Fintech: Evidence of the Urgent Need to Improve Financial Literacy in Portugal

Abstract

1. Introduction

- What is the level of knowledge and use of Fintech in Portugal?

- What do customers perceive to be the degree of security of Fintech?

- What do customers assess the regulation and supervision of traditional banking and Fintech to be?

2. Literature Review

2.1. Financial Innovation

2.2. Fintech

2.3. Use of Fintech

2.4. Security

2.5. COVID-19

2.6. Regulation and Supervision

3. Methods

3.1. Data Collection Procedure

3.2. Participants

3.3. Data Analysis Procedure

3.4. Instrument

4. Results

4.1. Descriptive Analysis of the Variables under Study

4.2. Independence Tests

4.3. Hypothesis Testing

5. Discussion

Limitations and Future Suggestions

6. Conclusions and Contributions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abu Daqar, Mohannad A. M., Samer Arqawi, and Sharif Abu Karsh. 2020. Fintech in the eyes of Millennials and Generation Z (the financial behavior and Fintech perception). Banks and Bank Systems 15: 20–28. [Google Scholar] [CrossRef]

- Andersson, Pedro, Flávio Valente, and Catarina Coutinho. 2024. No poupar está o ganho: Saiba como os seus filhos podem aprender a gerir o dinheiro desde cedo. Sic Notícias. Available online: https://sicnoticias.pt/video/2024-04-10-No-poupar-esta-o-ganho-saiba-como-os-seus-filhos-podem-aprender-a-gerir-o-dinheiro-desde-cedo-cc1eb411 (accessed on 16 April 2024).

- Anshari, Muhammad, Munirah Ajeerah Arine, Norzaidah Nurhidayah, Hidayatul Aziyah, and Md Hasnol Alwee Salleh. 2021. Factors influencing individual in adopting eWallet. Journal of Financial Services Marketing 26: 10–23. [Google Scholar] [CrossRef]

- Boot, Arnoud, Peter Hoffmann, Luc Laeven, and Lev Ratnovski. 2021. Fintech: What’s old, what’s new? Journal of Financial Stability 53: 100836. [Google Scholar] [CrossRef]

- Cahete, Jessica Nazarina Miguel. 2020. Traditional Banking at Digital Age. Are They Keeping up with Changes in Consumer Behaviour? Millenials’ Perception in the Portuguese Market. Master’s thesis, Repositório Institucional do Iscte, Lisbon, Portugal. Available online: https://repositorio.iscte-iul.pt/handle/10071/22349 (accessed on 16 April 2024).

- Chen, Sharon, Sebastian Doerr, Jon Frost, Leonardo Gambacorta, and Hyun Song Shin. 2023. The fintech gender gap. Journal of Financial Intermediation 54: 101026. [Google Scholar] [CrossRef]

- Chorzempa, Martin, and Yiping Huang. 2022. Chinese Fintech Innovation and Regulation. Asian Economic Policy Review 17: 274–92. [Google Scholar] [CrossRef]

- Decreto-Lei n.º 139/2012, de 5 de julho. 2012. Diário da República n.º 129/2012, Série I de 2012-07-05. Available online: https://diariodarepublica.pt/dr/detalhe/decreto-lei/139-2012-178548 (accessed on 16 April 2024).

- Del Sarto, Nicola, Lorenzo Gai, and Federica Ielasi. 2023. Financial Innovation: The Impact of Blockchain Technologies on Financial Intermediaries. Journal of Financial Management, Markets and Institutions 1: 1–21. [Google Scholar] [CrossRef]

- Dias, António, Arnaldo Oliveira, Cristina Pereira, Maria Teresa Abreu, Paulo Alves, Rita Basto, Rosália Silva, and Susana Narciso. 2013. Referencial de Educação Financeira para a Educação Pré-Escolar, o Ensiono Básico, o Ensino Secundário e a Educação e Formação de Adultos. Ministério da Educação e Ciência. Available online: https://www.dge.mec.pt/sites/default/files/ficheiros/referencial_de_educacao_financeira_final_versao_port.pdf (accessed on 16 April 2024).

- Duarte, Susana Catarina Alves. 2019. Tendências Futuras do Setor Bancário. O Ajustamento da Banca Tradicional às Novas Tecnologias e a Banca Nativa Digital. Master’s thesis, Repositório Institucional da Lisbon School of Economics and Management, Lisbon, Portugal. Available online: https://www.repository.utl.pt/handle/10400.5/19198 (accessed on 22 April 2023).

- Eichengreen, Barry. 2023. Financial regulation in the age of the platform economy. Journal of Banking Regulation 24: 40–50. [Google Scholar] [CrossRef]

- Fabris, Nikola. 2022. Impact of COVID-19 pandemic on financial innovation, cashless society, and cyber risk. Economics 10: 73–86. [Google Scholar] [CrossRef]

- Faria, Natália. 2023. Portugal está a envelhecer a um ritmo mais acelerado do que restantes países europeus. Público. Available online: https://www.publico.pt/2023/02/22/sociedade/noticia/populacao-portugal-envelhecer-ue-revela-eurostat-2039817 (accessed on 16 April 2024).

- Fernandes, Carlos Canhoto. 2019. O desafio da Banca face às Fintech. Master’s thesis, Repositório Institucional do Iscte, Lisbon, Portugal. Available online: https://iscte-iul.pt/tese/9451 (accessed on 22 September 2023).

- Galazova, S. S., and Leyla R. Magomaeva. 2019. The transformation of traditional banking activity in digital. International Journal of Economics and Business Administration 7: 41–51. [Google Scholar] [CrossRef]

- Gąsiorkiewicz, Lech, Jan Monkiewicz, and Marek Monkiewicz. 2020. Technology-driven innovations in financial services: The rise of alternative finance. Foundations of Management 12: 137–50. [Google Scholar] [CrossRef]

- Gopal, Sanghmitra, Priyanka Gupta, and Amrisha Minocha. 2023. Advancements in Fin-Tech and Security Challenges of Banking Industry. Paper presented at 2023 4th International Conference on Intelligent Engineering and Management (ICIEM), London, UK, May 9–11. [Google Scholar]

- Haddad, Christian, and Lars Hornuf. 2019. The emergence of the global Fintech Market: Economic and Technological Determinants. Small Business Economics 53: 81–105. [Google Scholar] [CrossRef]

- Hasan, Morshadul, Thuhid Noor, Jiechao Gao, Muhammad Usman, and Mohammad Zoynul Abedin. 2023. Rural Consumers’ Financial Literacy and Access to Fintech Services. Journal of the Knowledge Economy 14: 780–804. [Google Scholar] [CrossRef]

- Hesekova Bojmirova, Simona. 2022. FinTech and Regulatory Sandbox—New challenges for the financial market. The case of the Slovak Republic. Juridical Tribune 12: 399–411. [Google Scholar] [CrossRef]

- Jones, Ryan, and Pinar Ozcan. 2021. Rise of BigTech Platforms in Banking. Oxford: University of Oxford. Available online: https://www.sbs.ox.ac.uk/sites/default/files/2023-02/sustainability-report-2021-22.pdf (accessed on 22 September 2023).

- Jornal de Notícias. 2024. Portugueses são os segundos piores da UE em literacia financeira. Available online: https://www.jn.pt/7598372527/portugueses-sao-os-segundos-piores-da-ue-em-literacia-financeira/ (accessed on 16 April 2024).

- Jünger, Moritz, and Mark Mietzner. 2020. Banking goes digital: The adoption of Fintech services by German households. Finance Research Letters 34: 101260. [Google Scholar] [CrossRef]

- Lee, In, and Young Jae Shin. 2018. Fintech: Ecosystem, business models, investment decisions, and challenges. Business Horizons 61: 35–46. [Google Scholar] [CrossRef]

- Li, Gang, Ehsan Elahi, and Liangliang Zhao. 2022. Fintech, Bank Risk-Taking, and Risk-Warning for Commercial Banks in the Era of Digital Technology. Frontiers in Psychology 13: 934053. [Google Scholar] [CrossRef]

- Martincevic, Ivana, Sandra Črnjević, and Igor Klopotan. 2022. Novelties and benefits of fintech in the financial industry. International Journal of E-Services and Mobile Applications 14: 25. [Google Scholar] [CrossRef]

- Mills, Karen, and Brayden McCarthy. 2017. How Banks Can Compete Against an Army of Fintech Startups. Harvard Business Review. April 26. Available online: https://hbr.org/2017/04/how-banks-can-compete-against-an-army-of-fintech-startups (accessed on 20 September 2023).

- Moreira-Santos, Diana, Manuel Au-Yong-Oliveira, and Ana Palma-Moreira. 2022. Fintech Services and the Drivers of Their Implementation in Small and Medium Enterprises. Information 13: 409. [Google Scholar] [CrossRef]

- Moro-Visconti, Roberto, Salvador Cruz Rambaud, and Joaquin Lopez Pascual. 2020. Sustainability in Fintechs: An explanation through business model scalability and market valuation. Sustainability 12: 10316. [Google Scholar] [CrossRef]

- Nejad, Mohammad G. 2022. Research on financial innovations: An interdisciplinary review. International Journal of Bank Marketing 40: 578–612. [Google Scholar] [CrossRef]

- Paulsen, Carl. 2024. Fintech in Europe: A Comprehensive Overview. Eurodev. Available online: https://www.eurodev.com/blog/fintech-in-europe (accessed on 16 April 2024).

- Peráček, Tomáš. 2021. A few remarks on the (im)perfection of the term securities: A theoretical study. Juridical Tribune-Tribuna Juridica 11: 135–49. [Google Scholar] [CrossRef]

- Público. 2022. Portugal fica em último lugar no ranking de literacia financeira da zona euro. Available online: https://www.publico.pt/2022/01/13/economia/noticia/portugal-fica-ultimo-lugar-ranking-literacia-financeira-zona-euro-1991766 (accessed on 5 June 2023).

- Ramlall, Indranarain. 2018. Fintech and the Financial Stability Board. In Understanding Financial Stability (The Theory and Practice of Financial Stability, Vol. 1). Bingley: Emerald Publishing Limited. [Google Scholar] [CrossRef]

- Ringe, Wolf-Georg, and Christopher Ruof. 2020. Regulating fintech in the EU: The case for a guided sandbox. European Journal of Risk Regulation 11: 604–29. [Google Scholar] [CrossRef]

- Sarabando, Paula, Rogério Matias, Pedro Vasconcelos, and Tiago Miguel. 2023. Financial literacy of Portuguese undergraduate students in polytechnics: Does the area of the course influence financial literacy? Journal of Economic Analysis 2: 96–113. [Google Scholar] [CrossRef]

- Saunders, Mark N. K., Philip Lewis, and Adrian Thornhill. 2019. Research Methods for Business Students, 8th ed. New York: Pearson. [Google Scholar]

- Schueffel, Patrick. 2016. Taming the Beast: A Scientific Definition of Fintech. Journal of Innovation Management 4: 32–54. [Google Scholar] [CrossRef]

- Taujanskaitė, Kamilė, and Jurgita Kuizinaitė. 2022. Development of fintech business in Lithuania: Driving factors and future scenarios. Business, Management and Economics Engineering 20: 96–118. [Google Scholar] [CrossRef]

- Tilman, Leo M. 2020. The Imperative of Financial Innovation. Harvard Business Review. June 1. Available online: https://hbr.org/2010/06/the-imperative-of-financial-in (accessed on 24 September 2023).

- Tripathi, Sabyasachi, and Meenakshi Rajeev. 2023. Gender-Inclusive Development through Fintech: Studying Gender-Based Digital Financial Inclusion in a Cross-Country Setting. Sustainability 15: 10253. [Google Scholar] [CrossRef]

- Vardomatskya, Ludmila, valentina Kuznetsova, and Vladimir Plotnikov. 2021. The financial technologies transformation in the digital economy. E3S Web of Conferences 244: 10046. [Google Scholar] [CrossRef]

- Versal, Nataliia, Vasyl Erastov, Marija Balytska, and Ihor Honchar. 2022. Digitalization index: Case for banking System. Statistika 102: 426–42. [Google Scholar] [CrossRef]

- Vučinić, Milena. 2020. Fintech and financial stability potential influence of FinTech on financial stability, risks and benefits. Journal of Central Banking Theory and Practice 9: 43–66. [Google Scholar] [CrossRef]

- Wang, Xiaoying, Ramla Sadiq, Tahseen Mohsan Khan, and Rong Wang. 2021. Industry 4.0 and intellectual capital in the age of Fintech. Technological Forecasting and Social Change 166: 120598. [Google Scholar] [CrossRef]

- Zhou, Gideon, and Alouis Madhikeni. 2013. Systems, Processes and Challenges of Public Revenue Collection in Zimbabwe. American International Journal of Contemporary Research 3: 49–60. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Frequency | Percentage | |

|---|---|---|---|

| Gender | Female | 136 | 72.2% |

| Male | 38 | 21.8% | |

| Age | Between 18 and 30 years | 67 | 38.5% |

| Between 31 and 40 years | 30 | 17.2% | |

| Between 41 and 50 years | 45 | 25.9% | |

| 51 Years or over | 32 | 18.4% | |

| Educational qualifications | 12th-grade degree or less | 37 | 21.3% |

| Bachelor’s degree | 69 | 39.7% | |

| Master’s degree or higher | 68 | 39.1% | |

| Residence | Village | 31 | 17.8% |

| Town | 21 | 12.1% | |

| City | 122 | 70.1% | |

| Bank employee | No | 160 | 92% |

| Yes | 14 | 8% | |

| Construct | Question | Literature and Year |

|---|---|---|

| Fintech knowledge | Do you know what Fintechs are (technology companies operating in the financial sector—100% online)? | Based on Hasan et al. (2023, p. 7) |

| Perception of security | Considera as Fintech seguras? | Own source |

| Fintech customer | Are you a Fintech customer? | Own source |

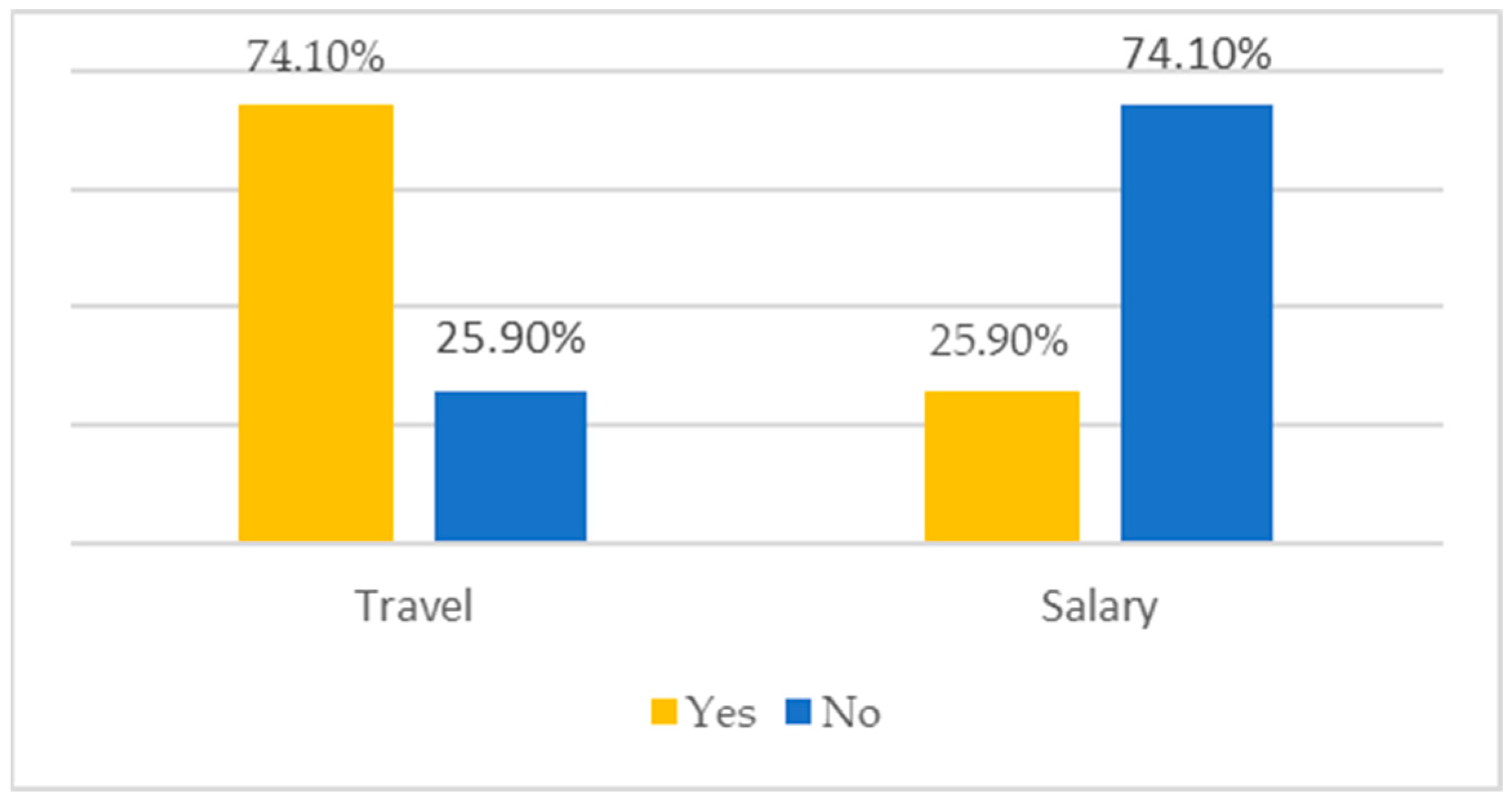

| Do you use Fintech for travel transactions? | Own source | |

| Do you use Fintech to receive your salary? | Own source | |

| Reason for being a Fintech client: | Lower costs; | Based on Martincevic et al. (2022); Fernandes (2019, p. 6) |

| Convenience; | ||

| Easy to use; | ||

| Better online experience compared to traditional banks. | ||

| Reason for not being a Fintech client: | Lack of awareness of its existence; | Based on Hasan et al. (2023, p. 7) |

| Limited knowledge of the internet; | ||

| Lack of security; | ||

| Preference for face-to-face and personalized service. | ||

| Changing banks | Would you change your traditional bank account for a Fintech one? | Based on Jones and Ozcan (2021, p. 6) |

| Impact of COVID-19 | After the COVID-19 pandemic, do you feel more inclined to use a Fintech? | Based on Versal et al. (2022, p. 8) |

| Perception of supervision and regulation: | Bank—Supervision | Own source |

| Bank—Regulation | ||

| Fintech—Supervision | ||

| Fintech—Regulation |

| Reason for Being a Fintech Client | Strongly Disagree | Disagree | Neither Agree nor Disagree | Agree | Strongly Agree |

|---|---|---|---|---|---|

| Lower costs | 0% | 3.7% | 7.4% | 37% | 51.9% |

| Convenience | 3.7% | 0% | 3.7% | 22.2% | 70.4% |

| Easy to use | 0% | 0% | 11.1% | 22.2% | 66.7% |

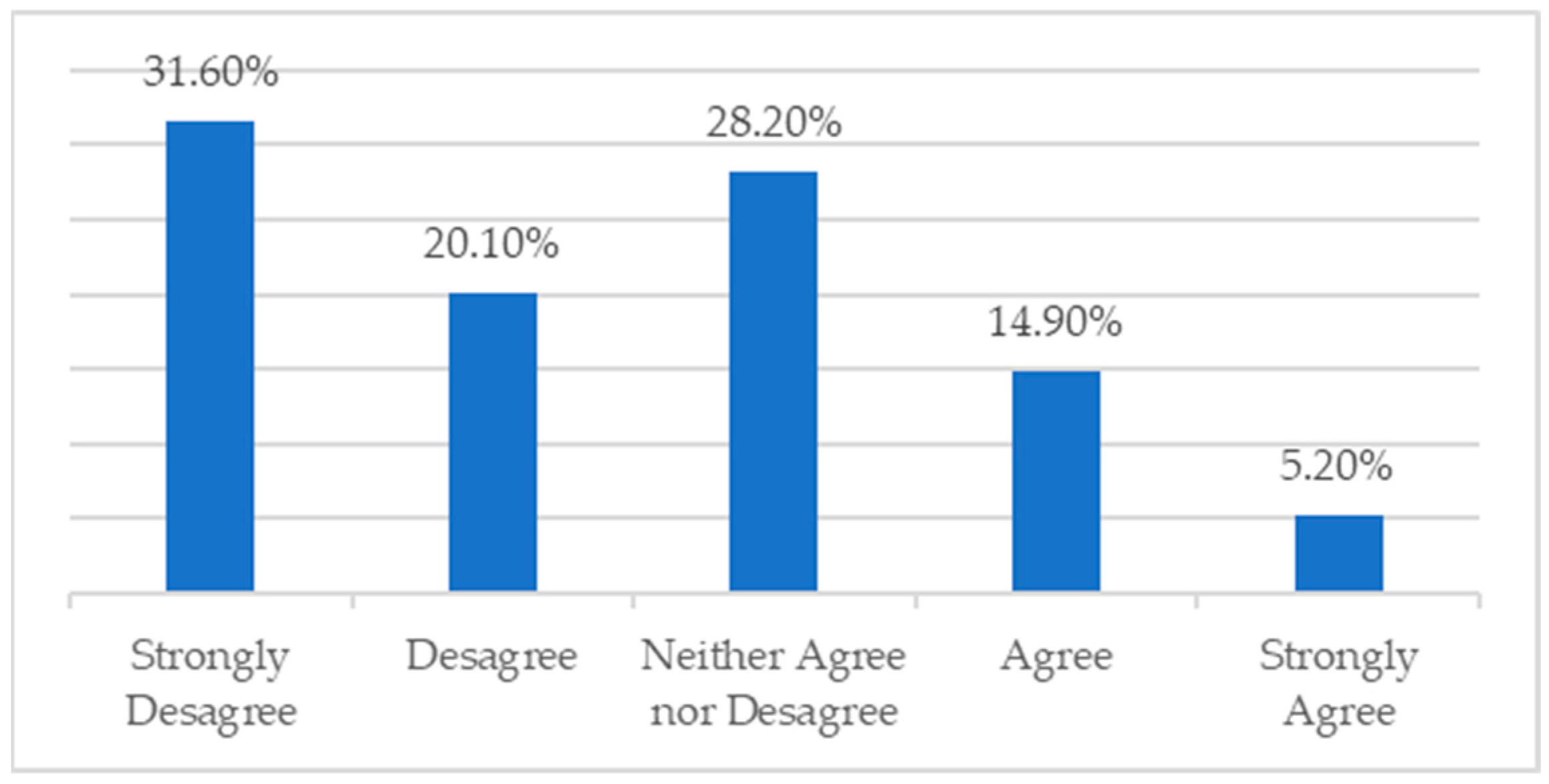

| Better online experience compared to traditional banks | 7.4% | 0% | 33.3% | 29.6% | 29.6% |

| Reason for Not Being a Fintech Client | Strongly Disagree | Disagree | Neither Agree nor Disagree | Agree | Strongly Agree |

|---|---|---|---|---|---|

| Lack of awareness of its existence | 19.7% | 4.8% | 12.2% | 11.6% | 51.7% |

| Limited knowledge of the internet | 57.1% | 12.9% | 15.6% | 6.1% | 8.2% |

| Lack of security | 26.5% | 16.3% | 29.9% | 12.9% | 14.3% |

| Preference for face-to-face and personalized service | 18.4% | 7.5% | 21.1% | 17.7% | 35.4% |

| Evaluation of the Degree of Supervision and Regulation | Not at All | Very Little | Neutral | Moderate | Very Much |

|---|---|---|---|---|---|

| Bank—Supervision | 6.3% | 16.1% | 36.8% | 24.1% | 16.7% |

| Bank—Regulation | 4.6% | 10.9% | 40.8% | 23.0% | 20.7% |

| Fintech—Supervision | 21.3% | 24.7% | 40.8% | 8.6% | 4.6% |

| Fintech—Regulation | 21.8% | 26.4% | 37.9% | 8.6% | 5.2% |

| Gender | Total | |||

|---|---|---|---|---|

| Female | Male | |||

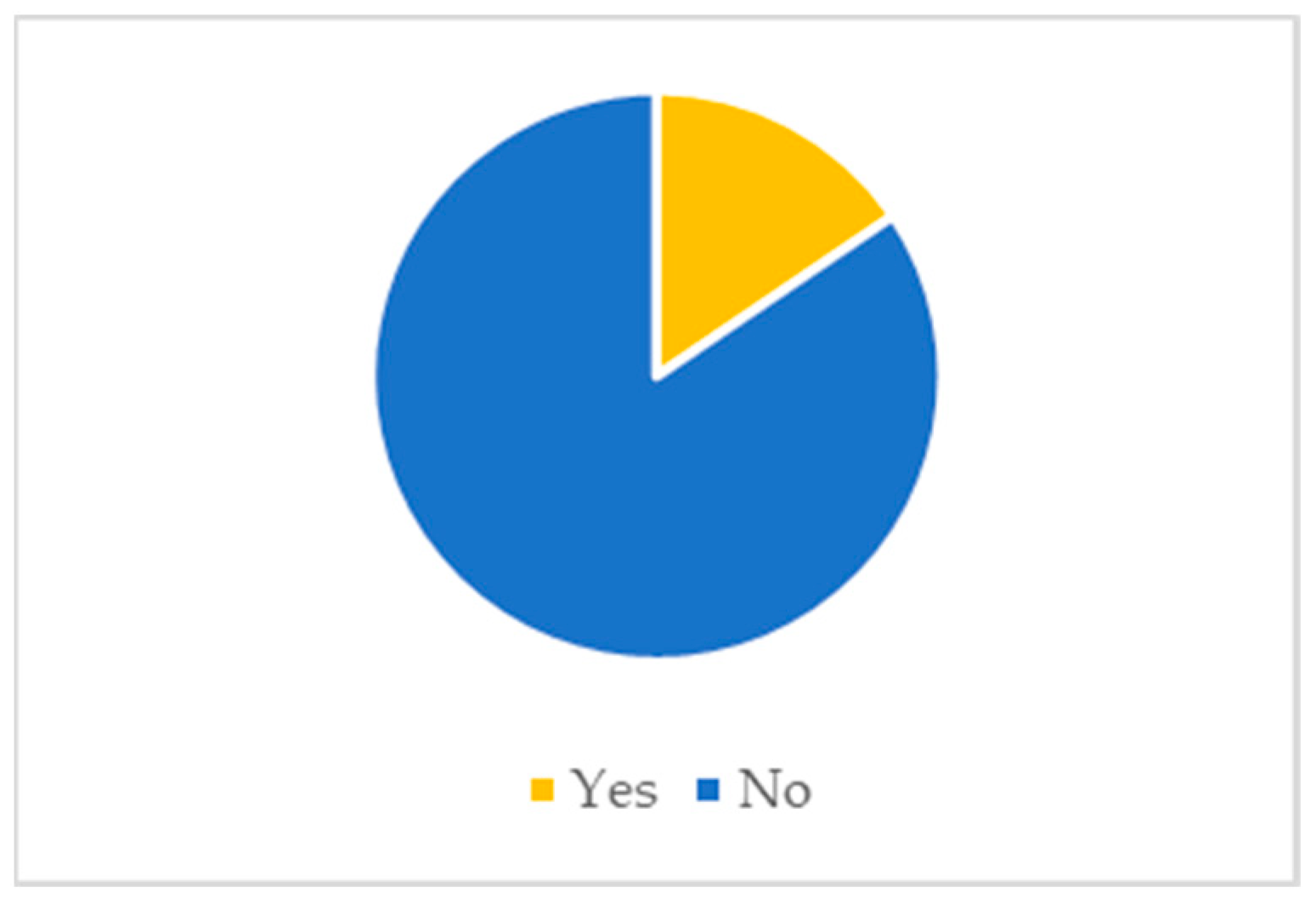

| Knowledge of Fintech | No | 102 | 15 | 117 |

| 75.0% | 39.5% | 67.2% | ||

| Yes | 34 | 23 | 57 | |

| 25.0% | 60.5% | 32.8% | ||

| Total | 136 | 38 | 174 | |

| 100.0% | 100.0% | 100.0% | ||

| Age Group | Total | |||||

|---|---|---|---|---|---|---|

| 18 to 30 Years | 31 to 40 Years | 41 to 50 Years | 51 Years or Older | |||

| Knowledge of Fintech | No | 40 | 24 | 35 | 18 | 117 |

| 59.7% | 80.0% | 77.8% | 56.3% | 67.2% | ||

| Yes | 27 | 6 | 10 | 14 | 57 | |

| 40.3% | 20.0% | 22.2% | 43.8% | 32.8% | ||

| Total | 67 | 30 | 45 | 32 | 174 | |

| 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | ||

| Worked or Had Worked in Banking | Total | |||

|---|---|---|---|---|

| No | Yes | |||

| Knowledge of Fintech | No | 114 | 3 | 117 |

| 71.3% | 21.4% | 67.2% | ||

| Yes | 46 | 11 | 57 | |

| 28.7% | 78.6% | 32.8% | ||

| Total | 160 | 14 | 174 | |

| 100.0% | 100.0% | 100.0% | ||

| Independent Variable | Dependent Variable | Z | p | r | Rank Means | |

|---|---|---|---|---|---|---|

| Yes (n = 57) | No (n = 117) | |||||

| Knowledge of Fintech | Changing banks | 4.65 *** | <0.001 | 0.35 | 111.74 | 75.69 |

| Independent Variable | Dependent Variable | Z | p | r | Rank Means | |

|---|---|---|---|---|---|---|

| Yes (n = 57) | No (n = 117) | |||||

| Fintech Security | Changing banks | 5.60 *** | <0.001 | 0.42 | 108.10 | 67.36 |

| Z | p | r | Rank Means | |

|---|---|---|---|---|

| Traditional Bank | Fintech | |||

| 7.47 *** | <0.001 | 0.33 | 1.71 | 1.29 |

| Z | p | r | Rank Means | |

|---|---|---|---|---|

| Traditional Bank | Fintech | |||

| 8.85 *** | <0.001 | 0.46 | 1.74 | 1.26 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Costa, M.; Au-Yong-Oliveira, M.; Moreira, A. Fintech: Evidence of the Urgent Need to Improve Financial Literacy in Portugal. Adm. Sci. 2024, 14, 99. https://doi.org/10.3390/admsci14050099

Costa M, Au-Yong-Oliveira M, Moreira A. Fintech: Evidence of the Urgent Need to Improve Financial Literacy in Portugal. Administrative Sciences. 2024; 14(5):99. https://doi.org/10.3390/admsci14050099

Chicago/Turabian StyleCosta, Mariana, Manuel Au-Yong-Oliveira, and Ana Moreira. 2024. "Fintech: Evidence of the Urgent Need to Improve Financial Literacy in Portugal" Administrative Sciences 14, no. 5: 99. https://doi.org/10.3390/admsci14050099

APA StyleCosta, M., Au-Yong-Oliveira, M., & Moreira, A. (2024). Fintech: Evidence of the Urgent Need to Improve Financial Literacy in Portugal. Administrative Sciences, 14(5), 99. https://doi.org/10.3390/admsci14050099