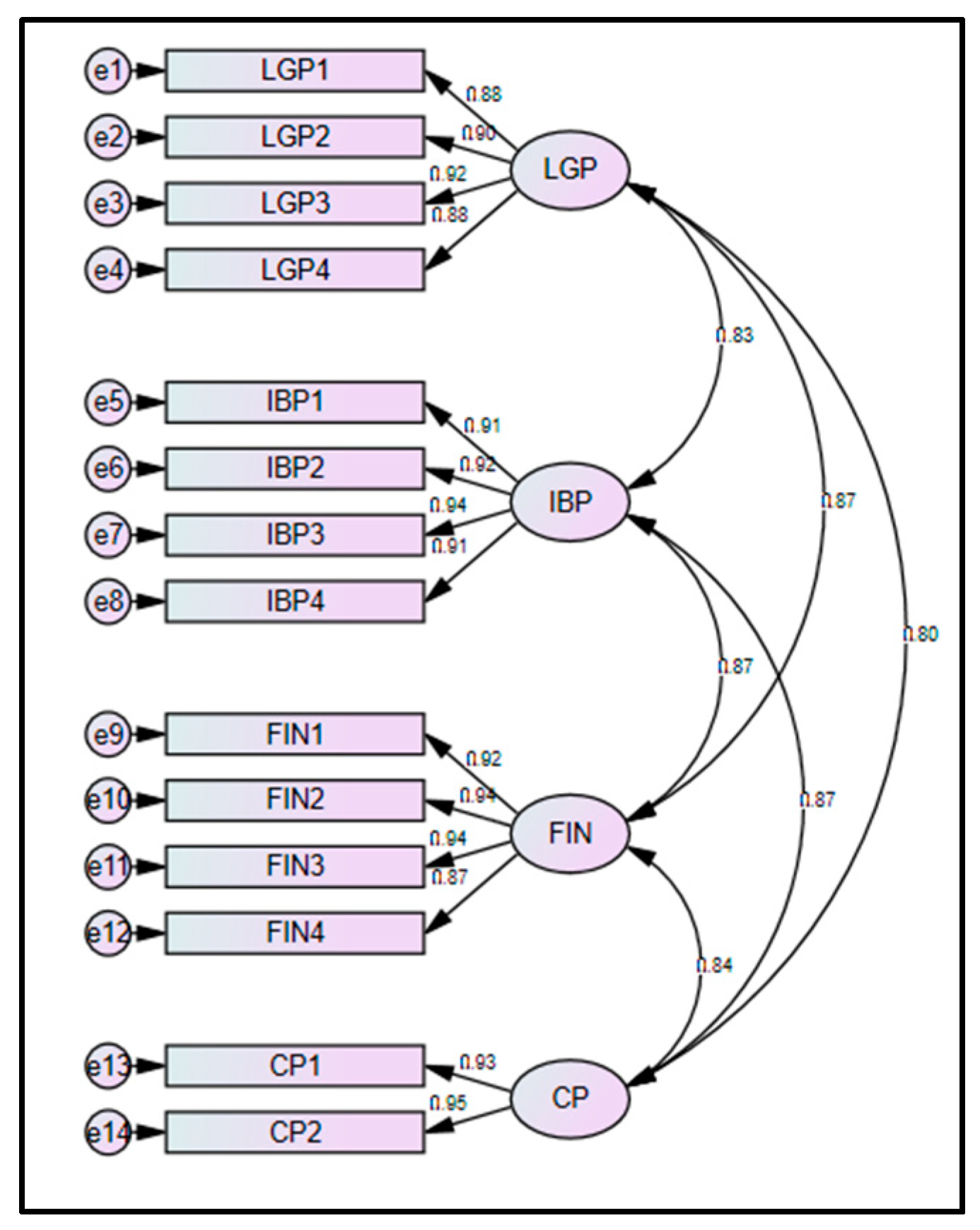

The measures used in this study are based on

Kaplan and Norton’s (

1992) BSC model. In the logistics industry, researchers typically develop performance indicators based on the context of the focal companies.

Kucukaltan et al. (

2016) surveyed previous research carried out in the logistics industry and used the Analytic Network Process (ANP) method to prioritize the key indicators in each perspective, in which they identified the most important indicators for each of the four perspectives of the BSC in the logistic industry. As such, the survey employed in this study is from

Kucukaltan et al. (

2016), although adapted to the context of the Saudi postal service. The survey was organized into four sections: the learning and growth perspective (4 items), the internal business process perspective (4 items), the customer perspective (2 items) and the financial performance perspective (4 items). The questionnaire was translated from English into Arabic and the back translation method was used to ensure that the English and Arabic version of the survey agreed. The indicators and their descriptions are provided in the

Appendix A. The respondents were asked to review the following measures using a five-point Likert scale whereby 1 = “strongly disagree” and 5 = “strongly agree”.

The learning and growth (LGB) perspective includes employee training and development with a corporate focus on staff self-development. In their model, Kaplan and Norton emphasize that “learning” encompasses not only training but also mentoring provided to employees. The LGB perspective is also considered the intangible drivers of performance and can be further classified into three components: (1) human capital, which consists of the employees’ skills, talents and knowledge; (2) information capital, which consists of databases, information systems, networks and technology infrastructure; and (3) organization capital, which consists of culture, leadership, employee alignment, teamwork and knowledge management (

Kaplan and Norton 2004a).

The internal business process (IBP) perspective is focused on how well an organization is running its operations in terms of efficiency, waste management, operations cycle time and throughput speed. In this perspective, organizations should excel in key areas expected to provide the organization with value while looking for ways to improve their processes, quality and capacity.

The customer perspective (CP) is focused on objectives related to customers and markets. The CP should measure (1) the value proposition, that is, the value delivered to customers, which includes improving service performance, reducing waiting times and improving service quality and thereby improving customer satisfaction and (2) the value proposition, that is, the outcome of those activities, which includes improving customer satisfaction and building brand awareness.

The financial performance (FIN) perspective is related to the organization’s financial status and performance as a result of implementing given strategies. The FIN is viewed as the tangible outcome of the different stages in which an organization implements its strategy.

Kaplan and Norton (

1996) referred to these stages as rapid growth, sustain and harvest and each can be identified in reference to its own set of financial objectives. In the rapid-growth stage, organizations measure sales volume and growth revenue; in the sustain stage, the focus is managing operations cost and return on capital; and in the harvest stage, the focus is cash flow analysis measures.

5. Conclusions

In this study, the effects of the BSC perspectives on the performance measures of the Saudi postal service were examined. The proposed model goes beyond the generic strategic map to account for the causal relationships and tests other relationships between the BSC perspectives, including direct and indirect effects.

The CFA results confirmed the convergent and discriminant validity of the instrument used herein. Further, the SEM analysis confirmed the generic causal relationships between the BSC perspectives in a strategy map (Hypotheses 1, 2 and 3). In addition, the SEM analysis showed that the learning and growth perspective has a direct effect on customer perspective, which is significantly mediated through the internal business process such that Hypothesis 4a is supported. Another interesting relationship is that the internal business process perspective also has a direct effect on the financial performance perspective and this link is mediated through the customer perspective, thereby providing support to Hypothesis 4b.

Based on the analysis, the study confirmed that mediating effects are integral to strategy maps and that the direct and indirect effects could potentially provide a deeper understanding of how these perspectives are linked to one another. Unlike other studies (

Pérez et al. 2017;

Valmohammadi and Sofiyabadi 2015;

Wu 2012), which focus on giving weight to perspectives or highlighting the most important perspective in a strategy map, this study shows that organizations should not ignore any of the causal relationships between the four perspectives.

Based on the study results, it is evident that the implications of strategy maps with clearly established causal links can easily be grasped by employees such that they gain a better understanding of their organization’s strategy. Many researchers have highlighted the importance of assigning appropriate weight to each of the BSC perspectives in order to prioritize them appropriately. However, only a few studies include a consideration of the causal relationships between these perspectives. Given that this is the case, in the present study, these causal relationships are explored using SEM and the mediating effects between these perspectives are also considered.

As this study relies on an instrument designed to assess the main indicators in each perspective of the BSC in the logistics industry based on the work of

Kucukaltan et al. (

2016), the results can be generalized to service providers in the logistics sector. From a managerial perspective, the results presented confirmed the existence of interrelationship between the BSC perspectives in the logistics industry. Thus, organizations should focus on the leading indicators to improve their financial outcomes. In addition, managers in this sector should draw more attention to intangible drivers of performance such as keeping pace with technological changes in the work environment and offering training programs to ensure that their employees have up-to-date skills and knowledge. Those activities will equip their employees with the skills and competencies needed to advance the business enterprise.

Another important managerial implication here is that organizations in other sectors should also look at these perspectives in a holistic way and identify and investigate all possible paths (direct and/or indirect) to improving the service they render. On this basis, managers can guide the organization toward taking the right steps to improve organizational performance in regard to all the BSC perspectives instead of devoting organizational resources to only one of these.

It is worth noting that the results of this paper apply only to the focal organization, that is, the Saudi Postal Corporation. Given that each organization is considered unique in terms of its strategy and measures, the findings of this paper should not be generalized. Further research should explore and document causal relationships in other types of organizations across all industry sectors.

Another limitation of the present study is that the data were measured subjectively using a questionnaire, which has inherent shortcomings, as is the case for all such instruments and the studies based on them. Therefore, it would be beneficial if researchers in this field were to consider different ways to assess these indicators. Examples in this regard could be collecting the number of customer complaints as an indicator of customer satisfaction or determining the number of training programs offered and the percentage of employees who attended them as a measure for well-trained employees.

{kind=link}