How Has COVID-19 Affected the Public Auction Market?

Abstract

:1. Introduction

2. Data and Methods

2.1. Focus on Public Auction Results at the Top Three Auction Houses (Christie’s, Sotheby’s, and Phillips)

2.2. Live Auction versus Online Auction Definition

2.3. “12-Month Rolling” Analysis Based on the Auction Calendar

2.4. Adjustment for Inflation

- -

- Non-USD daily revenues have been converted to USD by using the Bank of England’s daily exchange rate on the day each auction was arranged (for live sales) and closed (for online only sales).

- -

- Monthly USD revenues were compiled and then adjusted for inflation by using the Consumer Price Index (CPI-U), provided by the U.S. Department of Labor Bureau of Labor Statistics. November 2007 was used as a basis for comparison.

- -

- Twelve month rolling totals were then compiled using inflation adjusted monthly USD totals.

- -

- Index were created for each period based on what was considered as the first month of the crisis (October 2008 for the 2008–2009 financial crisis, October 2015 for the 2016 crisis, and October 2019 for the COVID-19 crisis).

3. Key Findings

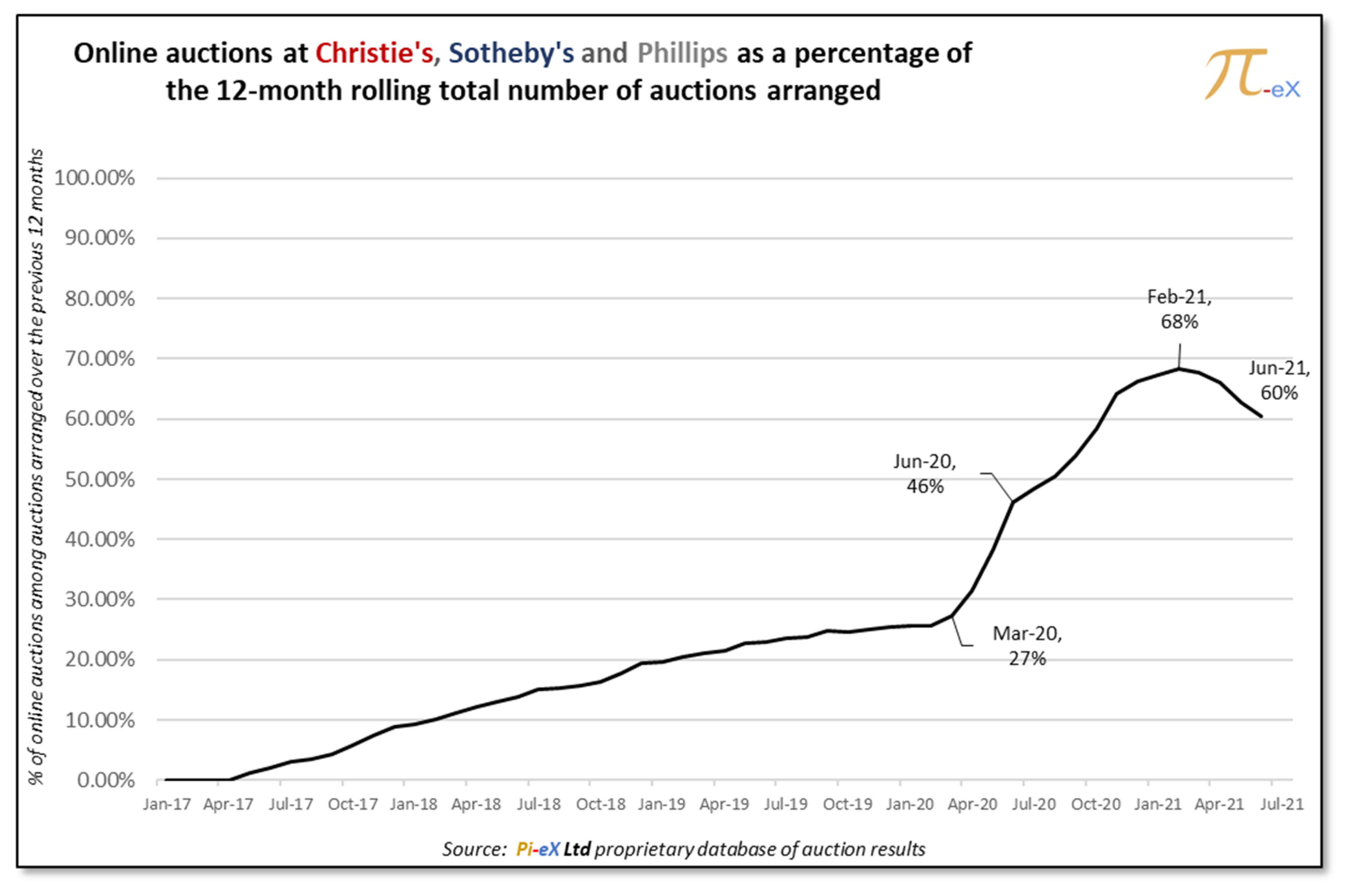

3.1. The Explosion of Online Auctions

3.2. Limitations of Online Auctions and the Rise of New Opportunities

3.3. Comparing the COVID-19 Crisis to Previous Art Market Crisis

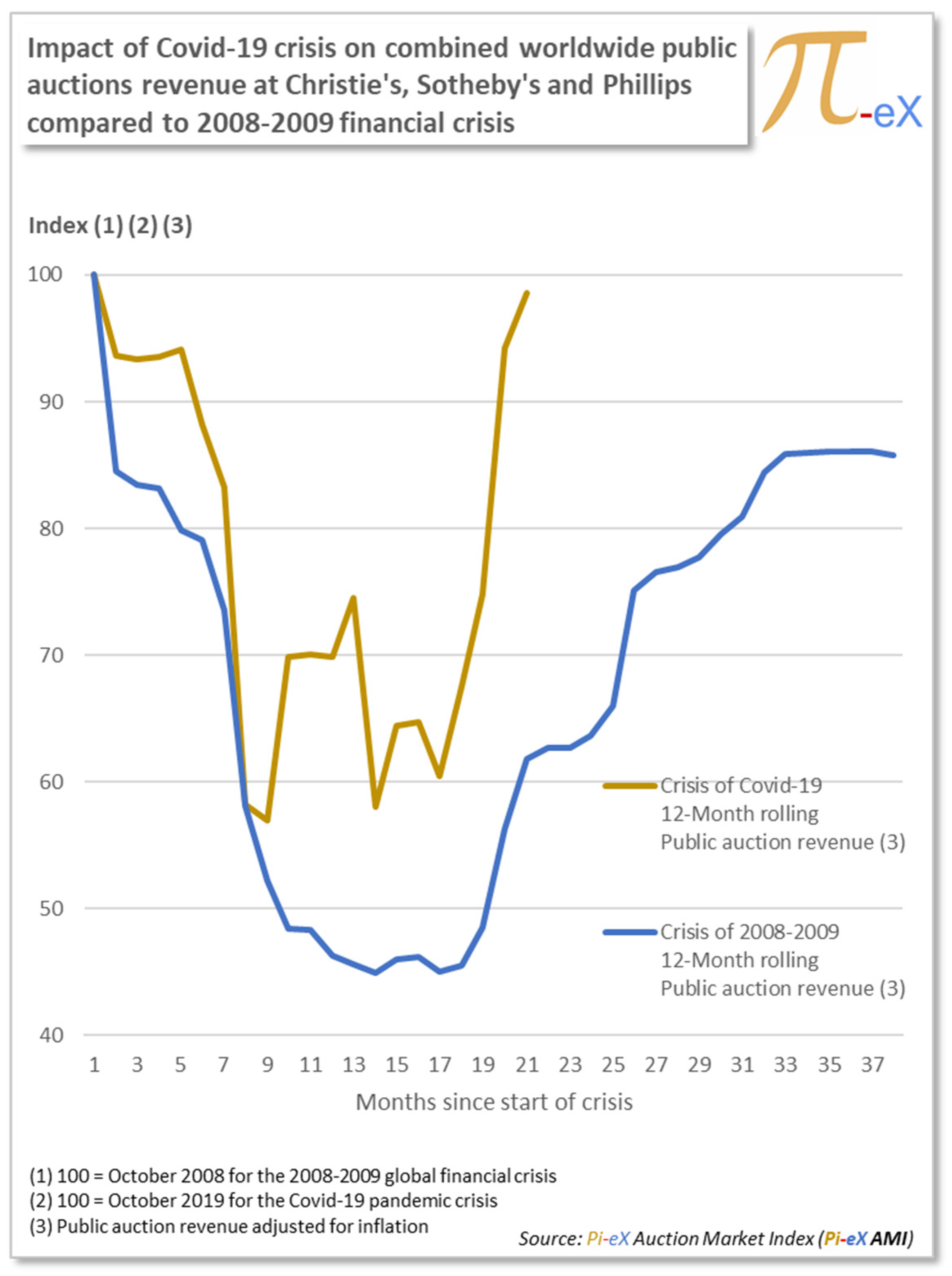

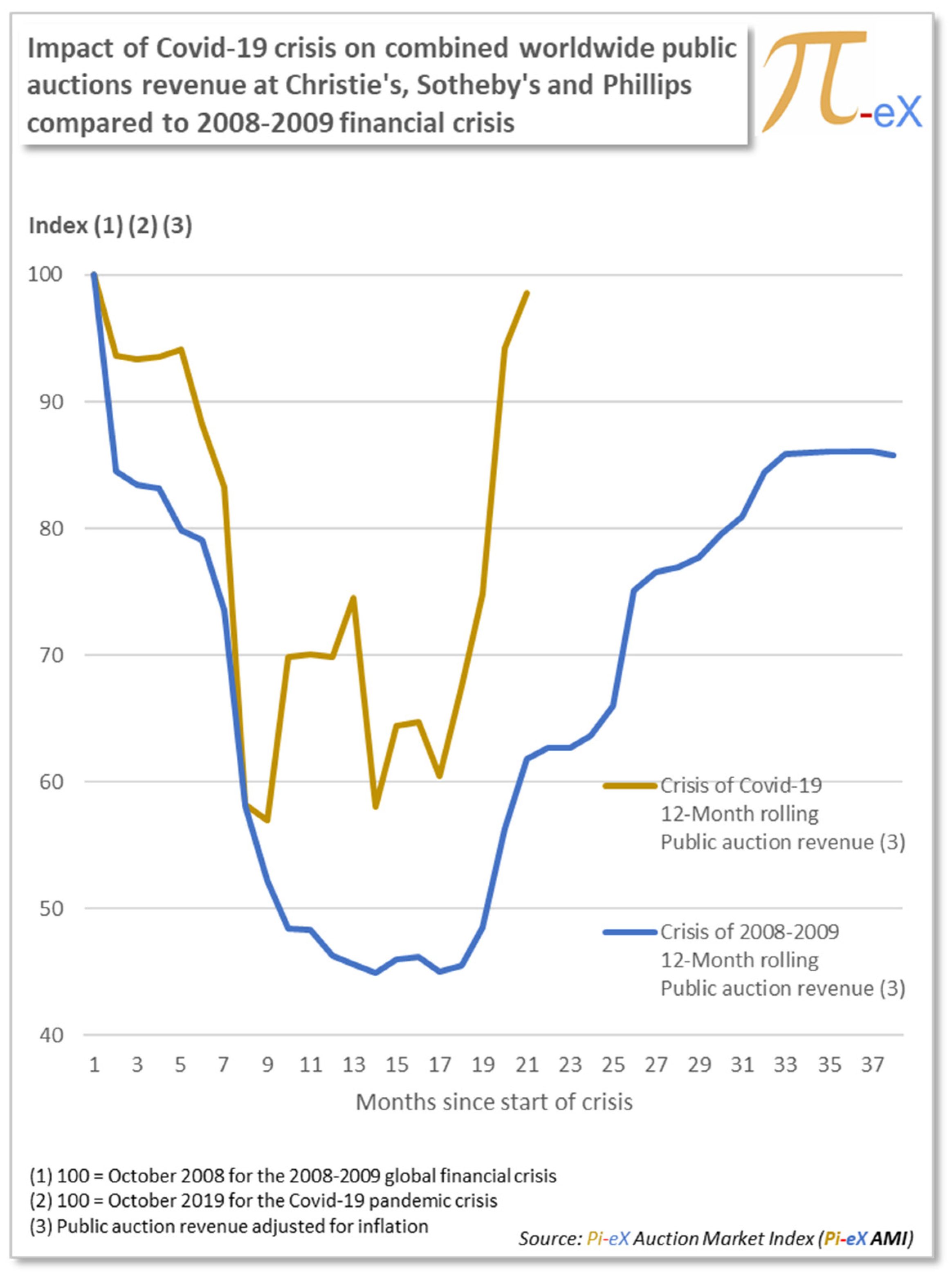

3.3.1. COVID-19 Crisis versus the 2008–2009 Financial Crisis

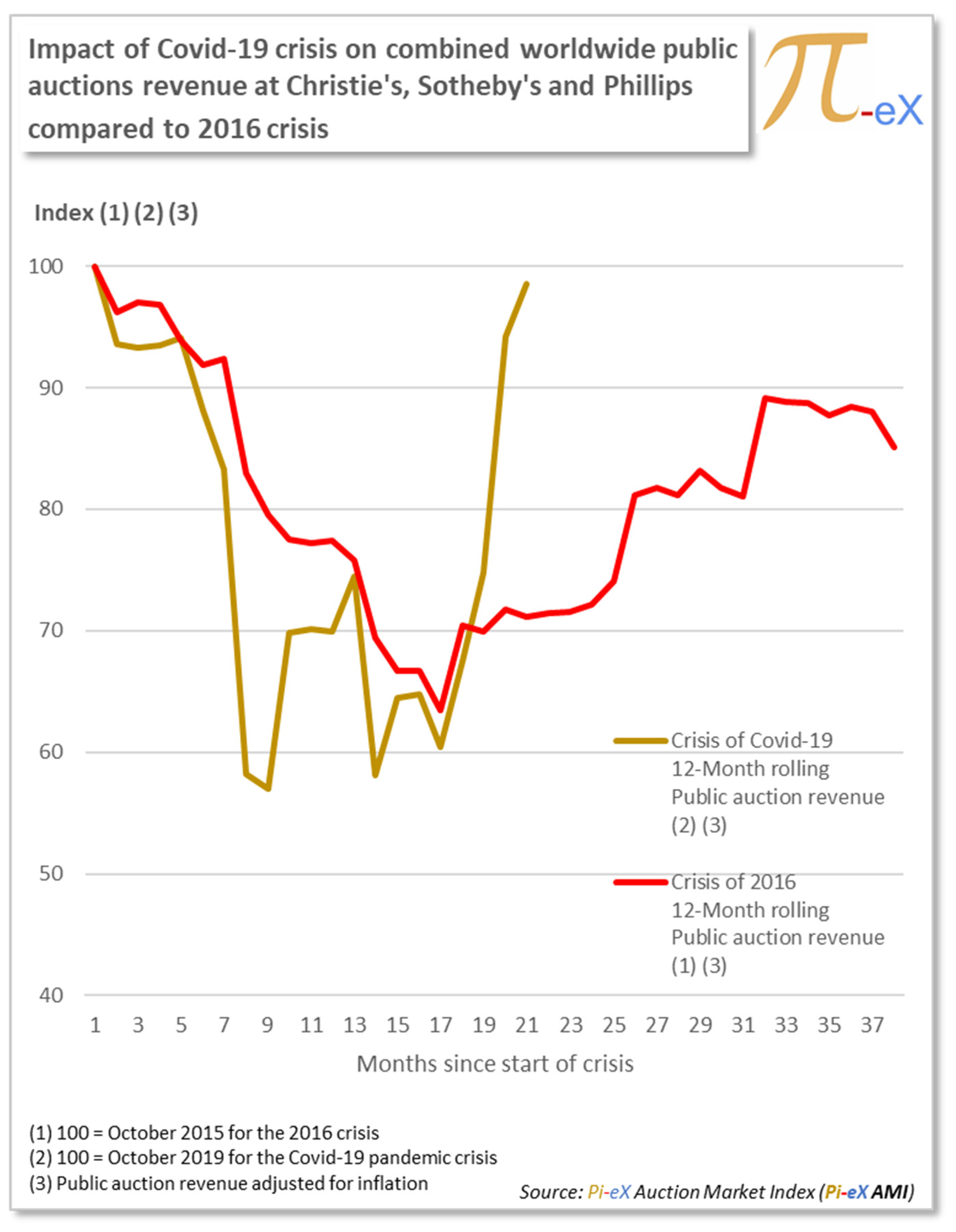

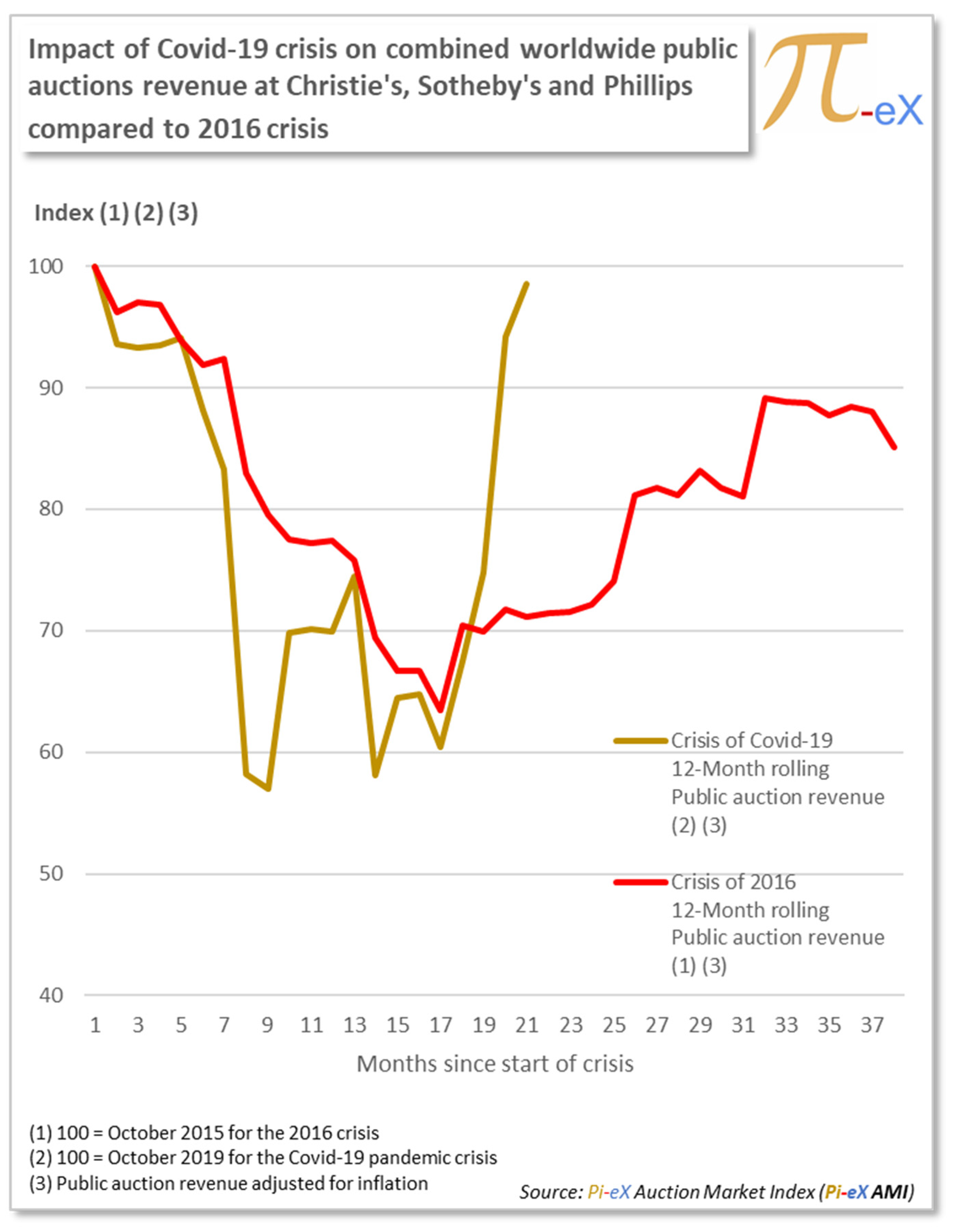

3.3.2. COVID-19 Crisis versus the 2016 Crisis

4. Conclusions

Funding

Data Availability Statement

Conflicts of Interest

| 1 | “Top Three Houses See 79 Percent Year-over-Year Drop in Second Quarter of 2020”, by Angelica Villa in August 2020, published by The Art Market Monitor (Villa 2020). |

| 2 | |

| 3 | In their article “Imperfect Data, Art Markets and Internet Research”, the authors highlight why current and aggregate data on auction markets, both offline and online, can be hard to come by. (Van Miegroet et al. 2019). |

| 4 | The dominance of Christie’s and Sotheby’s in the art market is highlighted in Don Thompson’s book “The Supermodel and the Brillo Box”, Part 4 “The Auction Houses” (Thompson 2014, p. 137). |

| 5 | In his book “Art Law and the Business of Art”, Martin Wilson, Chief General Councel, Phillips Auctioneers, describes in details the various forms of online auctions (Wilson 2019, chp. 7, p. 164). |

| 6 | The 2017 TEFAF Art Market Report (Pownall 2017) provides detailed information on the development of online sales and in particular the history of online sales at Christie’s and Sotheby’s. |

| 7 | “Christie’s Announces New $20 Million Investment as Digital Engagement Drives Growth in the Art Market”, Press Release by Christie’s to announce further investment in its digital platform (Christie’s 2014). |

| 8 | “Sotheby’s and the cybermasses: The most famous name in the art world has gone online. Does it know what it’s doing?”, in 29th January 2000 published in the Economist, see (The Economist 2000). |

| 9 | “Sotheby’s and Amazon.com Strike a Deal to Sell on Line”, by Carol Vogel in 17th June 1999 published in the New York Times, see (Vogel 1999). |

| 10 | “Live Auctions End at Christie’s South Ken. Will Online Sales Fill the Void?”, by Scott Reyburn in 21st July 2017published in the New York Times, see (Reyburn 2017b). |

| 11 | “Fewer and Smaller: A New Normal for London’s Summer Auctions”, Interview of Guillaume Cerutti by Scott Reyburn in 23rd June 2017 published in the New York Times, see (Reyburn 2017a). |

| 12 | “Sotheby’s Drops Buyer’s Premium for Online only Sales”, based on Sotheby’s CEO Letter to shareholders and clients released in 8-k filling with the SEC, see (Maneker 2017). |

| 13 | For further information on the state of the public auction market as of the end of the first semester 2020, see Sotheby’s Reports $2.5 Billion in Sales (Reyburn 2020). |

| 14 | As recently as April 2019, the chance of blockchain making an impact on the traditional art market was seen as distant (Ali et al. 2019). |

| 15 | See Artnet article “An NFT Artwork by Beeple Just Sold for an Unbelievable $69 Million at Christie’s—Making Him the Third Most Expensive Living Artist at Auction”, (Kinsella 2021). |

| 16 | See The Art Newspaper article “WTAF? Beeple NFT work sells for astonishing $69.3m at Christie’s after flurry of last-minute bids nearly crashes website”, (Jhala 2021). |

| 17 | For a state of AI-Generated Art sales at public auctions in the Fall of 2019, see (Goldstein 2019). |

| 18 | For a description of new speculative NFT buyers versus blue-chip art collectors, see the New York Times article “As Auctioneers and Artists Rush Into NFTs, Many Collectors Stay Away” (Small 2021). |

| 19 | “The Art Market 2017” published by Art Basel and UBS shows how Sales at public auction of fine and decorative art and antiques came under pressure in 2016 with aggreate value falling by 26% (McAndrew 2017). |

| 20 | “The Art Market 2021” published by Art Basel and UBS shows Sales at public auction of fine and decorative art and antiques suffered a decline of 30% in 2020 versus 2019 (McAndrew 2021). |

| 21 | Art Price report “2009 Art Market Trends” provides an annual reading of the impact of the 2008-2009 crisis versus previous years. |

| 22 | “Reconsidering hedonic art price indexes”, Economic Letters (Collins et al. 2009). |

| 23 | Broad analysis of the effect of the 2008–2009 financial crisis on financial markets “No Place To Hide: The Global Crisis in Equity Markets in 2008/09” (Bartram and Bodnar 2009). |

| 24 | Dynamics of public auctions transactions from 2002 to 2015 “Transformations of the Art Market in the World—Quantitative Approach” (Bialynicka-Birula 2017). |

| 25 | Analysis of art prices during macro economic cycles in the 21st century “The Art Market at Times of Economic Turbulence and High Inequality” (Solimano 2019). |

| 26 | Early impact of the COVID-19 pandemic on public auction trade “Top Auction Houses Saw 40 Percent Drop in Q1 Sales Revenue Because of Pandemic: Report” (Villa 2020). |

| 27 | Review of the art market in 2016 “The art market is a ‘catastrophe’” (Richter 2016). |

References

- Ali, Doha, Erin McDermott, Noah Michaud, and Mitchell Parekh. 2019. Online Auctions at Christie’s & Sotheby’s. DALMI Working Paper on Art & Markets No. 19213. Available online: https://www.dukedalmi.org/wpcontent/uploads/19213-Working-Paper.pdf (accessed on 20 October 2021).

- Bartram, Söhnke M., and Gordon M. Bodnar. 2009. No Place To Hide: The Global Crisis in Equity Markets in 2008/09. MPRA Paper No. 15955. Available online: https://mpra.ub.uni-muenchen.de/15955/ (accessed on 20 October 2021).

- Bialynicka-Birula, Joanna. 2017. Transformations of the Art Market in the World—Quantitative Approach. Institute of Economic Research Working Papers, No. 13/2017. Available online: http://hdl.handle.net/10419/219836 (accessed on 20 October 2021).

- Christie’s. 2014. Christie’s Announces New $20 Million Investment as Digital Engagement Drives Growth in the Art Market. Businesswire. Available online: https://www.businesswire.com/news/home/20140506006831/en/Christie%E2%80%99s-Announces-20-Million-Investment-Digital-Engagement (accessed on 20 October 2021).

- Collins, Alan, Antonello Scorcu, and Roberto Zanola. 2009. Reconsidering hedonic art price indexes. Economics Letters 104: 57–60. [Google Scholar] [CrossRef]

- Goldstein, Caroline. 2019. Has the AI-Generated Art Bubble Already Burst? Buyers Greeted Two Newly Offered Works at Sotheby’s with Lackluster Demand. Artnet News. Available online: https://news.artnet.com/market/obvious-art-sale-sothebys-1705608 (accessed on 27 June 2021).

- Jhala, Kabir. 2021. WTAF? Beeple NFT Work Sells for Astonishing $69.3m at Christie’s after Flurry of Last-Minute Bids Nearly Crashes Website. The Art Newspaper. Available online: https://www.theartnewspaper.com/2021/03/11/wtaf-beeple-nft-work-sells-for-astonishing-dollar693m-at-christies-after-flurry-of-last-minute-bids-nearly-crashes-website (accessed on 20 October 2021).

- Kinsella, Eileen. 2021. An NFT Artwork by Beeple Just Sold for an Unbelievable $69 Million at Christie’s—Making Him the Third Most Expensive Living Artist at Auction. Artnet. Available online: https://news.artnet.com/market/christies-nft-beeple-69-million-1951036 (accessed on 20 October 2021).

- Maneker, Marion. 2017. Sotheby’s Drops Buyer’s Premium for Online-Only Sales. Art Market Monitor. August. Available online: https://www.artmarketmonitor.com/2017/08/22/sothebys-drops-buyers-premium-for-online-only-sales/ (accessed on 20 October 2021).

- McAndrew, Clare. 2017. The Art Market 2017. Art Basel & UBS Report. Basel: Arts Economics. [Google Scholar]

- McAndrew, Clare. 2021. The Art Market 2021. Art Basel & UBS Report. Basel: Arts Economics. [Google Scholar]

- Pownall, Rachel. 2017. TEFAF Art Market Report. Maasatricht: The European Fine Art Foundation. [Google Scholar]

- Reyburn, Scott. 2017a. Fewer and Smaller: A New Normal for London’s Summer Auctions. New York Times. June. Available online: https://www.nytimes.com/2017/06/23/arts/christies-sothebys-london-art-auctions.html (accessed on 20 October 2021).

- Reyburn, Scott. 2017b. Live Auctions End at Christie’s South Ken. Will Online Sales Fill the Void? New York Times. July. Available online: https://www.nytimes.com/2017/07/21/arts/design/christies-south-kensington-auction.html (accessed on 20 October 2021).

- Reyburn, Scott. 2020. Sotheby’s Reports $2.5 Billion in Sales. New York Times. August. Available online: https://www.nytimes.com/2020/08/03/arts/design/sothebys-sales.html (accessed on 27 June 2021).

- Richter, Wolf. 2016. The Art Market is a ‘Catastrophe’. Business. Insider. Available online: https://www.businessinsider.com/the-art-market-is-a-catastrophe-2016-5?r=US&IR=T (accessed on 20 October 2021).

- Small, Zachary. 2021. As Auctioneers and Artists Rush into NFTs, Many Collectors Stay Away. New York Times. Available online: https://www.nytimes.com/2021/04/28/arts/design/nfts-art-collectors-copyright.html (accessed on 20 October 2021).

- Solimano, Andres. 2019. The Art Market at Times of Economic Turbulence and High Inequality. European Investment Bank. Available online: https://institute.eib.org/wp-content/uploads/2019/06/Art-Market-Economic-Trubulence-Inequality-Paper-Solimano.pdf (accessed on 20 October 2021).

- The Economist. 2000. Sotheby’s and the Cybermasses: The Most Famous Name in the Art World Has Gone Online. Does It Know What It’s Doing? The Economist. January. Available online: https://www.economist.com/moreover/2000/01/27/sothebys-and-the-cybermasses (accessed on 20 October 2021).

- Thompson, Donald N. 2014. The Supermodel and the Brillo Box. Houndmills: Palgrave McMillan, pp. 137–38. [Google Scholar]

- Van Miegroet, Hans J., Kaylee P. Alexander, and Leunissen Fiene. 2019. Imperfect Data, Art Markets and Internet Research. Arts 8: 76. [Google Scholar] [CrossRef] [Green Version]

- Villa, Angelica. 2020. Top Three Houses See 79 Percent Year-over-Year Drop in Second Quarter of 2020: Report. Art Market Monitor. August. Available online: https://www.artmarketmonitor.com/2020/08/05/top-three-houses-see-79-percent-year-over-year-drop-in-second-quarter-of-2020-report/ (accessed on 27 June 2021).

- Vogel, Carol. 1999. Sotheby’s and Amazon.com Strike a Deal to Sell on line. New York Times. June. Available online: https://www.nytimes.com/1999/06/17/business/sotheby-s-and-amazoncom-strike-a-deal-to-sell-on-line.html (accessed on 20 October 2021).

- Wilson, Martin. 2019. Art Law and the Business of Art. Cheltenham: Edward Elgar Publishing, pp. 164–71. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

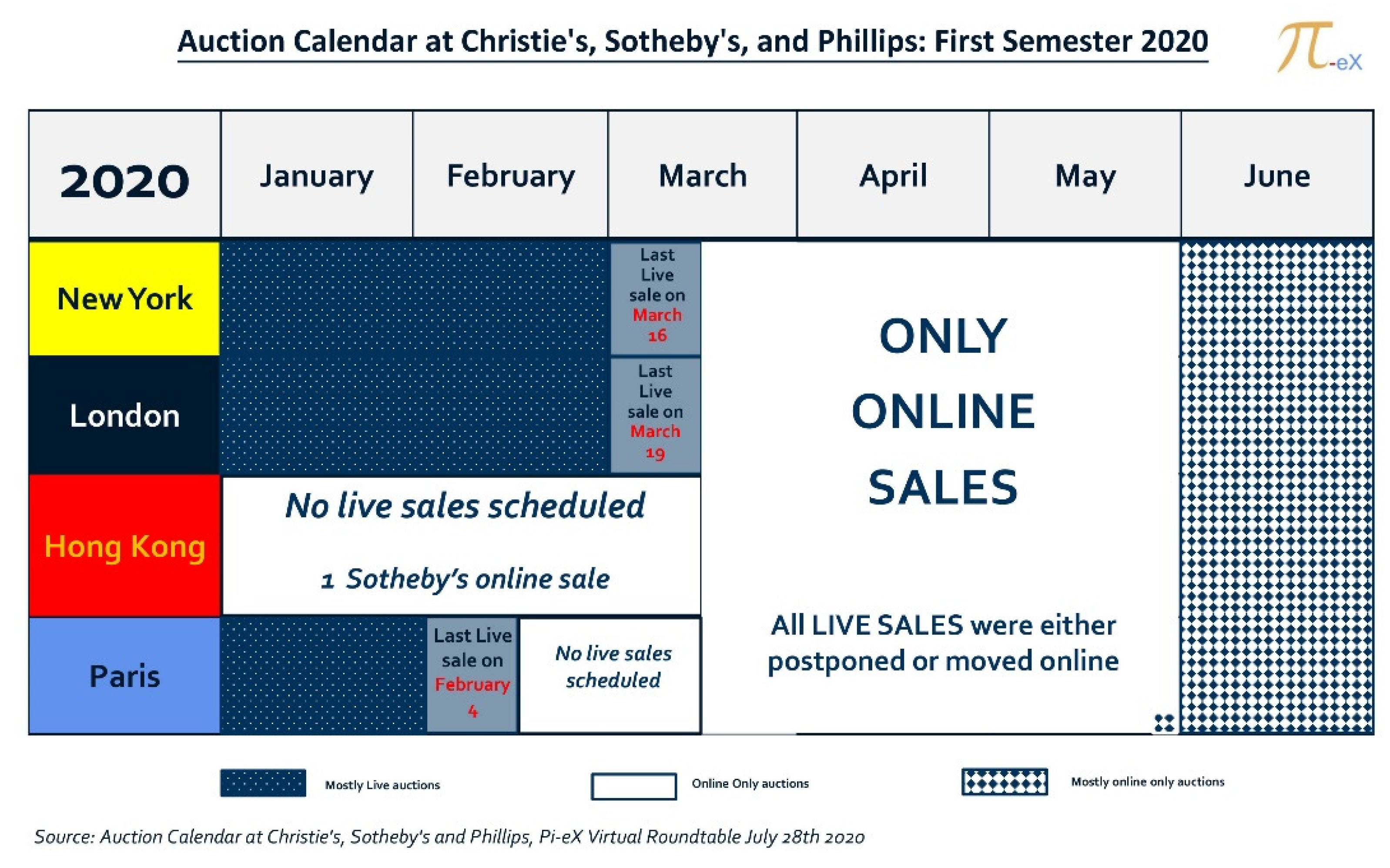

| City | Last Live Auction before First Covid Lockdown | First Live Auction after First Covid Lockdown |

|---|---|---|

| New York | 16 March 2020 | 18 June 2020 |

| London | 19 March 2020 | 10 June 2020 |

| Hong Kong | 8 December 2019 | 5 June 2020 |

| Paris | 4 February 2020 | 26 May 2020 |

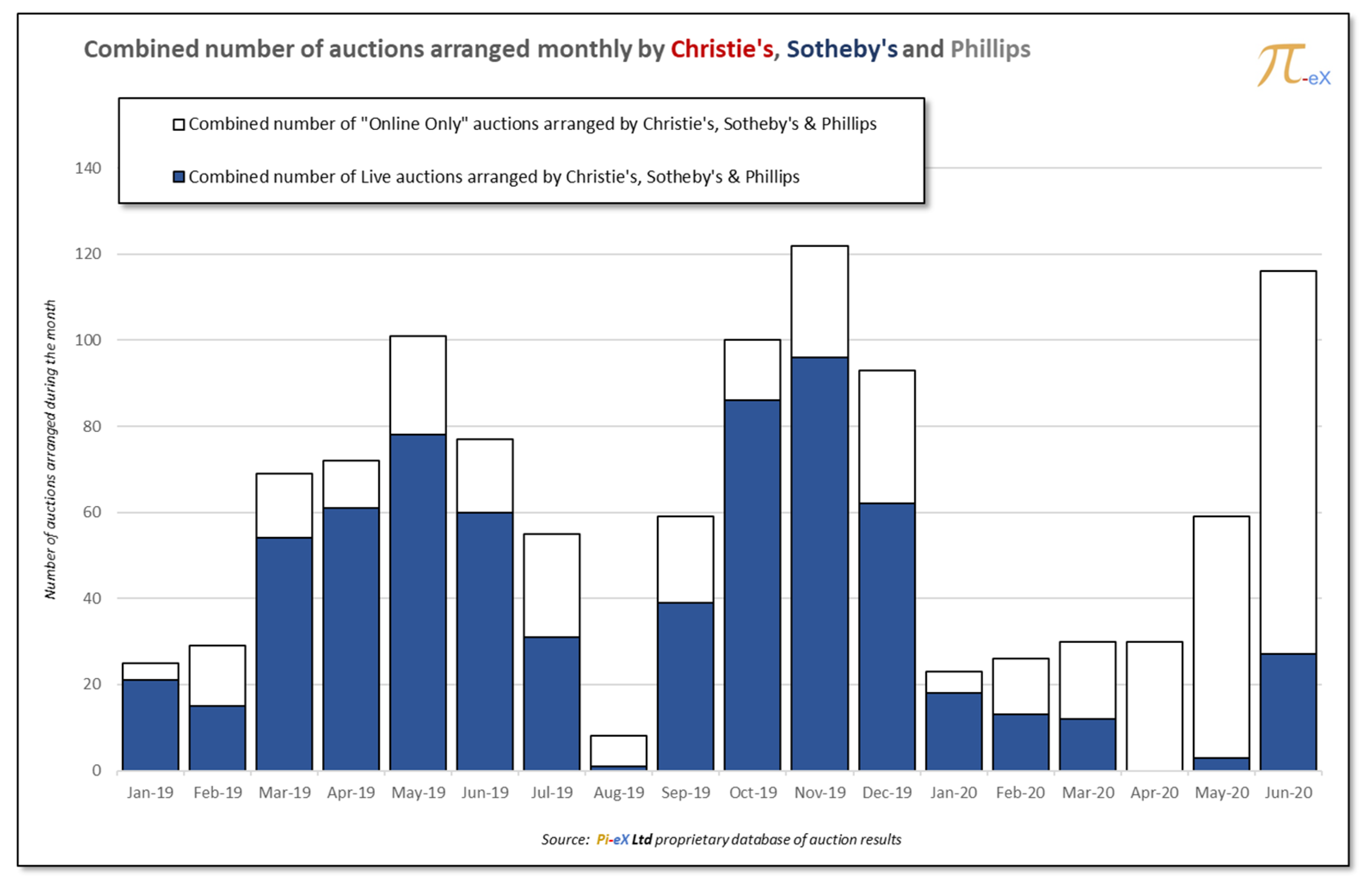

| Number of Auctions Arranged by Christie’s, Sotheby’s, and Phillips | Live Auctions | Online only Auctions | ||

|---|---|---|---|---|

| # per Month | % of Total | # per Month | % of Total | |

| Jan-19 | 21 | 84% | 4 | 16% |

| Feb-19 | 15 | 52% | 14 | 48% |

| Mar-19 | 54 | 78% | 15 | 22% |

| Apr-19 | 61 | 85% | 11 | 15% |

| May-19 | 78 | 77% | 23 | 23% |

| Jun-19 | 60 | 78% | 17 | 22% |

| Jul-19 | 31 | 56% | 24 | 44% |

| Aug-19 | 1 | 13% | 7 | 88% |

| Sep-19 | 39 | 66% | 20 | 34% |

| Oct-19 | 86 | 86% | 14 | 14% |

| Nov-19 | 96 | 79% | 26 | 21% |

| Dec-19 | 62 | 67% | 31 | 33% |

| Jan-20 | 18 | 78% | 5 | 22% |

| Feb-20 | 13 | 50% | 13 | 50% |

| Mar-20 | 12 | 40% | 18 | 60% |

| Apr-20 | 0 | 0% | 30 | 100% |

| May-20 | 3 | 5% | 56 | 95% |

| Jun-20 | 27 | 23% | 89 | 77% |

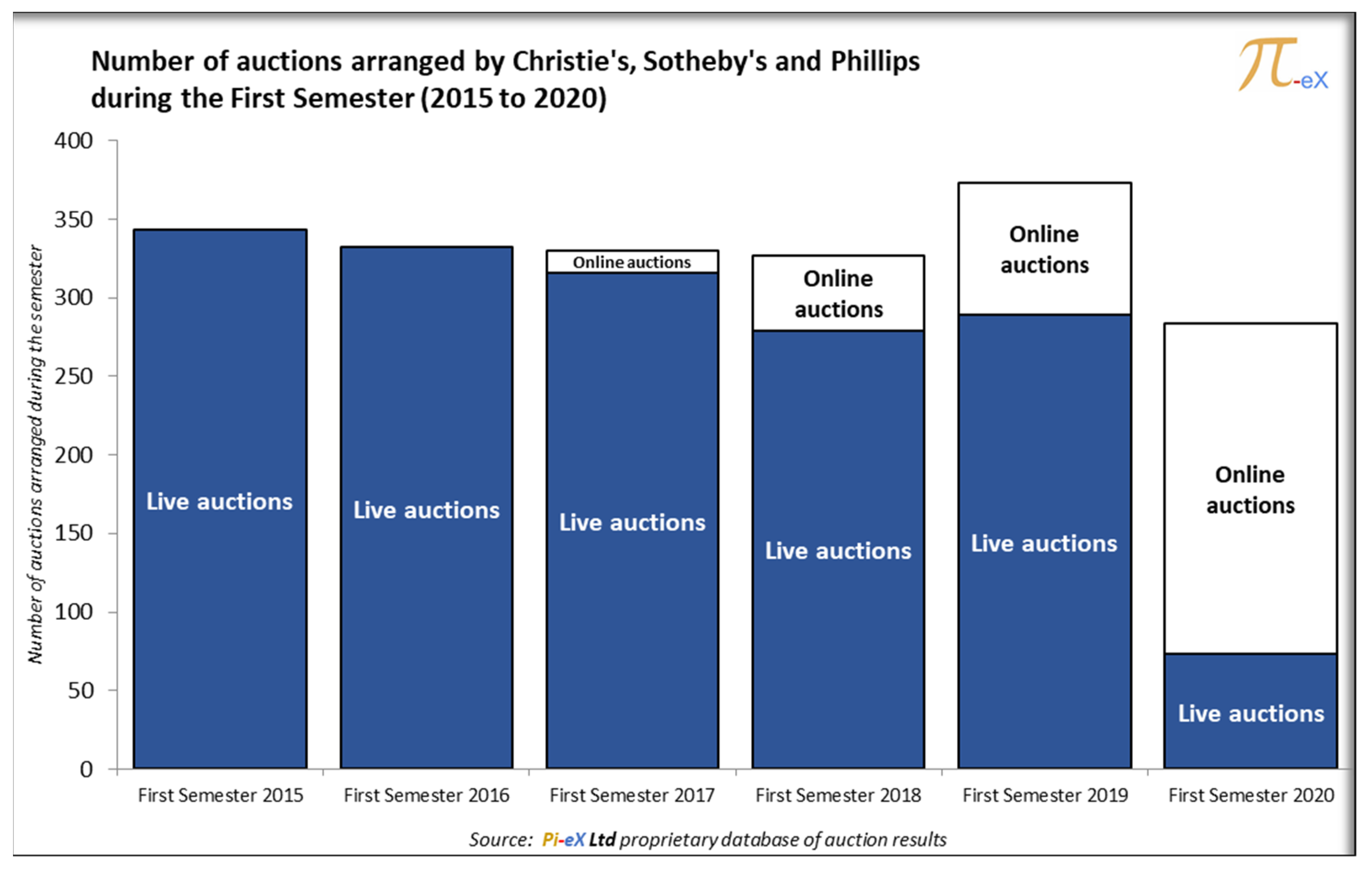

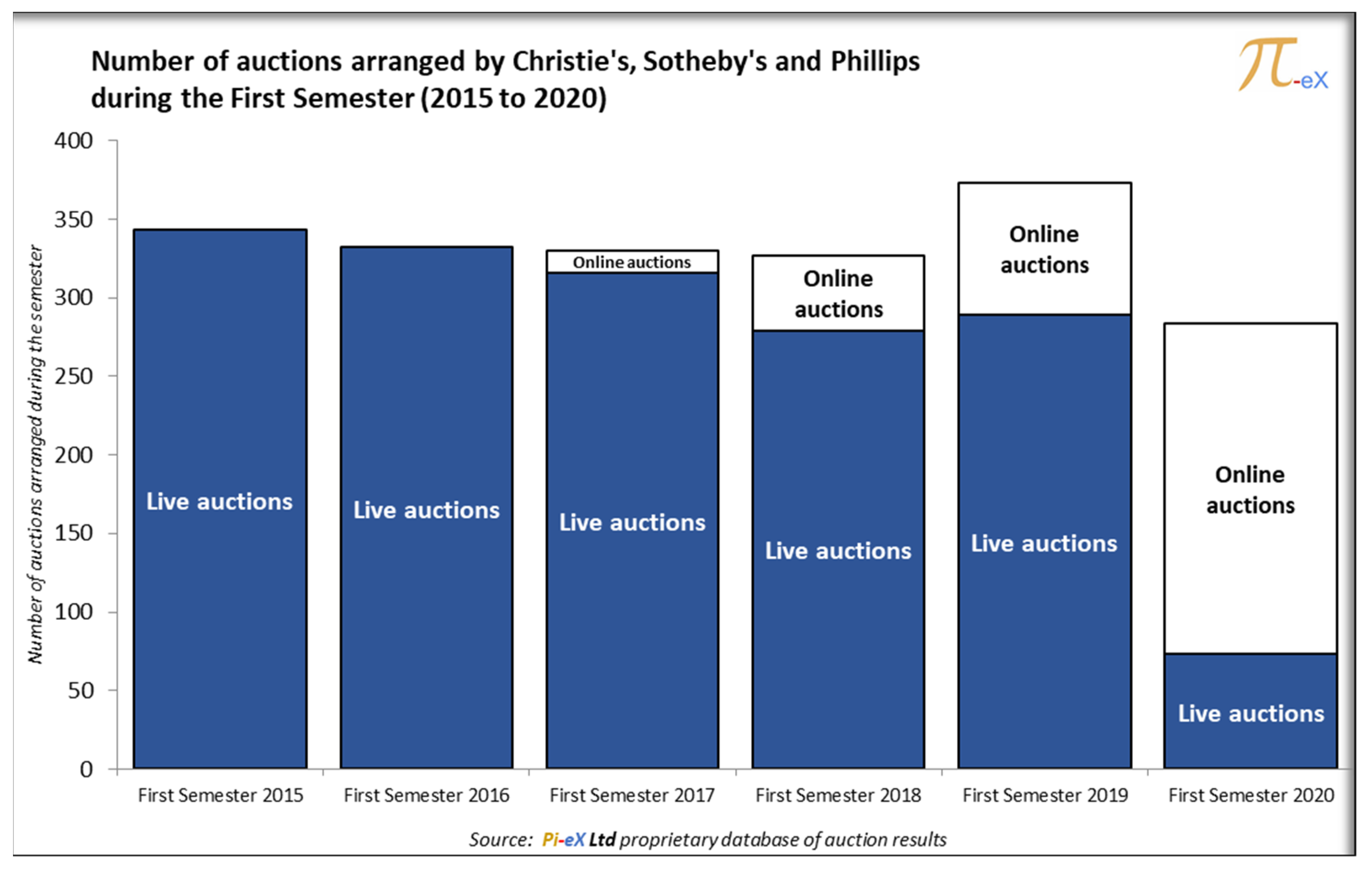

| Number of Auctions Arranged by Christie’s, Sotheby’s, and Phillips | Live Auctions # per Month % of Total | Online Only Auctions # per Month % of Total | ||

|---|---|---|---|---|

| First Semester 2015 | 343 | 100% | 0% | |

| First Semester 2016 | 332 | 100% | 0% | |

| First Semester 2017 | 316 | 96% | 14 | 4% |

| First Semester 2018 | 279 | 85% | 48 | 15% |

| First Semester 2019 | 289 | 77% | 84 | 23% |

| First Semester 2020 | 73 | 26% | 211 | 74% |

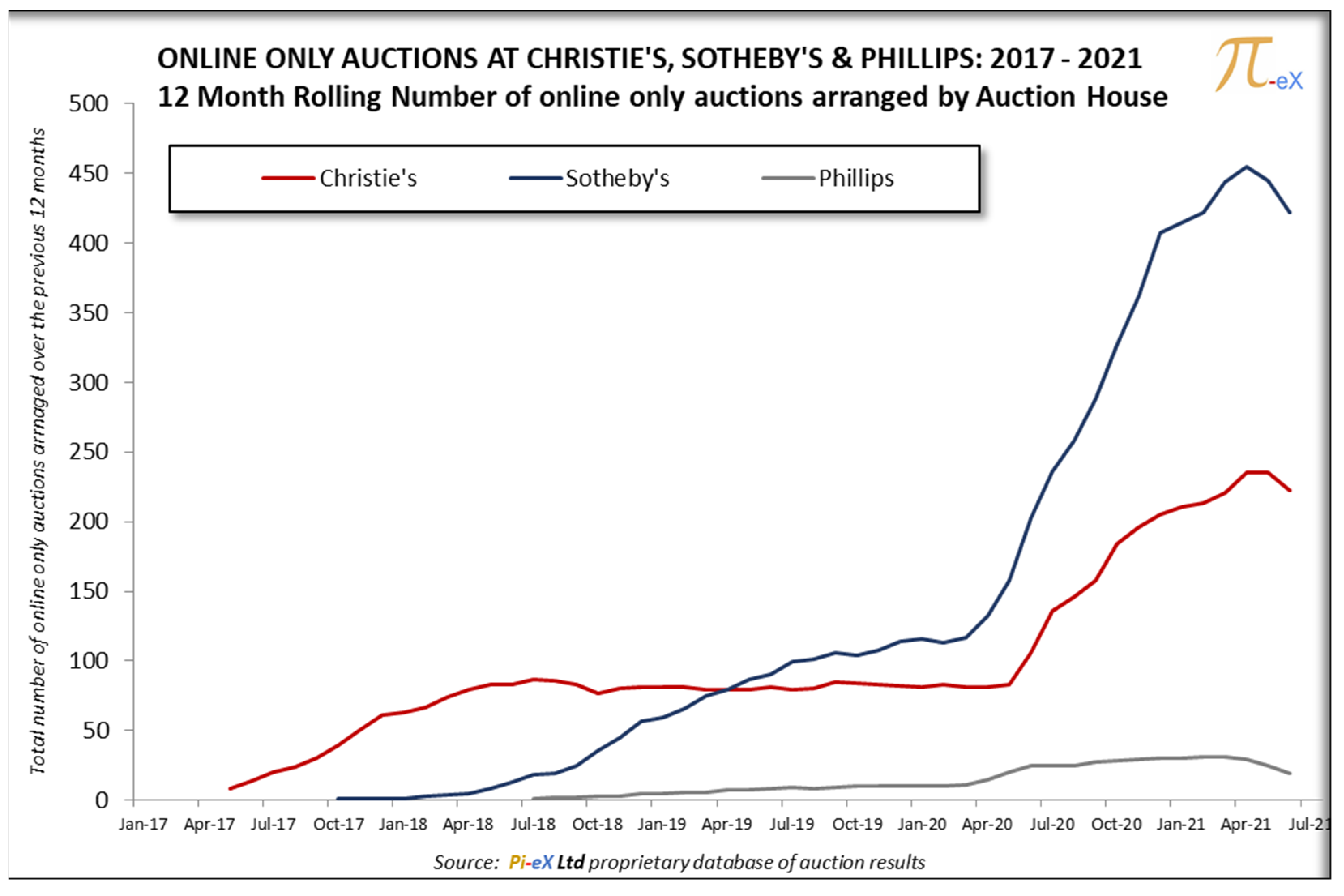

| 12 Month-Rolling Total Number of Online Only Auctions | |||

|---|---|---|---|

| Month | Christie’s | Sotheby’s | Phillips |

| Jan-17 | |||

| Feb-17 | |||

| Mar-17 | |||

| Apr-17 | |||

| May-17 | 8 | ||

| Jun-17 | 14 | ||

| Jul-17 | 20 | ||

| Aug-17 | 24 | ||

| Sep-17 | 30 | ||

| Oct-17 | 39 | 1 | |

| Nov-17 | 50 | 1 | |

| Dec-17 | 61 | 1 | |

| Jan-18 | 63 | 1 | |

| Feb-18 | 67 | 3 | |

| Mar-18 | 74 | 4 | |

| Apr-18 | 79 | 5 | |

| May-18 | 83 | 8 | |

| Jun-18 | 83 | 13 | |

| Jul-18 | 87 | 18 | 1 |

| Aug-18 | 86 | 19 | 2 |

| Sep-18 | 83 | 25 | 2 |

| Oct-18 | 77 | 36 | 3 |

| Nov-18 | 80 | 45 | 3 |

| Dec-18 | 81 | 57 | 5 |

| Jan-19 | 81 | 59 | 5 |

| Feb-19 | 81 | 66 | 6 |

| Mar-19 | 79 | 75 | 6 |

| Apr-19 | 79 | 79 | 7 |

| May-19 | 79 | 87 | 7 |

| Jun-19 | 81 | 90 | 8 |

| Jul-19 | 79 | 99 | 9 |

| Aug-19 | 80 | 101 | 8 |

| Sep-19 | 85 | 106 | 9 |

| Oct-19 | 84 | 104 | 10 |

| Nov-19 | 83 | 108 | 10 |

| Dec-19 | 82 | 114 | 10 |

| Jan-20 | 81 | 116 | 10 |

| Feb-20 | 83 | 113 | 10 |

| Mar-20 | 81 | 117 | 11 |

| Apr-20 | 81 | 132 | 15 |

| May-20 | 83 | 158 | 20 |

| Jun-20 | 106 | 202 | 25 |

| Jul-20 | 136 | 236 | 25 |

| Aug-20 | 146 | 258 | 25 |

| Sep-20 | 158 | 288 | 27 |

| Oct-20 | 184 | 327 | 28 |

| Nov-20 | 196 | 362 | 29 |

| Dec-20 | 205 | 407 | 30 |

| Jan-21 | 211 | 415 | 30 |

| Feb-21 | 213 | 422 | 31 |

| Mar-21 | 221 | 444 | 31 |

| Apr-21 | 235 | 455 | 29 |

| May-21 | 235 | 445 | 25 |

| Jun-21 | 222 | 422 | 19 |

| 12 Month-Rolling Total Number of Auctions | |||

|---|---|---|---|

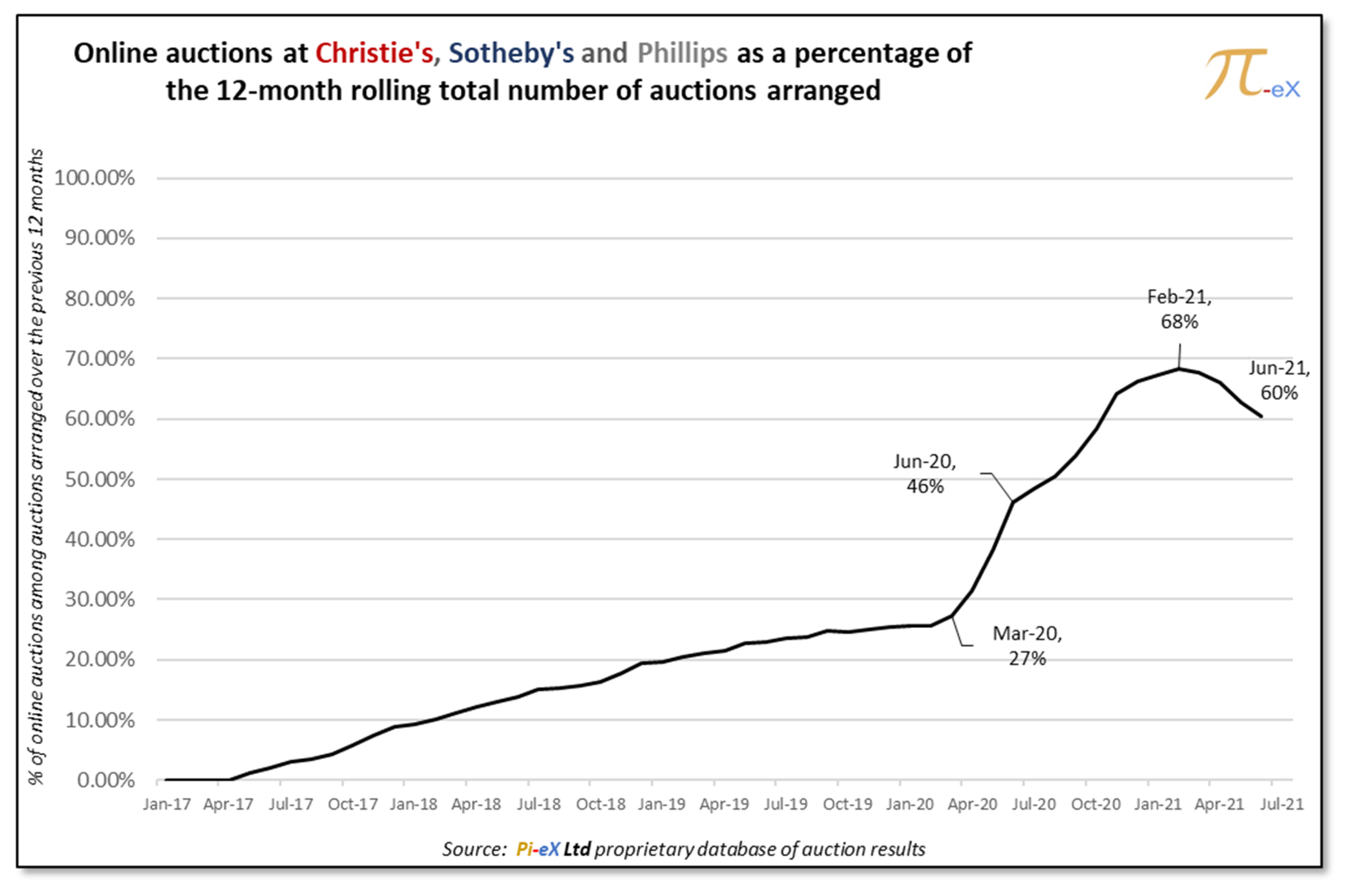

| Month | Online Auctions | All Auctions | Online as a % of Total |

| Jan-17 | 673 | 0% | |

| Feb-17 | 659 | 0% | |

| Mar-17 | 667 | 0% | |

| Apr-17 | 664 | 0% | |

| May-17 | 8 | 669 | 1% |

| Jun-17 | 14 | 672 | 2% |

| Jul-17 | 20 | 672 | 3% |

| Aug-17 | 24 | 675 | 4% |

| Sep-17 | 30 | 681 | 4% |

| Oct-17 | 40 | 686 | 6% |

| Nov-17 | 51 | 688 | 7% |

| Dec-17 | 62 | 695 | 9% |

| Jan-18 | 64 | 687 | 9% |

| Feb-18 | 70 | 694 | 10% |

| Mar-18 | 78 | 698 | 11% |

| Apr-18 | 84 | 687 | 12% |

| May-18 | 91 | 700 | 13% |

| Jun-18 | 96 | 690 | 14% |

| Jul-18 | 106 | 704 | 15% |

| Aug-18 | 107 | 704 | 15% |

| Sep-18 | 110 | 701 | 16% |

| Oct-18 | 116 | 713 | 16% |

| Nov-18 | 128 | 723 | 18% |

| Dec-18 | 143 | 732 | 20% |

| Jan-19 | 145 | 741 | 20% |

| Feb-19 | 153 | 750 | 20% |

| Mar-19 | 160 | 756 | 21% |

| Apr-19 | 165 | 765 | 22% |

| May-19 | 173 | 763 | 23% |

| Jun-19 | 179 | 778 | 23% |

| Jul-19 | 187 | 791 | 24% |

| Aug-19 | 189 | 793 | 24% |

| Sep-19 | 200 | 803 | 25% |

| Oct-19 | 198 | 804 | 25% |

| Nov-19 | 201 | 803 | 25% |

| Dec-19 | 206 | 810 | 25% |

| Jan-20 | 207 | 808 | 26% |

| Feb-20 | 206 | 805 | 26% |

| Mar-20 | 209 | 766 | 27% |

| Apr-20 | 228 | 724 | 31% |

| May-20 | 261 | 682 | 38% |

| Jun-20 | 333 | 721 | 46% |

| Jul-20 | 397 | 818 | 49% |

| Aug-20 | 429 | 849 | 51% |

| Sep-20 | 473 | 878 | 54% |

| Oct-20 | 539 | 922 | 58% |

| Nov-20 | 587 | 915 | 64% |

| Dec-20 | 642 | 970 | 66% |

| Jan-21 | 656 | 975 | 67% |

| Feb-21 | 666 | 974 | 68% |

| Mar-21 | 696 | 1029 | 68% |

| Apr-21 | 719 | 1087 | 66% |

| May-21 | 705 | 1122 | 63% |

| Jun-21 | 663 | 1098 | 60% |

| 12 Month-Rolling Total Revenue In USD (*) | |||

|---|---|---|---|

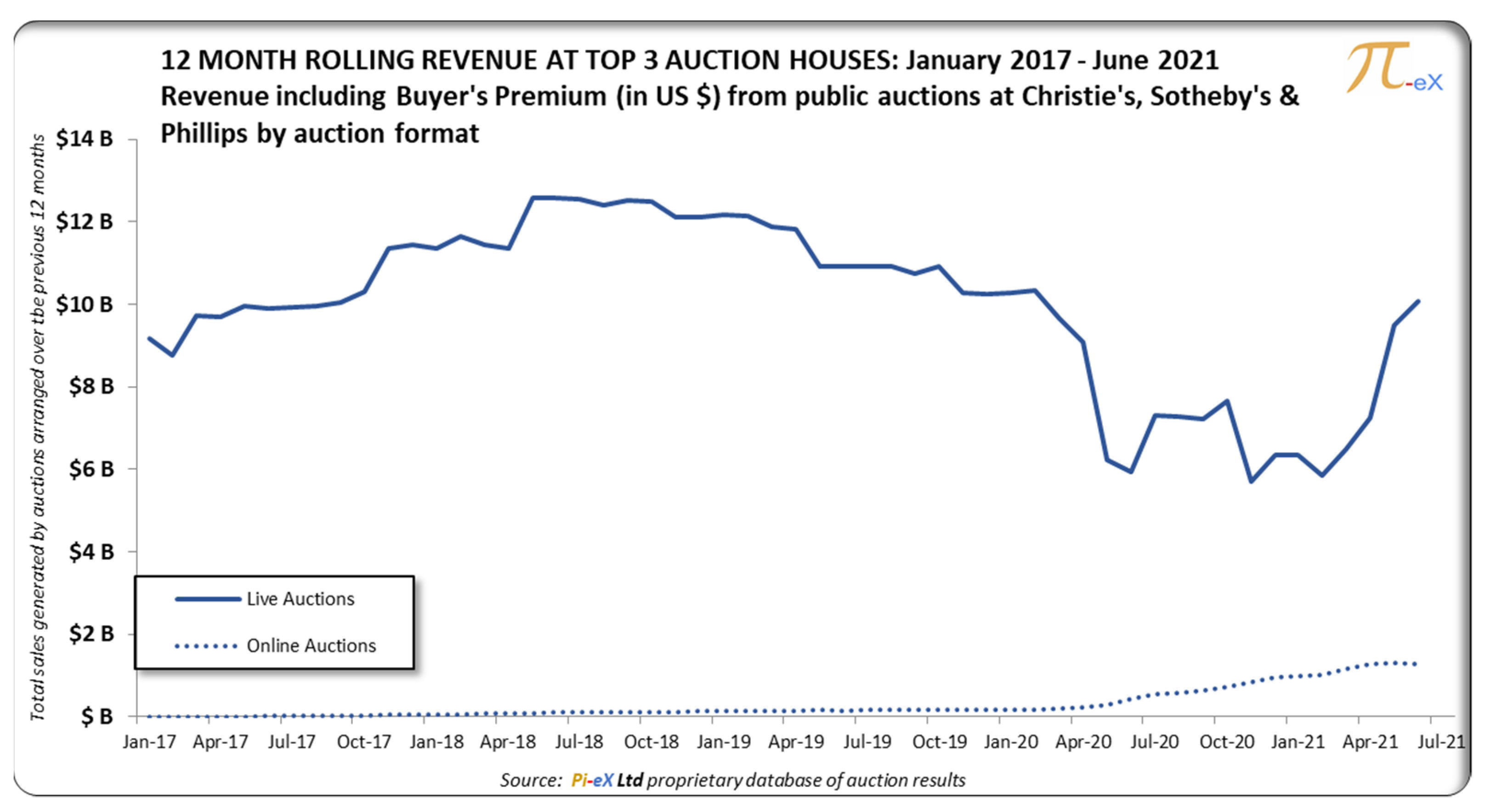

| Month | Live Auctions | Online Only Auctions | Online as a % of Total |

| Jan-17 | $9.2 B | $ M | 0% |

| Feb-17 | $8.7 B | $ M | 0% |

| Mar-17 | $9.7 B | $ M | 0% |

| Apr-17 | $9.7 B | $ M | 0% |

| May-17 | $10. B | $4 M | 0% |

| Jun-17 | $9.9 B | $9 M | 0% |

| Jul-17 | $9.9 B | $18 M | 0% |

| Aug-17 | $9.9 B | $21 M | 0% |

| Sep-17 | $10. B | $25 M | 0% |

| Oct-17 | $10.3 B | $33 M | 0% |

| Nov-17 | $11.4 B | $44 M | 0% |

| Dec-17 | $11.4 B | $57 M | 0% |

| Jan-18 | $11.3 B | $58 M | 1% |

| Feb-18 | $11.6 B | $64 M | 1% |

| Mar-18 | $11.4 B | $71 M | 1% |

| Apr-18 | $11.4 B | $76 M | 1% |

| May-18 | $12.6 B | $87 M | 1% |

| Jun-18 | $12.6 B | $101 M | 1% |

| Jul-18 | $12.5 B | $106 M | 1% |

| Aug-18 | $12.4 B | $106 M | 1% |

| Sep-18 | $12.5 B | $111 M | 1% |

| Oct-18 | $12.5 B | $115 M | 1% |

| Nov-18 | $12.1 B | $120 M | 1% |

| Dec-18 | $12.1 B | $133 M | 1% |

| Jan-19 | $12.2 B | $133 M | 1% |

| Feb-19 | $12.1 B | $135 M | 1% |

| Mar-19 | $11.9 B | $143 M | 1% |

| Apr-19 | $11.8 B | $146 M | 1% |

| May-19 | $10.9 B | $155 M | 1% |

| Jun-19 | $10.9 B | $148 M | 1% |

| Jul-19 | $10.9 B | $154 M | 1% |

| Aug-19 | $10.9 B | $156 M | 1% |

| Sep-19 | $10.7 B | $163 M | 1% |

| Oct-19 | $10.9 B | $161 M | 1% |

| Nov-19 | $10.3 B | $164 M | 2% |

| Dec-19 | $10.2 B | $165 M | 2% |

| Jan-20 | $10.3 B | $167 M | 2% |

| Feb-20 | $10.3 B | $175 M | 2% |

| Mar-20 | $9.7 B | $189 M | 2% |

| Apr-20 | $9.1 B | $224 M | 2% |

| May-20 | $6.2 B | $289 M | 4% |

| Jun-20 | $5.9 B | $439 M | 7% |

| Jul-20 | $7.3 B | $552 M | 7% |

| Aug-20 | $7.3 B | $582 M | 7% |

| Sep-20 | $7.2 B | $634 M | 8% |

| Oct-20 | $7.7 B | $727 M | 9% |

| Nov-20 | $5.7 B | $844 M | 13% |

| Dec-20 | $6.3 B | $945 M | 13% |

| Jan-21 | $6.3 B | $975 M | 13% |

| Feb-21 | $5.8 B | $998 M | 15% |

| Mar-21 | $6.5 B | $1170 M | 15% |

| Apr-21 | $7.2 B | $1261 M | 15% |

| May-21 | $9.5 B | $1291 M | 12% |

| Jun-21 | $10.1 B | $1264 M | 11% |

| Total Revenue in USD (*) | Contemporary Art | Impressionist & Modern Art | ||

|---|---|---|---|---|

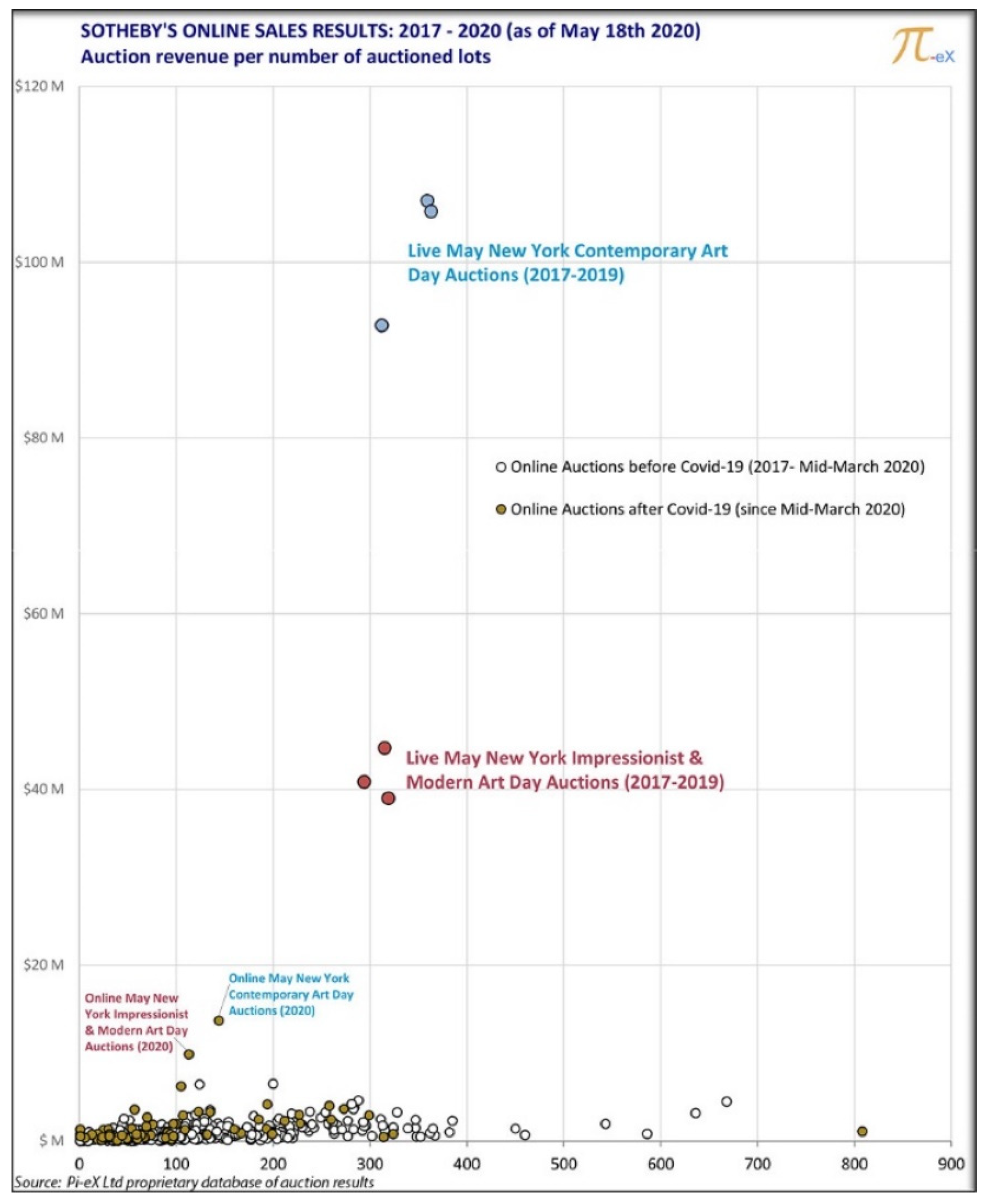

| Sotheby’s New York May Marquee Sales | Live Day Sale | Online Only Day Sales | Live Day Sale | Online Only Day Sales |

| May-17 | $92.8 M | $39.0 M | ||

| May-18 | $107.0 M | $40.9 M | ||

| May-19 | $105.8 M | $44.7 M | ||

| May-20 | $51.5 M | $13.7 M | $16.7 M | $9.9 M |

| May-21 | $80.1 M | $26.2 M | ||

| 2021 | 2020 | |||

|---|---|---|---|---|

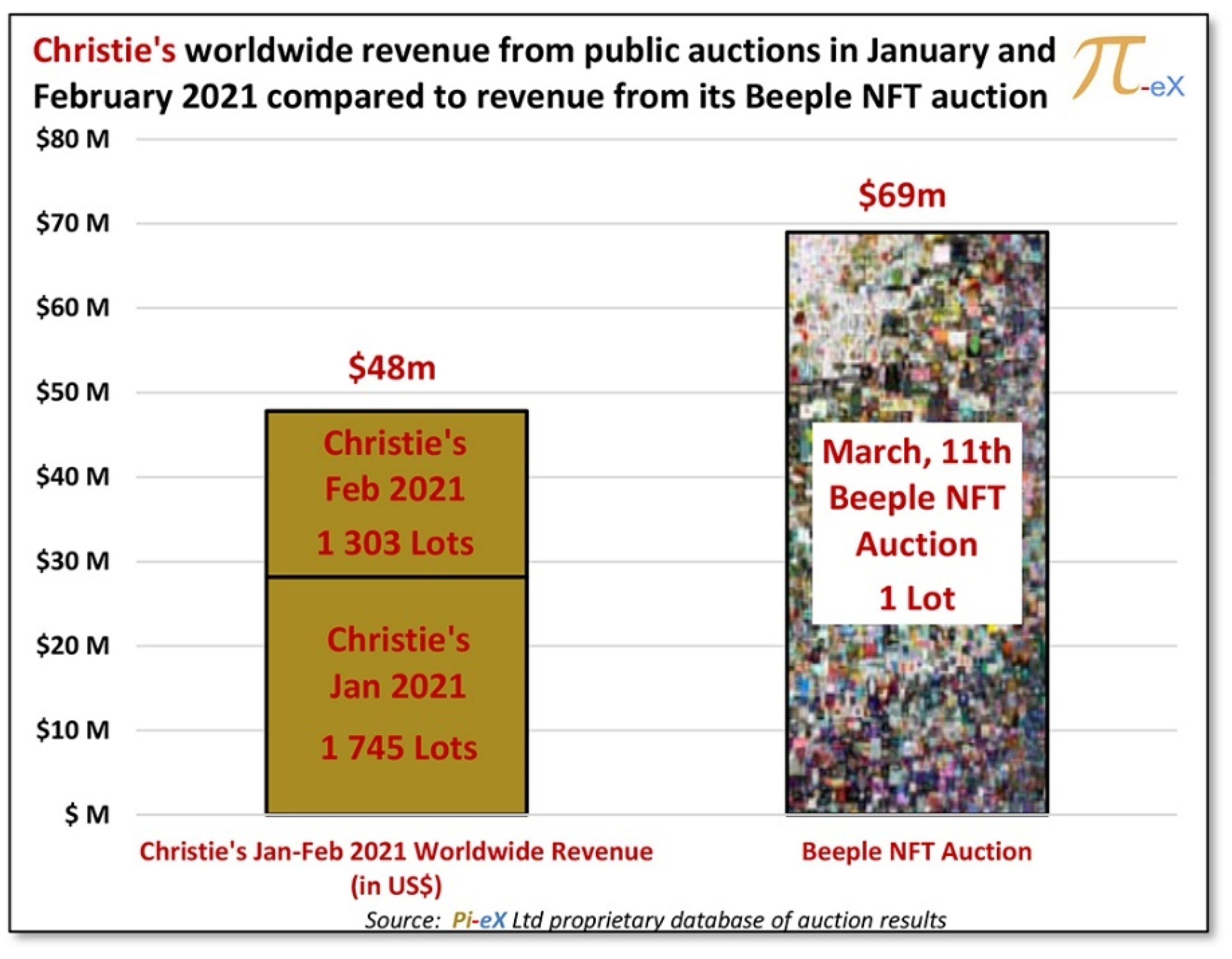

| Christie’s | Worldwide Revenue (in US$) (*) | # of Lots Catalogued at Auctions | Worldwide Revenue (in US$) | # of Lots Catalogued at Auctions |

| January | $28 M | 1745 | $40 M | 954 |

| February | $20 M | 1303 | $269 M | 1 170 |

| Crisis of 2008–2009 12-Month Rolling Public Auction Revenue (Adjusted for Inflation) | Crisis of Covid-19 12-Month Rolling Public Auction Revenue (Adjusted for Inflation) | |||

|---|---|---|---|---|

| Timeline | in USD (2) (3) | Indexed vs. October 2008 | in USD (2) (3) | Indexed vs. October 2019 |

| Month 1 (1) | $11.2 B | 100 | $9.1 B | 100 |

| Month 2 | $9.5 B | 84 | $8.5 B | 94 |

| Month 3 | $9.3 B | 83 | $8.5 B | 93 |

| Month 4 | $9.3 B | 83 | $8.5 B | 93 |

| Month 5 | $8.9 B | 80 | $8.6 B | 94 |

| Month 6 | $8.8 B | 79 | $8. B | 88 |

| Month 7 | $8.2 B | 74 | $7.6 B | 83 |

| Month 8 | $6.5 B | 58 | $5.3 B | 58 |

| Month 9 | $5.8 B | 52 | $5.2 B | 57 |

| Month 10 | $5.4 B | 48 | $6.4 B | 70 |

| Month 11 | $5.4 B | 48 | $6.4 B | 70 |

| Month 12 | $5.2 B | 46 | $6.4 B | 70 |

| Month 13 | $5.1 B | 46 | $6.8 B | 74 |

| Month 14 | $5. B | 45 | $5.3 B | 58 |

| Month 15 | $5.1 B | 46 | $5.9 B | 64 |

| Month 16 | $5.2 B | 46 | $5.9 B | 65 |

| Month 17 | $5. B | 45 | $5.5 B | 60 |

| Month 18 | $5.1 B | 45 | $6.1 B | 68 |

| Month 19 | $5.4 B | 48 | $6.8 B | 75 |

| Month 20 | $6.3 B | 56 | $8.6 B | 94 |

| Month 21 | $6.9 B | 62 | $9. B | 99 |

| Month 22 | $7. B | 63 | ||

| Month 23 | $7. B | 63 | ||

| Month 24 | $7.1 B | 64 | ||

| Month 25 | $7.4 B | 66 | ||

| Month 26 | $8.4 B | 75 | ||

| Month 27 | $8.6 B | 77 | ||

| Month 28 | $8.6 B | 77 | ||

| Month 29 | $8.7 B | 78 | ||

| Month 30 | $8.9 B | 80 | ||

| Month 31 | $9.1 B | 81 | ||

| Month 32 | $9.4 B | 84 | ||

| Month 33 | $9.6 B | 86 | ||

| Month 34 | $9.6 B | 86 | ||

| Month 35 | $9.6 B | 86 | ||

| Month 36 | $9.6 B | 86 | ||

| Month 37 | $9.6 B | 86 | ||

| Month 38 | $9.6 B | 86 | ||

| Crisis of 2016 12-Month Rolling Public Auction Revenue (Adjusted for Inflation) | Crisis of Covid-19 12-Month Rolling Public Auction Revenue (Adjusted for Inflation) | |||

|---|---|---|---|---|

| Timeline | in USD (2) (3) | Indexed vs October 2008 | in USD (2) (3) | Indexed vs October 2019 |

| Month 1 (1) | $12. B | 100 | $9.1 B | 100 |

| Month 2 | $11.5 B | 96 | $8.5 B | 94 |

| Month 3 | $11.6 B | 97 | $8.5 B | 93 |

| Month 4 | $11.6 B | 97 | $8.5 B | 93 |

| Month 5 | $11.2 B | 94 | $8.6 B | 94 |

| Month 6 | $11. B | 92 | $8. B | 88 |

| Month 7 | $11. B | 92 | $7.6 B | 83 |

| Month 8 | $9.9 B | 83 | $5.3 B | 58 |

| Month 9 | $9.5 B | 80 | $5.2 B | 57 |

| Month 10 | $9.3 B | 78 | $6.4 B | 70 |

| Month 11 | $9.2 B | 77 | $6.4 B | 70 |

| Month 12 | $9.3 B | 77 | $6.4 B | 70 |

| Month 13 | $9.1 B | 76 | $6.8 B | 74 |

| Month 14 | $8.3 B | 69 | $5.3 B | 58 |

| Month 15 | $8. B | 67 | $5.9 B | 64 |

| Month 16 | $8. B | 67 | $5.9 B | 65 |

| Month 17 | $7.6 B | 63 | $5.5 B | 60 |

| Month 18 | $8.4 B | 70 | $6.1 B | 68 |

| Month 19 | $8.4 B | 70 | $6.8 B | 75 |

| Month 20 | $8.6 B | 72 | $8.6 B | 94 |

| Month 21 | $8.5 B | 71 | $9. B | 99 |

| Month 22 | $8.5 B | 71 | ||

| Month 23 | $8.6 B | 72 | ||

| Month 24 | $8.6 B | 72 | ||

| Month 25 | $8.9 B | 74 | ||

| Month 26 | $9.7 B | 81 | ||

| Month 27 | $9.8 B | 82 | ||

| Month 28 | $9.7 B | 81 | ||

| Month 29 | $9.9 B | 83 | ||

| Month 30 | $9.8 B | 82 | ||

| Month 31 | $9.7 B | 81 | ||

| Month 32 | $10.7 B | 89 | ||

| Month 33 | $10.6 B | 89 | ||

| Month 34 | $10.6 B | 89 | ||

| Month 35 | $10.5 B | 88 | ||

| Month 36 | $10.6 B | 88 | ||

| Month 37 | $10.5 B | 88 | ||

| Month 38 | $10.2 B | 85 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bourron, C. How Has COVID-19 Affected the Public Auction Market? Arts 2021, 10, 74. https://doi.org/10.3390/arts10040074

Bourron C. How Has COVID-19 Affected the Public Auction Market? Arts. 2021; 10(4):74. https://doi.org/10.3390/arts10040074

Chicago/Turabian StyleBourron, Christine. 2021. "How Has COVID-19 Affected the Public Auction Market?" Arts 10, no. 4: 74. https://doi.org/10.3390/arts10040074

APA StyleBourron, C. (2021). How Has COVID-19 Affected the Public Auction Market? Arts, 10(4), 74. https://doi.org/10.3390/arts10040074