What Role Do Design Factors Play in Applying Performance Measurement Systems in Nonprofit Organizations?

, ,

, ,

Abstract

1. Introduction

What role do design factors play in applying performance measurement systems in nonprofit organizations?

2. Theoretical Background

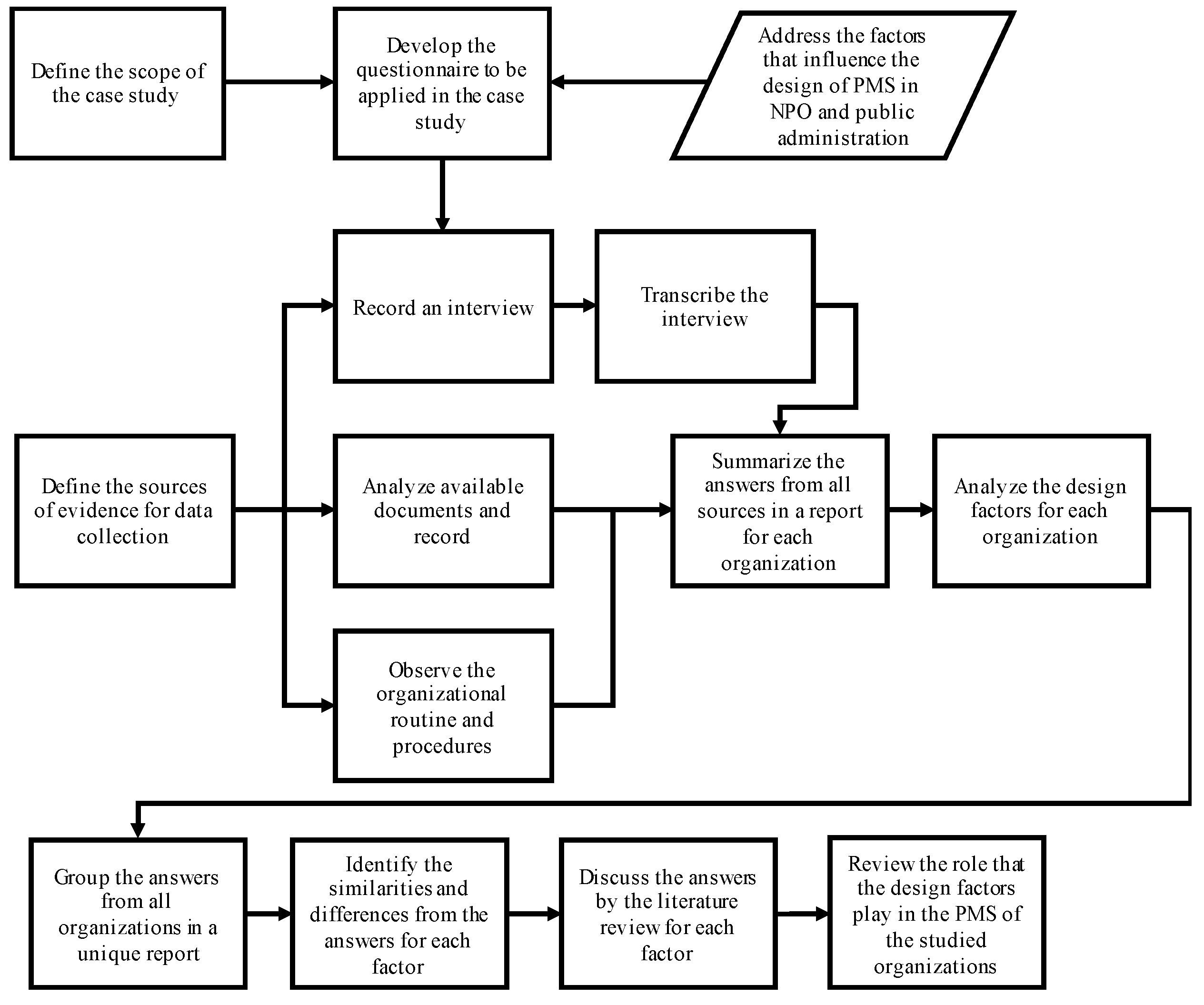

3. Research Design, Materials, and Methods

- -

- Prioritize the social mission;

- -

- Use the PM for making decision;

- -

- Should have implemented a new/redesigned PMS.

4. Results and Discussion

4.1. Overview of the Organizations

4.2. Main Outputs and Discussion

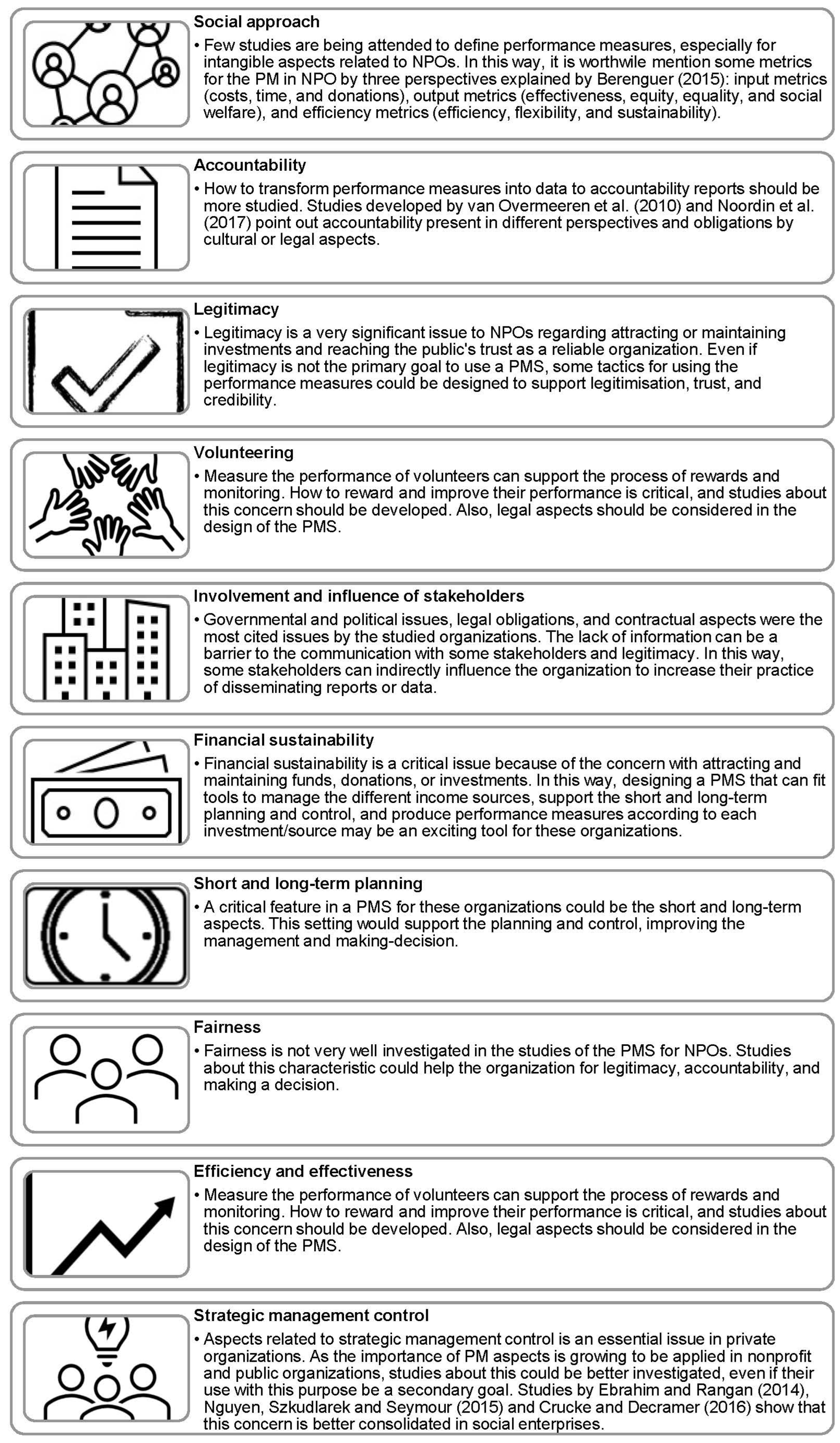

- What role does the “social approach” play in the PMSs applications in the studied NPOs?

- What role does “accountability” play in the PMSs applications in the studied NPOs?

- What role does the “legitimacy” play in the PMSs applications in the studied NPOs?

- What role does “volunteering” play in the PMSs applications in the studied NPOs?

- What role does the “involvement and influence of stakeholders” play in PMSs applications in the studied NPOs?

- What role does “financial sustainability” play in the PMSs applications in the studied NPOs?

- What role does the “short and long-term planning” play in the PMSs applications in the studied NPOs?

- What role does “fairness” play in the PMSs applications in the studied NPOs?

- What role does the “efficiency and effectiveness” play in the PMSs applications in the studied NPOs?

- What role does the “strategic management control” play in the PMSs applications in the studied NPOs?

4.3. Concerns, Insights, and Future Research Issues

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Group | Factor | Questions |

|---|---|---|

| Purpose | Social approach | How are the social value and impact evaluated? Are the community interests analysed and transformed into performance indicators? How? How do you assess if the mission is being accomplished? |

| Stakeholders | Accountability | Are the data on performance measurement communicated externally? How? Is the information generated in the system/spreadsheets used for accountability to stakeholders? How? |

| Legitimacy | Does the data generated and reported through the system contribute to the organization’s legitimacy? Does the use of the system have this purpose? | |

| Volunteering | Is there access/metric/evaluation developed for volunteers? Which are they? | |

| Involvement and influence of stakeholders | How can the PM be influenced by the difference of interests and metrics for different stakeholders? Has the system any adaptation in its design to meet some stakeholder requirements? | |

| Management | Financial sustainability | Does the PMS manage the different sources of income? |

| Short and long-term planning | How does the system consider goals and outcomes for the short and long term? Was there any system/spreadsheets/procedures adaptation to meet a short or long-term request by a stakeholder? | |

| Fairness | Does the organization meet some inter-local equity requirements? If yes, how is this procedure? | |

| Efficiency and effectiveness | How is efficiency measured? Are the criteria to measure results well-established in the PMS? How do you evaluate effectiveness? Does PM consider intangible results? If yes, how? How to indicate a positive result, although the financial impact does not show it? What are the difficulties in measuring performance and working with these data? Does the PMS allow for monitoring and generating performance reports? | |

| Strategic management control | Is the PMS available for use at all levels of the organization? Is the system developed to support learning and continuous improvement in the organization? |

References

- Amado, Carla Alexandra da Encarnação Fili, and Sérgio Pereira dos Santos. 2009. Challenges for performance assessment and improvement in primary health care: The case of the Portuguese health centres. Health Policy 91: 43–56. [Google Scholar] [CrossRef] [PubMed]

- Anonymous. 2020. Research from Brazil provides framework to design performance measurement systems (PMS) in non-profit and public administration organizations. Human Resource Management International Digest 28: 29–31. [Google Scholar] [CrossRef]

- Arena, Marika, Giovanni Azzone, and Irene Bengo. 2015. Performance Measurement for Social Enterprises. VOLUNTAS: International Journal of Voluntary and Non-Profit Organizations 26: 649–72. [Google Scholar] [CrossRef]

- Arvidson, Malin, and Fergus Lyon. 2014. Social Impact Measurement and Non-profit Organisations: Compliance, Resistance, and Promotion. Voluntas: International Journal of Voluntary and Non-profit Organizations 25: 869–86. [Google Scholar] [CrossRef]

- Balabonienė, Ingrida, and Giedrė Večerskienė. 2015. The Aspects of Performance Measurement in Public Sector Organization. Procedia—Social and Behavioral Sciences 213: 314–20. [Google Scholar] [CrossRef]

- Barratt, Mark, Thomas Y. Choi, and Mei Li. 2011. Qualitative case studies in operations management: Trends, research outcomes, and future research implications. Journal of Operations Management 29: 329–42. [Google Scholar] [CrossRef]

- Berman, Margo. 2014. Productivity in Public and Non-Profit Organizations, 2nd ed. New York: Routledge. [Google Scholar]

- Bititci, Umit S. 2015. Managing Business Performance: The Science and the Art. Chichester: John Wiley & Sons. [Google Scholar]

- Bracci, Enrico, Laura Maran, and Robert Inglis. 2017. Examining the process of performance measurement system design and implementation in two Italian public service organizations. Financial Accountability & Management in Governments, Public Services and Charities 33: 406–42. [Google Scholar]

- Cestari, José Marcelo Almeida Prado, Edson Pinheiro de Lima, Fernando Deschamps, Eileen Morton Van Aken, Fernanda Treinta, and Louisi Francis Moura. 2018. A case study extension methodology for performance measurement diagnosis in non-profit organizations. International Journal of Production Economics 203: 225–38. [Google Scholar] [CrossRef]

- Cestari, Jose Marcelo Almeida Prado, Fernanda Tavares Treinta, Louisi Francis Moura, Juliano Munik, Edson Pinheiro de Lima, Fernando Deschamps, Sergio E. Gouvea da Costa, Eileen M. Van Aken, Luciana Rosa Leite, and Rafael Duarte. 2021. The characteristics of non-profit performance measurement systems. Total Quality Management & Business Excellence 2021: 1–31. [Google Scholar] [CrossRef]

- Clark, Cheryl, and Linda Brennan. 2012. Entrepreneurship with social value: A conceptual model for performance measurement. Academy of Entrepreneurship Journal 18: 17–40. [Google Scholar]

- Cnaan, Ram A., and Toni A. Cascio. 1998. Performance and Commitment: Issues in management of volunteers in human service organizations. Journal of Social Service Research 24: 1–37. [Google Scholar] [CrossRef]

- Conaty, Frank J. 2012. Performance management challenges in hybrid NPO/public sector settings: An Irish case. International Journal of Productivity and Performance Management 61: 290–309. [Google Scholar] [CrossRef]

- Connolly, Ciaran, and Martin Kelly. 2011. Understanding accountability in social enterprise organisations: A framework. Social Enterprise Journal 7: 224–37. [Google Scholar] [CrossRef]

- Conrad, Lynne, and Pinar Guven Uslu. 2012. UK health sector performance management: Conflict, crisis and unintended consequences. Accounting Forum 36: 231–50. [Google Scholar] [CrossRef]

- Cordery, Carolyn, and Rowena Sinclair. 2013. Measuring performance in the third sector. Qualitative Research in Accounting & Management 10: 196–212. [Google Scholar]

- Crucke, Saskia, and Adelien Decramer. 2016. The Development of a Measurement Instrument for the Organizational Performance of Social Enterprises. Sustainability 8: 161. [Google Scholar] [CrossRef]

- Daff, Lyn, and Lee D. Parker. 2021. A conceptual model of accountants’ communication inside not-for-profit organisations. The British Accounting Review 53: 100959. [Google Scholar] [CrossRef]

- de Lima, Edson Pinheiro, Sergio E. Gouvea da Costa, Jannis Jan Angelis, and Juliano Munik. 2013. Performance measurement systems: A consensual analysis of their roles. International Journal of Production Economics 146: 524–42. [Google Scholar] [CrossRef]

- DeBusk, Gerald K., Robert M. Brown, and Larry N. Killough. 2003. Components and relative weights in utilization of dashboard measurement systems like the Balanced Scorecard. The British Accounting Review 35: 215–31. [Google Scholar] [CrossRef]

- Dobmeyer, Thomas W., Barry Woodward, and Lucille Olson. 2002. Factors Supporting the Development and Utilization of an Outcome-Based Performance Measurement System in a Chemical Health Case Management Program. Administration in Social Work 26: 25–44. [Google Scholar] [CrossRef]

- Duque-Zuluaga, Lola C., and Ulrike Schneider. 2008. Market Orientation and Organizational Performance in the Non-profit Context: Exploring Both Concepts and the Relationship between Them. Journal of Nonprofit & Public Sector Marketing 19: 25–47. [Google Scholar]

- Ebinger, Falk, Stephan Grohs, and Renate Reiter. 2011. The Performance of Decentralisation Strategies Compared: An Assessment of Decentralisation Strategies and their Impact on Local Government Performance in Germany, France and England. Local Government Studies 37: 535–75. [Google Scholar] [CrossRef][Green Version]

- Ebrahim, Alnoor, and V. Kasturi Rangan. 2014. What Impact? A framework for measuring the scale and scope of social performance. California Management Review 56: 118–41. [Google Scholar] [CrossRef]

- Felício, Teresa, António Samagaio, and Ricardo Rodrigues. 2021. Adoption of management control systems and performance in public sector organizations. Journal of Business Research 124: 593–602. [Google Scholar] [CrossRef]

- Grigoroudis, Evangelos, Eva Orfanoudaki, and Constantin Zopounidis. 2012. Strategic performance measurement in a healthcare organisation: A multiple criteria approach based on balanced scorecard. Omega 40: 104–19. [Google Scholar] [CrossRef]

- Henderson, Elisa, and Vicky Lambert. 2018. Negotiating for survival: Balancing mission and money. The British Accounting Review 50: 185–98. [Google Scholar] [CrossRef]

- Hoque, Zahirul. 2014. 20 years of studies on the balanced scorecard: Trends, accomplishments, gaps and opportunities for future research. The British Accounting Review 46: 33–59. [Google Scholar] [CrossRef]

- Hyndman, Noel, and Danielle McConville. 2018. Trust and accountability in UK charities: Exploring the virtuous circle. The British Accounting Review 50: 227–37. [Google Scholar] [CrossRef]

- Inamdar, Noorein S., Robert S. Kaplan, Mary Lou Helfrich Jones, and Rita Menitoff. 2000. The balanced scorecard: A strategic management system for multi-sector collaboration and strategy implementation. Quality Management in Health Care 8: 21–39. [Google Scholar] [CrossRef]

- Jevanesan, Thivya, Jiju Antony, Bryan Rodgers, and Anupama Prashar. 2021. Applications of continuous improvement methodologies in the voluntary sector: A systematic literature review. Total Quality Management & Business Excellence 32: 431–47. [Google Scholar]

- Jones, Sheri Chaney. 2014. Impact and Excellence: Data-Driven Strategies for Aligning Mission, Culture and Performance in Non-Profit and Government Organizations. Hoboken: John Wiley & Sons. [Google Scholar]

- Kale, Dinar. 2019. Mind the gap: Investigating the role of collective action in the evolution of Indian medical device regulation. Technology in Society 59: 101121. [Google Scholar] [CrossRef]

- Kaplan, Robert S. 2001. Strategic Performance Measurement and Management in Non-profit Organizations. Nonprofit Management and Leadership 11: 353–70. [Google Scholar] [CrossRef]

- Kaplan, Robert S., and David P. Norton. 1992. The balanced scorecard—Measures that drive performance. Harvard Business Review 83: 71–79. [Google Scholar]

- Kaplan, Robert S., and David P. Norton. 1996. Using the Balanced Scorecard as a Strategic Management System. Harvard Business Review 1996: 75–86. [Google Scholar]

- Karwan, Kirk R., and Robert E. Markland. 2006. Integrating service design principles and information technology to improve delivery and productivity in public sector operations: The case of the South Carolina DMV. Journal of Operations Management 24: 347–62. [Google Scholar] [CrossRef]

- Kong, Eric. 2010. Innovation processes in social enterprises: An IC perspective. Journal of Intellectual Capital 11: 158–78. [Google Scholar] [CrossRef]

- Kumar, Shashank, Rakesh D. Raut, Maciel M. Queiroz, and Balkrishna E. Narkhede. 2021. Mapping the barriers of AI implementations in the public distribution system: The Indian experience. Technology in Society 67: 101737. [Google Scholar] [CrossRef]

- Lee, Chongmyoung, and Branda Nowell. 2015. A Framework for Assessing the Performance of Nonprofit Organizations. American Journal of Evaluation 36: 299–319. [Google Scholar] [CrossRef]

- Leotta, Antonio, and Daniela Ruggerii. 2017. Performance measurement system innovations in hospitals as translation processes. Accounting, Auditing & Accountability Journal 30: 955–78. [Google Scholar]

- Liguori, Mariannunziata, and Ileana Steccolini. 2018. The power of language in legitimating public-sector reforms: When politicians “talk” accounting. The British Accounting Review 50: 161–73. [Google Scholar] [CrossRef]

- Maier, Florentine, Christian Schober, Ruth Simsa, and Reinhard Millner. 2015. SROI as a Method for Evaluation Research: Understanding Merits and Limitations. VOLUNTAS: International Journal of Voluntary and Non-Profit Organizations 26: 1805–30. [Google Scholar] [CrossRef]

- Maran, Laura, Enrico Bracci, and Robert Inglis. 2018. Performance management systems’ stability: Unfolding the human factor—A case from the Italian public sector. The British Accounting Review 50: 324–39. [Google Scholar] [CrossRef]

- Mauro, Sara Giovanna, Lino Cinquini, and Daniela Pianezzi. 2019. New Public Management between reality and illusion: Analysing the validity of performance-based budgeting. The British Accounting Review 53: 100825. [Google Scholar] [CrossRef]

- McEwen, Jessica, Mark Shoesmith, and Richard Allen. 2010. Embedding outcomes recording in Barnardo’s performance management approach. International Journal of Productivity and Performance Management 59: 586–98. [Google Scholar] [CrossRef]

- Mehrotra, Sonia, and Smriti Verma. 2015. An assessment approach for enhancing the organizational performance of social enterprises in India. Entrepreneurship in Emerging Economies 7: 35–54. [Google Scholar] [CrossRef]

- Merchant, Kenneth A., and Wim A. Van der Stede. 2007. Management Control Systems: Performance Measurement, Evaluation and Incentives. New York: Pearson. [Google Scholar]

- Micheli, Pietro, and Mike Kennerley. 2005. Performance measurement frameworks in public and non-profit sectors. Production Planning & Control 16: 125–34. [Google Scholar]

- Mouchamps, Hugues. 2014. Weighing elephants with kitchen scales: The relevance of traditional performance measurement tools for social enterprises. International Journal of Productivity and Performance Management 63: 727–45. [Google Scholar] [CrossRef]

- Moura, Louisi Francis, Edson Pinheiro de Lima, Sergio Eduardo Gouvea da Costa, Fernando Deschamps, and Eileen Van Aken. 2016. Identifying the Factors that Influence the Design of Performance Measurement Systems in Not-for-Profit Organizations. Paper presented at American Society for Engineering Management 2016 International Annual Conference, Indianapolis, IN, USA, October 26–29. [Google Scholar]

- Moura, Louisi Francis, Edson Pinheiro de Lima, Fernando Deschamps, Eileen Van Aken, Sergio E. Gouvea da Costa, Fernanda Tavares Treinta, and José Marcelo Almeida Prado Cestari. 2019. Designing performance measurement systems in non-profit and public administration organizations. International Journal of Productivity and Performance Management 68: 1373–410. [Google Scholar] [CrossRef]

- Moura, Louisi Francis, Edson Pinheiro de Lima, Fernando Deschamps, Eileen M. Van Aken, Sergio E. Gouvea Da Costa, Fernanda Tavares Treintaa, José Marcelo Almeida Prado Cestari, and Ronan Assumpção Silva. 2020. Factors for performance measurement systems design in non-profit organizations and public administration. Measuring Business Excellence 24: 377–99. [Google Scholar] [CrossRef]

- Moxham, Claire. 2009. Performance measurement: Examining the applicability of the existing body of knowledge to non-profit organisations. International Journal of Operations & Production Management 29: 740–63. [Google Scholar]

- Moxham, Claire. 2014. Understanding third sector performance measurement system design: A literature review. International Journal of Productivity and Performance Management 63: 704–26. [Google Scholar] [CrossRef]

- Munik, Juliano, Louisi Francis Moura, Edson Pinheiro de Lima, and Sergio Eduardo Gouvea da Costa. 2016. Performance measurement systems in non-profit organization: A bibliometric analysis. Paper presented at American Society for Engineering Management 2016 International Annual Conference, Charlotte, NC, USA, October 26–29; pp. 1–11. [Google Scholar]

- Munik, Juliano, Edson Pinheiro de Lima, Fernando Deschamps, Sergio E. Gouvea Da Costa, Eileen M. Van Aken, José Marcelo Almeida Prado Cestari, Louisi Francis Moura, and Fernanda Treinta. 2021. Performance measurement systems in non-profit organizations: An authorship-based literature review. Measuring Business Excellence 25: 245–70. [Google Scholar] [CrossRef]

- Navimipour, Nima Jafari, Farnaz Sharifi Milani, and Mehdi Hossenzadeh. 2018. A model for examining the role of effective factors on the performance of organizations. Technology in Society 55: 166–74. [Google Scholar] [CrossRef]

- Neely, Andy, Chris Adams, and Paul Crowe. 2001. The performance prism in practice. Measuring Business Excellence 5: 6–13. [Google Scholar] [CrossRef]

- Nguyen, Linh, Betina Szkudlarek, and Richard G. Seymour. 2015. Social impact measurement in social enterprises: An interdependence perspective. Canadian Journal of Administrative Sciences 32: 224–37. [Google Scholar] [CrossRef]

- Noordin, Nazrul Hazizi, Siti Nurah Haron, and Salina Kassim. 2017. Developing a comprehensive performance measurement system for waqf institutions. International Journal of Social Economics 44: 921–36. [Google Scholar] [CrossRef]

- Northcott, Deryl, and Tuivaiti Ma’amora Taulapapa. 2012. Using the balanced scorecard to manage performance in public sector organizations: Issues and challenges. International Journal of Public Sector Management 25: 166–91. [Google Scholar] [CrossRef]

- Pirozzi, Maria Grazia, and Giuseppe Paolo Ferulano. 2016. Intellectual capital and performance measurement in healthcare organizations: An integrated new model. Journal of Intellectual Capital 17: 320–50. [Google Scholar] [CrossRef]

- Popovich, Mark. G. 1998. Creating High-Performance Government Organizations. Edited by Mark G. Popovich. San Francisco: Jossey-Bass Publishers. [Google Scholar]

- Raus, Marta, Jianwei Liu, and Alexander Kipp. 2010. Evaluating IT innovations in a business-to-government context: A framework and its applications. Government Information Quarterly 27: 122–33. [Google Scholar] [CrossRef]

- Reda, Nigusse W. 2017. Balanced scorecard in higher education institutions: Congruence and roles to quality assurance practices. Quality Assurance in Education 25: 489–99. [Google Scholar] [CrossRef]

- Schwartz, Robert, and Raisa Deber. 2016. The performance measurement -management divide in public health. Health Policy 120: 273–80. [Google Scholar] [CrossRef] [PubMed]

- Shuman, Mark C. 1995. Managing legitimacy: Strategic and institutional approaches. Academy of Management Review 20: 571–610. [Google Scholar]

- Sinuany-Stern, Zilla, and H. David Sherman. 2014. Operations research in the public sector and non-profit organizations. Annals of Operations Research 221: 1–8. [Google Scholar] [CrossRef]

- Soysa, Ishani Buddika, Nihal Palitha Jayamaha, and Nigel Peter Grigg. 2018. Developing a strategic performance scoring system for healthcare non-profit organisations. Benchmarking: An International Journal 25: 3654–78. [Google Scholar] [CrossRef]

- Taylor, Margaret, and Andrew Taylor. 2014. Performance measurement in the Third Sector: The development of a stakeholder-focussed research agenda. Production Planning & Control 25: 1370–85. [Google Scholar]

- Treinta, Fernanda T., Louisi F. Moura, Jose M. Almeida Prado Cestari, Edson Pinheiro de Lima, Fernando Deschamps, Sergio Eduardo Gouvea da Costa, Eileen M. Van Aken, Juliano Munik, and Luciana R. Leite. 2020. Design and implementation factors for performance measurement in non-profit organizations: A literature review. Frontiers in Psychology 11: 1799. [Google Scholar] [CrossRef]

- Valentinov, Vladislav. 2011. The Meaning of Nonprofit Organization: Insights from Classical Institutionalism. Journal of Economic Issues XLV: 901–16. [Google Scholar]

- Wellens, Lore, and Marc Jegers. 2014. Effective governance in non-profit organizations: A literature based multiple stakeholder approach. European Management Journal 32: 223–43. [Google Scholar] [CrossRef]

- Yang, Cherrie, and Deryl Northcott. 2018. Unveiling the role of identity accountability in shaping charity outcome measurement practices. The British Accounting Review 50: 214–26. [Google Scholar] [CrossRef]

| GROUP | FACTOR | CONCEPT |

|---|---|---|

| PURPOSE | Social approach | The social approach’s description can be summarized in the key features of a PA’s or NPO’s mission. The pursuit of social goals ahead of profit differentiates an NPO and PA. Social value creation refers to the outcomes and tends to be intangible. The social impact will also be intangible, and is qualitative, with long-term effects, i.e., the changes promoted by the organization as an improvement in a patient or citizen’s well-being. Although financial results sometimes do not show it, positive results through social value creation translate into social impact in the long-term, an important index of the effectiveness and capacity of these organizations to realize their mission. |

| STAKEHOLDERS | Accountability | Accountability is one of the factors that most concerns NPO and PA and is a way of holding accounts and providing reports. Usually, legislation is the primary driver for accountability, mainly via financial reports as a contractual or statutory obligation. Those reports are addressed to external stakeholders, such as regulatory agencies, funders, and governmental departments. Legal financial reports are critical for these organizations because, in some cases, stakeholders require reports in the short term. Still, the social value and social impact can take more time to be perceived and measured. Accountability can also be a strategy to attract new donors and funders. |

| Legitimacy | Legitimacy in the NPO and PA context can be defined as the stakeholders’ perception that activities are being properly developed, considering legal and contractual obligations as well as the goals and the social mission. Legitimacy is motivated by a desire for organizations to be transparent and promote themselves through legal obligations and performance reports. Thus, demonstrating their activities is an important mechanism to increase legitimacy and attract new funders, donors, and other stakeholders. | |

| Involvement and influence of stakeholders | The public sector, donors, public and private funders, community, regulatory agencies, tax authorities, beneficiaries, suppliers, partners, staff, and volunteers are examples of stakeholders related to the context of NPO and PA. These stakeholders are involved with those organizations through funding, local needs, partnerships, and other motivations. They have a complex involvement with the organization and influence the management and organizational decisions, including the definition of performance measures. | |

| Volunteering | Volunteers contribute to public organizations and NPOs without contractual obligations but are interested in participating in social actions. They usually present different requirements and expectations than other internal stakeholders and influence management and organizational culture. | |

| MANAGEMENT | Financial sustainability | As the NPOs and PA have financial restrictions and focus on social value creation, their management is affected by that condition. Donations, investments, and subsidies are examples of sources of income. Some of these sources are not guaranteed for reasons such as political issues and economic crises. So, it is a matter of organizational survival for an NPO and a PA to maintain alternative income sources to maintain their financial sustainability and provide their services. |

| Short and long-term planning | NPOs and PAs need to manage the instability of resources influenced by the economic situation, political pressure, resources restrictions, interlocal equity, and other problems. This context makes long-term planning more complicated and, sometimes, the social impact can only be measured and assessed after several years. | |

| Fairness | The need to provide interlocal equity is a characteristic in some NPOs, and mainly in public organizations. For some, resources must be mobilized to provide an homogenous service level, guaranteeing that social value creation promotes the same social gain. | |

| Effectiveness and efficiency | Characteristics such as the social mission, financial sustainability, intangible results, and diversity and stakeholders’ involvement can contribute to NPO and PA operations’ complexity and influence their efficiency and effectiveness. Effectiveness refers to achieving social goals and their social impact. Efficiency is a dimension that translates the cost-efficiency of service production and relates to operations, resources, and delivery of outcomes and benefits to the public. | |

| Strategic Management Control | Developing an environment open to learning and continuous improvement can contribute to the PA’s and NPO’s promotion to stakeholders and create an organizational culture to measure its performance. In this context, a PMS can support the management and help provide a way to organizational learning and promote continuous improvement through its use by all staff and volunteers. |

| ORGANIZATION | US.NPO.1 | BR.NPO.2 |

|---|---|---|

| ACTIVITIES | Research and development | Research and development |

| STRUCTURE | Projects | Projects |

| BENEFICIARY FOCUS | National | National |

| NUMBER OF PAID STAFF | 453 | Around 175 |

| NUMBER OF VOLUNTEERS | Not applicable | Not applicable |

| ANNUAL INCOME * | USD 34,307,718 | Around BRL 30,000,000 |

| FUNDING MECHANISM | Mainly from contracts and sponsors | Mainly from contracts and subsidies |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Moura, L.F.; Lima, E.P.; Deschamps, F.; Van Aken, E.; Gouvea da Costa, S.E.; Duarte, R.; Kluska, R.A. What Role Do Design Factors Play in Applying Performance Measurement Systems in Nonprofit Organizations? Adm. Sci. 2022, 12, 43. https://doi.org/10.3390/admsci12020043

Moura LF, Lima EP, Deschamps F, Van Aken E, Gouvea da Costa SE, Duarte R, Kluska RA. What Role Do Design Factors Play in Applying Performance Measurement Systems in Nonprofit Organizations? Administrative Sciences. 2022; 12(2):43. https://doi.org/10.3390/admsci12020043

Chicago/Turabian StyleMoura, Louisi Francis, Edson Pinheiro Lima, Fernando Deschamps, Eileen Van Aken, Sergio Eduardo Gouvea da Costa, Rafael Duarte, and Rafael Araujo Kluska. 2022. "What Role Do Design Factors Play in Applying Performance Measurement Systems in Nonprofit Organizations?" Administrative Sciences 12, no. 2: 43. https://doi.org/10.3390/admsci12020043

APA StyleMoura, L. F., Lima, E. P., Deschamps, F., Van Aken, E., Gouvea da Costa, S. E., Duarte, R., & Kluska, R. A. (2022). What Role Do Design Factors Play in Applying Performance Measurement Systems in Nonprofit Organizations? Administrative Sciences, 12(2), 43. https://doi.org/10.3390/admsci12020043