Abstract

Collusion is an all-pervading illegal market behavior that can undermine the sustainable development of the construction industry. It is acknowledged that collusive bidding decision making is influenced by conspirators’ cognitive bias. Nevertheless, the understanding of such an influence mechanism remains vague in the literature. This study aims to examine the mechanism of conspirators’ to-collude decision making by establishing a system dynamic model. The model development is based on the theories of cognitive biases, collusive bidding, and complex adaptive system. Multiple scenarios were simulated in the context of the Chinese construction industry. Three most influential cognitive bias are overconfidence, the illusion of control, and cognitive dissonance. The simulation results reveal conspirators’ intrinsic mechanisms to decide whether they deserve to participate in collusive bidding. The evolution of to-collude decision making is characterized by nonlinearity, multiplier, and stimulus enhancement effects. Collusion motivation and enterprise network relationships expand conspirators’ to-collude decision making. The increase of government regulation intensity and enterprise performance inhibit conspirators’ to-collude decision making. This study provides an insight into the cycle of collusion emergence from a complex system perspective and implies that antitrust authorities can launch carrot-and-stick measures for better regulation.

1. Introduction

Trillions of dollars of construction projects around the world are implemented using a competitive bidding mechanism [1]. The delivery of construction projects and the realization of project development goals are highly vulnerable to the competitive bidding mechanism’s openness, justice, and operational efficiency [2]. Meanwhile, collusive bidding is an outstanding industrial issue in all international construction sectors. Numerous collusive bidding cases, including price cartel, bid rigging, and bid rotation, are often reported worldwide [3,4,5]. The lack of effective countermeasures has made collusive bidding a stubborn disturbance to market operation [6,7], resulting in economic disruption [8].

A generic feature of collusive biddings—horizontal [9], vertical [10], mixed—goes to their market misconduct nature. Bidders involved in these collusive bidding practices are called conspirators. Conspirators may be blacklisted, disqualified, or punished by antitrust authorities when their collusive behaviors are exposed. Notwithstanding serious potential punishment, the vast majority of bidders consistently decide to launch cover bidding, bid rotation, and bid suppression. The concealment of collusive bidding can contribute to the explanation, which makes partial bidders act in the way of guessing what rivals’ tactics are and performing to the best of their ability to get complete bidding information. The information cannot be fully disclosed for they are commercial secrets. According to the cognitive bias theory, the decision maker’s cognition owns the preference to be biased affected by the bounded information, resulting in risky decisions. Moreover, human attributions to learning and imitation demonstrated by anthropology tell that people’s next behaviors can be influenced by previous outcomes. It implies a cycle of collusion running in the AEC sector that makes collusive bidding emergence and all-pervading. Thus, finding and describing the deep mechanism of collusive bidding decision making with the aid of cognitive bias theory can offer new explanations to the collusion issue.

Collusive bidding embraces a decision-making process that bidders take to determine the best option to collude or not to collude. According to current behavioral decision theory, to-collude decision making is enveloped in a black box system. Revealing a collusive bidder’s decision-making mechanism is assumed to generate a golden key to open the black box. However, the mechanism is rather complicated. One of the main reasons is the complexity of collusive bidding that is implied by the game theory [11], the network theory [12,13], and the auction theory [14,15]. Asymmetric information can be another factor stimulating bidders to make egocentric decisions to choose collusive behaviors [16]. Furthermore, inadequate incentives for whistleblowing discourage explicit attempts to disclose information about collusion in local markets [17]. Factors affecting the to-collude decision making are anchored in bidders’ communication and trust [16]. Although the values of collusion detection [18,19], the causality of collusion [20], bidder’s collusive willingness [21], and the determinants and factors of collusion [22,23] have been presented in previous studies, further exploration seems feasible to construct conspirators’ decision-making mechanisms from the perspective of cognitive bias.

According to cognitive psychology, collusive behaviors can be manifested under the heading of cognitive bias using systematic and random factors. The systematic factors include industrial self-regulation and governmental intervention. The random factors might be business-specific or individual [24]. It is assumed that the cognitive bias influencing mechanisms on to-collude decision making are requisites for manipulating collusive behaviors. This study employs the theories of cognitive bias and complex adaptive system (CAS) to illustrate conspirators’ to-collude decision-making processes. A system dynamics model is proposed, based on collusive subjects’ interaction, which extends the associated decision making from individual behavior ontology to an entire evolution system. Thereby, the complex adaptive outline of to-collude decision making can be better imaged. Moreover, the paper reveals the influencing mechanism of to-collude decision making, describing the causes and effects of conspirator cognitive bias and recommending countermeasures for collusion mitigation. The contributions of this study can be addressed as we provide an insight into the cycle of collusion emergence from a complex system perspective and implies that antitrust authorities can launch carrot-and-stick measures for better regulation.

The paper is organized as follows. Section 2 reports the literature review and a conceptual framework. Section 3 describes models, data, and tests, etc. Scenario simulations are illustrated in Section 4. Section 5 presents the research findings and discussion. Finally, conclusions and limitations are provided in Section 6.

2. Literature Review

2.1. Cognitive Bias Theory

Cognitive bias, originating from human-bound rationality debates, has undergone three main development stages. Originally, decision makers were considered naive scientists owning objective cognitive ability who can make rational decisions as scientists do regularly [25]. With the introduction of social cognition and information psychology, researchers found that decision makers are prone to systematic bias and decision deviance, given the interaction between the internal and external environment. After that, academic debates reached another milestone. Decision makers were deemed cognitive misers [26], owning limited information processing ability. They prefer choosing strategic shortcuts based on experience and intuition, emphasizing that personal preference triggers the emergence of cognitive bias.

Since the 1990s, academic debates on cognitive bias have received closer attention and the significance of uncertain information interference on personal cognitive bias has been acknowledged [27]. Studies at this stage discerned two kinds of uncertain information of cognitive bias—personal and socio-environmental [28]—and subdivided the socio-environmental factors into multi sectors regarding policy, enterprise, and economy [29,30,31]. Cognitive bias has been framed in behavioral economics and enterprise management and is widely applied due to its representativeness, availability, and anchoring [32,33,34]. Recent years have witnessed additional types of cognitive bias, such as overconfidence [35], cognitive dissonance [36], illusion of control [37], correspondence bias [38], fundamental attribution error [39], self-serving bias [40], and matching bias [41]. The proliferation of previous research shows more clues about the factors determining cognitive biases toward finalizing a to-collude decision.

Cognitive bias twines around individuals’ decision-making processes. Keusch et al. [42] clarified that enterprise managers are accustomed to a thinking pattern of self-serving bias. The pattern will be more apparent when enterprises are stuck in the cycle of economic crisis. Enterprise stakeholders are unbeneficial from CEOs’ overconfidence as irrational decisions can give rise to return overestimation and risk underestimation [43]. Safari Gerayli et al. [44] echoed this statement and additionally demonstrated that managerial overconfidence erodes the enthusiasm of CEOs to monitor firms’ internal control, which may result in internal control weaknesses. The deeper the cognitive bias, the greater the probability of dissimilation of managerial decision deviance. Thus, it is no surprise that a directors’ board spends much time curbing managerial overconfidence to impede CEOs from making an ineffective investment decision [45].

2.2. A Conceptual Framework

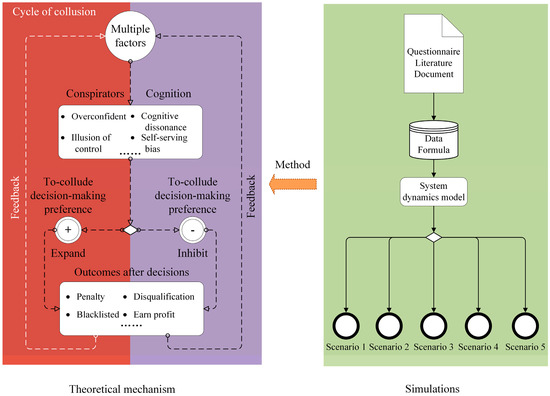

In line with the principle of cognitive bias, a conceptual framework is proposed to portray the influence of cognitive bias and its factors on to-collude decision making, as shown in Figure 1.

Figure 1.

A conceptual framework and methodology flow.

Conspirators are engaged in a collusion network characterized by individuals’ heterogeneity, isomorphism problems of communities, and unexpected external changes [46,47]. According to the complex adaptive system (CAS), conspirators tend to believe in the law of small numbers after successfully operating collusion in the network. The success this time enables them to imagine that they will likewise succeed the next time. Alignment effects facilitate other conspirators to imitate previous successful cases and arouse an emergence of collusive bidding. Being adaptive agents, conspirators have their own ability to examine the information about policy enforcement, financial punishment, and incumbent competitors. However, their decision-making preferences differ due to limited information and self-learning abilities. Sometimes, conspirators pursue closer collaboration with partners to form meta-agent and meta-meta-agent, such as price cartel, rotation, bid compensation, bid affiliation, and monopoly. Hence, a to-collude decision-making adaptive system (CDAS) was coined in this study to reflect the aggregation, diversity, and flow characteristics of collusive bidding. The CDAS is composed of considerable head, waist, and tail bidders, reflecting the tag characteristics of CAS.

The uncertainty produced by random factors alters the scope of conspirators’ cognitive bias and determines their to-collude tendency. For example, speculative delusion might enter conspirators’ minds as attracted by a high expected return of collusion and a low severity of punishment. In addition, the external environment is the main driving factor in conspirators’ cognitive biases regarding a highly competitive market environment and ineffective regulation [2], low professional quality of government employees [48], and an incomplete set of legal documents [49]. These factors function as the building blocks of the CDAS, adjusting conspirators’ cognitive biases and further promoting the evolution of the CDAS. As a result, collusion can be detected between enterprise performance and government regulation, and thus they are viewed as the key variables of the CDAS.

On the one hand, motivation involves the biological, emotional, social, and cognitive forces that activate behavior to describe why a person does something. In this paper, the term “collusion motivation” is used to address why bidders launch a collusive bidding. A stronger collusion motivation means higher expected returns of collusion. As a profit-driven bidder, they may continue falling into the illusion of profit making. The better accessibility and robustness of the enterprise network that conspirators belong to, the more conspirators capture the information of “reliable to-collude objects”. Thereby, a sense of overconfidence in collusive bidding is consolidated, triggering collusive behaviors. The success of collusive events exhibits recency effects and resonance to those bidders that take a wait-and-see attitude without undertaking collusion. Consequently, the whole CDAS is caught in the cycle of collusion. On the other hand, a better business performance reduces conspirators’ survival pressure; thus, their to-collude preference will be lower in a competitive bidding system. Moreover, conspirators’ cognition may be debiased by government regulation as they are subjected to financial punishment. Self-learning helps conspirators recognize the seriousness of regulation constraints, awaking that breaching market order may induce self-defeat and elimination from the market; thus, realizing expected collusion income at the risk of losing reputation and being blacklisted benefits conspirators from dropping out of to-collude decision making.

3. Methodology

System Dynamics (SD) is a top-down approach, combining social science with natural science, which concerns the structure and function of system. Compared with other models, SD is more suitable for dealing with social behavior issues constrained by small samples and low precision. The modeling of SD depends on existing academic experience and scientific conclusion. Making appropriate decisions and suggestions to solve real life problems, scenario-oriented tests and computer-based simulations are needed. In addition, the purpose of using SD in this study is to provide effective tactics’ comparison, as opposed to accurate numerical prediction. Hence, we employ an experts’ scoring and questionnaire method to build the SD model. The SD model of conspirators’ to-collude decision making was constructed following three major steps. First, variables were introduced to describe “conspirators’ cognitive biases” and “to-collude decision making”. Second, we identified factors for these two variables by the literature reviews. Lastly, all variables’ values were calculated and simulated. The methodology flow can be found in Figure 1.

3.1. Model Variables

Through critically reviewing the relevant literature [50,51,52], we categorized twelve types of cognitive biases (Table 1). Overconfidence refers to the belief that the accuracy of one’s own perception and knowledge is higher than that of the facts. Overconfident individuals will give a greater weight to the information he or she can get rather than to the unknown ones. Illusion of control—individuals overemphasizing the role of their own ability in the task—opportunity, and luck are key points. Cognitive dissonance means that individuals pursue their own internal consistency. When external evidence is inconsistent with internal cognition, it will arouse an unpleasant state and individuals will try to avoid this force. Self-attribution bias can be described as an individual attributing success to their own ability while failure belongs to external factors. In addition, people who are prone to take their previous tries as the references to guide their next decision in case of the little information they can gather will get stuck in anchoring. In short, as psychological concepts, the types and meanings of cognitive biases are diverse.

Table 1.

Scores of cognitive biases.

Experts’ scoring is an effective instrument for detecting conspirators’ cognitive biases. Hence, experts who had much knowledge of collusive bidding practices were invited to rate the importance of the twelve cognitive biases. The experts have both extensive experience and assume important posts in the industry, making the scoring trustworthy. The detailed profiles about the experts are given in Table A1 of Appendix A. We followed a rule of thumb to devise scoring criteria for experts to consider, namely extremely insignificant (0–20 score), insignificant (20–40 score), neutral (40–60 score), significant (60–80 score), and extremely significant (80–100 score). Those cognitive biases with an average score of more than 60 were treated as significant items. We sent the score sheet and criteria to experts by email. We removed samples that were not completely and correctly answered. We accepted the samples from experts with over 5 years of career experience. Ten score samples were included. To make samples more reliable, follow-up emails to the experts were utilized to check and discuss the score they offered. Consequently, the most significant cognitive biases are: overconfidence, the illusion of control, and cognitive dissonance (i.e., model variables). In particular, some variables were utilized to describe the “to-collude decision making,” such as “action of collusion” and “enterprise network relationship” (Table 2 and Table 3 and Figure 2).

Table 2.

Main variables and factors of the model.

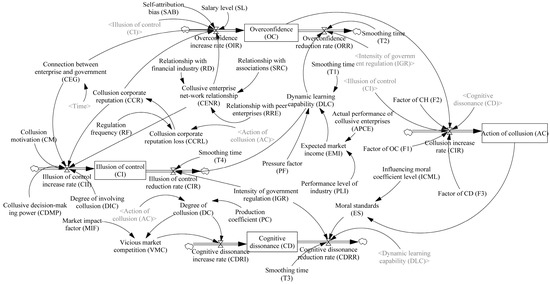

Figure 2.

A to-collude decision-making model.

Personal factors for “conspirators’ cognitive biases” were initially compiled through a comprehensive literature review, as shown in Table A2 of Appendix A. The appropriate factors selected by the same experts’ scoring are given in Table 2. Overconfidence is determined by the illusion of control [53] and self-attribution bias [54]. Thus, these two cognitive biases were viewed as the factors of overconfidence. In addition, the external factors for conspirators’ cognitive biases were screened, namely the connection between enterprise and government, intensity of government regulation, collusion corporate reputation, and enterprise network relationship.

3.2. Estimation and Data

China Judgment Online is an integrated and open platform for the Supreme People’s Court of China (SPC) to publicize court documents, offering high-valued materials for investigating collusion issues. The SPC is the highest trial organ in the country and exercises its right of trial independently. A combination of keywords “bid rigging”, “construction”, and “judgment of the first instance” was adopted to screen out relevant materials over the period from 2014 to 2020. Eventually, 207 cases were retrieved.

Seventy-six cases declared that a compensation fee was paid to collusive group members after winning a bid. These cases were used to calculate the collusion motivation (CM) (Equation (1)). Supposed refers to collusion motivation, which refers to the potential profits that conspirators can obtain through collusive bidding; stands for winning bid price; is the proportion of collusion fee indicated by the 76 cases. An equation of calculating the is as follows:

We excluded the maximum and minimum values in 76 cases and applied the logarithm of profits to all the cases. The average derived is 3.93.

The equation of calculating government regulation intensity is as follows:

where refers to the intensity of government regulation (), 5‰ was cited from “article 223” of China’s criminal law stipulating punishment for collusive bidding. We input the data of 207 cases into Equation (2) to calculate the , and the derived is on average 3.73. Similarly, expert interviews assigned other variables with different values, as shown in Table 4.

Table 3.

Eigenvalues of the main variables.

Table 3.

Eigenvalues of the main variables.

| Variables | Eigenvalues | Questionnaire Templates |

|---|---|---|

| Overconfidence | 5.25 | [55] |

| Illusion of control | 5.55 | [56] |

| Cognitive dissonance | 5.01 | [57] |

| Self-attribution bias | 3.49 | Derived by referring to Weiner’s attribution theory |

| Moral standards | 4.06 | [58] |

| Collusion corporate reputation | 4 | Rep Trak Pulse Scale |

| Salary level | 3.47 | If the income is less than CNY 5000, it will be assigned as 1, and so on to 5 |

| Degree of involving collusion | 2.75 | If the role is other, it will be assigned as 1, and so on to 5 |

| Collusive decision-making power | 2.11 | Engaged in construction projects for 0–3 years, it will be assigned as 1, and so on to 5 |

| Relationship with the financial industry | 1.08 | If one has never held a position in the financial industry, it will be assigned as 1, and so on to 5 |

| Relationship with peer enterprises | 1.84 | If one has never held a position in the construction enterprise, it will be assigned as 1 and changed to 5 |

| Relationship with associations | 1.10 | If one has never held a position in the engineering association, it will be assigned as 1 and changed to 5 |

Table 4.

Main items of the proposed model.

A questionnaire survey was implemented to obtain professionals’ views on the initial values of variables (Table 3). Weight per factor was calculated using a cloud model and expert scoring (Table 2). The results show that overconfidence, the illusion of control, and cognitive dissonance occur more frequently as their eigenvalues are greater than others.

3.3. Model Assumption and Setting

We made three assumptions below to ensure that the validity and operability of the proposed model are acceptable. First, we followed a hierarchical logical route called “factors-cognitive biases-collusion-factors” (i.e., A-B-C-A, cycle of collusion) to build the SD model. For instance, only the direct linear effects of overconfidence, the illusion of control, and cognitive dissonance on to-collude decision making were considered; otherwise, the SD model will be too complicated to employ. Second, according to existing research, we assumed that the interactions between cognitive biases and their interfering factors are linear while the interactions of partial factors to factors are nonlinear. Lastly, collusive bidding is clearly banned by laws in China, such as the “Tendering and Bidding Law of the People’s Republic of China” and the “Law of the People’s Republic of China Against Unfair Competition”; doing so will result in charges and financial penalties and will be reported by the media, ruining the corporate image. Therefore, we supposed that conspirators must bear reputation loss and financial punishment when collusion is uncovered.

Reputation loss is measured by the action of collusion (AC) and regulation frequency (RF), while financial punishment is quantified using the IGR. According to the above argument, a system dynamics model is proposed in Figure 2 to image conspirators’ to-collude decision making.

3.4. Model Testing

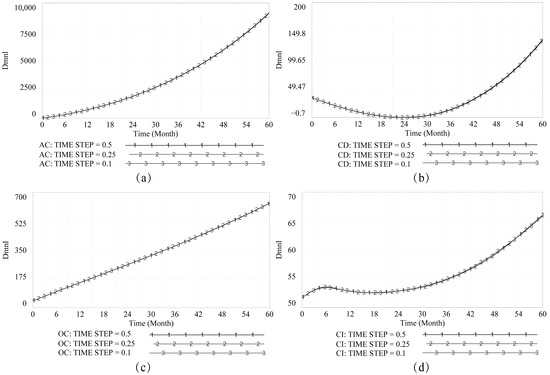

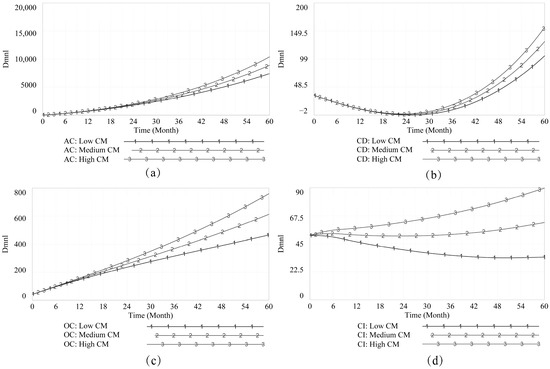

Defining an appropriate time scale is necessary for system examination. To-collude decision making is bidders’ behaviors, but the extent to which bidders’ behaviors represent company behavior is definitely high. According to the Enterprise Life Cycle theory (ELC), a company’s life cycle consists of four small stages (e.g., start-up, growth, maturity, and death); each is around 3–6 years. Hence, to better observe the system’s recurrent fluctuation, we assigned a time scale of sixty months to reflect the evolution of to-collude decision making. The initial time step was set as . After that, three scenarios were determined using different time steps: , and . As Figure 3 tells, the evolution of AC, CD, OC, and CI has minor differences between scenarios, suggesting that the model’s integral error is small and acceptable.

Figure 3.

Integral error test of the model. Subfigures (a–d) illustrate the AC, CD, OC, and CI curves under varied time steps.

We adjusted the CM from small to large and found that the AC increases simultaneously, demonstrating acceptable model sensitivity. In addition, the same results were obtained for the tests of other factors such as CENR and APCE. When the initial value of OC reduces from 41.66 to 0, the evolution of AC significantly decreases. Theoretically, debiasing overconfidence means the reduction of decision-making interference and the capability of objective evaluation and information acquisition will be improved. It is found that the model test results can echo such a statement. Thus, the model can be used for scenario simulation.

4. Scenario Simulations

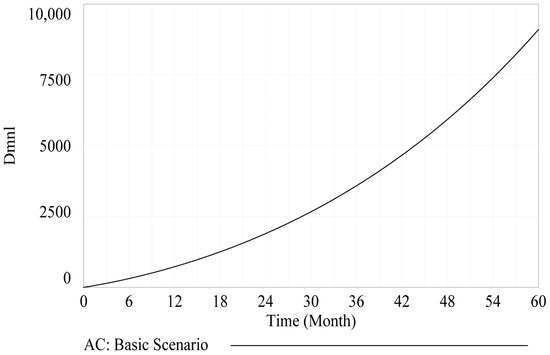

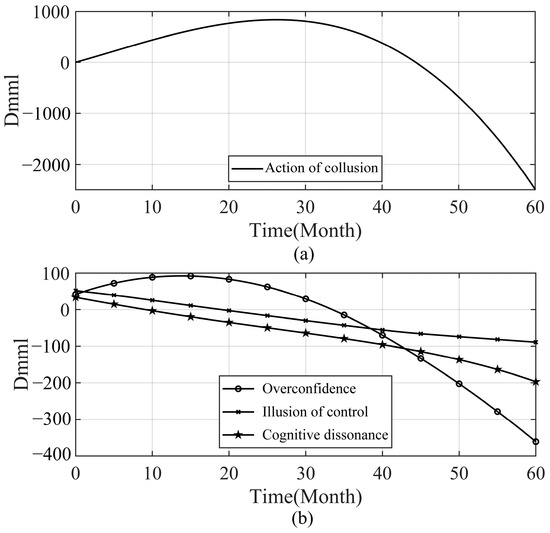

Five scenarios were included to explore the impacts of factors on to-collude decision making. Specifically, Scenario 1 functions as the basic scenario to illustrate the impacts without changing the external environment, that is, inputting the initial data collected to observe the system’s future evolution based on existing conditions and with no control group. In addition, four extra scenarios were set by adjusting the following factors: collusion motivation, enterprise performance, enterprise network relationship, and government regulation intensity. The basic scenario (Figure 4) describes the influence of cognitive biases on conspirators’ to-collude decision making. The evolution of to-collude decision making was analyzed with initial values of variables and parameters under invariant existing external environment (i.e., basic scenario). As Figure 4 indicates, the AC grows following an exponent curve, suggesting a stimulus enhancement effect in collusive bidding. Nevertheless, collusion is rampant, provided an explicit prohibition of laws and regulations. Thus, the results of basic-scenario simulation reflect a character of nonlinearity development of the CDAS.

Figure 4.

Evolution of AC under the basic scenario.

4.1. Collusion Motivation-Based Simulation

We adjusted collusion motivation (CM) to examine the system’s evolution under several interventions. We treated average CM calculation results as benchmark and determined three sub-simulation scenarios: low (CM = 0.5), medium (CM = 3.5), and high (CM = 6.5). The results reflect an expansion; overconfidence, the illusion of control, and cognitive dissonance have a more significant level when the CM becomes higher and the AC increases (Figure 5).

Figure 5.

Evolution of cognitive biases and AC under the CM scenarios. Subfigures (a–d) illustrate the AC, CD, OC, and CI curves under varied CMs.

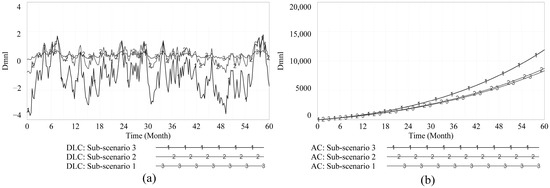

4.2. Enterprise Performance-Based Simulation

Enterprise performance is a key factor that conspirators appreciate before launching illegal business competition. Three sub-scenarios were simulated for the actual performance of collusive enterprises (APCE) and pressure factor (PF) (Table 5). Consequently, the dynamic learning capability curve (i.e., DLC) achieves the highest position and maintains the non-negative interval in Sub-Scenario 1. However, the DLC curve turns to the lowest position in Sub-Scenario 3. Moreover, the AC curve achieves the steepest curve position in Sub-Scenario 3 (Figure 6).

Table 5.

Enterprise performance scenario setting.

Figure 6.

Evolution of DLC and AC under the enterprise performance scenarios. Subfigures (a,b) illustrate the DLC and AC curves under varied sub-scenarios.

4.3. Enterprise Network Relationship-Based Simulation

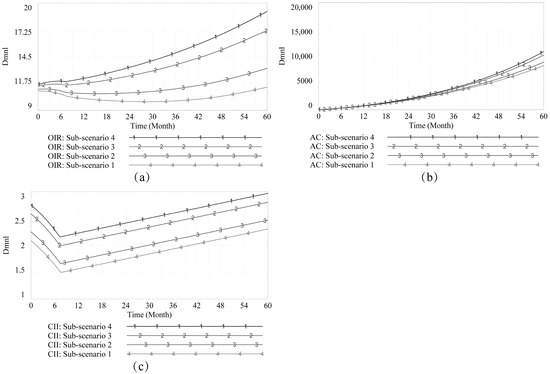

Enterprise network relationships mainly comprise financial industries, peer enterprises, and associations [59,60]. Relationships with financial industries and associations are reflections of the capital of obtaining bidding information and resources for enterprises. The relationship with peer enterprises implies the possibility of collusion. Four sub-scenarios were thus established (Table 6) to reflect the influence of enterprise network relationships on to-collude decision making. As Figure 7 indicates, the larger the enterprise network relationship embedded the higher the illusion of control increase rate (CII), overconfidence increase rate (OIR), and action of collusion (AC).

Table 6.

Enterprise network relationship scenario setting.

Figure 7.

Evolution of OIR, AC, and CII under the enterprise network relationship scenarios. Subfigures (a–c) illustrate the OIR, AC, and CII curves under varied sub-scenarios.

4.4. Government Regulation Intensity-Based Simulation

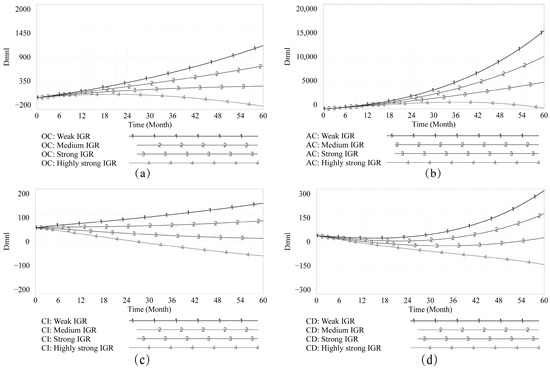

The impacts of IGR on cognitive bias and collusion were simulated using four scenarios of the IGR, namely weak (IGR = 1), medium (IGR = 3), strong (IGR = 5), and highly strong (IGR = 7). As shown in Figure 8, the strong intensity of government regulation is characterized by serious financial punishment, implying a high potential to-collude risk. The OC, CD, CI, and AC are significantly reduced and turn to a decreasing trend when the IGR becomes lower. Following this result, as shown in Figure 9, the reductions of AC, OC, CD, and CI are more significant under a compound scenario with highly strong IGR, low CM, high performance, and low pressure (i.e., Sub-Scenario 3 in Section 4.3), and non-over-embedded network relationship (i.e., RD = SRC = RRE = 1).

Figure 8.

Evolution of cognitive biases and AC under the IGR change scenario. Subfigures (a–d) illustrate the OC, AC, CI, and CD curves under varied IGRs.

Figure 9.

Evolution of AC and cognitive biases under a compound scenario. Subfigures (a,b) illustrate the AC, CD, OC, and CI curves under same compound scenario.

5. Findings and Discussion

5.1. A Multiplier Effect

There are multiple factors in the CDAS, such as high expected collusion return, weak supervision, and low enterprise performance caused by strong business competition. Conspirator cognitive bias results from the coexistence of these factors. As illustrated by Figure 4, to-collude decision making emerges as stimulated by overconfidence, the illusion of control, and cognitive dissonance. The decision-making outcomes, such as to-collude and profit earning, are encapsulated as information carried by factors input into the system to form a feedback mechanism, contributing to the cycle of collusion. As a result, to-collude decision-making preference will be enlarged and the whole CDAS is trapped in the cycle of collusion, reflecting the multiplier effects of the CDAS.

In practice, conspirators are interested in compiling a robust relationship network to obtain external information and maintain closer collaboration with partners, holding an overconfidence view that they can achieve regulatory evasion. Due to the illusion of control, conspirators are experienced in forming collusive bidding groups and manipulating competition outcomes without being detected. As a result, they earn much more relative to reputation loss and financial punishment. Furthermore, those who do not employ collusive bidding approaches would generate self-doubt for competitors’ successful implementation. This is why bidder cognitive dissonance occurs. Consequently, they imitate successful cases in the market and make themselves fit into groups. Collusion resonance gradually becomes the covert order of the to-collude decision-making system. Single collusive behavior induces collusive bidder groups due to the attribution of imitation [61]; therefore, a to-collude decision is made.

5.2. An Expansionary Effect

As demonstrated in collusion motivation simulations, collusion motivation, cognitive biases, and collusion action have the same direction. The to-collude decision-making preference will shift to a higher level when increasing the collusion motivation, reflecting an expansionary effect. The explanation can be given by the conspirator’s attribute of profit-driven [62] motivation. Higher collusion motivation refers to higher expected collusion returns and conspirators usually pay more attention to the benefits obtained by collusion and underestimate the risks brought by collusion. As a result, conspirators fall into more serious cognitive biases, resulting in an expansion of to-collude decision making. On the other hand, a decrease in collusion motivation denotes the reduction of expected collusion returns, which restrains the expansion of to-collude decision making and conspirator decision making tends to be rational.

The AC curve appears to be a straight line under the low CM scenario; thus, it is clear that low return guides conspirators to concentrate on the negative impacts of collusion. Based on the simulation results, we found that the effectiveness of collusion governance merely by reducing collusion motivation may not be high, as cognitive biases show a deepening trend in terms of overconfidence, the illusion of control, and cognitive dissonance. Regarding enterprise network relationship scenarios, our results concur with Jean Tirole’s [63] view that organizational relationships affect collusive bidding. The emergence of collusion is closely related to enterprise network relationships. When enterprise network relationships are excessively embedded, information flows conveniently between conspirators and fortifies interdependence between them. As a result, conspirators fall into the illusion of reckoning they can manage collusive bidding well.

The expansionary effect on to-collude decision making illuminates collusive bidding strategies such as price cartel, rotation, bid compensation, and bid affiliation; specifically, using complex network relations to form alliances encourages long-term collusive relationships. Zhang et al. [64] pointed out that excessive embedding of enterprise network relationships stimulates bidders to embrace overconfidence and the illusion of control. The OIR and CII curves in Figure 7 echo Zhang’s statement. If a conspirator is not engaged with any organization, e.g., an enterprise network relationship is set to 0, it is useless to reverse the increased tendency of to-collude decision making. However, enterprise network relationships are complicated and the collaboration between bidders becomes diversified [65]. Therefore, it may be impractical to enforce regulations to disrupt enterprise network relationships to reap effective governance of collusive bidding.

5.3. An Inhibition Effect

Based on enterprise performance scenarios, it is found that the APCE and the AC maintain a reverse direction. When increasing enterprise performance, the to-collude decision-making preference shifts to a lower level, reflecting an inhibitory effect on the decision making. Given such an inhibitory effect, the evolution curve of the DLC spells out the characteristics of rational decision making when enterprise performance is high and subjects in the complex adaptive system exhibit a self-learning trace. The accepted hypothesis coincides with the consensus that enterprise performance can determine business competition strategies [66]. It seems that bidders will adopt a stable bidding strategy through positive learning when performance exceeds the industry average; thus, boosting enterprise performance helps inhibit collusive bidding.

Conspirators with different tags own changing sensitivity to external information, resulting in cognitive biases and bidding strategies. Supposed governments have no interest in bidders’ heterogeneity and persist with a “one size fits all” intervention on collusive bidding governance. It appears possible to switch enterprise performance from good to poor and pressure from small to large, driving managers to adopt a radical bidding strategy. Thus, the similarity and information confusion caused by the contradiction between the integrity and individuality of the system will be aggravated. Hence, government policies should fit the segments of target bidders [67]. For instance, the carrot-and-stick approach can be adopted according to bidders’ behaviors. Moreover, in reality, excessive competition in the construction industry leads to compression of enterprise profit, low industrial average performance, and high pressure [68]; therefore, without governmental intervention, relying on market regulation to achieve collusion governance may lead to market failure from a long-term perspective.

As shown in Figure 8, the curves of overconfidence (OC), the illusion of control (CI), cognitive dissonance (CD), and collusion action (AC) become lower when the IGR becomes stronger, reflecting an inhibitory effect of IGR. The AC curve evolves into an inverted u-shaped curve when the IGR exceeds a threshold. The evolution of to-collude decision making no longer increases rigidly but decreases after that. Strengthening government regulation intensity gives rise to the failure of system rigidity, debiasing of cognitive biases, and containment of collusion impetus. The rising regulation intensity delivers a strong signal of an unbearable punitive sanction imposed by governments, such as higher financial penalty and employing more accurate collusive bidding detection tools [5]. As a result, the to-collude decision making will be confronted with an inhibition, that is, breaking out of the cycle of collusion. The results highlight the importance and particularity of administrative measures of market regulations. The government is the supervisor and maintainer of market operation, presenting a shred of evidence to strengthen the argument that was merely relying on the invisible hands of the market to deal with collusion. Based on the Keynesian Economic Theory, the superposition of market competition rule with governmental intervention is helpful to reap effective collusive bidding governance.

6. Conclusions and Limitations

Excessive collusion is conductive to eroding a high-quality business environment and weakening high-quality socio-economic development. To address such an industrial problem, the key is to identify conspirators’ to-collude decision-making systems and devise measures based on the characteristics of individuals and systems. This study recognizes conspirator cognitive biases and factors and proposes a system dynamics model to address conspirators’ to-collude decision-making processes. The proposed model shows that the stimulus enhancement effect exists in the decision-making mechanism. Stimulated by uncertain information flow posed by random factors, the feedback path represents an internal model. The feedback path deepens conspirators’ cognitive biases and induces a to-collude decision tendency, imaging the evolution of the complex adaptive system such as nonlinear development and multiplier effect. The greater the collusion motivation the higher the expected returns of participating in collusion. In other words, conspirators prefer executing collusion when having a stronger level of cognitive bias, expressing an expansionary effect driven by collusion motivation. Further scenarios indicate that the influence of enterprise network relationship on to-collude decision making is similar to that of collusion motivation; nevertheless, government regulation intensity shows an inhibitory effect. As the intensity increases the conspirator’s cognitive bias significantly decreases in the long run. Conspirators with better performance and less pressure seem to own more stable dynamic learning ability, low cognitive bias, and relatively low to-collude decision-making preference.

In terms of lifting the construction market out of the cycle of collusion and achieving better regulation, the de-biasing of conspirator cognition is needed. The policy implications can be imposing new regulations and rules to control the external environment mediately, such as expected collusion returns, enterprise network relationship, enterprise performance, and government regulation intensity. Specifically, on the one hand, utilizing grid management and laws makes conspirators feel it is unnecessary to collude. Antitrust authorities can guide masses and social organizations to monitor collusive bidding practices, divide supervision grids by administrative regions, strengthen supervision intensity, and increase financial penalties for collusion. On the other hand, antitrust authorities can utilize collusive members’ voluntary reporting systems to disintegrate collusion networks. They may also provide the carrot of assistance policies and construct a credit system, making conspirators feel unwilling to collude. Moreover, it is recommended to build a credit evaluation system reacting to collusion in the construction industry. An encouragement policy deserves launching for those enterprises with a good credit score. However, the companies with poor credit shall be blacklisted for punishment, promoting benign competition of heterogeneous enterprises through differentiated policies.

The study has some limitations. It is expected that a greater number of experts are needed for future research. Due to the limits of resources, we only consider three kinds of cognitive biases. Future study can be directed to an all-round investigation. In addition, the study is restricted to the AEC sector; findings and conclusions from other sectors with fundamentally varied characteristics may be different. Similarly, the data collected is based on the Chinese context. However, the outcomes of this paper can be a cleaner approach to innovate collusion regulation of countries that have similar cultures, social systems, economic developments, etc., to China.

Author Contributions

Data curation, Z.P. and J.L.; investigation, Z.P. and J.L.; visualization, Z.P.; writing—original draft, Z.P.; writing—review & editing, Z.P. and K.Y.; conceptualization, K.Y.; funding acquisition, K.Y.; supervision, K.Y.; methodology, J.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by National Natural Science Foundation of China (grant number 71871033).

Data Availability Statement

Data are available from the authors upon request.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Detailed profiles of the experts.

Table A1.

Detailed profiles of the experts.

| Experts | Organization | Role | Career Experience |

|---|---|---|---|

| 1 | University | Associate professor | 17 years |

| 2 | University | Associate professor | 10 years |

| 3 | University | Associate professor | 22 years |

| 4 | University | Lecturer | 6 years |

| 5 | A large construction company | Engineer | 12 years |

| 6 | A large construction company | Assistant engineer | 10 years |

| 7 | A large real estate company | Assistant engineer | 5 years |

| 8 | A large construction company | Assistant engineer | 6 years |

| 9 | A large consultant company | Assistant engineer | 6 years |

| 10 | A large real estate company | Assistant engineer | 7 years |

Table A2.

Personal factor screening for conspirators’ cognitive biases.

Table A2.

Personal factor screening for conspirators’ cognitive biases.

| Cognitive Bias | Factors | Source |

|---|---|---|

| Overconfidence | Salary level | [69] |

| Cognitive dissonance | [53] | |

| Self-attribution bias | [70] | |

| Experience | [71] | |

| Illusion of control | Control force | [72] |

| Power | [73] | |

| Involvement | [74] | |

| Skillset | [75] | |

| Motivation | [76] | |

| Feedback | [77] | |

| Cognitive dissonance | Knowledge | [78] |

| Foreseeable consequence | [79] | |

| Moral standard | [80] |

References

- Asgari, S. Comparative analysis of quantitative bidding methods using agent-based modelling. Civ. Eng. Environ. Syst. 2020, 37, 81–99. [Google Scholar] [CrossRef]

- Doree, A.G. Collusion in the Dutch construction industry: An industrial organization perspective. Build. Res. Informat. 2004, 32, 146–156. [Google Scholar] [CrossRef]

- Cheung, S.O. Are Agreements not to Compete Anticompetition? J. Leg. Aff. Dispute Resolution Eng. Constr. 2016, 8, 05016001. [Google Scholar] [CrossRef]

- Wang, X.W.; Ye, K.H.; Arditi, D. Embodied cost of collusive bidding: Evidence from China’s construction industry. J. Constr. Eng. Manag. 2021, 147, 04021037. [Google Scholar] [CrossRef]

- Huber, M.; Imhof, D.; Ishii, R. Transnational machine learning with screens for flagging bid-rigging cartels. J. R. Stat. Soc. Ser. A-Stat. Soc. 2022. [Google Scholar] [CrossRef]

- Wang, X.W.; Ye, K.H.; Chen, M.K.; Yao, Z.F. A Conceptual Framework for the Inclusion of Exogenous Factors into Collusive Bidding Price Decisions. J. Manag. Eng. 2021, 37, 04021071. [Google Scholar] [CrossRef]

- Barrus, D.; Scott, F. Single Bidders and Tacit Collusion in Highway Procurement Auctions. J. Ind. Econ. 2020, 68, 483–522. [Google Scholar] [CrossRef]

- Kim, K.J.; Kim, K.; Kim, E.W.; Nguyen, T.H.T. Estimating Damages of Bid-Rigging in Design-Build Contracts Based on Simulation Model. KSCE J. Civ. Eng. 2021, 25, 1568–1577. [Google Scholar] [CrossRef]

- Butz, D.A.; Kleit, A.N. Are vertical restraints pro- or anticompetitive? Lessons from Interstate Circuit. J. Law Econ. 2001, 44, 131–159. [Google Scholar] [CrossRef]

- Gilo, D.; Yehezkel, Y. Vertical collusion. Rand J. Econ. 2020, 51, 133–157. [Google Scholar] [CrossRef]

- Lorentziadis, P.L. Optimal bidding in auctions from a game theory perspective. Eur. J. Oper. Res. 2016, 248, 347–371. [Google Scholar] [CrossRef]

- Morselli, C.; Ouellet, M. Network similarity and collusion. Soc. Netw. 2018, 55, 21–30. [Google Scholar] [CrossRef]

- Reeves-Latour, M.; Morselli, C. Bid-rigging networks and state-corporate crime in the construction industry. Soc. Netw. 2017, 51, 158–170. [Google Scholar] [CrossRef]

- Imhof, D.; Wallimann, H. Detecting bid-rigging coalitions in different countries and auction formats. Int. Rev. Law Econ. 2021, 68, 106016. [Google Scholar] [CrossRef]

- Sujarittanonta, P.; Viriyavipart, A. Deterring collusion with a reserve price: An auction experiment. Exp. Econ. 2021, 24, 536–557. [Google Scholar] [CrossRef]

- Ortner, J.; Chassang, S. Making Corruption Harder: Asymmetric Information, Collusion, and Crime. J. Polit. Econ. 2018, 126, 2108–2133. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Y. The effects of perceived fairness and communication on honesty and collusion in a multi-agent setting. Account. Rev. 2008, 83, 1125–1146. [Google Scholar] [CrossRef] [Green Version]

- Signor, R.; Love, P.E.D.; Oliveira, A.; Lopes, A.O.; Oliveira, P.S. Public Infrastructure Procurement: Detecting Collusion in Capped First-Priced Auctions. J. Infrastruct. Syst. 2020, 26, 05020002. [Google Scholar] [CrossRef]

- Garca Rodrguez, M.J.; Rodriguez-Montequin, V.; Ballesteros-Perez, P.; Love, P.E.D.; Signor, R. Collusion detection in public procurement auctions with machine learning algorithms. Autom. Constr. 2022, 133, 104047. [Google Scholar] [CrossRef]

- Hosseini, M.R.; Martek, I.; Banihashemi, S.; Chan, A.P.C.; Darko, A.; Tahmasebi, M. Distinguishing Characteristics of Corruption Risks in Iranian Construction Projects: A Weighted Correlation Network Analysis. Sci. Eng. Ethics 2020, 26, 205–231. [Google Scholar] [CrossRef]

- Wang, X.W.; Ye, K.H.; Zhuang, T.Z.; Liu, R. The influence of collusive information dissemination on bidder’s collusive willingness in urban construction projects. Land 2022, 11, 643. [Google Scholar] [CrossRef]

- Brown, J.; Loosemore, M. Behavioural factors influencing corrupt action in the Australian construction industry. Eng. Constr. Archit. Manag. 2015, 22, 372–389. [Google Scholar] [CrossRef]

- Wang, X.; Arditi, D.; Ye, K. Coupling Effects of Economic, Industrial, and Geographical Factors on Collusive Bidding Decisions. J. Constr. Eng. Manag. 2022, 148, 04022042. [Google Scholar] [CrossRef]

- Cantarelli, P.; Belle, N.; Belardinelli, P. Behavioral Public HR: Experimental Evidence on Cognitive Biases and Debiasing Interventions. Rev. Public Pers. Adm. 2020, 40, 56–81. [Google Scholar] [CrossRef]

- Wegener, D.T.; Petty, R.E. The naive scientist revisited: Naive theories and social judgment. Soc. Cogn. 1998, 16, 1–7. [Google Scholar] [CrossRef]

- Ebenbach, D.H.; Keltner, D. Power, emotion, and judgmental accuracy in social conflict: Motivating the cognitive miser. Basic Appl. Soc. Psychol. 1998, 20, 7–21. [Google Scholar] [CrossRef]

- Francis, K.; Dugas, M.J.; Ricard, N.C. An exploration of Intolerance of Uncertainty and memory bias. J. Behav. Ther. Exp. Psychiatry 2016, 52, 68–74. [Google Scholar] [CrossRef] [Green Version]

- Dror, I.E. Cognitive and Human Factors in Expert Decision Making: Six Fallacies and the Eight Sources of Bias. Anal. Chem. 2020, 92, 7998–8004. [Google Scholar] [CrossRef]

- Libby, R.; Rennekamp, K. Self-Serving Attribution Bias, Overconfidence, and the Issuance of Management Forecasts. J. Account. Res. 2012, 50, 197–231. [Google Scholar] [CrossRef]

- Na, J.; Kim, B.; Sim, J. COO’s overconfidence and the firm’s inventory performance. Prod. Plan. Control 2021, 32, 19–33. [Google Scholar] [CrossRef]

- Wang, D.L.; Sutherland, D.; Ning, L.T.; Wang, Y.D.; Pan, X. Exploring the influence of political connections and managerial overconfidence on r & d intensity in China’s large-scale private sector firms. Technovation 2018, 69, 40–53. [Google Scholar] [CrossRef] [Green Version]

- Chen, G.M.; Kim, K.A.; Nofsinger, J.R.; Rui, O.M. Trading performance, disposition effect, overconfidence, representativeness bias, and experience of emerging market investors. J. Behav. Decis. Mak. 2007, 20, 425–451. [Google Scholar] [CrossRef]

- Hurd, M.D. Anchoring and acquiescence bias in measuring assets in household surveys. J. Risk Uncertain. 1999, 19, 111–136. [Google Scholar] [CrossRef]

- Stapel, D.A.; Reicher, S.D.; Spears, R. Contextual determinants of strategic choice—Some moderators of the availability bias. Eur. J. Soc. Psychol. 1995, 25, 141–158. [Google Scholar] [CrossRef]

- Hribar, P.; Yang, H. CEO Overconfidence and Management Forecasting. Contemp. Account. Res. 2016, 33, 204–227. [Google Scholar] [CrossRef]

- Cooper, J.; Feldman, L.A. Does Cognitive Dissonance Occur in Older Age? A Study of Induced Compliance in a Healthy Elderly Population. Psychol. Aging 2019, 34, 709–713. [Google Scholar] [CrossRef]

- Kaufmann, M.; Goetz, T.; Lipnevich, A.A.; Pekrun, R. Do Positive Illusions of Control Foster Happiness? Emotion 2019, 19, 1014–1022. [Google Scholar] [CrossRef]

- Scopelliti, I.; Min, H.L.; McCormick, E.; Kassam, K.S.; Morewedge, C.K. Individual Differences in Correspondence Bias: Measurement, Consequences, and Correction of Biased Interpersonal Attributions. Manag. Sci. 2018, 64, 1879–1910. [Google Scholar] [CrossRef]

- Ross, L. From the Fundamental Attribution Error to the Truly Fundamental Attribution Error and Beyond: My Research Journey. Perspect. Psychol. Sci. 2018, 13, 750–769. [Google Scholar] [CrossRef]

- Warach, B.; Josephs, L.; Gorman, B.S. Are Cheaters Sexual Hypocrites? Sexual Hypocrisy, the Self-Serving Bias, and Personality Style. Pers. Soc. Psychol. Bull. 2019, 45, 1499–1511. [Google Scholar] [CrossRef]

- Hersch, J.; Shinall, J.B. Imputation Match Bias in Immigrant Wage Convergence. Demography 2018, 55, 1475–1485. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Keusch, T.; Bollen, L.H.H.; Hassink, H.F.D. Self-serving Bias in Annual Report Narratives: An Empirical Analysis of the Impact of Economic Crises. Eur. Account. Rev. 2012, 21, 623–648. [Google Scholar] [CrossRef]

- Ahmed, A.S.; Duellman, S. Managerial Overconfidence and Accounting Conservatism. J. Account. Res. 2013, 51, 1–30. [Google Scholar] [CrossRef]

- Safari Gerayli, M.; Abdoli, M.; Valiyan, H.; Damavandi, A. Managerial overconfidence and internal control weaknesses: Evidence from Iranian firms. Account. Res. J. 2021, 34, 475–487. [Google Scholar] [CrossRef]

- Malmendier, U.; Tate, G. CEO overconfidence and corporate investment. J. Financ. 2005, 60, 2661–2700. [Google Scholar] [CrossRef] [Green Version]

- Xiao, L.; Ye, K.H.; Zhou, J.H.; Ye, X.T.; Tekka, R.S. A social network-based examination on bid riggers’ relationships in the construction industry: A case study of China. Buildings 2021, 11, 363. [Google Scholar] [CrossRef]

- Zhu, J.; Wang, B.; Li, L.; Wang, J. Bidder Network Community Division and Collusion Suspicion Analysis in Chinese Construction Projects. Adv. Civ. Eng. 2020, 2020, 6612848. [Google Scholar] [CrossRef]

- Bowen, P.A.; Edwards, P.J.; Cattell, K. Corruption in the South African construction industry: A thematic analysis of verbatim comments from survey participants. Constr. Manag. Econ. 2012, 30, 885–901. [Google Scholar] [CrossRef]

- Anna, Z.-F.; Martin, S. Decisions with moral content: Collusion. Constr. Manag. Econ. 2000, 18, 101–111. [Google Scholar] [CrossRef] [Green Version]

- Gudmundsson, S.V.; Lechner, C. Cognitive biases, organization, and entrepreneurial firm survival. Eur. Manag. J. 2013, 31, 278–294. [Google Scholar] [CrossRef]

- Li, K.; Cheung, S.O. Unveiling Cognitive Biases in Construction Project Dispute Resolution through the Lenses of Third-Party Neutrals. J. Constr. Eng. Manag. 2019, 145, 04019070. [Google Scholar] [CrossRef]

- Oreg, S.; Bayazit, M. Prone to Bias: Development of a Bias Taxonomy from an Individual Differences Perspective. Rev. Gen. Psychol. 2009, 13, 175–193. [Google Scholar] [CrossRef]

- Stotz, O.; von Nitzsch, R. The Perception of Control and the Level of Overconfidence: Evidence from Analyst Earnings Estimates and Price Targets. J. Behav. Financ. 2005, 6, 121–128. [Google Scholar] [CrossRef]

- Gervais, S.; Odean, T. Learning to Be Overconfident. Rev. Financ. Stud. 2001, 14, 1–27. [Google Scholar] [CrossRef]

- McKinley, W.; Zhao, J.; Rust, K.G. A sociocognitive interpretation of organizational downsizing. Acad. Manag. Rev. 2000, 25, 227–243. [Google Scholar] [CrossRef]

- Langer, E.J.; Roth, J. Heads I win, tails its chance-illusion of control as a function of sequence of outcomes in a purely chance task. J. Personal. Soc. Psychol. 1975, 32, 951–955. [Google Scholar] [CrossRef]

- Lee, D.H. An Alternative Explanation of Consumer Product Returns from the Postpurchase Dissonance and Ecological Marketing Perspectives. Psychol. Mark. 2015, 32, 49–64. [Google Scholar] [CrossRef]

- Aquino, K.; Reed, A. The self-importance of moral identity. J. Pers. Soc. Psychol. 2002, 83, 1423–1440. [Google Scholar] [CrossRef]

- Nahapiet, J.; Ghoshal, S. Social capital, intellectual capital, and the organizational advantage. Acad. Manag. Rev. 1998, 23, 242–266. [Google Scholar] [CrossRef]

- Peng, M.W.; Luo, Y.D. Managerial ties and firm performance in a transition economy: The nature of a micro-macro link. Acad. Manag. J. 2000, 43, 486–501. [Google Scholar] [CrossRef]

- Banerjee, A.V. A simple-model of herd behavior. Q. J. Econ. 1992, 107, 797–817. [Google Scholar] [CrossRef] [Green Version]

- Naylor, R.T. Towards a general theory of profit-driven crimes. Br. J. Criminol. 2003, 43, 81–101. [Google Scholar] [CrossRef]

- Tirole, J. Hierarchies and Bureaucracies: On the Role of Collusion in Organizations. J. Law Econ. Organ. 1986, 2, 181–214. [Google Scholar]

- Zhang, W.; Zhao, W.; Gao, Y.; Xiao, Z. How do managerial ties influence the effectuation and causation of entrepreneurship in China? The role of entrepreneurs’ cognitive bias. Asia Pac. Bus. Rev. 2020, 26, 613–641. [Google Scholar] [CrossRef]

- Lechner, C.; Dowling, M. Firm networks: External relationships as sources for the growth and competitiveness of entrepreneurial firms. Entrep. Reg. Dev. 2003, 15, 1–26. [Google Scholar] [CrossRef]

- Kotey, B.; Meredith, G.G. Relationships among owner/manager personal values, business strategies, and enterprise performance. J. Small Bus. Manag. 1997, 35, 37–64. [Google Scholar]

- Egmond, C.; Jonkers, R.; Kok, G. One size fits all? Policy instruments should fit the segments of target groups. Energy Policy 2006, 34, 3464–3474. [Google Scholar] [CrossRef]

- Yang, H.; Chan, A.P.C.; Yeung, J.F.Y.; Li, Q.M. Concentration Effect on Construction Firms: Tests of Resource Partitioning Theory in Jiangsu Province (China) from 1989 to 2007. J. Constr. Eng. Manag. 2012, 138, 144–153. [Google Scholar] [CrossRef] [Green Version]

- Hambrick, D.C.; Daveni, R.A. Top team deterioration as part of the downward spiral of large corporate bankruptcies. Manag. Sci. 1992, 38, 1445–1466. [Google Scholar] [CrossRef]

- Hirshleifer, D. Investor psychology and asset pricing. J. Financ. 2001, 56, 1533–1597. [Google Scholar] [CrossRef] [Green Version]

- Ringuest, J.L.; Graves, S.B. Overconfidence and Disappointment in Decision-making under Risk: The Triumph of Hope over Experience. Manag. Decis. Econ. 2017, 38, 409–422. [Google Scholar] [CrossRef]

- Biner, P.M.; Angle, S.T.; Park, J.H.; Mellinger, A.E.; Barber, B.C. Need state and the illusion of control. Pers. Soc. Psychol. Bull. 1995, 21, 899–907. [Google Scholar] [CrossRef]

- Lachman, M.E.; Weaver, S.L. The sense of control as a moderator of social class differences in health and well-being. J. Pers. Soc. Psychol. 1998, 74, 763–773. [Google Scholar] [CrossRef] [PubMed]

- Ladouceur, R.; Mayrand, M.; Dussault, R.; Letarte, A.; Tremblay, J. Illusion of control-effects of participation and involvement. J. Psychol. 1984, 117, 47–52. [Google Scholar] [CrossRef]

- Stern, G.S.; Berrenberg, J.L. Skill-set, success outcome, and mania as determinants of the illusion of control. J. Res. Pers. 1979, 13, 206–220. [Google Scholar] [CrossRef]

- Wolfgang, A.K.; Zenker, S.I.; Viscusi, T. Control motivation and the illusion of control in betting on dice. J. Psychol. 1984, 116, 67–72. [Google Scholar] [CrossRef]

- Shanks, D.R.; Dickinson, A. Associative accounts of causality judgment. Psychol. Learn. Motiv-Adv. Res. Theory 1987, 21, 229–261. [Google Scholar]

- Hidalgo-Baz, M.; Martos-Partal, M.; Gonzalez-Benito, O. Attitudes vs. Purchase Behaviors as Experienced Dissonance: The Roles of Knowledge and Consumer Orientations in Organic Market. Front. Psychol. 2017, 8, 8. [Google Scholar] [CrossRef] [Green Version]

- Goethals, G.R.; Cooper, J.; Naficy, A. Role of foreseen, foreseeable, and unforeseeable behavioral consequences in the arousal of cognitive-dissonance. J. Pers. Soc. Psychol. 1979, 37, 1179–1185. [Google Scholar] [CrossRef]

- Yang, N.; Lin, C.C.; Liao, Z.Y.; Xue, M. When Moral Tension Begets Cognitive Dissonance: An Investigation of Responses to Unethical Pro-Organizational Behavior and the Contingent Effect of Construal Level. J. Bus. Ethics 2021. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).