Abstract

The processing and transformation of natural resources into completed and semi-finished products is the primary function of industry in each nation’s economy. There is no denying the significance of industry and sectoral classification of the economy, but the slow development and extension of one industry could have resulted in the advancement of other sectors that are now a part of contemporary communities. Since there are statistically significant differences between various industries, numerous authors are currently investigating the impact of the industry on the financial structure of firms, revealing the industry as a crucial determinant of corporate indebtedness. Thus, the main aim of this study is to determine the debt level of a sample of 4237 enterprises operating in the market in the period of 2018–2021 from various sectors using eight debt indicators, as well as to identify relationships between them, which may help to reveal sectors with homogeneous patterns of indebtedness (using the cluster analysis) and thus understand which sectors are the most stable and independent. The Kruskal–Wallis test is then used to determine if there are statistically significant differences between the calculated ratios related to the economic sector. Based on the results, it can be concluded that the choice of financial structure is significantly influenced by the industry. Financial performance and indebtedness indicators are quantitative statistics used to assess, monitor, and forecast company or sectoral financial health. They act as instruments for business insiders and outsiders to assess a company’s performance, particularly in comparison to competitors, and to pinpoint its strengths and weaknesses, making the outputs of this study important for all types of stakeholders.

1. Introduction

Firms in dynamically evolving market sectors attempt to react to competition or established customer requirements by reacting to new impulses and environmental effects. Currently, when the economies of different countries around the world are experiencing adverse developments, mostly due to the COVID-19 pandemic, the war in Ukraine, or the energy crisis, overcoming a difficult period of business management is crucial. Along with measuring corporate performance (e.g., in terms of sustainable growth rate—Bagh et al. 2023, of sustainable development—Crișan-Mitra et al. 2016; Crișan-Mitra et al. 2020, or of debt level—Gajdosikova et al. 2023), this process also includes assessing the achieved results from the point of view of financial health, evaluating the methods used to measure performance, and fulfilling long-term corporate objectives for the future (Valaskova and Nagy 2023). Using these methods and procedures, firms are able to obtain and subsequently evaluate data that reflect not only the dynamics of corporate development but also quantify the impact of the economic crisis on changes in the structure of financial indicators over the years and formulate proposals and recommendations for the future (Stratone 2023). The corporate financial situation is constantly influenced by many factors that must be identified for the firm to maintain its long-term development, particularly considering integrating cutting-edge technologies such as artificial-blockchain- and Internet of Things-based fintech (Andronie et al. 2023; Barbu et al. 2021; Lăzăroiu et al. 2023). The assessment of the financial situation of the enterprise helps in identifying problems and critical circumstances in time, thus preventing bankruptcy. If a firm aims to be successful in the market and compete in a rapidly changing environment, it should consider not only an adequate financial nation but also subsequent financial development (Zhang and Ding 2023). In general, a financially healthy company (Kliestik et al. 2020b) fulfills two requirements: (i) it is liquid over the long term (i.e., it can pay its obligations on time both now and in the future as long-term liquidity is significantly influenced by the ratio of equity and debt financing in the overall capital structure of the company (Santos et al. 2022)); and (ii) it is profitable (i.e., it can generate enough profit to cover its costs through its business activities (Ogunode et al. 2022)). The ratio between equity and debt, represented by the corporate financial structure (Lăzăroiu et al. 2020b; Nagy et al. 2023; Valaskova et al. 2023), is an issue that is frequently discussed in relation to financial analysis. Decisions regarding the development of the corporate capital structure are strategic ones, the consequences of which manifest over several years. Therefore, it is necessary to take several factors into account when developing it. Numerous studies have been conducted regarding the impact of particular determinants on a corporate capital structure (Brendea et al. 2022; Sardo et al. 2022; Zakaria and Salawa 2023). However, the industry in which the enterprise operates has an impact on the capital structure. Enterprises operating in the same sector have certain similar characteristics, such as the products they sell, how their production costs are structured, the technologies they employ (Valaskova et al. 2022; Nagy and Lazaroiu 2022), and their levels of profitability, while these tendencies are also manifested in the area of corporate capital structure. According to Ibrahim and Lau (2019), each industry has a distinct average total debt ratio. Since Schwartz and Aronson (1967) first outlined the relationship between industry affiliation and the capital structures of corporations in the United States, more than 50 years have passed. The industry determinant is nevertheless frequently taken into account in empirical capital structure research. The main aim of this paper is to determine the debt level in the Slovak environment on a sample of 4237 enterprises from various sectors, as well as to identify relationships between them, which may aid in identifying sectors with homogeneous patterns of indebtedness and thus understand which sectors are the most stable and independent. From an economic standpoint, Slovakia stands as a compelling example of a nation that has undergone remarkable transformation and development. Nestled in the heart of Europe, the economy of Slovakia has evolved significantly since gaining independence in 1993. The country transitioned from a centrally planned economy to a market-oriented system, embracing reforms that propelled it into the European Union in 2004. One of the key drivers of the economic success of Slovakia has been its robust manufacturing sector, particularly automotive production. The presence of major international car manufacturers has not only contributed substantially to exports but has also spurred technological advancements and innovation within the country. Additionally, its strategic location and well-developed infrastructure have made it an attractive destination for foreign direct investment. Over the years, Slovakia has experienced steady economic growth, with GDP per capita gradually converging toward the European Union average. However, like many nations, it has faced challenges, including the need for continued economic diversification, addressing regional disparities, and adapting to global economic uncertainties. The economic landscape of Slovakia witnessed significant fluctuations and transformations from 2018 to 2021, reflecting a complex interplay of domestic and global factors. During this period, Slovakia navigated through challenges and opportunities that influenced its overall economic performance. As Slovakia continues to navigate the intricacies of the international economic landscape, its resilience and commitment to innovation position it as a noteworthy player in the European economic framework. Understanding the nuances of Slovakia’s economic journey provides valuable insights into the dynamics shaping its future growth and prosperity. Generally, the importance of one-country studies has arisen due to different changes in individual countries caused by divergent effects of the COVID-19 pandemic and other macroeconomic changes based on the industrial orientation of national economies.

The paper is divided into the following sections: the literature review includes the most pertinent and recent studies in the field. Concentrating on industries with homogeneous patterns of indebtedness and the existence of statistically significant differences in debt indicators due to the Nomenclature of Economic Activities (NACE) classification, the methodology section determines the sample of analyzed firms as well as the research methodological steps required for debt analysis implementation. The results and discussion section presents the findings from the statistical verification of selected debt indicators that were previously calculated. In the context of other international studies, these findings are discussed and argued. The most significant results from the research are highlighted in the conclusion section, along with limitations and further research challenges.

2. Literature Review

Firms have experienced certain changes over the past several decades as a result of the constantly changing circumstances in the market. This development was mainly caused by the advancement in science and research (Peng and Tao 2022), international integration (Onegina et al. 2022), and the growth in competitiveness (Marousek and Gavurova 2022; Adjei and Grega 2023; Privara 2022). For enterprises to maintain or improve their position in a specific business sector (Durana et al. 2022; Borowiecki et al. 2022), continuous evaluation and improvement regarding achieved business performance are necessary. The most important aspect is the corporate performance evaluation, which is used as the primary measure. The performance of the firm can be examined from the perspectives of marketing (Michulek et al. 2023; Michulek and Krizanova 2023), human resources (Zhang 2022), customer perspective (Kral and Janoskova 2023; Nahalkova Tesarova and Krizanova 2023), and management (Mazzucchelli et al. 2022). The financial performance analysis can provide the most detailed information about a specific corporate performance (Roy and Patro 2021; Galant and Cvek 2021), which occupies an invaluable position in the evaluation of the selected business entity (Oliver 2022).

The term performance is often used in everyday life in several areas, including sports and international finance (Kang and Kim 2023). Performance generally refers to how a particular investigated subject carries out an activity compared to the reference manner of completing the given activity. In the long term, however, in the current economic environment of the firm, it is not enough to rely on the currently achieved performance (Boulhaga et al. 2023), but it is necessary to focus on its continuous increase (Dana et al. 2021). Chen et al. (2023) characterize the measurement of corporate performance as a process whose key role is to support the development of the business into the future using the analysis and evaluation of established methods and procedures. Several definitions of performance agree on the success and achievement of established objectives. Performance can be broadly defined as a characteristic that helps in realizing the corporate future vision (Madaleno and Vieira 2020) through continuous measurement (Weqar et al. 2021) and comparison of past results with established criteria and predictions for the future (Barbuta-Misu and Madaleno 2020). The achieved results of individual financial analysis indicators (Li et al. 2021), industry statistics (Xu and Li 2019), or the effectiveness of the use of corporate production factors (Zhang and Aumeboonsuke 2022) are a few examples of these criteria in the area of the financial performance of enterprises. Business performance, which is additionally referred to as the operationalized level of business competitiveness, is the main subject of evaluation in several business studies, focusing on the success or productivity of corporate financial performance (Kristof and Virag 2022). Studies based on financial data and their analysis to ascertain the financial performance of the firm form the largest group of corporate performance evaluations. Through methods and techniques of financial analysis, financial performance describes the achieved corporate financial health (Durica et al. 2023; Kaczmarek et al. 2021). According to Hedija and Nemec (2021), Jin et al. (2022), and Kayani et al. (2023), data collected through financial performance evaluations have significant explanatory power. Many authors employ intricately constructed systems of indicators or constructed models that are separated into several parts to evaluate the performance of firms (e.g., in terms of labor productivity growth—Lăzăroiu and Rogalska 2023, of deliberate managerial strategy—Vătămănescu et al. 2020, and of organizational achievements—Vătămănescu et al. 2023) with the intention of introducing a more detailed comprehension of the achieved corporate performance.

Financial performance indicators generally focus on the data obtained from the profit and loss statement and balance sheet of the firm and are used to analyze not only revenues and expenses (Magni and Marchioni 2020) but also cash flow (Handoko et al. 2021). Financial indicators can be used to assess corporate activity (Zeynalli 2023), liquidity (Batrancea 2021), indebtedness (Guo and Zhao 2019), and overall performance (Stashchuk et al. 2021). Maximizing profit (Nyantakyi et al. 2023) and increasing the market value of the firm (Kluiters et al. 2023) are two fundamental objectives. In order to develop and make investments, a firm has to produce a profit (Jyoti and Khanna 2021). To monitor the achievement of this goal, return on equity (Wang et al. 2019) is often used, which is a crucial indicator of profitability because the investor needs to know the likely return on any investment made (Pham and Dao 2022) and return on sales, which is determined by operating profit as a percentage of sales. Goel (2021) states that a firm can be profitable but at the same time it can have cash flow problems. The ability of the firm to meet its short-term financial obligations is measured by liquidity indicators (Zhan et al. 2022). One of the best-known indicators of liquidity is current liquidity, which measures the ability of an enterprise to meet its short-term obligations due within one year with current assets that can be converted into cash (Vukovic et al. 2022). Although the monitoring of this financial indicator differs based on the sector in which the company operates, a value greater than 1 is recommended (Scalzer et al. 2019). The firm may have liquidity difficulties if this indicator displays a gradually decreasing trend or a lower value compared to the industry average. On the contrary, a high value of the ratio indicates that excess cash is not used efficiently (Farahani et al. 2020). It is the liquidity of the company that is a prerequisite for its financial stability (Casu et al. 2019), while, if it is disturbed, it is possible to point to the insolvency of the firm (Pulawska 2021), which is closely related to the indebtedness (Olujobi 2021). The use of borrowed funds by a firm for financing its business activities and assets is known as corporate indebtedness (Baines and Hager 2021). A high debt ratio indicates that the business relies heavily on debt to finance its long-term needs (Ahmed and Afza 2019). Many companies choose debt financing since they are unable to finance themselves entirely with their own resources in the present economic situation. Indicators of indebtedness reveal how extensively foreign resources are used (Benlemlih and Cai 2020), help in an in-depth evaluation (Jacobs et al. 2020), and analyze and plan adjustments to corporate financing sources (Amare 2021). Even though there are numerous indicators of indebtedness, total indebtedness is regarded as a complex indicator that captures the structure of financial resources (Jencova et al. 2021). Due to the wide variations among sectors, there is no set recommendation for what proportion of the requirements of a business should be financed by debt. When a company uses debt financing, its earnings and shareholder returns (Kliestik et al. 2020a; Santos-Jaén et al. 2023) might increase. Since the interest on the debt must be repaid even if the company does not make a profit, this type of financing represents a higher risk for the firm (Hudakova et al. 2023). Financial decision making requires particular attention to the optimal capital structure setting since it is a relatively complicated issue (Cerkovskis et al. 2022). The ratio of equity to debt funding is largely influenced by the sector in which the firm works (Kucera et al. 2021), the structure of the assets of the company (Srhoj 2022), and the interest rate charged by banks (Liao 2020). The profitability of equity capital is frequently increased by employing debt as long as the interest rate is less than the profit of the enterprise itself (Jedrzejczak-Gas 2013). Financial leverage may be categorized as debt-related actions. The more debt the firm generates, the higher the financial leverage indicator (Iqbal et al. 2022). The financial leverage indicator is predicated on the idea that using debt to finance corporate operations increases the relative profitability of equity (Toemoeri et al. 2021) and also assumes that debt financing is less expensive than equity financing (Hong et al. 2021). At the same time, however, the use of foreign capital also increases the riskiness of the firm (Kljucnikov et al. 2022).

Numerous determinants, such as prioritizing the financing of business operations basically through debt, have an impact on corporate indebtedness and affect the composition of corporate capital in different ways (Gajdosikova et al. 2023). The size of the firm greatly influences the level of corporate debt. As evidenced by their lower level of debt, smaller enterprises have a lower percentage of foreign resources than larger ones (Rahim et al. 2019). The legal form of the company is frequently mentioned (e.g., Dvoulety and Blazkova 2021; Allaya et al. 2022) as a significant factor affecting the choice of financing form. Even Farhangdoust et al. (2020) points out significant differences in the indebtedness of firms as a result of the impact of their selected legal form. Corporate indebtedness is significantly influenced by the level and volatility of corporate profits (Fischer and Jensen 2019; Kliestik et al. 2022), the costs of financial difficulties (Alvarez-Botas and Gonzalez 2021), the impact of inflation (Jaworski and Czerwonka 2021), the effort to maintain ownership control of the firm (Martins et al. 2020), dividend policy (Sierpinska 2022), requirements for the financial flexibility of the firm (Jameson et al. 2021), and the method and intensity of taxation (Sobiech et al. 2021), while earnings management may also have implications for corporate debt (Valaskova and Gajdosikova 2022). According to Ramelli and Wagner (2020), the market situation has significant consequences for the financial decision making of the business entity. The affiliation of the firm to the industry is another factor that Chen et al. (2022) identify as influencing the level of corporate indebtedness. Industry classification has a significant impact on the average corporate debt level ratio (Harris and Raviv 1991). Furthermore, Bradley et al. (1984) reveal that industry is a significant determinant of leverage and that there is greater diversity across sectors than within industries in corporate leverage ratios. The result indicates the consistency within an industry and the variability between industries. According to Gaud et al. (2005), small- and medium-sized enterprises are impacted by the industry in which they operate. Generally, small- and medium-sized enterprises within a particular sector additionally face identical present circumstances and frequently implement a similar financing pattern. Furthermore, Hall et al. (2004) presented evidence that agency costs may fluctuate throughout firms and provided inter-industry differences in the debt of these enterprises. According to La Rocca et al. (2011), industry-specific characteristics have an impact on the debt ratio by affecting the significance of business risk, tangible assets, and growth opportunities. Therefore, industry-specific variables may influence the capital structure of small- and medium-sized enterprises. Most research papers on the factors that determine the capital structure of a firm have investigated the impact of the industry using dummy variables or median industry variables (e.g., De Jong et al. 2008; Degryse et al. 2012). Nowadays, the impact of industry on corporate capital structure has been examined by many authors. Kayo and Kimura (2011) and Smith et al. (2015) used the three industry-specific determinants. La Rocca et al. (2011) concluded that firms in a developing sector frequently require additional external financing to cover their investment potential since internal financing may not be sufficient to cover all future opportunities. Danso et al. (2021) suggested that the characteristics of the firms and the nations where their shares are listed determine a significant amount of the predictive power of industry affiliation on firm capital structure. However, industry continues to contribute significantly to the difference in capital structure ratios, even after considering both firm and country impacts.

The perception that businesses and their debt levels should be systematically determined and evaluated was the inspiration in identifying clusters of sectors with homogeneous patterns of indebtedness and similar capital intensity levels in various economic conditions. Thus, the following hypothesis was set:

H1:

In particular Slovak conditions, there is a significant occurrence of homogeneous patterns of indebtedness across the sectors.

Due to internal differences among countries, industries, or the particulars of the enterprises themselves, the existing literature has not been able to reach a consensus on the crucial variables affecting the capital structure. The interaction of several factors affects how each capital component is represented in the capital structure. There are definitions of a number of factors that affect the corporate capital structure in the international literature. Although there are numerous theoretical models, there is no comprehensive method for developing an appropriate capital structure. There is no solution in the form of a general algorithm into which values may be inserted to calculate the actual optimal capital structure of the enterprise. The ability of the financial manager to appropriately identify the factors that determine indebtedness in the context of corporate features, which have a significant impact on how much indebtedness is perceived generally, is one of the many skills and aspects of knowledge that are required for the solution to be successful.

3. Materials and Methods

The main aim of this paper is to determine the debt level in the Slovak environment on a sample of 4237 enterprises from various sectors as well as to recognize relationships between them, which may aid in identifying sectors with homogeneous patterns of indebtedness and thus understanding which sectors are the most stable and independent.

A comprehensive debt analysis required financial parameters from the ORBIS database, which is considered a source of business and financial data on more than 400 million private and public enterprises operating worldwide. The database, which formed the basis for a debt analysis, contains financial data on 30,130 enterprises operating in Slovakia for the monitored period of 2018–2021. Because not all enterprises fulfilled the requirements for calculating the debt indicators, the data from the database were appropriately adjusted. Enterprises that did not provide all the required input data for the debt analysis throughout the monitored period were eliminated. Using the Z-Score method, any outliers that would have reduced the relevance of the findings from the realized financial analysis were also removed. This approach may be used to calculate the difference between each received signal strength observation and the time series mean received signal strength observation, while the result is divided by the standard deviation of the observation. This standardization process expresses each observation in terms of standard deviations from the mean, offering a measure of how far each data point deviates from the average. When the Z-Score is 0, the mean of the time series observation and the received signal strength observation are identical, and a positive Z-Score indicates that the received signal strength measurement is above or below the mean. A received signal strength observation is considered an outlier if its Z-Score value exceeds an established threshold (Jamshidi et al. 2022). In this paper, we considered a received signal strength observation to be an outlier if its Z-score value was higher than ±3 because Afzal et al. (2021) concluded that the most commonly used threshold for detecting outliers is ±3. Although a threshold of ±3 is relatively conservative as it requires a data point to deviate significantly from the mean to be classified as an outlier, this threshold corresponds to a high level of confidence as it covers a wide range of values within the tails of a normal distribution. Table 1 contains the elementary identification data for 4237 Slovak firms, such as firm size, legal form and ownership structure, firm age, and economic sector.

Table 1.

Firm-specific features of the sample.

The final dataset is composed of the information required for the debt analysis of firms operating in Slovakia. According to the requirements set in the ORBIS database to determine firm size characteristics, a very large enterprise is one that fulfills at least one of the following conditions: operating revenue ≥ EUR 100 million, total assets ≥ EUR 200 million, and employees ≥ 1000. A large enterprise is regarded as one with an operating revenue ≥ EUR 10 million, total assets ≥ EUR 20 million, and employees ≥ 150. An enterprise is classified as medium-sized if at least one of the following conditions is met: operating revenue ≥ EUR 1 million, total assets ≥ EUR 2 million, and employees ≥ 15. Small enterprises are those that do not satisfy these criteria. The final dataset contains the most enterprises operating in the medium-sized enterprise category. The category of very large enterprises, however, is the least well-represented.

The ORBIS database determines the following legal forms. The four types of ownership structures that enterprises operating in Slovakia implement are partnerships, private limited companies, public limited companies, and other legal forms. A private limited company has been legally incorporated into supplementary legal identities. With this type of ownership structure, the shareholders are only partially responsible for any debts acquired by the business (Ferlie and Trenholm 2019). Many firms in Slovakia have the legal form of a private limited company. A public limited company, which is occasionally confused with a private limited company, differs in that it can allow the public to buy the shares of the firm. According to Dolinsek et al. (2014), the enterprise might benefit financially from this approach. A partnership is another type of legal form developed by a small group of individuals who participate in the ownership and decision making of the firm and its earnings. According to Ahmad and Fakih (2022), each individual may provide a distinctive field of specialization to the firm in order to improve its marketability.

The ORBIS database also provides information about the number of years in the market. However, to improve the clarity of the obtained data, the firms were classified into age categories based on the length of their market participation. The firms that have been in the market the longest have the least share (more than 40 years). In Slovakia, there are many enterprises that have been operating for 10 to 20 years. These enterprises are sufficiently stable and will provide the necessary data for the research because they are recognized as market leaders and have been operating for over 10 years.

NACE is a standard classification system used to categorize economic activities at the European Union level. In general, the NACE classification system provides a common framework for statistical and economic analysis, facilitating the comparison of economic data across different countries and regions. The NACE classification is primarily used to classify businesses and economic activities based on their primary function or type of production because the classification system is hierarchical, organized into sections, divisions, groups, and classes. Most enterprises in Slovakia operate in category G—Wholesale and retail trade, repair of motor vehicles/motorcycles. This category took first place because Slovakia is well-known for its automotive manufacturing. Their subsequent sale and service have an unbreakable connection to automotive production. Category C—Manufacturing can also be considered a crucial economic sector because Slovakia still places a high priority on manufacturing. However, only a small number of enterprises in the sample are involved in category K—Financial and insurance activities.

Several methodological steps were followed to perform the financial analysis concerning the indebtedness of enterprises operating in the Slovak environment. A comprehensive evaluation of Slovak corporate indebtedness from 2018 to 2021 was performed using eight debt indicators. The formulas required for the following calculation are presented in Table 2.

Table 2.

Summarized formulas of indebtedness indicators.

Table 3 summarizes descriptive statistics over a 4-year time horizon, including average, median, standard deviation, minimum, maximum, and coefficient of variation. Financial data (in thousands of Euros) were used as the basis for the estimation of debt indicators.

Table 3.

Financial data descriptive statistics required to calculate indebtedness ratios.

Subsequently, the normality tests were applied to verify whether a dataset is well-modeled by a normal distribution. Since it can be challenging to determine whether a deviation from linearity is systematic or is just the consequence of sample variation, a statistical test of normality can be helpful (Henze and Koch 2020). The null hypothesis is that the sample comes from a normal distribution, and the alternative is that the sample is from a non-normal distribution. The Shapiro and Wilk (1965) test had a sample size restriction of 50, and this test was the first to be able to detect deviations from normality using either skewness, kurtosis, or both. It has become the preferred test due to its strong power characteristics (Hazelton 2003). A sample of real-valued observations is tested using the Shapiro–Wilk test, which evaluates the composite hypothesis that the data are independent, symmetrically distributed, and normal; i.e., for some unknown real and some . Sample skewness and kurtosis are both one-dimensional variables. Meanwhile, if the data are arranged in order, it is unlikely to lose any information to obtain the order statistics (Wei 2022). It is required to consider the expectations of as well as the correlation of in order to assess if the order statistics of are closely associated with expected standard normative order statistics. Meanwhile, a correlation substantially less than 1 would indicate non-normality; a correlation close to 1 would indicate a significant fit to normality. If a constant is added to all the , it is then added to their order statistics, as well as to , leaving and unchanged (Hanusz et al. 2016). If all are multiplied by a positive constant, the ratios and the correlation remain unchanged. Therefore, if the are independent, identically distributed normally, the correlation will have the same distribution regardless of the location or scale of the . There are several symmetry properties in the and their expectations . In contrast to the more well-known Shapiro–Wilk statistic, which utilizes both the means and covariances of the normal order statistics , the Shapiro and Francia (1972) statistic uses the squared correlation of with as a test statistic for normality. Given an ordered random sample, the original Shapiro–Wilk test statistic is defined by

as in Shapiro and Wilk (1965). The value of lies between zero and one. A value of one denotes that the data are normally distributed, whereas low values of result in the rejection of normality (Wei 2022). There are several more widely used normality tests to verify normality, such as Anderson–Darling test (Anderson and Darling 1954), Cramer–von Mises test (Cramer 1928), and Kolmogorov–Smirnov test (Kolmogorov 1933; Smirnov 1936). The Kolmogorov–Smirnov test statistic is the maximum absolute difference between the cumulative distribution function and the normal cumulative distribution function, compared to the Anderson–Darling and Cramer–von Mises tests, which are based on a weighted integral of the squared difference. The statistical software output usually includes the normality test p-values, and a small p-value is interpreted as evidence that the sample is not from a normal distribution. Because many statistical methods (such as t-tests and analysis of variance) are based on the assumption that data are normally distributed, this test of a parametric hypothesis is non-parametric. If they are not, non-parametric methods might be needed.

Since NACE provides the framework for collecting and presenting statistical data according to numerous economic sectors, cluster analysis is used to reduce the number of input data (categories under consideration). The provided review and analysis of the indebtedness ratios were followed by the application of cluster analysis to examine the relationship between debt level and sectors of economic activity, provided by the NACE classification of Slovak enterprises, which was conducted with an emphasis on the sector of economic activity in which the firm operates. Due to the heterogeneity of the sectors of economic activity, an attempt was made to divide these sectors into groups with similar assessments. Cluster analysis, one of the statistical multivariate analysis methods, was used for this. This method is an interdependency analysis one, which implies that all variables in the analysis are considered interdependent without being divided into dependent (effects) and independent variables (reasons) (Rodriguez and Laio 2014). According to Cipresso et al. (2018), cluster analysis allows researchers to group objects into clusters. Generally, the objects in the same cluster are as similar as possible, whereas those in other clusters are considerably dissimilar. To use cluster analysis, the calculations must fulfill a few assumptions: (i) the dataset cannot include outliers or missing data; (ii) it is appropriate to use standardized variables; and (iii) the existence of dependence among the variables may have a negative impact on the results (Yim and Ramdeen 2015). The cluster analysis was realized through the following methodological steps: (i) variable selection and adoption of the method to determine similarities between objects; (ii) method selection for assigning given objects to a homogeneous group; (iii) selection of the number of identified clusters; and (iv) interpretation and profiling of acquired clusters (Wade and Ghahramani 2018; Stahl and Sallis 2012).

The choice of the proper measurement method depends on the character of the application. In this research paper, agglomerative hierarchical clustering was used to cluster the economic sectors identified by the NACE classification of Slovak enterprises. Hierarchical clustering begins with n clusters, where each observation forms a separate homogeneous group, and ends with one cluster that includes all observations (Wang et al. 2010). In each step, the two closest observations, or observation clusters, are merged into one new cluster. The clustering method is represented by a dendrogram, which depicts the individual steps of hierarchical clustering, including the distances at which the separate clusters (or observations) were merged. The dendrogram is used to present the results. The method for expressing the similarity (distance) of individual cases is the starting point for clustering (Langfelder and Horvath 2012). Ward’s method, a hierarchical clustering method based on the creation of clusters with the highest possible internal homogeneity, was used to compute the hierarchical method when identifying sectors with homogeneous patterns of indebtedness in the Slovak environment. Ward’s method, which identifies and merges clusters with a minimum sum of squares, is based on the analysis of variance. This increase is a weighted squared distance between cluster centers (Bhaumik and Ghosal 2017). Firstly, all clusters are singletons (clusters containing a single point). The initial distance between individual objects must be the squared Euclidean distance in order to apply a recursive algorithm under this objective function. The squared Euclidean distance between points is consequently used to define the initial cluster distances in Ward’s minimum variance method:

where is the value of -th variable of the -th object and is the value of -th variable of the -th object.

The Kruskal–Wallis test was used to determine if there are statistically significant differences between two or more groups of an independent variable (Kruskal and Wallis 1952). When the assumptions for a normal distribution of each group with approximately equal variance in the scores are not fulfilled, the non-parametric Kruskal–Wallis test is used. The Kruskal–Wallis test is a non-parametric approach for comparing independent samples (Sangthong 2020) and is used to test for median or mean equality (Rayner and Livingston 2020). It is essential to compare the groups of sizes with in accordance with a continuous response variable Y if a random sample of size N from a large population consists of distinct groups or categories that are sufficiently represented in the sample. When the precise category assignment is identified, the Kruskal–Wallis test is performed by ranking each observation separately and comparing the sum of the ranks for each group. If is the rank of in the entire sample and is specified as an indicator variable, the Kruskal–Wallis test statistic is

where and (Kruskal and Wallis 1952). The Kruskal–Wallis test statistic for the total number of observations over all samples approximately follows a chi-squared distribution and has a degree of freedom, where should be more than 5 (Hecke 2012). In general, if , where , with k − 1 degrees of freedom, is the tabled value derived from the chi-squared table for a given , a small p-value is assumed to imply that some of the sample median values are different. However, the Kruskal–Wallis test result shows if there are differences among the medians of some of the k groups, but it does not show which groups are different from other groups.

To determine whether groups differ from one another, Bonferroni adjustment can be used. The Bonferroni method is the most frequently applied technique for adjusting for multiplicity since it is uncomplicated (Armstrong 2014). However, the technique is frequently used in research papers to adjust probability values while conducting multiple statistical tests in any context, and this application is generally linked to Dunn (1961). Bonferroni correction was created as a solution to the issue that, as the number of tests increases, so does the probability of a type I error, assuming the existence of a significant difference when it is not present. Generally, the error rate is

where is the critical value and is the total number of tests conducted. The adjusted significance level is utilized in practice as an approximation to the previous calculation (Fernandes and Stone 2011). As a result, the Bonferroni adjustment is applied to the probability values associated with each individual test to maintain a significance level across all tests at 0.05.

4. Results and Discussion

Using the financial data of the analyzed enterprises, the selected indebtedness ratios were calculated (total indebtedness ratio, self-financing ratio, current indebtedness ratio, non-current indebtedness ratio, debt-to-equity ratio, equity leverage ratio, interest coverage ratio, and interest burden ratio) over a 4-year horizon. Table 4 includes their average values.

Table 4.

Four-year average values of indebtedness indicators.

The total indebtedness ratio and the self-financing ratio, which are related indicators, i.e., their sum must equal 1 or 100%, determine the level of coverage required by an enterprise by using equity and debt financing. In general, the total indebtedness ratio indicates the ratio of debt to the total assets of a company, which averaged 0.619 during the period under review, meaning EUR 1 of the total assets of the firm is covered by EUR 0.619 of total liabilities. The level of debt that minimizes capital costs and enhances the firm value is recognized as optimal indebtedness (Johnson and Yushkov 2023). The risk that the company will rely significantly on debt financing as well as its liquidity requirements due to the need to repay the debt are determined by the level of indebtedness. In developed market economies, the optimal level of debt is set in the range of 70–80% (Jencova et al. 2021), and 30–60% in other economies (Kalusova and Badura 2017). One of the most relevant debt ratios, the level of total indebtedness, was previously computed using Slovak market data (Kucera et al. 2021; Valaskova et al. 2018; Stasova 2022; Mazanec 2023). In the Slovak companies operating in the market, the indicator achieved an average value of 63.4%, and the indebtedness was considered optimal. The equity to total assets ratio of the firm determines the self-financing ratio. According to the calculated average values, EUR 1 of the corporate total assets was covered by EUR 0.381 of shareholders’ funds. The ratio should not exceed 20–30% (Basic and Globan 2023). The average self-financing ratio among enterprises operating in Slovakia was slightly higher than the optimal level, and these companies decided to finance their business activities using debt. Due to the complementarity between these ratios, if the total indebtedness ratio increases, the self-financing ratio decreases, and vice versa. In general, it is important to focus on the debt structure by reviewing the partial complementary financial structure criteria of the current indebtedness ratio and the non-current indebtedness ratio if the enterprise largely uses debt for financing. Both indicators show the share of short-term or long-term liabilities of the company in its total assets. According to the financial analysis results that focused on corporate debt, companies financed their business activities during the period under review with 16.2% of long-term debt and 45.7% of short-term debt. The current indebtedness ratio provides information on how much of the corporate debt must be repaid in the current year (Naz and Sheikh 2023). This part of the debt is crucial because it determines whether the firm has sufficient liquidity to repay its current liabilities, which is beneficial to both its investors and creditors (Sardo et al. 2022). The non-current indebtedness ratio is defined as a prolonged liability with a maturity of more than 12 months. The indicator should have a value of 0.5 or less (Dong et al. 2022), but the optimal ratio level depends on the industry. The average indicator value was 46.4%, indicating that the firms were in the optimal range. The debt-to-equity ratio is a crucial indicator in corporate finance since it indicates how long it will take the firm to repay its obligations under the assumption of constant annual cash flow development (Ghardallou 2022). To determine how much leverage a firm is using, the debt-to-equity ratio compares the total liabilities of an enterprise to its equity. The debt-to-equity ratio essentially shows the same thing as the total indebtedness ratio—both grow as debts grow—but, while the total debt grows linearly, the debt ratio grows exponentially. During the period under review, EUR 1 of shareholders’ funds was covered by EUR 2.520 of corporate debt. In most industries, a debt-to-equity ratio in the range of 0.5 to 1.5 is considered optimal. Because a high value of the indicator is frequently related to higher risk, the smaller the ratio, the better (Bhattacharya and Sharma 2019). The significance of the observed ratio increases with the level of corporate debt. A value between 0 and 2.5 is optimal, but a higher value is unfavorable. In the Slovak business environment, the average indicator value slightly exceeds the optimal value (Stefko et al. 2021). Due to the combined use of equity and debt in financing business operations, each enterprise needs to monitor the equity leverage ratio (Gungoraydinoglu and Oztekin 2022). Any enterprise that operates in the market must precisely determine the volume of its debt and its ability to repay it within a particular period of time (Dang 2020). The results revealed that EUR 1 of shareholders’ funds was burdened by EUR 3.520 of the total corporate assets. According to Kengne (2022), if the indicator value is 1, the firm focuses only on equity when financing its business activities. While the range of 2 to 3 is the ideal ratio, an increase in value can be linked to the firm using debt more frequently. The number of enterprises with an equity leverage ratio of 2, i.e., business units in which debt was in proportions of up to 50%, increased during the monitored period. Contrarily, the largest group of firms with a financial leverage of more than 3 gradually declined. This ratio depicts the relationship between the total assets of the enterprise and the part held by shareholders. A value of 4 of the indicator is regarded as optimal when debt financing for business activities is at a level of 75% (Yadav et al. 2020). The indicator, which is the inverted value of the self-financing ratio (Endri et al. 2020), reveals the share of assets covered by equity. The higher this ratio, the higher the share of foreign sources in total financing (Rahmati et al. 2012). Financial independence is generally dependent on the stability and independence of the larger more equity-holding firm (Tarighi et al. 2022). The interest coverage ratio, which monitors the ratio of EBIT to interest paid, is another indicator of indebtedness. It is one of the most important debt ratios as it reveals how often a firm can pay the interest on foreign capital after all costs related to business activities have been covered (Al Amosh et al. 2022). The indicator averaged 13.389 during the period under review. The lower the value, the more the enterprise is burdened with interest costs. The optimal ratio value is five, and it cannot be less than three (Noghondari et al. 2022). The indicator averaged 13.389, implying that a larger coverage ratio is typically preferred. However, the optimal indicator may vary by industry. The interest burden ratio, which is the inverted indicator linked to the interest coverage ratio, represents the share of interest paid by the enterprise in the generated profit. The average value of this indicator was 0.131, and EUR 1 earnings before interest and taxes were covered by EUR 0.131 of interest paid. A high number implies that there is sufficient profit to secure the debt, but it may additionally indicate that the firm does not appropriately use its debt. Hence, the value of the indicator must be less than 100% (Guariglia et al. 2016).

The main objective of a more detailed debt analysis of Slovak enterprises was to identify sectors with homogeneous patterns of indebtedness and determine if there were statistically significant differences in the individual indebtedness indicators depending on the NACE classification or if the individual values of the ratios differed significantly. The normality of the dataset had to be verified by applying the Kolmogorov–Smirnov and Shapiro–Wilk tests, even though the results rejected the assumption that the data had a normal distribution. Subsequently, the cluster analysis was performed after having the descriptive statistics for all ratios to reduce the number of input data. Based on selected descriptive characteristics (such as mean, median, standard deviation, minimum, and maximum) calculated for individual sectors, hierarchical clustering of NACE categories was conducted to detect and identify homogeneous subgroups (clusters) of the monitored set of firms in various economic sectors (classified by NACE). Sectors within a cluster are often comparable based on a particular level of debt, although sectors in diverse clusters have varying debt ratios. Computing the distances between the objects is the clustering principle. In this research paper, Ward’s method and squared Euclidean distance were used.

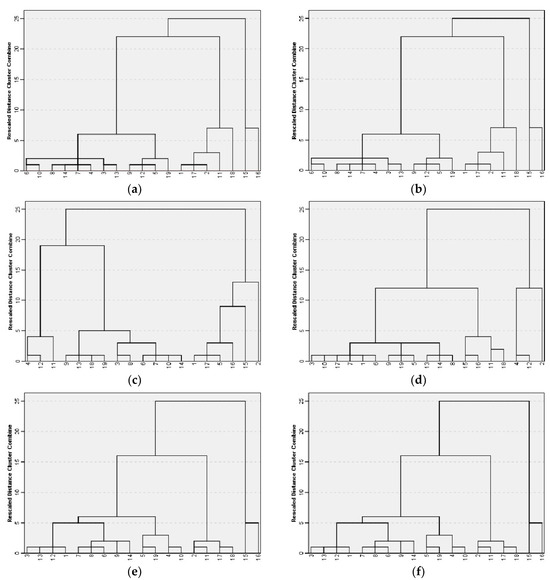

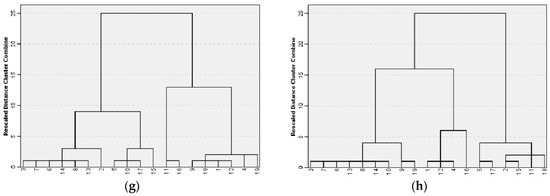

The sectors with comparable debt levels, as determined by selected indebtedness ratios, were identified using the cluster analysis results. Dendrograms present the results of clustering of 19 individual NACE categories for each indebtedness ratio, while the individual NACE categories in the clusters are the most similar within the monitored debt indicator. Conversely, economic sectors in other clusters are heterogeneous. The graph is divided at the tenth Euclidean distance, and thus several basic clusters were formed (Figure 1a–h).

Figure 1.

Dendrograms of individual NACE categories for selected indebtedness ratios. (a) Total indebtedness ratio; (b) self-financing ratio; (c) current indebtedness ratio; (d) non-current indebtedness ratio; (e) debt-to-equity ratio; (f) equity leverage ratio; (g) interest coverage ratio; (h) interest burden ratio. Note: sectors are identified on the horizontal axis by numbers; i.e., 1 is for NACE A, 2 for B, 3 for C, 4 for D, 5 for E, 6 for F, 7 for G, 8 for H, 9 for I, 10 for J, 11 for K, 12 for L, 13 for M, 14 for N, 15 for O, 16 for P, 17 for Q, 18 for R, 19 for S. Source: own elaboration.

In general, the total indebtedness ratio is a crucial indicator of indebtedness, and the clustering of NACE categories according to this debt indicator is presented in Figure 1a. Although financing with debt can increase corporate profitability and thus the payment of its short-term obligations, a large share of debt represents a higher risk for creditors and a lower willingness to provide additional financial sources. An additional one is the self-financing ratio, the change of which depends on the total indebtedness ratio, and the dendrogram focused on the developed clusters according to the NACE categories for this indicator is shown in Figure 1b. Since these are mutually complementary indebtedness indicators, the clusters or economic sectors are also the same. Based on the results of cluster analysis, which are summarized in Table 5, the three basic groups of economic sectors classified by NACE categories were developed. When monitoring the total indebtedness ratio and self-financing ratio, most economic sectors belong to Cluster 1, Cluster 2 is formed by sectors A, B, K, Q, and R, and sectors O and P represent Cluster 3.

Table 5.

Developed clusters of individual NACE categories for total indebtedness ratio and self-financing ratio.

Figure 1c shows the dendrogram in which the economic sectors form clusters according to current indebtedness ratio, and it can be seen that four main clusters were identified. Table 6 summarizes the results of the cluster analysis, focused on identifying sectors with homogeneous patterns of indebtedness when monitoring this debt indicator. Based on the results, it can be summarized that Cluster 1 includes sectors D, K, and L, Cluster 3 is formed by sectors A, E, O, P, and Q, and sector B can be included in Cluster 4. The dendrogram shows that the most numerous homogeneous unit primarily consists of Cluster 2, which includes 10 economic sectors.

Table 6.

Developed clusters of individual NACE categories for current indebtedness ratio.

The results of clustering of NACE categories according to non-current indebtedness ratio are summarized in Figure 1d. When monitoring the non-current indebtedness ratio, four main clusters were formed whose individual sectors are classified in Table 7. The largest group is represented by Cluster 1, created by 12 economic sectors. Cluster 2 includes sectors K, O, P, and R, sectors D and L represent Cluster 3, and, similar to the current indebtedness ratio, sector B can be included in Cluster 4.

Table 7.

Developed clusters of individual NACE categories for non-current indebtedness ratio.

Figure 1e records the clusters of economic sectors in Slovak enterprises by debt-to-equity ratio. Table 8 summarizes the results of the cluster analysis and it is obvious that three main clusters were identified. Similarly to the non-current indebtedness ratio, the dendrogram focused on the debt-to-equity ratio identifies the most economic sectors included in

Table 8.

Developed clusters of individual NACE categories for debt-to-equity ratio.

Cluster 1, which comprises 13 sectors. Cluster 2 consists of sectors B, K, Q, and R, and sectors O and P are integrated in Cluster 3.

The results of clustering of NACE categories according to equity leverage ratio are summarized in Figure 1f. Three main clusters were formed whose individual sectors are classified in Table 9, while they are identically included in the clusters as for the debt-to-equity ratio.

Table 9.

Developed clusters of individual NACE categories for equity leverage ratio.

The clustering of NACE categories according to the level of interest coverage ratio is presented in Figure 1g, while the dendrogram shows that the sectors are also divided into three clusters in this case (Table 10). The dendrogram shows that the most numerous homogeneous unit primarily consists of Cluster 1, which includes 11 economic sectors. Sectors K and P are included in Cluster 2, and Cluster 3 consists of sectors A, D, I, L, R, and S.

Table 10.

Developed clusters of individual NACE categories for interest coverage ratio.

The last monitored indicator is the interest burden ratio, and the results of clustering of NACE categories according to this debt indicator are summarized in Figure 1h. Table 11 identifies the results of the cluster analysis and shows that three main clusters were formed. Even when monitoring the interest burden ratio, the most numerous group of economic sectors is primarily Cluster 1, which includes nine NACE categories. Cluster 2 is formed by sectors A, D, L, and P, and Cluster 3 identified sectors B, E, K, O, Q, and R as having homogeneous patterns of indebtedness.

Table 11.

Developed clusters of individual NACE categories for interest burden ratio.

The cluster analysis results may be considered to have verified that several sectors have considerable similarities in their debt levels. To summarize the findings in response to the research question, the cluster analysis results demonstrate homogeneous patterns of indebtedness across sectors in the Slovak environment. Sectors C—Manufacturing, F—Construction, G—Wholesale and retail trade, repair of motor vehicles/motorcycles, H—Transportation and storage, J—Information and communication, M—Professional, scientific and service activities, and N—Administrative and support service activities are considered a group of NACE activities in which the enterprises are so similar that it is appropriate to evaluate their debt level together using the selected indebtedness ratios. Almost all the sectors belong to the tertiary sector, providing services for people, governments, and other industries. However, the tertiary sector can also include the sectors K—Financial and insurance activities, Q—Human health and social work activities, and R—Arts, entertainment and recreation. According to the cluster analysis results, these sectors are all found in the same cluster when considering not only the total indebtedness and self-financing ratio but also the debt-to-equity ratio, equity leverage, and the interest coverage ratio. While the rural economy has generally been related to the primary sector, the relevance of the latter in terms of GDP and as a provider of employment in rural regions has been declining. In recent decades, the number of Estonian firms of the tertiary sector has exceeded that of primary sector enterprises (Nurmet et al. 2012). The tertiary sector is one of the most significant forms of developed and developing economies (Alshehhi and Popp 2017) because of the proportion of the field of operation and production that it takes up, as well as the importance that it plays in generating employment and the GDP of the country. This is also confirmed by the sample of enterprises in our study as the tertiary sector represents more than half of all the operating enterprises in the market because this sector is considered a key one for economic growth throughout its industries, contributing significantly to the value-added growth and employment growth even in Slovakia. Sakk et al. (2013) focused on financial indicators in Estonian firms developing in the industry in which they operate. Their results reveal that current liabilities and debt increased more quickly than sales, which is typical of a recession. Enterprises in the secondary and tertiary sectors saw a decline in net profit, but, if this trend continues with an increase in debt, the firms could face financial instability. Generally, a firm with sufficient capital, consistent revenue, and a positive net income is more financially secure. The clustering of NACE categories according to the level of the selected indebtedness ratio concluded that sectors C—Manufacturing and E—Water supply; sewerage, waste management, etc., may also be grouped in one cluster (except for the current indebtedness ratio and the interest burden ratio), which form the secondary sector. Most papers on other national economies look at clusters as local concentrations of specific industries, not groups of related industries. Spencer et al. (2010) developed different cluster definitions to find similar results for Canadian data. Aharonson et al. (2014) showed that firms located in strong clusters generate significantly more financial performance than firms in locations without a similar presence of related industries. According to Kincaid (2005), industry clusters provide a wide range of advantages to all participating members, especially efficiency, productivity, and innovation initiatives, thus contributing to the enhancement of financial performance and competitiveness. A broad range of studies look at clusters as well as at many other potential drivers of prosperity differences across economic sectors (Wynn and Jones 2019; Addoum et al. 2023). Porter (2003) found that having economic activity concentrated in strong clusters is significantly more important for prosperity levels for US firms. Spencer et al. (2010) reported similar findings for Canadian data. Martin et al. (2011) empirically analyzed the effect of spatial agglomeration of activities using French firms and found cluster presence to matter more in groups of related industries that use skills extensively. On the contrary, the literature also presents studies that highlight the lack of consistent evidence for the positive impact of clusters on financial performance. Among such studies is Kukalis (2010), which examined the financial performance in the pharmaceutical and computer industries concerning cluster memberships over an extended timeframe, but it failed to demonstrate a positive effect of clusters on financial performance. Similarly, Ruland (2013) reached a similar conclusion when comparing the profitability of US companies within industry clusters and those outside such clusters, taking into account the company’s size. Notably, for small firms, the research revealed that their profitability within clusters is significantly lower than that of non-clustered companies. Conversely, for large companies, no significant difference in performance was identified concerning cluster membership.

However, many researchers have utilized cluster analysis to analyze debt policy in terms of various parameters (Su 2010; Koralun-Bereznicka 2017; Khan et al. 2021; Lukac et al. 2021; Hidayat et al. 2022; Herman et al. 2022). Cluster analysis methods may categorize firms into groups based on the financial strategies they use, as proven by Dzuba and Krylov (2021). Thus, it demonstrates that, while enterprises between classes should be viewed as diverse, homogeneity may be assumed inside these groups. Pivac and Pecariec (2010) used cluster analysis to classify ten countries in transition according to the key indicators of the state and trends in foreign indebtedness. According to Campos and Cysne (2021), a crucial factor in determining the likelihood of a debt default is the link between sovereign risk and the degree of debt. The market discipline hypothesis establishes that the risk premium rises with the debt-to-GDP ratio. However, the research results concluded that those countries whose debt-to-GDP ratio exceeded their limits either had difficulties in obtaining new loans to finance their debt or required assistance from international institutions, as predicted by the strong version of the market discipline hypothesis. Moritz et al. (2016) created an empirical taxonomy of the financing patterns of small- and medium-sized enterprises throughout Europe. The results reveal that financing in Europe is not homogeneous but that different financing patterns exist. Six distinct financing types are identified by the cluster analysis, which differ in the quantity and combinations of the financial instruments used.

After reducing the number of input data to the clusters, the Kruskal–Wallis test was performed to determine if there are statistically significant differences between the calculated ratios related to the economic sector. Table 12 summarizes the outputs of the Kruskal–Wallis test, which examined statistically significant differences in debt ratios concerning NACE categories. Based on the results, there are statistically significant differences between all the indicators of indebtedness.

Table 12.

The output of the Kruskal–Wallis test concerning the NACE categories.

A post hoc analysis was performed as the next step due to significant differences in several indebtedness ratios. When conducting multiple pairwise comparisons across different economic sectors, the likelihood of observing at least one significant result by chance increased, known as the problem of multiple comparisons. The Bonferroni adjustment addressed this issue by lowering the significance level for each test. The Bonferroni correction is considered a conservative approach because it places a stricter criterion on statistical significance. The post hoc analysis results determined whether particular debt ratios concerning the NACE categories were statistically significant. In Table 13, the results of the pairwise comparison of economic sectors are presented. According to the pairwise comparison, analyzing six relevant indicators of indebtedness, Cluster 1 and Cluster 2 differ significantly from each other (except for non-current indebtedness ratio and interest coverage ratio). When monitoring the current indebtedness ratio and non-current indebtedness ratio, statistically significant differences can be identified not only between Cluster 1 and Cluster 3 but also between Cluster 2 and Cluster 3, while the interest coverage ratio and interest burden ratio are also different in these formed clusters. Additionally, Cluster 1 and Cluster 2 differ from Cluster 4 in the non-current indebtedness ratio. In the context of examining differences across economic sectors based on corporate debt level, applying the Bonferroni correction helps in ensuring that any significant findings are less likely to be spurious and are more reliable for drawing meaningful conclusions.

Table 13.

The output of the pairwise comparison concerning the NACE categories.

Decisions regarding the capital structure of companies are strategic decisions, and the consequences appear over a longer time horizon. Therefore, it is necessary to take into account a number of factors when forming it. Numerous studies (Kumar et al. 2017; Ramli et al. 2019; Neykov et al. 2022; Kristofik and Medzihorsky 2022) examined the impact of particular aspects on the corporate capital structure and indebtedness. Enterprises operating in the same sector have a wide range of characteristics, including a tendency to offer comparable goods in the market, structure their production costs similarly, use almost identical technologies, and achieve comparable profitability. The capital structure of the firm reflects these characteristics as well.

Sector characteristics identified in the literature play a significant role in explaining corporate debt levels in other national economies. De Almeida and Tressel (2020) investigated the country and industry determinants of the change in corporate debt level in numerous national economies. The authors concluded that cross-industry differences are also crucial as the retail, telecommunications, transportation, and utilities industries appear more leveraged and less reliant on short-term debt than other sectors. The huge differences in average leverage ratios among industries today are still challenging to be explained clearly (Ross et al. 2016). Except for the insurance and banking sectors, the average industry leverage ratio in the United States from 1999 to 2015 was 25%, ranging from 17% for technological hardware and equipment firms to 50% for real estate investment trusts. Li and Stathis (2017) examined many factors that affect the leverage decisions of Australian publicly traded companies and determined whether these factors are reliably important. Multiple linear panel regressions were used to evaluate the relationship between these variables and the leverage decision. Profitability, log of assets, median industry leverage, industry growth, market-to-book ratio, tangibility, capital expenditure, and investment tax credits belong to a group of eight characteristics identified by the authors as being consistently significant in determining capital structure. Sector classification is a relevant determinant also defined by the results of our study as we pointed out that different industries may exhibit distinct capital structure preferences. Using an extensive sample of enterprises from 37 different countries, Oztekin (2015) investigated the global factors influencing capital structure. The reliable determinants for leverage were not only firm size, tangibility, profits, and inflation but also industry leverage. The impact of the latter on corporate performance was also examined by Chang et al. (2014), who focused on the basic determinants of capital structure in Chinese firms, by Ahsan et al. (2016) and Umeair et al. (2022), who investigated the capital structure of Pakistani listed non-financial firms focused on firm, industry, and country level, and by Sohrabi and Movaghari (2020), who focused on Iranian firms. The impact of corporate and industrial characteristics on the capital structure of small enterprises was investigated by Degryse et al. (2012). According to the authors, growth leads to a rise in long-term debt, while profit specifically lowers short-term debt. They concluded that industry effects play a significant role when considering the corporate capital structure because average debt levels vary between industries. Additionally, there is a significant amount of intra-industry heterogeneity, revealing that both the level of industry competitiveness and the variety of technology used are significant factors in capital structure. Breuer et al. (2023) also claim that various industries exhibit extremely different leverage levels. Therefore, knowing that the literature has extensively investigated the impact of capital structure determinants is not surprising. These investigations have, however, mainly been performed within one industry or using simple industry dummies across industries. Studies have focused on the statistical and economic significance of estimated coefficients but not on the reasons for the difference in leverage, which goes beyond such an analysis, in cases where single industries have not been examined, such as construction (Ruckova and Skulanova 2022), tourism (Athari and Bahreini 2023), manufacturing (Sardo et al. 2022), the financial sector (Boateng et al. 2022), and the non-financial sector (Bazhair and Alshareef 2022; Khan et al. 2023). On the contrary, Yang et al. (2015) concluded that almost all the studies carried out in China regarding debt examinations do not recognize differences among business sectors. The authors presented an in-depth understanding of debt decisions in listed firms in China using a joint model to test the interaction between employee productivity and debt, thus providing a new perspective on investigations regarding the debt decisions of firms across sectors.

5. Conclusions

Since there are statistically significant differences between various industries, many authors are currently investigating the impact of the industry on the financial structure of firms (e.g., in terms of entrepreneurial intention—Cegarra-Navarro et al. 2023, of green public procurement—Lăzăroiu et al. 2020a, and of stakeholder satisfaction and trust—Nemțeanu et al. 2022), revealing the industry as a crucial determinant of corporate indebtedness. This fact is supported by the research paper results, which indicate that significant differences in the financial structures of companies in different industries exist. As a result, it can be concluded that the choice of financial structure is significantly influenced by the industry.

Thus, to identify sectors with homogeneous patterns of indebtedness and to understand which sectors are the most stable and independent, the main aim of this paper was to determine the debt level in the Slovak environment on a sample of 4237 enterprises from different sectors as well as to recognize relationships between them. Using Ward’s hierarchical clustering method with squared Euclidean distance, the sectors with comparable debt levels determined by selected indebtedness ratios were identified. To summarize the findings in response to the research question, the cluster analysis findings indicate homogeneous patterns of indebtedness across sectors in Slovakia. Sectors C—Manufacturing, F—Construction, G—Wholesale and retail trade, repair of motor vehicles/motorcycles, H—Transportation and storage, J—Information and communication, M—Professional, scientific and service activities, and N—Administrative and support service activities are regarded as a group of NACE activities in which enterprises are sufficiently comparable such that it is appropriate to evaluate their debt levels together using the selected indebtedness ratios. Most sectors provide services to people, governments, and other industries as part of the tertiary sector. However, the tertiary sector can also include the sectors K—Financial and insurance activities, Q—Human health and social work activities, and R—Arts, entertainment and recreation, all found in the same cluster. Sectors C—Manufacturing and E—Water supply; sewerage, waste management, etc., may also be grouped in one cluster (except for the current indebtedness ratio and the interest burden ratio), forming the secondary sector, according to the clustering of NACE categories regarding the level of the selected indebtedness ratio. The Kruskal–Wallis test confirmed that there are statistically significant differences between all the indicators of indebtedness related to the NACE categories after reducing the amount of input data to the clusters.

The research presented in this paper extends the literature on corporate finance in several ways: (i) firms within sectors identified with specific debt levels can make more informed strategic decisions, while understanding the clustering patterns allows for targeted planning, resource allocation, and risk management strategies tailored to the financial characteristics of their sector; (ii) recognizing the debt clustering within sectors enables companies to assess and manage industry-specific risks more effectively; and (iii) sector-specific clustering information serves as a benchmark for companies to compare their debt levels and financial practices against industry averages, and this benchmarking can guide companies in setting realistic financial goals and performance expectations.

This study is useful in helping governments, shareholders, and company owners understand how the economic sector affects corporate indebtedness. Investors and lenders can use the clustering insights to make more informed investment and lending decisions. However, understanding the debt dynamics within sectors provides valuable insights into the risk–return profiles of different industries, aiding in portfolio management and credit risk assessment. Even policymakers can use the findings to develop targeted policies that address the specific needs and challenges of sectors with distinct debt levels, which can include designing industry-specific financial regulations and support programs or incentives to promote responsible financial practices. Firms can leverage the knowledge of clustering sectors based on debt levels for competitive positioning. Understanding how debt practices vary across sectors allows companies to benchmark their financial strategies against industry norms and make adjustments to enhance competitiveness. In general, sectors with similar debt profiles can explore collaboration opportunities because sharing best practices, industry-specific challenges, and financial strategies within clustered sectors can foster collaboration and mutual support among companies facing common financial dynamics. The research outputs identified the industries with the highest and lowest levels of debt across the Slovak business environment. The key relevance of our findings is the benchmark of selected sectors from the perspective of indebtedness, which can be used to further assess its growth in each of the V4 nations, which we feel is a crucial area for the expansion of the European economy as a whole.

Despite the contribution of this paper to the existing literature, the following limitations need to be highlighted. The extent of relevance of the findings is constrained by the scope of the paper. Since research may be constrained by a limited time horizon and extending the analysis over a longer period could provide a more comprehensive understanding of trends, future research should examine this phenomenon over a longer time horizon than that configured for this research. While experimenting with multiple clustering algorithms and comparing their performance on a dataset is often a prudent approach to finding the most suitable method for summarizing similarities across corporate indebtedness in various sectors, the use of another clustering method can also be considered a future direction of research because relying solely on hierarchical clustering may overlook nuances captured by alternative clustering methods, potentially limiting the robustness of the results. In order to determine if there might be differences in the findings and to enable greater generalization and applicability, future research should examine this phenomenon in all the sectors of the national economy in Slovakia.

Author Contributions

Conceptualization, D.G. and K.V; methodology, K.V., D.G. and G.L.; software, K.V.; validation, D.G. and G.L.; formal analysis, K.V. and D.G.; investigation, D.G. and G.L.; resources, G.L.; data curation, K.V. and D.G.; writing—original draft preparation, D.G. and K.V.; writing—review and editing, D.G., K.V. and G.L.; visualization, D.G.; supervision, K.V and D.G.; project administration, D.G. and K.V.; funding acquisition, G.L. and K.V. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the faculty institutional research 1/KE/2023: The use of quantitative methods to assess the impact of the latest crisis on the performance of business entities in V4 countries at the Faculty of Operation and Economics of Transport and Communications, University of Zilina, Slovakia.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding authors.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Addoum, Jawad M., Stefanos Delikouras, Da Ke, and George M. Korniotis. 2023. Industry Clusters and the Geography of Portfolio Choice. Journal of Financial and Quantitative Analysis, 1–33. [Google Scholar] [CrossRef]

- Adjei, Raymond Kofi, and Libor Grega. 2023. Economic growth effects of de facto and de jure trade globalization in ECOWAS. Journal of Competitiveness 15: 18–35. [Google Scholar] [CrossRef]

- Afzal, Saima, Ayesha Afzal, Muhammad Amin, Sehar Saleem, Nouman Ali, and Muhammad Sajid. 2021. A Novel Approach for Outlier Detection in Multivariate Data. Mathematical Problems in Engineering 2021: 1899225. [Google Scholar] [CrossRef]

- Aharonson, Barak, Joel Baum, and Maryann Feldman. 2014. Industrial Clustering and Innovative Output. In Innovation and IT in an International Context. London: Palgrave Macmillan, pp. 65–81. [Google Scholar]

- Ahmad, Issam Abdo, and Ali Fakih. 2022. Does the legal form matter for firm performance in the MENA region? Annals of Public and Cooperative Economics 93: 205–27. [Google Scholar] [CrossRef]

- Ahmed, Naveed, and Talat Afza. 2019. Capital structure, competitive intensity and firm performance: Evidence from Pakistan. Journal of Advances in Management Research 16: 796–813. [Google Scholar] [CrossRef]

- Ahsan, Tanveer, Man Wang, and Muhammad Azeem Qureshi. 2016. Firm, industry, and country level determinants of capital structure: Evidence from Pakistan. South Asian Journal of Global Business Research 5: 362–84. [Google Scholar] [CrossRef]

- Al Amosh, Hamzeh, Saleh Khatib, and Khaled Hussainey. 2022. The Financial Determinants of Integrated Reporting Disclosure by Jordanian Companies. Journal of Risk and Financial Management 15: 375. [Google Scholar] [CrossRef]