Quantitative Analysis of the Accident Prevention Costs in Korean Construction Projects

Abstract

:1. Introduction

- Occupational safety and health management funds (OSHMF): Article 72 of the Occupational Safety and Health Act (OSHA) administered by the Ministry of Employment and Labor (MOEL) [29].

- Safety management expense (SME): Article 63 of the Construction Technology Promotion Act (CTPA) administered by the Ministry of Land, Infrastructure and Transport (MOLIT) [30].

2. Literature Review

2.1. Quantitative Framework Development

2.2. Prevention Cost Effectiveness Analysis

3. Materials and Methods

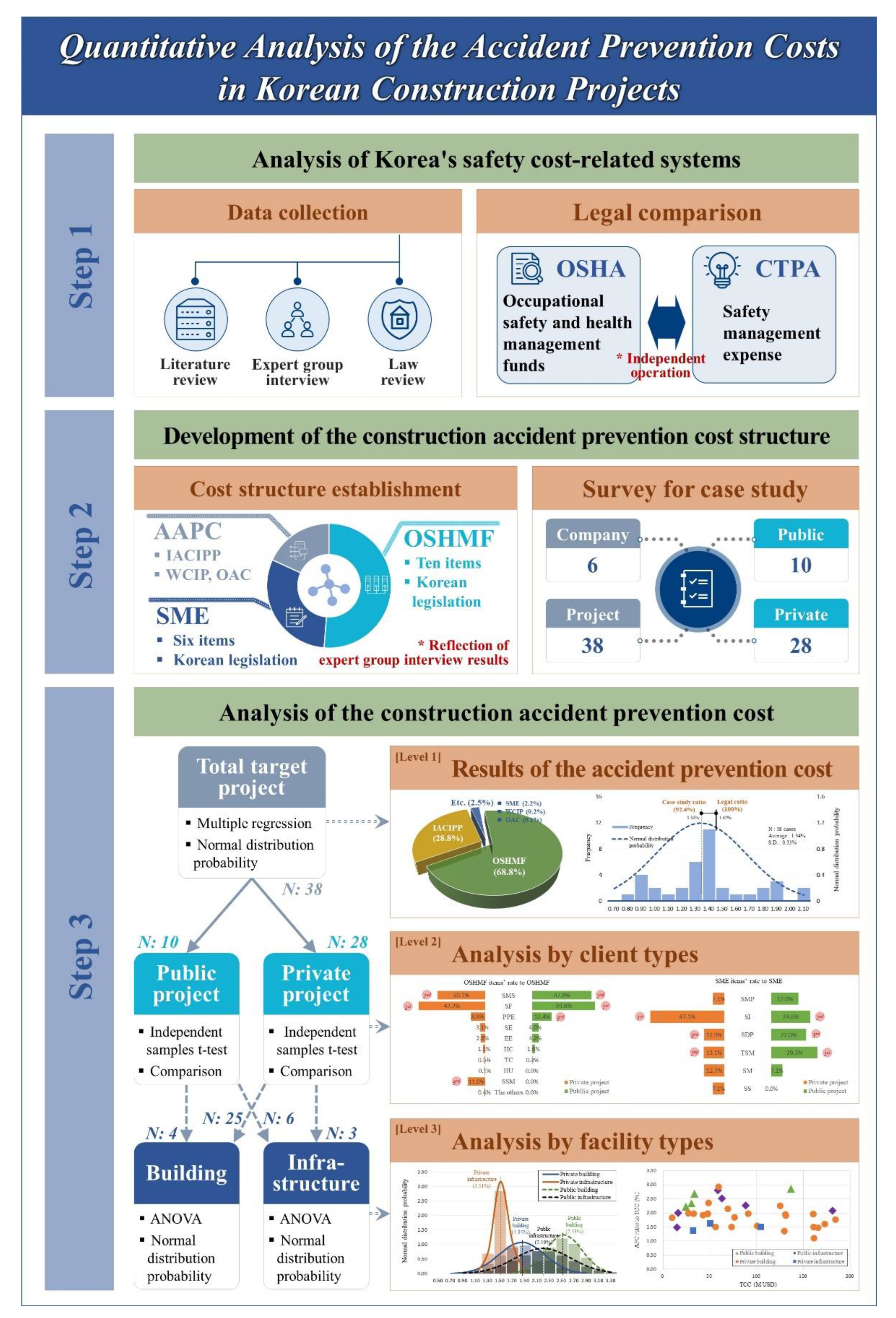

3.1. Analysis of Korea’s Safety Cost-Related System

3.2. Development of Construction APC Structure

3.3. Analysis of Construction Accident Prevention Cost

4. Results and Discussion

4.1. Results of the Accident Prevention Cost

4.2. Analysis by Client Types

4.3. Analysis by Facility Types

5. Conclusions

- An APC quantification analysis structure that considers the characteristics of the Korean construction industry was derived based on a literature review, an expert group interview, and a law review.

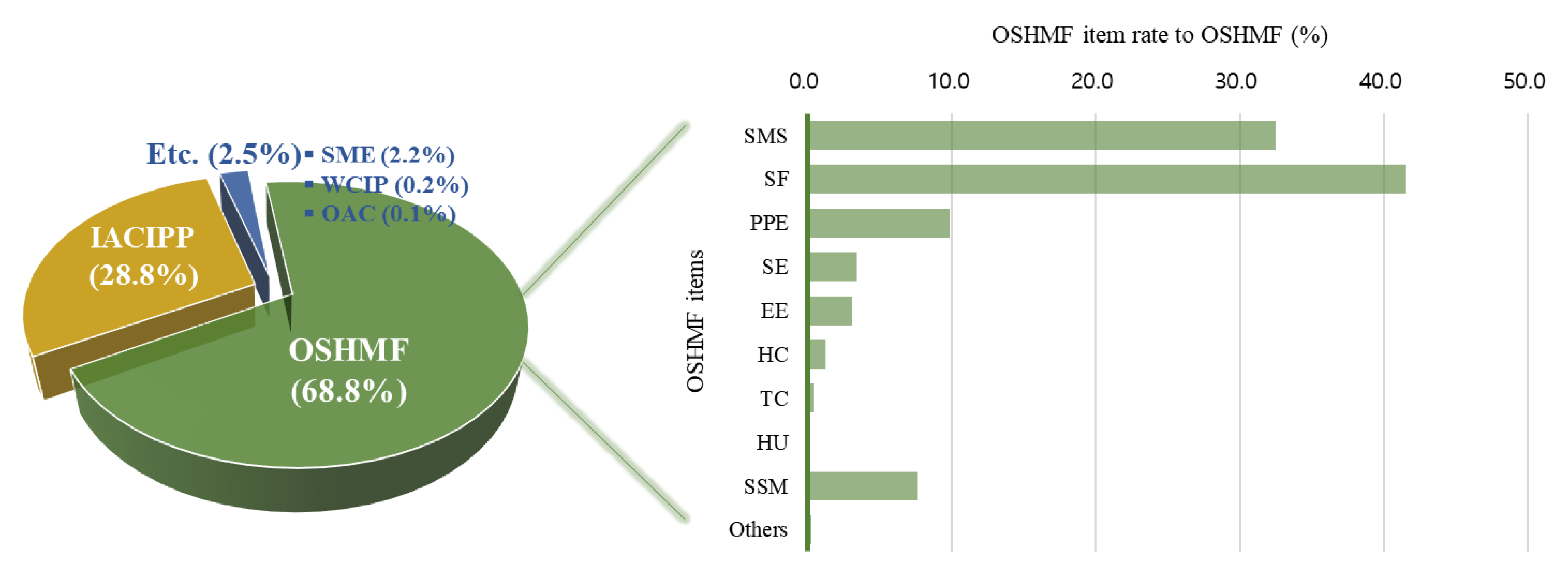

- The APC structure of the Korean construction industry comprised the following five items: OSHMF, SME, IACIPP, WCIP, and OAC.

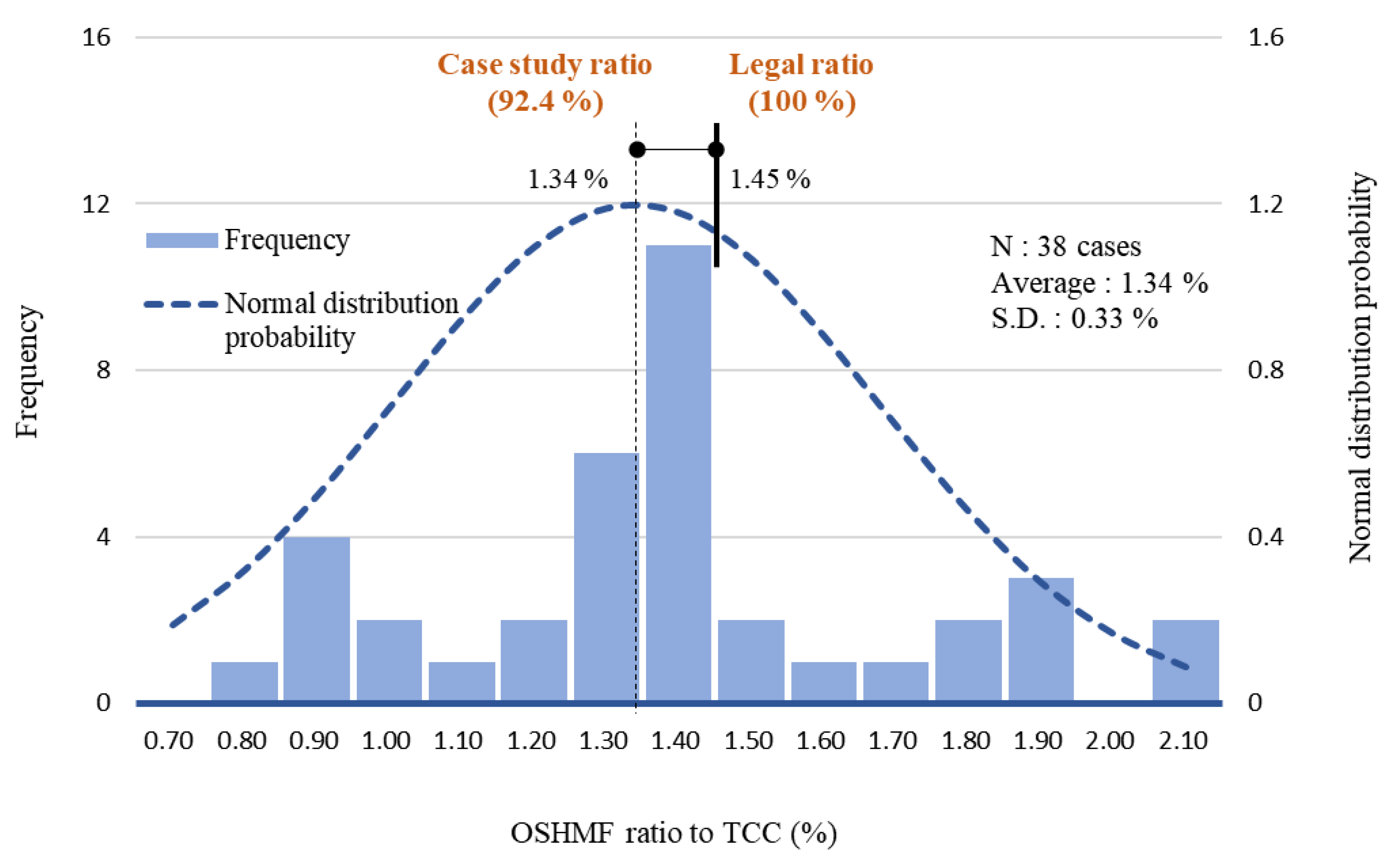

- When a survey was conducted for a case study, the questionnaires of 38 construction projects were recovered, excluding missing data.

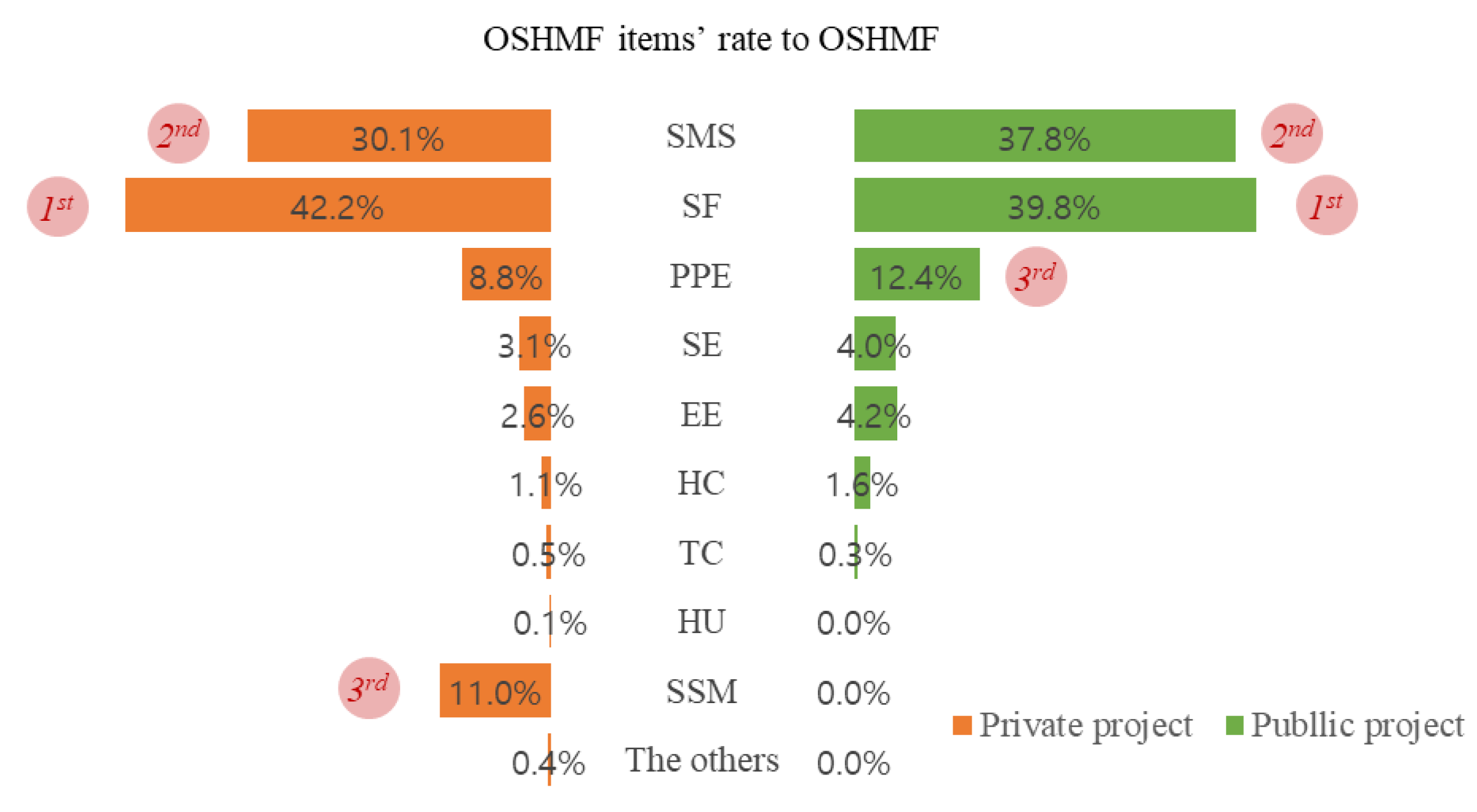

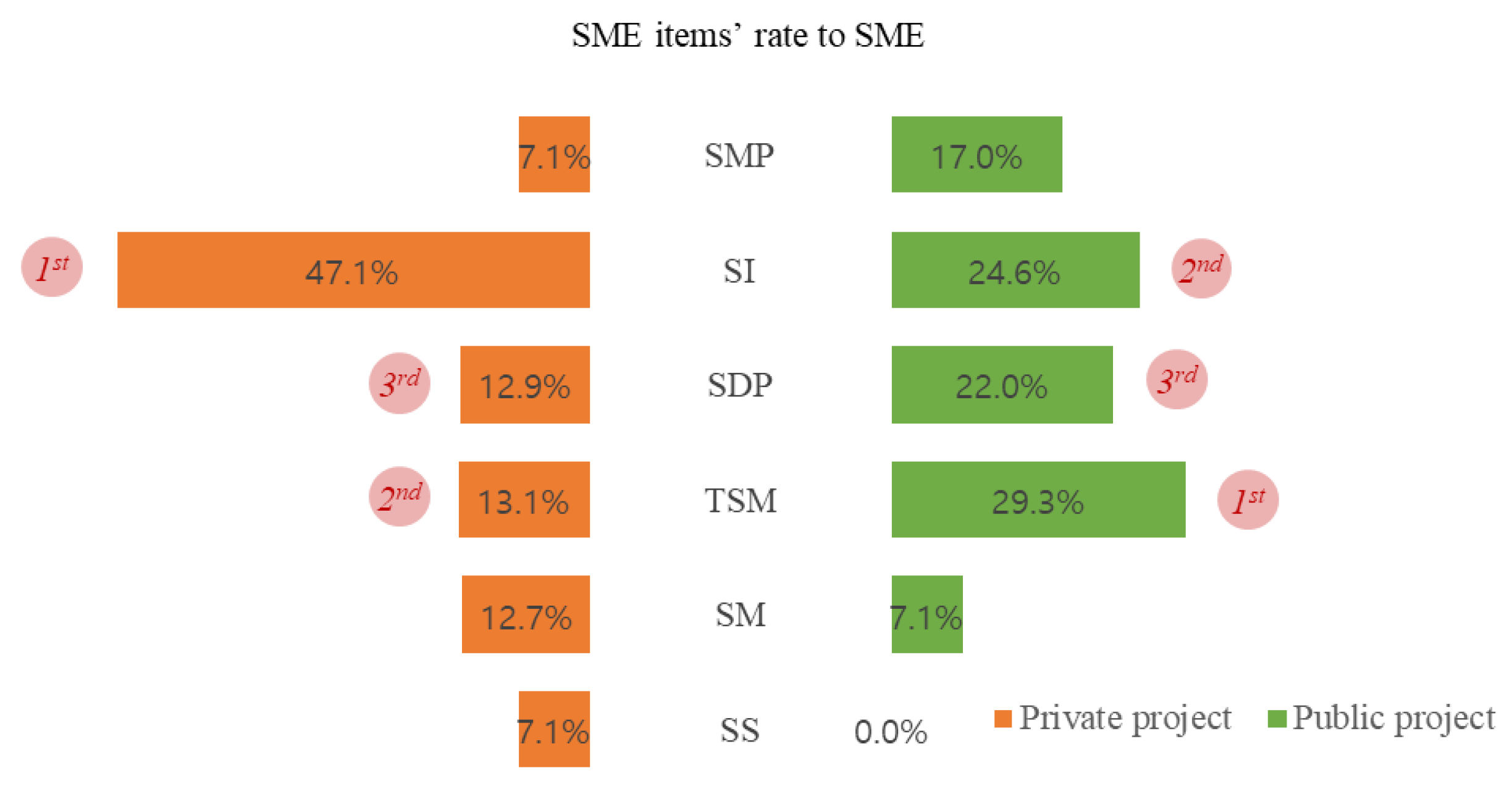

- For the 38 target projects, the average ratio values of APC to TCC were calculated to be 1.95%. Among the detailed items of APC, OSHMF exhibited the largest proportion (68.8%), followed by IACIPP (28.8%). When multiple regression was performed, the relationship of APC (USD) = 5,531,443 (USD) + 49.40 × OSHMF (USD) + 54.50 × IACIPP (USD) was derived.

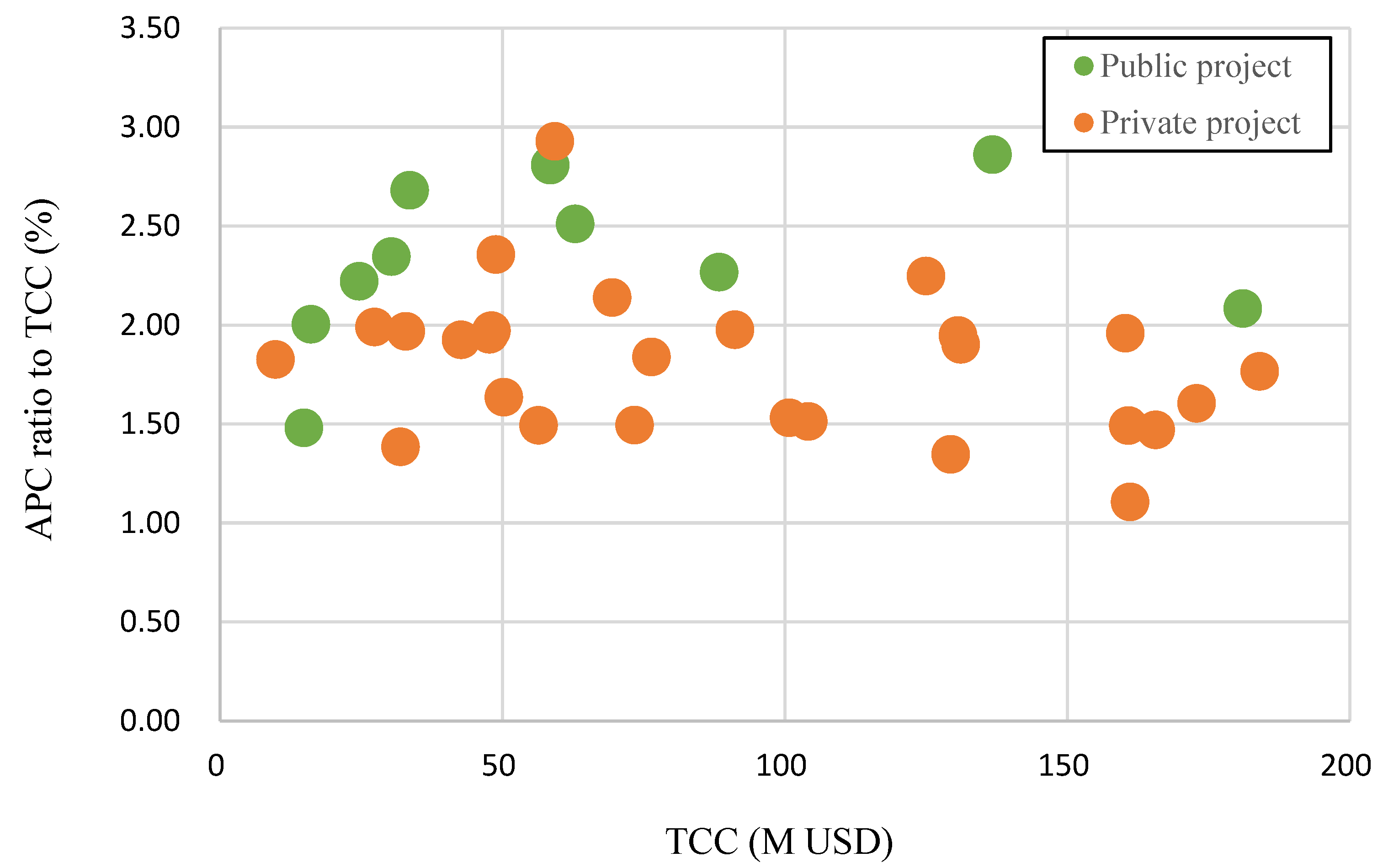

- When the independent samples t-test was conducted on public and private projects according to client types, a significant difference between the average values of the two groups was observed because two-tailed significance values were calculated to be 0.001. It was found that the average APC of public projects was approximately 128.7% higher than that of private projects.

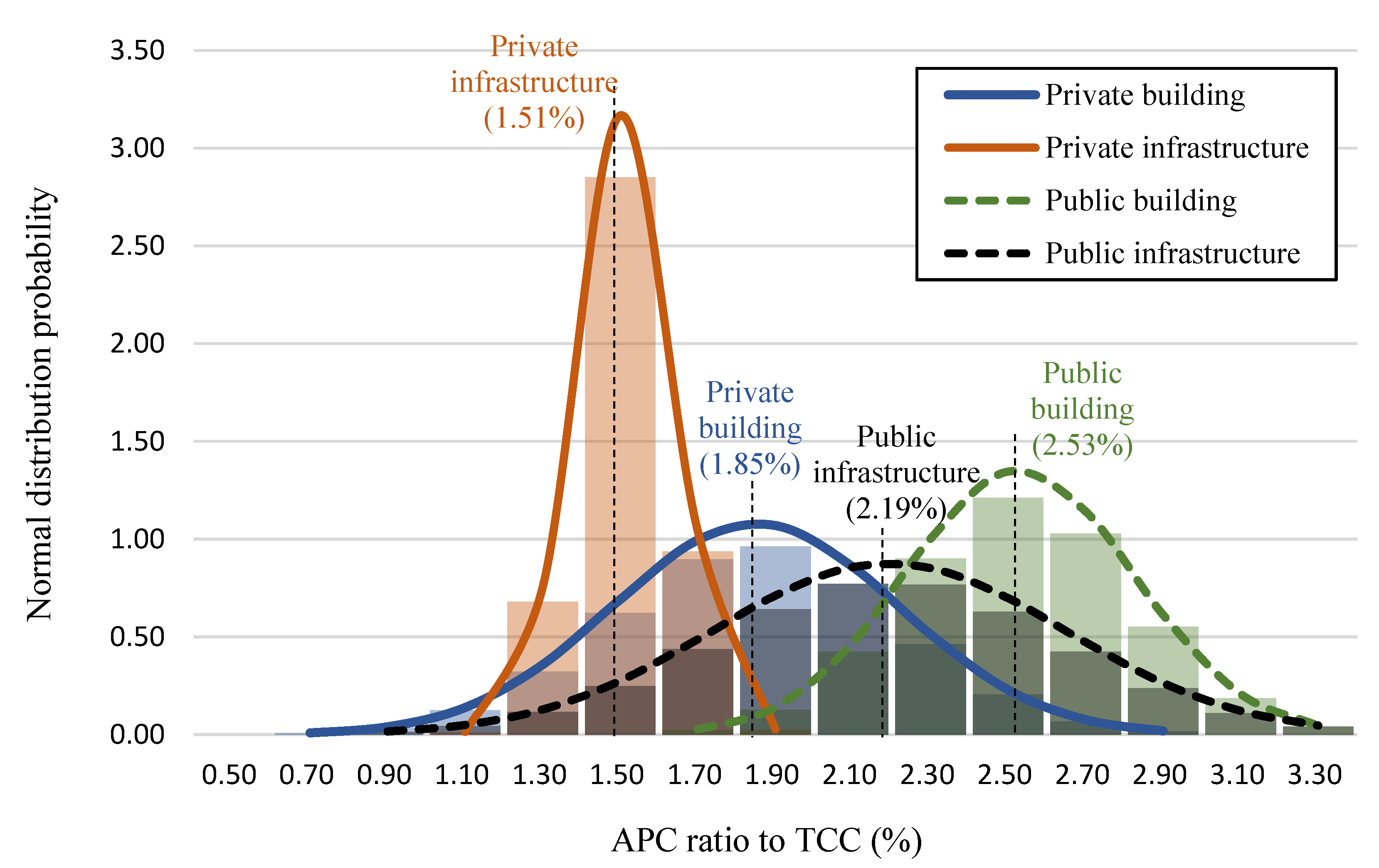

- ANOVA and post hoc tests were conducted after dividing the 38 target projects into four groups according to facility types, with the results indicating a significant difference among the average values of public buildings, private buildings, public infrastructure, and private infrastructure groups at the 95% confidence interval.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| TCC | Total construction cost |

| OSHMF | Occupational safety and health management funds |

| SMS | Safety manager salary |

| SF | Safety facility |

| PPE | Personal protective equipment |

| SE | Safety examination |

| EE | Educational events |

| HC | Health care |

| TC | Technical consultant |

| HU | Headquarter use |

| SSM | Subcontractor safety management |

| APC | Accident prevention cost |

| SME | Safety management expenses |

| SMP | Safety management plan |

| SI | Safety inspection |

| SDP | Surrounding damage prevention |

| TSM | Traffic safety measure |

| SM | Safety monitoring |

| SS | Structural safety |

| AAPC | Additional accident prevention cost |

| IACIPP | Industrial accident compensation insurance and prevention premiums |

| WCIP | Worker’s compensation insurance premiums |

| OAC | Other additional cost |

| OSHA | Occupational Safety and Health Act |

| MOEL | Ministry of Employment and Labor |

| CTPA | Construction Technology Promotion Act |

| MOLIT | Ministry of Land, Infrastructure and Transport |

| IACIA | Industrial Accident Compensation Insurance Act |

References

- International Labour Organization (ILO). International Labour Standards on Occupational Safety and Health. 2019. Available online: https://www.ilo.org/global/standards/subjects-covered-by-international-labour-standards/occupational-safety-and-health/lang--en/index.htm (accessed on 19 April 2022).

- International Labour Organization (ILO). World Day for Safety and Health at Work 2019. 2019. Available online: https://www.ilo.org/safework/events/safeday/lang--en/index.htm (accessed on 19 April 2022).

- Jeong, J.; Jeong, J. Comparative analysis of degree of risk between the frequency aspect and probability aspect using integrated uncertainty method considering work type and accident type in construction industry. Appl. Sci. 2022, 12, 1131. [Google Scholar] [CrossRef]

- Shim, Y.; Jeong, J.; Jeong, J.; Lee, J.; Kim, Y. Comparative analysis of the national fatality rate in construction industry using time-series approach and equivalent evaluation conditions. Int. J. Environ. Res. Public Health 2022, 19, 2312. [Google Scholar] [CrossRef] [PubMed]

- Heidary Dahooie, J.; Vanaki, A.S.; Firoozfar, H.R.; Zavadskas, E.K.; Čereška, A. An extension of the failure mode and effect analysis with hesitant fuzzy sets to assess the occupational hazards in the construction industry. Int. J. Environ. Res. Public Health 2020, 17, 1442. [Google Scholar] [CrossRef] [PubMed]

- Rodrigues, F.; Baptista, J.S.; Pinto, D. BIM approach in construction safety—A case study on preventing falls from height. Buildings 2022, 12, 73. [Google Scholar] [CrossRef]

- Sánchez Colmenarejo, J.I.; Camprubí, F.M.; González-Gaya, C.; Sánchez-Lite, A. Power Plant Construction Projects Risk Assessment: A Proposed Method for Temporary Systems of Commissioning. Buildings 2022, 12, 1260. [Google Scholar] [CrossRef]

- Sola-Caraballo, J.; Rincón-Calderón, J.M.; Rivera-Gómez, C.; López-Martínez, J.A.; Galán-Marín, C. On-Site Risk Assessment Methodology of Historic Timber Structures: The Case Study of Santa Cruz Church. Buildings 2022, 12, 935. [Google Scholar] [CrossRef]

- Marić, M.K.; Ivanković, A.M.; Srbić, M.; Skokandić, D. Assessment of Performance Indicators of a Large-Span Reinforced Concrete Arch Bridge in a Multi-Hazard Environment. Buildings 2022, 12, 1046. [Google Scholar] [CrossRef]

- Jeong, J.; Jeong, J. Quantitative risk evaluation of fatal incidents in construction based on frequency and probability analysis. J. Manag. Eng. 2022, 38, 04021089. [Google Scholar] [CrossRef]

- Moaveni, S.; Banihashemi, S.Y.; Mojtahedi, M. A conceptual model for a safety-based theory of lean construction. Buildings 2019, 9, 23. [Google Scholar] [CrossRef]

- Soh, J.; Jeong, J.; Jeong, J. Improvements of design for safety in construction through multi-participants perception analysis. Appl. Sci. 2020, 10, 4550. [Google Scholar] [CrossRef]

- Gurcanli, G.E.; Bilir, S.; Sevim, M. Activity based risk assessment and safety cost estimation for residential building construction projects. Saf. Sci. 2015, 80, 1–12. [Google Scholar] [CrossRef]

- Lee, J.; Jeong, J.; Soh, J.; Jeong, J. Development of framework for estimating fatality-related losses in the Korean construction industry. Int J. Environ. Res. Public Health 2021, 18, 8787. [Google Scholar] [CrossRef] [PubMed]

- Hallowell, M.R. Risk-based framework for safety investment in construction organizations. J. Construct. Eng. Manag. 2011, 137, 592–599. [Google Scholar] [CrossRef]

- Lu, M.; Cheung, C.M.; Li, H.; Hsu, S.C. Understanding the relationship between safety investment and safety performance of construction projects through agent-based modeling. Accid. Anal. Prevent. 2016, 94, 8–17. [Google Scholar] [CrossRef] [PubMed]

- Han, Y.; Li, J.; Cao, X.; Jin, R. Structural equation modeling approach to studying the relationships among safety investment, construction employees’ safety cognition, and behavioral performance. J. Construct. Eng. Manag. 2020, 146, 04020065. [Google Scholar] [CrossRef]

- Yiu, N.S.; Chan, D.W.; Sze, N.N.; Shan, M.; Chan, A.P. Implementation of safety management system for improving construction safety performance: A structural equation modelling approach. Buildings 2019, 9, 89. [Google Scholar] [CrossRef]

- Tan, H.; Wang, H.; Chen, L.; Ren, H. Empirical analysis on contribution share of safety investment to economic growth: A case study of Chinese mining industry. Saf. Sci. 2012, 50, 1472–1479. [Google Scholar] [CrossRef]

- Wang, Z.; Hofer, C.; Dresner, M.E. Financial condition, safety investment and accident propensity in the US airline industry: A structural analysis. Transport. Res. Part. E Logist. Transport. Rev. 2013, 49, 24–32. [Google Scholar] [CrossRef]

- Aminbakhsh, S.; Gunduz, M.; Sonmez, R. Safety risk assessment using analytic hierarchy process (AHP) during planning and budgeting of construction projects. J. Saf. Res. 2013, 46, 99–105. [Google Scholar] [CrossRef]

- Ma, Y.; Zhao, Q.; Xi, M. Decision-makings in safety investment: An opportunity cost perspective. Saf. Sci. 2016, 83, 31–39. [Google Scholar] [CrossRef]

- Lee, J.; Jeong, J.; Soh, J.; Jeong, J. Quantification analysis of safety investment cost and fatal accident cost in construction. J. Archit. Inst. Korea 2021, 37, 211–218. [Google Scholar]

- Tappura, S.; Sievänen, M.; Heikkilä, J.; Jussila, A.; Nenonen, N. A management accounting perspective on safety. Saf. Sci. 2015, 71, 151–159. [Google Scholar] [CrossRef]

- Mohammadi, A.; Tavakolan, M.; Khosravi, Y. Factors influencing safety performance on construction projects: A review. Saf. Sci. 2018, 109, 382–397. [Google Scholar] [CrossRef]

- Muhammad, B.A.; Abdulateef, I.; Ladi, B.D. Assessment of cost impact in health and safety on construction projects. Am. J. Eng. Res. 2015, 4, 25–30. [Google Scholar]

- Akcay, C.; Aslan, S.; Sayin, B.; Manisalı, E. Estimating OHS costs of building construction projects based on mathematical methods. Saf. Sci. 2018, 109, 361–367. [Google Scholar] [CrossRef]

- Aven, T.; Hiriart, Y. The use of a basic safety investment model in a practical risk management context. Reliab. Eng. Syst. Saf. 2011, 96, 1421–1425. [Google Scholar] [CrossRef]

- Ministry of Employment and Labor (MOEL). Occupational Safety and Health Act (OSHA). Article 72. 2020. Available online: https://elaw.klri.re.kr/kor_service/lawView.do?hseq=55395&lang=ENG (accessed on 30 April 2022).

- Ministry of Land, Infrastructure and Transport (MOLIT). Construction Technology Promotion Act (CTPA). Article 63. 2020. Available online: https://elaw.klri.re.kr/kor_service/lawView.do?hseq=54608&lang=ENG (accessed on 30 April 2022).

- Baek, Y.; Wee, K.; Baek, I.; Kim, J. A study on improvement of occupational safety and health management cost accounting standards. Korean J. Construct. Eng. Manag. 2020, 21, 39–46. [Google Scholar]

- Kim, S.H.; Kim, J.H.; Kim, B.S.; Park, J.K. A study on the actual condition of OSH expenses appropriation in the construction industry. J. Korea Saf. Manag. Sci. 2016, 18, 25–31. [Google Scholar]

- Yoon, Y.G.; Oh, T.K.; Lee, M.G.; Seong, J.H.; Jung, M.H. A study on the estimation of the proper rates of safety management cost in the construction technology promotion law for reasonable construction safety management. J. Korean Soc. Saf. 2018, 33, 84–91. [Google Scholar]

- Yi, K.J. Accident prevention cost-effectiveness of current safety manager assignment policies. J. Archit. Instit. Korea Struct. Construct. 2008, 24, 161–168. [Google Scholar]

- Ibarrondo-Dávila, M.P.; López-Alonso, M.; Rubio-Gámez, M.C. Managerial accounting for safety management. The case of a Spanish construction company. Saf. Sci. 2015, 79, 116–125. [Google Scholar] [CrossRef]

- Yılmaz, M.; Kanıt, R. A practical tool for estimating compulsory OHS costs of residential building construction projects in Turkey. Saf. Sci. 2018, 101, 326–331. [Google Scholar] [CrossRef]

- Ikpe, E.; Hammon, F.; Oloke, D. Cost-benefit analysis for accident prevention in construction projects. J. Construct. Eng. Manag. 2012, 138, 991–998. [Google Scholar] [CrossRef]

- López-Alonso, M.; Ibarrondo-Dávila, M.P.; Rubio-Gámez, M.C.; Munoz, T.G. The impact of health and safety investment on construction company costs. Saf. Sci. 2013, 60, 151–159. [Google Scholar] [CrossRef]

- Feng, Y. Effect of safety investments on safety performance of building projects. Saf. Sci. 2013, 59, 28–45. [Google Scholar] [CrossRef]

- Feng, Y.; Teo, E.A.L.; Ling, F.Y.Y.; Low, S.P. Exploring the interactive effects of safety investments, safety culture and project hazard on safety performance: An empirical analysis. Int. J. Proj. Manag. 2014, 32, 932–943. [Google Scholar] [CrossRef]

- Feng, Y. Mathematical models for determining the minimum level of voluntary safety investments for building projects. J. Construct. Eng. Manag. 2015, 141, 04015015. [Google Scholar] [CrossRef]

- Korea Workers’ Compensation & Welfare Service (COMWEL). Website of the Korea Workers’ Compensation & Welfare Service. Available online: https://www.comwel.or.kr/eng/index.jsp (accessed on 5 May 2022).

- AIG Korea Branch. Website of AIG Korea Branch. Available online: https://m.aig.co.kr/wp/dpwpt072.html?menuId=MS121&prodCd=GC012 (accessed on 5 May 2022).

- Wang, B.; Wu, C.; Huang, L.; Kang, L. Using data-driven safety decision-making to realize smart safety management in the era of big data: A theoretical perspective on basic questions and their answers. J. Clean Prod. 2019, 210, 1595–1604. [Google Scholar] [CrossRef]

- Ko, J.H. A study on the improvement of industrial safety and health management cost using the survey of construction safety experts. J. Soc. Disaster Inf 2020, 16, 331–342. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Aims | Number | Authors | Cost Items | Results |

|---|---|---|---|---|

| Quantitative framework development | 1 | Hallowell, 2011 [15] |

|

|

| 2 | Gurcanli and Sevim, 2015 [13] |

|

| |

| 3 | Ibarrondo-Dávila et al., 2015 [35] |

|

| |

| 4 | Akcay et al., 2018 [27] |

|

| |

| 5 | Yılmaz and Kanıt, 2018 [36] |

|

| |

| Prevention cost effectiveness analysis | 1 | Ikpe and Oloke, 2012 [37] |

|

|

| 2 | López-Alonso et al., 2013 [38] |

|

| |

| 3 | Feng, 2013 [39] |

|

| |

| 4 | Feng et al., 2014 [40] |

|

| |

| 5 | Feng, 2015 [41] |

|

|

| Number | Accident Prevention Cost Item |

|---|---|

| 1 | Safety manager salary (SMS) |

| 2 | Safety facility (SF) |

| 3 | Personal protective equipment (PPE) |

| 4 | Safety examination (SE) |

| 5 | Educational events (EE) |

| 6 | Health care (HC) |

| 7 | Technical consultant (TC) |

| 8 | Headquarter use (HU) |

| 9 | Subcontractor safety management (SSM) |

| 10 | Others |

| Number | Accident Prevention Cost Item |

|---|---|

| 1 | Safety management plan (SMP) |

| 2 | Safety inspection (SI) |

| 3 | Surrounding damage prevention (SDP) |

| 4 | Traffic safety measure (TSM) |

| 5 | Safety monitoring (SM) |

| 6 | Structural safety (SS) |

| Company | Group | Number of Interviewees | Position | Career |

|---|---|---|---|---|

| Contractor A | Environment, safety, and health | 5 | Manager | More than 10 years |

| Contractor B | Health and safety | 7 | Manager | More than 15 years |

| Contractor C | Safety | 3 | General manager | More than 12 years |

| Accident Prevention Cost | Definition | |

|---|---|---|

| Level 1 | Level 2 | |

| Occupational safety and health Management funds | SMS | Labor cost of safety manager |

| SF | Cost of installing SF | |

| PPE | Cost of purchasing PPE | |

| SE | Cost of SE | |

| EE | Cost of safety training and event | |

| HC | Cost of health care of worker | |

| TC | Cost of technical consultant for accident Prevention | |

| HU | Cost used by headquarters’ safety Department | |

| SSM | Safety management cost used by subcontractor | |

| Others | Other costs required for safety | |

| Safety management expenses | SMP | Cost of developing an SMP |

| SI | Cost of SI | |

| SDP | Cost of damage prevention for buildings in the surrounding area | |

| TSM | Cost of traffic safety measure around construction sites | |

| SM | Cost of installing and operating safety monitoring devices | |

| SS | Cost of structural safety of temporary Structures | |

| Additional APCs | Industrial accident compensation insurance and prevention premiums (IACIPP) | Cost of insurance premium operated by the government |

| Worker’s compensation insurance premiums (WCIP) | Cost of insurance premium operated by a private company | |

| Other additional costs | Additional costs for the safety of construction workers by contractor | |

| Section | Questions | Purpose | |

|---|---|---|---|

| Company | Company name | Company identification | |

| Revenue of company | Calculation to IACIPP | ||

| Industrial accident insurance premiums of company | Calculation to IACIPP | ||

| Number of projects | Project identification | ||

| Project | Project name | Project identification | |

| Type of building | Project identification | ||

| Private/Public construction | Project identification | ||

| Construction cost | Calculation of IACIPP | ||

| Construction period | Project identification | ||

| Occupational safety and health expenses | SMS | Calculation of SMS cost | |

| SF | Calculation of SF cost | ||

| PPE | Calculation of PPE cost | ||

| SE | Calculation of SE cost | ||

| EE | Calculation of EE cost | ||

| HC | Calculation of HC cost | ||

| TC | Calculation of TC cost | ||

| HU | Calculation of HU cost | ||

| SSM | Calculation of SSM cost | ||

| Others | Calculation of other costs | ||

| Safety management expenses | SMP | Calculation of SMP cost | |

| SI | Calculation of SI cost | ||

| SDP | Calculation of SDP cost | ||

| TSM | Calculation of TSM cost | ||

| SM | Calculation of SM cost | ||

| SS | Calculation of SS cost | ||

| Additional APC | WCIP | Calculation of WCIP | |

| Other additional costs | Calculation of OAC | ||

| Items | APC Items | APC (A–E Subtotal) | ||||

|---|---|---|---|---|---|---|

| OSHMF (A) | SME (B) | AAPC | ||||

| IACIPP (C) | WCIP (D) | OAC (E) | ||||

| Ratio of average APC value to TCC (%) | 1.34 | 0.04 | 0.56 | 0.00 | 0.00 | 1.95 |

| Standard deviation of APC ratios to TCC (%) | 0.33 | 0.14 | 0.17 | 0.02 | 0.01 | 0.44 |

| APC item rate to APC (%) | 68.8 | 2.2 | 28.8 | 0.2 | 0.1 | 100.0 |

| Statistics | Regression Analysis Results | ||||

|---|---|---|---|---|---|

| Items | Value | Items | Coefficient | t-Statistic | p-Value |

| Multiple correlation coefficient | 0.924 | Y-intercept | 5.53 | 0.83 | 0.41 |

| Adjusted coefficient of determination | 0.845 | OSHMF | 49.40 | 6.49 | 1.7 × 10−7 |

| Standard error | 21.554 | IACIPP | 54.50 | 2.97 | 5.4 × 10−3 |

| Items | OSHMF Items | OSHMF (A–J Subtotal) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| SMS (A) | SF (B) | PPE (C) | SE (D) | EE (E) | HC (F) | TC (G) | HU (H) | SSM (I) | Others (J) | ||

| Average of OSHMF item ratio to TCC (%) | 0.43 | 0.56 | 0.13 | 0.05 | 0.04 | 0.02 | 0.01 | 0.00 | 0.10 | 0.00 | 1.34 |

| Standard deviation of OSHMF item ratio to TCC (%) | 0.17 | 0.28 | 0.08 | 0.03 | 0.03 | 0.01 | 0.02 | 0.01 | 0.22 | 0.02 | 0.33 |

| OSHMF item rate to OSHMF (%) | 32.5 | 41.5 | 9.9 | 3.4 | 3.1 | 1.2 | 0.4 | 0.1 | 7.7 | 0.3 | 100.0 |

| Items | SME Items | SME (A–F Subtotal) | |||||

|---|---|---|---|---|---|---|---|

| SMP (A) | SI (B) | SDP (C) | TSM (D) | SM (E) | SS (F) | ||

| Average SME item ratio to TCC (%) | 0.01 | 0.01 | 0.01 | 0.01 | 0.00 | 0.00 | 0.04 |

| Standard deviation of SME item ratio to TCC (%) | 0.03 | 0.03 | 0.04 | 0.06 | 0.01 | 0.00 | 0.14 |

| SME item rate to SME (%) | 14.9 | 29.5 | 20.0 | 25.7 | 8.3 | 1.6 | 100.0 |

| Independent Variable | Client Types | N | Mean | Standard Deviation | Levene’s Test for Equality of Variances | Independent Samples Test | ||

|---|---|---|---|---|---|---|---|---|

| F | Sig. | t | Significance (Two-Tailed) | |||||

| APC | Public project | 10 | 2.33 | 0.42 | 0.175 | 0.678 | 3.676 | 0.001 |

| Private project | 28 | 1.81 | 0.37 | |||||

| Variable | Facility Types | N | Mean | Standard Deviation | Test of Homogeneity of Variances | One-Way ANOVA | ||

|---|---|---|---|---|---|---|---|---|

| Levene Statistic | Significance | F Value | Significance | |||||

| APC | Public building | 4 | 2.53 | 0.29 | 0.787 | 0.510 | 6.180 | 0.002 |

| Public infrastructure | 6 | 2.19 | 0.46 | |||||

| Private building | 25 | 1.85 | 0.37 | |||||

| Private infrastructure | 3 | 1.51 | 0.13 | |||||

| Dependent Variable: APC | Post hoc Test (Multiple Comparisons, Scheffé) | |||

|---|---|---|---|---|

| Variable 1 | Variable 2 | Mean Difference | Standard Error | Significance |

| Public building | Public infrastructure | 0.334 | 0.238 | 0.583 |

| Public building | Private building | 0.678 | 0.198 | 0.017 * |

| Public building | Private infrastructure | 1.014 | 0.281 | 0.011 * |

| Public infrastructure | Private building | 0.344 | 0.167 | 0.257 |

| Public infrastructure | Private infrastructure | 0.680 | 0.260 | 0.098 ** |

| Private building | Private infrastructure | 0.336 | 0.225 | 0.534 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, J.; Jeong, J.; Soh, J.; Jeong, J. Quantitative Analysis of the Accident Prevention Costs in Korean Construction Projects. Buildings 2022, 12, 1536. https://doi.org/10.3390/buildings12101536

Lee J, Jeong J, Soh J, Jeong J. Quantitative Analysis of the Accident Prevention Costs in Korean Construction Projects. Buildings. 2022; 12(10):1536. https://doi.org/10.3390/buildings12101536

Chicago/Turabian StyleLee, Jaehyun, Jaewook Jeong, Jayho Soh, and Jaemin Jeong. 2022. "Quantitative Analysis of the Accident Prevention Costs in Korean Construction Projects" Buildings 12, no. 10: 1536. https://doi.org/10.3390/buildings12101536

APA StyleLee, J., Jeong, J., Soh, J., & Jeong, J. (2022). Quantitative Analysis of the Accident Prevention Costs in Korean Construction Projects. Buildings, 12(10), 1536. https://doi.org/10.3390/buildings12101536