1. Introduction

In today’s complex and dynamic financial landscape, effective FRM [

1] has become increasingly critical for organizations striving to maintain stability and achieve sustainable growth. FRM entails the enumeration, evaluation, and categorization of financial risks and then declaring the optimal use of funds to alter the chance of regrettable occurrences. The increasing complexity of financial markets and various risks, including market risks, credit risks, liquidity risks, and regulatory risks, make the use of other traditional risk measurement models less capable of addressing the uncertainties and vagueness of financial data.

In the field of FRM, MCGDM [

2] approaches have stepped forward because they allow for more straightforward evaluations with multiple conflicting criteria. However, there is a significant limitation for those current MCGDM techniques where deterministic models are used in the assessment while financial information is normally associated with fuzziness. Some of the decision outcomes would not be optimal, and the decision-makers would also be unable to dictate the various facets of financial risk. The fuzzy set (FS) theory, together with its concepts, was initiated by Zadeh [

3] in 1965, where it addressed inherent vagueness by allowing elements to belong to a set at a degree between

and

rather than belonging or not belonging to a set. However, applying the concept of a traditional FS fails to formulate the different aspects of decision-making conditions. To this end, Intuitionistic Fuzzy Sets (IFS), developed by Atanassov [

4], use both the membership degree (MD) and non-membership degree (NMD), leading to a probabilistic approach to uncertainty. However, IFS has problems describing hesitation and uncertainty; Yager [

5] proposed Pythagorean Fuzzy Sets (PyFS) and q-Rung Orthopair Fuzzy Sets (q-ROFS) [

6], where flexibility is attained with the freedom to have the MD and NMD vary across more than one dimension. picture fuzzy sets (PFS) were introduced by Cuong [

7], which include abstinence degrees (ADs) that provide more flexibility. Finally, interval-valued picture fuzzy sets (IV-PFS) [

8] expand on PFS by incorporating interval values to represent uncertainty, making them particularly useful for financial applications where precise information is often unavailable.

This study uses the interval-valued picture fuzzy (IVPF) approach integrated with the MARCOS approach to FRM. Thus, applying IVPF with MARCOS helps to provide a more solid approach to managing uncertainty and imprecision, which characterizes addressing critical financial decisions. IVPF is a more suitable method to depict uncertainty since it combines MD and NMD with AD intervals, making it more ideal for decision-making than conventional fuzzy systems. The IVPF-MARCOS methodology is superior to expert-based and data-based approaches since it can incorporate accurate additional expert knowledge and provide decision scheme flexibility without needing massive amounts of data, which are often lacking in FRM. This combination is beneficial where instability and reliance on the need for judgment are paramount. When combining IVPF for uncertainty modeling and MARCOS for ranking and evaluating the alternatives, the proposed methodology is superior for use in FRM in terms of efficiency and effectiveness.

1.1. Objectives

This research’s primary objective is to assess ten different investment options based on seven essential factors, with the implementation of views of various decision-makers for the analysis. Recognizing the strengths of the IVPF-MARCOS approach, this research advances our understanding of FRM and offers practitioners the framework to make their investments more resilient to uncertainties.

The following are the secondary objectives of this study.

- (a)

To involve multiple decision-makers and make financial decisions more secure.

- (b)

To enhance the capability of decision-makers under uncertainty through detecting and managing the impacts of fuzzy information in FRM.

- (c)

To enhance advanced fuzzy techniques in the process of financial decision-making.

1.2. Contributions

This study has the following contributions:

- (a)

This research explores the use of IVPF information to improve the MARCOS application for evaluating MCGDM methods of FRM.

- (b)

This study contributes an assessment framework that facilitates the structured analysis of financial issues for practice application.

- (c)

The IVPF-MARCOS algorithm is an advanced instrument used in practice by financial decision-makers. It allows them to make choices that consider the uncertainty of financial data.

- (d)

This work responds to a gap in the literature emphasizing that new forms of fuzzy techniques can be implemented in FRM and offers more research into new approaches to managing financial risks.

1.3. Research Gap and Motivations

While the interest and need for FRM are huge and ever-increasing, given the current economic instability, there are still many shortcomings in how methodologies are developed to address the issues and concerns that have become prominent in decision-making. The quantitative approaches applied to risk management often involve computational methods most suitable for deterministic environments and do not consider that the data involved exhibit a certain level of imprecision. Moreover, although various MCGDM methods are used when implementing FRM, most of these methodologies do not consider the issue of fuzzy information and, therefore, provide low-quality decisions. However, there is a gap in the literature regarding integrating IVPF information into MCGDM frameworks, which restricts the applicability and impact of risk management approaches in today’s world. Hence, developing efficient decision-making structures capable of handling uncertain data has become increasingly important. Still, at the same time, more systematically structured methods have arisen that evaluate these multiple competing factors in financial domains. This gap underlines the need for new approaches that could increase the effectiveness and relevance of FRM approaches and improve investment decisions’ efficiency.

The motivations for this study come from the inherent gap arising from the limitations of existing FRM methodologies. In the capacity of providing basic information on risks and returns, decision-makers need sharper tools that are capable of analyzing fuzzy markets. Therefore, while implementing the MARCOS algorithm within an IVPF context, the present investigation expects to devise a more efficient decision-making instrument to improve the evaluation and ranking of investment options. In addition, an extension of IVPF in MCGDM also solves the problem of vagueness that may exist in financial assessments. It facilitates a more comprehensive analysis of trade-offs in the management of FRM. This research will, therefore, aim to arm organizations with a strong framework of how they can best manage investment opportunities to ensure their increased readiness in the face of any uncertainty and, thus, increased financial stability. With this work, we would like to help enhance our knowledge about fuzzy decision-making techniques, especially in the context of the financial environment, and promote the development of the type of FRM used in the literature.

1.4. Structure of the Study

This paper is arranged to ensure that the proposed IVPF-MARCOS framework and its role in FRM are explained in detail. The literature review in

Section 2 is a fitting starting point because it discusses earlier work in FRM and the MARCOS approach. In

Section 3, preliminaries are introduced to the reader regarding the main mathematical concepts related to IV-PFS. In

Section 4, the methodology is described in detail, showing the integration of IVPF information into the MARCOS algorithm and explaining step by step how the IVPF-MARCOS framework works to demonstrate its ability to deal with uncertainty in financial data.

Section 5 illustrates a real-life application of the IVPF-MARCOS method, evaluating ten investment alternatives against seven criteria based on decision-maker evaluations; it further shows how this technique helps to make financial risk decisions. In

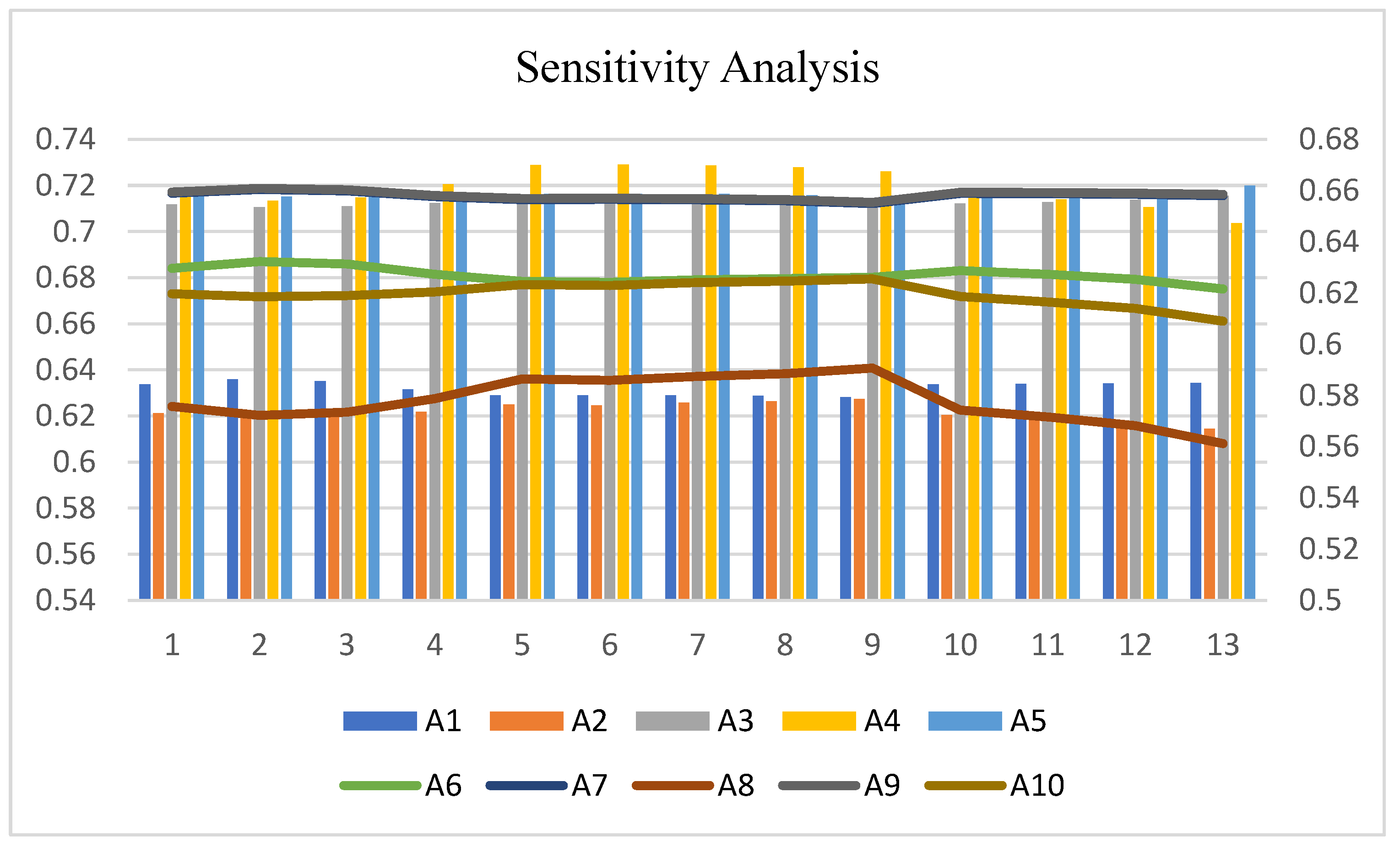

Section 6, sensitivity analysis is performed, and the research benefits are outlined. Lastly,

Section 7 provides a brief conclusion to the present study in addition to the limitations encountered with real-time data integration and applications to broader areas of finance.

4. Interval-Valued Picture Fuzzy-MARCOS Technique

In this study, we used the IVPF method and the interval-valued picture fuzzy weighted averaging (IVPFWA) operator to compute the weights for each criterion using the MCGDM methodology. In addition, linguistic parameters were converted into IVPFVs for further analysis. The MARCOS approach is based on ranking and measuring choices to obtain a compromise answer. Although the MARCOS approach can be an effective decision-making tool, it cannot express confusing or uncertain facts. As a result, providing a fuzzy extension to the approach is critical to increasing its capability. The IVPF-MARCOS technique is described as follows:

- (a)

, denotes the collection of users with weights represented by

and

.

- (b)

There are

criteria, and each weight is

- Step 1.

Experts evaluate criteria.

Table 1 shows the linguistic assessments for the users and the criteria.

- Step 2.

Generate an aggregated IVPF decision matrix.

The IVPF decision matrix for a given collection of users is . signifies the evaluation of about users with the criteria. is an IVPFV.

The aggregated IVPF decision matrix is represented as follows:

where

.

Table 2 is used to conduct linguistic assessments of the alternatives.

- Step 3.

Determine the best solutions for IVPF.

and are the best solutions for the IVPF-positive ideal solution (IVPFPIS) and IVPF-negative ideal solution (IVPFNIS), respectively. The results stated do not differ considerably from one another, even though the maximum operator and minimum operator define IVPFNIS and IVPFPIS.

- Step 4.

Calculate the distance measurement.

The distance measure is calculated using a fuzzy normalized Euclidean distance equation. The positive and negative distance measures in the following equations are determined using

and

, respectively.

- Step 5.

Determine the closeness coefficients’ (CCs’) values.

denotes the CCs of the

criterion, and it employs IVPFPIS

and IVPFNIS

as shown below.

- Step 6.

Calculate the weights of each criterion and alternative.

The CC values show the relative importance of each criterion. The concluded weights are supposed to be calculated using normalization, and the weights’ sum should equal one. A decision matrix,

, remains after steps 5 and 6.

- Step 7.

For IVPF, construct an expanded decision matrix.

By identifying the anti-ideal AI and ideal I solutions, an expanded decision matrix

could be generated.

In this case, I performed the best, and AI performed the worst. Using Equations (7) and (8), respectively, they can be determined.

It is evident that B is made up of criteria of the benefit type, whereas C is made up of criteria of the cost type.

- Step 8.

Construct the normalized IVPF decision matrix.

The procedure for determining the alternatives’ normalized value,

, is as follows.

- Step 9.

Construct the IVPF weighted decision matrix.

The weighted values for all options are calculated as follows.

in Equation (10) denotes the criterion’s relative relevance.

- Step 10.

Construct the matrix .

The values of the

matrix are gained by applying Equation (11).

- Step 11.

Determine the various degrees of utility of the options. Equations (12) and (13), when applied to alternatives, find the utility degrees of each alternative.

- Step 12.

Determine the alternatives’ utility function.

By using Equation (14), the utility functions of alternatives can be calculated.

In Equation (14),

represents the utility function of the ideal solution, whereas

represents the utility function of the anti-ideal solution. Equations (15) and (16) were used to determine

and

.

- Step 13.

Rank the alternatives.

In the final stage, alternatives are ranked using the final values of the utility functions. Stated differently, the most preferred alternative is the one with the highest utility value.

4.1. Assessment of Financial Risk Management

FRM recognizes, evaluates, and controls the risks affecting organizations investing and operating in the financial markets and making business decisions. It encompasses the methods applied in an organization to reduce the adverse effects of market, credit, liquidity, and operational risks. These risks come from numerous areas, including exchange rates, interest rates, stock prices, the credit risk of the borrowers, and operational risks. Specifically, emphasizing how financial risk managers measure risks, several techniques are applied, such as statistical analysis, stress tests, economic scenarios, and the application of such instruments as options and futures. The aim is to try to maintain stability for the long term, especially for banking institutions, investment houses, and companies engaged in significant funds transactions.

MCGDM methods are essential because incorporating numerous factors when addressing risk management in FRM is a tremendous advantage. Financial risks have traditionally contained dimensions where more than one criterion, which may sometimes be opposed, forms the basis of decision-making, such as profitability, liquidity, market exposure, or legal requirements. MCGDM assists financial managers in striking the above-competing aims and selecting the best course of action based on several criteria. To summarize, the application of MCGDM to FRM adheres to organized decision-making because it proposes how criteria could be gauged, how trades-offs among them might be evaluated, and how suitable options under conditions of uncertainty can be identified. More precisely, the MARCOS method allows for the ranking and identification of the most preferable FRM strategy. Thus, extending to an IVPF environment, MARCOS can adopt more uncertainty and ambiguity in decision-making as the IVPF can offer a more liberal expression of fuzzy data. This is particularly true where actual data may be imprecise or decision-maker assessments more subjective.

The problem consists of applying the IVPF-MARCOS method to address a Financial Risk Management decision regarding ten investment options assessed by seven criteria and considering the opinions of five decision-makers. Each alternative may be an investment or a financing plan, and each criterion defines a different dimension of financial risk. In the context of FRM, the decision-makers are either experts or those who want to take financial risks from another angle. They offer opinions on how well each of the alternatives progresses in the seven criteria in the RFM model. Most may be from another department or functional position within the financial institution or the organization.

- (a)

: Risk Management Officer;

- (b)

: Investment Analyst;

- (c)

: Compliance Officer;

- (d)

: Financial Controller;

- (e)

: External Financial Consultant.

4.1.1. Evaluation of Criteria

- (a)

Market Risk : Short-term risks include the possibility of losses being realized due to variations in factors such as stock prices and exchange rates.

- (b)

Credit Risk (): Risks include the failure of debtors or counterparties to pay the amount back in full on due dates.

- (c)

Liquidity Risk (): There is credit risk or inability to meet short-term liabilities.

- (d)

Operational Risk (): Internal variations risk association with corrupted internal activities or programs (for instance, threats to cyber security).

- (e)

Legal/Regulatory Risk (): There are possible penalties for law violations or other kinds of losses.

- (f)

Reputational Risk (): A counter risk may include damage to the company’s brand or reputation.

- (g)

Return on Investment (): Projected returns on intended stocks are significant for the best alternative investment.

These seven criteria have been chosen because they all cover the different aspects of FRM. They include some fundamental factors of risk and return, which are quantitative and qualitative, and form the basis for analyzing investment opportunities. These criteria have been derived from a literature survey and consultation with financial management experts, making them realistic and suitable for application in real-life financial decision-making situations.

4.1.2. Evaluation of Alternatives

As stated in the FRM note, each alternative is a possible business or investment solution that can be implemented or made in an organization. The alternatives should be varied and consist of concepts of probable approaches to financial management regarding risk.

- (a)

: Conservative Stock Portfolio;

- (b)

: High-Yield Bond Investment;

- (c)

: Real Estate Investment Trust;

- (d)

: Venture Capital Investment;

- (e)

: International Market Diversification (IMD);

- (f)

: Commodities Investment;

- (g)

: Hedge Fund Investment;

- (h)

: Corporate Bonds Portfolio;

- (i)

: Government Securities, also known as Treasury Bonds;

- (j)

: Cryptocurrency Portfolio.

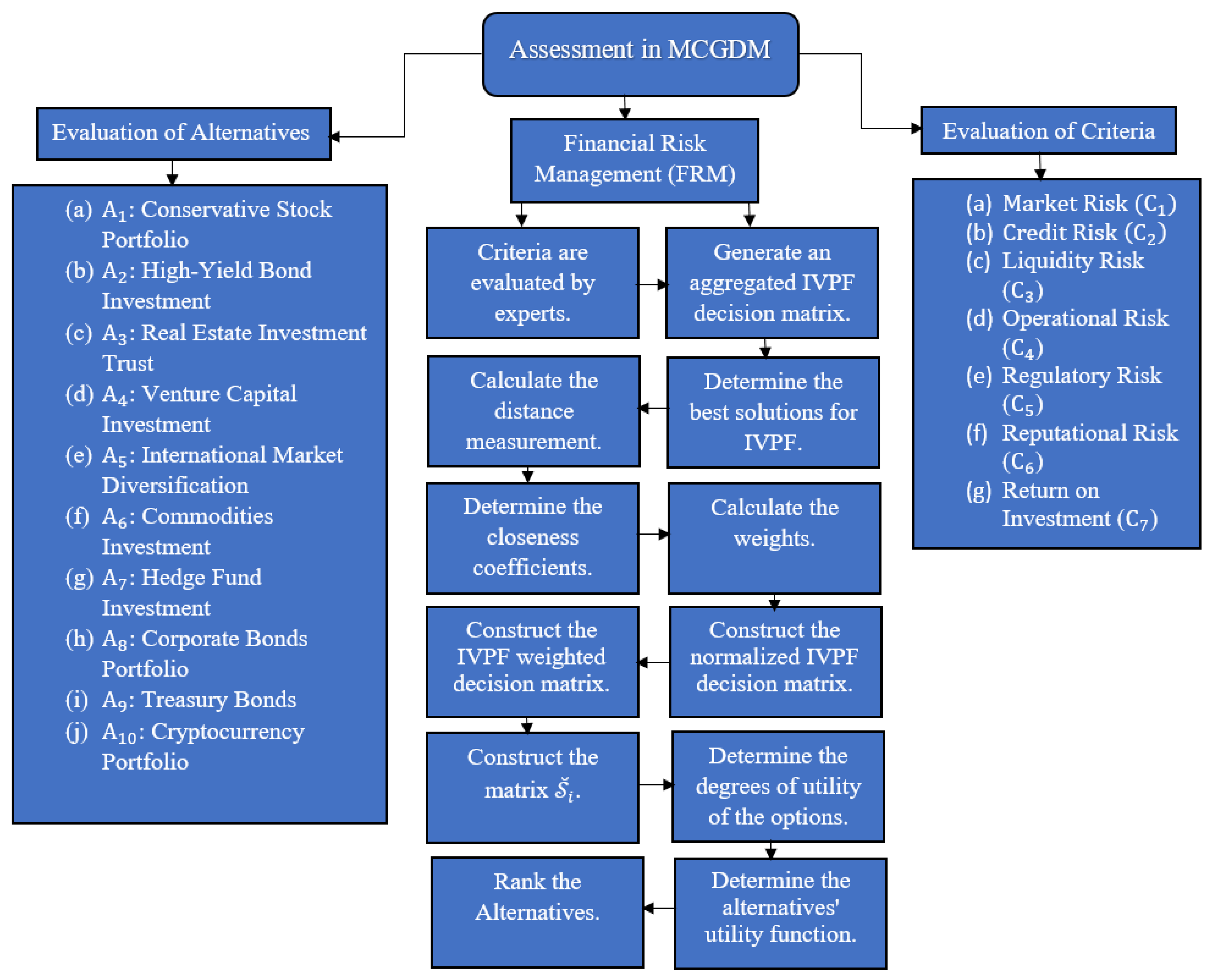

These alternatives are selected to represent as many possible scenarios concerning financial investments as possible and, thus, check the proposed methodology’s efficiency in the most practical cases possible. Their risks and returns are different, which allows for a comparison of how the FRM algorithm is efficient. The diversity helps enhance the generalization of the results, thus proving the efficiency of the methodological approach to actual financial decision-making dilemmas. These ten alternatives used in the study ensure good coverage while at the same time ensuring that the findings can be practically applied. A detailed flowchart of the above-discussed methodology is given in

Figure 1.

The alternatives are ranked using the MARCOS approach. This method determines each platform’s utility by contrasting it with both ideal (best) and anti-ideal (worst) options. The IVPF-MARCOS method’s ability to incorporate decision-maker hesitancies and various levels of confidence by including the IVPFVs can result in a more accurate and consensus-based option. In constructing the decision matrix in this research, five decision-makers, the Risk Management Officer, Investment Analyst, Compliance Officer, Financial Controller, and External Financial Consultant, assessed each criterion’s relevance and ranked the alternatives. Predefined linguistic expressions representing evaluations included criteria qualities such as “Very Important”, “Important”, and “Medium” and qualities of other options such as “Extremely Good”, “Very Good”, and “Very Bad”. These linguistic terms were then translated into IVPFVs, as highlighted in

Table 1 and

Table 2. For instance, a decision-maker may assign an IVPF value to a particular criterion as “Very Important” with an IVPF interval

. This ensures that a proven expert’s opinion is understandable and can be replicated; the values capture the necessary vagueness of decision-making. Incorporating these values enables the capturing of expert judgment so that effective decision-making can be enhanced.

Steps 1 and 2: Decision-makers evaluate the ten alternatives using the seven criteria and the rating scales in

Table 2 after completing linguistic assessments of the seven criteria using the rating scales in

Table 1. The linguistic assessments of the criteria and alternatives are provided in

Table 3 and

Table 4.

Step 3: The committee determines the decision-maker’s ratings using

Table 3. Next, each decision-maker’s weight is extracted. Their weights are shown in

Table 5.

Step 4:

Table 6 displays the aggregated IVPF decision matrix.

Step 5: The results of calculating the IVPF weights,

and

for each criterion are shown in

Table 7.

Step 6: The variables

,

, and

are determined in the next step using

Table 4, just like in Step 4.

Table A1 presents these values. Second,

Table A1 is used to generate

Table A2.

Step 7: Using the CC values from

Table A2, we construct an extended decision matrix, as shown in

Table A3.

Step 8: Each criterion’s normalized values are computed. The normalized IVPF decision matrix is shown in

Table A4.

Table A5 shows the weighted normalized IVPF decision matrix.

Step 9: Applying Equations (11)–(16), we obtain

Table 8.

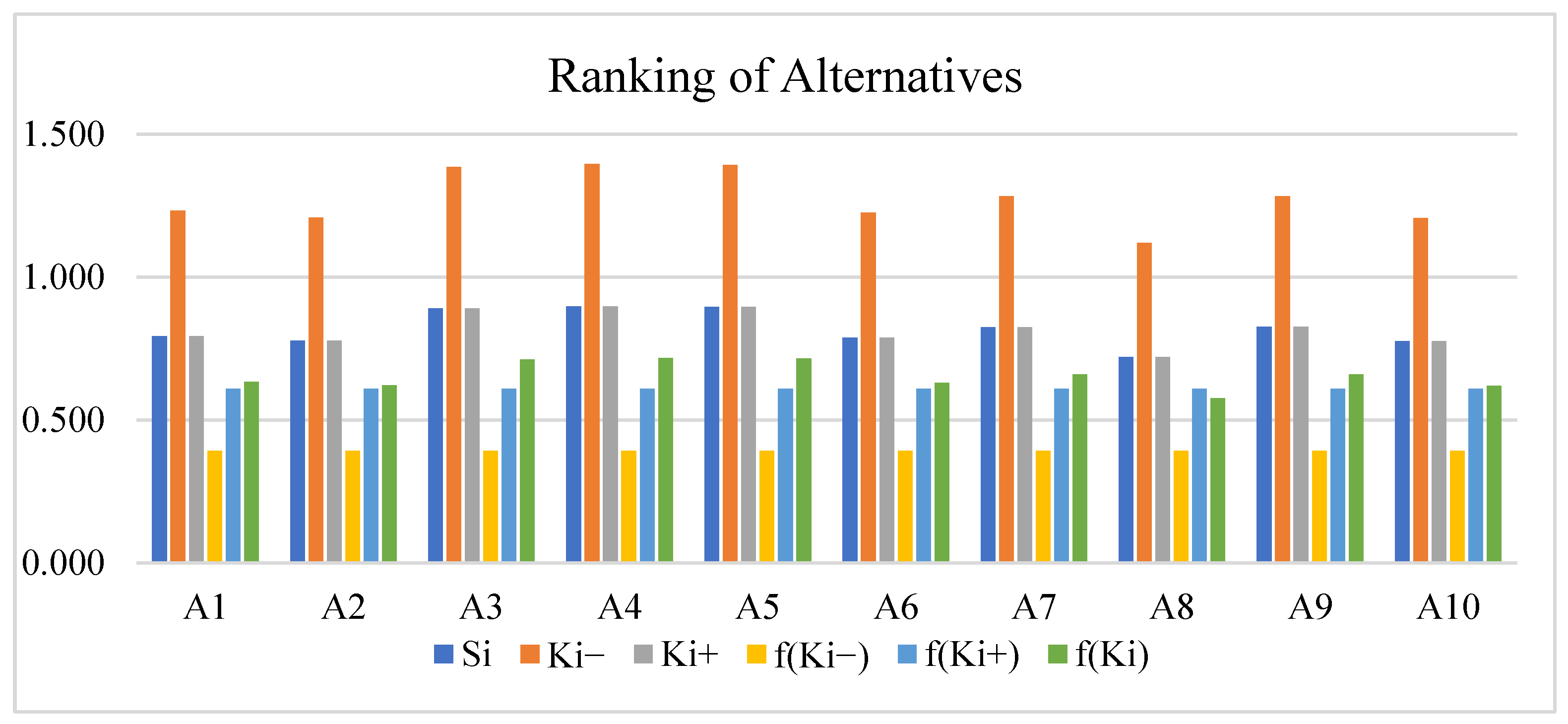

Figure 2 shows the graphical representation of the ranking of alternatives.

5. Result Discussion

The financial risk assessment further shows that and are the most advantageous for venture capital investment due to their high growth factor but low risk. Real estate investment trusts () are also on the favorable side, giving stability with moderate gains. Government securities and ) corporate bonds are ranked slightly down due to their attractive risk–reward profile, essentially benefiting the conservatives. Nevertheless, high-risk, low-return investments, like cryptocurrency , and commodities , are placed at the bottom of the pyramid since they tend to be relatively unstable compared to more reliable investment forms. Thus, the presented rankings reflect the expanse regarding risk–return constraints, which may suit conservative and large risk-taker investors. The proposed IVPF-MARCOS methodology is further demonstrated to be strong conceptually by the ability to accommodate various investment alternatives and possibilities, as well as the required criteria under conditions of risk and fuzziness. Using the IVPF framework, the methodology can minimize hesitation and incomplete information, which could be a problem in managing financial risk. Furthermore, the repetitions in ranking and evaluating the alternatives over a broad range of scenarios prove the reliability of the framework. The current study does not compare the framework on large datasets to see how it performs in different decision-making scenarios. Still, the results imply that the framework could be extended to accommodate the differences. This robustness, in turn, is underpinned by the diverse investment options and criteria captured by this model, making it well-suited for various financial environments where investments might exist.

{kind=link}

{kind=link}

{kind=link}