The Content Scope of Airline Sustainability Reporting According to the GRI Standards—An Assessment for Europe’s Five Largest Airline Groups

Abstract

1. Introduction

2. Literature

2.1. Sustainability and Corporate Social Responsibility

2.2. Sustainability Reporting

2.3. Sustainability (Reporting) and Aviation

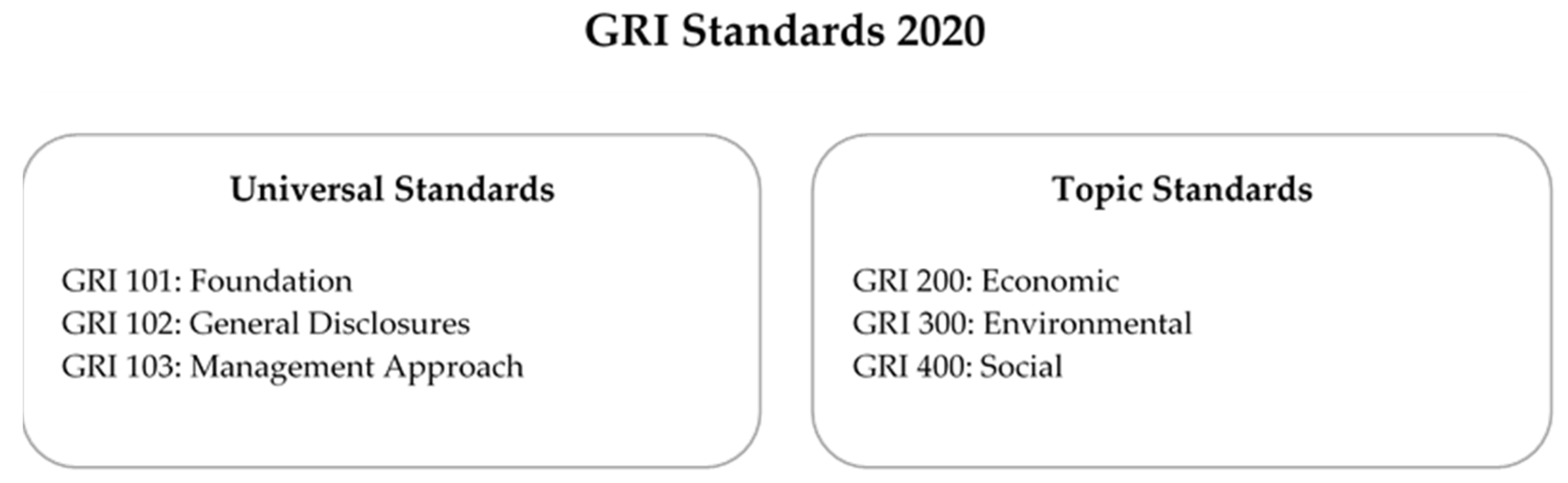

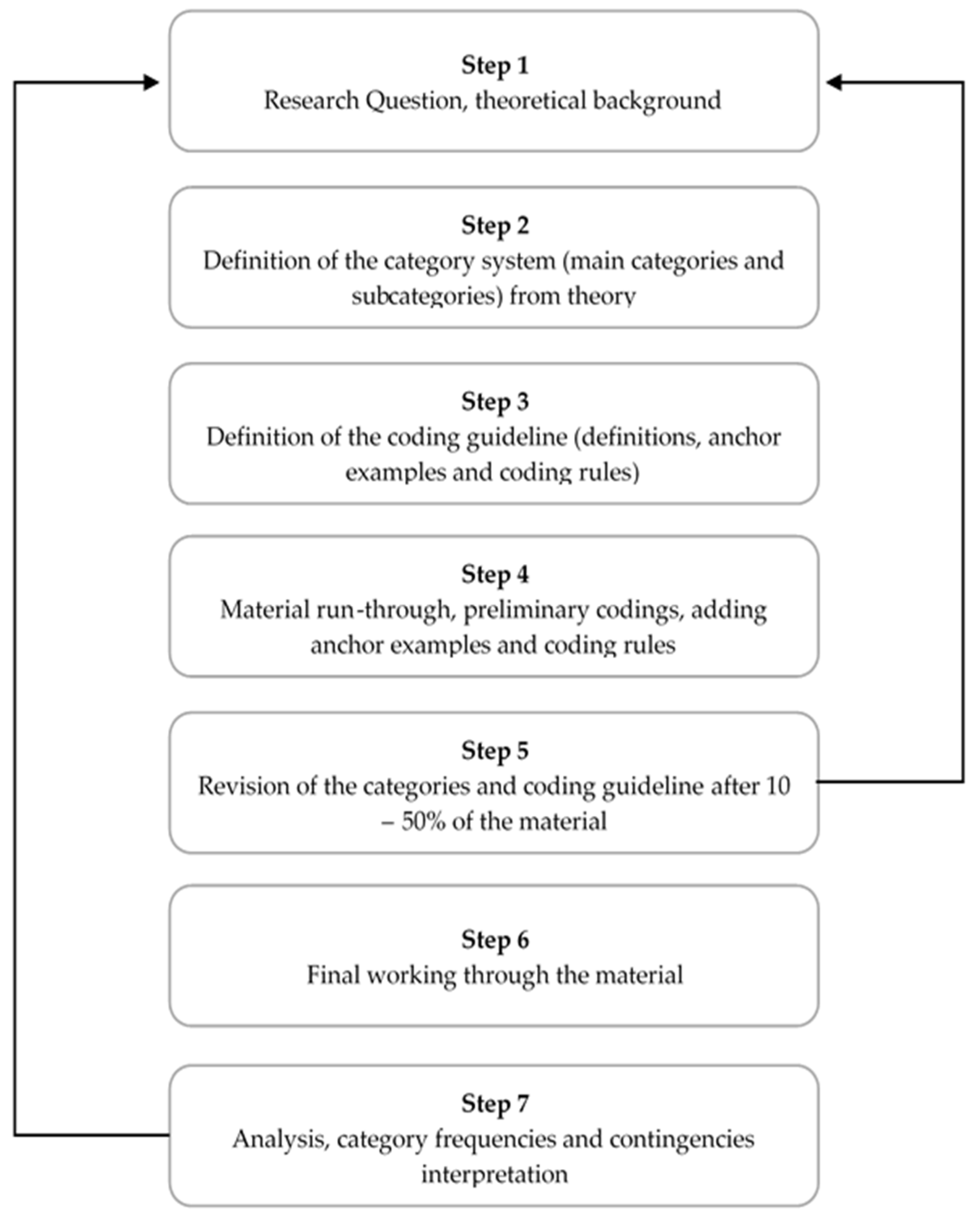

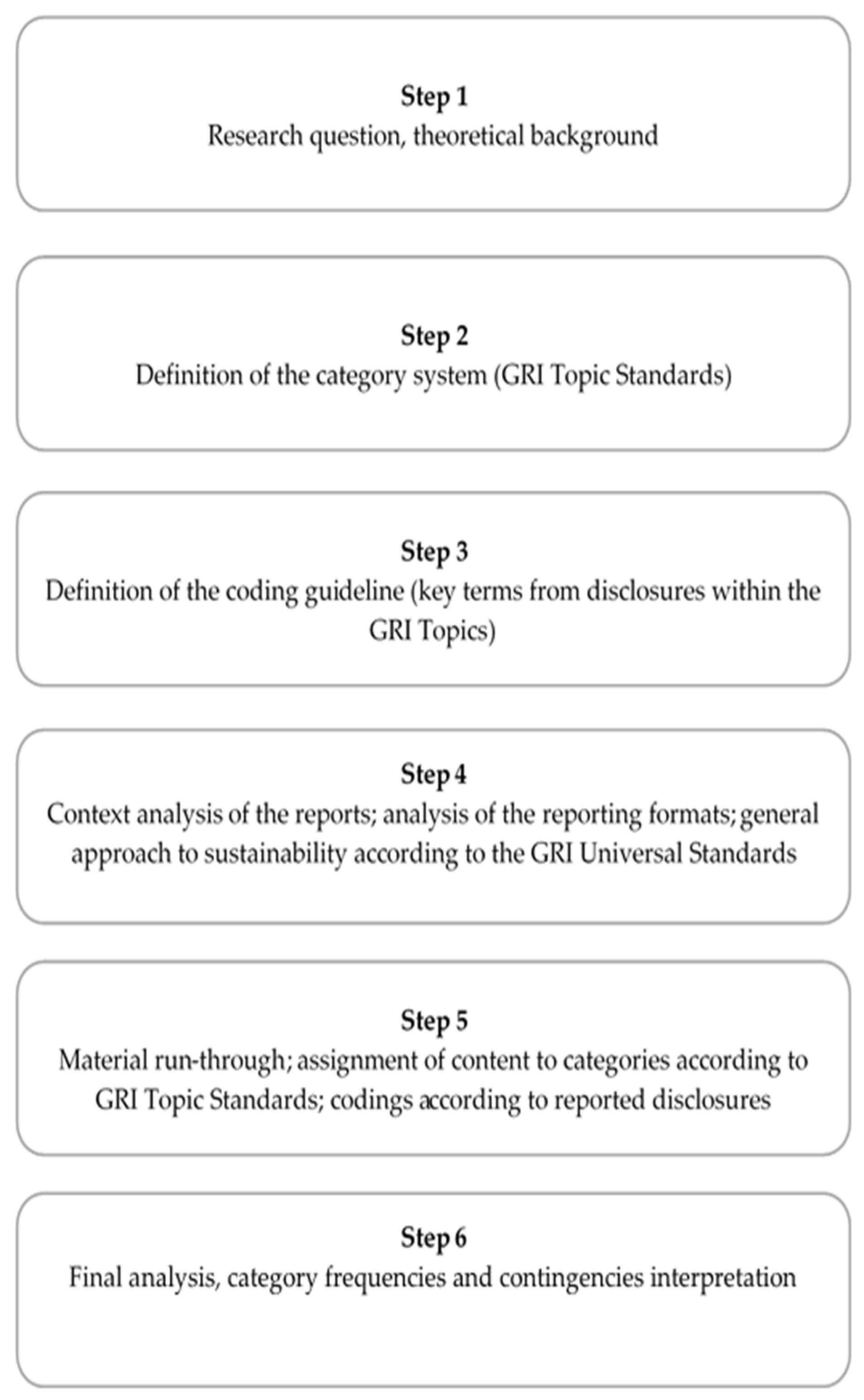

3. Methodology

3.1. Research Objects

- (Air France-KLM 2019). Air France-KLM takes care: Sustainability Report 2018.

- (EasyJet 2019). The Warmest Welcome in the Sky: Annual Report and Accounts 2018.

- (International Airlines Group 2019). Consolidated statement of non-financial information.

- (Lufthansa Group 2019). Balance. Sustainability Report 2019.

- (Ryanair 2019). Annual Report 2019.

3.2. Content Analysis

4. Results

4.1. Reporting Approaches and Formats

4.2. GRI 200 (Economic)

4.3. GRI 300 (Environmental)

4.4. GRI 400 (Social)

4.5. Discussion

5. Conclusions, Recommendations and Limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | See https://www.lufthansagroup.com/de/verantwortung/berichte.html (accessed on 25 December 2022). |

References

- Ahlgren, Linnea. 2021. EU Concerned About Austria’s Minimum Air Fare Policy. Simple Flying. February 4. Available online: https://simpleflying.com/austria-minimum-air-fare-concern/ (accessed on 10 November 2022).

- Air France-KLM. 2019. Air-France KLM Takes Care: Sustainability Report 2018. Available online: https://www.avionews.com/resources/6954063100c07782165d586efd1b5b5d.pdf (accessed on 20 December 2022).

- ATAG–Air Transport Action Group. 2020. Aviation Benefits beyond Borders. Available online: https://aviationbenefits.org/media/167517/aw-oct-final-atag_abbb-2020-publication-digital.pdf (accessed on 25 December 2022).

- BDL. 2019. Report 2019: Luftfahrt und Wirtschaft. Available online: https://www.bdl.aero/wp-content/uploads/2019/05/Report-Luftfahrt-und-Wirtschaft-2019.pdf (accessed on 22 April 2022).

- Belobaba, Peter, Amedeo Odoni, and Cynthia Barnhart. 2016. The Global Airline Industry, 2nd ed. Hoboken: Wiley. [Google Scholar]

- Burghouwt, Guillaume, and Renato Redondi. 2013. Connectivity in Air Transport Networks: An Assessment of Models and Applications. Journal of Transport Economics and Policy 47: 35–53. [Google Scholar]

- Carbo, Jose M., and Daniel J. Graham. 2020. Quantifying the impacts of air transportation on economic productivity: A quasi-experimental causal analysis. Economics of Transportation 24: 100195. [Google Scholar] [CrossRef]

- Chapman, Alex, Leo Murray, Griffin Carpenter, Christiane Heisse, and Lydia Prieg. 2021. A Frequent Flyer Levy. New Economics Foundation. Available online: https://neweconomics.org/2021/07/a-frequent-flyer-levy (accessed on 10 November 2022).

- Charpentreau, Clement. 2022. Will France ban private jet flying? Aerotime Hub. August 26. Available online: https://www.aerotime.aero/articles/32014-will-france-ban-private-jet-flying (accessed on 10 November 2022).

- Chiaramonti, David. 2019. Sustainable Aviation Fuels: The challenge of decarbonization. Energy Procedia 158: 1202–7. [Google Scholar] [CrossRef]

- Connelly, Brian L., S. Trevis Certo, R. Duane Ireland, and Christopher R. Reutzel. 2011. Signaling Theory: A Review and Assessment. Journal of Management 37: 39–67. [Google Scholar] [CrossRef]

- Cooper, Adrian, and Phil Smith. 2005. The Economic Catalytic Effects of Air Transport in Europe, Oxford: Eurocontrol Experimental Centre. Available online: https://www.eurocontrol.int/archive_download/all/node/9840 (accessed on 10 November 2022).

- Cunningham, Ed. 2022. Could short-haul flights soon be banned in Europe? TimeOut. April 7. Available online: https://www.timeout.com/news/could-short-haul-flights-soon-be-banned-in-europe-040622 (accessed on 10 November 2022).

- EasyJet. 2019. The Warmest Welcome in the Sky: Annual Report and Accounts 2018. Available online: https://corporate.easyjet.com/~/media/Files/E/Easyjet/pdf/investors/results-centre/2018/2018-annual-report-and-accounts.pdf (accessed on 22 April 2022).

- European Commission. 2006. Implementing the Partnership for Growth and Jobs: Making Europe a Pole of Excellence on Corporate social Responsibility. Available online: https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX:52006DC0136:EN:HTML (accessed on 22 April 2022).

- European Commission. 2019. The European Green Deal. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1588580774040&uri=CELEX%3A52019DC0640 (accessed on 22 April 2022).

- European Commission. 2021. ‘Fit for 55 ’: Delivering the EU’s 2030 Climate Target on the Way to Climate Neutrality. Available online: https://ec.europa.eu/info/sites/default/files/chapeau_communication.pdf (accessed on 22 April 2022).

- European Commission. n.d.a Corporate Sustainability Reporting. Available online: https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en (accessed on 10 November 2022).

- European Commission. n.d.b Reducing Emissions from Aviation. Available online: https://ec.europa.eu/clima/policies/transport/aviation_en (accessed on 22 April 2022).

- European Parliament. 2022. Aviation’s Contribution to European Union Climate Action–Revision of EU ETS as Regards Aviation, Briefing, EU Legislation in Progress, Brussels. Available online: https://www.europarl.europa.eu/RegData/etudes/BRIE/2022/698882/EPRS_BRI(2022)698882_EN.pdf (accessed on 22 April 2022).

- Freeman, R. Edward, and David L. Reed. 1983. Stockholders and Stakeholders: A New Perspective on Corporate Governance. California Management Review 25: 88–106. [Google Scholar] [CrossRef]

- Gély, Denis, and Ferenc Márki. 2022. Understanding the Basics of Aviation Noise. In Aviation Noise Impact Management. Cham: Springer. [Google Scholar]

- Global Reporting Initiative. 2020. Consolidated Set of the GRI Standards 2020. Available online: https://www.globalreporting.org/how-to-use-the-gri-standards/resource-center/ (accessed on 3 June 2022).

- Global Reporting Initiative. n.d.a Our Mission and History. Available online: https://www.globalreporting.org/about-gri/mission-history/ (accessed on 10 November 2022).

- Global Reporting Initiative. n.d.b A Short Introduction to the GRI Standards. Available online: https://www.globalreporting.org/media/wtaf14tw/a-short-introduction-to-the-gri-standards.pdf (accessed on 10 November 2022).

- Graf, Luca. 2005. Incompatibilities of the low-cost and network carrier business models within the same airline grouping. Journal of Air Transport Management 11: 313–27. [Google Scholar] [CrossRef]

- Graver, Brandon, Dan Rutherford, and Sola Zheng. 2020. CO2 Emissions from Commercial Aviation: 2013, 2018, and 2019. Available online: https://theicct.org/publication/co2-emissions-from-commercial-aviation-2013-2018-and-2019/ (accessed on 3 June 2022).

- Greenpeace. 2021. Get On Track: Train alternatives to short-haul flights in Europe. Briefing. October 27. Available online: https://www.greenpeace.org/eu-unit/issues/climate-energy/45898/get-on-track-train-alternatives-to-short-haul-flights-in-europe/ (accessed on 31 August 2022).

- Hametner, Markus. 2021. Was ein Verbot von Kurzstreckenflügen wirklich Bringen Würde. Available online: https://www.sueddeutsche.de/politik/kurzstreckenfluege-klimaschutz-verbote-datenanalyse-1.5330637?reduced=true (accessed on 22 April 2022).

- Homburg, Christian, Marcel Stierl, and Torsten Bornemann. 2013. Corporate Social Responsibility in Business-to-Business Markets: How Organizational Customers Account for Supplier Corporate Social Responsibility Engagement. Journal of Marketing 77: 54–72. [Google Scholar] [CrossRef]

- IATA. 2020. Annual Review 2020. Available online: https://www.iata.org/contentassets/c81222d96c9a4e0bb4ff6ced0126f0bb/iata-annual-review-2020.pdf (accessed on 3 June 2022).

- IATA. n.d. Net Zero 2050: Sustainable Aviation Fuels. Available online: https://www.iata.org/en/iata-repository/pressroom/fact-sheets/fact-sheet---alternative-fuels/ (accessed on 4 September 2022).

- International Airlines Group. 2019. Consolidated Statement of Non-Financial Information. Available online: https://www.iairgroup.com/~/media/Files/I/IAG/annual-reports/2018-statement-of-non-financial-information-en.pdf (accessed on 22 April 2022).

- International Organization for Standardization. 2010. ISO 26000 Guidance on social Responsibility. Available online: https://www.iso.org/files/live/sites/isoorg/files/store/en/PUB100258.pdf (accessed on 30 August 2022).

- Janić, Milan. 2016. The Sustainability of Air Transportation: A Quantitative Analysis and Assessment. New York: Routledge. [Google Scholar]

- Johansson, Eljas. 2022. An Analysis of Sustainability Reporting Practices of the Global Airline Industry. Paper presented at the 5th International Conference on Tourism Research, Porto, Portugal, May 19–20; pp. 507–16. Available online: https://papers.academic-conferences.org/index.php/ictr/article/view/234/271 (accessed on 25 December 2022).

- Kilic, Merve, Ali Uyar, and Abdullah S. Karaman. 2019. What impacts sustainability reporting in the global aviation industry? An institutional perspective. Transport Policy 79: 54–65. [Google Scholar] [CrossRef]

- Lawton, Thomas C. 2002. Cleared for Take-Off: Structure and Strategy in the Low-Fare Airline Business. London: Routledge. [Google Scholar]

- LeBlanc, Brendan, Jennifer Leitsch, and Rick Pearl. 2021. The evolution of sustainability reporting. The Corporate Citizen 35: 32–35. Available online: https://bc-ccc.uberflip.com/i/1344292-corporatecitizen-issue35-2021/33? (accessed on 25 December 2022).

- Lee, David, David W. Fahey, Piers M. Forster, Peter J. Newton, Ron C.N. Wit, Ling L. Lim, Bethan Owen, and Robert Sausen. 2009. Aviation and global climate change in the 21st century. Atmospheric Environment 43: 3520–37. [Google Scholar] [CrossRef] [PubMed]

- Leipold, Alexandra, Gubaz Aptsiauri, Amir Ayazkhani, Uwe Bauder, Richard-Gregor Becker, Ralf Berghof, Axel Claßen, Alireza Dadashi, Katrin Dahlmann, Niclas Dzikus, and et al. 2021. DEPA 2050: Development Pathways for Aviation up to 2050. Available online: https://elib.dlr.de/142185/1/DEPA2050_StudyReport.pdf (accessed on 22 April 2022).

- Lufthansa Group. 2019. Balance. Sustainability Report 2019. Available online: https://www.lufthansagroup.com/media/downloads/en/responsibility/LH-sustainability-report-2019.pdf (accessed on 22 April 2022).

- Mayring, Philipp. 2014. Qualitative Content Analysis: Theoretical Foundations, Basic Procedures and Soft-Ware Solution. Available online: https://nbn-resolving.org/urn:nbn:de:0168-ssoar-395173 (accessed on 22 April 2022).

- Mayring, Philipp. 2015. Qualitative Inhaltsanalyse: Grundlagen und Techniken, 12th ed. Weinheim and Basel: Beltz Verlag. [Google Scholar]

- Meadows, Donella H., Dennis L. Meadows, Jørgen Randers, and William W. Behrens, III. 1972. The Limits to Growth: A Report for the Club of Rome’s Project on the Predicament of Mankind. New York: Universe Books. [Google Scholar]

- Morlotti, Chiara, Mattia Cattaneo, Paolo Malighetti, and Renato Redondi. 2017. Multi-dimensional price elasticity for leisure and business destinations in the low-cost air transport market: Evidence from easyJet. Tourism Management 61: 23–34. [Google Scholar] [CrossRef]

- Porter, Michael E., and Mark R. Kramer. 2011. Creating Shared Value. Harvard Business Review 89: 62–77. [Google Scholar]

- Ryanair. 2019. Annual Report 2019. Available online: https://investor.ryanair.com/wp-content/uploads/2019/07/Ryanair-2019-Annual-Report.pdf (accessed on 22 April 2022).

- Scheelhaase, Janina, Sven Maertens, and Wolfgang Grimme. 2019. Synthetic fuels in aviation. Current barriers and potential political measures. Transportation Research Procedia 43: 21–30. [Google Scholar] [CrossRef]

- Scheelhaase, Janina, Marc Gelhausen, and Sven Maertens. 2020. How would ambitious CO2 prices affect air transport? Transportation Research Procedia 52: 428–36. [Google Scholar] [CrossRef]

- Schuurman, Richard. 2021. EU Stakeholders Fear ‘Carbon Leakage’. Available online: https://airinsight.com/eu-stakeholders-fear-carbon-leakage/ (accessed on 22 April 2022).

- Wappelhorst, Annika. 2020. How Did Flight Shame Become a Societal Issue in Germany and Sweden? Medium.com. September 24. Available online: https://medium.com/climate-conscious/how-did-flight-shame-become-a-societal-issue-in-germany-and-sweden-138740288a8 (accessed on 7 December 2022).

- Wittman, Michael D. 2014. Are low-cost carrier passengers less likely to complain about service quality? Journal of Air Transport Management 35: 64–71. [Google Scholar] [CrossRef]

- World Commission on Environment and Development. 1987. Our Common Future. Available online: https://sustainabledevelopment.un.org/content/documents/5987our-common-future.pdf (accessed on 22 April 2022).

- Yang, Lu, Cindy S. B. Ngai, and Wenze Lu. 2020. Changing trends of corporate social responsibility reporting in the world-leading airlines. PLoS ONE 15: 1–19. [Google Scholar] [CrossRef] [PubMed]

- Zhang, Fangni, and Daniel J. Graham. 2020. Air transport and economic growth: A review of the impact mechanism and causal relationships. Transport Reviews 40: 506–28. [Google Scholar] [CrossRef]

- Zhang, Xing. 2021. Communicating social responsibilities through CSR reports: Comparative study of top European and Asia-Pacific airlines. PLoS ONE 16: 1–14. [Google Scholar] [CrossRef] [PubMed]

- Zhang, Chi, Xin Hui, Yuzhen Lin, and Chih-Jen Sung. 2016. Recent development in studies of alternative jet fuel combustion: Progress, challenges, and opportunities. Renewable and Sustainable Energy Reviews 54: 120–38. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Airline Group | RPK * | Associated Carriers (FSNC, Regional) (RPK *) | Associated Carriers (LCC, Holiday) (RPK *) |

|---|---|---|---|

| Air France-KLM | 55,808 | Air France (15,051) KLM Royal Dutch Airlines (12,851) KLM Cityhopper (6469) | Transavia Airlines (12,958) HOP! (4300) Transavia France (5948) Joon (1730) |

| easyJet | 87,347 | n/a | easyJet Airline Company (87,347) |

| IAG | 85,249 | British Airways (22,033) Iberia (9723) Air Nostrum (2819) BA Cityflyer (1980) Sun Air Of Scandinavia (87) | Vueling Airlines (30,283) Aer Lingus (9898) Iberia Express (7001) Anisec (Level) (1426) |

| Lufthansa Group | 71,605 | Deutsche Lufthansa (26,086) SWISS (7626) Austrian Airlines (5910) Brussels Airlines (5890) Lufthansa CityLine (3564) Air Dolomiti (1284) | Eurowings (10,062) Germanwings (4899) Eurowings Europe (4535) Edelweiss Air (2022) SunExpress Deutschland (826) |

| Ryanair | 125,202 | n/a | Ryanair (117,824) Laudamotion (5661) Malta Air (1523) Ryanair UK (171) Ryanair Sun (23) |

| LHG | IAG | AF-KLM | RYR | EZY | |

|---|---|---|---|---|---|

| Standalone Sustainability Report | X | -- | X | -- | -- |

| Non-Financial Statement | X | X | X | X | X |

| Page count of main sustainability publication | 138 pages | 56 pages | 148 pages | 7 pages | 10 pages |

| Materiality Analysis | X | X | X | -- | -- |

| GRI Reference | X | X | X | -- | -- |

| GRI Content Index | X | X | -- | -- | -- |

| GRI 200 ECONOMIC | LHG | AF-KLM | IAG | EZY | RYR |

|---|---|---|---|---|---|

| 201 Economic Performance | |||||

| 201-1 Direct economic value generated and distributed | X | X | X | X | X |

| 201-2 Financial implications and other risks and opportunities due to climate change | X | X | X | X | |

| 201-3 Defined benefit plan obligations and other retirement plans | |||||

| 201-4 Financial assistance received from government | |||||

| 202 Market Presence | |||||

| 202-1 Ratios of standard entry-level wage by gender compared to local minimum wage | |||||

| 202-2 Proportion of senior management hired from the local community | X | ||||

| 203 Indirect Economic Impacts | |||||

| 203-1 Infrastructure investments and services supported | X | ||||

| 203-2 Significant indirect economic impacts | X | X | |||

| 204 Procurement Practices | |||||

| 204-1 Proportion of spending on local suppliers | X | ||||

| 205 Anti-corruption | |||||

| 205-1 Operations assessed for risks related to corruption | X | X | |||

| 205-2 Communication and training about anti-corruption policies and procedures | X | X | X | X | X |

| 205-3 Confirmed incidents of corruption and actions taken | X | ||||

| 206 Anti-competitive Behaviour | |||||

| 206-1 Legal actions for anti-competitive behavior, anti-trust, and monopoly practices | |||||

| 207 Tax | |||||

| 207-1 Approach to tax | X | ||||

| 207-2 Tax governance, control, and risk management | X | ||||

| 207-3 Stakeholder engagement and management of concerns related to tax | |||||

| 207-4 Country-by-country reporting | X | X |

| GRI 300 ENVIRONMENTAL | LHG | AF-KLM | IAG | EZY | RYR |

|---|---|---|---|---|---|

| 301 Materials | |||||

| 301-1 Materials used by weight or volume | X | X | |||

| 301-2 Recycled input materials used | |||||

| 301-3 Reclaimed products and their packaging materials | |||||

| 302 Energy | |||||

| 302-1 Energy consumption within the organization | X | X | X | ||

| 302-2 Energy consumption outside of the organization | |||||

| 302-3 Energy intensity | X | X | X | X | |

| 302-4 Reduction of energy consumption | X | X | X | X | X |

| 302-5 Reductions in energy requirements of products and services | X | X | X | X | X |

| 303 Water and Effluents | |||||

| 303-1 Interactions with water as a shared resource | |||||

| 303-2 Management of water discharge-related impacts | X | ||||

| 303-3 Water withdrawal | |||||

| 303-4 Water discharge | |||||

| 303-5 Water consumption | X | ||||

| 304 Biodiversity | |||||

| 304-1 Operational sites owned, leased, managed in, or adjacent to, protected areas and areas of high biodiversity value outside protected areas | |||||

| 304-2 Significant impacts of activities, products, and services on biodiversity | X | ||||

| 304-3 Habitats protected or restored | X | ||||

| 304-4 IUCN Red List species and national conservation list species with habitats in areas affected by operations | |||||

| 305 Emissions | |||||

| 305-1 Direct (Scope 1) GHG emissions | X | X | X | X | X |

| 305-2 Energy indirect (Scope 2) GHG emissions | X | X | X | ||

| 305-3 Other indirect (Scope 3) GHG emissions | X | X | X | ||

| 305-4 GHG emissions intensity | X | X | X | X | X |

| 305-5 Reduction of GHG emissions | X | X | X | X | X |

| 305-6 Emissions of ozone-depleting substances (ODS) | |||||

| 305-7 Nitrogen oxides (NOx), sulfur oxides (SOx), and other significant air emissions | X | X | X | ||

| 306 Waste | |||||

| 306-1 Waste generation and significant waste-related impacts | X | X | |||

| 306-2 Management of significant waste-related impacts | X | X | X | X | X |

| 306-3 Waste generated | X | X | |||

| 306-4 Waste diverted from disposal | X | X | X | ||

| 306-5 Waste directed to disposal | |||||

| 307 Environmental Compliance | |||||

| 307-1 Non-compliance with environmental laws and regulations | |||||

| 308 Supplier Environmental Assessment | |||||

| 308-1 New suppliers that were screened using environmental criteria | X | X | X | ||

| 308-2 Negative environmental impacts in the supply chain and actions taken | X |

| GRI 400 SOCIAL | LHG | AF-KLM | IAG | EZY | RYR |

|---|---|---|---|---|---|

| 401 Employment | |||||

| 401-1 New employee hires and employee turnover | X | ||||

| 401-2 Benefits provided to full-time employees that are not provided to temporary or part-time employees | |||||

| 401-3 Parental leave | X | X | |||

| 402 Labor/Management Relations | |||||

| 402-1 Minimum notice periods regarding operational changes | X | ||||

| 403 Occupational Health and Safety | |||||

| 403-1 Occupational health and safety management system | X | X | X | X | X |

| 403-2 Hazard identification, risk assessment, and incident investigation | X | X | |||

| 403-3 Occupational health services | X | X | |||

| 403-4 Worker participation, consultation, and communication on occupational health and safety | X | X | |||

| 403-5 Worker training on occupational health and safety | X | X | X | X | |

| 403-6 Promotion of worker health | X | X | X | X | |

| 403-7 Prevention and mitigation of occupational health and safety impacts directly linked by business relationships | |||||

| 403-8 Workers covered by an occupational health and safety management system | X | X | X | ||

| 403-9 Work-related injuries | X | X | |||

| 403-10 Work-related ill health | |||||

| 404 Training and Education | |||||

| 404-1 Average hours of training per year per employee | X | X | |||

| 404-2 Programs for upgrading employee skills and transition assistance programs | X | X | X | X | |

| 404-3 Percentage of employees receiving regular performance and career development reviews | X | X | |||

| 405 Diversity and Equal Opportunity | |||||

| 405-1 Diversity of governance bodies and employees | X | X | X | X | X |

| 405-2 Ratio of basic salary and remuneration of women to men | X | X | X | ||

| 406 Non-discrimination | |||||

| 406-1 Incidents of discrimination and corrective actions taken | |||||

| 407 Freedom of Association and Collective Bargaining | |||||

| 407-1 Operations and suppliers in which the right to freedom of association and collective bargaining may be at risk | X | X | |||

| 408 Child Labor | |||||

| 408-1 Operations and suppliers at significant risk for incidents of child labor | |||||

| 409 Forced or Compulsory Labor | |||||

| 409-1 Operations and suppliers at significant risk for incidents of forced or compulsory labor | X | ||||

| 410 Security Practices | |||||

| 410-1 Security personnel trained in human rights policies or procedures | |||||

| 411 Rights of Indigenous People | |||||

| 411-1 Incidents of violations involving rights of indigenous peoples | |||||

| 412 Human Rights Assessment | |||||

| 412-1 Operations that have been subject to human rights reviews or impact assessments | X | X | |||

| 412-2 Employee training on human rights policies or procedures | X | X | X | X | |

| 412-3 Significant investment agreements and contracts that include human rights clauses or that underwent human rights screening | X | X | |||

| 413 Local Communities | |||||

| 413-1 Operations with local community engagement, impact assessments, and development programs | X | X | X | X | X |

| 413-2 Operations with significant actual and potential negative impacts on local communities | X | X | X | X | X |

| 414 Supplier Social Assessment | |||||

| 414-1 New suppliers that were screened using social criteria | X | X | X | X | |

| 414-2 Negative social impacts in the supply chain and actions taken | X | X | |||

| 415 Public Policy | |||||

| 415-1 Political contributions | X | X | |||

| 416 Customer Health and Safety | |||||

| 416-1 Assessment of the health and safety impacts of product and service categories | X | X | X | X | X |

| 416-2 Incidents of non-compliance concerning the health and safety impacts of products and services | |||||

| 417 Marketing and Labeling | |||||

| 417-1 Requirements for product and service information and labeling | |||||

| 417-2 Incidents of non-compliance concerning product and service information and labeling | |||||

| 417-3 Incidents of non-compliance concerning marketing communications | |||||

| 418 Customer Privacy | |||||

| 418-1 Substantiated complaints concerning breaches of customer privacy and losses of customer data | X | ||||

| 419 Socioeconomic Compliance | |||||

| 419-1 Non-compliance with laws and regulations in the social and economic area |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rüger, M.; Maertens, S.U. The Content Scope of Airline Sustainability Reporting According to the GRI Standards—An Assessment for Europe’s Five Largest Airline Groups. Adm. Sci. 2023, 13, 10. https://doi.org/10.3390/admsci13010010

Rüger M, Maertens SU. The Content Scope of Airline Sustainability Reporting According to the GRI Standards—An Assessment for Europe’s Five Largest Airline Groups. Administrative Sciences. 2023; 13(1):10. https://doi.org/10.3390/admsci13010010

Chicago/Turabian StyleRüger, Martin, and Sven Ulrich Maertens. 2023. "The Content Scope of Airline Sustainability Reporting According to the GRI Standards—An Assessment for Europe’s Five Largest Airline Groups" Administrative Sciences 13, no. 1: 10. https://doi.org/10.3390/admsci13010010

APA StyleRüger, M., & Maertens, S. U. (2023). The Content Scope of Airline Sustainability Reporting According to the GRI Standards—An Assessment for Europe’s Five Largest Airline Groups. Administrative Sciences, 13(1), 10. https://doi.org/10.3390/admsci13010010