1. Introduction

We live in a globalized world in which many companies and agents invest in financial markets. The problem lies in the uncertainty associated with these investments and the likelihood that security yields will increase or decrease, affecting their liquidity. These variations may be due to numerous factors, such as interest and inflation rates. Therefore, this research studies which models best explain the sensitivity of stock market prices to variations in the risk factors analysed in this paper.

Thus, this paper analyses the consistency of the extensions of the Fama and French three- and five-factor models [

1,

2,

3,

4] in the Spanish stock market, approximated through the IBEX-35 market index. Specifically, the aim of this paper is to study the returns of the Spanish companies that currently comprise this index and their variation in response to changes in the risk factors proposed in the aforementioned extensions of the Fama and French models. With regard to the analysis period, this paper covers the period from January 2000 to December 2018. Moreover, for robustness, we split our sample period into three subperiods—precrisis, crisis and postcrisis—as the scenario changes according to the economic cycle. This analysis allows us to make a robust contrast of the results found in the estimates for the entire sample period, which could allow us to identify different sensitivities of stock returns depending on the stage of the economy.

On the other hand, this paper estimates the factor models proposed through the quantile regression (QR) technique, which provides numerous advantages over more traditional techniques. In addition, this paper focuses on the IBEX-35 companies’ returns of the Spanish stock market for several reasons. First, the Spanish market is one of the most relevant stock markets in the Eurozone [

5]. Second, Spain has suffered the most from the consequences of the recent global financial crisis [

6]. Third, in the context of the Fama and French factor models, not many studies analyse the Spanish market (with the exception of [

4]) or include the Spanish market when the European markets are studied (see [

7,

8] and other studies at the company level in [

9,

10]).

Although some papers, such as [

3,

4], have carried out a study based on the Fama and French models, the present study contributes to the literature in the following three ways. First, we add three explanatory factors to the three- and five-factor Fama and French models [

1,

2]: momentum, reversal momentum and the liquidity factor. To the best of our knowledge, this study is the first to apply this extension to the Spanish stock market. Second, we compare the current five-factor model of Fama and French [

2] with the original three-factor model of Fama and French [

1] to determine which model best explains the Spanish companies’ returns for both the whole sample period and for the three subperiods to demonstrate the effect of the stage of the economic cycle in our results. Third, the method used to estimate the relationship between the variables is QR. This method provides information about the median and considers the different quantiles to observe how the variable behaves in the different theta values.

Specifically, this methodology addresses the relevant issue of asymmetries by analysing whether the sensitivity of the Spanish companies’ returns to changes in the explanatory factors changes across the quantiles, that is, in different states of the market. Moreover, this study analyses the potentially different behaviours and reactions of the Spanish companies in several (pre-, during and postcrisis) scenarios. Thus, our null hypothesis assumes that the sensitivity of the Spanish companies’ returns to changes in the risk factors included in the proposed factor models are quantile- and stage-of-the-economy-dependent. Specifically, we hypothesize that the greatest levels of explanatory power are at the extreme quantiles.

Finally, the rest of this research is divided into four sections.

Section 2 includes a review of the literature.

Section 3 presents the variables included in the study and the method used.

Section 4 shows the most relevant results, including a robustness test. Finally,

Section 5 presents the main conclusions of this study.

2. Literature Review

The financial literature has proposed different factor models to try to explain the behaviour of stock market returns. These models have been applied to different international markets and sample periods, the latter of which distinguish phases of expansion and recession.

The first generally accepted unifactorial model that appears in the financial literature is the capital asset pricing model (CAPM), which incorporates the stock market portfolio return as an explanatory factor. Since then, different multifactor models have emerged, adding other explanatory factors to the model.

One of the most well-known models is the Fama and French three-factor model [

1], where the explanatory factors are the stock market return, size and growth. Subsequently, Fama and French expanded their previous model by adding profitability and investment risk factors, thus proposing the Fama and French five-factor model [

2]. These two models have been applied in numerous studies, such as [

11], who test both models on the CNX500 market in an emerging economy, India, and conclude that the five-factor model has greater explanatory power than the three-factor model does. [

12] did the same in the Australian stock market, finding that the five-factor model provides an acceptable but still incomplete description of stock returns. The risk factors of profitability and investment have also been studied in papers such as [

13], who studied stock returns in cases in which small companies invest greatly in return for low profitability, specifically in the USA. These companies are called “abnormal” because they invest a lot despite their low profitability, so the explanatory power of the profitability factor is limited for this type of company.

The five-factor model of Fama and French [

2] observes some anomalies by examining the problems that occur when studying the low stock returns of companies that invest aggressively. Subsequently, [

14] have analysed some international markets such as North America, Japan, Europe and Asia Pacific, focusing on the U.S. stock market. In North America, Europe and Asia Pacific, stock returns are positively related to the profitability factor and market portfolio returns, but decline with the investment factor. In Japan, stock returns are positively related to stock market returns, but have little to do with profitability and investment.

Later, [

4] extend the Fama and French five-factor model by including additional explanatory factors such as the nominal and real interest rate and the expected inflation rate. Thus, [

6] analyse the degree of exposure of Spanish sector stock returns to variations in interest rates by using the QR method and applying the Fama and French three-factor model (as in [

15]). This research shows a statistically significant sensitivity that is more pronounced in times of crisis.

Finally, [

3] conclude that other factors may also explain the sensitivity of stock market returns. This latest research proposes to include the risk factors momentum (MOM) and momentum reversal (LTREV) [

16] and the liquidity factor negotiated (LIQV) [

17] to extend the explanatory power of the Fama and French models.

The present research is focused on the extension of the Fama and French three- and five-factor models, according to [

3], to study the behaviour of the Spanish companies’ returns to variations in the risk factors of these two models in the whole sample period and in three subperiods according to the economic cycle (called precrisis, crisis and postcrisis).

Additionally, regarding the reactions of companies to crisis, according to [

9,

10], the companies’ reaction (proactive/reactive) and the perception of uncertainty (high/low) would be connected, assuming that uncertainty essentially appears in times of economic turmoil. Thus, this perspective is very interesting when analysing the reaction of companies to crisis periods. [

9], among others, suggest that companies characterized by a proactive behaviour show a riskier orientation, aimed at opportunity search and creation in times of economic downturns. However, companies with reactive behaviour present more passive and conservative profiles, reducing investments in innovative activities in crisis periods and focusing on short-term strategies.

In this way, a cyclical hypothesis suggests that investments in innovations increase in expansion periods, but decrease in economic turmoil. Therefore, some previous literature (such as [

9,

10]) assumes potential different responses and strategies towards crisis. Specifically, [

10] suggest the pro-cyclicality and the counter-cyclicality hypothesis, and their results support the idea that proactiveness may be sensitive to the business cycle, because they assume that investments in innovation increase during economics expansions and decrease in recession periods. This point of view could be applied to our research to explain the potential different behaviour of Spanish companies’ stock returns to changes in some relevant risk factors included in our study.

To contribute to the previous literature, this study analyses the sensitivity of Spanish companies’ returns to changes in the explanatory factors across the quantiles, focusing on the relevant issue of potential asymmetries. Furthermore, this research examines whether the behaviour of Spanish companies in several (pre-, during and postcrisis) scenarios is different (or not). Specifically, we assume that the sensitivity of Spanish companies’ returns to changes in the risk factors included in the proposed factor models depends on the quantiles and the stage of the economy.

5. Conclusions

This paper analyses the sensitivity of the Spanish stock market at the company level to changes in different risk factors commonly accepted in the financial literature. For this purpose, we compare two factor models (called Models A and B in this paper) based on the extended three- and five- models of Fama and French [

1,

2] to explain the behaviour of the IBEX-35 companies’ returns in the period between January 2000 and December 2018. The QR method is used to obtain the best possible estimate. Moreover, we divide the entire sample period (January 2000–December 2018) into three subperiods: precrisis (January 2000–January 2008), crisis (February 2008–January 2014) and postcrisis (February 2014–December 2018). This division allows us to contrast the robustness of the results and the different behaviours of our two models depending on the stage of the economic cycle.

Regarding this paper’s conclusions about the explanatory factors of the two models analysed in it, several variables have similar behaviours in all periods. These variables include RM, which shows the most statistically significant coefficients, and which shows a positive sign for most companies, especially in the full period and in the postcrisis subperiod. Specifically, on average, between the quantiles, approximately 94% and 97% for Models A and B, respectively, of the companies show positive sensitivity to variations in this factor in the full period. Consistently, for Models A and B respectively, 76% and 80% in the precrisis subperiod, 65% and 72% in the crisis subperiod and 80% and 86% of the companies show the same behaviour. Moreover, Model B shows a higher number of the companies with positive and statistically significant sensitivity to variations in this factor in all periods. In addition, the lowest quantiles have more statistically significant companies in most periods.

On the other hand, the nominal interest rate (i) varies during the analysis, depending on the stage of the economic cycle. In all periods, Model A (vs. B) has more statistically significant coefficients. With respect to the sign, in the lowest quantiles, it is positive, and as we advance in theta values, this sign becomes negative in most periods. The crisis subperiod has more statistically significant coefficients to changes in this risk factor than, in general, to variations in the rest of explanatory factors. This result is relevant, as it could suggest that the variable interest rate has a greater impact on Spanish companies’ returns in the stages of economic recession. In addition, the observed sign would determine that changes in interest rates imply changes in business returns in different directions at low theta values, while they imply changes in the same direction at high theta values.

We observe the same trend with MOM and LTREV in most periods. The sensitivity of the companies’ returns to variations in these two risk factors is positive in the low quantiles and becomes negative as we move towards the high quantiles. Moreover, for the first variable, MOM, a higher number of companies show statistically significant coefficients than for the second variable, LTREV, in most periods, especially in the last subperiod. Additionally, in both factors, most statistically significant coefficients are in the extreme quantiles. These results confirm that the methodology used in this paper is appropriate.

SMB is one of the most significant variables explaining the behaviour of companies’ returns. Specifically, it presents a positive and statistically significant sensitivity in all periods and models, mainly in the crisis subperiod according to [

3]. With regard to HML, results were inconsistent, but the variable is the second most significant (after RM) for the first model in the postcrisis subperiod and for the full period. Meanwhile, the least relevant factor in terms of statistical significance is LIQV, as even at the medium quantiles (especially in the precrisis and postcrisis subperiods) no companies have statistically significant coefficients.

Regarding the specific factors of Model B, the trend in RMW is linear in terms of statistically significant coefficients. Moreover, the sign of these coefficients is positive in the lowest quantiles and becomes negative in the highest quantiles in most periods (except for the crisis subperiod, where this factor is not relevant). With respect to CMA, the extreme quantiles in most periods have many statistically significant coefficients (except for the postcrisis subperiod, where the trend is decreasing). These coefficients are positive in the low quantiles, but become negative as we advance towards the high quantiles in all periods.

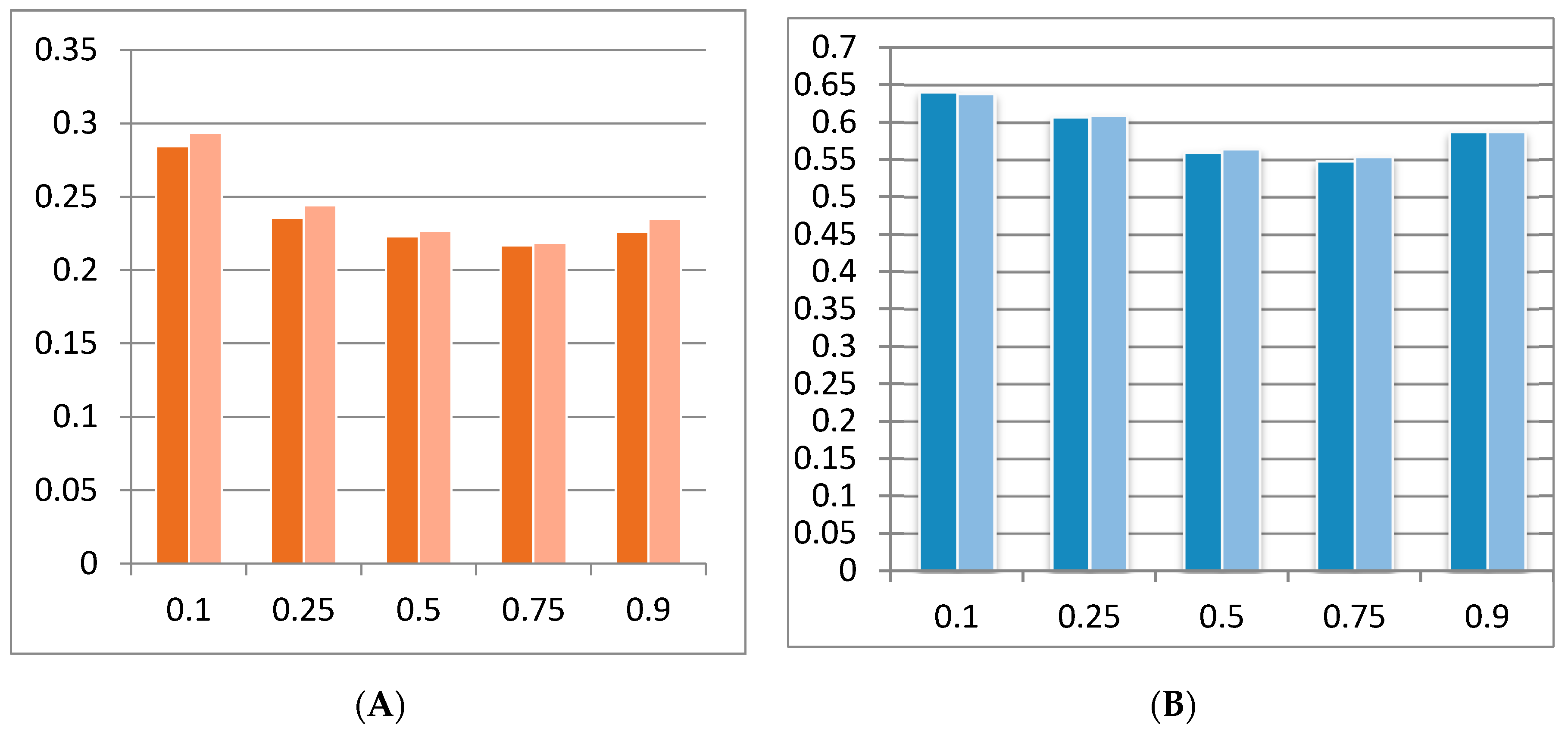

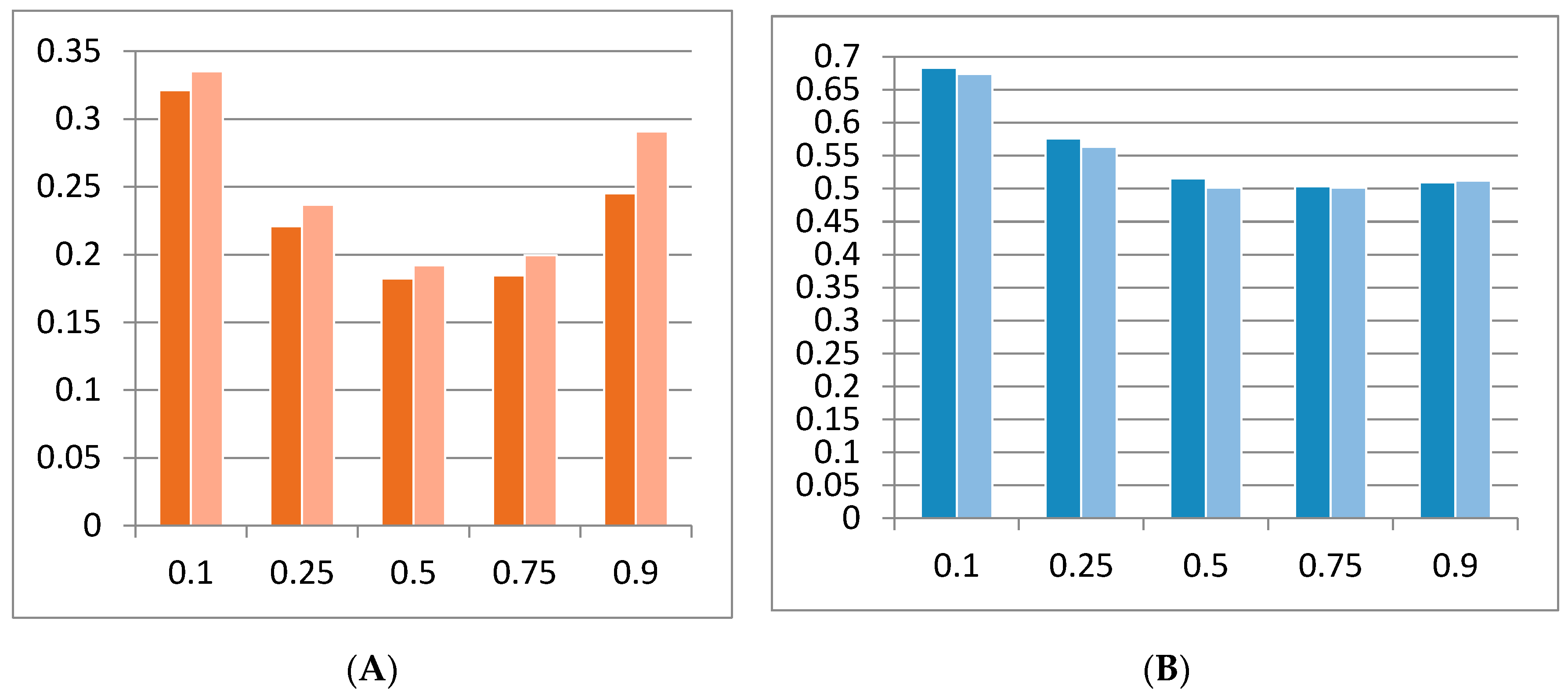

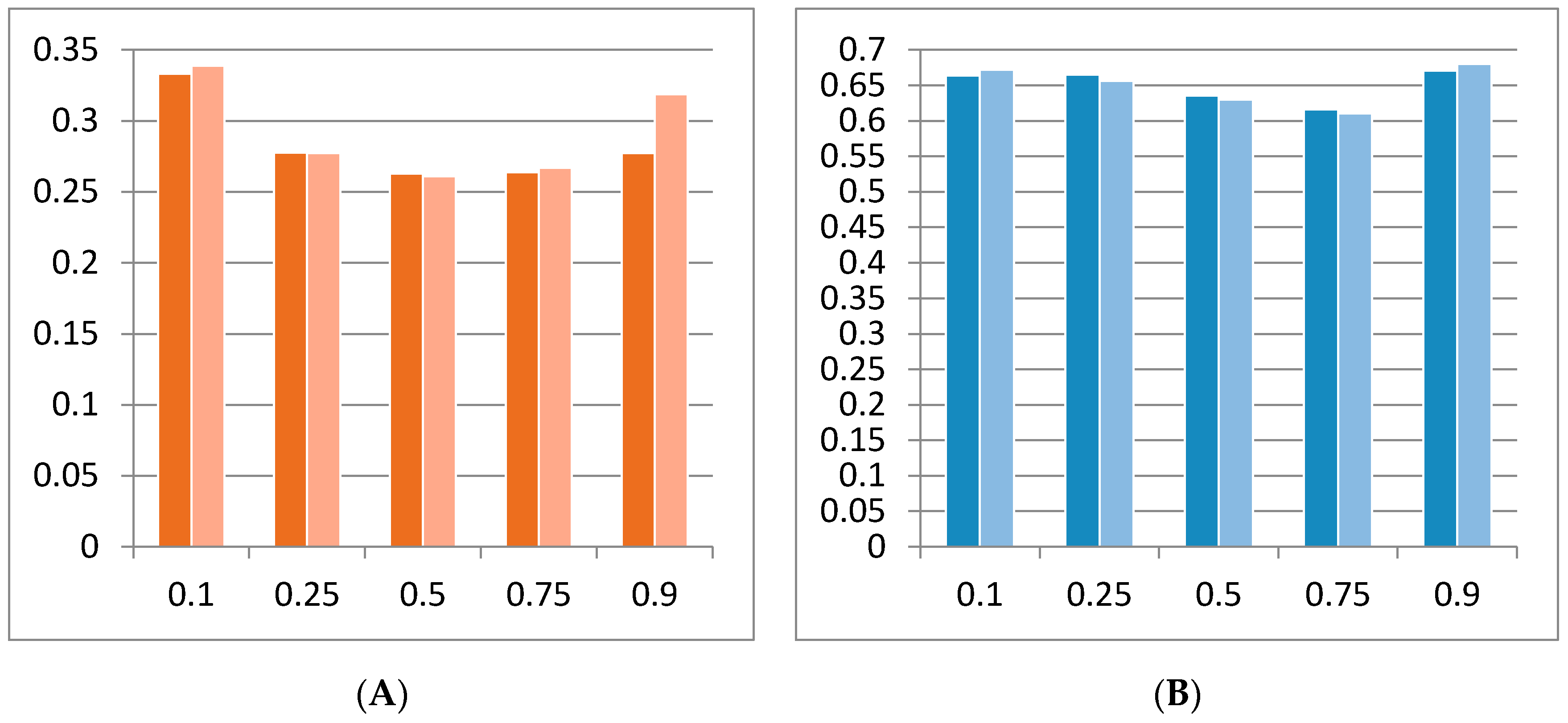

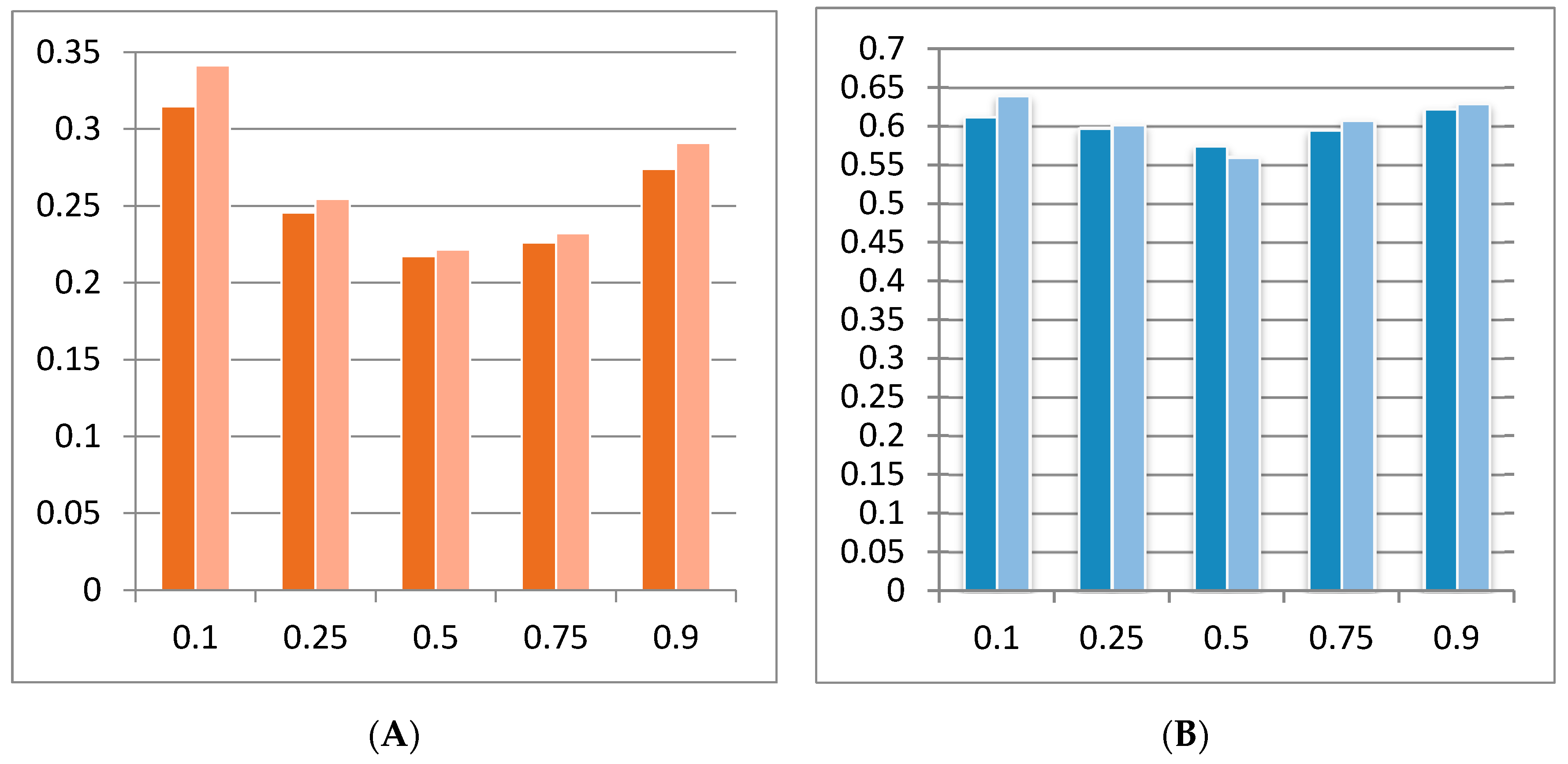

Finally, focusing on the explanatory power, we obtain several conclusions. First, the trend observed in all periods and subperiods has been corroborated, which consists of an evolution of the explanatory power in the U-shape as the value of theta increases in both models and in both mean and maximum adjusted

R2. Thus, these models have the greatest explanatory power in the extreme quantile and, specifically, in the lowest quantile, 0.1, in line with previous studies such as [

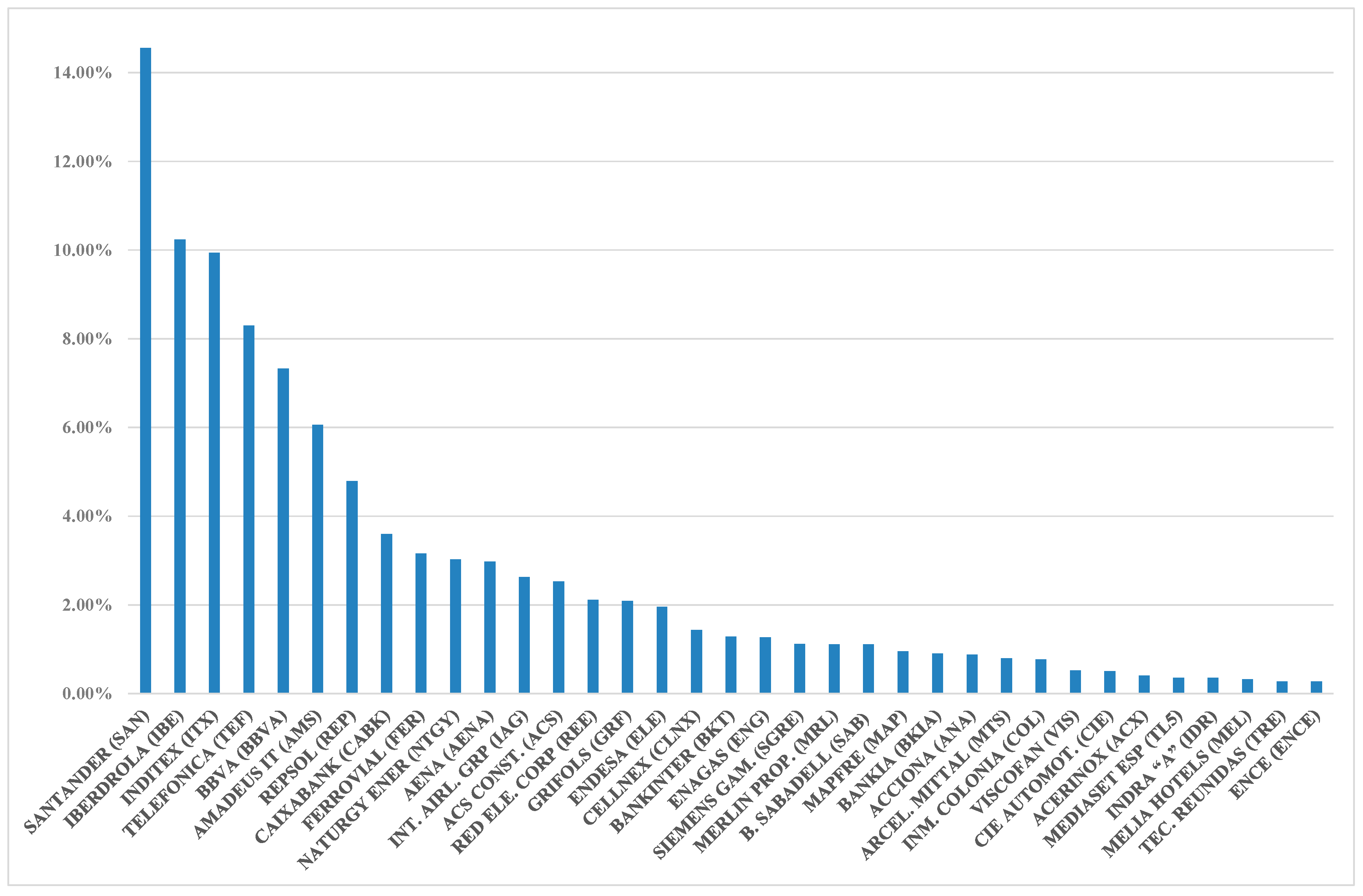

3]. Second, Model B explains the Spanish companies’ returns better than Model A does in the full period and in the three subsample periods. Third, BBVA has the maximum adjusted

R2 value in all periods, except for the postcrisis subperiod, where the maximum explanatory power corresponds to Santander. Thus, Models A and B best explain stock returns for companies that belong to the same banking sector. Fourth, the crisis subperiod is the economic stage with the highest values of this coefficient (adjusted

R2) in all of the quantiles. Therefore, the proposed factor models and, in particular, the second model, explain the variations in Spanish companies’ returns the best in crisis stages.

For all these reasons, we can justify the relevance of the QR approach when estimating the models proposed in the whole sample period and in the contrast of robustness proposed in this research. Both analyses have allowed us to study in depth the sensitivity of the Spanish companies’ returns to changes in the risk factors included in the proposed factor Models A and B based on the well-known Fama and French three- and five-factor models.

This methodology has allowed the detection of asymmetries in the behaviours and reactions of Spanish companies’ returns to changes in some explanatory factors across the quantiles in several (pre-, during and postcrisis) subperiods. Our null hypothesis has been accepted, confirming that the sensitivity of the Spanish companies’ returns to changes in the risk factors included in the proposed factor models are quantile- and stage-of-the-economy-dependent, reaching the greatest levels of explanatory power at the extreme quantiles.

Policy recommendations would consist of following the strategies implemented in companies that have reduced the negative consequences in times of financial crisis. Furthermore, a crucial implication for market participants would be that investors should consider the regime-dependent nature of the companies’ sensitivity to changes in the risk factors. Therefore, this suggestion would have implications for risk management and economic policy decisions, mainly during crisis periods.

Our research raises questions for further research regarding the sensitivity of Spanish companies’ stock returns to changes in relevant risk factors across the quantiles and in pre-, during and postcrisis scenarios. Our results confirm the different behaviours and reactions of Spanish companies in different stages of the economy and across the quantiles, but future studies on this topic should include analysis to detect sector patterns in terms of innovation profiles (proactive or reactive), debt levels, etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}