1. Introduction

The construction sector, and, thus, public works, has a significant impact on economies globally [

1,

2,

3]. In Spain, public tenders for construction reached €30.07 billion in 2022 [

4], with €18.52 billion specifically for civil engineering. This represents a 27.9% increase from the previous year. The public administration requests bids through public procurement, inviting construction companies to submit proposals.

The Spanish tendering system is complex and diverse, with various contracts and tender types. Most contracts are secured by selecting the most economically advantageous proposal [

5]. This is influenced by the significant weight attributed to the economic price criterion within the potential award criteria, typically ranging from 60% to 80% of the overall scoring. The construction company must follow public procurement laws when awarding projects to ensure successful execution and completion. This principle applies to all public contracts in Spain [

6]. Budget management and cost overruns are significant challenges for contracting parties and society [

7]. Contractors are legally obligated to adhere to the proposed budget, with exceptions. Therefore, their proposals during the bidding process must be realistic and truthful.

However, one of the most reported and addressed issues concerning civil engineering projects is the regular occurrence of cost overruns [

8], primarily due to their significant size and society’s growing demand for the efficient use of public funds. The definition of the term “cost overrun” has received extensive consideration, generally referring to the difference between budgeted costs during project planning (the “awarding price” in public procurement) and the final costs incurred at project completion [

9]. The various causes involved include technical constraints primarily from imperfect designs, human biases in planning, inadequate information, or lack of experience [

10,

11]. The involvement of public administrations as project sponsors is also known to be a factor [

12,

13].

Change orders, or project modifications, in Spain, are a major factor in construction projects [

14]. These modifications, initiated or accepted by public administrations, can lead to conflicts, delays, legal disputes, and decreased productivity [

15]. The management of these modifications in Spain has been controversial, primarily due to scandals involving excessive cost overruns, as depicted in

Table 1 [

16].

Project modifications have been defined in the literature as tasks or work added or removed from the initial scope of a project contract, thereby altering the budget and/or schedule of the original contract [

17]. They are legal frameworks that address situations where modifying the original project or budget is necessary for successful completion.

Project modifications do not inherently possess a deleterious nature, as they can be instigated by reasons that may result in benefits for the project’s stakeholders, despite increasing its planned budget. Nevertheless, their emergence inevitably gives rise to inconveniences in terms of management, financial aspects, bureaucracy, legality, and even politics for the involved public administrations, which can potentially lead to project failure.

They have evolved significantly in recent decades, with changes in their definitions, classifications, and allowable cost overrun limits. In Spain, these changes can be attributed to two primary factors:

Cost overruns in civil engineering projects have led to legislative revisions, with numerous significant overruns. A study found that 77% of projects experienced an average cost overrun of 14% [

18], with 63% due to flawed or incomplete project designs, highlighting the need for improved project design and oversight;

The European Union has had a significant impact on Spain’s approach to cost overruns from project modifications, leading to disciplinary actions and legislative adjustments [

19]. The release of Directive 2014/24/EU obligated Spain to incorporate the directive into its legal framework, requiring a subsequent regulatory revision [

20].

This paper explores the impact of evolving legal frameworks in Spain on modifications in public works projects, focusing on cost overruns in civil engineering projects. It identifies design flaws and human biases as causes and highlights how modifications can exacerbate these overruns, affecting project efficiency and budget adherence. The study uses data mining from the Public Sector Contracting Platform (PLACSP) to compare predefined cost overrun limits with actual observations, providing insights into contractors’ responses in a changing legal context. The structured approach includes literature review, contextual exploration, database development, and meticulous analysis, offering practical insights into project management strategies, transparency initiatives, and responsible public funds allocation.

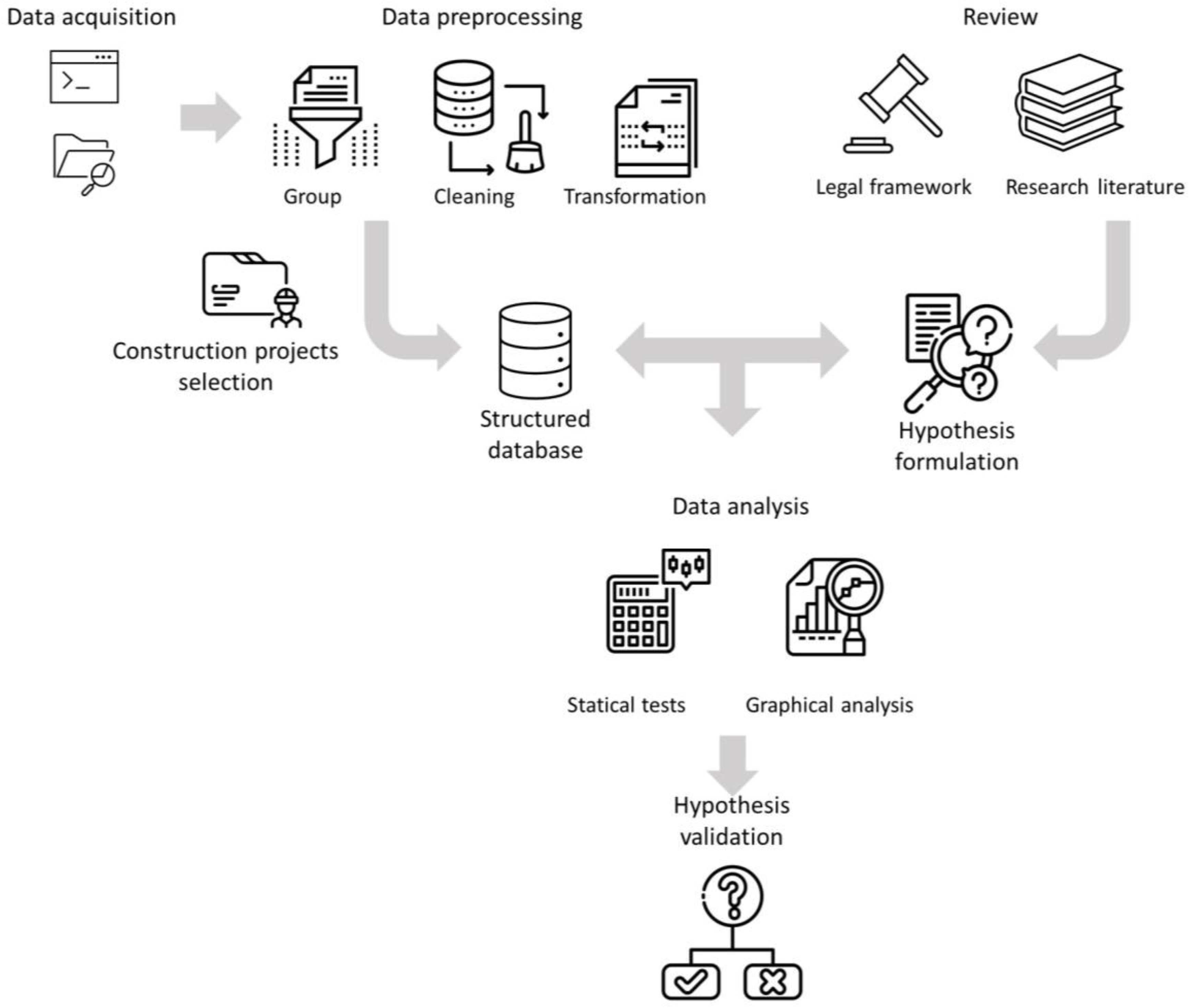

In order to conduct this research, the following approach is proposed as depicted in

Figure 1. First, a literature review (

Section 2) is conducted to provide an overview of the academic research on cost overruns and project modifications in civil engineering projects. Additionally, an explanation of the Spanish context and legal framework (

Section 3) applicable to contract modifications in public procurement in recent years is presented.

Subsequently, a database (

Section 4) of real project cases involving modifications is developed using data obtained from the Public Sector Contracting Platform (PLACSP, the main portal for contracting, transparency, and open data related to Spanish public administrations). These cases are then analysed through descriptive analysis of the key variables (

Section 5.1). Hypothesis testing (

Section 5.2) and graphical representation of data and results about initial and final costs relationship are conducted. The behaviour of project modifications before and after the legislative change (

Section 5.3) with the implementation of Law 9/2017 (latest in force, which applies less restrictive limits) is compared and analysed to further examine the relationship between modifications and the legal framework in the case of Spain. Finally, research conclusions and emerging future research options are described in the last section (

Section 6).

2. Literature Review

2.1. Cost Overruns in Civil Engineering Projects

Research into quantifying cost overruns faces challenges due to complexities in accessing and identifying final project costs, lack of availability or traceability of actual costs, opacity in certain procedures, and conflicting interests of stakeholders [

21]. However, several case studies offer insights into this issue (as shown in

Table 2). These studies have been selected for their quantitative data quality, which is not common in the field of project cost overruns. They offer exact descriptive statical information, as well as managing a considerable number of projects in each case, and five of them are related to the last two decades.

The problem of cost overrun quantification is evident in geographical, temporal, and quantitative dimensions, leading to numerous studies exploring its nature and causes, and identifying best practices for prevention or mitigation.

Research indicates a correlation between cost overruns, a country’s developmental stage, and socioeconomic conditions [

28]. More developed countries often experience fewer instances due to better control and monitoring procedures [

25]. Human bias is a key driver of project cost overruns, leading to changes in project scope over its lifecycle [

29]. Kaming et al. [

30] highlight incorrect estimation of material and human resources as the primary cause, influenced by project complexity. Other causes include technical constraints, imperfect designs, insufficient information, and a lack of experience [

31,

32].

2.2. Project Modifications in Civil Engineering

The study of modifications in civil engineering projects has gained global attention due to advancements in information technologies and increased accessibility to project data due to institutional transparency policies. These modifications involve adding or removing tasks, altering the contract’s budget and schedule [

17]. The literature on modifications is divided into two research lines: mitigating their effects and studying their causes and impacts.

The first line focuses on developing processes to minimize the effects of modifications, resulting in numerous studies.

Table 3 lists some notable examples.

The other research line has shown that 65% of 98 projects experienced cost overruns due to modifications, averaging 8% [

39]. This is primarily due to repeated work requests, with only 0.39% attributed to these changes. The causes of these overruns can be identified through various typologies, including reviews [

40], survey-based case studies [

41], real project data-based case studies [

42], and the development of methodologies or models [

43]. Commonly identified causes of modifications include:

requested by project promoters for new work expanding the project’s scope;

design errors stemming from omissions or faulty project design;

lack of co-ordination among project stakeholders;

financial difficulties on the part of the promoter;

unforeseen circumstances were not considered during project design;

lack of resources (time and budget) for designing phases, particularly compared to construction phase resources.

Recent studies have extended the search for causes to other aspects of public construction projects, such as bidding processes. For example, Olaolu Titus et al. [

44] studied bid types influencing modifications in Ethiopia. Other studies link changes in construction productivity, often tied to project modifications, to shifts in the business environment, and to country-specific institutional regulations [

45,

46]. Azrai Azman et al. [

47] explored the impact of regulatory changes on construction productivity in Malaysia, emphasizing the link between productivity and long-term institutional regulations as companies adapt to their legal frameworks.

Following this literature review of project modifications and their relationship to cost overruns, three primary research gaps emerge:

Limited studies adopt a big data analysis perspective to address cost overruns and project modification challenges. A case study compiling a dataset of real public works projects and its analysis could significantly contribute to expanding knowledge;

There needs to be more international literature examining the influence of legislative frameworks on project modifications. This gap highlights the need for research in the context of civil engineering projects, particularly public infrastructure development in Spain, which could be valuable as a unique case study with relevance to other countries;

This paper focuses on the relationship between base bidding prices and final project costs, exploring potential causes that elucidate this connection. In the current literature, there are no studies that approach this topic from the perspective of the behaviour of construction companies and how they adapt to the established legal framework within a developed public sector such as the Spanish one.

3. Spanish Legal Framework for Construction Project Modifications

Change orders in public infrastructure projects in Spain have been a topic of controversy due to the misuse of modifications by government authorities and contractors to introduce additional costs [

10,

18]. Since 2000, legislation has been enacted to address public contracts and modifications as shown in

Table 4. Although minor amendments to the Public Sector Procurement Law (LCSP) have been included in general budget laws for 2018, 2021, 2022, and 2023, they have not affected project modifications.

During Spain’s “construction boom” in the 21st century, the regulatory landscape was defined by RD 2/2000 TRLCAP. This allowed contract modifications of up to 20% of the tender price, requiring justification by necessity and public interest, and allowing termination of contracts if modifications exceeded this threshold. However, agreements were typically reached for specific cases.

In 2008, the European Commission filed disciplinary proceedings against Spain for allowing tendering entities to modify essential award clauses during execution. This led to significant cost overruns in construction projects due to the need for more transparency and fair competition [

16].

Law 2/2011 on sustainable economy and subsequent RD 3/2011 TRLCSP were enacted to address this issue and resolve the European case. These regulations redefined modifications to emphasize their extraordinary nature and impose limitations:

The contractor’s right to terminate the contract due to modifications exceeding 20% was revoked, reserving this right solely for the administration. Contractors are obligated to meet new legal requirements for modifications;

The size of unforeseen modifications (or their cumulative total within a project) was capped at 10% of the contract’s tender price as long as essential bidding and award conditions were unaffected. Any essential modification necessitated contract termination and a new bidding process with revised terms.

The European Commission closed disciplinary proceedings against Spain due to a legal overhaul to reduce cost overruns and unfair competition [

48]. However, Directive 2014/24/EU on public procurement was published in 2014 and incorporated into Spanish law through Law 9/2017 on public sector procurements in 2017. Although Spanish law is more restrictive than the directive, it limits modifications and their cumulative sum within a project—a step backward from TRLCSP.

Law 9/2017 divides modifications into administrative and non-administrative clauses. Non-administrative modifications allow 20% of tender prices, while substantial changes (like new works or services) have a 50% cap. Non-substantial extraordinary modifications, like construction works, have a 15% limit, and other contracts have a 10% limit. Price revisions, excessive measurements, and new prices are exempt from these limits and are governed by separate regulations.

4. Materials and Methods

A comprehensive compilation and development of a database comprising real projects in Spain was undertaken. This enabled a thorough analysis of data and the validation of the following initial hypotheses:

H1. There is a significant disparity between the base bidding prices and the final costs for Spanish civil engineering projects.

H2. There is a significant relationship between the legally stipulated percentage limits for project cost modifications and the values registered from real cases of Spanish civil engineering projects.

The H1 hypothesis postulates the proper and efficient performance of the public tendering process in Spain. Therefore, there should be a significant disparity between the base bidding prices and the final project costs, as this process aims to reduce the project’s cost through competition among various companies to undertake it. Hence, since companies submit bids lower than the base price to secure the contract (given that price is the most influential factor), even after modifications the final cost should ideally be markedly lower. It would be rejected if statically significant correlation is found, corroborated by graphical analysis.

The H2 hypothesis postulates the existence of a relationship between the legally stipulated percentage limits for project cost modifications, and the values registered from real cases of civil engineering projects in Spain. In this way, the data will show how contractors incur these planned cost overruns, with their distribution not being heterogeneous and concentrated on those legal limits (that changed over time, so will be compared in different periods).

The study scrutinized Spain’s legal framework and existing knowledge involving data science procedures like database assembly, variable formulation, case selection, and data treatment. It used data analysis tools like correlation heat maps and hypothesis testing to characterize the database. The graphical representation of variables facilitated interpretation and discourse, emphasizing the importance of correlations among variables.

4.1. Data Compilation

Spanish public administrations are modernizing and digitizing public procurement processes to improve transparency and data accessibility. This is driven by community and national laws and guidelines [

49] aiming to improve transparency through open data publication. This has led to applications in data science, big data, and artificial intelligence harnessing data from public administrations [

50]. The Platform for Public Sector Procurement (PLACSP) is at the forefront of this progress.

Article 347 of the LCSP defines the PLACSP as an “electronic platform that allows the dissemination of contracting profiles through the Internet, as well as providing other services associated with the computer processing of this data”. It is a central platform for central, regional, and local administrations to publish tender data with direct or aggregated entries. Since 2018, the number of tenders published on the PLACSP has steadily increased.

The datasets accessible for consultation on the PLACSP are in a structured .atom format, representing labelled XML files that receive daily updates. These datasets are classified into three distinct sets:

Public sector: Comprising contracting records directly disclosed on the PLACSP by state, regional, and local administrations that lack individual platforms. Minor contracts are excluded;

Aggregated: Includes contracting records aggregated to the PLACSP through syndication from distinct platforms, with minor contracts omitted;

Minor contracts of the public sector: Involves minor contracts (below €40,000 for construction work and €15,000 for other types) published in the contracting profiles on the PLACSP. These contracts are also excluded from the present study.

The PLACSP datasets are structured in a predefined CODICE format, simplifying their application and exploration. They cover tender data fields like bid prices, bidder numbers, administering authority, contract CPV, dates, required guarantees, and registered modifications. This database presents an unprecedented opportunity for research in project management as well as public procurement, grounded in data analysis and big data. It constitutes a public platform with objective, unaltered data, offering complete transparency and reliability. While it is true that the quality of data can be improved, the quantity available remains its strength.

Furthermore, the data are accessible worldwide from anywhere, facilitating a high degree of reproducibility for studies conducted. It encompasses data from a wide array of projects, ranging from healthcare and educational to procurement and construction. It even includes data from services or concessions. Hence, the existence of this database has been pivotal in conducting this study. Without it, conducting the research in the manner it was executed would not have been feasible. More information is available on the PLACSP website.

The Spanish Department for Electronic Procurement Co-ordination launched the

OpenPLACSP software in 2021, which allows the extraction of .atom file data into .xlsx format, enhancing usability. The software categorizes potential variables into general and award data, with version 1.0 allowing up to 22 variables for each category (key variables provided are mentioned in

Table 5). Both methods are currently used for querying PLACSP data.

OpenPLACSP, despite its usefulness, has limitations in selecting certain fields within .atom files, such as required guarantees or registered modifications. This led to the use of a hybrid data acquisition methodology. A custom XML script was developed to extract modification-related fields (summarized in

Table 6) from .atom files and integrate them into the database.

Over 85,000 modification cases were obtained across various economic sectors, with many being duplicated projects. Contracts undergo successive changes, generating new entries. Filtering based on the economic sector is essential, using the Common Procurement Vocabulary (CPV) system. Civil engineering projects have cases with CPV codes starting with 451* and 452*, while building construction works have cases with 4521*.

Data quality assurance is crucial when processing the PLACSP, as inconsistencies can lead to mismatches and incorrect contract prices. To ensure data quality, discrepancies between the final contract price and tender price and modifications are identified. Inconsistencies are filtered out, focusing on contracts where values align. Cases with modification values exceeding −50%, signifying contract cancellations, are excluded. The processed modification database is merged with OpenPLACSP variables.

The data treatment process involves converting variables like administration type or process type into numeric formats for correlation tests, standardizing modification delay into common units like days, and incorporating percentage-based variables like “% modification” and “% discount” into the database to compensate for the PLACSP’s registration of only absolute values in its fields.

The database’s development faced several limitations, including project modification fields being only accessible for cases directly uploaded to PLACSP profiles and not aggregated platforms, limiting its scope to the public sector dataset. The tool’s data structure also hindered the identification and grouping of awarding batches when one tender was divided into multiple contracts. Therefore, only projects needing more batches were chosen for construction.

4.2. Statistical Methods Applied

The study used various statistical techniques to analyse data, starting with investigating correlations among database variables. Spearman’s rank correlation method was used to assess monotonic correlations [

51], where variables increase or decrease in tandem but not necessarily at an equal pace, which is the expected outcome of the study.

Spearman’s rank correlation coefficient is a non-parametric statistical method that measures the strength and direction of the linkage between two ranked variables [

52]. It is useful in non-linear relationships or ordinal data, where values can be ranked but not measured on a continuous scale. It is commonly used in correlation analysis, especially when dealing with non-linear relationships, tied observations, and non-normally distributed or categorical variables [

53]. It has greater resilience against outliers and less influence on original value series variations.

Upon identifying “Tender Price” and “Final Cost” as pivotal variables for correlation analysis, two additional tests were selected for hypothesis testing. Before any statistical testing, the normality of the variables was assessed using the Anderson–Darling test to determine the subsequent statistical techniques. This test is particularly suitable for analysing large samples, as it relies on the empirical distribution function (EDF) and uses a quadratic statistic to measure the disparity between the data’s EDF and the EDF of the normal distribution [

54].

The Spearman correlation test and Wilcoxon and Kolmogorov–Smirnov tests were used to test hypothesis H1 regarding tender price and final cost. The Wilcoxon test, a non-parametric method, compares two independent samples and determines if a significant difference exists between their distributions [

55]. It operates based on data ranks and is resilient against outliers, making it applicable when data does not meet the assumptions of a parametric

t-test.

The Kolmogorov–Smirnov test is a non-parametric technique that evaluates a sample’s distribution relative to a reference or two separate samples [

56]. It is particularly effective in quantifying the magnitude of differences between variables based on the maximum difference between the cumulative distribution functions of the two samples. To validate the hypotheses posited, the following analytical tasks were undertaken.

For H1 testing, two tasks were carried out to examine the proper performance of the Spanish public procurement framework through the correlation analysis of base bid price and final project cost. First, the above hypothesis testing methods were applied. Null hypotheses were rejected for p-values below 0.01.

In the Spearman correlation test, the null hypothesis corresponds to the absence of a significant correlation between variables;

In the Wilcoxon test, the null hypothesis corresponds to the absence of a difference between the distributions of median prices;

In the K-S test, the null hypothesis corresponds to the absence of a significant difference between cumulative distributions of variables.

Moreover, a graphical analysis involving pairwise representation of variables was conducted. The trend and ratio of their relationship were examined to verify their approximation to a 1:1 relationship.

Conclusion of the acceptance or rejection of H1 will be made based on both statical tests and graphical analysis as a whole.

For H2 testing, an analysis was performed using frequency-based graphical analysis for the second hypothesis, as well as mean values analysis. These analyses pertain to the impact of legally mandated limits on the percentages of cost overruns in project modifications. Pareto charts were created for cases before and after the last legislative change to assess the distribution and concentration around specific percentage values. A box chart is also analysed for comparison between both different legal periods.

5. Results and Discussion

This section presents the research findings and hypotheses, focusing on the case study of public procurement in civil engineering in Spain. It aims to provide transparency to society, industry professionals, and fellow researchers, allowing them to determine if the data aligns with the observed practices of government bodies and contractors regarding modifications, potentially inflating the final project cost. The presentation serves as a platform for broader understanding and informed decision making.

5.1. Database Analysis and Correlation Matrix

The database contains 793 civil engineering projects with cost overruns due to budget modifications from 2016 to 2021, including 440 cases with cost and project schedule changes. The database addresses challenges and constraints faced during its development, covering the period.

Table 7 displays a diverse range of variables in database cases, with values ranging from minimum to maximum, significantly deviating from means or medians. The standard deviation (SD) values support this variance, while the interquartile range (Range_IQR) values are acceptable. This distribution is suitable for case study analysis, as it concentrates most cases within intermediate ranges and allows examination of exceptional cases.

Table 8 presents a summary of qualitative variables, with a particular focus on certain values like “Ordinary” for procurement urgency type and “Open” or “Simplified Open” for procedure contracts, which presents challenges in studying correlations or dependencies.

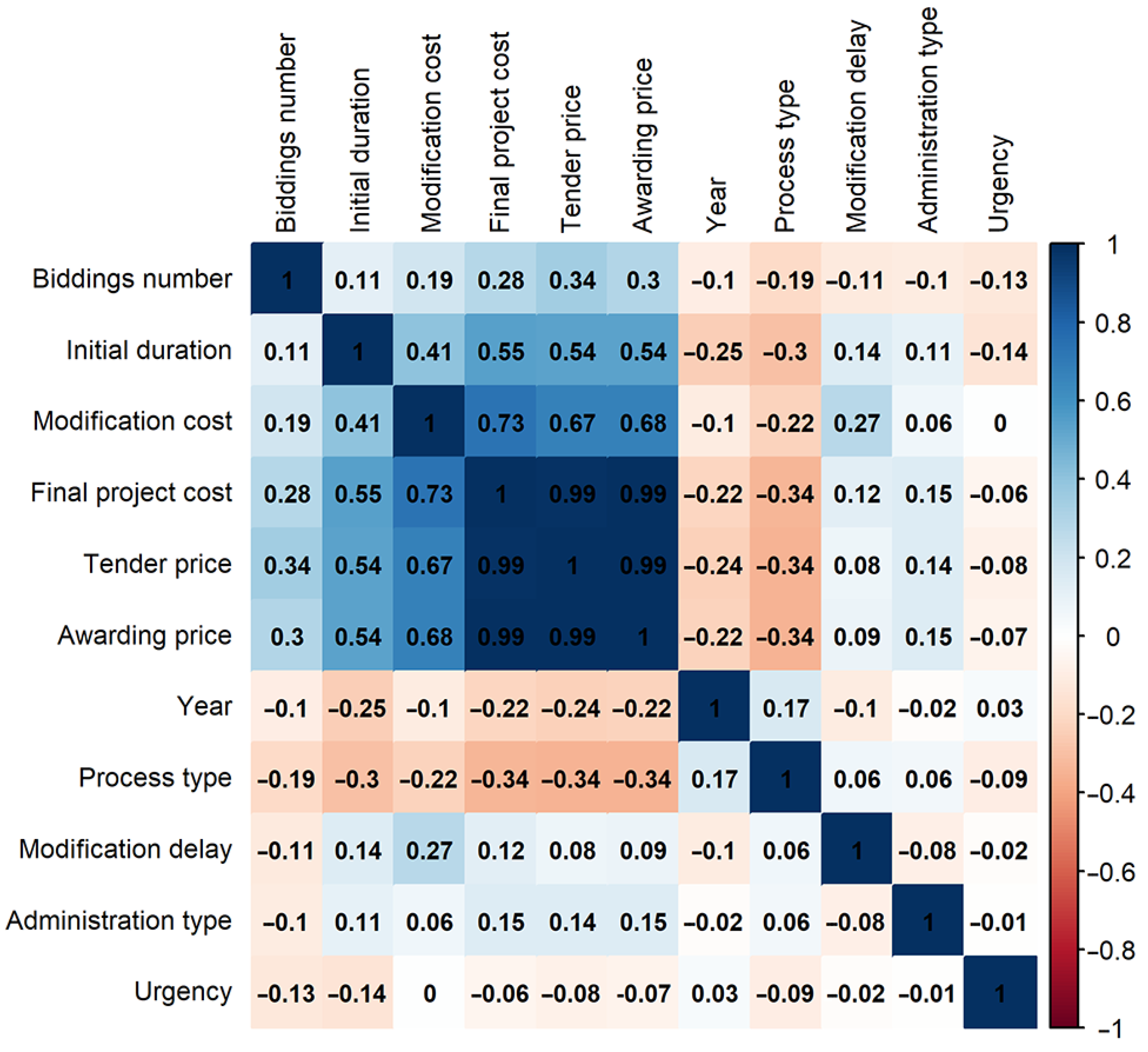

A correlation matrix (

Figure 2) was created using the Spearman correlation test and the corrupt package in R to identify the principal dependencies and relationships among database variables. Positive values indicate direct relationships, while negative values indicate indirect ones. The range of values ranges from 1 to −1, with 1 indicating strong positive correlation, 0 indicating no correlation, and −1 indicating strong negative correlation. The following notable relationships emerged from the analysis:

Modification cost vs. Modification delay: There are low correlation relationships between variables like “Modification cost” and “Modification delay” (0.27), contradicting the assumption that increases in one should correlate. It may be supposed that delays would cost more money for the extra time working, however, it shows that in the database exits cases with project delays at no extra cost;

Modification cost vs. Urgency: The relationship between modification variables and “Urgency of processing” also contradicts intuition (very low, −0.14). Urgent processes with less time to be developed, may result in less efficient and accurate tendering that would need later modifications. Despite that, likely influenced by the limited number of urgent or emergency cases, this relationship is not shown in this research database;

Bidding number: The bidding number positively correlates with cost-related variables. The higher coefficients correspond to “Tender price” (0.34) and “Awarding price” (0.3). It is notable that “Awarding price” has less correlation than “Tender price”, as it can be thought that competitiveness (number of bidders) would have to influence it more in awarding than in base bidding. However, theses coefficients would have been expected to be higher;

Initial Duration vs. Prices: The study reveals a significant correlation between “Initial duration” and other cost-related variables (“Final project cost”, “Tender price”, and “Awarding price”), with longer project durations often leading to higher costs across all project price metrics. It also shows a moderate correlation with “Modification cost” of 0.41, as larger projects are more likely to face problems than smaller ones;

Modification cost vs. Final project cost, Tender price, and Awarding price: The correlation of “Modification cost” with these variables are its highest values (0.73, 0.67, and 0.68). It shows that larger projects lead into larger “Modification cost” with relatively high correlation. It can be noticed that the higher correlation is obtained with “Final project cost” as it is the price affected by “Modification cost”, but not by a large margin, which corroborates that the larger the project, the larger the modification in absolute terms;

Final project cost vs. Tender price vs. Awarding price: The correlation of theses variables is very strong, with a coefficient of 0.99. A detailed analysis is conducted for H1 test between “Final project cost” and “Tender price”, which are crucial in Spain.

5.2. Hypothesis Analysis: Final Project Cost vs. Tender Price (H1)

The study focuses on the relationship between “Final project cost” and “Tender price” after analyzing the database. The aim of this analysis is to understand the relationship between initial and final costs when project modifications appear, instead of how and why they are caused.

The Anderson–Darling test assesses normality, with low

p-values nearing 0. This assessment guides the selection of statistical methods for further analysis. As depicted in

Table 9, Spearman’s rank correlation test confirms a statistically substantial correlation between the variables, with a coefficient of 0.99 and a

p-value of zero.

The Wilcoxon test showed a significant difference between the distributions of the medians of variables. In contrast, the Kolmogorov–Smirnov test has no substantial difference between the prices of the variables, with a parameter D value of 0.03 and a p-value of 0.86. The different results are due to their different focus points. The Wilcoxon test focuses on variations between variables, detecting significant differences in final and tender price medians, even if data distributions are similar. On the other hand, the Kolmogorov–Smirnov test examines the complete distribution of data and detects significant disparities in cumulative distribution functions. It is possible that the Wilcoxon test can detect significant disparities in medians.

As conclusions from the hypothesis testing showed above, it can be stated that it exists a statistically significant correlation between “Final project cost” and “Tender price” resulting in a Spearman’s rank correlation of 0.99. It was supposed to be a high correlation between them (but maybe not that high), as both prices are directly related, so Wilcoxon and K–S test have been also performed to clarify it. From them, it can be stated that differences between medians of both variables are statistically significant because, after the award processes, the budget upon which modification calculations are based has changed significantly, making it impossible to reach the exact bidding price. This is typically the case as bid reductions often exceed the permitted limit values for modifications. Nevertheless, as indicated by the K–S test, the distribution of both variables aligns, as in most cases, the aim is to attain the maximum legal limit for modifications, following a common pattern that preserves the distribution of both prices.

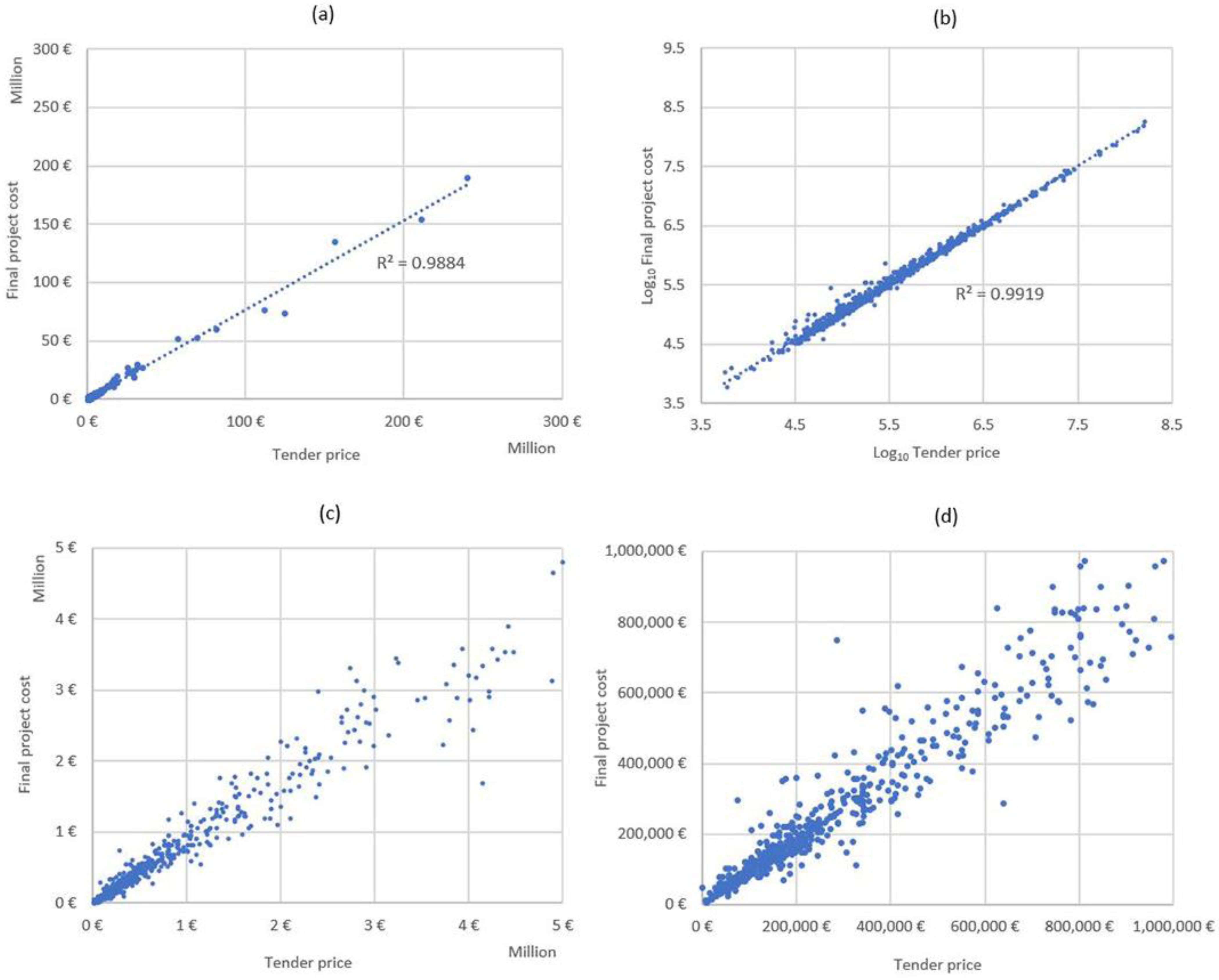

In order to complete the hypothesis testing, graphical analysis is used to confirm and look for more findings.

Figure 3 shows a distinct connection between two variables, particularly in smaller projects, as the correlation test outcome predicted. The graphs reveal several observations, particularly in cases with budgets of up to €5 million and €1 million, enhancing the observation of this phenomenon.

The correlation between “Tender price” and “Final project cost” is strong, with coefficient of determination (R2) values exceeding 0.98 in all four scenarios;

Logarithmic representation helps us understand the correlation between variables across the dataset, especially in cases with varying values, as seen in

Table 6. It reinforces the relationship with higher R

2 values, thereby confirming the relationship;

The trend line in all four scenarios follows a 45-degree line, indicating equivalence between variables. However, as project price limits increase, the trend line diverges, shifting towards the “Tender price” axis;

The trend suggests that a more efficient bidding process leads to lower final project costs due to higher overall project costs;

The correlation between the two prices in smaller projects is nearly 1:1.

Figure 4 shows histograms comparing bid reduction and the percentage correlation between the “Final project cost” and bid price. The results show a divergence in values and the impact of modifications on the contract cost. In an ideal scenario, both histograms would coincide, but a significant discrepancy is evident in the final cost histogram, particularly around the 95–100% range, often exceeding these values.

Spanish public construction companies often exploit legal margins by modifying project proposals to increase costs [

57]. They submit substantial reductions to secure contract awards, expecting later recovery of margins through modifications. These modifications are justified by technical deficiencies, new project requirements, and the inconvenience of initiating new procurements [

19].

Modifications intended to rectify errors in project design have become a common practice, with contracting firms artificially inflating final project prices. This deviation is due to poor quality initial construction projects; inadequate technical and administrative bidding documents; and a lack of completeness, thorough study, specificity, and practicality. The Council of State and the Court of Justice of the European Union have criticized Spain for its deficient project approval processes (Judgment of the CJEU on 31 January 2013, No. T-235/2011). This has a significant impact on project execution.

The process of halting a project, changing contractors, and initiating new tender processes for modifications is often complicated by administrative hurdles, increased workload, and delays due to tender deadlines. The costs of terminating contracts, indemnifying contractors, drafting new projects, and starting new tasks often exceed the costs of accepting modifications. Additionally, corruption in public administration positions [

58] and changes in the legal framework governing public contracts and modifications have led construction companies to adapt their behaviour to maximize self-benefit within the prevailing legal framework. In summary, the results of statistical tests, graphical analyses, and insights from other studies support the possibility of rejecting the initial hypothesis. It is plausible to assert the existence of inefficiencies within Spain’s public construction tendering system, where final project costs often align with initial bid prices through modifications as a legal tool.

5.3. Hypothesis Analysis: Legal Framework Limits Analysis and Comparison (H2)

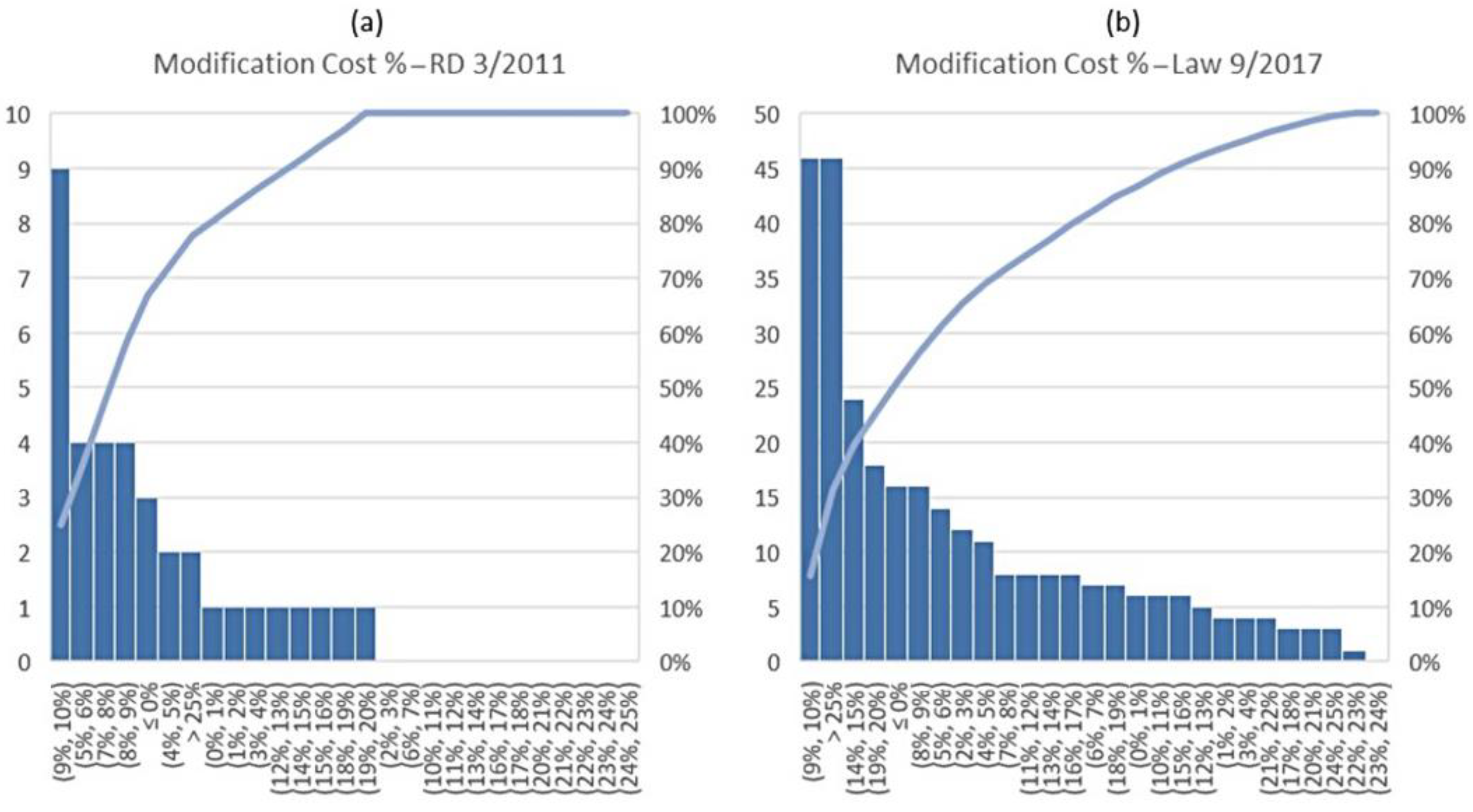

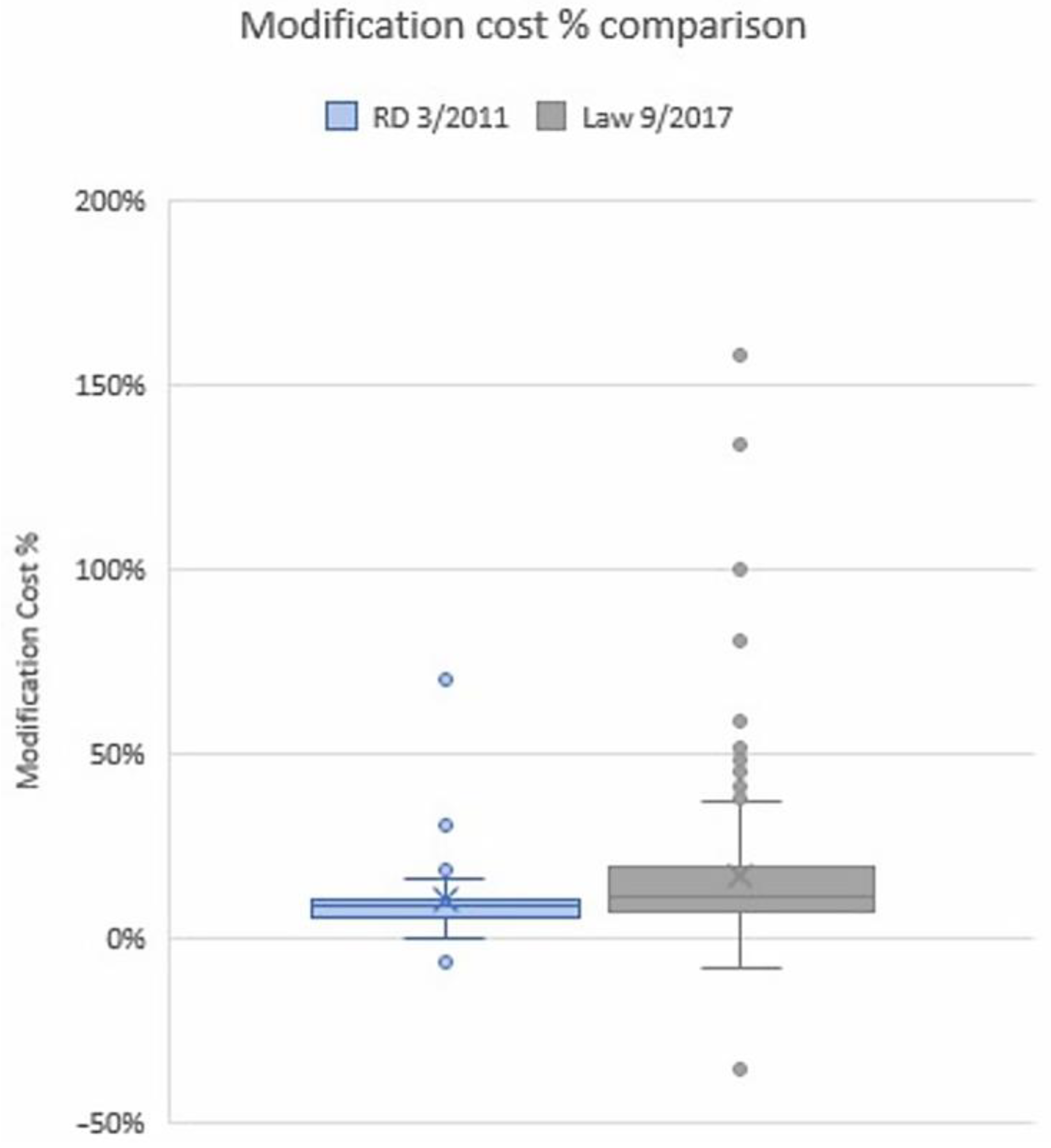

To analyse the second hypothesis concerning the correlation between stipulated legal limits of modifications and their actual recorded values, a Pareto chart illustrating “Modification cost” as a percentage (modification cost/awarding price) has been illustrated in

Figure 5. The database is segmented into two time intervals: 36 cases recorded before March 2018 under the influence of RD 3/2011 and 293 cases between March 2018 and April 2020 impacted by Law 9/2017. The analysis terminates in April 2020 to avoid the exceptional effects of COVID-19.

Figure 5a, focusing on cases influenced by RD 3/2011, illustrates a dominant frequency around the stipulated legal limit of 10%, with few instances surpassing this threshold. A more varied distribution is evident in the second period governed by Law 9/2017 (

Figure 5b). However, three of the highest frequencies align with the legal limits, particularly the most prominent one at approximately 10%. This trend can be attributed to several factors:

The acceptance of 10% as a reasonable value for modifications in Spanish civil engineering project management;

The concentration near 15% aligns with the legal limit marking non-substantial modifications in construction contracts, the most prevalent category in the dataset;

Cases clustering around 20% may be due to legal limits set in administrative regulations;

Instances exceeding 25% are higher due to unforeseen circumstances that can justify modifications up to 50% of the initial cost.

Figure 6 reveals that the average modification value in Spanish civil engineering projects increased from 9.99% in the first period to 16.52% in the second period, indicating that the expanded legal limits intentionally influenced modifications’ distribution. Additionally, Law 9/2017’s leniency, compared to its predecessor, may have contributed to greater cost overruns.

In summary, following the comparison using the Pareto chart and box plot between both legal periods, a distinction in the behavior of recorded project cost modifications could be observed. Despite the limited number of cases in the first period, the trends in both periods are sufficiently clear to argue the significance of the influence of the prevailing legal framework in each era. Prior to the enactment of Law 9/2017, both the mean values, quartiles, and histogram distribution encompassed smaller values compared to the subsequent period with more lenient legislation.

Spain has been subject to sanctions by the European Union in the past due to excessively high project modifications. With the current legal framework, a resurgence of this issue is being observed, which could potentially lead to new disputes with the EU. In addition, addressing this problem internally is more challenging, as construction companies operate within the bounds of the legal framework, exploiting every possible aspect of the regulations.

Nonetheless, there is currently greater awareness against such practices, and more and more institutions and organizations are working to combat them. Although not directly related to project modifications, in July 2022, the Spanish National Commission on Market and Competition (

Comisión Nacional del Mercado y Competencia) imposed a significant fine of 203.6 million euros on six of the country’s largest construction companies for illicit oligopoly practices [

59]. It was proven that these companies colluded and shared information about public tenders to divide the market among themselves.

Hence, through endeavors such as this study that shed light on this issue and the transparency efforts of certain institutions, it is possible for stakeholders to work towards finding a solution to this problem. This can also serve as a valuable lesson for other sectors or countries, helping them to avoid similar issues.

6. Conclusions and Future Research

The study uses a database of actual projects and various variables to explore the link between project cost overruns and modifications in Spain’s public civil engineering projects. To address it, the relationship between base bid price and final project cost after modifications is investigated. In addition, cost overruns via modifications are analysed for two different legal periods, to reveal the influence of legal framework on these modifications. However, the aim of this paper is to highlight and describe the problematic public works modifications in Spain, more than explore possible solutions that are out of the scope of this research and within the scope of future research. The findings suggest that:

While the relationship is established in academic literature, the quantitative percentages need improvement due to reliance on expert surveys rather than case studies;

Spain’s legal framework for project modifications has significantly evolved over the past two decades, with Law 9/2017 increasing the modification percentage limit over the awarded price for public works;

Cases before Law 9/2017 had lower modification percentage values, with mean costs at 9.99% and increased to 16.52% in the later period;

The study confirms the relevance of the Spanish legal framework to project modification costs, showing that mean values align with legal limits, and a Pareto chart indicates case concentration around these limits;

The inefficiency of Spain’s public construction procurement system is confirmed by significant correlations between base bidding prices and final project costs, disparities in price reduction relative to base bidding prices, and graphical analyses;

Limitations of the study include data quality issues leading to a smaller database and the exclusion of inflation effects on project costs due to separate legal mechanisms.

These findings have implications for Spanish society and public administrations, providing insights into current management and legal frameworks for cost overruns in public works. The study’s relevance extends to other countries, offering opportunities for improvement and lessons to avoid. Potential future research includes predictive models for project cost overruns, examining bid processes’ influence on modifications and final costs, and exploring relationships between project characteristics and bid outcomes.

Primarily drawn from data on the Public Sector Contracting Platform (PLACSP), the study’s findings are contingent upon data accuracy and availability. Potential data incompleteness or inaccuracies could introduce biases and influence conclusions. Furthermore, the study’s scope is confined to a specific time frame and context, potentially limiting the generalizability of the results. Assumptions of stable economic criteria and practices over time might only partially encapsulate the intricacies of project dynamics. Moreover, while the analysis identifies correlations, attributing causality remains intricate due to the multifaceted nature of the interplay between legal changes, project complexities, and stakeholder behaviour.

To address these limitations and further enrich the understanding of the legal framework’s influence on project modifications and cost overruns, as well as possible solutions for the problem exposed, future research avenues present promising prospects:

Conducting longitudinal analyses over extended periods could provide more nuanced insights into trends and developments;

Comparative studies across diverse countries could unveil the context-dependent impact of regulatory changes on project outcomes;

Employing advanced analytical techniques, such as predictive modelling, could yield forecasts and enhance the predictive accuracy of the relationship between legal changes and project performance;

Through interviews or surveys with industry experts, qualitative research could offer deeper insights into decision-making processes and adaptive strategies;

Exploring policy implications, the role of transparency, and comparative legal analysis across countries is pivotal to further illuminating the intricate dynamics of legal frameworks and their ramifications on construction projects;

Solutions for the tendering system can be developed for this problem. For example, BIM modulation could enhance project performance and modifications processes, both for large and small projects;

Causes that lead to these modifications can also be studied for problem solving; the relationship between design phase resources with the rest of the project emerges as a possibility, among others.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}