Symmetry Analysis of an Interest Rate Derivatives PDE Model in Financial Mathematics

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Governing Equation and Symmetry Analysis

3. Exact Invariant Solutions of Equation (5)

3.1. New Solutions via Group Point Transformations

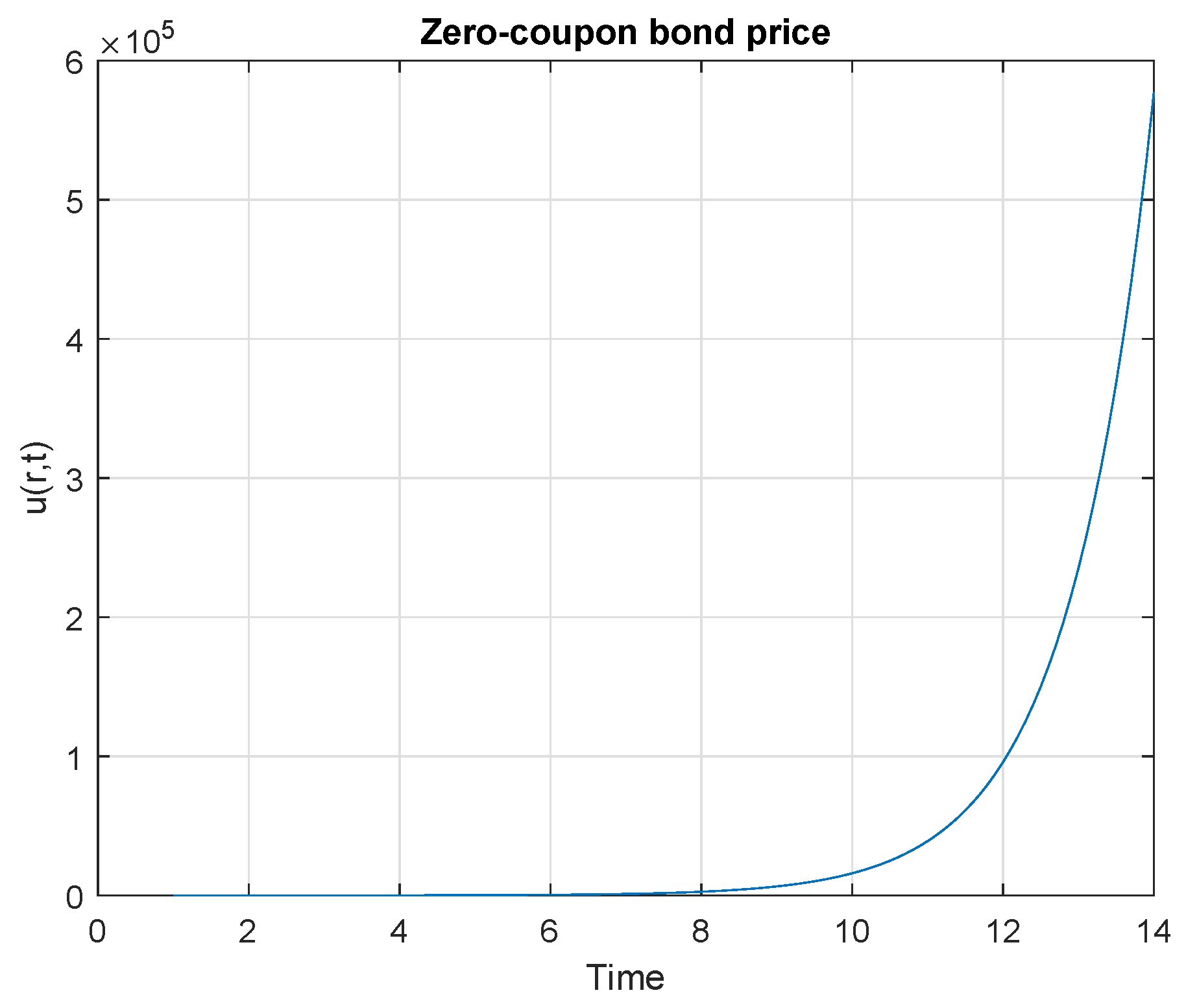

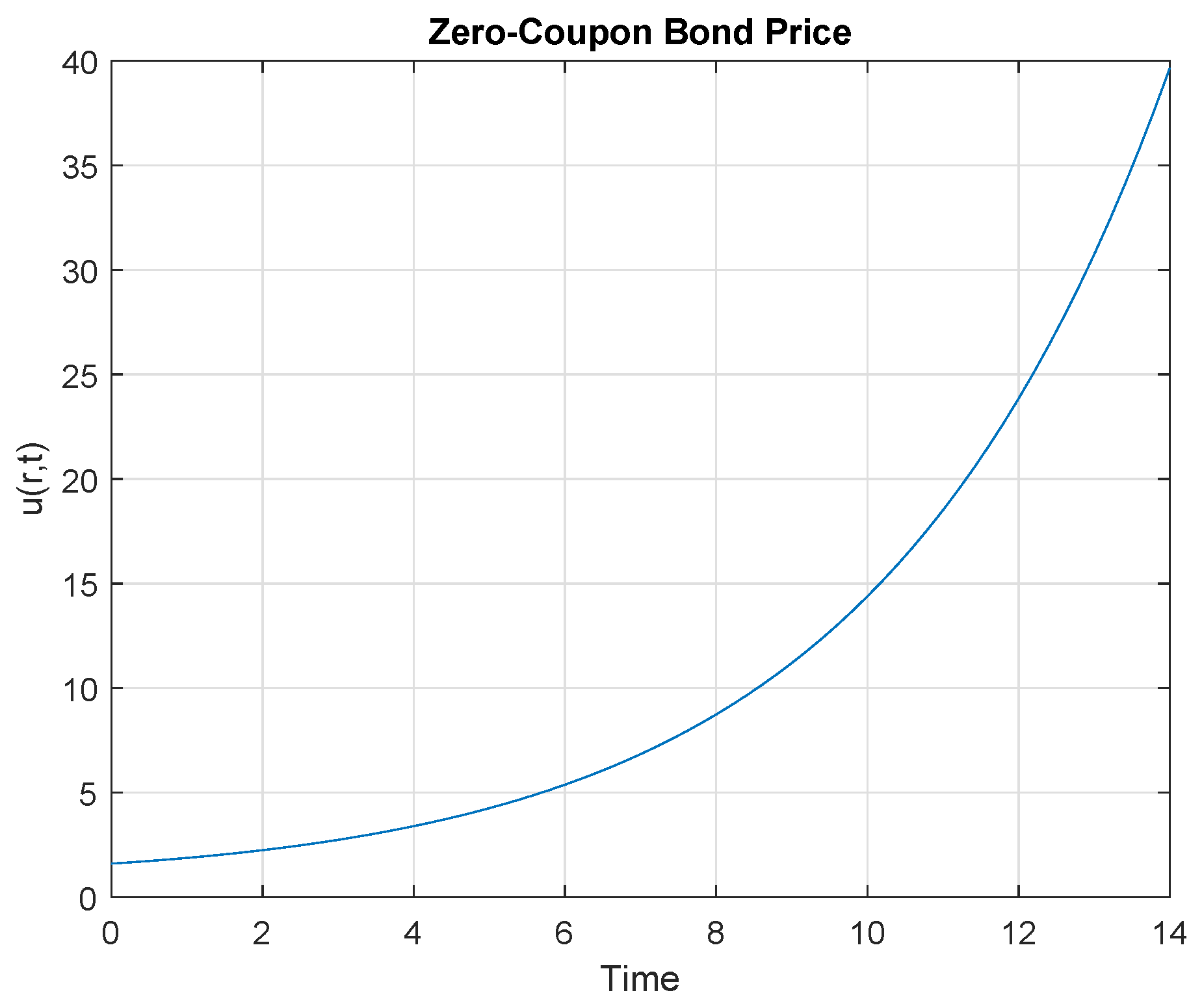

4. Results Discussion

- interest rate (risk-free) r = 0.90,

- volatility ,

- parameter ,

- parameter ,

- constant 1 ,

- constant 2 ,

- time to expiration T = 14 years.

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Vasicek, O. An equilibrium characterization of the term structure. J. Financ. Econ. 1973, 5, 177–188. [Google Scholar] [CrossRef]

- Cox, J.C.; Ingersoll, J.E.; Ross, S.A. An intertemporal general equilibrium model of asset prices. Econometrica 1985, 53, 363–384. [Google Scholar] [CrossRef]

- Wilmott, P.; Dewynne, J.; Howison, S. Option Pricing: Mathematical Models and Computation; Oxford Financial Press: Oxford, UK, 1994. [Google Scholar]

- Black, F.; Scholes, M. The Pricing of Options and Corporate Liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Merton, R.C. Theory of rational option pricing. Bel. J. Econ. Man. Sci. 1973, 4, 141–183. [Google Scholar] [CrossRef]

- Gazizov, R.K.; Ibragimov, N.H. Lie symmetry analysis of differential equations in finance. Nonlinear Dyn. 1998, 17, 387–407. [Google Scholar] [CrossRef]

- Goard, J. New solutions to the bond-pricing equation via Lie’s classical method. Math. Comput. Model. 2000, 32, 299–313. [Google Scholar] [CrossRef]

- Pooe, C.A.; Mohomed, F.M.; Soh, C.W. Fundamental solutions for zero-coupon bond pricing models. Nonlinear Dyn. 2004, 36, 69–76. [Google Scholar] [CrossRef]

- Sinkala, W.; Leach, P.G.L.; O’ Hara, J.G. Zero-coupon bond prices in the Vasicek and CIR models: Their computation as group-invariant solutions. Math. Methods Appl. Sci. 2008, 31, 665–678. [Google Scholar] [CrossRef]

- Khalique, C.M.; Motsepa, T. Lie symmetries, group-invariant solutions and conservation laws of the Vasicek pricing equation of mathematical finance. Phys. A Stat. Mech. Appl. 2018, 505, 871–879. [Google Scholar] [CrossRef]

- Luo, S.; Yan, J.; Zhang, Q. A functional transformation approach to interest rate modelling. In Stochastic Processes, Finance and Control: A Festschrift in Honor of Robert J Elliott; World Scientific: Hackensack, NJ, USA, 2012; pp. 303–315. [Google Scholar]

- Dimas, S.; Soubelis, D.T. SYM: A new symmetry—Finding package for Mathematica. In Proceedings of the 10th International Conference in Modern Group Analysis, Larnaca, Cyprus, 24–31 October 2004; Ibragimov, N.H., Sophocleous, C., Damianou, P.A., Eds.; University of Cyprus Press: Nicosia, Cyprus, 2005; pp. 64–70. [Google Scholar]

- Abramowitz, M.; Stegun, I.A. Handbook of Mathematical Functions; Dover Publication, INC: New York, NY, USA, 1972. [Google Scholar]

- Chern, I.L.; Financial Mathematics. Department of Mathematics, National Taiwan University and University of Hong Kong. Available online: http://www.math.ntu.edu.tw/~chern/notes/finance.pdf (accessed on 14 December 2017).

- Bodie, Z.; Kane, A.; Marcus, A. Investments, 5th ed.; McGraw-Hill Education: New York, NY, USA, 2003. [Google Scholar]

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kaibe, B.C.; O’Hara, J.G. Symmetry Analysis of an Interest Rate Derivatives PDE Model in Financial Mathematics. Symmetry 2019, 11, 1056. https://doi.org/10.3390/sym11081056

Kaibe BC, O’Hara JG. Symmetry Analysis of an Interest Rate Derivatives PDE Model in Financial Mathematics. Symmetry. 2019; 11(8):1056. https://doi.org/10.3390/sym11081056

Chicago/Turabian StyleKaibe, Bosiu C., and John G. O’Hara. 2019. "Symmetry Analysis of an Interest Rate Derivatives PDE Model in Financial Mathematics" Symmetry 11, no. 8: 1056. https://doi.org/10.3390/sym11081056

APA StyleKaibe, B. C., & O’Hara, J. G. (2019). Symmetry Analysis of an Interest Rate Derivatives PDE Model in Financial Mathematics. Symmetry, 11(8), 1056. https://doi.org/10.3390/sym11081056