Abstract

The global food market makes international players intrinsically connected through the flow of commodities, demand, production, and consumption. Local decisions, such as new economic policies or dietary shifts, can foster changes in coupled human–natural systems across long distances. Understanding the causes and effects of these changes is essential for agricultural-export countries, such as Brazil. Since 2000, Brazil has led the expansion of soybean planted area—19 million hectares, or 47.5% of the world’s increase. Soybean is among the major crop commodities traded globally. We use the telecoupling framework to analyze (i) the international trade dynamics between Brazil and China as the cause of the increased production of Brazilian soybean since 2000; (ii) and the cascading effects of the Sino-Brazilian telecoupled soybean system for Brazilian maize production and exports, with attention to consequences on domestic prices, availability, and risks associated with climatic extreme events. Census-based data at state and county levels, policy analysis, and interviews with producers and stakeholders guided our methodological approach. We identified that the Brazilian soybean production decreased maize single crop production and accelerated maize as a second crop following soybean, a practice that makes farmers more vulnerable to precipitation anomalies (e.g., rainfall shortage). In addition, the two-crop system of soybean/maize pressures the Brazilian maize market when unexpected events such as extreme droughts strike and when this results in a failed maize harvest in the second crop, most of which is for domestic consumption rather than export. Our study suggests the need to incorporate the telecoupling framework in land use decision-making and understanding landscape changes.

1. Introduction

International agricultural commodity trading trends have shaped the food production landscapes in recent years. From the 2000s, the volume of the world’s agricultural exports increased 60 percent [1], embracing many developing countries in South America and Asia into the international agricultural business [2]. The domestic pressure on food production in many countries has been “outsourced” to foreign countries. For instance, the arable land requirement for Brazil to feed its population did not show a significant increase [3], yet the expansion and intensification of agricultural lands during the past two decades led Brazil to be one of the world’s major food exporters. Meanwhile, China has become an important market for these food commodities [4]. The observed high rate of rural to urban migration fluxes in China [5] increases crop demand due to the change of population structure and consumption demand, especially for more livestock food sources [6].

These international flows of agricultural commodities have impacts on many aspects of both importing and exporting countries, including land-use changes, deforestation, biodiversity loss, economic growth and inequalities, social effects (i.e., displacement of smallholders, livelihood improvement in producing regions), and food security [2,7]. Among the many processes, cascading effects are particularly important, but have rarely been addressed due to the lack of efficient tools or adequate frameworks [8,9]. For example, although substituting gasoline with biofuels can reduce greenhouse gas emissions, it drives up the price of biofuels, which contribute to the conversion of native vegetation and pasturelands to new cropland worldwide [10,11], a phenomenon known as indirect land use change [12,13]. Cascading effects, in the case of this study, are chain events caused by the trade of one crop from one country to another country affecting other components (e.g., another crop or ecosystem) in the sending system; however, cascading effects also exist outside the sending system. There are few studies that investigate cascading effects caused by the international trade of food commodities [8].

In this article, we address the question, ‘What are the cascading effects of a telecoupled food-system on the sending system’s food markets and production?’. Under the telecoupling approach (i.e., socioeconomic and environmental interactions over distances [9]), we use soybean trading between Brazil and China as an example to understand cascading effects on the Brazilian agricultural system (i.e., maize production and trade). The telecoupling framework, a new systems integration approach, is a logical extension of research on coupled human and natural systems [9] in which interaction occurs not just within particular geographic locations, but also addresses globalized, long-distance and cross-scale system interactions. Among the major crop commodities, soybean is one of the most important traded globally. Its global production increased 61% between 2000 and 2014 [14]. The major players in soybean trading include China as the major importer that pushed Brazil to become the largest exporter, together with the U.S., in the 2010s [15]; an international trade that, since the 2000s, has become economically important to Brazilian agribusiness and for socioeconomic changes [7,15].

By following the flows of soybean in the telecoupling framework, we can systematically examine the soybean exports and production dynamics, and bring awareness to the maize production as a second-crop that emerged in Brazil (i.e., crop rotation with soybean as primary, and maize following the soybean as a second-crop, two crops year-round); particularly, the associated risk with this strategy. In this article, we analyze the cascading effects of the Brazil and China telecoupled soybean system on the Brazilian maize exports and production system, and its consequences on the domestic prices and availability of maize.

2. Materials and Methods

We address soybean trading between China and Brazil to demonstrate the cascading effect on maize, using the telecoupling framework as a methodological approach.

2.1. Telecoupling Framework and the Telecouled Soybean System

To understand environmental and socioeconomic sustainability, an integrated analysis of the interactions between the environmental and socioeconomic dimensions across multiple coupled human and natural systems is required [16]. The telecoupling framework is used to analyze such interactions between Brazil and China [9,16]. The components of the telecoupling soybean system are presented in Table 1. The receiving system represents the region where the flows converge, while the sending system is the one where the flows come from [9]. Among the soybean import and export flows between China and Brazil, China is the receiving system, while Brazil is the sending system, given its role as a soybean exporter to China.

Table 1.

The five components of the Brazil and China telecoupled soybean system.

2.2. Research Area and Data

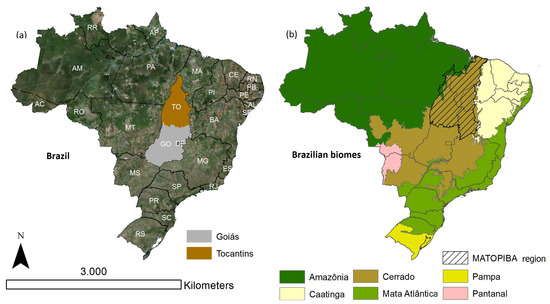

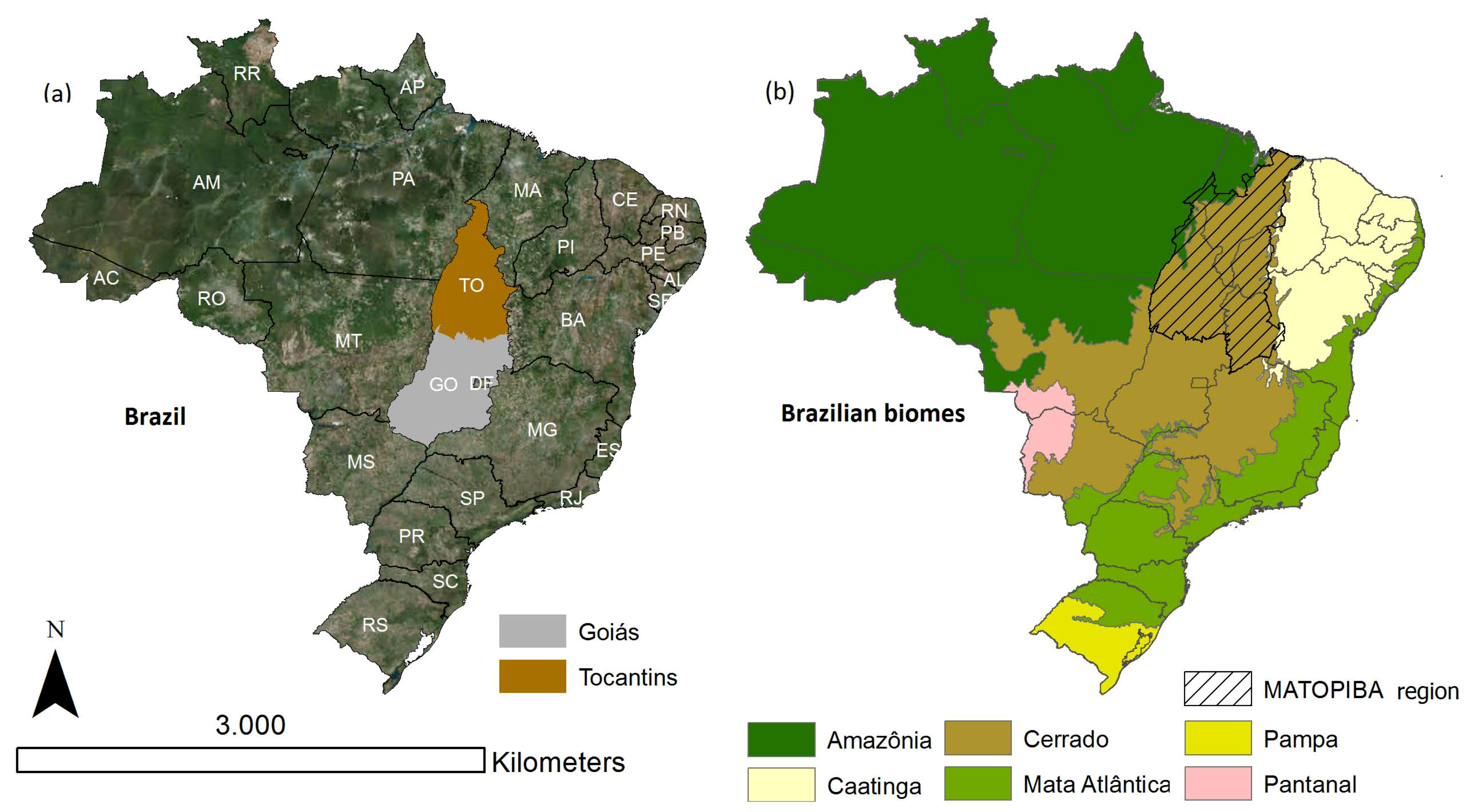

We compiled a historical multisource dataset (Table 2) from government agencies and research institutes in the two systems: the sending system (Brazil) and receiving system (China). Given the Brazilian agricultural land-change history, this research developed a multi-level analysis from the country to the region including two soybean producer states in the Cerrado: Goiás in the Central-West and Tocantins in the North (Figure 1a). The latter is also part of the recent so-called region of MATOPIBA, which includes portions of the States of Maranhão, Tocantins, Piauí, and Bahia). The vast majority of both the states of Goiás and Tocantins is located within the Cerrado biome (Figure 1b).

Table 2.

Data used in this study.

Figure 1.

The Brazilian maps highlight: (a) the two States where fieldwork and other data analyses were conducted; (b) the biomes distribution over the territory, and the Maranhão, Tocantins, Piauí, and Bahia (MATOPIBA) region.

These two states have developed soybean production in different periods of the agricultural history; Goiás since the 1970s, and Tocantins in the 2000s. Thus, comparing these two realities contributed to understanding the telecoupled consequences of the international market of food commodities (i.e., export flows from Brazil and import flows of China) over the agricultural system (e.g., producer regions, land change, two-crop non-tillage system). Goiás is an established producer state with a well-developed two-crop non-tillage system (i.e., mainly soybean and maize). More than thirty years of large-scale grain production, high internal demand of grain by the food and feed processing industry, and China as the major soybean buyer are characteristics of the system. Tocantins has developed as a soybean producer since the 2000s in a different global context, pushed primarily by the international rather than by the internal demand. It followed a similar land management system as Goiás, but fewer producers adopted the two-crop non-tillage system with soybean and maize. Tocantins is a region of cropland expansion and also has China as its major soybean buyer. Both states have pasturelands as their major land use, and Goiás has the second largest sugarcane planted area after São Paulo state, which eventually has replaced soybean planted areas in recent years [17].

Tocantins still has 72% of its territory covered by native vegetation in the portion within the Cerrado biome (which accounts for 91% of the State’s territory), while Goiás has 41% [18]. While Goiás has well-developed industry and service sectors and a total population of 6.5 million inhabitants [19], Tocantins is an emerging economy in Brazil with a high dependency on agribusiness and a population of 1.38 million inhabitants [19]. The multi-level analysis allows a comprehensive perspective of the sending system, which is key to understanding its heterogeneity and similarities, as well as identifying the extent of causes and their cascading effects.

Between 22 June and 12 August 2016, we conducted fieldwork in the states of Tocantins and Goiás to collect qualitative data for the study of soybean and maize production systems, market and supply chains. Fieldwork included thirteen interviews with farmers (seven from Tocantins, six from Goiás), seventeen interviews with representatives of the soybean and maize producers and government agencies, and attendance at a meeting with agribusiness consultants in the well-developed agricultural region of Cristalina, state of Goiás. Using a semi-structured questionnaire, we considered farmers’ stories about the soybean and maize production systems, future scenarios, incentives for production and how farmers behave according to price and market demands.

To approach the interviewees, we previously set up appointments in the national capital of Brasília with the Brazilian Agricultural Research Corporation (Embrapa), Soy and Maize Producers Association (Aprosoja Brazil) and with the National Company of Food and Supply (Conab). Then, using a snowball sampling approach [20], we reached out to State groups, like Aprosoja Tocantins and Aprosoja Goiás, as well as the Agricultural Confederation of each State and other State agencies. Finally, we reached soybean farmers in both states.

3. Brazil and China Telecoupled Soybean System

This section presents the main policies and historic events in China which boosted its internal demand of soybean and placed the country as the major soybean buyer in the world. Consequently, Brazil, already engaged in soybean production for internal demand and diffuse international markets, boosted its planted area expansion and production to achieve a competitive position in the emergent soybean international market, driven by the Chinese demand.

3.1. The Dynamics of Chinese Soybean Imports: Receiving System

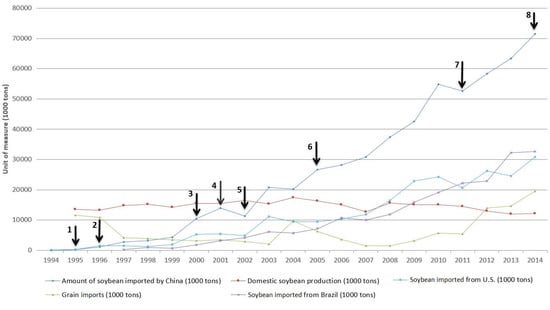

China has been the country purchasing the majority of Brazil’s soybean exports (over 50%) since 2009 [21]. Based on the trading amount and its increasing rate, the soybean import trend of China was divided into three periods: before 2000, between 2000 and 2004, and after 2005. Figure 2 displays the dynamics of soybean imported and domestically produced in China.

Figure 2.

China’s soybean production and import, and critical time points. Each arrow in the figure highlights a key event in the Chinese policy or economy with impact on soybean imports (see text for details). Data source: [22,23].

Being a net soybean exporter until 1993, China started to import soybean in a large scale in 1995 (arrow 1, Figure 2). The Chinese government adjusted the soybean importing policies due to the low yield in 1995 and 1996: the regular tariff for import was 180%, the discount tariff was 40%; however, the tariff, if within quota, was only 3% [24,25] (arrow 2, Figure 2). China’s imports of soybean reached 4.3 million tons in 1999, which was only a third of that year’s domestic production, but 86 times its import quantity in 1995.

A chain of events that placed China in the soybean import pathway marks the beginning of the twenty-first century. The cancellation of a quota limitation in 2000 (arrow 3, Figure 2) and China joining the World Trade Organization (WTO) in 2001 (arrow 4, Figure 2) stimulated the import of soybean to a historical level, when the import (13.9 million tons) almost matched China’s domestic production (15.4 million tons) for the first time. The promulgation of the management mode policy and regulations of genetically modified (GM) food by the Ministry of Agriculture in China in 2002 caused a pause in soybean trade between China and U.S. for a short period [26] (arrow 5, Figure 2). A similar fluctuation happened again in 2003 and 2004; however, the imported soybean amount still reached 26.6 million tons in 2005 (arrow 6, Figure 2), which was also the first time that China became the top country in soybean imports and exceeded the total amount of the countries in second and third places (i.e., the Netherlands and Spain).

China soybean imports have grown almost threefold (i.e., from 28.2 million tons to 71.4 million tons) from 2006 to 2014, with an annual average increase of 5.4 million tons. The annual growth itself is four times Tocantins’ total soybean production in 2014; in other words, 6% of Tocantins’ land would have to be converted to soybean to fulfill this demand increase every year (based on a yield of 3.03 tons per hectare). Despite soybean being a traditional crop, many Chinese farmers have lost motivation to grow soybean due to lower competition capacity in price and government policy incentives that favor maize cultivation in China.

Joining WTO opened China to international agricultural trading; however, only soybean growth is exponential. The monetary value of primary products imported by China increased 26 times from 24,417 million dollars in 1995 to 646,939 million dollars in 2014 [27]. The increase of soybean amount, however, was 243 times during the same period. The other grains imported by China (i.e., wheat, rice, maize) do not come close to the increases seen for soybean (i.e., from 11.6 million tons in 1994 to 19.5 million tons in 2014) and with a standard deviation of up to 5 million tons every year.

The annual growth in the absolute quantity of China’s imports increased from 853 thousand tons in the period of 1994–1999 to 4.97 million tons in 2005–2014, which is an almost six fold increase. The exports from the U.S. to China have a similar pattern, as the annual growth rate increased from 370 tons in the first period (1994–1999) to 2.37 million tons in the third period (2005–2014). Nevertheless, China has been increasing its soybean imports from Brazil, with an annual growth rate in the third period (2005–2014) 22 times bigger than the previous one, or about 124 thousand tons per year during 1994–1999. Gradually, Brazil matched the dominance of the U.S. in China’s soybean imports. In 2014 (arrow 8, Figure 2), the share of Brazil and the U.S. in China’s soybean market were similar, or 45.7% and 43.1%, respectively.

The decline of China’s total soybean imports after 2005 happened in 2011 (arrow 7, Figure 2), with a reduction of 2.1 million tons largely caused by the reduction (3.6 million tons compared to the previous year) from the U.S. To stabilize the trading, the U.S. and China signed a purchase contract of 8.6 million tons of soybean during an Agricultural Symposium in 2012. Over the years, there is no negative oscillation in the Brazil–China soybean trading volume compared to the U.S–China trading pattern.

First grown in China, soybean has always been one of the major crops in the country. Domestically produced soybean is directly destined for human consumption, which counts for approximately 80% of the total production. However, the low competition capacity of Chinese soybean (e.g., small farming scale) drives a reduction of total planted area and production. The shrinking domestic production combining with the increasing demand represents a growing opportunity in the international market.

The Dietary Habit Change Driving the Increase in Soybean Demand

Soybean can be used in many ways, including direct consumption (i.e., tofu, soy milk, and bean sprouts), and “crushed” products (i.e., soybean meal and soybean oil). The majority of soybean imported from Brazil and U.S. are used for extracting soybean meal as feedstock for swine, poultry, and cattle, to meet the shift in dietary habits among Chinese citizens [28]. Besides the population growth, China has experienced an explosive growth of the middle-class and associated purchasing power in the past decades [29], which has caused a notable shift in dietary habits, favoring meat, milk, and egg products. The consumption of beef and poultry in China has doubled, 2.14 times and 1.85 times, respectively, during the period of 1994–2014. The growth average worldwide, in the same period, was only 1.48 and 1.03-fold. The average consumption per capita per day in China of both poultry and beef in 2014 is still lower than in the world generally (Table 3). The daily per capita consumption of pork has increased from 73 g in 1994 to 115 g in 2014, while the world average increased from 40 g to 42 g (Table 3). This is largely affected by the Chinese average, as this number will be reduced from 28.2 in 1994 to 27.1 in 2014 when excluding China. The total meat consumption in China is 155 g per capita per day, which is still much lower than developed countries (i.e., 262 g per capita per day), but it is beyond the recommended quantity by health organizations [30] and it will become substantial when multiplied by the number of the Chinese population.

Table 3.

Daily per capita meat consumption and its changes, China and world average. Data source: [31,32].

Using the average food conversion rate for poultry, beef, and swine [33], as well as the crush percentage from soybean to soybean meal (i.e., 80%), approximately 366.2 million tons of soybean were demanded to raise animals for Chinese consumers in 2014, 171.9 million tons more compared to 1994 (Table 4). This amount of soybean was almost the entire production imported from both the U.S. (106.8 million tons) and Brazil (86.12 million tons) in 2014. By 2022, an additional 8% of the urban population will enter the middle class compared to the 68% in 2012 [29]. The USDA projects a 30% increase in swine, poultry, and beef consumption in China in 2024, which enables an expanding market of soybean and other grains.

Table 4.

Increasing demand for soybean based on meat consumption in China. Data source: [31,32].

3.2. The Dynamics of Brazilian Soybean Exports: Sending System

Brazilian large-scale agriculture and livestock production are economic activities developed through the modernization of traditional practices, including the adoption of mechanization, fertilizers, biological nitrogen fixation, and the non-tillage system, and has attracted the development of an industrial chain to support the needs of this economic activity [34]. Focusing on production for local and international markets, the soybean expansion in Brazil followed the South to North pathway, beginning in the States of Rio Grande do Sul (Pampa biome) and Paraná (Atlantic forest biome) in the 1910s. Since the 1970s, soybean fields expanded to the Central-Western region of Brazil (Cerrado and Amazon biomes) [7]. After the 1980s, the Cerrado was consolidated as the modern agricultural frontier (i.e., high productivity, large-scale farming) [35]. Finally, the soybean expanded to specific portions of the Amazon region in the 1990s and more recently, efforts were made to develop the MATOPIBA region within the Cerrado biome [36]. The soybean planted area of 2015 in Brazil accounted for 32.2 million hectares, 3.8% of the country´s territory.

The hardening of export rules in the U.S. during the 1970s, after a shortage of soybean stocks for internal consumption, provided an opportunity for the emerging Brazil soybean exports, which quickly found a growing niche in both Europe and Asia [15].

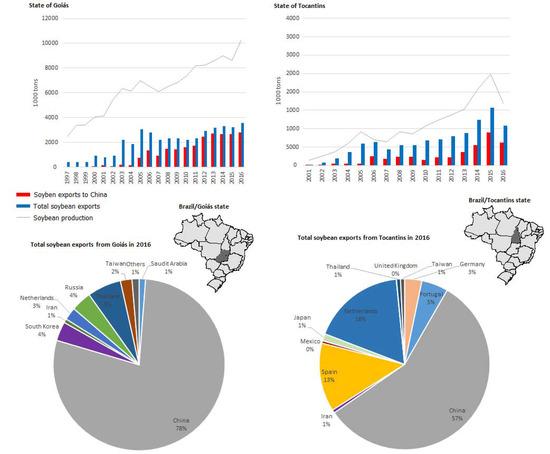

The state of Tocantins, a newer soybean-producing region with around fifteen years of continuous expansion, has demonstrated the impact of the international market in the region. The production increased 1668% between 2000 and 2015, from 138 thousand tons to 2.45 million tons. The gross production value (GPV) of soybean in Tocantins was of 631 million US Dollars in 2015, 205% higher than in 2005—the soybean GPV of 2015 represented 71% of the total GPV for the agricultural production of Tocantins. This increase in soybean production and value added is the result of an increase in the Chinese demand for soybean, according to local producers interviewed during fieldwork in 2016. In 2015, 64% of the total soybean produced in Tocantins was exported (in natura), 36% only to China (890 thousand tons) and 28% to many other countries (e.g., Spain) (Figure 3).

Figure 3.

Export destinations of soybean produced in Goiás and Tocantins, Brazil (AGROSTAT, Supplementary Material S1).

Soybean comprise 38% of the rural economy of Tocantins and play an important role in the state’s finances. This dynamic development attracted the attention of the commodity traders, and the largest commodity trading companies have already built storage facilities and commercial offices in the state. The stakeholders interviewed during fieldwork argued that the soybean business boosts local development and is pushing the modernization of logistics in the region. Soybean producer regions have benefited from improvements in local transportation, health and education infrastructure; however, these have not been translated to better income distribution [7]. Despite the economic importance to the state of Tocantins, only a minimum portion of the grain is industrialized (aggregating more value to the state’s internal production chain). In the state of Goiás, around 37% is exported (Figure 3), remaining as an important fraction of the total production to the state’s internal demand. Goiás has a better-developed industrial chain to transform the soybean into animal feed and other products, which aggregates more value to the state’s revenues.

As an agricultural commodity exporter [8], Brazil increased 378% the soybean planted area between 1977 and 2016, with a 65% increase in productivity (i.e., production per hectare) [37]. However, from 1977 to 2000, soybean planted area increased 96% with 57% of an increase in productivity, while in the period after (2000–2016), the planted area increased 144% with only 9% of gains in productivity [37]. The second period (2000–2016) is when China became the major soybean importer. Brazil is leading the soybean planted area expansion with 19 million hectares since 2000, or 47.5% of the world’s increase—i.e., 40 million hectares [38]. The increase in productivity was key to maximize the farmers’ profits and represent the main target of farmers in agricultural consolidated areas such as Goiás, given the higher land prices and lower land availability in traditional producer regions within the state, according to local producers interviewed during fieldwork. Since 2000, when Goiás started the soybean exports to China (Figure 3), the cropland increased 113% until 2016 with 15% gains in productivity [37]. During the previous period (1977–2000), the State increased its planted area by 2164% with a 104 % increase in productivity [37]. Meanwhile, Tocantins experienced a 1219% of soybean cropland expansion since 2000 with productivity gains around 38% [37]. Before 2000 (1987–2000), Tocantins experienced an increase of soybean planted area of 135% with productivity around 25% [37]. According to the observations during fieldwork and from the famers´ personal communications, the competitive land prices and high land availability in Tocantins offer opportunities to new farmers which are not possible in older agricultural frontiers. In Goiás, farmers are focusing on maximizing profits, keeping high standards of soybean productivity, and investing (capital and technology) in maize as the second-crop. In Tocantins, farmers are investing in soybean planted area expansion and productivity gains with less focus on the second-crop. There, farmers commonly adopt a less expensive crop (e.g., millet) following the soybean harvest mainly to cover the soil, to produce organic matter, and to keep soil humidity until the next season.

In Goiás, the period of 1977–2000 reveals the modernization era of tropical agriculture in the Cerrado biome, given the expressive gains in productivity and planted area. This era was boosted by Federal Government development programs (e.g., POLOCENTRO—Program of Cerrado Development), and by the role of regional public research agencies, as the Agricultural Research Corporation of Goiás (EMGOPA) and the Center for Agricultural Research in the Cerrado (Embrapa). The success of soybean in the region promoted economic development, increases in farmers’ profitability, which further stimulated the soybean expansion. Tocantins in recent years (2000–2016) represents a soybean production dynamic similar to Goiás between 1977 and 2000. However, the adoption of well-developed soybean varieties, management techniques, and the support of seed and agro-chemical input companies, assured better productivity to Tocantins since 2000 (2100 kg per hectare). Thus, Tocantins had the higher national rates of increase in soybean planted area (since 2000) with productivity gains less than the observed for Goiás, or even Brazil, during the period of soybean expansion in the decades from the 1970s to the 1990s.

4. Cascading Effects on the Agricultural System and the Internal Market in the Sending Country

Brazilian agribusiness has contributed to the gross domestic product over the last decade. In 2015, the sector contributed 46% (88 billion US dollars) of the total exports and 7% (13 billion US dollars) of the total imports, a positive commercial balance of 75 billion US dollars [39]. However, sudden export outbreaks, given the importer’s currency appreciation, may lead the exporter country to face impacts in the internal market supply [40]. Planted areas for commodity production may also convert existing agricultural lands used for staple food, important for domestic market consumption and regulation [2]. The cascading effects are often nonlinear, and sometimes they take time to appear (e.g., time lag effects) after the telecoupled flows are initiated [9,41,42].

4.1. Soybean and Maize: Two Crops, One System

When planted in a double crop system, maize production in Brazil is strongly connected to soybean production through the supply chain, logistics, producer regions and farmers. The soybean and maize markets in Brazil have interactions regarding land use (supply) or by the complementary demand of animal feed [43], which creates an interdependent system where the soybean market affects the maize exports and price [44]. The primary interest in soybean production, the infrastructure and logistics developed for the soybean and the second-crop harvest—between June and September in the Cerrado biome, unique among the main maize producers—facilitated the international market pathway for this commodity. These important causes emerged from the telecoupled soybean system that is leading to cascading effects over maize production and markets in Brazil. The transportation costs in Brazil vary from the coastal producer regions (i.e. closer to ports) to inner continent regions, with the highest costs in the inner continent with poor road and railroad infrastructure [45]. Thus, for the maize production in Goiás and Tocantins, the logistics developed for soybean have benefitted maize exports in favorable windows of international prices when the devaluation of the Brazilian currency increases the competitiveness of the Brazilian grain. The maize harvest season also increased the importance of the Brazilian maize in the international fluxes of commodities, given its availability out of the harvest season in China and U.S., between September and October. For producers, this market dynamic encouraged the development of a risky agronomic activity [46].

4.2. Maize Planted Area and Maize as the Second-Crop

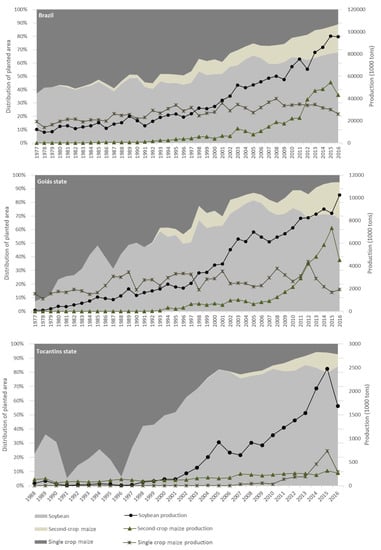

In 1998, the soybean cropland in Brazil surpassed the maize planted area (Figure 4). In 2011, maize planted area in the second-crop (i.e., following the soybean in the non-tillage double crop system, two crops year round) surpassed the maize single crop area (i.e., one single crop of maize year round). Soybean replaced the most suitable maize areas, and maize farmers (commercial scale) moved to soybean production [47]. Over a period of 25 years (1990–2015), the agricultural crop area in Brazil, discounting maize (single crop and second-crop) and soybean planted areas, increased 3.7%; however, maize single crop decreased 47%, and soybean and maize second-crop increased 178% and 174%, respectively [48]. Given the context of the Brazilian cropland expansion, the soybean expansion features as the main driver to the decrease of the maize single crop planted area and its displacement to second-crop status.

Figure 4.

The graphics represent land-use changes from the one-crop system of predominantly maize (maize single crop), to the two-crop system of soybean and maize as the second-crop. The left axis shows the proportion (colored area) and the right axis shows the absolute production (lines) (Conab, Supplementary Material S2).

Decomposing the expansion dynamics of maize into two periods, before the exports to China (1990–2000) and after (as in the Section 3.2 for the Brazilian soybean), the maize single crop decreased 18% (or 1724 thousand hectares) in the first period and it decreased 37% (or 3707 thousand hectares) between 2000–2015 [49]. In these periods, the second-crop maize increased by 2389 thousand hectares and 6642 thousand hectares, respectively [49]. During the expansion of soybean in Brazil, the soybean production replaced maize single-crop given the global demand and prices for soybean; a very different situation to the maize focused on internal markets and traded with less competitive prices than soybean. The soybean price and the projections of future markets defined by the Chicago Board of Trade (CBOT) keep a relatively stable market for the soybean with higher prices than maize, which increases the confidence in the soybean production chain (e.g., traders and producers). These are characteristics of the soybean market that pushed the Brazilian first-crop to soybean, conditioning the major maize production to the second-crop.

The internal demand for maize production, its use as a food source, animal feed and, more recently, for exports, pushed the development of short-cycle soybean varieties (maturing in 90–95 days) to permit a second-crop. Given the short-cycle varieties, farmers produce maize as the second-crop in a tight window (planting date between the middle of January to the middle of February, on average). The soybean production directly influenced the productivity increase of maize, given the incentives and technologies applied into the soybean production chain [43].

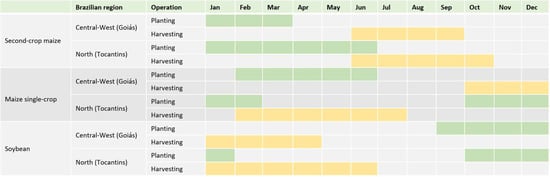

In Goiás and Tocantins, maize second-crop planting starts in January, before the rainfall starts to diminish in April, increasing the likelihood of water shortage during weeks or months when the crop is vulnerable to droughts and high temperatures. Nonetheless, due to Brazil’s size, this agricultural practice has different planting and harvesting periods among producer regions. Figure 5 presents usual dates for planting and harvesting soybean and maize in Goiás and Tocantins. Second-crop is considered to be a riskier agronomic activity given the climatic extreme events (e.g., precipitation anomalies) associated with the shortage (amount of water) and regularity (frequency) of rainfall during the second-crop growing season [50,51]. During the period associated with the second-crop (Figure 5), according to the interviewed farmers, the rainfall tends to diminish in amount and frequency compared to the period of growing soybean, putting maize production in a less favorable growing season. However, farmers consider second-crop maize to be a feasible practice in response to historical reasonable rainfall. From 2000 to 2015, the Brazilian productivity of this second-crop increased twofold (from 2661 kg per hectare to 5761 kg per hectare). In 2016, farmers’ confidence level was shaken up for the first time, especially in major producing regions located in Central-Western Brazil (e.g., Goiás). El Niño-related events (i.e., decrease and abnormal distribution in rainfall during the second crop) resulted in drastic losses of 30% in productivity and 22% in production (Figure 4). Together with the increase of production costs for the second-crop, the financial damage for farmers became a matter for serious concern.

Figure 5.

Planting (represented in green) and harvesting (represented in yellow) periods for soybean and maize in Central-West and North regions of Brazil (Adapted from the “Calendário de Plantio 2015” of the Brazilian Ministry of Agriculture).

4.3. International Prices and Market Effects on Internal Feedbacks in the Sending Country

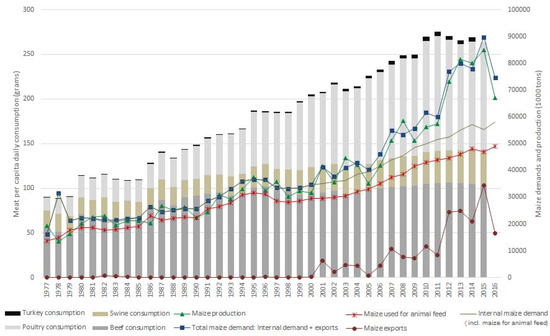

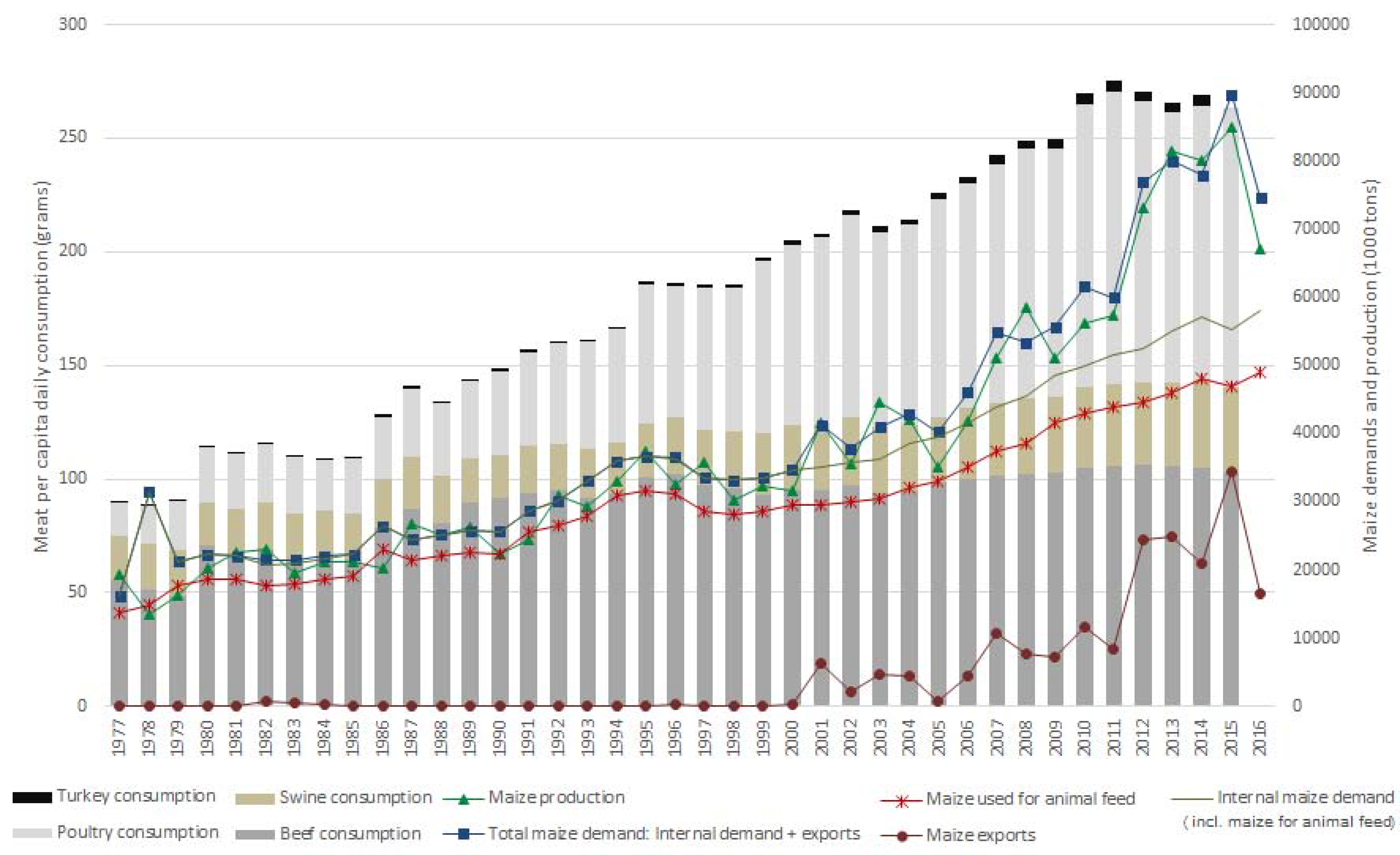

The Brazilian dietary change since the 1970s to 2010s included an increase of meat consumption (Figure 6), which fostered the national demand for maize-based animal feed, mainly for poultry. The production of animal feed demanded around 87% of the internal maize production between 1977 and 2005, but a different share was observed between 2006 and 2016: around 67%. During this period, the maize exports increased from 10% to 24% of the total Brazilian production, reaching a peak in 2015 of around 40% (Figure 6). Only in 2008, 2013 and 2014 did Brazil produce more maize than the national demand (including maize for exports), putting pressure on the national stocks. Based on agribusiness projections for 2024 [52], the Brazilian internal maize consumption will reach 64 million tons in 2024; exports may reach 33 million tons, less than the 34 million tons exported in 2015, and the production will increase 32%, reaching 102 million tons. These historical data and projections highlight the tight production of maize in Brazil in the face of the country’s internal demand and for exports, creating a competitive scenario of maize demand between the export sector and the Brazilian animal production industry. In this scenario, price fluctuations, international demand, and weak governance over the internal market supply may lead the sending country to face a sudden lower availability of grain and high prices in the internal market.

Figure 6.

Brazilian national statistics for meat consumption and maize demand by the country’s internal demand and for exports (USDA, Supplementary Material S3).

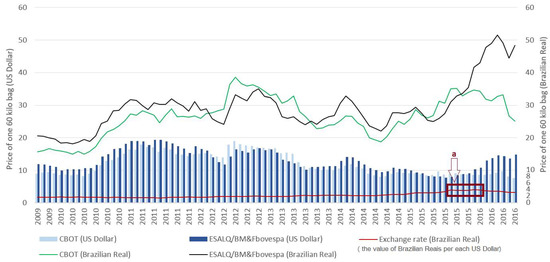

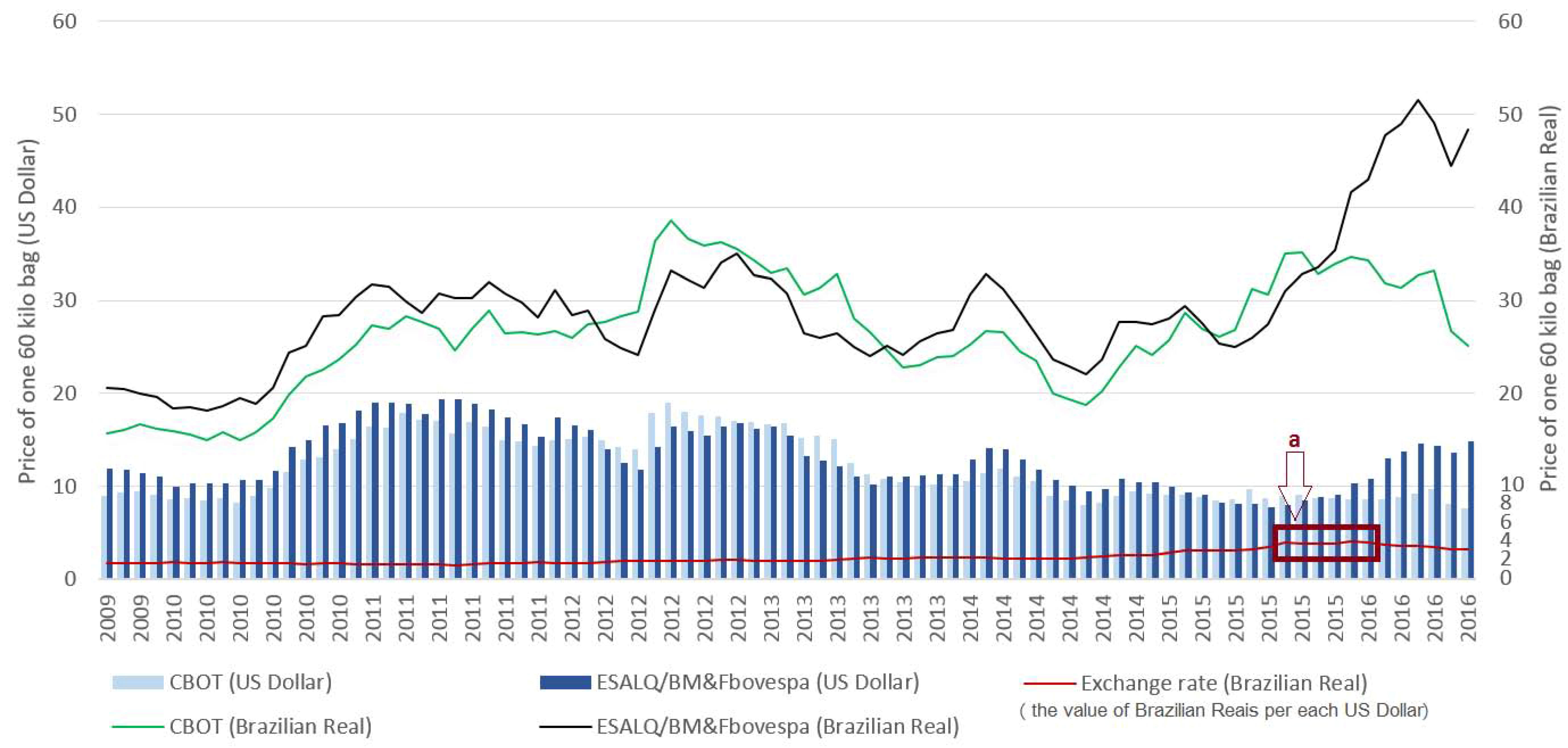

The recent valorization of the US dollar made Brazilian exports more competitive in the global market [53] and stimulated the international trade of maize, given its higher profitability when compared to the prices in the internal market. Abrupt import outbreaks induced by the devaluation of the exporter’s currency or by the valorization of the importer’s currency may shift the food producers in exporting countries from the domestic markets to international markets [40], pressing the internal supply chain of the exporters. This imbalance between currencies in a globalized market promoted a massive flow of maize exports from Brazil in 2015 (Figure 6) pushing the maize prices in the internal market to an unprecedented level (Figure 7). The international price of maize affects the domestic price in Brazil [44]. Before 2015, Brazil reached higher rates of maize exports in 2012 when the prices at the CBOT (US Dollar, Chicago Board of Trade) were higher than within the Brazilian market (Brazilian Real, ESALQ/BM&Fbovespa). In 2015, the situation happened again but with better exchange rates for the Brazilian currency (Figure 7a), which favored the exports. During the period highlighted in Figure 7a, the exchange rate between the Brazilian Real and the US Dollar reached historic peaks of up to 4.05 Real per US Dollar.

Figure 7.

Historical prices of maize traded in the Brazilian internal market (Luiz de Queiroz College of Agriculture—ESALQ/BM&FBovespa) compared to the prices in the Chicago Board of Trade (CBOT). The daily exchange rate between the Brazilian currency and the US Dollar was used to present the value of one 60-kilo bag of maize (Cepea and CBOT, Supplementary Material S4).

Due to the high flows of maize exports in 2015 from Goiás, the State government issued the Decree no. 8548 in 2016 for the taxation of soybean and maize exports, previously free of export taxes under the Kandir Federal Law (Law no. 83 of 1996 that exempts the taxation over the exports of raw materials as food commodities). The State government proposed this measure to balance tax revenues and to benefit the processing food industry of Goiás. Processing industries suffered a shortage of maize and price volatility since the beginning of 2016 due to the higher rates of maize exports. However, the soybean and maize producer representatives of the State, and at the Federal level, positioned themselves against this proposal, and the State Government pulled back. Governments may impose export restrictions (e.g., export taxes) to finance their expenditures and to embolden the agribusiness, which improve the domestic economy adding more export value to the processed products [40].

The scenario of maize shortages and high volatility prices, not suffered exclusively in Goiás but also in other Brazilian states, boosted the production costs of animal protein in the internal market, reflected in the higher price of meat. Maize represents around 70% of the costs of poultry [44]. The authors have predicted negative impacts over the competitiveness of animal feed production as a side effect of the increases in Brazilian maize exports. Production costs of chicken increased 10% between August 2014 and June 2015 in Brazil (5.35% pushed by nutrition, and 4.65% by transportation, energy and other expenditures), while they increased 25.04% during the same months between 2015 and 2016 (25% pushed by nutrition, and 0.4% by other expenditures) [54]. The price of frozen chicken meat for retail increased from 3.43 R$/Kg (Brazilian currency) to 4.17 R$/Kg between August 2015 and August 2016. Previously, between 2014 and 2015, the price was more stable—from 3.19 R$/Kg to 3.43 R$/Kg [55].

The losses in the production of maize as a second crop in 2016 represent around 22% of the Brazilian production in 2015, an anomalous production year hampered by rainfall shortages [37]. In an important producing region of Goiás, the municipality of Rio Verde, farmers’ losses of maize reached 50 to 100% in some cases, as observed during fieldwork, conducted at the end of the harvest season of the maize second-crop. The decision of farmers to produce two crops per year established maize production in a less favorable period of rainfalls compared to the maize produced in the single crop season, an unexpected side effect of the increased soybean production. Until the next harvest season, beginning in June 2017, the expectation is for considerable flows of maize imports. The measure would control internal prices through free taxation for the maize imports, and foster the implementation of higher minimum prices (i.e., minimum price policy) to stimulate maize production and maize trade in the internal market. In May 2016, the federal government issued the freed maize imports from taxation, that used to be 12%, and the amount of maize imports for the same year in Brazil reached 2.9 million tons (4.5% of the national production in 2016 [56]), an increase of 684% compared to the imports in 2015,. In this context, Argentina emerged as a maize exporter country to Brazil given the huge increase of maize exports in 2016 compared to 2015, from 1.9 thousand tons in 2015 to 1.45 million tons in 2016 [56]. Thus, Argentina may be considered a spillover system under the telecoupling framework [9], and more studies are needed to investigate how this spillover relationship affects the sending and receiving countries under a variety of scenarios.

4.4. Perspective

In this paper, we consider only one receiving system (China), although the telecoupling framework accommodates two or more countries as receiving systems [57,58]. In the case of soybean trade, multiple countries such as many in Europe also import soybean from Brazil [59]. When two or more receiving systems are involved, there would be increased demand and competition among receiving systems [60,61], thus potentially enhancing the cascading effects in the sending system.

Cascading effects occur not only in a sending system such as Brazil, but also in receiving systems. For example, with more soybean from Brazil to China, many Chinese farmers have increased planted areas for corn and rice while reducing or even abandoning soybean production [62,63]. It is expected that, as meat demand continues to increase in China, there will be an increasing demand for soybean from Brazil [28]. Such demand may further increase soybean production areas in Brazil while reducing soybean production area in China [64]. Land use, ecosystem services and other environmental aspects will also change accordingly. So far, Brazil has not considered specific farm policies or environmental export taxes in response to environmental impacts of soybean trade between Brazil and China. If export taxes are increased, the soybean price will likely rise and thus reduce the competiveness of Brazil’s soybean.

5. Conclusions

The Sino-Brazilian telecoupled soybean system boosted the Brazilian expansion of soybean planted area threefold from 2000 to 2016 in comparison with the planted area increase over the previous 23 years. After the Brazilian engagement in the soybean international market with China, the rates of soybean planted area expansion and exports accelerated, as well as the decrease of maize as a single crop (planted area and production) and the increase of maize exports. This scenario consolidated maize as the second-crop, planted after soybean in a non-tillage system. The increased production of maize oversupplied the internal market consumption and positioned maize as a new commodity for the Brazilian exports beginning in 2012.

Cascading effects analyzed in this study include (i) maize exports increased, putting pressure over the country’s stocks and internal supply, which drove a historic maize shortage in 2015 after the highest peak of exports boosted by the increased devaluation of the Brazilian currency in the same year. Consequently, the prices of maize in the internal market reached its highest peak in 2016, inflating internal prices for meat consumption, observed in the case of the increased costs of chicken production and the price of frozen chicken for retail markets; (ii) in 2016, climatic anomalies during the second crop growing season in important producing regions (e.g., Goiás) struck maize production, for the first time in history, 16 years after the telecoupled soybean system began.

The telecoupling framework is a powerful tool to investigate socio-ecological systems across distances. Through this framework, numerous components of the telecoupled system can be assessed, as well as socioeconomic and environmental changes and their cascading effects in local systems. As observed on the historic Brazilian maize production system, synergies and flows among producing and receiving countries can lead to nonlinear cascading effects, which reshape the production system of the sending country, and force producers to adapt their practices.

Thus, local land-use and land-cover change (e.g., in Brazil) can be affected by food dietary shifts over long distances (e.g., Chinese meat consumption), trade policies (e.g., the Chinese joining the WTO, Brazilian tax exemption for export products) and by the international market of food commodities (e.g., soybean). The knowledge that emerges from long-distance analyses is essential to design policies for the long-term, since cascading effects may occur years after a telecoupled system was initiated (e.g., time-lag effects). Policies designed for food production and in response to the market must consider long-term relations among sending and receiving countries to better address (a) land-use change (e.g., displacement of maize single crop to produce soybean); and (b) internal market supply regulations to avoid food shortage driven by exports (e.g., Brazilian maize exports of 2015).

Supplementary Materials

The following are available online at www.mdpi.com/2073-445X/6/3/53/s1, Supplementary S1: Export destinations of soybean from Tocantins and Goiás states; Supplementary S2: Soybean and maize prodution in Brazil; Supplementary S3: Meat consumption in Brazilian and maize demand; Supplementary S4: Historical prices of maize in Brazil and in the Chicago Board of Trade.

Acknowledgments

We acknowledge the São Paulo Research Foundation (FAPESP), process numbers 2014/50628-9 and 2015/25892-7 for the funding support to develop this research. We also acknowledge the National Science Foundation, award numbers 1518518 and 1531086. However, none of these agencies should be responsible for the views the authors have expressed herein. They are the sole responsibility of the authors. We are also grateful to three anonymous reviewers for their constructive comments and suggestions, which have helped to improve this paper.

Author Contributions

Silva, Batistella and Dou conceived the manuscript and conducted fieldwork. Moran and Torres participated in the fieldwork, reviewed and improved the discussion section. Liu supported the use of the telecoupling framework and improved the paper´s discussion.

Conflicts of Interest

The authors declare no conflict of interest. The founding sponsors had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, and in the decision to publish the results.

References

- World Trade Organization. Trade and Development: Recent Trends and the Role of the WTO; WTO Secretariat: Geneva, Switzerland, 2014; Available online: https://www.wto.org/english/res_e/booksp_e/world_trade_report14_e.pdf (accessed on 6 March 2017).

- Meyfroidt, P.; Carlson, K.M.; Fagan, M.E.; Gutiérrez-Vélez, V.H.; Macedo, M.N.; Curran, L.M.; DeFries, R.S.; Dyer, G.A.; Gibbs, H.K.; Lambin, E.F.; et al. Multiple pathways of commodity crop expansion in tropical forest landscapes. Environ. Res. Lett. 2014, 9, 074012. [Google Scholar] [CrossRef]

- Kastner, T.; Rivas, M.J.I.; Koch, W.; Nonhebel, S. Global changes in diets and the consequences for land requirements for food. Proc. Natl. Acad. Sci. USA 2012, 109, 6868–6872. [Google Scholar] [CrossRef] [PubMed]

- FAO, Food and Agriculture Organization. The State of Agricultural Commodity Markets; United Nations: Rome, Italy, 2015; Available online: http://www.fao.org/3/a-i5090e.pdf (accessed on 6 March 2017).

- Wang, L.; Chen, L. Spatiotemporal dataset on Chinese population distribution and its driving factors from 1949 to 2013. Sci. Data 2016, 3, 160047. [Google Scholar] [CrossRef] [PubMed]

- Delgado, C. Rising consumption of meat and milk in developing countries has created a new food revolution. J. Nutr. 2003, 133, 3907–3920. [Google Scholar]

- Garret, R.D.; Rausch, L.L. Green for gold: Social and ecological tradeoffs influencing the sustainability of the Brazilian soy industry. J. Peasant Stud. 2016, 43, 461–493. [Google Scholar] [CrossRef]

- Lambin, E.F.; Meyfroidt, P. Global land use change, economic globalization and the looming land scarcity. Proc. Natl. Acad. Sci. USA 2011, 108, 3465–3472. [Google Scholar] [CrossRef] [PubMed]

- Liu, J.; Hull, V.; Batistella, M.; Defries, R.; Dietz, T.; Fu, F.; Hertel, T.W.; Izaurralde, R.C.; Lambin, E.F.; Li, S.; et al. Framing sustainability in a Telecoupled World. Ecol. Soc. 2013, 18, 26. [Google Scholar] [CrossRef]

- Searchinger, T.; Heimlich, R.; Houghton, R.A.; Dong, F.; Elobeid, A.; Fabiosa, J.; Tokgoz, S.; Hayez, D.; Yu, T. Use of U.S. croplands for biofuels increases greenhouse gases through emissions from land-use change. Science 2008, 319, 1238–1240. [Google Scholar] [CrossRef] [PubMed]

- Lapola, D.M.; Schaldach, R.; Alcamo, J.; Bondeau, A.; Koch, J.; Koelking, C.; Priess, J. Indirect land-use changes can overcome carbon savings from biofuels in Brazil. Proc. Natl. Acad. Sci. USA 2010, 107, 3388–3393. [Google Scholar] [CrossRef] [PubMed]

- Meyfroidt, P.; Lambin, E.F.; Erb, K.H.; Hertel, T.W. Globalization of land use: Distant drivers of land change and geographic displacement of land use. Curr. Opin. Environ. Sustain. 2013, 5, 438–444. [Google Scholar] [CrossRef]

- Harvey, M.; Pilgrim, S. The new competition for land: Food, energy, and climate change. Food Policy 2011, 36, 40–51. [Google Scholar] [CrossRef]

- USDA, Department of Agriculture. Market and Trade Data. Available online: https://www.fas.usda.gov/data/search?f[0]=field_report_type%3AWorld%20Production%2C%20Markets%2C%20and%20Trade%20Reports (accessed on 29 May 2017).

- Oliveira, G.L.T. The geopolitics of Brazilian soybeans. J. Peasant Stud. 2016, 43, 348–372. [Google Scholar] [CrossRef]

- Liu, J.; Hull, V.; Moran, E.; Nagendra, H.; Swaffield, S.R.; Turner, B.L. Applications of the Telecoupling Framework to Land-Change Science. In Rethinking Global Land Use in an Urban Era; Seto, K.C., Reenberg, A., Eds.; MIT Press: Cambridge, MA, USA, 2014; Volume 14, pp. 119–139. [Google Scholar]

- Petrini, M.A.; Rocha, J.V. Identification of grain areas replaced by sugarcane and analysis of the relationship with family farming production in the state of Goiás. Eng. Agríc. 2014, 34, 1296–1306. [Google Scholar] [CrossRef]

- MMA (Ministério do Meio Ambiente). Mapeamento do Uso e Cobertura do Cerrado: Projeto TerraClass Cerrado 2013; MMA: Brasília, Brazil, 2015. [Google Scholar]

- IBGE (Instituto Brasileiro de Geografia e Estatística). Censo Demográfico 2010; IBGE: Rio de Janeiro, Brazil, 2010.

- Atkinson, R.; Flint, J. Accessing hidden and hard-to-reach populations: Snowball research strategies. Soc. Res. Update 2001, 33, 1–4. [Google Scholar]

- AGROSTAT (Ministry of Agriculture, Livestock and Food Supply). Search Criteria: Exportações, Soja. Available online: http://indicadores.agricultura.gov.br/agrostat/index.htm (accessed on 9 July 2017).

- USDA. Foreign Agricultural Service. Available online: https://apps.fas.usda.gov/gats/default.aspx (accessed on 7 March 2017).

- China Statistical Yearbook 2015. Available online: http://www.stats.gov.cn/tjsj/ndsj/2015/indexeh.htm (accessed on 30 November 2016).

- China Labour Bulletin. Available online: http://www.clb.org.hk/schi/content/%E8%BF%9B%E5%8F%A3%E5%A4%A7%E8%B1%86%E5%86%B2%E5%87%BB3000%E4%B8%87%E8%B1%86%E5%86%9C-0 (accessed on 29 May 2017).

- Free Trade. Available online: http://www.feedtrade.com.cn/special/dadoulunxian/ (accessed on 29 May 2017).

- China’s Official Website. Available online: http://www.gov.cn/flfg/2005-08/06/content_21003.htm (accessed on 29 May 2017).

- National Bureau of Statistics of China. Available online: http://data.stats.gov.cn/easyquery.htm?cn=C01 (accessed on 12 July 2017).

- Hansen, J.; Gale, F. China in the Next Decade: Rising Meat Demand and Growing Imports of Feed. In USDA Amber Waves; 2014. Available online: https://www.ers.usda.gov/amber-waves/2014/april/china-in-the-next-decade-rising-meat-demand-and-growing-imports-of-feed/ (accessed on 9 July 2017).

- Barton, D.; Chen, Y.; Jin, A. Mapping China’s Middle class. McKinsey Q. 2013, 3, 54–60. Available online: http://www.mckinsey.com/industries/retail/our-insights/mapping-chinas-middle-class (accessed on 7 March 2017).

- World Health Organization. Available online: http://www.who.int/features/qa/cancer-red-meat/en/ (accessed on 12 July 2017).

- USDA; Foreign Agricultural Service. Search Criteria: Swine and Beef Meat. Available online: https://apps.fas.usda.gov/psdonline/psdquery.aspx (accessed on 30 November 2016).

- FAO. Corporate Document Repository. Available online: http://www.fao.org/docrep/005/y4252e/y4252e05b.htm (accessed on 30 November 2016).

- Nuboer, J.F.W.; Hagens, S.; Loessner, M.J.; Offerhaus, M.L. A Method of Feeding an Animal to Improve Growth Efficiency. PCT/EP2015/064248. 25 May 2017. Available online: http://www.freepatentsonline.com/y2017/0143778.html (accessed on 12 July 2017).

- Buainain, A.M.; Alves, E.; Silveira, J.M.; Navarro, Z. (Eds.) O Mundo Rural no Brasil do Século 21; Embrapa: Brasília, Brazil, 2014. [Google Scholar]

- Jepson, W. Producing a modern agricultural frontier: Firms and cooperatives in Eastern Mato Grosso, Brazil. Econ. Geogr. 2006, 82, 289–316. [Google Scholar] [CrossRef]

- Spera, S.A.; Galford, G.L.; Coe, M.T.; Macedo, M.N.; Mustard, J.F. Land-use change affects water recycling in Brazil’s last agricultural frontier. Glob. Chang. Biol. 2016, 22, 3405–3413. [Google Scholar] [CrossRef] [PubMed]

- Conab Companhia Nacional de Abastecimento. Search Criteria: Soja. Available online: http://www.conab.gov.br/conteudos.php?a=1252&t=&Pagina_objcmsconteudos=3#A_objcmsconteudos (accessed on 7 March 2017).

- FAOSTAT (Food and Agriculture Organization). Available online: http://www.fao.org/faostat/en/#data/QC (accessed on 7 March 2017).

- Agricultura, Pecuária e Abastecimento. Available online: http://www.agricultura.gov.br/assuntos/relacoes-internacionais/documentos/estatisticas-do-agronegocio/dezembro-2016-balanca-comercial-do-agronegocio-resumida.xls/view (accessed on 13 July 2017).

- Sanogo, I. Do export restrictions affect food security and humanitarian food assistance in Africa? Bridges Africa 2014, 3, Number 9. [Google Scholar]

- Norder, S.J.; Seijmonsbergen, A.C.; Loon, E.E.; Tatayah, V.; Kamminga, A.T.; Rijsdijk, K.F. Assessing temporal couplings in social–ecological island systems: Historical deforestation and soil loss on Mauritius (Indian Ocean). Ecol. Soc. 2017, 22, 29. [Google Scholar] [CrossRef]

- Liu, J.; Dietz, T.; Carpenter, S.R.; Alberti, M.; Folke, F.; Moran, E.; Pell, A.N.; Deadman, P.; Kratz, T.; Lubchenco, J.; et al. Complexity of coupled human and natural systems. Science 2007, 317, 1513–1516. [Google Scholar] [CrossRef] [PubMed]

- Caldarelli, C.E.; Bacchi, M.R.P. Fatores de Influência no Preço do Milho no Brasil. Nova Econ. 2012, 22, 141–164. [Google Scholar] [CrossRef]

- Favro, J.; Caldarelli, C.E.; Camara, M.R.G. Modelo de Análise da Oferta de Exportação de Milho Brasileira. RESR 2015, 53, 455–476. [Google Scholar]

- Meade, B.; Puricelli, E.; McBride, W.; Valdes, C.; Hoffman, L.; Foreman, L.; Dohlman, E. Corn and Soybean Production Costs and Export Competitiveness in Argentina, Brazil and the United States; Economic Research Service/USDA: Washington, MD, USA, 2016.

- Ageitec, Agência Embrapa de Informação Tecnológica. Ávore do Conhecimento: Milho. Available online: http://www.agencia.cnptia.embrapa.br/gestor/milho/arvore/CONT000fya0krse02wx5ok0pvo4k3mp7ztkf.html (accessed on 7 March 2017).

- Mattoso, M.J.; Garcia, J.C.; Duarte, J.O.; Cruz, J.C. Aspectos de produção e mercado do milho. Inf. Agropecu. Belo Horiz. 2006, 27, 95–104. [Google Scholar]

- IBGE, Sistema IBGE de Recuperação Automática. Search Criteria: Pesquisa Agrícola Municipal. Available online: https://sidra.ibge.gov.br/pesquisa/pam/tabelas (accessed on 7 March 2017).

- Conab Companhia Nacional de Abastecimento. Search Criteria: Milho. Available online: http://www.conab.gov.br/conteudos.php?a=1252&t=&Pagina_objcmsconteudos=3#A_objcmsconteudos (accessed on 9 July 2017).

- Brunini, O.; Zullo, J.; Pinto, H.S.; Assad, E.; Sawazaki, E.; Duarte, A.P.; Patterniani, M.E.Z. Riscos climáticos ara a cultura de milho no estado de São Paulo, Brasil. Rev. Bras. Agrometeorol. 2001, 9, 519–526. [Google Scholar]

- Gonçalves, S.L.; Caramori, P.H.; Wrege, M.S.; Shioga, P.; Gerage, A.C. Épocas de semeadura do milho “safrinha”, no Estado do Paraná, com menores riscos climáticos. Acta Sci. Agron. 2002, 24, 1287–1290. [Google Scholar] [CrossRef]

- MAPA, Ministry of Agriculture, Livestock and Food Supply. Projections of Agribusiness: Brazil 2013/14 to 2023/24 Long Term Projections; MAPA: Brasília, Brazil, 2014.

- FAO, Food and Agriculture Organization. OECD-FAO Agricultural Outlook 2016–2025; OECD: Paris, France, 2016. [Google Scholar]

- Embrapa, Swine & Poultry. Available online: https://www.embrapa.br/suinos-e-aves/cias/custos/icpfrango (accessed on 7 March 2017).

- Cepea, ESALQ/USP. Available online: http://www.cepea.esalq.usp.br/br/indicador/frango.aspx (accessed on 7 March 2017).

- AGROSTAT (Ministry of Agriculture, Livestock and Food Supply). Search Criteria: Importações, Milho. Available online: http://indicadores.agricultura.gov.br/agrostat/index.htm (accessed on 7 March 2017).

- Liu, J.; Yang, W.; Li, S. Framing ecosystem services in the telecoupled Anthropocene. Front. Ecol. Environ. 2016, 14, 27–36. [Google Scholar] [CrossRef]

- Liu, J.; Hull, V.; Luo, J.; Yang, W.; Liu, W.; Vina, A.; Vogt, C.; Xu, Z.; Yang, H.; Zhang, J.; et al. Multiple telecouplings and their complex interrelationships. Ecol. Soc. 2015, 20, 44. [Google Scholar] [CrossRef]

- Schaffer-Smith, D.; Maguire, D.Y.; Tomscha, S.A.; Treglia, M.L.; Jarvis, K.J.; Liu, J. Network analysis as a tool for quantifying the spatial, temporal, and cross-scale dynamics of telecoupled systems: An example using global soybean trade. Ecol. Soc. 2017, in press. [Google Scholar]

- Liu, J.; Mooney, H.; Hull, V.; Davis, S.J.; Gaskell, J.; Hertel, T.; Lubchenco, J.; Seto, K.C.; Gleick, P.; Kremen, C.; Li, S. Systems integration for global sustainability. Science 2015, 347, 1258832. [Google Scholar] [CrossRef] [PubMed]

- Liu, J.; Hull, V.; Yang, W.; Viña, A.; Chen, X.; Ouyang, Z.; Zhang, H. (Eds.) Pandas and People: Coupling Human and Natural Systems for Sustainability; Oxford University Press: Oxford, UK, 2016. [Google Scholar]

- Sun, J.; Wu, W.; Tang, H.; Liu, J. Spatiotemporal Patterns of Non-Genetically Modified Crops in the Era of Expansion of Genetically Modified Food. Sci. Rep. 2015, 5, 14180. Available online: http://www.nature.com/articles/srep14180 (accessed on 9 July 2017). [CrossRef] [PubMed]

- Sun, J.; Tong, Y.; Liu, J. Telecoupled land-use changes in distant countries. J. Integr. Agric. 2017, 16, 368–376. [Google Scholar] [CrossRef]

- USDA, Foreign Agricultural Service. World Agricultural Production; Circular Series WAP 07-17; 2017. Available online: https://apps.fas.usda.gov/psdonline/circulars/production.pdf (accessed on 9 July 2017).

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).