Performance of Survey Forecasts by Professional Analysts: Did the European Debt Crisis Make it Harder or Perhaps Even Easier?

Abstract

:1. Introduction

2. ECB and the Financial Crisis

3. Literature Review

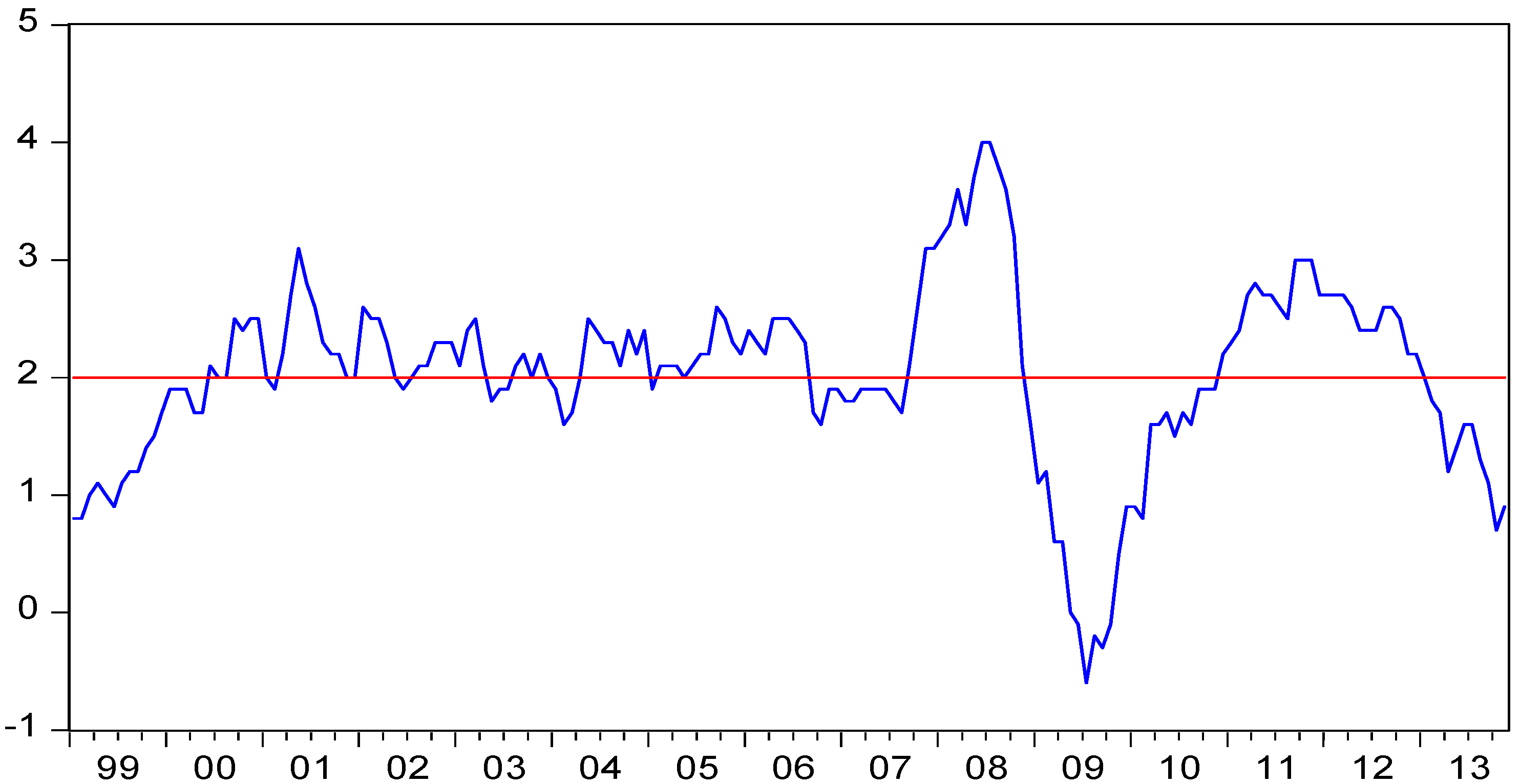

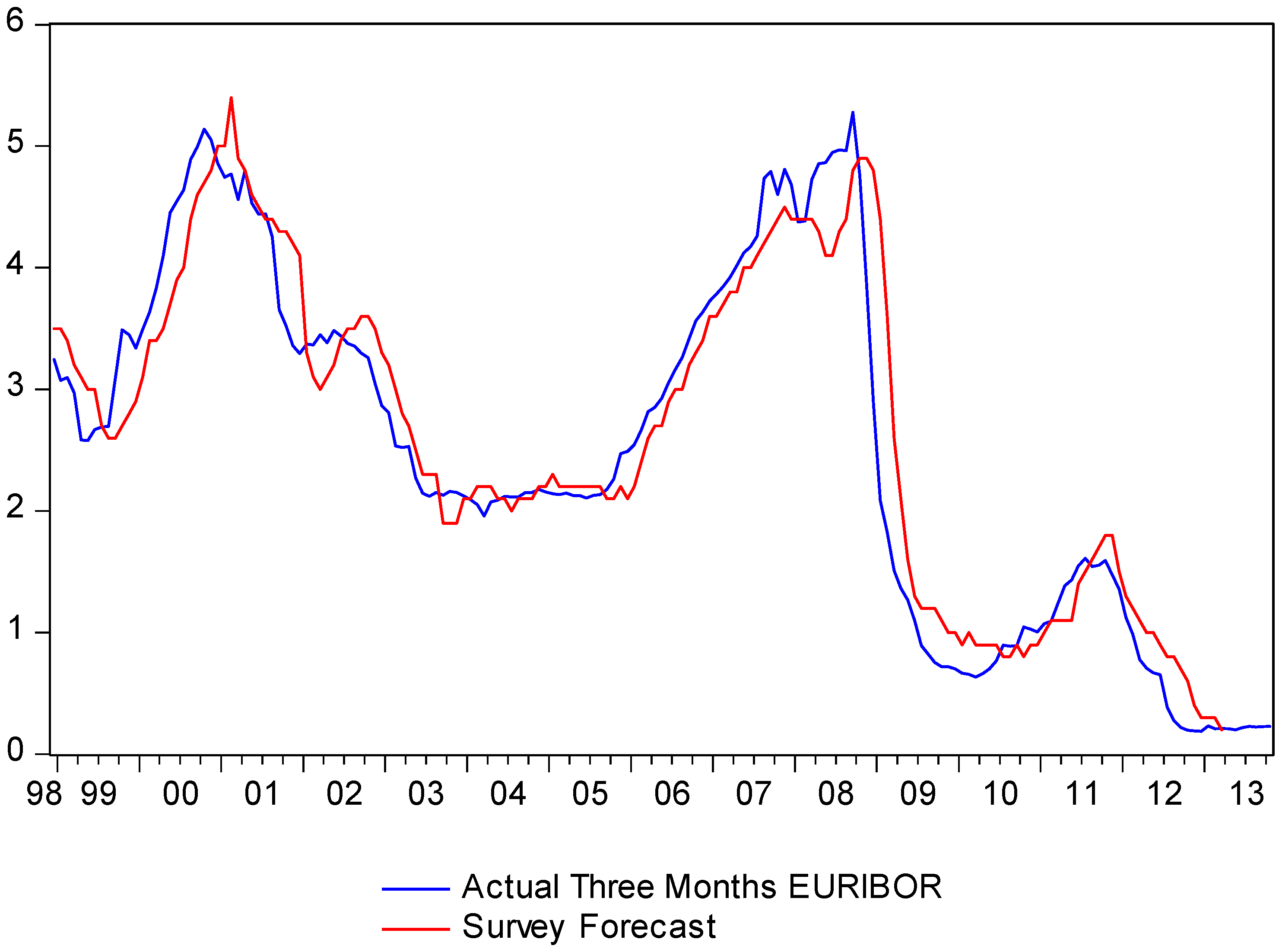

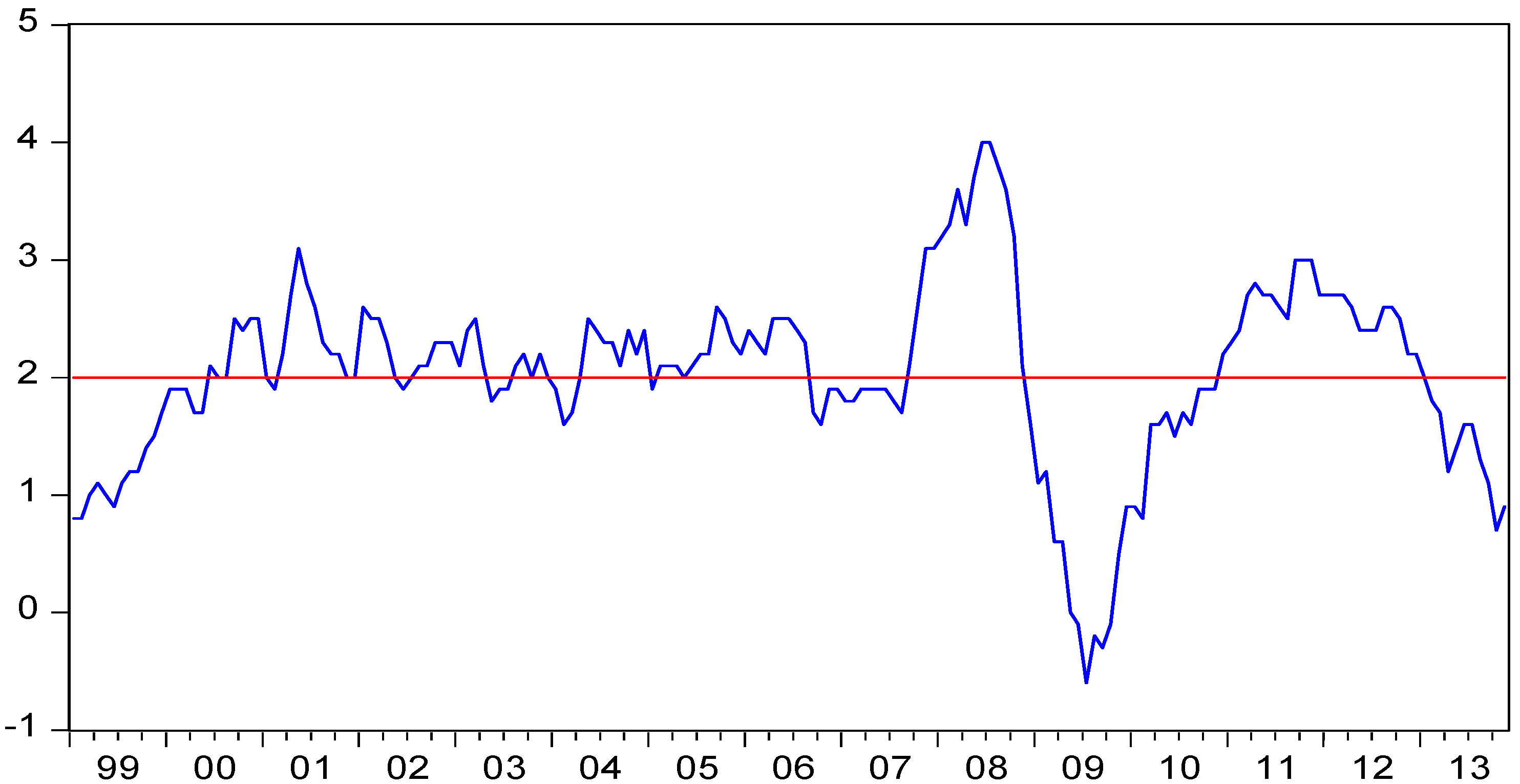

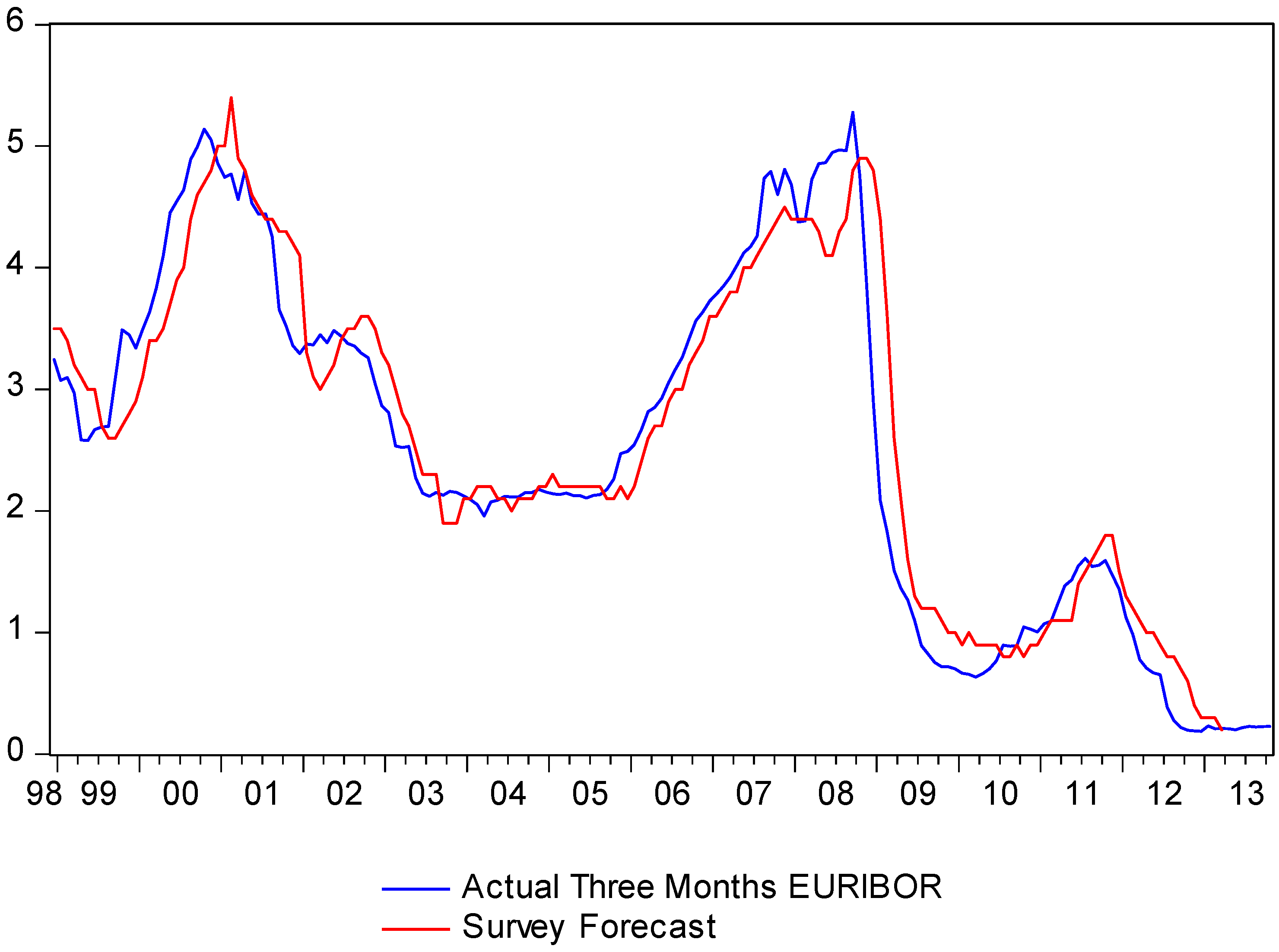

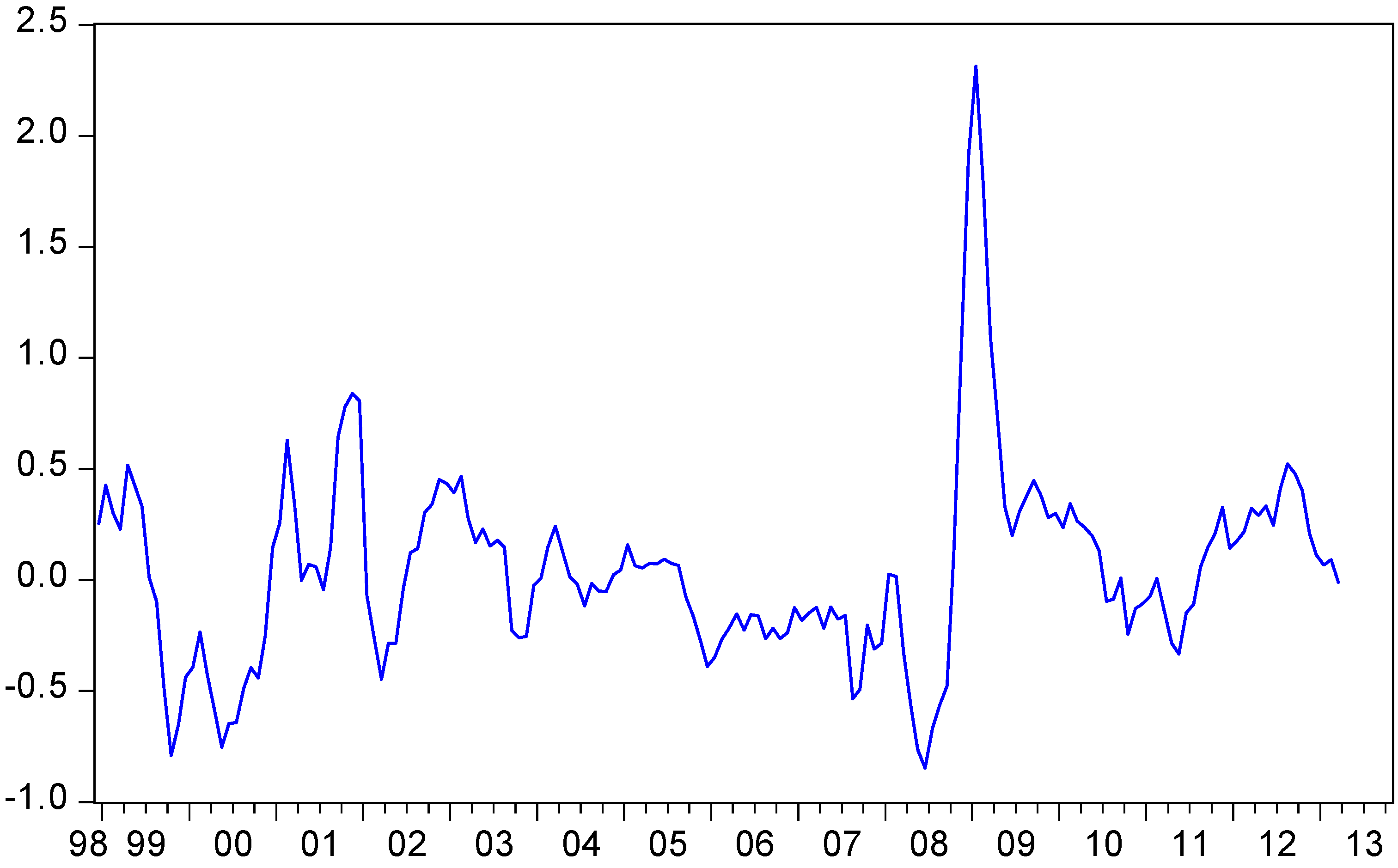

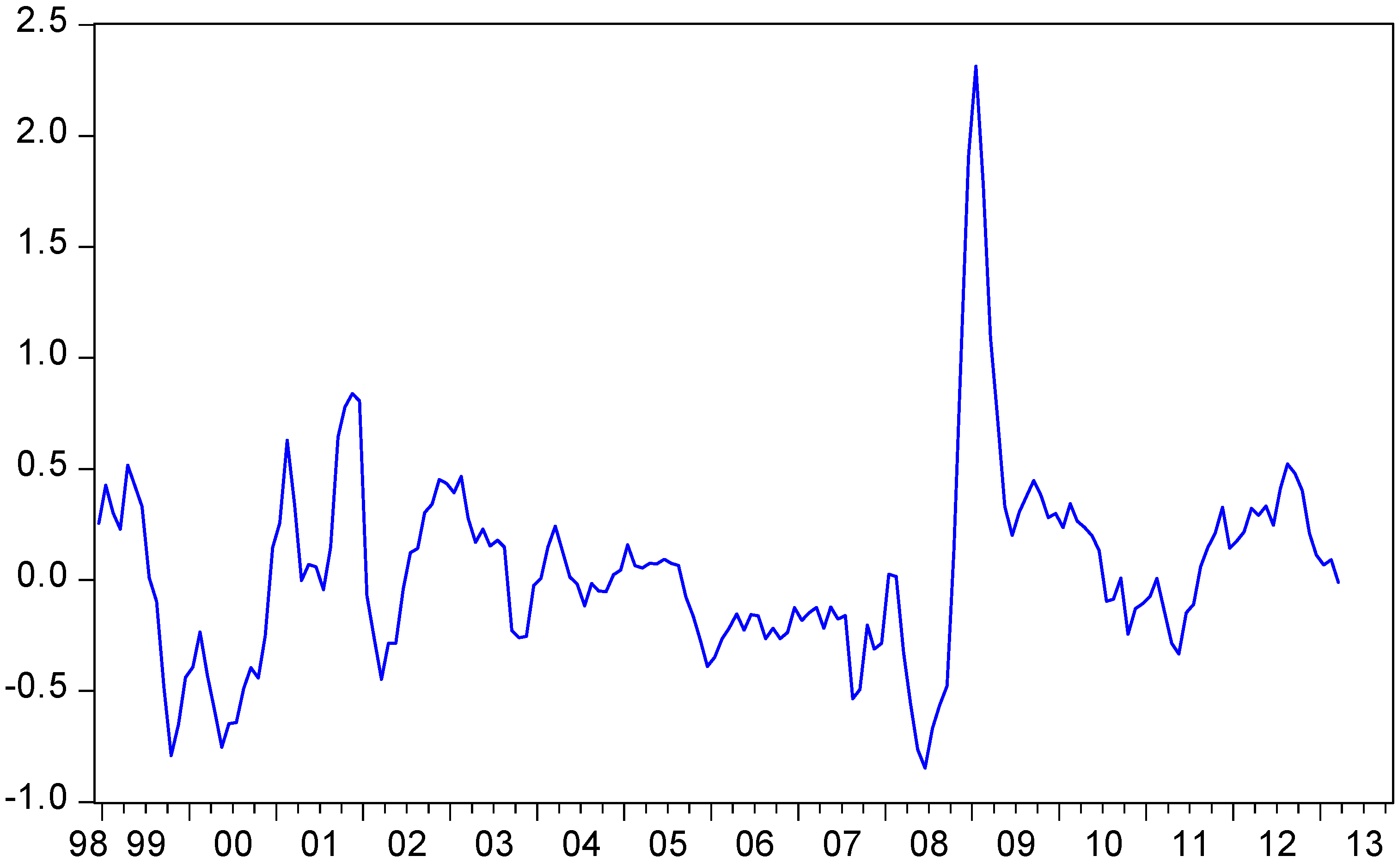

4. Data and Methodology

{kind=link}

{kind=link}

{kind=link}

| Null Hypothesis: Three-Month EURIBOR has a unit root | ||||

| Exogenous: Constant | ||||

| Bandwidth: 8 (Newey-West automatic) using Bartlett kernel | ||||

| Adj. t-Stat | Prob.* | |||

| Phillips-Perron test statistic | −1.205573 | 0.6718 | ||

| Test critical values: | 1% level | −3.467205 | ||

| 5% level | −2.877636 | |||

| 10% level | −2.575430 | |||

| Null Hypothesis: Survey Forecast has a unit root | ||||

| Exogenous: Constant | ||||

| Bandwidth: 8 (Newey-West automatic) using Bartlett kernel | ||||

| Adj. t-Stat | Prob.* | |||

| Phillips-Perron test statistic | −1.197263 | 0.6753 | ||

| Test critical values: | 1% level | −3.468749 | ||

| 5% level | −2.878311 | |||

| 10% level | −2.575791 | |||

5. Empirical Results

| Quandt-Andrews unknown breakpoint test | ||

| Null Hypothesis: No breakpoints within 15% trimmed data | ||

| Varying regressors: All equation variables | ||

| Equation Sample: 1999M02 2013M03 | ||

| Test Sample: 2001M04 2011M02 | ||

| Number of breaks compared: 119 | ||

| Statistic | Value | Prob. |

| Maximum LR F-statistic (2008M11) | 9.462575 | 0.0001 |

| Maximum Wald F-statistic (2008M11) | 28.38772 | 0.0001 |

| Exp LR F-statistic | 1.329651 | 0.0647 |

| Exp Wald F-statistic | 9.437692 | 0.0010 |

| Ave LR F-statistic | 1.626766 | 0.1190 |

| Ave Wald F-statistic | 4.880299 | 0.1190 |

| Measure | 1999/04–2013/03 | 1999/04–2008/11 | 2008/12–2013/03 |

|---|---|---|---|

| Theil’s U | 0.7454545 | 0.8460556 | 0.6893854 |

| Theil’s Ur | 0.8711607 | 0.8262579 | 0.8834104 |

6. Conclusions

Author Contributions

Acknowledgements

Conflicts of Interest

References and Notes

- Conference of the Representatives of the Governments of the Member States. “Consolidated version of the Treaty on the Functioning of the European Union.” European Union, 2008/C 115/01.

- Patricia Pollard. “A Look Inside two Central Banks: The European Central Bank and the Federal Reserve.” Federal Reserve Bank of St. Louis Review 85 (2008): 11–30. [Google Scholar]

- Willem Thorbecke. “A dual mandate for the federal reserve: The pursuit of price stability and full employment.” Eastern Economic Association 28, no. 2 (2003): 255–68. [Google Scholar]

- Tore Ellingsen, and Ulf Söderström. “Monetary Policy and Market Interest Rates.” The American Economic Review 91, no. 5 (2000): 1594–607. [Google Scholar] [CrossRef]

- John B. Taylor. “Discretion versus policy rules in practice.” Carnegie-Rochester Conference Series on Public Policy 39 (1993): 195–214. [Google Scholar] [CrossRef]

- Richard Clarida, Jordi Galí, and Mark Gertler. “Monetary policy rules in practice: Some International Evidence.” European Economic Review 42, no. 6 (1998): 1033–67. [Google Scholar] [CrossRef]

- Richard Clarida, Jordi Galí, and Mark Gertler. “Monetary policy rules and macroeconomic stability: Evidence and some Theory.” Quarterly Journal of Economics 115 (2000): 147–80. [Google Scholar] [CrossRef]

- Katrin Ullrich. “A comparison between the Fed and the ECB: Taylor rules.” ZEW Discussion Papers 03–19 (2003): 1–35. [Google Scholar] [CrossRef]

- Ansgar Belke, and Jens Klose. “Does the ECB Rely on a Taylor Rule during the Financial Crisis? Comparing Ex-post and Real Time Data with Real Time Forecasts.” Economic Analysis and Policy 41, no. 2 (2011): 147–71. [Google Scholar] [CrossRef]

- Dieter Gerdesmeier, and Barbara Roffia. “Taylor Rules for the Euro Area: The Issue of Real-time Data.” Discussion paper Series Volkswirtschaftliches Forschungszentrum der Deutschen Bundesbank 37 (2004): 1–44. [Google Scholar]

- Ansgar Belke. “Non-standard Monetary Policy Measures: Magic Wand or Tiger by the Tail? ” Ruhr Economic Papers 447 (2013): 1–32. [Google Scholar] [CrossRef]

- Mario Draghi. “ECB Press Conference July.” Frankfurt am Main, Germany, 4 July 2013.

- Mohamed A. El-Erian. “Evolution, Impact, and Limitations of Unusual Central Bank Policy Activism.” Federal Reserve Bank of St. Louis Review 94 (2012): 243–64. [Google Scholar]

- Brett W. Fawley, and Christopher C. Neely. “Four Stories of Quantitative Easing.” Federal Reserve Bank of St. Louis Review 95 (2013): 51–88. [Google Scholar]

- Henri Theil. “Who forecasts best? ” International Economic Papers 5 (1955): 194–99. [Google Scholar]

- Oliver Guedj, and Jean-Philipee Bouchaud. “Experts’ Earning Forecasts: Bias, Herding, and Gossamer Information.” International Journal of Theoretical and Applied Finance 8, no. 7 (2005): 933–46. [Google Scholar] [CrossRef]

- Markus Spiwoks, and Oliver Hein. “Die Währungs-, Anleihen- und Aktienmartkprognosen des Zentrums für Europäische Wirtschaftsforschung – Eine empirische Untersuchung des Prognoseerfolges von 1995 bis 2004.” Wirt. Sozialstat Archiv 1 (2007): 43–52. [Google Scholar] [CrossRef]

- Wolfgang Bessler, and Matthias Stanzel. “Qualität und Effizienz der Gewinnprognosen von Analysten – Eine empirische Untersuchung für den deutschen Kapitalmarkt.” Kredit und Kapital 40, no. 1 (2007): 89–129. [Google Scholar]

- Kon S. Lai. “An Evaluation of Survey Exchange Rate Forecasts.” Economic Letters 32 (1990): 61–65. [Google Scholar] [CrossRef]

- Pasquale Della Corte, and Ilias Tsiakas. “Statistical and Economic Methods for Evaluating Exchange Rate Predictability.” In Handbook of Exchange Rates, rev. ed. London: Wiley, 2012. [Google Scholar]

- Benjamin M. Friedman. “Survey Evidence on the “rationality” of interest rate expectations.” Journal of Monetary Economics 6, no. 4 (1980): 453–65. [Google Scholar]

- Michael T. Belongia. “Predicting Interest Rates: A Comparison of Professional and market-based Forecasts.” Federal Reserve Bank of St. Louis Review, 1987, 9–15. [Google Scholar]

- Zulia Gubaydullina, Oliver Hein, and Markus Spiwoks. “The Status Quo Bias of Bond Market Analysts.” Journal of Applied Finance & Banking 1, no. 1 (2011): 31–51. [Google Scholar]

- Georgios Chortareas, Boonlert Jitmaneeroj, and Andrew Wood. “Forecast Rationality and Monetary Policy Frameworks: Evidence from UK Interest Rate Forecasts.” Journal of International Financial Markets, Institutions and Money 22, no. 1 (2012): 209–31. [Google Scholar] [CrossRef]

- Christoph Schwarzbach, Frederik Kunze, Norman Rudschuck, and Torsten Windels. “Asset Management in the German Insurance Industry: The Quality of Interest Rate Forecasts.” Zeitschrift für die gesamte Versicherungswissenschaft 101, no. 5 (2012): 693–703. [Google Scholar] [CrossRef]

- Markus Spiwoks, Nils Bedke, and Oliver Hein. “The Pessimism of Swiss Bond Market Analysts and the Limits of the Sign Accuracy Test – An Empirical Investigation of Their Forecasting Success between 1998 and 2007.” International Bulletin of Business Administration 4 (2009): 6–19. [Google Scholar]

- Frederik Kunze, Jens Kramer, and Norman Rudschuck. “Interest Rate Forecasts in Times of Financial Crisis: What Might be Interesting to Know? ” European Journal of Political Economy, 2013, in press. [Google Scholar] [CrossRef]

- Markus Spiwoks, Nils Bedke, and Oliver Hein. “Topically Orientated Trend Adjustment and Autocorrelation of the Residuals - An Empirical Investigation of the Forecasting Behavior of Bond Market Analysts in Germany.” Journal of Money, Investment and Banking 14 (2010): 16–35. [Google Scholar]

- Markus Spiwoks, Nils Bedke, and Oliver Hein. “Forecasting the Past: The Case of US Interest Rate Forecasts.” Financial Markets and Portfolio Management 22 (2008): 357–79. [Google Scholar] [CrossRef]

- Tobias Basse, Meik Friedrich, and Anne Kleffner. “Italian Government Debt and Sovereign Credit Risk: An Empirical Exploration and some Thoughts about Consequences for European Insurers.” Zeitschrift für die gesamte Versicherungswissenschaft 101, no. 5 (2012): 571–79. [Google Scholar] [CrossRef]

- Mario Gruppe, and Carsten Lange. “Spain and the European sovereign debt crisis.” European Journal of Political Economy, 2013, in press. [Google Scholar] [CrossRef]

- Tobias Basse. “Searching for the EMU Core Member Countries.” European Journal of Political Economy, 2013, in press. [Google Scholar] [CrossRef]

- Claus Brand, Daniel Buncic, and Jarkko Turunen. “The Impact of ECB Monetary Policy Decisions and Communication on the Yield Curve.” Journal of the European Economic Association 8, no. 6 (2010): 1266–98. [Google Scholar] [CrossRef]

- Henri Theil. Applied Economic Forecasting, rev. ed. Amsterdam: North-Holland Publishing Company, 1966. [Google Scholar]

- Rob J. Hyndman. Forecasting with Exponential Smoothing: The State Space Approach, rev. ed. Springer-Verlag: Berlin Heidelberg, 2008. [Google Scholar]

- Peter Andres, and Markus Spiwoks. “Prognosegütemaße: State of the Art der statistischen Ex-post-Beurteilung von Prognosen.” In Sofia-Studien zur Institutionenanalyse. Darmstadt, 2000, Nr. 00-1. [Google Scholar]

- Donald W.K. Andrews. “Tests for Parameter Instability and Structural Change with Unknown Change Point.” Econometrica: Journal of the Econometric Society 61, no. 4 (1993): 821–56. [Google Scholar] [CrossRef]

- Bruce E. Hansen. “Approximate Asymptotic P Values for Structural-Change Tests.” Journal of Business and Economic Statistics 15, no. 1 (1997): 60–67. [Google Scholar] [CrossRef]

© 2014 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Kunze, F.; Gruppe, M. Performance of Survey Forecasts by Professional Analysts: Did the European Debt Crisis Make it Harder or Perhaps Even Easier? Soc. Sci. 2014, 3, 128-139. https://doi.org/10.3390/socsci3010128

Kunze F, Gruppe M. Performance of Survey Forecasts by Professional Analysts: Did the European Debt Crisis Make it Harder or Perhaps Even Easier? Social Sciences. 2014; 3(1):128-139. https://doi.org/10.3390/socsci3010128

Chicago/Turabian StyleKunze, Frederik, and Mario Gruppe. 2014. "Performance of Survey Forecasts by Professional Analysts: Did the European Debt Crisis Make it Harder or Perhaps Even Easier?" Social Sciences 3, no. 1: 128-139. https://doi.org/10.3390/socsci3010128

APA StyleKunze, F., & Gruppe, M. (2014). Performance of Survey Forecasts by Professional Analysts: Did the European Debt Crisis Make it Harder or Perhaps Even Easier? Social Sciences, 3(1), 128-139. https://doi.org/10.3390/socsci3010128