The Costs of Ambiguity in Strategic Contexts

Abstract

:1. Introduction

1.1. Related Literature

1.2. Conceptualizing Ambiguity

When Is Ambiguity Strategically Interesting?

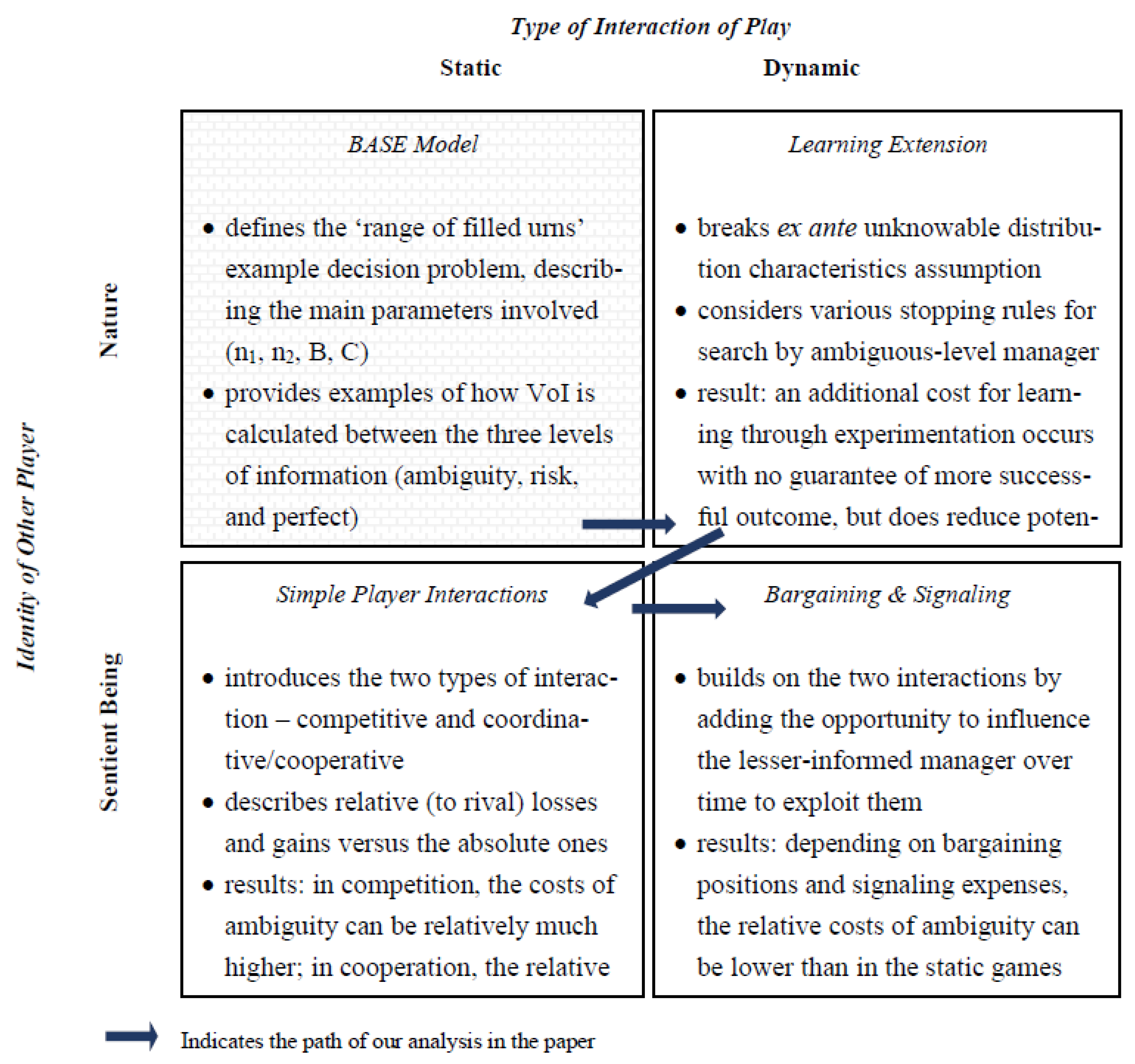

1.3. Structuring the Analysis along Game Theoretic Dimensions

1.4. A Simple Model of Ambiguity for Analysis

1.5. The Value of Information and Its Levels

- Ambiguity is the range (from 0 to n2) that n1 could occupy, where the distribution of the values over that range is unknowable, at least ex ante. Ambiguity implies a range of possible payoffs. At worst, it is harmful and costs ‘(n2 − n1)·C’ if one were to choose every empty urn to draw from and no others. At best, it is beneficial and pays off ‘n1·(B − C)’ if one were to draw only from full urns. However, for ambiguity, n1 is unknown, and so the possible payoff range faced by the entrepreneurial manager effectively spans from ‘−n2·C’ to ‘+n2·(B − C)’, from the case where she tries all urns and they are all empty to the case where they are all full.

- Risk is often defined as knowing, objectively, all of a factor’s future outcome-states and their probabilities beforehand (e.g., Knight 1921). It is equivalent to knowing n1 (or the distribution characteristics from which n1 is drawn) in this model. The expected payoff is precise; it is simply ‘max [0; n1·B − n2·C]’. It is straightforward to prove that the best strategy to play when ‘n1·B − n2·C > 0′ is all-in, and otherwise, it is all-out8. Thus, the expected payoff is, in the worst case, the opportunity cost and, in the best case (i.e., when n1 = n2), is ‘n2·(B − C)’.

- Perfect Information is often defined as knowing the future with accuracy (i.e., knowing which outcome will occur, with certainty). This implies not only knowing n1, but also knowing each specific location that will provide success (i.e., knowing which specific urns contain a ball), ex ante. The value of perfect information is equal to ‘n1·(B − C)’. If we assume that n1 can take on any number in the range, then this certain payoff also includes the opportunity cost level (i.e., when n1 = 0) in addition to the maximum payoff ‘n2·(B − C)’ level (i.e., occurring when n1 = n2).

2. Model Analysis

2.1. The First Cost in Terms of the Maximum Willingness to Pay for Better Information

- when incremental information increases the lower bound to rule out any potential losses;

- when incremental information decreases the upper bound to rule out any potential gains; and

- when incremental information constricts the range to decrease either the maximum potential losses or the maximum potential gains. In case (i), to the manager who would have gone all-out, the additional information is worth, at most, ‘n2·(B − C)’, which is the maximum potential gain that would have been missed. In case (ii), to the manager who would have gone all-in, the additional information is worth, at most, ‘n2·C’, which is the maximum potential loss avoided.

2.2. The Second Cost in Terms of How Information Directs Action

2.3. What Happens When Dynamics Occur?

2.4. The Third Cost in Terms of Playing against a Second Sentient Party

2.4.1. The Analysis of Static Games Involving a Rival

2.4.2. The Analysis of Dynamic Games Involving a Rival

3. Discussion

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | In this paper, ambiguity is the Ellsbergian (1961) type. It is a form of Knightian uncertainty where only the range of possible future outcome-states is known; nothing else about the distribution of probabilities for any outcome-state is known. |

| 2 | This perspective differs from the mainstream, experimental lens that instead seeks to explain human behavior in lab settings, focusing on the heuristics used and biased revealed. The approach we use here could be labeled more as ‘rational’—borrowing from the game theory versus behavioral theory dichotomy, although that would depend on one’s definition of rational (Gilboa and Schmeidler 2001). |

| 3 | Note that we are not suggesting that every ambiguity problem is represented in our basic model, just as not every game is represented by a prisoner’s dilemma model; what we are suggesting is that new and non-specific insights can emerge from analyzing a single decision model, sufficient to make a contribution to the literature, just as so many game theory papers based on the analysis of single games have in the past. |

| 4 | Ambiguity-as-range is a more realistic modeling of what highly uncertain business decisions look like than alternatives. For example, assuming an unbounded distribution of outcome payoffs is less credible because infinite losses and gains do not exist in the real world (e.g., due to bankruptcy laws and budget constraints). Assuming either unknowable possible outcomes or their payoff levels is also less realistic, as their modeling is equivalent to the unbounded distribution alterative. (Note that other ambiguity range types can exist, but probability is the most researched—Aggarwal and Mohanty 2021). |

| 5 | Other strategic decision-making problems exist under ambiguity that we do not consider here, given the focus here is on costs of ambiguity. For example, if all players in a competitive game were equally ignorant about the outcomes, then there are standard heuristics that work effectively for the player currently in the lead. The sailing tactic of imitating every move of the second place player, who is also making adjustments to the same unpredictable shifting winds, often works to keep the lead. |

| 6 | Perhaps the best-known reference to ambiguity is the Ellsberg paradox (Ellsberg 1961), where an urn contains 90 balls, 30 red and the rest (60) either blue or green in color, and experimental subjects are asked to make choices over possible bets on the outcomes of drawing a ball from the urn. The ambiguity is the range from 0 to 60 balls that the non-red balls could span. It should be noted, however, that the paradox actually relies upon a very specific construction of ambiguity—i.e., that a given ambiguity (say, about the green-colored balls) has an available complement—the one provided by the blue-colored balls—providing a way to reduce the ambiguity to certainty (e.g., bet on blue-or-green). In this note, we have explicitly assumed that the given ambiguity is irreducible. |

| 7 | Note that there is a near-infinite number of alternative specifications of decision problems that involve ambiguity. This is because the range of parameter values across the possible relevant dimensions (e.g., of the payoffs, the outcome states, and the possible choices) of such a problem is large. And that number does not even consider the large array of possible ways to model the bounded rationality of players, or their possible initial beliefs, incentives and decision-making processes. |

| 8 | The optimization problem that indicates what probability (p) to play in order to maximize payoffs when playing against nature (which sets its probability of a full urn to ‘n1/n2’) leads to the strategy to set p equal to 1 when ‘n1/n2 > C/B’, and to 0 otherwise. |

| 9 | Such an asymmetry (i.e., of the possibility of a relatively catastrophic loss) may be the basis for an additional ambiguity-avoidance bias in human decision-making behavior (e.g., Ellsberg 1961). Besides the standard ambiguity-avoidance bias arising from the discomfort of not knowing the mean of the distribution, and the bias in over-weighting potential regular losses relative to gains arising from risk (e.g., Kahneman and Tversky 1979), and possibly the asymmetrical weighting under ambiguity described by the decision weight model in venture theory (e.g., Hogarth and Einhorn 1990), there may be this additional bias that could be teased out in future lab experiments regarding potential losses that are greater than the apparent stakes. |

| 10 | The manager faces a gross cost of ‘n2·C’ whenever the opportunity is entered but only a gross benefit of ‘n1·B’. Given ‘n2 > n1’, the highest rate of return on altering one of the known factors (either C or B) to the manager with ambiguity-level information comes from reducing C. Note that this investment would only be made when the manager believed entering is a good choice. |

| 11 | Additional informational precision can provide added benefits in the real world as well. For example, when two receptive product markets or two gushing oil-drilling locations (i.e., two ‘full’ urns) are geographically close and known ahead of time, then many costly redundancies can be eliminated by sharing activities across the locations (e.g., marketing campaigns, training and refining facilities, transportation hubs). Other scale, scope and synergy economies may also be possible when the locations that pay off (i.e., the ‘full’ urns) are known ahead of striking them. |

| 12 | The learning functions we describe involve ‘triggers’ that are activated by updated information, mostly to call for a stop to further experimentation. In our simple dynamic model, there is no time value of money or scale economies or threats of rivals competing in the landscape. When that is not the case, a manager may wish to accelerate the learning (e.g., by making multiple urn-draws per period). This possibility provides a basis for a real-world prediction that a minimal level of consistent initial success in an ambiguous context will more likely lead to an acceleration of entrepreneurial action. |

| 13 | Lost benefits to the partner in cooperative interactions are another potential cost of ambiguity. These occur when the less-informed manager does not play the optimal strategy. |

| 14 | As with the static cooperative game, there exists an apparent identifiable optimal strategy for the less-informed manager to take when there are only two firms in the game as we have assumed; and, that is to refuse to take any bargain and then to go all-in. That assures the less-informed manager half of whatever net payoff exists when the more-informed manager correctly enters the opportunity. However, if there is more than one less-informed firm in the pool for the one more-informed manager to bargain with, then the more-informed manager is likely to be successful at bargaining and in shifting the less-informed firm’s resource benefits to her firm. |

| 15 | Ambiguity is always the most costly information level in games against sentient rivals, absolutely and relatively, with those maximum potential relative losses increasing in the size of n2 and most often in the size of B as well. |

| 16 | We have assumed that ambiguity involves a range that is big. Future work could examine at what point the range becomes small enough to be considered ‘non-strategic’. This is interesting because the range is actually a collapsible construct that, in its shrinking limit, must end in point precision (i.e., compressing into the discrete expected factor value). |

| 17 | Such work may provide further examples of where ambiguity is beneficial. For example, for some specifications of ignorance, predictable mistakes that are made based on not knowing can actually increase payoffs, relative to knowing more and not making those mistakes. |

References

- Aggarwal, Divya, and Pitabas Mohanty. 2021. Influence of imprecise information on risk and ambiguity preferences: Experimental evidence. Managerial and Decision Economics 43: 1025–38. [Google Scholar] [CrossRef]

- Anderson, Axel, and Lones Smith. 2008. The Durable Information Monopolist. Available online: http://economics.uwo.ca/newsletter/misc/2008/anderson_dec8.pdf (accessed on 21 January 2018).

- Arend, Richard J. 2020. Strategic decision-making under ambiguity: A new problem space and a proposed optimization approach. Business Research 13: 1231–51. [Google Scholar] [CrossRef]

- Arend, Richard J. 2022. Strategic decision-making under ambiguity: Insights from exploring a simple linked two-game model. Operational Research, 1–17. [Google Scholar] [CrossRef]

- Bhattacharjee, Swagata. 2022. Dynamic contracting for innovation under ambiguity. Games and Economic Behavior 132: 534–52. [Google Scholar] [CrossRef]

- Cerreia-Vioglio, Simone, Fabio Maccheroni, Massimo Marinacci, and Luigi Montrucchio. 2013. Ambiguity and robust statistics. Journal of Economic Theory 148: 974–1049. [Google Scholar] [CrossRef]

- Courtney, Hugh, Jane Kirkland, and Patrick Viguerie. 1997. Strategy under uncertainty. Harvard Business Review 75: 67–79. [Google Scholar]

- Dimov, Dimo. 2010. Nascent entrepreneurs and venture emergence: Opportunity confidence, human capital, and early planning. Journal of Management Studies 47: 1123–53. [Google Scholar] [CrossRef]

- Dubin, Robert. 1969. Theory Building. New York: Free Press. [Google Scholar]

- Einhorn, Hillel J., and Robin M. Hogarth. 1986. Decision making under ambiguity. The Journal of Business 59: S225–S250. [Google Scholar] [CrossRef]

- Ellsberg, Daniel. 1961. Risk, Ambiguity, and the Savage Axioms. Quarterly Journal of Economics 75: 643–69. [Google Scholar] [CrossRef]

- Farrell, Joseph. 1987. Cheap talk, coordination, and entry. The RAND Journal of Economics 18: 34–39. [Google Scholar] [CrossRef]

- Forbes, Daniel P. 2007. Reconsidering the strategic implications of decision comprehensiveness. Academy of Management Review 32: 361–76. [Google Scholar] [CrossRef]

- Gader, Paul, Magdi Mohamed, and Jung-Hsien Chiang. 1995. Comparison of crisp and fuzzy character neural networks in handwritten word recognition. IEEE Transactions on Fuzzy Systems 3: 357–63. [Google Scholar] [CrossRef]

- Ghemawat, Pankaj. 1991. Commitment. New York: Simon and Schuster. [Google Scholar]

- Ghirardato, Paulo, Fabio Maccheroni, and Massimo Marinacci. 2004. Differentiating ambiguity and ambiguity attitude. Journal of Economic Theory 118: 133–73. [Google Scholar] [CrossRef]

- Gilboa, Itzhak, and David Schmeidler. 1989. Maxmin Expected Utility With Non-Unique Prior. Journal of Mathematical Economics 18: 141–53. [Google Scholar] [CrossRef]

- Gilboa, Itzhak, and David Schmeidler. 2001. A Theory of Case-Based Decisions. Cambridge: Cambridge University Press. [Google Scholar]

- Gollier, Chrsitian. 2014. Optimal insurance design of ambiguous risks. Economic Theory 57: 555–76. [Google Scholar] [CrossRef]

- Heath, Chip, and Amos Tversky. 1991. Preference and belief: Ambiguity and competence in choice under uncertainty. Journal of Risk and Uncertainty 4: 5–28. [Google Scholar] [CrossRef]

- Hirshleifer, Jack. 1971. The private and social value of information and the reward to inventive activity. The American Economic Review 61: 561–74. [Google Scholar]

- Hogarth, Robin M., and Hillel J. Einhorn. 1990. Venture theory: A model of decision weights. Management Science 36: 780–803. [Google Scholar] [CrossRef]

- Howard, Ronald A. 1966. Information value theory. IEEE Transactions on Systems Science and Cybernetics 2: 22–26. [Google Scholar] [CrossRef]

- Johannisson, Bengt, and Mette Monsted. 1997. Contextualizing entrepreneurial networking: The case of Scandinavia. International Studies of Management and Organization 27: 109–36. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 1979. Prospect theory: An analysis of decision under risk. Econometrica 47: 263–91. [Google Scholar] [CrossRef]

- Kane, Edward J. 2004. Continuing dangers of disinformation in corporate accounting reports. Review of Financial Economics 13: 149–64. [Google Scholar] [CrossRef] [Green Version]

- Klibanoff, Peter, Massimo Marinacci, and Sujoy Mukerji. 2005. A smooth model of decision making under ambiguity. Econometrica 73: 1849–92. [Google Scholar] [CrossRef]

- Knight, Frank H. 1921. Risk, Uncertainty, and Profit. Boston: Houghton Mifflin. [Google Scholar]

- Kuechle, Graciela, Beatrice Boulu-Reshef, and Sean D. Carr. 2016. Prediction-and control-based strategies in entrepreneurship: The role of information. Strategic Entrepreneurship Journal 10: 43–64. [Google Scholar] [CrossRef]

- Leiblein, Michael J., Jeffrey J. Reuer, and Todd Zenger. 2018. What Makes a Decision Strategic? Strategy Science 3: 558–73. [Google Scholar] [CrossRef]

- Lund, Anne K. 2019. Leading knowledge-workers through situated ambiguity. Scandinavian Journal of Management 35: 101060. [Google Scholar] [CrossRef]

- Maccheroni, Fabio, Massimo Marinacci, and Aldo Rustichini. 2006. Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica 74: 1447–98. [Google Scholar] [CrossRef]

- Machina, Mark J. 2014. Ambiguity Aversion with Three or More Outcomes. American Economic Review 104: 3814–40. [Google Scholar] [CrossRef]

- March, James G. 1994. Primer on Decision Making: How Decisions Happen. New York: Simon and Schuster. [Google Scholar]

- McMullen, Jeffery. S., and Dean A. Shepherd. 2006. Entrepreneurial action and the role of uncertainty in the theory of the entrepreneur. Academy of Management Review 31: 132–52. [Google Scholar] [CrossRef]

- Mintzberg, Henry. 1978. Patterns in strategy formation. Management Science 24: 934–48. [Google Scholar] [CrossRef]

- Petkova, Antoaneta P., Anu Wadhwa, Xin Yao, and Sanjay Jain. 2014. Reputation and Decision Making Under Ambiguity: A Study of U.S. Venture Capital Firms’ Investments in the Emerging Clean Energy Sector. Academy of Management Journal 57: 422–48. [Google Scholar] [CrossRef]

- Raiffa, Howard, and Robert O. Schlaifer. 1961. Applied Statistical Decision Theory. Cambridge: Graduate School of Business Administration, Harvard University. [Google Scholar]

- Rich, Patricia. 2021. The key to the knowledge norm of action is ambiguity. Synthese 199: 9669–98. [Google Scholar] [CrossRef]

- Rumelt, Richard P., Dan E. Schendel, and David J. Teece. 1994. Fundamental Issues in Strategy: A Research Agenda. Boston: Harvard Business School Press. [Google Scholar]

- Runge, Michael C., Sarah J. Converse, and James E. Lyons. 2011. Which uncertainty? Using expert elicitation and expected value of information to design an adaptive program. Biological Conservation 144: 1214–23. [Google Scholar] [CrossRef]

- Sakhartov, Arkadiy V. 2018. Stock market undervaluation of resource redeployability. Strategic Management Journal 39: 1059–82. [Google Scholar] [CrossRef]

- Savage, Leonard J. 1954. The Foundations of Statistics. New York: Wiley. [Google Scholar]

- Schmeidler, David. 1989. Subjective probability and expected utility without additivity. Econometrica 57: 571–87. [Google Scholar] [CrossRef]

- Srivastava, Sameer B. 2015. Intraorganizational Network Dynamics in Times of Ambiguity. Organization Science 26: 1365–80. [Google Scholar] [CrossRef]

- Sull, Donald N. 2004. Disciplined entrepreneurship. MIT Sloan Management Review 46: 71–77. [Google Scholar]

- Townsend, David M., Richard A. Hunt, Jeffery S. McMullen, and Saras D. Sarasvathy. 2018. Uncertainty, knowledge problems, and entrepreneurial action. Academy of Management Annals 12: 659–87. [Google Scholar] [CrossRef]

- Tversky, Amos, and Daniel Kahneman. 1992. Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty 5: 297–323. [Google Scholar] [CrossRef]

{kind=link}

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Arend, R.J. The Costs of Ambiguity in Strategic Contexts. Adm. Sci. 2022, 12, 108. https://doi.org/10.3390/admsci12030108

Arend RJ. The Costs of Ambiguity in Strategic Contexts. Administrative Sciences. 2022; 12(3):108. https://doi.org/10.3390/admsci12030108

Chicago/Turabian StyleArend, Richard J. 2022. "The Costs of Ambiguity in Strategic Contexts" Administrative Sciences 12, no. 3: 108. https://doi.org/10.3390/admsci12030108

APA StyleArend, R. J. (2022). The Costs of Ambiguity in Strategic Contexts. Administrative Sciences, 12(3), 108. https://doi.org/10.3390/admsci12030108