The COVID-19 Sentiment and Office Markets: Evidence from China

Abstract

1. Introduction

2. Literature Review

2.1. Office Market Research

2.2. COVID-19 and Real Estate Markets

2.3. Hypotheses Development

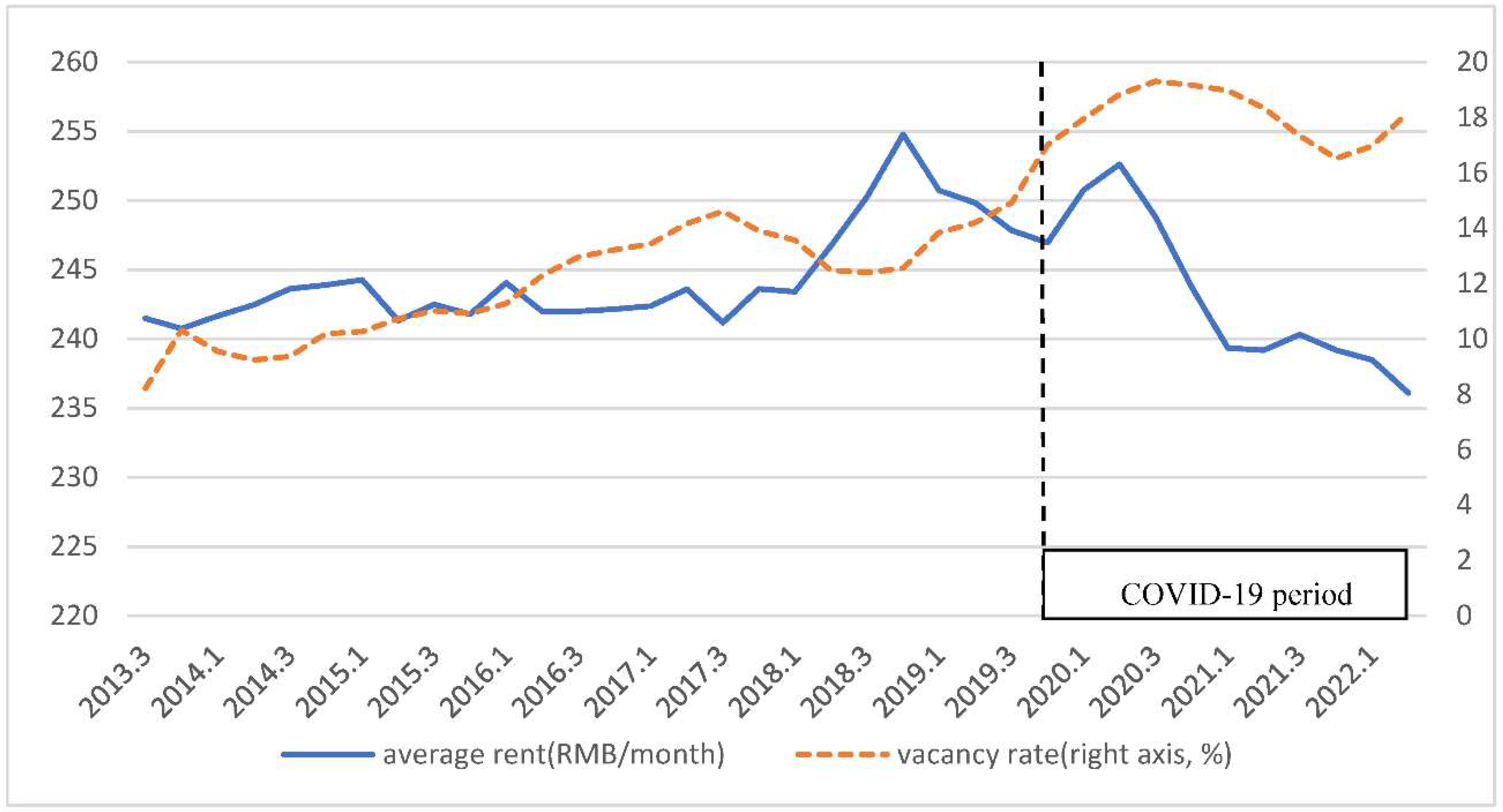

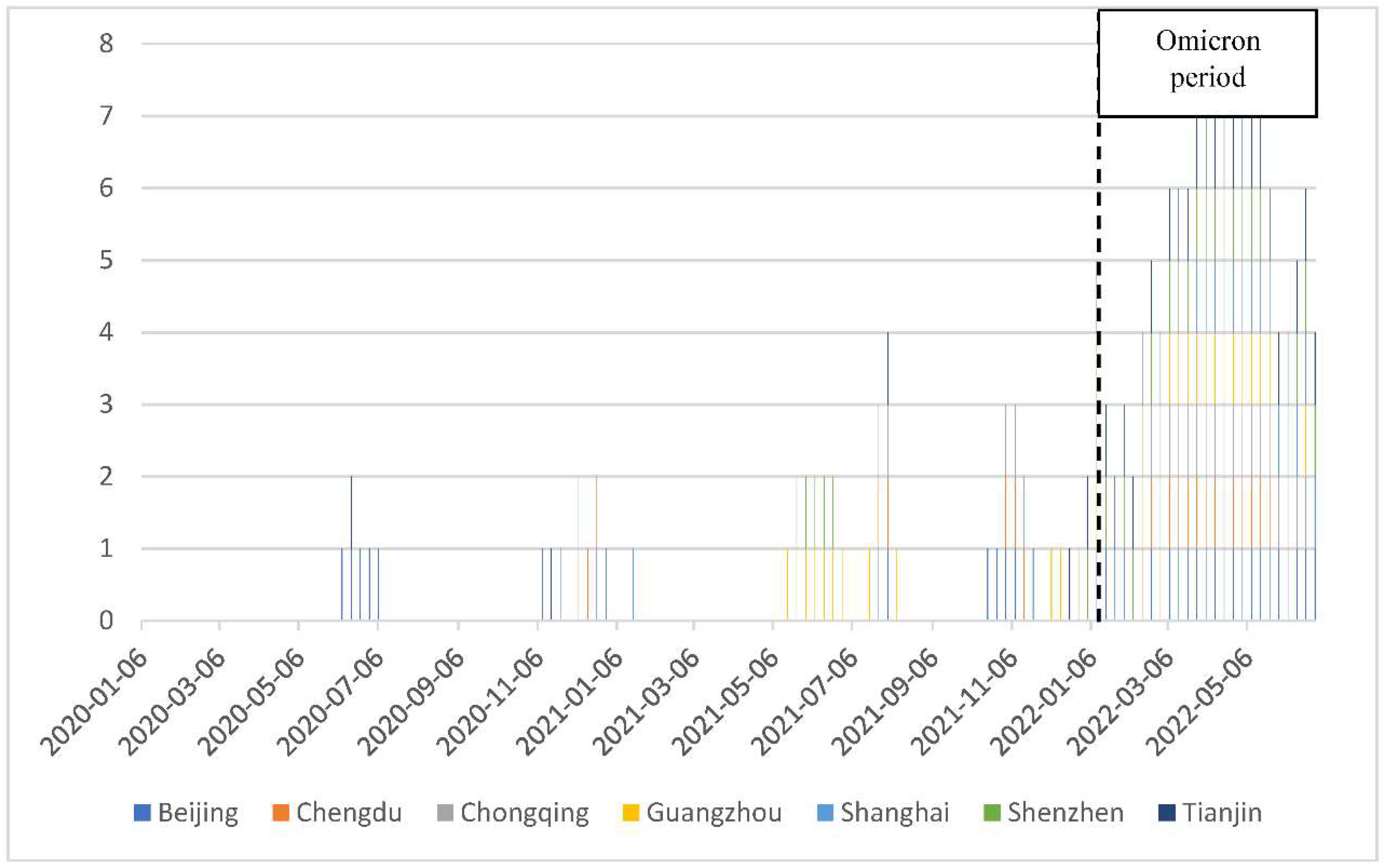

3. Data and Methodology

3.1. Data

3.2. Methodology

4. Results and Discussion

4.1. Rent Long-Term Determinants and Short-Term Adjustment

4.2. Vacancy Rate Changes, Supply Analysis

4.3. Robust Test and Further Analysis

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- CBRE,2022. 2022 China Real Estate Market Outlook. Available online: https://www.cbre.com/insights/reports/2022-china-real-estate-market-outlook (accessed on 18 October 2022).

- Wang, X.; Wang, L.; Zhang, X.; Fan, F. The spatiotemporal evolution of COVID-19 in China and its impact on urban economic resilience. China Econ. Rev. 2022, 74, 101806. [Google Scholar] [CrossRef] [PubMed]

- Davis, M.A.; Ghent, A.C.; Gregory, J.M. The Work-from-Home Technology Boon and Its Consequences; National Bureau of Economic Research: Cambridge, MA, USA, 2021. [Google Scholar]

- Chen, C.; Liu, L.; Zhao, N. Fear sentiment, uncertainty, and bitcoin price dynamics: The case of COVID-19. Emerg. Mark. Financ. Trade 2020, 56, 2298–2309. [Google Scholar] [CrossRef]

- Da, Z.; Engelberg, J.; Gao, P. The Sum of All FEARS Investor Sentiment and Asset Prices. Rev. Financ. Stud. 2015, 28, 1–32. [Google Scholar] [CrossRef]

- Narayan, P.K.; Phan, D.H.B.; Liu, G. COVID-19 lockdowns, stimulus packages, travel bans, and stock returns. Financ. Res. Lett. 2021, 38, 101732. [Google Scholar] [CrossRef] [PubMed]

- He, P.; Sun, Y.; Zhang, Y.; Li, T. COVID–19′s impact on stock prices across different sectors—An event study based on the Chinese stock market. Emerg. Mark. Financ. Trade 2020, 56, 2198–2212. [Google Scholar] [CrossRef]

- Lee, C.L.; Gumulya, N.; Bangura, M. The Role of Mandatory Building Efficiency Disclosure on Green Building Price Premium: Evidence from Australia. Buildings 2022, 12, 297. [Google Scholar] [CrossRef]

- Tetlock, P.C. Giving Content to Investor Sentiment: The Role of Media in the Stock Market. J. Financ. 2007, 62, 1139–1168. [Google Scholar] [CrossRef]

- Lee, C.L.; Stevenson, S.; Cho, H. Listed real estate futures trading, market efficiency, and direct real estate linkages: International evidence. J. Int. Money Financ. 2022, 127, 102693. [Google Scholar] [CrossRef]

- Allan, R.; Liusman, E.; Lu, T.; Tsang, D. The COVID-19 Pandemic and Commercial Property Rent Dynamics. J. Risk Financ. Manag. 2021, 14, 360. [Google Scholar] [CrossRef]

- Hoesli, M.; Malle, R. Commercial real estate prices and COVID-19. J. Eur. Real Estate Res. 2021, 15, 295–306. [Google Scholar] [CrossRef]

- Wheaton, W.C.; Torto, R.G. Vacancy rates and the future of office rents. Real Estate Econ. 1988, 16, 430–436. [Google Scholar] [CrossRef]

- Sanderson, B.; Farrelly, K.; Thoday, C. Natural vacancy rates in global office markets. J. Prop. Investig. Financ. 2006, 24, 490–520. [Google Scholar] [CrossRef]

- McCartney, J. Short and long-run rent adjustment in the Dublin office market. J. Prop. Res. 2012, 29, 201–226. [Google Scholar] [CrossRef]

- Bruneau, C.; Cherfouh, S. Long-run equilibrium for the Greater Paris office market and short-run adjustments. J. Prop. Res. 2015, 32, 301–323. [Google Scholar] [CrossRef]

- Hendershott, P.H.; Lizieri, C.M.; MacGregor, B.D. Asymmetric adjustment in the city of London office market. J. Real Estate Financ. Econ. 2010, 41, 80–101. [Google Scholar] [CrossRef]

- Ho, D.; Newell, G.; Walker, A. The importance of property-specific attributes in assessing CBD office building quality. J. Prop. Investig. Financ. 2005, 23, 424–444. [Google Scholar] [CrossRef]

- Newell, G.; MacFarlane, J.; Walker, R. Assessing energy rating premiums in the performance of green office buildings in Aus-tralia. J. Prop. Investig. Financ. 2014, 32, 352–370. [Google Scholar] [CrossRef]

- Onishi, J.; Deng, Y.; Shimizu, C. Green Premium in the Tokyo Office Rent Market. Sustainability 2021, 13, 12227. [Google Scholar] [CrossRef]

- Chau, K.W.; Wong, S.K. Information asymmetry and the rent and vacancy rate dynamics in the office market. J. Real Estate Financ. Econ. 2016, 53, 162–183. [Google Scholar] [CrossRef]

- Nowak, K.; Gluszak, M.; Belniak, S. Dynamics and asymmetric rent adjustments in the office market in warsaw. Int. J. Strat. Prop. Manag. 2020, 24, 428–440. [Google Scholar] [CrossRef]

- Newell, G. The inflation-hedging characteristics of Australian commercial property: 1984–1995. J. Prop. Financ. 1996, 7, 6–20. [Google Scholar] [CrossRef]

- Hoesli, M.; Lizieri, C.; MacGregor, B. The inflation hedging characteristics of US and UK investments: A multi-factor error cor-rection approach. J. Real Estate Financ. Econ. 2008, 36, 183–206. [Google Scholar] [CrossRef]

- van der Vlist, A.J.; Francke, M.K.; Schoenmaker, D.A.J. Agglomeration Economies and Capitalization Rates: Evidence from the Dutch Real Estate Office Market. J. Real Estate Financ. Econ. 2021, 1–23. [Google Scholar] [CrossRef]

- Crosby, N.; Devaney, S.; Lizieri, C.; Mansley, N. Modelling sustainable rents for estimation of long-term or fundamental values of commercial real estate. J. Prop. Res. 2021, 39, 30–55. [Google Scholar] [CrossRef]

- Hordijk, A.; De Kroon, H.; Theebe, M. Long-run return series for the European continent: 25 years of Dutch commercial real estate. J. Real Estate Portf. Manag. 2004, 10, 217–230. [Google Scholar]

- Wang, S.; Hartzell, D. Real Estate Return in Hong Kong and its Determinants: A Dynamic Gordon Growth Model Analysis. Int. Real Estate Rev. 2021, 24, 113–138. [Google Scholar] [CrossRef]

- An, X.; Deng, Y.; Fisher, J.D.; Hu, M.R. Commercial Real Estate Rental Index: A Dynamic Panel Data Model Estimation. Real Estate Econ. 2015, 44, 378–410. [Google Scholar] [CrossRef]

- Lee, C.L.; Lee, M.L. Do European real estate stocks hedge inflation? Evidence from developed and emerging markets. Int. J. Strateg. Prop. Manag. 2014, 18, 178–197. [Google Scholar] [CrossRef]

- Khan, M.A.; Wang, C.C.; Lee, C.L. A framework for developing green building rating tools based on Pakistan’s local context. Buildings 2021, 11, 202. [Google Scholar] [CrossRef]

- Wang, J.; Lee, C.L.; Shirowzhan, S. Macro-Impacts of Air Quality on Property Values in China—A Meta-Regression Analysis of the Literature. Buildings 2021, 11, 48. [Google Scholar] [CrossRef]

- Wang, J.; Lee, C.L. The value of air quality in housing markets: A comparative study of housing sale and rental markets in China. Energy Policy 2022, 160, 112601. [Google Scholar] [CrossRef]

- Hui, E.C.M.; Chan, K.K.K. Foreign direct investment in China’s real estate market. Habitat Int. 2014, 43, 231–239. [Google Scholar] [CrossRef]

- Zhang, J.; Lee, C.L.; Chan, N. The Asymmetric Effect of Institutional Quality on Chinese Outward Real Estate Investment. Int. J. Strat. Prop. Manag. 2019, 23, 435–449. [Google Scholar] [CrossRef]

- Ke, Q.; White, M. An econometric analysis of Shanghai office rents. J. Prop. Investig. Financ. 2009, 27, 120–139. [Google Scholar] [CrossRef]

- White, M.; Ke, Q. Investigating the dynamics of, and interactions between, Shanghai office submarkets. J. Prop. Res. 2014, 31, 26–44. [Google Scholar] [CrossRef]

- Ke, Q.; White, M. A Tale of Two Chinese Cities: The Dynamics of Beijing and Shanghai Office Markets. J. Real Estate Portf. Manag. 2013, 19, 31–47. [Google Scholar] [CrossRef]

- Ke, Q.; Sieracki, K. Market maturity: China commercial real estate market. J. Prop. Investig. Financ. 2015, 33, 4–18. [Google Scholar] [CrossRef]

- Ke, Q.; Wang, W. The factors that determine shopping centre rent in Wuhan, China. J. Prop. Investig. Financ. 2016, 34, 172–185. [Google Scholar] [CrossRef]

- Ling, D.C.; Wang, C.; Zhou, T. A first look at the impact of COVID-19 on commercial real estate prices: Asset-level evidence. Rev. Asset Pricing Stud. 2020, 10, 669–704. [Google Scholar] [CrossRef]

- Milcheva, S. Volatility and the Cross-Section of Real Estate Equity Returns during Covid-19. J. Real Estate Financ. Econ. 2021, 65, 293–320. [Google Scholar] [CrossRef]

- Rosenthal, S.S.; Strange, W.C.; Urrego, J.A. JUE insight: Are city centers losing their appeal? Commercial real estate, urban spatial structure, and COVID-19. J. Urban Econ. 2022, 127, 103381. [Google Scholar] [CrossRef]

- Gupta, A.; Mittal, V.; Peeters, J.; Van Nieuwerburgh, S. Flattening the curve: Pandemic-Induced revaluation of urban real estate. J. Financ. Econ. 2021, 146, 594–636. [Google Scholar] [CrossRef]

- D’Lima, W.; Lopez, L.A.; Pradhan, A. COVID-19 and housing market effects: Evidence from U.S. shutdown orders. Real Estate Econ. 2021, 50, 303–339. [Google Scholar] [CrossRef]

- Liu, S.; Su, Y. The impact of the COVID-19 pandemic on the demand for density: Evidence from the US housing market. Eco-Nomics Lett. 2021, 207, 110010. [Google Scholar] [CrossRef]

- Liu, H.; Wang, Y.; He, D.; Wang, C. Short term response of Chinese stock markets to the outbreak of COVID-19. Appl. Econ. 2020, 52, 5859–5872. [Google Scholar] [CrossRef]

- Huang, N.; Pang, J.; Yang, Y. JUE Insight: COVID-19 and Household Preference for Urban Density in China. J. Urban Econ. 2022, 103487. [Google Scholar] [CrossRef] [PubMed]

- Shen, H.; Fu, M.; Pan, H.; Yu, Z.; Chen, Y. The impact of the COVID-19 pandemic on firm performance. Emerging Markets Finance and Trade 2020, 56, 2213–2230. [Google Scholar] [CrossRef]

- Li, L.; Wan, L. Understanding the Spatial Impact of COVID-19: New Insights from Beijing after One Year into Post-Lockdown Recovery. SSRN 2021, 3908277. [Google Scholar] [CrossRef]

- SCMP. What does China’s move to relax hukou residency curbs mean for the property sector? 2022. South China Morning Post. Available online: https://www.scmp.com/property/hong-kong-china/article/3005615/what-does-chinas-move-relax-residency-curbs-mean-property (accessed on 28 November 2022).

- State Council. The notice to further support the relief and development of small and medium-sized enterprises and individual industrial and commercial housing rent in 2022 2022. In State Council of China. Available online: http://www.gov.cn/zhengce/zhengceku/2022-10/12/content_5717962.htm (accessed on 19 October 2022).

- Phan DH, B.; Narayan, P.K. Country responses and the reaction of the stock market to COVID-19—A preliminary exposition. Emerg. Mark. Financ. Trade 2020, 56, 2138–2150. [Google Scholar] [CrossRef]

- Wan, D.; Xue, R.; Linnenluecke, M.; Tian, J.; Shan, Y. The impact of investor attention during COVID-19 on investment in clean energy versus fossil fuel firms. Financ. Res. Lett. 2021, 43, 101955. [Google Scholar] [CrossRef]

- Baum, A.E.; Hartzell, D. Real Estate Investment: Strategies, Structures, Decisions; Wiley: Hoboken, NJ, USA, 2021. [Google Scholar]

- Engsted, T.; Pedersen, T.Q. Predicting returns and rent growth in the housing market using the rent-price ratio: Evidence from the OECD countries. J. Int. Money Financ. 2015, 53, 257–275. [Google Scholar] [CrossRef]

- Brounen, D.; Jennen, M. Asymmetric properties of office rent adjustment. J. Real Estate Financ. Econ. 2009, 39, 336–358. [Google Scholar] [CrossRef]

- Brounen, D.; Jennen, M. Local office rent dynamics. J. Real Estate Financ. Econ. 2009, 39, 385. [Google Scholar] [CrossRef]

- Qian, X.; Qiu, S.; Zhang, G. The impact of COVID-19 on housing price: Evidence from China. Financ. Res. Lett. 2021, 43, 101944. [Google Scholar] [CrossRef]

- Al-Masum, A.; Lee, C.L. Modelling housing prices and market fundamentals: Evidence from the Sydney housing market. Int. J. Hous. Mark. Anal. 2019, 12, 746–762. [Google Scholar] [CrossRef]

- Lee, C.L.; Stevenson, S.; Lee, M.L. Low-frequency volatility of real estate securities and macroeconomic risk. Account. Financ. 2018, 58, 311–342. [Google Scholar] [CrossRef]

- Liu, Y.S.; Su, C.W. The relationship between the real estate and stock markets of China: Evidence from a nonlinear model. Appl. Financ. Econ. 2010, 20, 1741–1749. [Google Scholar] [CrossRef]

- Lai, R.N.; Van Order, R.A. A Tale of Two Countries: Comparing the US and Chinese Housing Markets. J. Real Estate Financ. Econ. 2020, 61, 505–547. [Google Scholar] [CrossRef]

- Campbell, S.D.; Davis, M.A.; Gallin, J.; Martin, R.F. What moves housing markets: A variance decomposition of the rent–price ratio. J. Urban Econ. 2009, 66, 90–102. [Google Scholar] [CrossRef]

- Bangura, M.; Lee, C.L. The determinants of homeownership affordability in Greater Sydney: Evidence from a submarket analysis. Hous. Stud. 2021, 1–27. [Google Scholar] [CrossRef]

- Dunse, N.; Jones, C. The existence of office submarkets in cities. J. Prop. Res. 2002, 19, 159–182. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | Definition and Function | Resource/ Built Method | |

|---|---|---|---|

| Office | rent | A-class office average rent, the key indicator of office market performance | Savills China |

| vacancy rate | Proportion of vacancy A class buildings in the office buildings stock of a city | ||

| stock | Total available buildings within a city in each period, a measure of office market scale. | ||

| Economic | GDP | Gross domestic product, it is the key variables to measure economic prosperity of an economic, a widely used office market demand variable. | National Bureau of Statistics of China |

| Stock price | Shanghai Composite (SSEC), we use stock price as an demand variable for office space in robust test | Investing.com | |

| Interest rate | We use 10-year China government bond yield as a measure of risk-free rate; it might have influence on office rent | ||

| COVID | COVID sentiment | Measure of public concern of COVID-19, a sentiment index based on Baidu search queries on COVID-19-related keyword | Built from Baidu Search data |

| Variables | Mean | Std. Dev. | Min | Max | Observations |

|---|---|---|---|---|---|

| Rent (RMB/m2/month) | 187.4 | 86.21 | 81.70 | 369 | 252 |

| GDP (100 million RMB) | 5654 | 2040 | 2238 | 11250 | 252 |

| Stock (104 m2) | 590.4 | 447.7 | 61.40 | 1590 | 252 |

| Vacancy | 0.205 | 0.128 | 0.0350 | 0.524 | 252 |

| COVID-19 Exposure | 0.0565 | 0.185 | 0 | 1 | 252 |

| Housing Rent (RMB/m2/month) | 65.83 | 29.59 | 25.17 | 121.30 | 252 |

| Housing Price (RMB/m2) | 34,978.84 | 19,719.92 | 7280.54 | 78,588.07 | 252 |

| Tier 1 Cities | Tier 2 Cities | ||||||

|---|---|---|---|---|---|---|---|

| Beijing | Shanghai | Guangzhou | Shenzhen | Tianjin | Chengdu | Chongqing | |

| Yearly Rent Increase Rate | 1.05 | 1.27 | 0.62 | −1.99 | −2.66 | −0.67 | −1.55 |

| Average Vacancy Rate | 8.38 | 11.11 | 9.49 | 15.60 | 32.64 | 28.28 | 37.93 |

| Yearly Stock Increase Rate | 5.41 | 2.03 | 8.07 | 11.24 | 12.20 | 9.38 | 15.19 |

| Yearly GDP Increase Rate | 9.10 | 8.36 | 7.48 | 9.56 | 0.86 | 9.88 | 10.07 |

| COVID-19 Exposure | 5.79 | 3.47 | 4.40 | 4.17 | 5.09 | 3.94 | 3.47 |

| Housing Rent Increase Rate | 4.24 | 6.27 | 0.37 | 4.77 | −0.11 | 2.79 | 1.57 |

| Housing Price Increase Rate | 9.26 | 12.90 | 13.21 | 25.71 | 4.33 | 15.12 | 10.53 |

| Dependent Variable: lnRent | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| All Cities | Tier 1 Cities | Tier 2 Cities | All Cities | Tier 1 Cities | Tier 2 Cities | |

| lnGDP | 0.117 *** | 0.329 *** | 0.052 | 0.102 *** | 0.316 *** | 0.016 |

| (0.022) | (0.029) | (0.037) | (0.022) | (0.028) | (0.037) | |

| lnStock | −0.136 *** | −0.190 *** | −0.122 *** | −0.126 *** | −0.178 *** | −0.111 *** |

| (0.019) | (0.034) | (0.021) | (0.019) | (0.033) | (0.020) | |

| Vacancy | −0.000 | −0.937 *** | 0.163 * | −0.032 | −0.899 *** | 0.169 * |

| (0.062) | (0.090) | (0.092) | (0.061) | (0.088) | (0.087) | |

| COVID | −0.083 *** | −0.037 * | −0.100 *** | 0.149 ** | 0.198 *** | 0.570 *** |

| (0.021) | (0.022) | (0.030) | (0.062) | (0.075) | (0.191) | |

| COVID*vacancy | −1.026 *** | −1.394 *** | −2.240 *** | |||

| (0.258) | (0.426) | (0.629) | ||||

| Constant | 5.744 *** | 4.310 *** | 4.829 *** | 5.806 *** | 4.338 *** | 5.057 *** |

| (0.155) | (0.185) | (0.256) | (0.151) | (0.179) | (0.251) | |

| City fixed | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 252 | 144 | 108 | 252 | 144 | 108 |

| R-squared | 0.985 | 0.979 | 0.905 | 0.986 | 0.980 | 0.915 |

| Dependent Variable: | ||||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| All_City | Tier1_City | Tier2_City | All_City | Tier1_City | Tier2_City | |

| 0.041 | −0.022 | 0.031 | 0.043 | −0.026 | 0.032 | |

| (0.034) | (0.067) | (0.042) | (0.034) | (0.068) | (0.042) | |

| −0.019 | −0.021 | −0.006 | −0.019 | −0.021 | −0.008 | |

| (0.017) | (0.025) | (0.024) | (0.017) | (0.025) | (0.024) | |

| −0.097 | −0.412 *** | 0.031 | −0.099 | −0.422 *** | 0.031 | |

| (0.067) | (0.111) | (0.087) | (0.067) | (0.111) | (0.087) | |

| −0.014 | −0.014 | −0.015 | −0.008 | −0.001 | −0.002 | |

| (0.010) | (0.011) | (0.019) | (0.029) | (0.037) | (0.145) | |

| −0.027 | −0.083 | −0.053 | ||||

| (0.122) | (0.201) | (0.462) | ||||

| ECM (−1) | −0.079 *** | −0.122 *** | −0.111 ** | −0.084 *** | −0.126 *** | −0.130 *** |

| (0.024) | (0.042) | (0.044) | (0.025) | (0.044) | (0.046) | |

| Constant | 0.003 | 0.005 | −0.001 | 0.003 | 0.005 | −0.001 |

| (0.004) | (0.003) | (0.004) | (0.004) | (0.003) | (0.004) | |

| Observations | 245 | 140 | 105 | 245 | 140 | 105 |

| R-squared | 0.088 | 0.188 | 0.079 | 0.092 | 0.188 | 0.093 |

| city fixed | Yes | Yes | Yes | Yes | Yes | Yes |

| Dependent Variable: | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| All Cities | Tier 1 Cities | Tier 2 Cities | |

| Vacancy(−1) | −0.073 *** | −0.047 * | −0.091 ** |

| (0.021) | (0.026) | (0.035) | |

| −0.019 | −0.005 | −0.027 | |

| (0.016) | (0.019) | (0.027) | |

| 0.174 *** | 0.036 | 0.203 *** | |

| (0.031) | (0.053) | (0.043) | |

| COVID | 0.009 | 0.011 | 0.004 |

| (0.007) | (0.007) | (0.013) | |

| ECM_rent(−1) | 0.051 ** | 0.030 | 0.073 |

| (0.023) | (0.033) | (0.048) | |

| Constant | 0.007 * | 0.006 * | 0.019 * |

| (0.004) | (0.003) | (0.011) | |

| City fixed | Yes | Yes | Yes |

| Observations | 245 | 140 | 105 |

| R-squared | 0.187 | 0.043 | 0.261 |

| Dependent Variable: | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| All Cities | Tier 1 Cities | Tier 2 Cities | |

| Vacancy(−1) | 0.076 * | 0.067 * | 0.078 |

| (0.044) | (0.040) | (0.079) | |

| ECM_rent(−1) | 0.082 * | −0.026 | 0.187 * |

| (0.048) | (0.050) | (0.110) | |

| Constant | 0.007 | 0.007 | 0.002 |

| (0.008) | (0.005) | (0.024) | |

| City fixed | Yes | Yes | Yes |

| Observations | 245 | 140 | 105 |

| R-squared | 0.069 | 0.112 | 0.046 |

| Dependent Variable: lnrent | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| SSEC | SSEC Crossterm | Interest | Interest Crossterm | |

| lnShanghai Index | 0.050 ** | 0.047 ** | ||

| (0.025) | (0.024) | |||

| Risk free rate | −2.254 ** | −2.118 ** | ||

| (1.025) | (0.984) | |||

| lnStock | −0.088 *** | −0.085 *** | −0.092 *** | −0.089 *** |

| (0.018) | (0.017) | (0.018) | (0.017) | |

| vacancy | −0.050 | −0.082 | −0.057 | −0.088 |

| (0.065) | (0.063) | (0.065) | (0.063) | |

| COVID | −0.067 *** | 0.208 *** | −0.074 *** | 0.199 *** |

| (0.022) | (0.063) | (0.022) | (0.063) | |

| Covid×vacancy | −1.226 *** | −1.219 *** | ||

| (0.263) | (0.263) | |||

| Constant | 6.056 *** | 6.048 *** | 6.560 *** | 6.527 *** |

| (0.181) | (0.174) | (0.147) | (0.141) | |

| City fixed | Yes | Yes | Yes | Yes |

| Observations | 252 | 252 | 252 | 252 |

| R-squared | 0.983 | 0.985 | 0.983 | 0.985 |

| Dependent Variable: | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| All_City | Tier1_City | Tier2_City | |

| 0.198 ** | 0.577 *** | 0.034 | |

| −0.089 | −0.171 | −0.087 | |

| GDP | 2.744 *** | 3.114 *** | 2.477 *** |

| −0.19 | −0.285 | −0.229 | |

| COVID | −0.077 ** | −0.051 | −0.129 *** |

| −0.031 | −0.044 | −0.041 | |

| Constant | −1.326 *** | −2.144 *** | −1.717 *** |

| −0.415 | −0.622 | −0.48 | |

| City fixed | Yes | Yes | Yes |

| Observations | 245 | 140 | 105 |

| R-squared | 0.979 | 0.887 | 0.932 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, S.; Lee, C.L.; Song, Y. The COVID-19 Sentiment and Office Markets: Evidence from China. Buildings 2022, 12, 2100. https://doi.org/10.3390/buildings12122100

Wang S, Lee CL, Song Y. The COVID-19 Sentiment and Office Markets: Evidence from China. Buildings. 2022; 12(12):2100. https://doi.org/10.3390/buildings12122100

Chicago/Turabian StyleWang, Shizhen, Chyi Lin Lee, and Yan Song. 2022. "The COVID-19 Sentiment and Office Markets: Evidence from China" Buildings 12, no. 12: 2100. https://doi.org/10.3390/buildings12122100

APA StyleWang, S., Lee, C. L., & Song, Y. (2022). The COVID-19 Sentiment and Office Markets: Evidence from China. Buildings, 12(12), 2100. https://doi.org/10.3390/buildings12122100