The Role of Top Managers in Implementing Corporate Sustainability—A Systematic Literature Review on Small and Medium-Sized Enterprises

Abstract

1. Introduction

2. Theoretical Background

2.1. Domain Theories: Greenblushing and Corporate Sustainability in SMEs

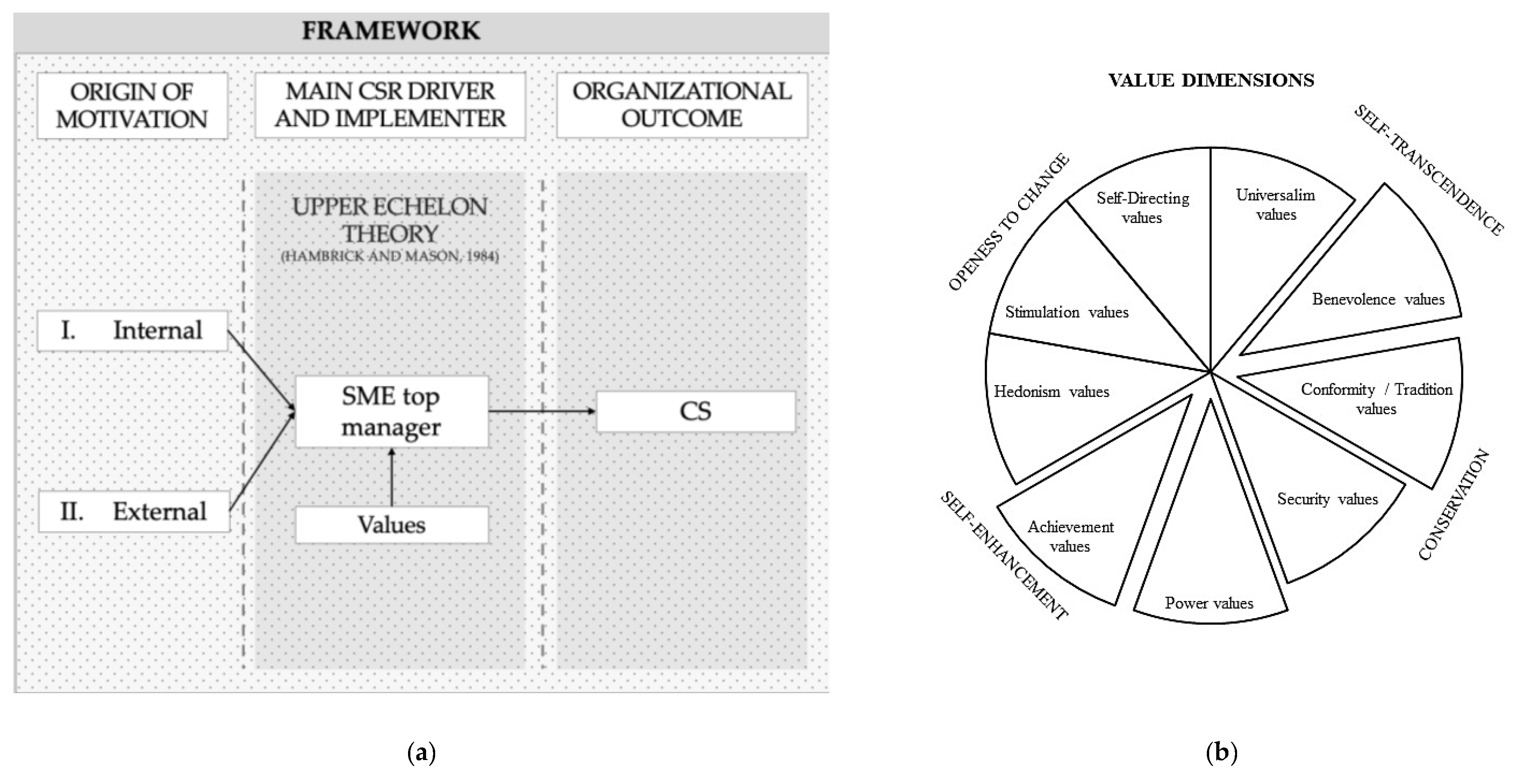

2.2. Meta Theories: Upper Echelons and the Schwartz Value System

3. Methodology

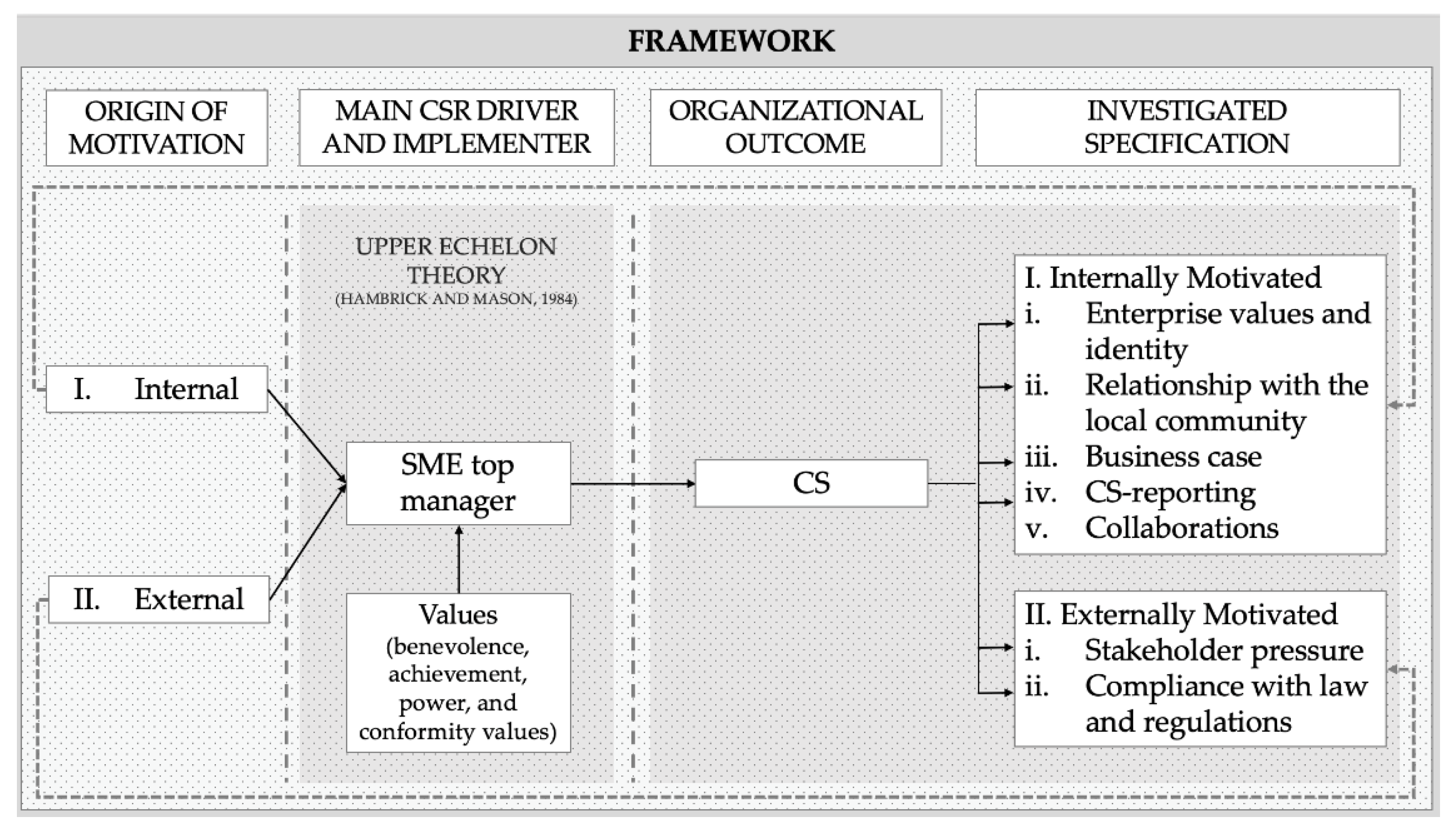

3.1. Research Framework

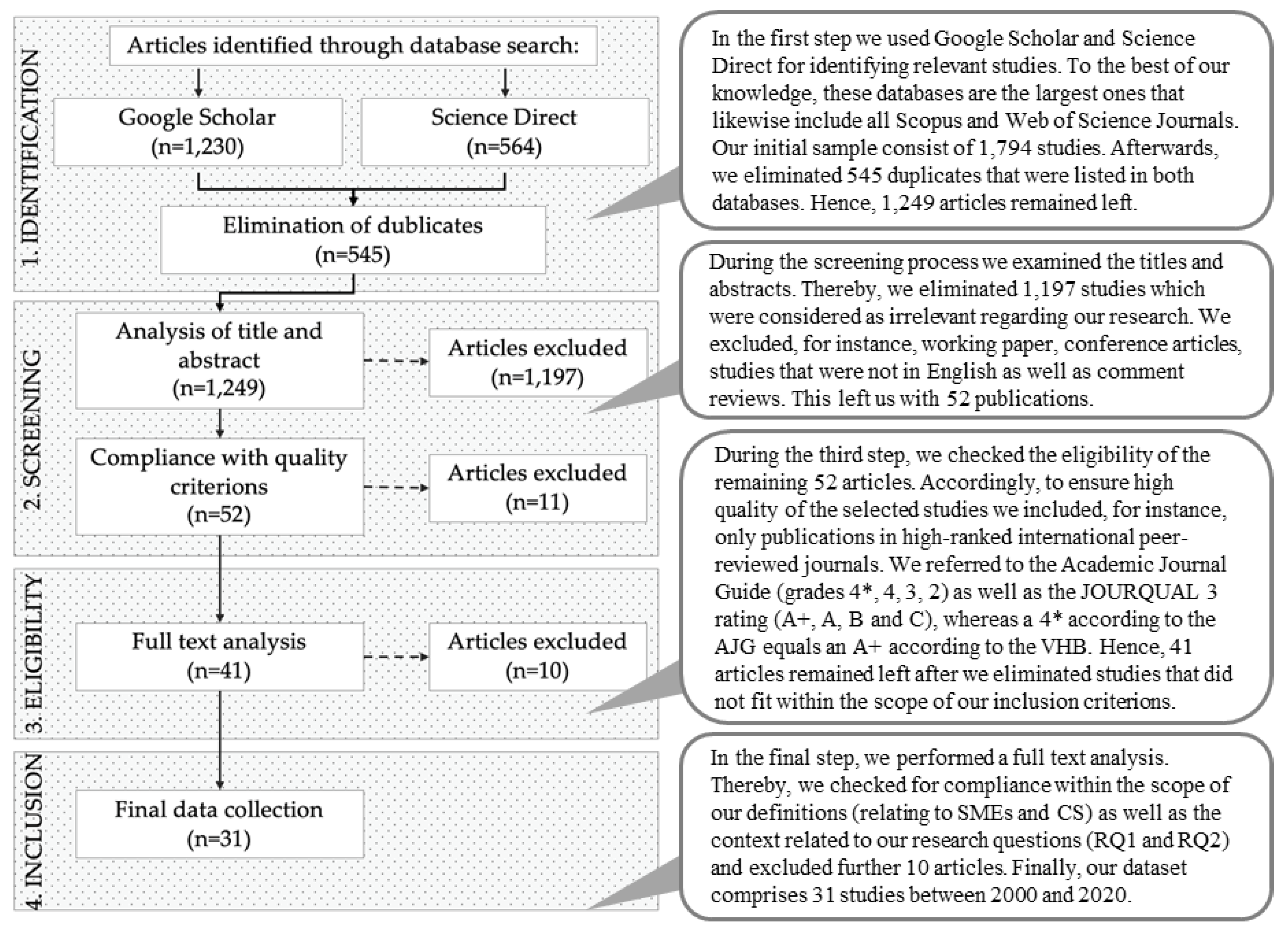

3.2. Sample Selection

4. Findings

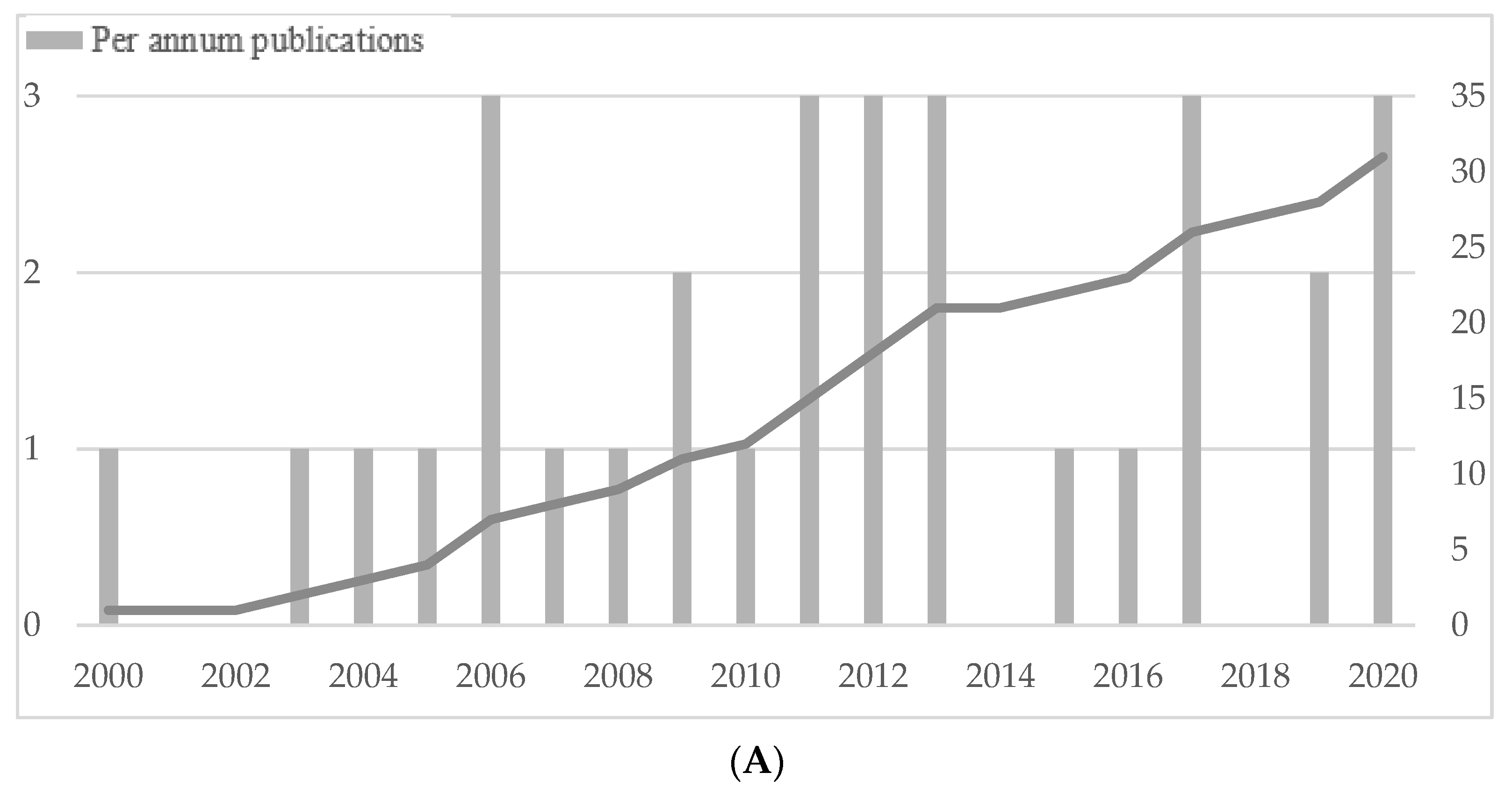

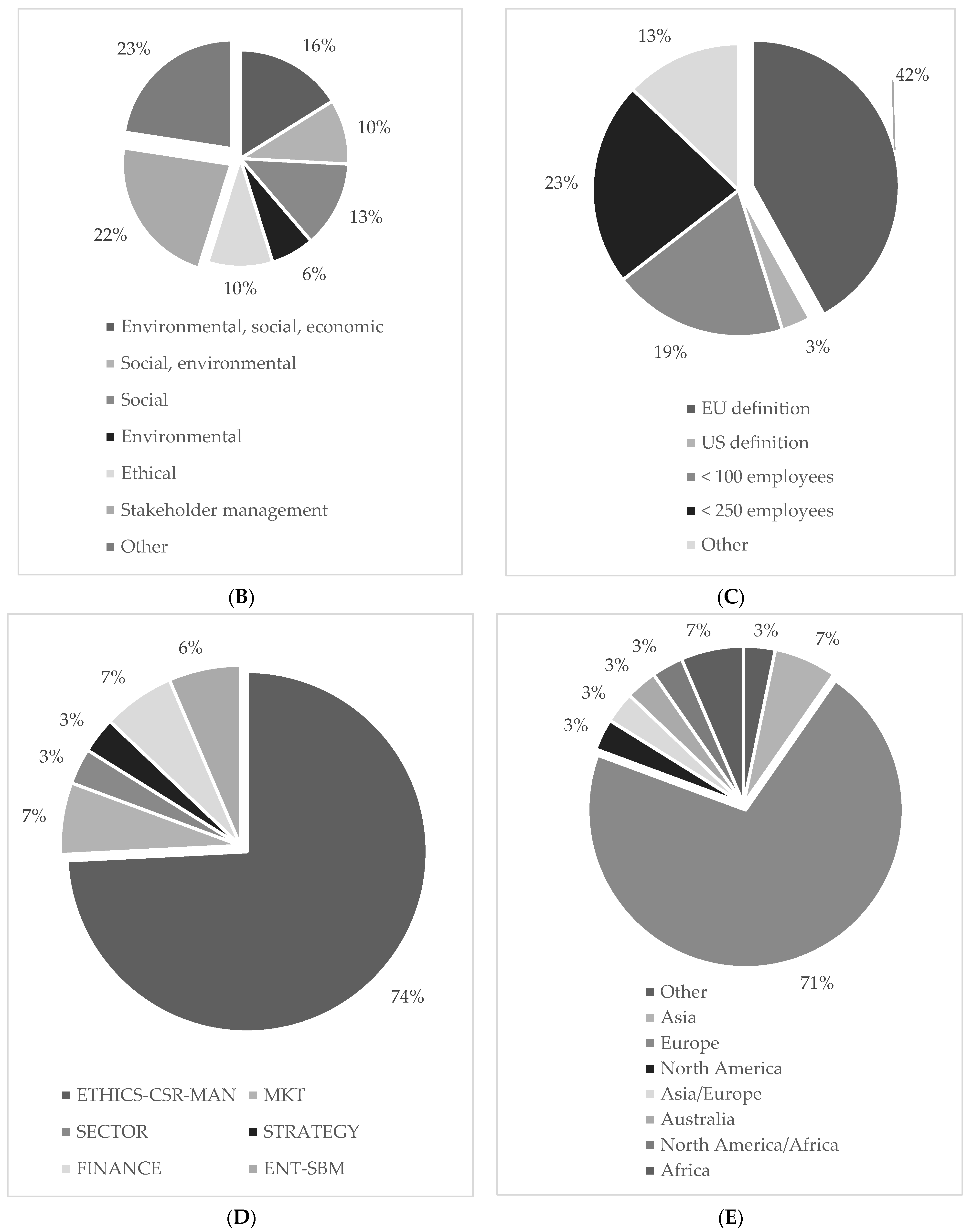

4.1. Bibliometric Analysis

4.2. Content Analysis

4.2.1. Enterprise Values and Identity

4.2.2. Relationship with the Local Community

4.2.3. Business Case

4.2.4. CS-Reporting

4.2.5. Collaborations

4.2.6. Stakeholder Pressure

4.2.7. Compliance with Law and Regulations

5. Discussion and Conclusions

5.1. Synthesis of the Findings

5.1.1. Benevolence and Power Values: Identity, Local Community and Collaborations

5.1.2. Power Values: Business Case and Reporting

5.1.3. Conformity Values: Stakeholder Pressure and Compliance

5.2. Contribution to Theory and Practice

5.3. Future Research Agenda and Critical Reflection

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Acar, F. Pinar. 2016. The effects of top management team composition on SME export performance: An upper echelons perspective. Central European Journal of Operations Research 24: 833–52. [Google Scholar] [CrossRef]

- Ahmad, Noor Hazlina, and T. Ramayah. 2012. Does the notion of ‘doing well by doing good’ prevail among entrepreneurial ventures in a developing nation? Journal of Business Ethics 106: 479–90. [Google Scholar] [CrossRef]

- AJG (Academic Journal Guide). 2018. Academic Journal Guide—Methodology. Available online: https://charteredabs.org/wp-content/uploads/2018/03/AJG2018-Methodology.pdf (accessed on 1 May 2020).

- Albertsen, Oana, and Rainer Lueg. 2014. The Balanced Scorecard’s missing link to compensation: A literature review and an agenda for future research. Journal of Accounting and Organizational Change 10: 431–65. [Google Scholar] [CrossRef]

- Andersen, Christian Vium, and Rainer Lueg. 2017. Management Control Systems, culture and upper echelons—A systematic literature review on their interactions. Corporate Ownership and Control 14: 312–25. [Google Scholar] [CrossRef]

- Apospori, Eleni, Konstantinos G. Zografos, and Solon Magrizos. 2012. SME corporate social responsibility and competitiveness: A literature review. International Journal of Technology Management 58: 10–31. [Google Scholar] [CrossRef]

- Aragón, Cristina, Lorea Narvaiza, and Maite Altuna. 2016. Why and how does social responsibility differ among SMEs? A social capital systemic approach. Journal of Business Ethics 138: 365–84. [Google Scholar] [CrossRef]

- Azam, S. M. Ferdous, and Moha A. Abdullah. 2015. Differential roles between owner and manager in financial practice contribute to business success: An analysis on Malaysian small business. Academic Journal of Interdisciplinary Studies 4: 123. [Google Scholar] [CrossRef][Green Version]

- Baden, D., I. Harwood, and D. Woodward. 2011. The effects of procurement policies on downstream CSR activity: Content analytic insights into the views and actions of SME owner–manager. International Small Business Journal 29: 259–77. [Google Scholar] [CrossRef]

- Baumann-Pauly, Dorothée, Christopher Wickert, Laura J. Spence, and Andreas Georg Scherer. 2013. Organizing corporate social responsibility in small and large firms: Size matters. Journal of Business Ethics 115: 693–705. [Google Scholar] [CrossRef]

- Berk, Abigail. 2017. Small Business Social Responsibility—More than Size. The Journal of Corporate Citizenship 67: 12–38. [Google Scholar] [CrossRef]

- Borisov, Boris, and Rainer Lueg. 2012. Are you sure about what you mean by ‘uncertainty’? The actor’s perspective vs. the institutional perspective. Proceedings of Pragmatic Constructivism 2: 51–58. [Google Scholar]

- Bouzzine, Yassin Denis, and Rainer Lueg. 2020. The contagion effect of environmental violations: The case of Dieselgate in Germany. Business Strategy and the Environment 29: 3187–202. [Google Scholar] [CrossRef]

- Burkert, Michael, and Rainer Lueg. 2013. Differences in the sophistication of Value-based Management—The role of top executives. Management Accounting Research 24: 3–22. [Google Scholar] [CrossRef]

- Campbell, Jeffrey M., and Joohyung Park. 2017. Extending the resource-based view: Effects of strategic orientation toward community on small business performance. Journal of Retailing and Consumer Services 34: 302–8. [Google Scholar] [CrossRef]

- Cao, Qing, Zeki Simsek, and Hongping Zhang. 2010. Modelling the Joint Impact of the CEO and the TMT on Organizational Ambidexterity. Journal of Management Studies 47: 1272–96. [Google Scholar] [CrossRef]

- Ciliberti, Francesco, Pierpaolo Pontrandolfo, and Barbara Scozzi. 2008. Investigating corporate social responsibility in supply chains: A SME perspective. Journal of Cleaner Production 16: 1579–88. [Google Scholar]

- Colovic, Ana, Sandrine Henneron, Maik Huettinger, and Ruta Kazlauskaite. 2019. Corporate social responsibility and SMEs. European Business Review 17: 523–40. [Google Scholar] [CrossRef]

- CROCIS-CCIP. 2007. Le Développement Durable dans les PME-PMI de la Région Parisienne. Baromètre. Available online: http://www.crocis.ccip.fr (accessed on 1 February 2021).

- Dacin, M. Tina, Kamal Munir, and Paul Tracey. 2010. Formal dining at cambridge colleges: Linking ritual performance and institutional maintenance. Academy of Management Journal 53: 1393–418. [Google Scholar] [CrossRef]

- Davis, Peter S., Emin Babakus, Paula Danskin Englis, and Tim Pett. 2010. The Influence of CEO Gender on Market Orientation and Performance in Service Small and Medium-Sized Service Businesses. Journal of Small Business Management 48: 475–96. [Google Scholar] [CrossRef]

- Del Brìo, Jesùs Angel, and Beatriz Junquera. 2003. A review of the literature on environmental innovation management in SMEs: Implications for public policies. Technovation 23: 939–48. [Google Scholar] [CrossRef]

- Demuijnck, Geert, and Hubert Ngnodjom. 2013. Responsibility and informal CSR in formal Cameroonian SMEs. Journal of Business Ethics 112: 653–65. [Google Scholar] [CrossRef]

- Denyer, David, and David Tranfield. 2008. Producing a systematic review. In The Sage Handbook of Organizational Research Methods. Edited by D. Buchanan and A. Bryman. London: Sage, pp. 671–89. [Google Scholar]

- Enderle, Georges. 2004. Global competition and corporate responsibilities of small and medium sized enterprises. Business Ethics: A European View 13: 51–63. [Google Scholar] [CrossRef]

- European Commission. 2003. Observatory of European SMEs: Report 2003, SMEs in Europe 2003. Luxembourg: Office for Official Publications of the European Communities. [Google Scholar]

- Eweje, Gabriel. 2020. Proactive environmental and social strategies in a small-to medium-sized company: A case study of a Japanese SME. Business Strategy and the Environment 29: 2927–38. [Google Scholar]

- Fassin, Yves. 2008. SMEs and the fallacy of formalizing CSR. Business Ethics: A European Review 17: 364–78. [Google Scholar] [CrossRef]

- Fassin, Yves, Annick Van Rossem, and Marc Buelens. 2011. Small-business owner-managers’ perceptions of business ethics and CSR-related concepts. Journal of Business Ethics 98: 425–53. [Google Scholar] [CrossRef]

- Fassin, Yves, Andrea Werner, Annick Van Rossem, Silvana Signori, Elisabet Garriga, Heidi von Weltzien Hoivik, and Hans-Jörg Schlierer. 2015. CSR and related terms in SME owner–managers’ mental models in six European countries: National context matters. Journal of Business Ethics 128: 433–56. [Google Scholar] [CrossRef]

- Finkelstein, Sydney. 1992. Power in top management teams: Dimensions, measurement, and validation. Academy of Management Journal 35: 505–38. [Google Scholar]

- Fisher, Kyla, Jessica Geenen, Marie Jurcevic, Katya McClintock, and Glynn Davis. 2009. Applying asset-based community development as a strategy for CSR: A Canadian perspective on a win–win for stakeholders and SMEs. Business Ethics: A European Review 18: 66–82. [Google Scholar] [CrossRef]

- Fitjar, Rune Dahl. 2011. Little big firms? Corporate social responsibility in small businesses that do not compete against big ones. Business Ethics: A European Review 20: 30–44. [Google Scholar] [CrossRef]

- Fraj-Andrés, Elena, M. Eugenia López-Pérez, Iguácel Melero-Polo, and Rosario Vázquez-Carrasco. 2012. Company image and corporate social responsibility: Reflecting with SMEs’ managers. Marketing Intelligence & Planning 30: 266–80. [Google Scholar]

- Giovanna, Campopiano, and Cassia Lucio. 2012. Corporate social responsibility: A survey among SMEs in Bergamo. Procedia-Social and Behavioral Sciences 62: 325–41. [Google Scholar] [CrossRef]

- Graafland, Johan, and Bert Van de Ven. 2006. Strategic and moral motivation for corporate social responsibility. Journal of Corporate Citizenship 22: 111–23. [Google Scholar] [CrossRef]

- Grayson, David, and Tom Dodd. 2007. Small Is Sustainable (and Beautiful): Encouraging European Smaller Enterprises to be Sustainable. Cranfield: Doughty Centre for Corporate Responsibility, Cranfield University. [Google Scholar]

- Hambrick, Donald C. 2007. Upper echelons theory: An update. Academy of Management Review 32: 334–43. [Google Scholar] [CrossRef]

- Hambrick, Donald C., and Sydney Finkelstein. 1987. Managerial discretion: A bridge between two polar views on organizations. In Research in Organizational Behavior. Edited by B. M. Staw and L. L. Cummings. Greenwich: JAI Press, vol. 9, pp. 369–406. [Google Scholar]

- Hambrick, Donald C., and Phyllis A. Mason. 1984. Upper echelons: The organization as a reflection of its top managers. Academy of Management Review 9: 193–206. [Google Scholar] [CrossRef]

- Hammann, Eva-Maria, Andre Habisch, and Harald Pechlaner. 2009. Values that create value: Socially responsible business practices in SMEs—Empirical evidence from German companies. Business Ethics: A European Review 18: 37–51. [Google Scholar] [CrossRef]

- Hannafey, Francis T. 2003. Entrepreneurship and Ethics: A Literature Review. Journal of Business Ethics 46: 99–110. [Google Scholar] [CrossRef]

- Jamali, Dima, Mona Zanhour, and Tamar Keshishian. 2009. Peculiar strengths and relational attributes of SMEs in the context of CSR. Journal of Business Ethics 87: 355–77. [Google Scholar] [CrossRef]

- Jenkins, Heledd. 2004. A critique of conventional CSR theory: An SME perspective. Journal of General Management 29: 37–57. [Google Scholar] [CrossRef]

- Jenkins, Heledd. 2006. Small business champions for corporate social responsibility. Journal of Business Ethics 67: 241–56. [Google Scholar] [CrossRef]

- Jenkins, Heledd. 2009. A ‘business opportunity’ model of corporate social responsibility for small- and medium-sized enterprises. Business Ethics: A European Review 18: 21–36. [Google Scholar] [CrossRef]

- Johnson, Phil, James Curran, Joanne Duberley, and Robert A. Blackburn. 2001. Researching the Small Enterprise. London: Sage. [Google Scholar]

- Kechiche, Amina, and Richard Soparnot. 2012. CSR within SMEs: Literature review. International Business Research 5: 97–104. [Google Scholar] [CrossRef]

- Kiefhaber, Eva, Kathryn Pavlovich, and Katharina Spraul. 2020. Sustainability-Related Identities and the Institutional Environment: The Case of New Zealand Owner–Managers of Small-and Medium-Sized Hospitality Businesses. Journal of Business Ethics 163: 37–51. [Google Scholar]

- Klewitz, Johanna, and Erik G. Hansen. 2014. Sustainability-oriented innovation of SMEs: A systematic review. Journal of Cleaner Production 65: 57–75. [Google Scholar] [CrossRef]

- Lähdesmäki, Merja, Marjo Siltaoja, and Laura J. Spence. 2019. Stakeholder salience for small businesses: A social proximity perspective. Journal of Business Ethics 158: 373–85. [Google Scholar] [CrossRef]

- Lamberti, Lucio, and Giuliano Noci. 2012. The relationship between CSR and corporate strategy in medium-sized companies: Evidence from Italy. Business Ethics: A European Review 21: 402–16. [Google Scholar]

- Lenssen, Gilbert, Francesco Perrini, Antonio Tencati, Peter Lacy, and Lorraine Sweeney. 2007. Corporate social responsibility in Ireland: Barriers and opportunities experienced by SMEs when undertaking CSR. Corporate Governance: The International Journal of Business in Society 7: 516–23. [Google Scholar]

- Lepoutre, Jan, and Aimé Heene. 2006. Investigating the impact of firm size on small business social responsibility: A critical review. Journal of Business Ethics 67: 257–73. [Google Scholar] [CrossRef]

- Longenecker, Justin G., Carlos W. Moore, J. William Petty, Leslie E. Palich, and Joseph A. McKinney. 2006. Ethical attitudes in small businesses and large corporations: Theory and empirical findings from a tracking study spanning three decades. Journal of Small Business Management 44: 167–83. [Google Scholar] [CrossRef]

- Longo, Mariolina, Matteo Mura, and Alessandra Bonoli. 2005. Corporate social responsibility and corporate performance: The case of Italian SMEs. Corporate Governance: The International Journal of Business in Society 32: 646–72. [Google Scholar]

- Lubatkin, Michael H., Zeki Simsek, Yan Ling, and John F. Veiga. 2006. Ambidexterity and performance in small- to medium-sized firms: The pivotal role of TMT behavioral integration. Journal of Management 32: 1–17. [Google Scholar] [CrossRef]

- Lueg, Rainer. 2009. Führt der Einsatz externer Berater zur Überimplementierung innovativer Steuerungsinstrumente? Zeitschrift der Unternehmensberatung 4: 249–53. [Google Scholar]

- Lueg, Rainer, and Boris Genadiev Borisov. 2014. Archival or perceived measures of environmental uncertainty? Conceptualization and new empirical evidence. European Management Journal 32: 658–71. [Google Scholar] [CrossRef]

- Lueg, Rainer, and Ana Carvalho e Silva. 2013. When one size does not fit all: A literature review on the modifications of the balanced scorecard. Problems and Perspectives in Management 11: 86–94. [Google Scholar]

- Lueg, Rainer, and Pernille Julner. 2014. How are Strategy Maps linked to strategic and organizational change? A review of the empirical literature on the Balanced Scorecard. Corporate Ownership & Control 11: 439–46. [Google Scholar]

- Lueg, Rainer, and Magdalena Knapik. 2016. Risk management with management control systems: A pragmatic constructivist perspective. Corporate Ownership and Control Journal 13: 72–81. [Google Scholar] [CrossRef]

- Lueg, Klarissa, and Rainer Lueg. 2020. Detecting green-washing or substantial organizational communication: A model for testing two-way interaction between risk and sustainability reporting. Sustainability 12: 2520. [Google Scholar] [CrossRef]

- Lueg, Rainer, and Ronny Radlach. 2016. Managing sustainable development with management control systems: A literature review. European Management Journal 34: 158–71. [Google Scholar] [CrossRef]

- Lueg, Rainer, and Utz Schäffer. 2010. Assessing empirical research on Value-based Management: Guidelines for improved hypothesis testing. Journal für Betriebswirtschaft 60: 1–47. [Google Scholar] [CrossRef]

- Lueg, Rainer, and Louisa Vu. 2015. Success factors in Balanced Scorecard implementations—A literature review. Management Revue: Socio-Economic Studies 26: 306–27. [Google Scholar] [CrossRef]

- Lueg, Rainer, Maria Medelby Pedersen, and Søren Nørregaard Clemmensen. 2015. The role of corporate sustainability in a low-cost business model—A case study in the Scandinavian fashion industry. Business Strategy and the Environment 24: 344–59. [Google Scholar] [CrossRef]

- Lueg, Klarissa, Rainer Lueg, Karina Andersen, and Veronica Dancianu. 2016. Integrated reporting with CSR practices: A pragmatic constructivist case study in a Danish cultural setting. Corporate Communications: An International Journal 21: 20–35. [Google Scholar] [CrossRef]

- Lueg, Klarissa, Boris Krastev, and Rainer Lueg. 2019. Bidirectional effects between sustainability disclosure and risk—A disaggregate analysis of listed companies in South Africa. Journal of Cleaner Production 229: 268–77. [Google Scholar] [CrossRef]

- Masud, Md. Abdul Kaium, Md. Harun Ur Rashid, Tehmina Khan, Seong Mi Bae, and Jong Dae Kim. 2019. Organizational Strategy and Corporate Social Responsibility: The Mediating Effect of Triple Bottom Line. International Journal of Environmental Research and Public Health 16: 4559. [Google Scholar] [CrossRef]

- Meyer, Maryline, Sébastien Narjoud, and Julien Granata. 2017. When collective action drives corporate social responsibility implementation in small and medium-sized enterprises: The case of a network of French winemaking cooperatives. International Journal of Entrepreneurship and Small Business 32: 7–27. [Google Scholar] [CrossRef]

- Mirosa, Miranda, Rob Lawson, and Daniel Gnoth. 2013. Linking personal values to energyefficient behaviors in the home. Environment & Behavior 45: 455–75. [Google Scholar]

- Moher, David, Alessandro Liberati, Jennifer Tetzlaff, and Douglas G. Altman. 2009. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. PLoS Medicine 6: e1000097. [Google Scholar] [CrossRef] [PubMed]

- Morris, Michael H., Minet Schindehutte, John Walton, and Jeffrey Allen. 2002. The ethical context of entrepreneurship: Proposing and testing a development framework. Journal of Business Ethics 40: 331–62. [Google Scholar] [CrossRef]

- Morros, Jordi. 2016. The integrated reporting: A presentation of the current state of art and aspects of integrated reporting that needed further development. Intangible Capital 12: 336–56. [Google Scholar] [CrossRef]

- Muheki, Mark K., Klarissa Lueg, Rainer Lueg, and Christian Schmaltz. 2014. How business reporting changed during the financial crisis: A comparative case study of two large U.S. banks. Problems and Perspectives in Management 12: 191–208. [Google Scholar]

- Murillo, David, and Josep M. Lozano. 2006. SMEs and CSR: An approach to CSR in their own words. Journal of Business Ethics 67: 227–40. [Google Scholar] [CrossRef]

- Nielsen, Janni Grouleff, Rainer Lueg, and Dennis van Liempd. 2019. Managing Multiple Logics: The Role of Performance Measurement Systems in Social Enterprises. Sustainability 11: 2327. [Google Scholar] [CrossRef]

- Nielsen, Janni Grouleff, Rainer Lueg, and Dennis Van Liempd. 2021. Challenges and boundaries in implementing social return on investment: An inquiry into its situational appropriateness. Nonprofit Management and Leadership 31: 413–35. [Google Scholar] [CrossRef]

- Nkiko, Cedric Marvin. 2013. SME owner–managers as key drivers of corporate social responsibility in Uganda. International Journal of Business Governance and Ethics 8: 376–400. [Google Scholar] [CrossRef]

- Nooteboom, Bart. 1994. Innovation and Diffusion in Small Firms: Theory and Evidence. Small Business Economics 6: 327–47. [Google Scholar] [CrossRef]

- Onali, Enrico, Ramilya Galiakhmetova, Philip Molyneux, and Giuseppe Torluccio. 2016. CEO power, government monitoring, and bank dividends. Journal of Financial Intermediation 27: 89–117. [Google Scholar] [CrossRef]

- Onkila, Tiina Johanna. 2009. Corporate argumentation for acceptability: Reflections of environmental values and stakeholder relations in corporate environmental statements. Journal of Business Ethics 87: 285–98. [Google Scholar] [CrossRef]

- Preuss, Lutz, and Jack Perschke. 2010. Slipstreaming the larger boats: Social responsibility in medium-sized businesses. Journal of Business Ethics 92: 531–51. [Google Scholar] [CrossRef]

- Rahman, Mahfuzur, Che Ruhana Isa, Teng-Tsai Tu, Moniruzzaman Sarker, and Md Abdul Kaium Masud. 2020. A bibliometric analysis of socially responsible investment sukuk literature. Asian Journal of Sustainability and Social Responsibility 5: 1–19. [Google Scholar] [CrossRef]

- Ralston, David A., Carolyn P. Egri, Emmanuelle Reynaud, Narasimhan Srinivasan, Olivier Furrer, David Brock, Ruth Alas, Florian Wangenheim, Fidel León Darder, Christine Kuo, and et al. 2011. A twenty-first century assessment of values across the global workforce. Journal of Business Ethics 104: 1–31. [Google Scholar] [CrossRef]

- Rekik, Lilia, and Francois Bergeron. 2017. Green Practice Motivators and Performance in SMEs: A Qualitative Comparative Analysis. Journal of Small Business Strategy 27: 1–18. [Google Scholar]

- Rhim, Jong C., Joy V. Peluchette, and Inam Song. 2006. Stock market reactions and firm performance surrounding CEO succession: Antecedents of succession and successor origin. American Journal of Business 21: 21–30. [Google Scholar] [CrossRef]

- Russo, Angeloantonio, and Antonio Tencati. 2009. Formal vs. informal CSR strategies: Evidence from Italian micro, small, medium-sized, and large firms. Journal of Business Ethics 85: 339–53. [Google Scholar] [CrossRef]

- Saeed, Abubakr, and Hafiz Muhammad Ziaulhaq. 2019. The Impact of CEO Characteristics on the Internationalization of SMEs: Evidence from the UK. Canadian Journal of Administrative Sciences 36: 322–35. [Google Scholar] [CrossRef]

- Schaefer, Anja, Sarah Williams, and Richard Blundel. 2020. Individual Values and SME Environmental Engagement. Business & Society 59: 642–75. [Google Scholar]

- Schwartz, Shalom H. 1994. Are there universal aspects in the structure and contents of human values? Journal of Social Issues 50: 19–45. [Google Scholar] [CrossRef]

- Schwartz, Shalom H. 2012. An Overview of the Schwartz Theory of Basic Values. Online Readings in Psychology and Culture 2: 2307-0919. [Google Scholar] [CrossRef]

- Schwartz, Shalom H., and Wolfgang Bilsky. 1987. Toward a universal psychological structure of human values. Journal of Personality and Social Psychology 53: 550–62. [Google Scholar] [CrossRef]

- Simon, Herbert Alexander. 1982. Models of Bounded Rationality. In Behavioral Economics and Business Organizations. Cambridge: MIT Press. [Google Scholar]

- Spence, Laura J. 2007. CSR and small business in a European policy context: The five “C”s of CSR and small business research agenda 2007. Business and Society Review 112: 533–52. [Google Scholar] [CrossRef]

- Spence, Laura J. 2016. Small business social responsibility: Expanding core CSR theory. Business and Society 55: 23–55. [Google Scholar] [CrossRef]

- Spence, Laura J., and José Félix Lozano. 2000. Communicating about ethics with small firms: Experiences from the UK and Spain. Journal of Business Ethics 27: 43–53. [Google Scholar] [CrossRef]

- Spence, Laura J., René Schmidpeter, and André Habisch. 2003. Assessing social capital: Small and medium sized enterprises in Germany and the UK. Journal of Business Ethics 47: 17–29. [Google Scholar] [CrossRef]

- Toft, Jon, and Rainer Lueg. 2015. Does EVA beat earnings? A literature review of the evidence since Biddle et al. (1997). Corporate Ownership and Control 12: 8–18. [Google Scholar] [CrossRef]

- Torres, Olivier. 2000. Du rôle et de l’importance de la proximité dans la spécificité de gestion des PME. Paper presented at 5ème Congrès International Francophone PME (CIFPME), Lille, France, October 25–27. [Google Scholar]

- Torrès, Olivier. 2003. Petitesse des entreprises et grossissement des effets de proximité. Revue Française de Gestion 144: 119–38. [Google Scholar] [CrossRef]

- Van Marrewijk, Marcel, and Marco Werre. 2003. Multiple levels of corporate sustainability. Journal of Business Ethics 44: 107–19. [Google Scholar] [CrossRef]

- Verhees, Frans J. H. M., and Matthew T. G. Meulenberg. 2004. Market Orientation, Innovativeness, Product Innovation, and Performance in Small Firms. Journal of Small Business Management 42: 134–54. [Google Scholar] [CrossRef]

- VHB (Verband der Hochschullehrer für Betriebswirtschaft). 2020. JOURQUAL3: Methode. Available online: https://vhbonline.org/en/vhb4you/vhb-jourqual/vhb-jourqual-3/complete-list (accessed on 1 May 2020).

- von Weltzien Hoivik, Heidi, and Domènec Melé. 2009. Can an SME become a global corporate citizen? Evidence from a case study. Journal of Business Ethics 88: 551–63. [Google Scholar] [CrossRef]

- von Weltzien Høivik, Heidi, and Deepthi Shankar. 2011. How can SMEs in a cluster respond to global demands for corporate responsibility? Journal of Business Ethics 101: 175–95. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kutzschbach, J.; Tanikulova, P.; Lueg, R. The Role of Top Managers in Implementing Corporate Sustainability—A Systematic Literature Review on Small and Medium-Sized Enterprises. Adm. Sci. 2021, 11, 44. https://doi.org/10.3390/admsci11020044

Kutzschbach J, Tanikulova P, Lueg R. The Role of Top Managers in Implementing Corporate Sustainability—A Systematic Literature Review on Small and Medium-Sized Enterprises. Administrative Sciences. 2021; 11(2):44. https://doi.org/10.3390/admsci11020044

Chicago/Turabian StyleKutzschbach, Jannika, Parvina Tanikulova, and Rainer Lueg. 2021. "The Role of Top Managers in Implementing Corporate Sustainability—A Systematic Literature Review on Small and Medium-Sized Enterprises" Administrative Sciences 11, no. 2: 44. https://doi.org/10.3390/admsci11020044

APA StyleKutzschbach, J., Tanikulova, P., & Lueg, R. (2021). The Role of Top Managers in Implementing Corporate Sustainability—A Systematic Literature Review on Small and Medium-Sized Enterprises. Administrative Sciences, 11(2), 44. https://doi.org/10.3390/admsci11020044